ORDER

S.R. Raghunatha, Accountant Member.- The present appeal is filed by the revenue being aggrieved by order of the Ld. Commissioner of Income Tax (Appeals) Chennai – 20 (in short ‘Ld.CIT(A)) dated 26.03.2025 in Appeal No.CIT(A), Chennai – 18/10926/201819 for the Assessment Year 2019-20.

2. The brief facts of the present case are that the assessee is a Charitable Trust registered u/s.12AA of Income Tax Act, 1961 (in short ‘the Act’) in F.No.DIT(E)No.2(17)/07-08 in the file of the then Director of Income Tax(Exemptions), Chennai dated 10.10.2007.

3. The assessee trust for the assessment year 2019-20 had filed its return of income u/s.139(1) Act on 30.10.2019 in declaring Total income at Rs.Nil after claiming exemption u/s.11 of Act. It is also seen that the assessee had filed Form No.10 30.10.2019 by seeking accumulation of funds in terms of Section 11(2)(a) of the Act to the extent of Rs.11,22,95,380/-.

4. The Income Tax Department had conducted search and seizure action u/s.132 of the Act on 09.12.2020 in the case of Chettinad Group, wherein the assessee herein was also searched.

5. The Assessing Officer (AO) had accordingly issued notice u/s.153A of Act on 16.08.2021. The assessee in response to the same had filed its return of income for the on 21.01.2022 in declaring taxable total income at Rs. Nil after claiming exemption u/s.11 of Act.

6. The AO had thereafter issued notice u/s.143(2) of the Act and notice(s) in terms of Section 142(1) of the Act in calling for details in support of the return of income filed for the A.Y. under consideration.

7. The AO during the course of search assessment proceedings had issued a Show Cause Notice in proposing to disallow a sum of Rs.13,74,25,896/-, being the revenue expenditure claimed on account of income tax paid as the said sums were not applied for the purpose of charitable activity.

8. The assessee in response to the said Show Cause Notice had submitted that the said amount had been claimed as application inadvertently and requested that the same to be considered as accumulation and to be utilized for the objects of the trust u/s.11(2)(a) of the Act.

9. The assessee in support of the above submissions had filed a revised Form 10 on 14.03.2022 in seeking accumulation to the extent of Rs.13,74,25,896/- as against the original Form No.10 filed on 30.10.2019 in seeking accumulation to the extent of Rs.11,22,95,380/-. However, the AO had rejected the revised Form No.10 filed on 14.03.2022 by holding that the same was not filed within the stipulated time limit u/s.139(1) of the Act and proceeded to disallow a sum of Rs.13,74,25,896/- debited in the Income & Expenditure account and accounted for as application towards charitable purposes and computed the same as income in hands of the assessee trust vide search assessment passed u/s.153A of the Act dated 31.03.2022 by determining the taxable total income at Rs.11,88,16,000/-.

10. The assessee trust aggrieved by the said search assessment order dated 31.03.2022, had challenged the same before the Ld.CIT(A).

11. The assessee during the course of appellate proceedings had contended that it was not case of a taxpayer filing fresh / original Form No.10 for the first time during the course of assessment proceedings beyond the time limit prescribed u/s.139(1) of the Act, rather it was a case of the assessee filing a revised Form No.10 by revising the original Form No.10 filed well within the stipulated time limit prescribed u/s.139(1) of the Act and as such the assessee had sufficiently complied with the conditions seeking accumulation u/s.11(2)(a) of the Act. The assessee had placed reliance upon the decision of the jurisdictional High Court in the case CIT v. National College Council [TCA No. 584 of 2014] and Chandraprabhuji Maharaj Jain v. Dy. CIT (Madras)/TCA No. 517 of 2019 in support of the above submissions.

12. The Ld.CIT (A) vide their appellate order 26.03.2025 had observed that there was no specific prohibition under the statue to file modified / revised Form No.10 during the course of assessment proceedings so as long as the original Form No.10 was found to have been filed within the time limit prescribed u/s.139(1) of the Act. The Ld.CIT(A) had further concluded that law laid down by the jurisdictional Madras High Court in National College Council as well as in Shri Chandraprabhuji Maharaj Jain would also be applicable for the assessment year under consideration. The Ld.CIT(A) after examining the provisions had come to a conclusion that even after the amendment brought to the statute by the Finance Act, 2015, w.e.f 01.04.2016 (from Assessment Year: 2016-17) the ratio law laid down in the said judgements would not change in view of the fact that Rule 17 of Income Tax Rules, 1962, which rule prescribes filing of Form No.10 in terms of Section 11(2)(a) of the Act, had prescribed a time limit for filing the Form No.10, even before the statutory amendment to Section 11(2)(c), introducing the time limit for filing the said Form No.10. The Ld.CIT(A) had accordingly allowed the appeal of the assessee in directing the AO to delete the disallowance forming part of the search assessment order passed u/s.153A of the Act dated 31.03.2022.

13. The revenue challenging the said appellate order passed by the ld.CIT(A) dated 26.03.2025 had filed the present appeal by raising the following grounds of appeal:

The order of the learned Commissioner of Income Tax (Appeals) is erroneous on facts of the case and in law.

| (i) |

|

The Ld.CIT(A) erred by deleting the disallowance of revised exemption of Rs. 13,74,25,896/- by deciding the issue solely based on the criteria as to whether the assessee is eligible to file revised Form 10 during the assessment proceeding, without considering the legal fact that accumulation u/s 11(1) and 11(2) does not include payments made to fulfil the personal statutory obligations of the assessee like Income-tax dues. |

| (ii) |

|

The Ld CIT(A) has failed to appreciate that the section 11(1)(a) & (2) of the Income-tax Act allows accumulation only if the income is to be applied to the objects of the trust, i.e., charitable/ religious purposes, while Income Tax dues are personal statutory obligations of the assessee and cannot be considered charitable application and hence are not eligible for accumulation. |

| (iii) |

|

The Ld. CIT(A) erred by placing reliance on the judgment of Hon’ble High Court in the case of CIT v National College Council CIT v. National College Council [TCA No. 584 of 2014] which is distinguishable from the facts of the instant case |

| (iv) |

|

Ld. CIT(A) failed to consider that in the case of CIT v National College Council the Hon’ble Court allowed enhancement of accumulation and filing of revised Form-10 on the disallowed claim of application in respect of the depreciation, which is otherwise accepted as either a non-cash expense indirectly contributing to charitable activity, or capable of being ‘applied’ in revised From 10 under judicial interpretations, while in the assessee’s case, the revised Form 10 was filed to cover Income tax dues, which cannot be considered a part of the trust’s charitable activities as analogous to depreciation (which is related to charitable capital asset use). |

| (v) |

|

The Ld.CIT(A) has failed to consider that w.e.f 01.04.2016, after introduction of Clause (c) to sub-section 11(2) of the Income-tax Act, the assessee is bound to file Form-10 on or before the due date specified under sub-section (1) of section 139 for claiming accumulation and prior to this there was no provision delineating a time limit, either in the Act or Rule, for filing of Form-10. |

| (vi) |

|

For these grounds and any other ground including amendment of grounds that may be raised during the course of the appeal proceedings, the order of learned CIT(Appeals) may be set aside and that of the Assessing Officer be restored. |

14. The ld.DR before us argued that the Ld.CIT(A) ought not to have allowed claim of accumulation through the revised Form No.10 as the same was not filed within the time limit prescribed u/s.11 of the Act and the non-filing of the revised Form No.10 within the said limit would dis-entitle the assessee from claiming the revised computation of accumulation u/s.11(2)(a) of the Act. Furthermore, it was argued that the decisions rendered by the Hon’ble Madras High Court referred to by the assessee during the appellate proceedings as well as relied upon by the Ld.CIT(A) were rendered prior to amendment brought out to Finance Act, 2015 and accordingly the same would not applicable to the facts of the present case in view of the assessment year under consideration being A.Y.2019-20. The ld.DR accordingly pleaded for reversing the decision rendered by the Ld.CIT(A) in restoring the order of search assessment passed u/s.153A of the Act.

15. Per contra, the Ld.AR argued that the original Form No.10 was filed on 30.10.2019, which was well within the stipulated time limit prescribed u/s.139(1) of the Act and it was only a case of the revised Form No.10 being filed during the course of assessment on 14.03.2022 and hence it was not case of the complete non filing of Form No.10. The Ld. AR argued that in any event, filing of even the Form No.10 within the time limit prescribed u/s.139(1) of the Act was only a directory and not mandatory inasmuch the non filing of the same within the time limit stipulated u/s.139(1) of the Act would not automatically result in disentitle of claim of accumulation u/s.11(2)(a) of the Act so as long the same was filed before the completion of assessment proceedings. However, on the facts of the present case, it was argued that the original Form No.10 was filed within the prescribed time limit and only the revised Form No.10 was filed before the completion of assessment. The Ld. AR argued that the revised Form No.10 was filed on 14.03.2022 and the same was made available in the file of the AO while prior to passing the search assessment order dated 31.03.2022 passed u/s.153A of the Act and accordingly pleaded for dismissing the revenue’s appeal in confirming the order of the Ld.CIT(A) which places reliance on judgments of the Jurisdictional High Court supra.

16. We have heard the rival contentions perused the material available on record and gone through the orders of the lower authorities along with judicial precedents relied on. The moot question for our consideration is whether the action of the assessee in revising the Form No.10 earlier filed within the due date as prescribed during the course of assessment proceedings would disentitle the claim of revised accumulation on ground of not filing within the prescribed time limit.

17. It is an undisputed fact that the assessee trust had filed its original return of income as well as the Form No.10 within time limit prescribed u/s.139(1) of the Act on 30.10.2019. The assessee in the said Form No.10, i.e. original Form No.10 had reported a sum of Rs.11,22,95,380/- as the amount being accumulated or set apart. The assessee trust during the course of search assessment proceedings had filed revised Form No.10 on 14.03.2022 in reporting a sum of Rs.13,74,25,896/- as amount being accumulated or set apart. However, the said revised claim of accumulation u/s.11(2)(a) of the Act came to be rejected for the reasons captured in the preceding paragraphs.

18. To answer the said issue, we are drawing an analogy to the procedure for filing revised return of income u/s.139(5) of the Act, wherein the return of income so revised would relate back to the original return of income, be it a return of income filed u/s.139(1) of the Act or a belated return of income u/s.139(5) of the Act.

19. The revised return of income would most definitely be filed beyond the time limit prescribed u/s.139(1) of the Act, while however the same would only relate back to the original return of income in sense, the assessee is only revising reporting of a particular, which reporting was already made by the assessee. The doctrine of relation back postulates that when there are some infirmities / irregularities in the original return filed by the tax payer, which is rectified, although at a later point in time, the revised filing of the return would only relate back to the date of the original filing of return.

20. The Hon’ble Delhi High Court in the case of Commissioner of Income-tax v. Haryana Sheet Glass Ltd (Delhi)/[2009] 318 ITR 173 (Delhi), while examining the validity of the revised return of income had held as follows:

“2. We are of the opinion that the Tribunal rightly applied the doctrine of relation back. This doctrine postulates that when there are some irregularities in the original return, which though is rectified at a later date, and the defect is cured, the filing of the return will relate back to the original date.

3. Learned counsel for the revenue has drawn our attention to the judgment of this Court in the case of

Electrical Instrument Co. v.

CIT [2001] 250 ITR 734. That was a case where original Income-tax return filed was unsigned and unverified. In these circumstances, it was treated as invalid return.

4. It is trite law that if an act is invalid, it may not be cured and in these circumstances, the doctrine of relation back was not applied in the said case. Therefore, a fine distinction is to be drawn and understood. If the irregularity in the original return is curable, then the doctrine of relation back would apply, on the other hand, if there is a fundamental defect in the original return, which cannot be cured, then such a doctrine cannot be applied. It is clear that the Secretary has signed the return who is otherwise, as per the provisions of the Company Act, is competent to sign. Provision of section 140 of the Income-tax mandates that the Managing Director or some other responsible officers can sign. Because of this reason, we are of the opinion that in a case like this, the irregularity was curable and the doctrine of relation back was rightly applied.”

21. Thus, drawing the same analogy to the facts of the present case, the revised Form No.10 on 14.03.2022 would definitely relate back to the original Form No.10 filed on 30.10.2019 and according the consequences would follow, which is that the revised Form No.10 dated 14.03.2022 is to be reckoned as Form No.10 filed originally. Hence, we do not agree with the ld.DR that the revised Form No.10 should be seen and considered on a standalone basis and not on a conjoint consideration with the original Form No.10 filed on 30.10.2019. In any event, the revised Form No.10 filed on 14.03.2022 was very much made available in the file of the AO at the time of passing of the search assessment order u/s.153A of the Act and it would not appropriate to say that the AO was deprived from scrutinising the revised reporting / claim of accumulation u/s.11(2)(a) of the Act.

22. We find that the Hon’ble Supreme Court in the case of

Commissioner of Income-tax v.

Nagpur Hotel Owners’ Association,

ITR 201 (SC) while examining the validity of the claim of accumulation u/s.11(2)(

a) of the Act in the event of the tax payer filing the same beyond the time limit prescribed u/s.139(1) of the Act but during the course of assessment proceedings, had held as follows:

“6. It is abundantly clear from the wordings of sub-section (2) of section 11 that it is mandatory for the person claiming the benefit of section 11 to intimate to the assessing authority the particulars required under rule 17 in Form No. 10 of the Act. If during the assessment proceedings the Assessing Officer does not have the necessary information, question of excluding such income from assessment does not arise at all. As a matter of fact, this benefit of excluding this particular part of the income from the net of taxation arises from section 11 and is subjected to the conditions specified therein. Therefore, it is necessary that the assessing authority must have this information at the time it completes the assessment. In the absence of any such information, it will not be possible for the assessing authority to give the assessee the benefit of such exclusion and once the assessment is so completed, in our opinion, it would be futile to find fault with the assessing authority for having included such income in the assessable income of the assessee. Therefore, even assuming that there is no valid limitation prescribed under the Act and the Rules, even then, in our opinion, it is reasonable to presume that the intimation required under section 11 has to be furnished before the assessing authority completes the concerned assessment because such requirement is mandatory and without the particulars of this income, the assessing authority cannot entertain the claim of the assessee under section 11, therefore, compliance of the requirement of the Act will have to be any time before the assessment proceedings. Further, any claim for giving the benefit of section 11 on the basis of information supplied subsequent to the completion of assessment would mean that the assessment order will have to be reopened. In our opinion, the Act does not contemplate such reopening of the assessment. In the case at hand it is evident from the records of the case that the respondent did not furnish the required information till after the assessments for the relevant years were completed. In the light of the above, we are of the opinion that the stand of the revenue that the High Court erred in answering the first question in favour of the assessee is correct, and we reverse that finding and answer the said question in the negative and against the assessee. In view of our answer to the first question, we agree with Mr. Verma that it is not necessary to answer the second question on the facts of the case.”

23. The Hon’ble Delhi High Court in the case of Commissioner of Income-tax (Exemptions) v. Canara Bank Relief and Welfare Society (Delhi), under identical circumstances had held as follows:

21. Insofar as the issue concerning the timing of the filing of Form No.10 is concerned, i.e., in the course of reassessment proceedings, this stands covered by a decision of a coordinate Bench of this court rendered in Association of Corporation & Apex Societies of Handlooms case (supra). For convenience, the relevant parts of the judgment are extracted hereafter:

“5. Having considered the arguments advanced by the counsel for the parties on this aspect of the matter we feel that it would be necessary to set out the reasoning adopted by the Supreme Court in Nagpur Hotel Owners Association (supra). The Supreme Court held as under:-

“It is abundantly clear from the wording of sub-section (2) of section 11 that it is mandatory for the person claiming the benefit of section 11 to intimate to the assessing authority the particulars required, under rule 17 in Form No. 10 of the Rules. If during the assessment proceedings, the Assessing Officer does not have the necessary information, question of excluding such income from assessment does not arise at all. As a matter of fact, this benefit of excluding this particular part of the income from the net of taxation arises from section 11 and is subjected to the conditions specified therein. Therefore, it is necessary that the assessing authority must have this information at the time he completes the assessment. In the absence of any such information, it will not be possible for the assessing authority to give the assessee the benefit of such exclusion and once the assessment is so completed, in our opinion, it would be futile to find fault with the assessing authority for having included such income in the assessable income of the assessee. Therefore, even assuming that there is no valid limitation prescribed under the Act and the Rules even then, in our opinion, it is reasonable to presume that the intimation required under section 11 has to be furnished before the assessing authority completes the concerned assessment because such requirement is mandatory and without the particulars of this income, the assessing authority cannot entertain the claim of the assessee under section 11 of the Act, therefore, compliance with the requirement of the Act will have to be any time before the assessment proceedings. Further, any claim for giving the benefit of section 11 on the basis of information supplied subsequent to the completion of assessment would mean that the assessment order will have to be reopened. In our opinion, the Act does not contemplate such reopening of the assessment. In the case in hand it is evident from the records of the case that the respondent did not furnish the required information till after the assessments for the relevant years were completed. In the light of the above, we are of the opinion that the stand of the Revenue that the High Court erred in answering the first question in favour of the assessee is correct, and we reverse that finding and answer the said question in the negative and against the assessee. In view of our answer to the first question, we agree with Mr. Verma that it is not necessary to answer the second question on the facts of this case.”

On going through the above extract we find that the Supreme Court observed that it was necessary that the assessing authority must have the information under Form-10 at the time he completes the assessment and in its absence it is not possible for the assessing authority to give benefit of such exclusion. Furthermore, once the assessment is so completed it would be futile to find fault with the assessing authority for having included such income in the assessable income of the assessee. The Supreme Court held categorically that without the particulars of this income as given in Form-10, the assessing authority cannot entertain the claim of the assessee under section 11 of the Act and therefore, compliance with the requirement of the Act will have to be at any time before the assessment proceedings are completed. The Supreme Court also observed that any claim for giving the benefit of section 11 on the basis of information supplied subsequent to the completion of assessment would mean that the assessment order will have to be reopened. The Supreme Court noticed that the Act did not contemplate such re-opening of the assessment.

6. The learned counsel for the revenue relied on this portion of the finding of the Supreme Court to contend that during re-assessment proceedings, the said Form-10 could not be furnished by an assessee. However, we have to keep in mind the fact that while reopening of an assessment cannot be asked for by the assessee on the ground that he had not furnished the Form-10 during the original assessment proceedings, this does not mean that when the revenue reopens the assessment by invoking section 147 of the said Act, the assessee would be remediless and would be barred from furnishing Form-10 during those assessment proceedings. Consequently, insofar as the second question is concerned and with regard to the appeal Nos 524/2012, 525/2012 and 526/2012, the same has to be answered in favour of the assessee/appellant and against the revenue. However, with regard to the ITA No.523/2012 because the Form-10 was filed only before the Tribunal, the question has to be decided, in that appeal, against the assessee and in favour of the revenue.”

[Emphasis is ours]

22. Clearly, the respondent/assessee is not precluded from filing a revised Form No.10 during reassessment proceedings.”

24. We find that on the facts of the present case, the revised Form No.10 was very well filed on 14.03.2022 and made available in the file of the AO prior to the completion of assessment proceedings u/s.153A of the Act and the conditions laid down by the Hon’ble Supreme Court in the aforesaid decision is complied by the assessee for the purpose of validly claiming accumulation u/s.11(2)(a) of the Act, even though the same is was on account of belated filing of Form No.10.

25. We find that the Hon’ble Madras High Court in the case of Chandraprabhuji Maharaj Jain (supra) under identical circumstances had held as follows:

“7. Admittedly, the statute does not prescribe any time limit for filing statutory Form No.10. This aspect of the matter was considered by the Honourable Supreme Court in CIT v. Nagpur Hotel Owners Association

(SC)/[2001] 247 ITR 201 (SC). In the said decision, it was pointed out that it is necessary that the Assessing Officer must have information as required under Rule 17 by furnishing Form No.10 and this information should be available with the Assessing Officer at the time when he completes the assessment and in the absence of any such information, it will not be possible for the Assessing Officer to give the assessee, the benefit of such exclusion and once the assessment is complete, it would be futile to find fault with the Assessing Officer. Further, it was pointed out that even assuming that there is no valid limitation prescribed under the Act and Rules, yet it is reasonable to presume that the intimation required under Section 11 has to be furnished before the Assessing Officer completes the concerned assessment, because such requirement is mandatory and without the particulars of the assessee’s income, the Assessing Officer cannot entertain the claim of the assessee under Section 11 and therefore, compliance of the requirement of the Act will have to be any time before the assessment proceedings are completed. The ultimate decision went in favour of the Revenue. Yet, we take note of the findings rendered in the decision, stating that before completion of the assessment, the information should be made available to be Assessing Officer.

8. As noted by us earlier, the assessee filed the return of income for the assessment year under consideration on 02.04.2009, which was processed and intimation under Section 143(1) of the Act was issued on 21.01.2011. Thus, there was no assessment under Section 143(3) of the Act. The assessee, while filing the petition under Section 154 of the Act, on 22.03.2011, pointed out that the assessee filed the Form No.10 along with the Board Resolution along with the covering letter dated 01.04.2019. However, the mistake done by the assessee was to file hard copies before the Assessing Officer, and not filing the same along with the return of income, which they filed on 02.04.2019. Thus, on the date when the return was taken up for assessment, there was record to show that the assessee had intimated the department about the resolution passed by the Board of the assessee Trust and the statutory Form No.10. Admittedly, the assessment was not completed under Section 143(3) of the Act and therefore, there would have been no error had the assessing officer taken up the copy of the Board Resolution and Form No.10. Thus, on the date when the return was filed, the assessee had separately filed Form No.10 along with the Board Resolution along with a covering letter dated 01.04.2009. Thus, in our considered opinion, when the assessee was entitled to a statutory benefit, it would be incumbent upon the concerned authority to examine the admissibility of the benefit than to foreclose the assessee on technicalities.”

26. Furthermore, the Hon’ble Madras High Court in the case of The Commissioner of Income Tax, Trichy v. National College Council in Tax Case Appeal No.584 of 2014 dated 18.03.2021, while examining the validity of the revised Form No. 10 filed during assessment proceedings had held as follows:

“8. On a reading of the said Judgment, it is clear that if Form 10 is filed within the stipulated time and during the course of assessment proceedings before the Assessing Officer, there is no bar prohibiting the assessee from modifying the figure in the application. Only in the case of revised Form 10 being filed after the assessment proceedings, the same cannot be accepted. The said ratio laid down by the Hon’ble Supreme Court supports the case of the assessee.

9. It is not in dispute that the assessee filed Form 10 within the stipulated time. Since the Assessing Officer disallowed the claim of application in respect of the depreciation, it filed a revised Form 10 enhancing the claim. The very intention of the assessee is to accumulate the surplus for the subsequent years. As per the ratio laid down in the Judgment reported in

318 ITR 96 [cited supra], modified Form 10 may be furnished in the course of assessment proceedings and there is no specific bar prohibiting the assessee from modifying the figure of application. The order passed by the Tribunal as well as the Commissioner of Income Tax (Appeals) are just and proper. 10. In these circumstances, we do not find any ground much less any substantial question of law to interfere with the order passed byt he Tribunal. The Tax Case Appeal is liable to be dismissed. Accordingly, the Tax Case Appeal is dismissed. No costs”

27. Thus, we find that the Hon’ble Madras High Court in aforesaid decision had observed that the tax payer is not precluded from filing a revised Form No.10 so as long the same is not filed after the completion of assessment proceedings. On the facts of the present case, the revised Form No.10 was filed on 14.03.2022 before the completion of assessment proceedings vide search assessment order dated 31.03.2022. Hence, on this count too we reject the arguments put forth by the ld.DR.

28. In so far as the argument of the ld.DR that the law declared by the Hon’ble Madras High Court in the preceding paragraphs were in the context prior to the insertion of amendment to Section 11(2) of the Act by the Finance Act, 2015, w.e.f. 01.04.2016, the same is unable to be countenanced by this Tribunal, in view of the language in Rule 17 of the Income Tax Rules, 1962, which Rule corresponds to Section 11(2) of the Act, pre and post amendment by way of Finance Act, 2015.

29. The said Rule prior to the amendment reads as follows:

30. The said Rule post amendment reads as follows:

Prior to substitution, rule 17, as amended by the IT (Amdt.) Rules 1971, w.e.f. 1-41971 and IT (Fifth Amdt) April, 2016 shall be in Form No. 9A and shall be furnished before the expiry of the time allowed under sub-section (1) section 139 of the Act for furnishing the return of income of the relevant assessment year.

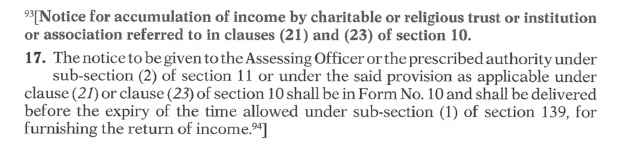

(2) The statement to be furnished to the Assessing Officer or the prescribed authority under clause (a) of the Explanation 3 to the third proviso to clause (23C) of section 10 of the Act or under clause (a) of sub-section (2) section 11 of the Act or under the said provision as applicable under clause (21) of section 10 of the Act shall be in Form No. 10 and shall be furnished before the expiry of the time allowed under subsection (1) of section 139 of the Act, for furnishing the return of income.

(3) The option in Form No. 9A referred to in sub-rule (1) and the statement in Form No 10 referred to in sub-rule (2) shall be furnished electronically either under digital signature or electronic verification code.

(4) The Principal Director General of Income-tax (Systems) or the Director General of Income-tax (Systems), as the case may be, shall—

(i) specify the procedure for filing of Forms referred to in sub-rule (3);

(ii) specify the data structure, standards and manner of generation of electronic verification code, referred to in sub-rule (3), for purpose of verification of the person furnishing the said Forms; and

(iii) be responsible for formulating and implementing appropriate security, archival and retrieval policies in relation to Forms so furnished.]

31. Thus, it can be seen that the Rule 17 of Income Tax Rules, 1962 had indeed prescribed a time limit for filing of Form No.10 being the time limit stipulated u/s.139(1) of the Act. However, the provisions in Section 11(2)(a) of the Act was amended by Finance Act, 2015, w.e.f. 01.04.2016, the statute envisaged filing of Form No.10 u/s.139(1) of the Act which was a stipulation prior to amendment as per Rule 17.

32. The above judgements referred to by us rendered by the Hon’ble Madras High Court were prior to the Finance Act, 2015, wherein the Rule 17 of Income Tax Rules, 1962 had indeed prescribed the time limit for filing Form No.10.

33. Hence, we reject this argument of the ld.DR too. The final argument put forth by the ld.DR is that the filing Form No.10 within the stipulated time limit prescribed u/s.11(2)(a) of the Act is mandatory and the failure to do so would be detrimental to claim of accumulation u/s.11(2)(a) of the Act.

34. On facts, as referred to above, the original Form No.10 was filed within the statutorily prescribed time limit and only the revision of the Form No.10 was made during the course of assessment but before the completion of assessment. There is no express prohibition under the Act for revising Form No.10 earlier filed. Therefore, the argument of the revenue deserves to be rejected.

35. In any event, de hors our findings rendered in the preceding paragraphs, we find that the assessee trust has substantially complied with the conditions laid for claiming accumulation u/s.11(2)(a) of the Act, which are

| (a) |

|

such person furnishes a statement in the prescribed form and in the prescribed manner to the Assessing Officer, |

| (b) |

|

the money so accumulated or set apart is invested or deposited in the forms or modes specified in sub-section (5); |

| (c) |

|

the statement referred to in clause (a) is furnished on or before the due date specified under sub-section (1) of section 139 for furnishing the return of income for the previous year: |

36. It is an undisputed fact that the assessee has complied with the all the conditions envisaged for claiming accumulation u/s.11(2) of the Act. We find that the Hon’ble Supreme Court in the case of Commissioner of Central Excise v. Hari Chand Shri Gopal 2011 AIR SCW 1119, while examining the doctrine of substantial compliance had held as follows:

“24. The doctrine of substantial compliance is a judicial invention, equitable in nature, designed to avoid hardship in cases where a party does all that can reasonably expected of it, but failed or faulted in some minor or inconsequent aspects which cannot be described as the “essence” or the “substance” of the requirements. Like the concept of “reasonableness”, the acceptance or otherwise of a plea of “substantial compliance” depends upon the facts and circumstances of each case and the purpose and object to be achieved and the context of the prerequisites which are essential to achieve the object and purpose of the rule or the regulation. Such a defence cannot be pleaded if a clear statutory prerequisite which effectuates the object and the purpose of the statute has not been met. Certainly, it means that the Court should determine whether the statute has been followed sufficiently so as to carry out the intent for which the statute was enacted and not a mirror image type of strict compliance. Substantial compliance means “actual compliance in respect to the substance essential to every reasonable objective of the statute” and the court should determine whether the statute has been followed sufficiently so as to carry out the intent of the statute and accomplish the reasonable objectives for which it was passed. Fiscal statute generally seeks to preserve the need to comply strictly with regulatory requirements that are important, especially when a party seeks the benefits of an exemption clause that are important. Substantial compliance of an enactment is insisted, where mandatory and directory requirements are lumped together, for in such a case, if mandatory requirements are complied with, it will be proper to say that the enactment has been substantially complied with notwithstanding the non- compliance of directory requirements. In cases where substantial compliance has been found, there has been actual compliance with the statute, albeit procedurally faulty. The doctrine of substantial compliance seeks to preserve the need to comply strictly with the conditions or requirements that are important to invoke a tax or duty exemption and to forgive non-compliance for either unimportant and tangential requirements or requirements that are so confusingly or incorrectly written that an earnest effort at compliance should be accepted. The test for determining the applicability of the substantial compliance doctrine has been the subject of a myriad of cases and quite often, the critical question to be examined is whether the requirements relate to the “substance” or “essence” of the statute, if so, strict adherence to those requirements is a precondition to give effect to that doctrine. On the other hand, if the requirements are procedural or directory in that they are not of the “essence” of the thing to be done but are given with a view to the orderly conduct of business, they may be fulfilled by substantial, if not strict compliance. In other words, a mere attempted compliance may not be sufficient, but actual compliance of those factors which are considered as essential.”

37. We find that since, the assessee trust has substantially complied with the conditions precedent for claiming accumulation u/s.11(2)(a) of the Act, the same should be not denied on the mere technical ground.

38. Hence, for all the reasons stated in the preceding paragraphs, the appeal filed by the revenue is dismissed and the order of the Ld. CIT(A) is upheld.

39. In the result, the appeal of the revenue is dismissed.