ORDER

CM APPL. 57376/2025

V. Kameswar Rao, J.- Exemption allowed, subject to all just exceptions.

2. The application is disposed of.

W.P.(C) 14027/2025 CM APPL. 57375/2025 (Stay)

3. The present petition has been filed by the petitioner seeking the following prayers:

“1. To set aside the notice dated 24.03.2025 and 28.05.2025 issued u/s 148A(1), the order passed u/s 148A(3) and notice dated 23.06.2025 issued u/s 148 of the income tax act for the assessment year 2019-20 by the respondent.

2. To stay the operations of the impugned notice dated 23.06.2025 issued u/s 148 of the Income Tax Act.

3. Pass such other order or orders as this Hon’ble court may deem fit and proper in the circumstances of the case.”

4. The present petition has been filed seeking quashing of the impugned notices dated 24.03.2025 and 28.05.2025 issued under Section 148A(1) of the Income Tax Act, 1961 (‘the Act’, hereinafter); order dated 23.06.2025 under Section 148A(3) of the Act pertaining to the Assessment Year 201920 and notice dated 23.06.2025 under Section 148 of the Act.

5. Mr. Mukesh Gupta, learned counsel for the petitioner has argued that the petitioner had filed its return of income on 17.10.2019 wherein the petitioner declared the income of Rs. 3,06,93,740/- and the same was revised on 21.12.2019 and 20.01.2020. He contends that the respondent issued a notice under Section 148A(1) of the Act wherein the respondent returned certain findings regarding the petitioner company being involved in a bogus transaction amounting to Rs. 82,25,822/- with IFFCO TOKYO General Insurance Company Ltd (‘IFTGI’, hereinafter). He stated that the petitioner company thereafter filed response on 15.04.2025 to the notice under Section 148A(1) and was further directed to again furnish a reply on 29.05.2025 in response due to change of the incumbent under Section 129 of the Act. It is his contention that the respondent passed the impugned order dated 23.06.2025 under Section 148A(3) of the Act on the ground that no details of the commission in terms of the percentage of premium receipts was given.

6. According to Mr. Gupta, this amount of Rs.82,25,822/- had already been declared by the petitioner company in its accounts and had already paid tax on the said amount. He stated that this amount was received from IFTGI as commission on the premium paid to IFTGI through the policies of the petitioner’s clients. The same has been referred to in the letter dated 15.04.2025. Mr. Gupta, has alluded to the copies of the tax invoices, details of policies and the amount of premium received by IFTGI on such policies and the commission that accrued to the petitioner from these policies.

7. As per Mr. Gupta, the respondent had changed its opinion after considering the reply of the petitioner company dated 15.04.2025 and passed an order under Section 148A(3) of the Act on the ground that the petitioner company had not submitted the percentage of the commission on the premium. It is his submission that the respondent had neither directed the petitioner company to furnish these details during the proceedings under Section 148A(1) of the Act nor the respondent was in possession of relevant material based on which such a conclusion could be drawn. He stated that the re-opening of the assessment is bereft of evidence and further there was no material evidence to show that an income of more than Rs. 50,00,000/-has escaped the assessment. Mr. Gupta has relied on a judgment of this Court in the case of Jindal Saw Ltd. v. Dy./Asstt. CIT 634 (Delhi), in support of his submission to contest the impugned notice.

8. Having heard the learned counsel for the petitioner and perused the record, we must at the outset refer to the notice dated 24.03.2025 issued under Section 148A(1) of the Act on the ground that the income subject to tax has escaped assessment within the meaning of Section 147 of the Act as per “information in accordance with the risk management strategy formulated in this regard”. Further, as per the impugned notice the respondent has mentioned that a search and seizure under Section 132 of the Act on Middle Layer Business Entities (‘MLBE’, henceforth) of the insurance sector was conducted on 30.11.2022 to verify the claim of services against which these entities had received payments from the insurance companies. According to the notice, these MLBEs were neither authorized to receive commission nor registered under Insurance Regulatory and Development Authority of India (‘IRDAI’, hereinafter) and have acted as pass-through entities for the insurance companies. These payments were masked under various heads such as online media expenses, advertisement services, online marketing, marketing activities, brand promotion expense, etc., and that these were finally paid to the insurance agents or insurance intermediaries or their nominees. Such search and seizure has covered 37 MLBEs and 32 insurance companies were part of post search verification.

9. According to the impugned notice, the respondents have stated that the insurance companies have signed several service agreements with several MLBEs to facilitate transfer of such payments. The notice states that the analysis of this financial data was carried out and has indicated that these MLBEs do not have the capacity to render such services and the funds which have been received from the insurance companies were simply passed on without rendering any relevant services. The amount of Rs. 82,25,822/-from IFTGI was found to be one such transaction of the assessee company.

10. The relevant paragraphs of the impugned order dated 23.06.2025 reads as under:

“2. 1 On perusal of the information uploaded on the insight portal, it is noticed that a Search and seizure u/s 132 on Middle Layer Business Entities (MLBEs) of Insurance Sector was conducted on 30.11.2022 by Investigation Unit -1 and Unit-5, Mumbai under names Wings Brand Group and Ajay Mehta group respectively to verify the claim of services against which these entities have received huge payments from the insurance companies. These MLBEs were not authorized to receive the commission since they are not registered with the IRDAI and they acted as pass-through entities for Insurance Companies. These payments were masked as various heads of expenses such as online media and advertisement services, online marketing, marketing activities, brand promotion expense etc. These were finally paid either to Insurance agents/insurance intermediaries/MPHs or to their nominees. 37 Entities (MLBEs) were covered during search operation and 32 insurance companies were covered as part of post search verification.

2.2 The search action revealed that these MLBEs have acted merely as pass-through entities and transferred the additional commission (also called as Overriding commission-ORC), over and above the IRDAI limit, to Insurance intermediaries/agents, Master Policy holders or their nominees. The evidences gathered from different premises clearly established the nexus between Insurance Companies and the end beneficiaries who are either the Insurance agents/intermediaries Master Policy holders, or their nominees. The Middle Layer Business Entities have shown the payments received from Insurance Companies under the head business promotion, marketing expenses, advertisement expense etc. and have further debited expenses under different heads to transfer the commission over and above the IRDAI limit to the end beneficiaries. These middle layer entities acted as payment facilitator and passed on the amount received from insurance companies to nominees of insurance intermediaries and agents.

2.3 The Insurance companies have signed service agreements with several middle layer business entities (MLBEs) for transferring huge payments under the head marketing and business promotion to various entities. Analysis of financial data and enquiries of these entities were carried out by the Investigation Wing which indicated that these entities are not having the capacity to render such services. They have received the fund from the Insurance companies and simply passed on the funds to other individuals and other business entities without receiving any services.

2.4 From the investigation report it is gathered that the assessee company also found to be involved in bogus transaction amounting to Rs. 82,25,822/- with IFFCO-TOKIO General Insurance Company Ltd.

3. Considering the above referred credible information and analysis, subsequent to the information, proceedings u/s 148A of the Income-tax Act, 1961 was initiated. In view of the above facts and circumstances of the case, a show cause notice u/s 148A(1) was issued to the assessee on 31/03/2025 requesting the assessee company to respond by 17/04/2025, as it appeared that income chargeable to tax has escaped assessment for the transaction mentioned above amounting to Rs. 82,25,822/-during the year under consideration. In response of the notice the assessee has submitted its submission on 17-04-2025. Relevant portion of the reply is reproduced as under:-

“..In the matter under consideration the assessee has taken a written email confirmation from ITGI stating that the amount of INR 82,25,822/- as shown in the insight portal is a genuine transaction and it pertains to the brokerage income against the premium placed by the assessee to ITGI on behalf of their various client’s insurance policies.

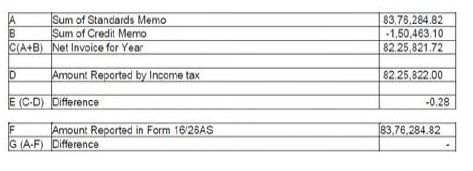

In the email confirmation received from ITGI dated 14/04/2025, the officials of ITGI shared a reconciliation summary of Form 26AS versus the amount reported on income tax insight portal. In the reconciliation received over the mail, the difference is on account of credit memos which are not reported in Form 26AS but reported on insight portal.

The assesee hereby further states that they have reported a taxable income of Rs. 83,28,333/- as brokerage (basis on the monthly statements received from the ITGI) in their Audited Financials ofAY 19-20. A reconciliation of reported income versus the amount reported in the Insight portal is as below:

It can be verified from the above reconciliation that during the Financial Year 2018-19 (AY 2019-20), the assessee has reported a taxable income of Rs. 83,28,333/-which is higher than the amount of Rs. 82,25,822/- as reported on Insight portal of the Income Tax department.

2. This is a legitimate income within IRDAI rules and regulations and the same has also been declared in our profit and loss account.

3. Please find attached here with a list of invoices along with copies of invoices (backed up by insurer statements) that were raised on Iffco-Tokio General Insurance Company Ltd during the period from 1st of April 2018 to 31st of March 2019, (AY 2019-20). The total of all these invoices is INR. 83,28,333/- and the same amount has been appropriated as income in the profit and loss account for the FY 2018-19 (AY 201920).

4. So, all the relevant documents have been reconciled and are matching with each other confirming that an amount of Rs. 83,28,333/- is the only amount received from ITGI against the premium placed by us to them through the policies of our various clients. And this amount has already been accounting in our profit and loss statement and due tax has already been paid on the same.

Also, it would not be out of place to mention that throughout the life span of our existence, we as company have remained profitable, deposited our taxes diligently and have contributed significantly to the cause of the country. Last 5years data is self-explanatory and have been reproduced below for your kind perusal: –

| FY | Revenue (in Cr) | Profit Before tax (Amount in Cr| | %age profit reported |

| 23-24 | 80.83 | 27.79 | 34% |

| 22-23 | 72.09 | 21.69 | 30% |

| 21-22 | 46.56 | 11.67 | 25% |

| 20-21 | 33.59 | 8.47 | 25% |

| 19-20 | 23.29 | 7.16 | 31% |

| Total | 256.36 | 76.78 | 30% |

Further kindly note below points also:

(a) Any income/payment which we have received from ITGI have been booked in our profit and loss account and tax has been paid on the same. (Annexure 4a to 4c Invoice copies with ITGI statements)

(b) We have no relationship whatsoever with Wings Brand Group and Ajay Mehta group herein referred as MLBES.

(c) We have not received any income/payment directly or indirectly through any of these MLBES.

(d) As per our limited knowledge the practice of additional commissions over and above IRDAI prescribed norms were prevalent in retail insurance business and not in corporate or group insurance business.

(e) We are a IRDAI broker whose more than 99% of business is group business and not retail business.

(f) We categorically deny our involvement in any bogus transaction and all the above submissions are evident of the same.

In view of above stated facts, we pray that your Honor shall accept our submission as our true and correct submission.

The notice under section 148 of the Income Tax Act, 1961 should not be issued as there is no suppression of income and that we have earned only the legitimate brokerage as per prescribed IRDA guidelines which has been fully disclosed in the return of income filed with the Income Tax Authorities for the AY 2019-20.

We assure you of our full cooperation in this matter and are committed toproviding all necessary information and documentation.”

Alongwith the above reply, documents in support of assessee’s claim was also furnished

4. The entire submissions of the assessee have been considered and carefully gone through and it is found that the reply of the assessee is vague and inconclusive. ITGI’s email confirmation (14/04/2025) is a self-serving document without third-party verification which can not be relied upon. Similarly, the invoices furnished alone does not prove the genuineness of transactions.

4.1 The core issue as mentioned in the showcause notice has not at all been addressed as no comment has been made with regard to percentage of commission received from IFFCO Tokyo General Insurance Company Ltd(ITGI) and has given very vague reply stating:

” as per our limited knowledge the practice of additional commissions over and above IRDAI prescribed norms were prevalent in retail insurance business and not in corporate or group insurance business”.

No working of commission in terms of % of premium receipts has been given. Mere denial of the issues involved is insufficient to accept the plea of the assessee. In light of the same, the reply of the assessee is considered evasive and devoid of substantial documentary evidence and therefore can not be accepted.

5. In this case income likely to escape is more than Rs.50 lakhs and the same is represented in the form of transaction or entries as mentioned above which shows the income chargeable to tax, which has escaped assessment, amounts to more than fifty lakhs rupees. Thus, the assessee’s case is covered under provision of section 149 (1)(b) of the Income Tax Act, 1961. Accordingly, it is concluded that it is a fit case for issuing notice u/s 148 of the Act for A.Y. 2019-20.

6. Accordingly, after considering the facts of the case, as mentioned above, it is concluded that this case is a fit case for issuing notice u/s 148 of the I.T. Act.”

11. We have recently decided a matter which squarely covers the issue in the case of R S Alloys v. ITO 217 (Delhi)/2025 SCC OnLine Del 5798

“29. The conclusion of the AO is that mere maintenance of the documents and books of accounts provided by the assessee does not mean that there are no discrepancies in the sales and purchases made by the assessee. He has laid stress on the fact that M/s. Karthik Alloys Pvt. Ltd. was a defaulter and debtor of huge payments towards a second party on account of nonpayment against purchases. He also stated that these facts further weaken the stand of the assessee that M/s. Karthik Alloys Pvt. Ltd. has made genuine transactions with the assessee amounting to Rs. 88,86,000/-. In fact he has also noted that the order passed by the NCLAT, Mumbai Bench in the case of Karthik Alloys Pvt. Ltd. would also show that it was not in a position to make huge transactions and ultimately to run business and it only suggested that M/s. Karthik Alloys Pvt. Ltd. had financial crises during the relevant year under consideration. It was also noted that M/s. Karthik Alloys Pvt. Ltd. had filed return of income only for the year 2018-2019 showing nil’ ‘ income and ni.il ‘profit before tax. In other words, huge business transactions undertaken by the entity does not appear commensurate with the ITR filed by the said entity.

30. Suffice it to state, while the petitioner contends that the transaction relating to the amount of Rs. 88,86,000/- is genuine, it is the stand of the respondents that it is a sham transaction whereby M/s. Karthik Alloys Pvt. Ltd. has issued bogus bills to the assessee in order to suppress actual income by claiming Input Tax Credit in GST returns. This is a pure question of fact and needs to be looked into and enquired scrupulously and it is necessary to issue notice primarily to carry out the reassessment proceedings and ascertain as to whether the said transaction needs to be added to income for the purpose of tax or not. In fact, the Revenue has taken precisely this stand in these proceedings, that on the basis of the documentary evidence filed by the assessee and after hearing it, such an exercise needs to be carried out.

31. Having said that, it is also apposite to mention here that there is no violation of the principles of natural justice, as alleged by the assessee. It is based on the notice dated 28.03.2025, to which response was filed by the assessee that the reassessment order has been passed.

32. It is not the case of the assessee that no opportunity of hearing was granted by the AO pursuant to the notice under Section 148A(1) of the Act, which resulted into the order under Section 143A(3) of the Act. It is also not contested that the present action has been taken based on the information available with the respondent under Risk Management Strategy formulated by the CBDT, which is recognised under Section 148(3)(i) of the Act. It is in pursuance of this that the respondent has taken a view that that income chargeable to tax has escaped assessment in the case of the assessee during the relevant AY. A reference to the same has been made in the show cause notice issued under Section 148A(1) of the Act, which reads as under:—

“2. Information available with this office under risk management strategy formulated by CBDT suggests that income chargeable to tax has escaped assessment in the case of assessee during the relevant assessment year. Copy of case related information as downloaded from the Insight Portal in your case is also annexed herewith. ”

If that be so, initiation of the reassessment proceedings cannot be faulted. “

(Emphasis supplied)

12. In another judgment on a similar issue a co-ordinate Bench of this Court in the case titled Majestic Handicraft (P.) Ltd. v. Dy. CIT 2024 SCC OnLine Del 8858 held as under:

“19. At the stage of issuance of notice under Section 148 of the Act, the AO is required to have reasons to assume that the income of the assessee has escaped assessment. Section 148A of the Act sets out a mechanism for ensuring that the AO’s decisions are not based on any unfounded suspicion. The scheme thus, entails a preliminary enquiry, which in this case was done by the department. It is then followed by a notice under Section 148A(b) of the Act to enable the assessee to respond to the information that is available. The AO is required to consider the assessee’s response under Section 148A(c) of the Act in taking an informed decision whether it is a fit case to reopen the assessment by passing an order under Section 148A(d) of the Act. This exercise is for a limited scope of merely determining whether the assessment is required to be reopened. It does not foreclose the assessee’s contention regarding the genuineness of the ITRs. All rights and contentions of an assessee to support its declaration of ITR is available to the assessee.

20. At the stage of Section 148A of the Act, the AO is merely required to form a view whether he has reasons which indicate that the assessee’s income has escaped assessment. In the present case, there is material on record – the sufficiency of which, this court is not required to examine – which bears a live nexus to the opinion that the petitioner’s income has escaped assessment. The material indicates that there is evidence that two of the entities from whom the petitioner had procured materials are not genuine. The bank accounts indicate matching of inflows and outflows coupled with the high turnover in a short span of time. This provides the reasons for the AO to question the purchases that are declared by the petitioner.”

13. It is seen from the above that the contention of the petitioner in respect of the sum of Rs. 82,25,822/- being an amount which has been declared in books and return of income tax and as such the impugned notice which alleges that such an amount has escaped the assessment is clearly untenable, is concerned the issue need to be seen in facts for which it is imperative that the notice is issued to elicit a reply and to check whether the sum of Rs. 82,25,822/- is a result of a spurious transaction, resulting in the income escaping assessment/Tax. Such an exercise shall be undertaken by the Assessing Officer, and surely not by this Court.

14. Suffice to state that the reliance placed by Mr. Gupta on the judgment in the case of Jindal Saw Ltd. ( supra) can be distinguished on facts in as much as the notice under Section 148A(b) was issued on account of undeclared/unexplained income whereas, the assessee in that case had sufficiently explained the amount and the impugned order in that case was seen to be at variance with the allegations made in the impugned notice in the said case. Needless to state, the reliance placed by Mr. Gupta on this judgment is misplaced.

15. In view of the above, we find no merit in this petition and the same is dismissed along with the accompanying application for stay.