GST Demand for Pre-CIRP Period Quashed; IBC “Clean Slate” Extinguishes Past Dues

Issue

Whether the GST Department can validly raise a demand under Section 73 for a period prior to the approval of a Resolution Plan (FY 2017-18), once the National Company Law Tribunal (NCLT) has approved the plan under the Insolvency and Bankruptcy Code (IBC) which extinguishes past liabilities.

Facts

-

Petitioner: A company engaged in warehousing and logistics services.

-

The Event: The company underwent the Corporate Insolvency Resolution Process (CIRP). The NCLT, Chennai approved the Resolution Plan with an “Effective Date” of 11.01.2023.

-

The Plan Terms: The approved plan explicitly recorded the extinction of all indirect tax dues and the termination of legal proceedings for periods prior to the effective date.

-

The Conflict: Despite the binding NCLT order, the GST authorities issued a show cause notice and passed a demand order for FY 2017-18 (a period falling well before the plan’s effective date).

-

The Appeal: The department’s demand was confirmed in the initial appeal, compelling the petitioner to approach the High Court.

Decision

-

Binding Effect (Section 31 IBC): The High Court reiterated the settled legal principle (notably from the Supreme Court’s Ghanashyam Mishra judgment) that once a Resolution Plan is approved under Section 31 of the IBC, it becomes binding on all stakeholders, including the Central and State Governments.

-

Clean Slate Doctrine: Consequently, all claims that were not part of the approved Resolution Plan stand extinguished. No person (including Tax Authorities) is entitled to initiate or continue any proceedings regarding dues for the period prior to the plan’s approval.

-

Jurisdictional Bar: Since the demand pertained to FY 2017-18 (pre-CIRP), the Department had no jurisdiction to raise it after the plan was approved.

-

Ruling: The impugned orders (demand and appellate order) were quashed. The petition was allowed in favour of the assessee.

Key Takeaways

Operational Creditor Status: Under the IBC, Tax authorities are classified as “Operational Creditors.” If they fail to file their claim with the Resolution Professional (RP) during the CIRP, or if their claim is settled at a haircut (reduced value) in the plan, the right to recover the balance is lost forever.

Defense against Legacy Notices: If you represent a company that has been taken over through NCLT, keep the Resolution Plan handy. Any notice received for a period prior to the takeover date can be immediately challenged and quashed using this precedent.

CM APPL. No. 72086 of 2025

| (i) | Firstly, separate Forms DRC-07 have not been issued for different financial years. |

| (ii) | Secondly, Section 74 of the Central Goods and Services Tax Act, 2017 (hereinafter, ‘CGST Act’) could not have been invoked as the Show Cause Notice (hereinafter, ‘SCN’) dated 26th July, 2025 was itself based on GSTR-3B, GSTR-9 and the balance sheet which were all available on the portal itself. |

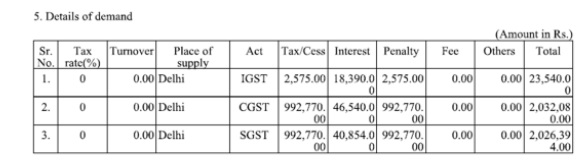

| Audit Paragraph No. | Head | Amount |

| 1. | Short payment of tax due to reconciliation of GSTR-3B, GSTR-9 and Balance Sheet. | Rs.17,44,603/- |

| 2. | Excess availment of Input Tax Credit as shown in GSTR-2A and GSTR-3B during the Financial Year 201920 & 2020-21. | Rs.36,125/- |

| 3. | Non-payment of tax on other income. | 10,636/- |

| 4. | Interest on late payment of tax due to late filing of GSTR-3B. | 5,686/- |

| 5. | Non-payment of interest on payments made to the suppliers beyond 180 days. | 1,00,098/- |

| 6. | Reversal of Input Tax Credit in respect of blocked credit as per Section 17(5) of the CGST Act, 2017 during the Financial Year 2018-19. | 1,75,226/- |

| 7. | Non payment of tax on profit on sale of fixed assets shown in books of accounts. | 21,524/-, 1,05,784/-and 19,88,114/- |