HC Remands Ex Gratia Payment Case for Fresh Decision on Taxability.

Issue

Whether a voluntary, ex-gratia payment made by an employer to an employee upon resignation is taxable as ‘profits in lieu of salary’ under Section 17 of the Income-tax Act, or if it falls outside the scope of taxable income.

Facts

- An assessee resigned from his employment during the Financial Year 2017-18.

- Upon leaving, he received an ex-gratia payment from his former employer, which he claimed was not taxable.

- The Assessing Officer (AO) disagreed and added the entire amount to the assessee’s income, treating it as undisclosed salary.

- The assessee challenged this by citing a precedent from the Pune Tribunal (Mahadev Vasant Dhangekar v. Asstt. CIT), which had held that a truly voluntary payment made out of appreciation is not taxable under Section 17(3).

Decision

- The High Court did not give a final ruling on whether the payment was taxable or not.

- It took cognizance of the legal precedent cited by the assessee, which supported the view that such payments could be non-taxable.

- The matter was remanded back to the Assessing Officer for a fresh (de novo) adjudication.

- The AO was directed to re-examine the issue of taxability after considering the principles laid down in the cited Tribunal order.

Key Takeaways

- Voluntary vs. Obligatory is Key: The taxability of an ex-gratia payment hinges on whether it was made voluntarily out of goodwill or as a result of a contractual or legal obligation. The latter is taxable, while the former may not be.

- Not All Post-Employment Payments are Taxable: A payment is not automatically “profit in lieu of salary” just because it comes from an ex-employer. The nature and reason for the payment are critical.

- Precedent is a Powerful Tool: The court’s decision to remand the case was directly influenced by the assessee’s reliance on a relevant judicial precedent. This underscores the importance of citing favorable case law.

- Remand for Factual Verification: By remanding the case, the court has instructed the AO to re-investigate the facts. The AO will now need to determine if the payment in this specific case was truly voluntary, similar to the facts in the precedent case.

IN THE ITAT PUNE BENCH ‘SMC’

Suhas Jagannath Kanase

v.

Income-tax officer, National e Assessment Centre, Delhi.

Vinay Bhamore, Judicial Member

and Manish Borad, Accountant Member

and Manish Borad, Accountant Member

IT Appeal No. 1638 (PUN) OF 2025

[Assessment year 2018-19]

[Assessment year 2018-19]

OCTOBER 10, 2025

Pritesh Raka and Bhavesh Lodha for the Appellant. Harshit Bari for the Respondent.

ORDER

Vinay Bhamore, Judicial Member. – This appeal filed by the assessee is directed against the order dated 19.03.2025 passed by Ld. CIT(A)/NFAC for the assessment year 2018-19.

2. There is delay of 38 days in filing of the present appeal. We are satisfied with the reasons mentioned in the affidavit for condonation that the applicant was prevented by sufficient cause for not filing the appeal within the prescribed time limit. After hearing Ld. DR, we condone the delay of 38 days and proceed to adjudicate the appeal.

3. The appellant has raised the following grounds of appeal :-

“Each of the grounds and/or sub-grounds of the appeal are independent and without prejudice to the others.

Ground No. 1:

On the facts and in the circumstances of the case, Learned Commissioner of Income Tax (Appeal) has erred addition of income of Rs. 42,11,657/- a $ undisclosed salary without providing reasonable/adequate opportunity to be heard is violation of principle of natural justice The Appellant prays that the assessment order passed in violation of principle of natural justice, be quashed. The Appellant prays that the addition of Rs. 42,11,657/- be deleted.

Ground No. 2:

Without prejudice to ground no.1 above, the facts and in the circumstances of the case, the Learned Commissioner of Income Tax (Appeal) have erred in holding that the amount of Rs.42,11,657/-received by the assessee could be treated as income under the charging section or under the section dealing with the computation of income of the assessee

The Appellant prays that the addition of Rs. 42,11,657/- be deleted.

Ground No. 3

Without prejudice to ground no.1 & 2 above, on the facts and circumstances of the case and in law the Learned Commissioner of Income Tax (Appeal) is erred on holding that the payment made voluntarily by an employer out of his own sweet will and not conditioned by any legal duty or legal obligation, whether on sympathetic reasons or otherwise is assessable to tax under the Income

Tax Act, 1961 disregarding the fact that the receipt was capital receipt and there is no provision to tax such receipt

The Appellant prays that the addition of Rs. 42,11,657/- be deleted.

Ground No. 4

On the facts and in the circumstances of the case, Learned Commissioner of Income Tax (Appeal) has erred in disallowing loss of Rs. 1,26,043/- under head of House property undisclosed salary without providing reasonable/adequate opportunity to be heard is violation of principle of natural justice by the learned assessing officer.

The Appellant prays that the disallowance of Rs. 1,26,043/- be deleted.

Ground No. 5

On the facts and in the circumstances of the case, Learned Commissioner of Income Tax (Appeal) has erred in confirming addition of Rs. 23,360/- without providing reasonable/adequate opportunity to be heard is violation of principle of natural justice by the learned assessing officer.

The Appellant prays that the addition of Rs. 23,360/- be deleted.

Ground No. 6

On the facts and in the circumstances of the case, Learned Assessing officer has erred in disallowing of Rs. 2,398/- without providing reasonable/adequate opportunity to be heard is violation of principle of natural justice

The Appellant prays that the disallowance of Rs. 2,398/- be deleted.

Ground No.7

On the facts and in the circumstances of the case, the Learned Commissioner of Income Tax (Appeal) has erred in initiating penalty proceedings under section 270A of the Act.

It is prayed that the Learned AO be directed to drop the penalty proceedings

GENERAL:

The Appellant reserves its right / craves leave to add, alter, amend and / or modify all or any of the Grounds of Appeal stated herein and to submit such statements, documents and papers as may be considered necessary to dispose off this appeal according to law and craves leave for the same.”

4. Facts of the case, in brief, are that the assessee is an individual salaried employee. The assessee has filed his return of income on 31.08.2018. The case was selected for scrutiny for the reason that salary income shown in ITR is less than the salary income appearing in Form 26AS. Statutory notices u/s 143(2) and 142(1) were issued to the assessee. As per Form 26AS, the assessee was paid a total amount of Rs.43,42,004/- by Racold Thermo Private Limited and TDS u/s 192A of the IT Act of Rs.11,47,224/- was deducted. In response to statutory notices, it was submitted by the assessee that he resigned in financial year 2017-18 and the company paid him voluntarily ex-gratia of Rs.42,15,561/- which is not taxable. After considering this reply and not being satisfied with the same, the Assessing Officer completed the assessment on a total income of Rs.43,63,458/-. The above assessed income includes an amount of Rs.42,11,657/- as undisclosed salary and Rs.1,49,403/-being house property loss disallowed and disallowance of Rs.2,398/- u/s 80TTA of the IT Act.

5. Since the assessee remained absent, Ld. CIT(A)/NFAC dismissed the appeal filed by the assessee.

6. It is the above order against which the assessee is in appeal before this Tribunal.

7. Ld. AR appearing from side of the assessee submitted before us that the order passed by Ld. CIT(A)/NFAC is unjustified. Ld. AR submitted that an identical issue came up before the coordinate bench of this Tribunal in the case of Mahadev Vasant Dhangekar v. Asstt. CIT, NFAC, Delhi 170/201 ITD 5 (Pune – Trib.) in ITA No.472/PUN/2022 order dated 03.04.2023 by the other assessee who was also in receipt of ex-gratia amount from the same company i.e. Racold Thermo Private Limited. Therefore, Ld. AR prayed before this Bench to allow the instant appeal filed by the assessee and further requested to direct the Assessing Officer to delete the addition made in the hands of the assessee.

8. Ld. DR appearing from side of the Revenue relied on the orders of the subordinate authorities and requested to confirm the same.

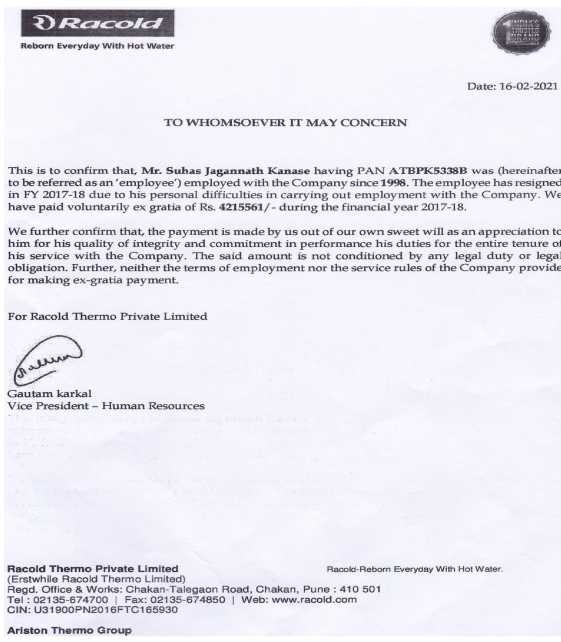

9. We have heard Ld. Counsels from both the sides and perused the material available on record including case law and copy of letter issued by Racold Thermo Private Limited, which is an additional evidence and reads as under:-

10. We further find that under identical facts & involving the similar issue a coordinate bench of this Tribunal in the case of Mahadev Vasant Dhangekar (supra) has already hold that ex-gratia payment paid by Racold Thermo Private Limited to its employee is not taxable by observing as under :-

“6. We have heard the rival submissions, considered relevant materials/documents on record, analysed the facts and circumstances in this case. The assessee had received Rs. 47,21,154/- from his erstwhile company as ex-gratia and from this amount claimed Rs. 5,00,000/- u/s 10(10C) VRS compensation/termination of Service and balance remaining amount of Rs. 47,21,154/- from ex-gratia taken as capital receipt. The ld. A.O taxed the amount u/s 17(3)(iii) of the Act by treating it as additional compensation received by the assessee from his employer as profit in lieu of salary u/s 17(3)(iii) of the Act. Section 17(3)(iii) of the Act provides as follows:

“17. For the purposes of sections 15 and 16 of this section

(1) ——–

(3) “profits in lieu of salary” includes

———

(iii) any amount due to or received, whether in lump sum or otherwise, by any assessee from any person

(A) before his joining any employment with that person or

(B) after cessation of his employment with that person.

Therefore, as per the aforesaid provision, it is clearly evident that any payment received whether in lump sum or otherwise by an assessee from any person after cessation of his employment with that person is also considered as profit in lieu of salary and is to be brought to tax accordingly being defined inclusively as per the Act. The ld. A.O has invoked this provision and has brought to tax the disputed amount. The NFAC while upholding the addition has discussed that the amount received by the assessee is part and parcel of Form No. 16 issued to him and that the TDS has also been paid in respect of the said amount and that further the letter which was produced by the assessee was signed by Vice President (Human Resources) only surfaced once the scrutiny started and notices u/s 143(2) and 143(1) were issued to the assessee. On the other hand, it is contended by the assessee that the payment has been made voluntarily by the employer out of his own sweet will and not bound by any or condition by any legal duty or legal obligations which are on sympathetic reason or otherwise. Further, neither the terms of employment nor the service rules of the employer company provides for making ex-gratia payment. Thus, the said amount is totally voluntary and it is not compensation.

7. Admittedly, the amount was received by the assessee after cessation of his employment with the employer company. In the normal course, section 17(3)(iii) of the Act would apply and the payment would be covered within the definition of profit in lieu of salary as brought out by the department. However, in this case, the letter which has been issued by the employer clearly stated that the payment of the amount has been made voluntarily to the assessee and is not the compensation. This letter has not been doubted by the department. Neither, the ld. A.O nor the NFAC conducted any independent inquiry regarding the veracity of this letter and none of the authorities have held this letter issued by the employer to the assessee as bogus. Without establishing the letter as non-genuine or without examining the sanctity of the payment made simply invoking the provisions of the Act for making addition is not appropriate for a quasi-judicial authority. The revenue should have verified and examined the genuineness of the letter which was produced by the assessee wherein the employer had stated that it is a voluntary payment made as per appreciation for the employee without entering into this exercise simply invoking the provision of the Act is not legally tenable and takes the colour of arbitrariness. The ld. D.R could not produce any documents/evidences on record to show that the payment received from the employer nor voluntary in nature or that the payment was coupled with some legal obligation on the part of the employer to pay to the employee. No such facts were produced before us. We are of the considered view, therefore, in this case, when the employer itself stated that the payment has been made voluntarily by them out of appreciation for the employee thus falls outside the rigours of section 17(3)(iii) of the Act. In view thereof, we set aside the order of the NFAC and direct the ld. A.O to delete the addition from the hands of the assessee. The grounds of appeal of the assessee are allowed.

8. In the result, appeal of the assessee is allowed.”

11. Respectfully following the above decision passed in the case of Mahadev Vasant Dhangekar (supra), we deem it appropriate to set-aside the impugned order passed by Ld. CIT(A)/NFAC & remand the matter back to the file of Jurisdictional Assessing Officer to decide the issue of taxability of ex-gratia payment afresh in the light of letter issued by Racold Thermo Private Limited (employer of the assessee) and also in the light of decision passed by coordinate bench of this Tribunal in the case of Mahadev Vasant Dhangekar (supra) after providing reasonable opportunity of hearing to the assessee. Thus, the grounds no.1, 2 & 3 raised by the assessee in this regard are allowed for statistical purposes.

12. With regard to ground no.4, 5 & 6 involving the issue of house property loss and deduction u/s 80TTA of the IT Act, we remit the matter back to the file of the Assessing Officer to decide the issue afresh after providing reasonable opportunity of hearing to the assessee. Accordingly, ground no.4, 5 & 6 are allowed for statistical purposes.

13. The ground no.7 challenging the initiation of penalty u/s 270A of the IT Act is premature hence dismissed.

14. In the result, the appeal filed by the assessee is allowed for statistical purposes.