ORDER

Madhusudan Sawdia, Accountant Member. – This appeal is filed by Smt. Neha Jain (“the assessee”), feeling aggrieved by the order passed by the Learned Commissioner of Income Tax (Appeals), National Faceless Appeal Centre (NFAC), Delhi (“Ld. CIT(A)”) dated 27.06.2025 for the A.Y 2016-17.

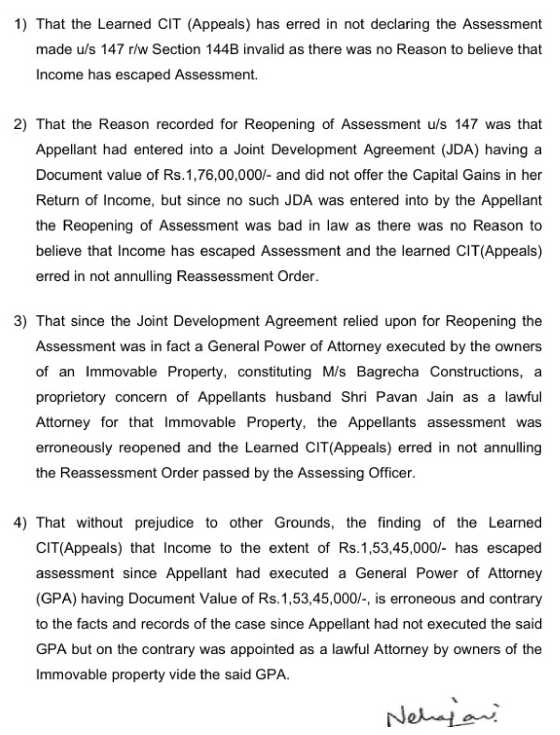

2. The assessee has raised the following grounds of appeal:

3. The brief facts of the case are that the assessee is an individual who filed her return of income for the Assessment Year 2016-17 declaring total income of Rs.3,05,700/-. The case of the assessee was reopened under section 147 of the Income Tax Act, 1961 (“the Act”), as the Learned Assessing Officer (“Ld. AO”) observed that the assessee had not declared capital gain arising from an alleged Joint Development Agreement (“JDA”). After considering the submissions of the assessee, the Ld. AO made an addition of Rs.1,76,00,000/- under section 69A of the Act and passed reassessment order dated 21.03.2022 under section 147 read with section 144B of the Act.

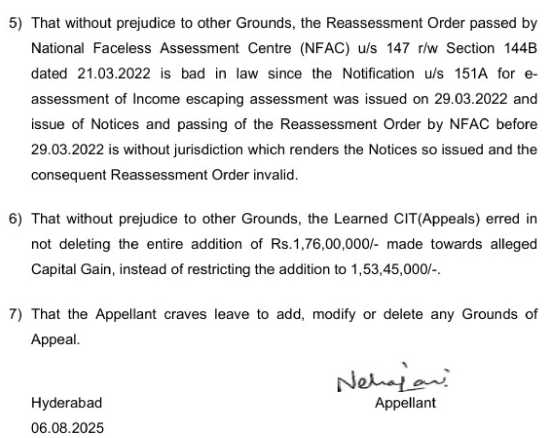

4. Aggrieved with the order of the Ld. AO, the assessee filed appeal before the Ld. CIT(A). The Ld. CIT (A) found that Document No. 680/2016 (value Rs.1,76,00,000/-) on the basis of which the addition has been made by the Ld. AO pertained to the assessee’s husband, while Document No. 685/2016 pertained to the assessee and reflected document value of Rs.1,53,45,000/-. Accordingly, the addition was reduced to Rs.1,53,45,000/- by the Ld. CIT (A).

5. Aggrieved with the order of the Ld. CIT (A), the assessee is now in appeal before this Tribunal. The Learned Authorized Representative (“Ld. AR”) submitted that the sole issue in dispute is the addition of Rs.1,53,45,000/- sustained by the Ld. CIT(A) on the allegation of a JDA. The Ld. AR further submitted that the assessee has never entered into any JDA. Further, the Ld. AR invited our attention to the reasons recorded by the Ld. AO placed at page no. 11 of the paper book and submitted that the Ld. AO wrongly assumed that the assessee had executed a development agreement valued at Rs.1,76,00,000/-. Before the Ld. AO, the assessee categorically denied having entered into any JDA. However, the Ld. AO relied solely on the document which is only a General Power of Attorney (“GPA”) documents No. 680/2016 and 685/2016, dated 25.02.2016 and made the said addition. The Ld. CIT(A) explained that Document No. 680/2016 on the basis of which the addition was made by the Ld. AO relates to the assessee’s husband. However, the Ld. CIT (A) contending that Document No. 685/2016 belongs to the assessee, reduced the addition to Rs. 1,53,45,000/-. The Ld. AR further submitted that the document No.680/2016 finally relied on by the Ld. CIT (A) for sustaining the addition of Rs.1,53,45,000/- is only a GPA, executed by four joint owners of a house property in favour of the assessee, authorizing her to act on their behalf. In this regard, the Ld. AR invited our attention to page nos. 26 to 34 of the paper book and demonstrated that the document is not an agreement to sell, it is not a JDA, it does not transfer any ownership or development rights and the assessee is not the owner of the property. Accordingly, he argued that the capital gain cannot arise in the hands of the assessee when the assessee does not own the property, and the alleged document is merely a GPA and not a JDA. Hence, the Ld. AR prayed before the Bench to delete the addition made by the Ld. Ld. AO.

6. Per contra, the Learned Departmental Representative (“Ld. DR”) relied on the orders of the lower authorities.

7. We have considered the rival submissions and perused the material available on record. We find that the addition sustained by the Ld. CIT(A) is premised entirely on Document No. 685/2016, presumed to be a JDA. In this regard, we have gone through Document No. 685/2016, placed at page nos. 26 to 34 of the paper book. On perusal of the same, we find that it is merely a GPA, executed by four joint owners of a house property in favour of the assessee. We also observe that the document does not evidence transfer of any capital asset within the meaning of section 45 of the Act resulting in any capital gain in the hands of the assessee. It is also undisputed that the assessee is not the owner of the land. In the absence of ownership of a capital asset, no capital gains can arise in the hands of the assessee. A GPA issued in favour of the assessee does not constitute transfer, nor can it be treated as a JDA. Thus, the very foundation of the addition fails. We accordingly direct the Ld. AO to delete the addition of Rs.1,53,45,000/- sustained by the Ld. CIT(A).

8. The assessee had also raised a legal ground challenging the validity of the reassessment proceedings. However, since we have allowed the appeal of the assessee on merits, we are not adjudicating the said legal issue, and the same is kept open.

9. In the result, the appeal of the assessee is allowed.