ORDER

Madhusudan Sawdia, Accountant Member. – This appeal is filed by Shri Penninti Vivekananda Rao (“the assessee”), feeling aggrieved by the order passed by the Learned Commissioner of Income Tax (Appeals)-10, Hyderabad (“Ld. CIT(A)”) dated 29.07.2025 for the A.Y 2020-21.

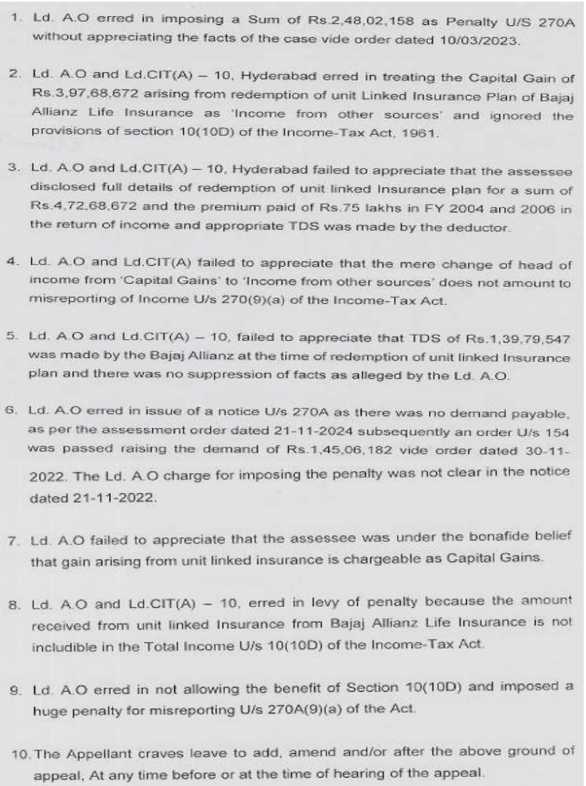

2. The assessee has raised the following grounds of appeal:

3. The brief facts of the case are that the assessee is a non-resident individual who filed his return of income for A.Y. 2020-21 on 02.12.2020, declaring a total income of Rs.5,20,66,038/-, consisting of Capital Gains of Rs.4,78,14,391/-and Income from Other Sources of Rs.42,61,647/-. Out of the total capital gains, the assessee had shown Rs.3,22,68,672/- arising from surrender of three Equity Plus Fund issued by Bajaj Allianz Life Insurance Co. Ltd. (“Bajaj Equity Plus Fund”). The case of the assessee was selected for complete scrutiny under CASS, and statutory notices under section 143(2) and 142(1) of the Income Tax Act,1961 (” the Act”) were issued to the assessee. The assessee had purchased the three Bajaj Equity Plus Fund of Rs.25 lakhs each on 28.11.2004, 28.03.2005 and 22.01.2006 respectively. During the assessment proceedings, the Ld. AO held that the gain on surrender of Bajaj Equity Plus Fund is taxable under the head “Income from Other Sources” and not “Capital Gains.” Accordingly, the Ld. AO initiated the penalty proceedings under section 270A of the Act for misreporting of income. The assessee sought immunity under section 270AA of the Act, which was rejected, and ultimately penalty of Rs.2,48,02,158/- was levied by the Ld. AO under section 270A of the Act, vide penalty order dated 10.03.2023.

4. Aggrieved with the order of the Ld. AO, the assessee filed appeal before the Ld. CIT(A). The Ld. CIT (A) upheld the penalty levied by the Ld. AO.

5. Aggrieved with the order of the Ld. CIT (A), the assessee is now in appeal before the Tribunal. At the outset, the Learned Authorized Representative (“Ld. AR”) submitted that the solitary issue arising out of the grounds of appeal of the assessee is on account of the levy of penalty of Rs. Rs.2,48,02,158/- under section 270A of the Act. The arguments of the Ld. AR were manifold. One of the objections raised by the Ld. AR is that there is no case of misreporting under section 270A (9) of the Act in the case of the assessee. In this regard, the Ld. AR invited out attention to the computation of income of the assessee placed at page no. 13 of the paper book and submitted that the assessee disclosed all facts fully and truly in his return of income. The only dispute in the present case is regarding the head of taxability of the income, whether it is taxable under the head of capital gain or under the head of income from other sources. The assessee under a bonafide belief had offered the income under the head of capital gain. However, the Ld.AO made it taxable under the head of income from other source. As such there is no misrepresentation or suppression of facts on the part of the assessee. Hence, the case of the assessee does not fall under any of the clauses (a) to (f) of section 270A (9) of the Act and the penalty levied by the Ld. AO is liable to be deleted. In support of his contention, the Ld. AR placed reliance on the following judicial precedents:

| (a) |

|

Hon’ble Supreme Court in the case of CIT, Ahmedabad v. Reliance Petroproducts (P.) Ltd. ITR 158 (SC) |

| (b) |

|

ITAT Mumbai Benches in the case of D.C. Polyester Ltd. v. DCIT (Mumbai – Trib.)/(ITA No. 188/Mum/2023, dated 17.10.2023) |

| (c) |

|

ITAT Chennai Benches in the case of S. Saroja v. Dy. CIT (Chennai – Trib.)/(ITA No. 418/Chny/2023, dated 31.05.2023) |

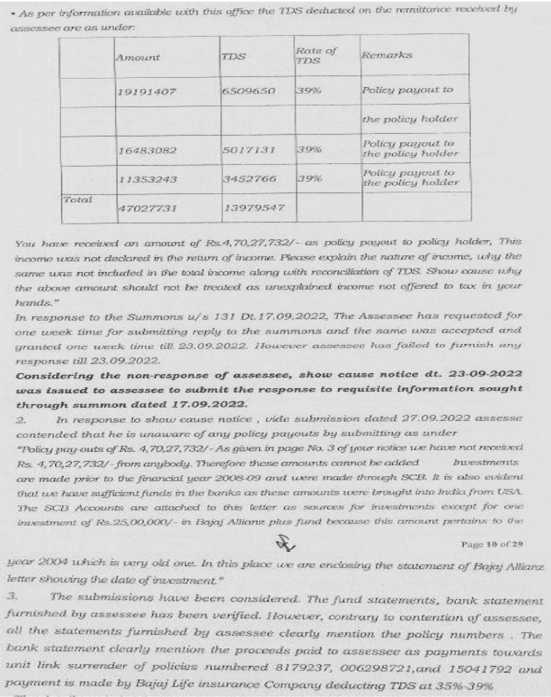

6. Per contra, the Departmental Representative (“Ld. DR”) supported the orders of the lower authorities. The Ld. DR also invited our attention to page nos. 10 and 11 of the order of the Ld. CIT (A), the relevant portion of the same is reproduced as under:

6.1 On the basis of above findings of the Ld. CIT (A), the Ld. DR submitted that the assessee had not offered the income from surrender of the Bajaj Equity Plus Fund in his return of income. Accordingly, the lower authority has rightly levied the penalty under section 270A of the Act on the assessee. He accordingly prayed for sustaining the penalty.

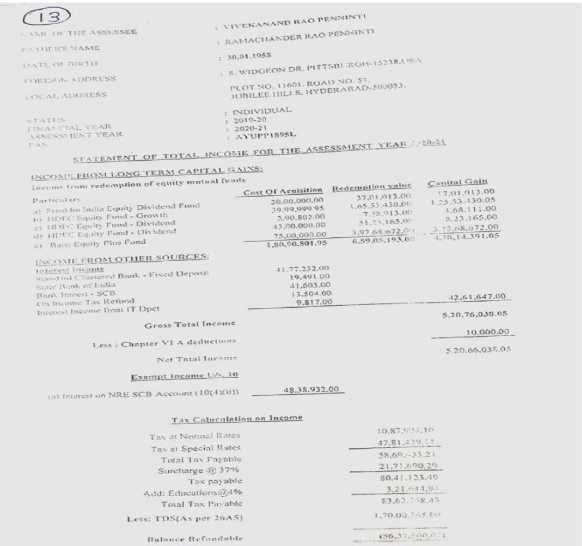

7. We have considered the rival submissions and perused the material available on record including the judicial precedents relied upon. As regards the objection of the Ld. DR that the assessee had not offered the income from surrender of the Bajaj Equity Plus Fund in his return of income, we have gone through the computation of income of the assessee placed at page no. 13 of the paper book which is to the following effect:

8. On perusal of the above, we find that the assessee has offered income of Rs.3,22,68,672/- with regard to surrender of the Bajaj Equity Plus Fund in his return of income. Accordingly, this objection of the Ld. DR is factually incorrect and is rejected. On the other hand, the Ld. AR has argued that there is no case of misreporting under section 270A (9) of the Act in the case of the assessee. The Ld. AR has submitted that the assessee disclosed all facts fully and truly in his return of income. The Ld. AR has also submitted that the assessee under a bonafide belief had offered the income under the head of capital gain. However, the Ld.AO made it taxable under the head of income from other source. As such there is no misrepresentation or suppression of facts on the part of the assessee. Hence, the Ld. AR has submitted that the case of the assessee does not fall under any of the clauses (a) to (f) of section 270A (9) of the Act and the penalty levied by the Ld. AO is liable to be deleted. In this regard, on perusal of the computation of income of the assessee, we find that the assessee has offered income of Rs.3,22,68,672/- with regard to surrender of the Bajaj Equity Plus Fund in his return of income. Hence we are of the considered view that the assessee has disclosed all facts fully and truly in his return of income. Therefore, the only issue left for our consideration is that where the assessee has offered an income under the head of capital gain instead of under the head of income from other sources, whether the penalty of misreporting under section 270A (9) of the Act can be levied on the assessee or not. In this context, it is crucial to go through the provisions of section 270A(9) of the Act dealing with the penalty in the case of misreporting of income, which is to the following effect :

Section 270A(9) in The Income Tax Act, 1961

(9)The cases of misreporting of income referred to in subsection (8) shall be the following, namely:— (a)misrepresentation or suppression of facts;(b) failure to record investments in the books of account; (c)claim of expenditure not substantiated by any evidence;(d)recording of any false entry in the books of account;(e)failure to record any receipt in books of account having a bearing on total income; and(f) failure to report any international transaction or any transaction deemed to be an international transaction or any specified domestic transaction, to which the provisions of Chapter X apply.”

9. On perusal of above, it is evident that for levy of penalty under section 270A(9) of the Act, the case of the assessee must fall under one of the clauses (a) to (f) of the said sub-section. In the present case, the assessee has duly offered the income arising on transfer of Bajaj Equity Plus Fund in the return of income. The only issue involved is that the assessee has offered the said income under an incorrect head, i.e., under the head “Capital Gains” instead of under the head “Income from Other Sources.” In our considered view, as the assessee has disclosed the income in the return of income, there is no misrepresentation or suppression of facts on the part of the assessee. Consequently, the assessee’s case does not fall under any of the clauses (a) to (f) of section 270A(9) of the Act. The situation is merely one of wrong reporting of the income under an incorrect head, and nothing more. In this regard, we have gone through the para nos. 10 & 11 of the decision of the Co-ordinate Bench of the ITAT, Mumbai, in the case of D.C. Polyester Ltd v. DCIT (supra), relied upon by the assessee, which is to the following effect:

“10. We heard rival contentions and perused the record. We notice that section 270A of the Act uses the expression “the

Assessing Officer ‘may direct”. Hence there is merit in the contention of the assessee that levying of penalty is not automatic and discretion is given to the Assessing Officer not to initiate penalty proceedings under section 270A of the Act. From the facts discussed earlier, it can be noticed that the addition came to be made on account of change in the head of income for assessing the rental income. We noticed that the assessee had offered rental income under the head “Income from House Property,” but the assessing officer has assessed the same under the head “Income from business.” The standard deduction @ 30% allowable u/s 24(a) while computing income under the head Income from house property will not be available when it is assessed under the Income from business. Thus, it is not a case that the assessee has suppressed or under reported any income. The addition came to be made to the total income returned by the assessee, due to change in the head of income, i.e., the addition has arisen on account of computational methodology prescribed in the Act. In our view, this kind of addition will not give rise to under reporting of income. Accordingly, we are of the view that the AO should have exercised his discretion not to initiate penalty proceedings u/s 270A of the Act in the facts and circumstances of the case.

11. As submitted by Ld A.R that sub. Sec. (2) of sec. 270A lists out the instances which are considered to be “under reporting” of income and clause (g) of it covers the case, when loss is converted into income. However, subsection (6) of section 270A lists out exceptions to sub. Sec (2), i.e., the instances which will not be considered as cases of ‘under reporting’ of income. Clause (a) of sub. Sec. (6) specifically states that the amount of income in respect of which the assessee offers an explanation and the Assessing Officer is satisfied that the explanation is bonafide and the assessee has disclosed all material facts to substantiate explanation so offered will not be considered as under reporting of income. In the instant case, as noticed earlier, the assessee has not under reported any income. The addition has arisen on account of change in head of income. We notice that the assessee has offered an explanation as to why it reported the rental income under the head Income from House property and the said explanation is not found to be false. Accordingly, we are of the view that the case of the assessee is covered by clause (a) of sub.sec. (6) of sec. 270A of the Act. We notice that the Chennai bench of Tribunal has held in the case of S Saroja (supra) that bonafide mistake committed while computing total income, the penalty u/s 270A of the Act should not be levied.”

10. On perusal of above, we find that in that case also, the assessee had offered income under the head “Income from House Property” instead of under the correct head “Profits and Gains of Business or Profession.” The ITAT held that penalty under section 270A of the Act cannot be levied merely because of a change of head of income. Hence, respectfully following the same, under the present facts and circumstances of the case, we are of the considered view that no penalty can be levied under section 270A(9)of the Act in the case of the assessee. Accordingly, we direct the Ld. AO to delete the penalty.

11. Since we have decided the issue in favour of the assessee on merit, other alternative arguments of the assessee on merits and the legal grounds challenging the validity of the impugned order are rendered academic and are not adjudicated.

12. In the result, the appeal of the assessee is allowed.