ORDER

Ravish Sood, Judicial Member. – The captioned appeals filed by the assessee company are directed against the respective orders passed by the Learned Commissioner of Income Tax (Appeals)-11, Hyderabad, dated 31/05/2025, which in turn arises from the respective orders passed by the Income Tax Officer (TDS), CPC, Ghaziabad under section(s) 200A/206CB r.w.s 154 r.w.s 200A of the Income-tax Act, 1961 (for short, “Act”) for the respective quarters pertaining to AY 2021-22 and AY 2022-23. As common issues are involved in the present appeals, the same are being taken up and disposed of by way of a consolidated order. We shall first take up the appeal filed by the assessee for AY 2021-22 in ITA No.1236/Hyd/2025, and the order therein passed shall apply mutatis mutandis with respect to the common issues for the other appeal. The assessee company has assailed the impugned order on the following grounds of appeal before us:

| 1. |

|

The Order of the Ld. CIT(A) u/s 250 dated 31.05.2025 is erroneous both on facts and in law to the extent the order is prejudicial to the interests of the appellant |

| 2. |

|

The Lid. CTT(A) ought to have appreciated that the Ld. TDS CPC erred in passing the orders u/s 2004, 206CB and u/s 154 of the Act by charging late fee u/s 234E, calculating the short deduction u/s 201(1) and Interest u/s 311(1A) & 220(2) of the Act without appreciating the facts of the case. |

| 3. |

|

The Lud. CIT(A) erred in stating that the submissions made by the appellant are not satisfactory and justifiable. |

| 4. |

|

The Lid. CIT(A) ought to have appreciated that the interest levied is not warranted since the assessee has not been treated as an assessee in default u/s 201 of the Act for any amount of non-deduction for the year. |

| 5. |

|

The Ld. CIT(A) ought to have appreciated that due to covid-19. the Hon’ble Supreme Court in MA 665 of 2021 had extended the period of limitation for the furnishing of TDS statements (quarterly) and hence the interests u/s 201(1), 201(1A) & fine u/s 234E are not chargeable. |

| 6. |

|

The Ld. CTT(A) ought to have considered that when no interests u/s 201(1), 201(1A) & fine u/s 234E are eligible for charging, the question of charging interest u/s 220(2) is not applicable. |

| 7. |

|

The Ld. CTT(A) ought to have appreciated the fact that assessee has neither will fully nor intentionally delayed in filing of TDS statements but it was beyond its control and thus the levy of penal interest is not justified. |

| 8. |

|

The appellant may add or alter or amend or modify or substitute or delete and/or rescind all or any of the grounds of appeal at any time before or at the time of hearing of the appeal.” |

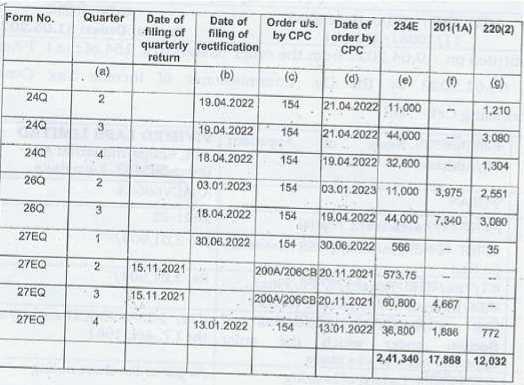

2. Succinctly stated, the assessee company had filed its quarterly TDS/TCS statements for the Financial Year 2020-21 on various dates. The ITO (TDS), CPC, Ghaziabad, considering the TDS/TCS statements passed orders under section(s) 200A/206CB r.w.s 154 r.w.s 200A for the respective quarters, wherein demands under section 201(1A), 234E and 220(2) were raised, as under:

3. Apart from that, the ITO (TDS), CPC had also raised demands of Rs.13,660/- for short payment and short deduction/collection of tax at source vide his order under section 154 of the Act, dated 19/04/2022 with respect to Form-26Q for the 3rd Quarter (Q3).

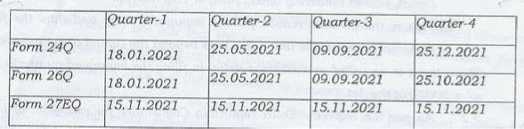

4. Aggrieved, the assessee company carried the matter in appeal before the CIT(A). Ostensibly, the assessee company submitted before the CIT(A) that it had filed its TDS returns for the FY 2020-21, as under:

5. Elaborating further on its contention, it was submitted by the assessee company that the ITO (TDS), CPC had levied interest under section 201(1A), fee under section 234E and interest under section 220(2) of the Act for the reason that there was a delay in delivering/filing the statements within the time prescribed under section 200(3) of the Act. The assessee company has assailed the charging of the interest/fee primarily for two-fold reasons, viz., (i) that as its accountant who was attending to the work relating to TDS provisions was during the relevant period taken unwell, therefore, the assessee company was prevented by sufficient cause in filing the statements in accordance with the provisions of section 200(3) of the Act; and (ii) that due to lockdown protocols the business of the assessee company was affected due to COVID-19 during the year under consideration. Accordingly, it was the claim of the assessee company that as the delay in filing of the TDS statements was neither willful nor intentional, but for the reasons beyond its control, therefore, the levy of fees and interest under the aforementioned provisions of the Act was not justified.

6. Ostensibly, the CIT(A) did not find favour with the explanation of the assessee company regarding the delay in filing the TDS statements.

7. Apropos the claim of the assessee company that the demands as contested were not tallying with the orders passed under section 154 r.w.s 200A by the CPC, Ghaziabad for the various quarters, the CIT(A) issued a notice, dated 08/05/2025, wherein the assessee company was called upon to file a breakup of the disputed demand which was duly placed on record. The CIT(A) referring to the breakup/details filed by the assessee company observed that the same was comprised of, viz., (i) demand towards fee under section 234E: Rs.2,41,340/-; (ii) interest under section 201(1A): Rs.48,529/-; and (iii) interest under section 220(2): Rs.12,032/-. The CIT(A) observed that the amount of interest under section 201(1A) of Rs.48,529/- was comprised of, viz., (i) short payment of tax: Rs.17,004/-; (ii) short deduction/collection of tax: 13,660/-; and (iii) interest under section 201(1A): Rs.17,868/-. The CIT(A) observed that other than the aforementioned discrepancy, the total disputed breakup given by the assessee tallied with the orders passed under section 200A/206CB and orders passed under section 154 of the Act, respectively. Accordingly, the CIT(A) thereafter proceeded to adjudicate the sustainability of the demands that were raised by the AO (TDS), CPC.

8. The CIT(A) observed that it was the claim of the assessee company that it was during the Financial Year 2020-21 prevented by a sufficient cause in filing the statements in accordance with the provisions of section 200(3) of the Act since its accountant, who was attending the work related to the TDS provisions, was taken unwell and could not attend the office due to prevailing lockdown situation in the country and thus, could not compile the data and deposit the amounts in the Government Treasury within the time prescribed. Accordingly, the assessee company had assailed the levy of fees for the late filing of TDS statements because the said delay had crept in for reasons beyond its control and not for any willful or deliberate act on its part. However, we find that the CIT(A) did not find favour with the aforesaid explanation of the assessee company. It was observed by him that the Government of India, keeping in view the challenges faced by taxpayers in meeting the statutory and regulatory challenges due to the outbreak of COVID-19, brought the Taxation and Other Laws (Relaxation of Certain Provisions) Ordinance, 2020 (‘the Ordinance’) on 31st March, 2020, which, inter alia, extended various time limits. Accordingly, the CBDT issued a Notification, dated 24/06/2020, extending various time limits. Thereafter, the aforesaid Ordinance was replaced by the Taxation and Other Laws (Relaxation and Amendment of Certain Provisions) Act, 2020 (No.38 of 2020), dated 29/11/2020, wherein the due date for filing of TDS returns was extended but only for the quarter ended 31st March, 2020, and not for any further periods. Also, it was observed by him that the assessee company had not submitted any CBDT notification which had extended the due dates for filing of TDS returns for any quarter for the year under consideration, i.e., AY 2020-21. The CIT(A) further observed that the Hon’ble Supreme Court, vide its order in MA 665 of 2021, had referred to only the filing of the petitions/applications /suits appeals/all other quasi-proceedings relating to the judicial or quasi-judicial proceedings, but not for any other matters. Accordingly, the CIT(A) based on his aforesaid deliberations observed that as the assessee company had failed to file the TDS statements within the time prescribed in sub-section (3) of section 200 or the proviso to section 206C(3) of the Act, therefore, as per the clear mandate of section 234E of the Act, it was liable to pay by way of fee, a sum of Rs.200/- for every day during which the failure continued. The CIT(A) based on his aforesaid observations, found no infirmity in the levy of fee under section 234E of the Act by the ITO (TDS), CPC, and upheld the same.

9. Apropos the challenge by the assessee company to the demand that was raised by the ITO (TDS), CPC, viz., (i) short payment of tax: Rs.17,005/-; and (ii) short deduction of tax: Rs.1,22,275/- (Rs.13,600/- as per order under section 154, dated 19/04/2022), the CIT(A) observed that as the assessee company had not submitted any details for substantiating its claim that there was no short deduction or short payment/collection of tax, therefore, the said claim being devoid and bereft of any substance was liable to be rejected.

10. Apropos the challenge of the assessee company to the levy of interest under section 201(1A) of the Act of Rs.17,868/-, the CIT(A) observed that it was the claim of the assessee company that as there was no default on its part in depositing the amount of tax deducted at source (TDS) for being treated as an assessee in default under section 201 of the Act, therefore, no interest under the aforesaid statutory provision was liable to be imposed in its case. The CIT(A) did not find favour with the aforesaid explanation of the assessee company. The CIT(A) observed that it was not the case of the assessee company that it had deducted the tax at source (TDS) and remitted the same in the Government Treasury as per the extant provisions.

11. Apropos the claim of the assessee company that it was not to be held as an assessee-in-default under section 201(1) of the Act, the CIT(A) observed that as per the “first proviso” to sub-section (1A) of section 201 in a case where the deductor fails to deduct the whole or any part of the tax in accordance with the provisions of Chapter XVII on the sum paid to the payee (deductee) or on the sum credited to the account of a payee, but is not to be deemed to be an assessee-in-default under sub-section (1) of section 201 then the interest under clause (i) of section 201(1A) shall be payable from the date on which such tax was deductible to the date of furnishing of return of income by such payee (deductee). However, the CIT(A) observed that a deductor for not to be considered as an assessee-in-default have to cumulatively fulfil three conditions as provided in the proviso, viz., (i) payee should have furnished return of income under section 139 of the Act; (ii) payee should take into account such sum (amount on which tax was supposed to be deducted) for computing income disclosed in such return of income; and (iii) payee should have paid the tax due on the income declared in such return of income. The CIT(A) observed that as the assessee company had failed to place on record the requisite details to support its claim that it be not considered as an assessee-in-default within the meaning of “first proviso” to sub-section (1A) of section 201 of the Act, therefore, its contention that no interest under section 201(1A) was liable to be imposed did not merit acceptance.

12. Apropos, the assessee’s claim that the AO had erred in charging interest under section 220(2) on the deemed belated remittance of tax deducted at source (TDS), the CIT(A) observed that as the assessee company had neither proved that the demand raised by the CPC due to late filing or late remittance/short deduction/short payment of TDS was contrary to the provisions of Chapter-XVII of the Act; nor it had proved that it had duly filed its TDS statements and remitted the tax deducted at source within the prescribed time limits, therefore, there was no infirmity in levy of interest under section 220(2) of Act by the CPC.

13. Accordingly, the CIT(A), based on his aforesaid observations, dismissed the appeal.

14. Aggrieved, the assessee company has carried the matter in appeal before us.

15. We have heard the Learned Authorized Representatives of both parties, perused the orders of the authorities below and the material available on record.

16. Controversy involved in the present appeal primarily hinges around the aspect, as to whether or not the assessee company had delayed in filing the TDS returns, rendering it exigible to saddling of fees under section 234E of the Act.

17. We have given thoughtful consideration to the order of the Hon’ble Supreme Court in the case in Cognizance for Extension of Limitation, In re (SC)/MA 21 of 2022, dated 10/01/2022 r.w. MA No.29 of 2022 r.w. MA No.665 of 2021, wherein it had after taking cognizance of the devastating and debilitating effect of the outbreak of COVID-19 Pandemic in March 2020, which had caused difficulties to the litigants in filing petitions/ applications/ suits/ appeals/ all other proceedings within the period of limitation prescribed under the general law of limitation or under any special laws (both Central and/or State) had observed, viz. (i). that the period from 15/03/2020 till 28/02/2022 for computing the period of limitation in filing petitions/ applications/ suits/ appeals/ all other proceedings shall stand excluded for the purposes of limitation as may be prescribed under any general or special laws in respect of all judicial or quasi-judicial proceedings; (ii) the balance period of limitation remaining as on 03/10/2021, if any, shall become available with effect from 01/03/2022; (iii) that in cases where the limitation would have expired during the period between 15.03.2020 till 28/02/2022, notwithstanding the actual balance period of limitation remaining, all persons shall have a limitation period of 90 days from 01/03/2022, and in case the actual balance period of limitation remaining w.e.f 01/03/2022 is greater than 90 days, that longer period shall apply; (iii) that the period from 15.03.2020 till 28/02/2022 shall be excluded in computing the period prescribed under section(s) 23(4) and 29A of the Arbitration and Conciliation Act, 1996, Section 12A of the Commercial Courts Act, 2015 and provisos (b) and (c) of Section 138 of the Negotiable Instruments Act, 1881 and any other laws, which prescribe period(s) of limitation for instituting proceedings, outer limits (within which the court or tribunal can condone delay) and termination of proceedings. In our view, the prescribed time limit for filing TDS returns as contemplated in the Income Tax Act, 1961 does not fall within the scope and gamut of the aforesaid order passed by the Hon’ble Supreme Court in MA 21 of 2022, dated 10/01/2022. We say so, for the reason that the Hon’ble Apex Court in its order had specifically observed that the period from 15/03/2020 till 28/02/2022 shall be excluded for computing the period of limitation for, viz., (i) any judicial or quasi-judicial proceedings; and (ii) period prescribed under Sections 23 (4) and 29A of the Arbitration and Conciliation Act, 1996, Section 12A of the Commercial Courts Act, 2015 and provisos (b) and (c) of Section 138 of the Negotiable Instruments Act, 1881 and any other laws, which prescribe period(s) of limitation for instituting proceedings, outer limits (within which the court or tribunal can condone delay) and termination of proceedings. We concur with the observations of the CIT(A) that the Hon’ble Supreme Court in MA 21 of 2022 (supra) as was relied upon by the assessee company speaks only of filing of petitions/applications/suits/appeals/all other quasi proceedings relating to the judicial or quasi-judicial proceedings, but not for any other matters. Accordingly, we are of a firm conviction that the reliance placed by the Ld. AR on the order passed by the Hon’ble Supreme Court in MA 21 of 2022, dated 10/01/2022 is misplaced and will not come to its rescue qua the delay in filing of the quarterly TDS returns for the subject year.

18. Apart from that, we find that the Government of India, keeping in view the challenges faced by the taxpayers in meeting the statutory and regulatory compliances due to the outbreak of COVID-19, had brought the Taxation and Other Laws (Relaxation of Certain Provisions) Ordinance, 2020 (“the Ordinance”) on 31/03/2020, which, inter alia, extended various time limits. Accordingly, the CBDT had issued a notification, dated 24/06/2020, extending various time limits. Thereafter, the said Ordinance was replaced by the Taxation and Other Laws (Relaxation and Amendment of Certain Provisions) Act, 2020 (No.38 of 2020), dated 29/09/2020, wherein the due dates for filing of TDS return were extended specifically for the quarter ended 31/03/2020, only, and not for any further periods. However, we find that the CBDT vide its Circular No.12/2021, dated 25/06/2021, had, inter alia, observed that the statement of Deduction of Tax for the last quarter of the Financial Year 2020-21 may be furnished on or before 15th July, 2021. Considering the aforesaid CBDT Circular No.12/2021, we herein direct the AO (TDS) not to treat the assessee company as being in default for the delay in the filing of the TDS statement for the last quarter for the subject year up to 15/07/2021. Apart from that, as observed by the CIT(A), we find that the assessee company had not submitted any CBDT notification as per which the “due dates” for filing of TDS returns for any other quarter for the impugned assessment year had been extended.

19. Apropos the reliance placed by the Ld. AR on the judgment of the Hon’ble High Court of Orissa in the case of D.N. Homes (P.) Ltd v. UOI ITR 211 (Orissa), we are of the view that as the same is distinguishable on facts, thus, the same will not carry the case of the assessee company any further. In the said case the Hon’ble High Court was seized of the issue as to whether or not the assessee company was liable for being visited with prosecution qua the offences contemplated under section(s) 279B, 2(35) and section 278B of the Act for the failure on its part to deposit the tax deducted at source (TDS) within the statutory time limit. It was observed that though the assessee company had deducted tax at source (TDS), but delayed deposit of the same by 31 to 214 days on account of reasonable cause of prevalence of COVID-19 Pandemic standing, on their way, therefore, the order of sanction for prosecution that was passed without due application of mind and in a mechanical manner could not be sustained. At this stage, we may herein observe that the “proviso” to section 278B of the Act carves out an exception to the deeming of an assessee as guilty of the offence in case he proves that the same was committed without his knowledge or that he had exercised due diligence to prevent the commission of such offence. However, we find that as there is no such exception from being saddled with fees under section 234E of the Act for the delay involved in filing of the quarterly TDS statements, therefore, no support can be drawn from the aforesaid judicial pronouncement that has been pressed into service by the Ld. AR.

20. Apropos the order of the ITAT “C” Bench, Kolkata in the case of Madhu Bhardwaj v. ITO [IT Appeal No.30/Kol/2023, dated 27-6-2023], we find that as the same is distinguishable based on the facts therein involved, thus, the same would not advance the case of the assessee company before us.

21. Apropos the interest under section 201(1A) of the Act levied upon the assessee company, we are of the view that as the assessee company had failed to pay the said amount in the Government Treasury, and has also not established that it cumulatively satisfied the set of conditions for not being treated as an assessee in default, therefore, no infirmity emerges from the interest so levied by the AO (TDS), CPC.

22. Apropos, the interest under section 220(2) of the Act, we are of the view that as the same flows from the failure on the part of the assessee company to deposit the amount specified in the notice of demand under section 156 of the Act within 30 days of the service of the said notice, the same is mandatorily required to be charged. Only remedy against charging of the said interest lies with the assessee by filing an application before the prescribed authority under section 220(2A) of the Act. Accordingly, we are of the view that no infirmity emerges from the order of the authorities below, who had rightly subjected the assessee company to interest under section 220(2) of the Act.

23. Coming to the Ld. AR’s claim that the demands raised in its case did not tally with the orders under section 154 and orders under section 200A passed by the ITO (TDS, CPC) for various quarters, we find that the said aspect had been looked into by the CIT(A) at Para No.6.3.1 of his order. The CIT(A) had filed a breakup of the disputed demand, which was comprised of, viz., (i) late fee under section 234E: Rs.2,41,340/-; (ii) interest under section 201(1A): Rs.48,529/-; and (iii) interest under section 220(2): Rs.12,032/-. Also, it was observed by him that the interest under section 201(1A) actually included, viz., (i) short payment of tax: Rs. 17,004/-; (ii) short deduction/collection of tax: Rs. 13,660/-; and (iii) interest under section 201(1A): Rs. 17,868/-. The CIT(A) had observed that, except for the aforesaid discrepancy, the remaining amounts provided in the breakup by the assessee company tallied with the orders passed under section 200A/206CB and the orders passed under section 154 of the Act, respectively. As the Ld. AR has failed to point out any perversity in the aforesaid observations of the CIT(A), therefore, we find no reason to dislodge the same.

24. Resultantly, the appeal filed by the assessee company is partly allowed for statistical purposes in terms of our aforesaid observations.

ITA No. 1237/Hyd/2025

(AY: 2022-23)

25. As the facts and the issue involved in the present appeal remain the same as were there before us in the case of the assessee company for the immediately preceding year, i.e., AY 2021-22 in ITA No.1236/Hyd/2025, except for the fact that in one of the quarters, i.e., 4th Quarter (Q4), the date for filing of the TDS statement/return had been extended by the CBDT vide its Circular No.12/2021, dated 25/06/2021, which is not relevant to the present case before us, therefore, the order therein passed shall apply mutatis mutandis for the purpose of disposing of the present appeal. Accordingly, the appeal filed by the assessee company, being devoid and bereft of any substance, is dismissed.

26. Resultantly, the appeal of the assessee in ITA No.1236/Hyd/2025 for AY 2021-22 is partly allowed for statistical purposes, while the appeal for the AY 2022-23 in ITA No. 1237/Hyd/2025 is dismissed.