ORDER

Dr. Manish Borad, Accountant Member.- The captioned appeal at the instance of assessee pertaining to A.Y. 2015-16 is directed against the order dated 20.12.2019 framed by CIT(A), Pune-1 arising out of Assessment Order dated 26.12.2017 passed u/s.143(3) of the Income Tax Act, 1961.

2. Assessee has raised following grounds of appeal :

“The grounds hereinafter taken by the Appellant are without prejudice to one another

1:0 Re.: Disallowance of depreciation on ‘Goodwill’ u/s. 32 of the Income-tax Act, 1961:

1:1 The Commissioner of Income-tax (Appeals) has erred in confirming the disallowance of depreciation of Rs.1,49,30,000/- on ‘Goodwill’ of Rs.5,97,20,000/ – u/ s. 32 of the Income-tax Act, 1961.

1:2 The Appellant submits that considering the facts and circumstances of its case and the law prevailing on the subject, depreciation is allowable on goodwill and the stand taken by the Assessing Officer is illegal, incorrect, erroneous and misconceived and not in accordance with law and the Commissioner of Income-tax (Appeals) ought to have held as such.

1:3 The Appellant submits that the Assessing Officer be directed to delete the disallowance made by him and to re-compute its total income accordingly.

2:0 Re.: Levying of Buy Back Tax u/s. 1150A of the Income-tax Act, 1961:

2:1 The Commissioner of Income-tax (Appeals) has erred confirming the levy of Buy Back Tax u/s.115QA of the Income-tax Act, 1961 of Rs.99,57,776/-.

2:2 The Appellant submits that considering the facts and circumstances of its case and the law prevailing on the subject, tax u/s. 115QA of the Income-tax Act, 1961 is not leviable in the instant case, and the action of the Assessing Officer is illegal, incorrect, erroneous and misconceived and the Commissioner of Income-tax (Appeals) ought to have held as such.

2:3 The Appellant submits that the Assessing Officer be directed to delete the erroneous levy of Buy Back Tax u/ s.115QA of the Incometax Act, 1961 of Rs.99,57,776/-levied by him and to re-compute its tax liability accordingly.

3:0 Re.: Deduction in respect of ‘Education Cess on income-tax’ and ‘secondary and higher education cess on income-tax’ (collectively referred to as ‘education. cess in income-tax’) payable for the year under consideration, while computing the total income of the Appellant:

3:1 The Assessing Officer has erred in not allowing a deduction for the ‘education cess on income-tax payable for the year under consideration.

3:2 The assessee submits that considering the facts and circumstances of its case and the law prevailing on the subject, education cess on income-tax’ for the year under consideration, though not claimed as a deduction by the assessee while filing its return of income for the year under consideration, ought to have been allowed while assessing its income for the year under consideration.

3:3 The assessee submits that the Assessing Officer be directed to re-compute its total income and tax thereon after allowing deduction for ‘education cess on income-tax’.

4:0 Re: General

4:1 The Appellant craves leave to add, alter, amend, substitute and/or modify in any manner whatsoever all or any of the foregoing grounds of appeal at or before the hearing of the appeal.”

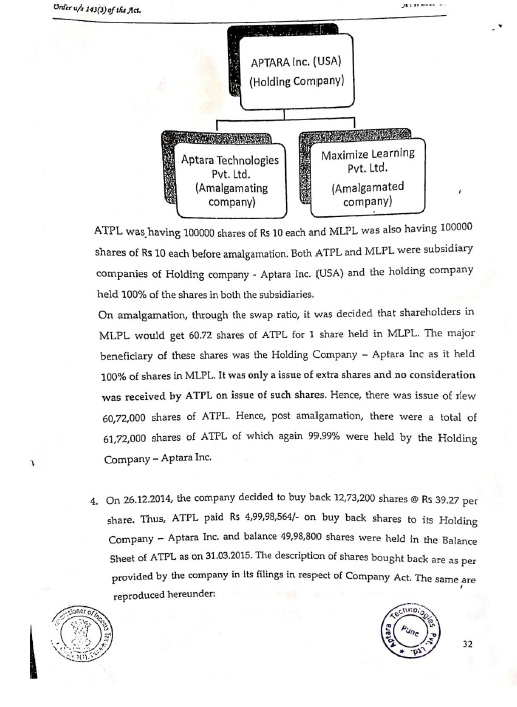

3. Brief facts of the case are that the assessee is a Private Limited Company engaged in the field of providing IT enabled conversion services which include content conversion and management, e-learning solutions, imaging, graphic arts and other related services. The assessee Aptara Technologies Pvt. Ltd. (in short ‘APTL’) is a 100% subsidiary of Aptara Inc. USA which holds 100000 Equity shares of face value of Rs.10/-each. Along with the assessee, there is another subsidiary company namely Maximise Learning Pvt. Ltd. (in short ‘MLPL’) which is also 100% owned by the holding company Aptara Inc. USA.

4. The assessee filed its original return of income u/s.139(1) of the Act on 25.11.2015 declaring income of Rs.1,66,65,240/-. After the regular processing of return u/s.143(1)(a) of the Act, case of the assessee selected for scrutiny followed by serving of valid notices u/s.143(2) and 142(1) of the Act. During the course of assessment proceedings, ld. Assessing Officer observed that there is an amalgamation in the nature of merger with MLPL (Transferor company) and Assessee-ATPL (Transferee company). Hon’ble Bombay High Court vide order dated 19.09.2014 has sanctioned the scheme of amalgamation effective from 01.04.2014 (Appointed date) u/s.391 to 394 of the Companies Act which has been subsequently filed with the Registrar of Companies on 24.11.2014. As per the scheme of amalgamation, the shareholders of MLPL got 60.72 Equity shares (face value of Rs.10/- each) in ATPL for every1 Equity share held by the shareholders in MLPL. Ld. Assessing Officer has further observed that as per the merger note through which net assets of the MLPL have been taken over by ATPL, consideration of Rs.6,07,20,000/- is shown to be due to the shareholder of amalgamating company. Against this outstanding, ATPL has issued 60,72,000 Equity shares to the existing shareholder of MLPL. After the reduction of the face value of the share capital of MLPL, remaining amount of consideration is said to be towards Goodwill amounting to Rs.5,97,20,000/- and this Goodwill has been shown as Intangible asset in the books of Transferee company and depreciation @ 25% has been claimed thereon. Ld. Assessing Officer asked the assessee to state that why the difference amount has not been reduced from the Capital Reserve rather than creating it as an Intangible asset, i.e. Goodwill. Ld. Assessing Officer also referred to the Accounting Standard-14 issued by the Institute of Chartered Accountants of India (ICAI) applicable for treatment of Reserves on amalgamation. Ld. Assessing Officer also observed that this creation of Goodwill is in violation of Explanation 7 to section 43(1) of the Act as per which in a scheme of amalgamation any capital asset if transferred from amalgamating company to amalgamated company and the amalgamated company is an Indian company, the actual cost of the transferred capital asset to the amalgamated company shall be taken to be the same as if it would have been if the amalgamating company it has continued to hold the capital asset for the purposes of its own business. However, the assessee in its reply submitted that the said treatment of creation of Goodwill is in the light of judgment of Hon’ble Apex Court in the case of CIT v. Smifs Securities Ltd. ITR 302 (SC). Assessee also submitted that Hon’ble Bombay High Court in approving the scheme has given reference to the Affidavit of the Regional Director who has stated that the deficit if any arising in the scheme shall be debited to Goodwill account of the Transferee company. Thereafter, ld. Assessing Officer on due consideration of the submissions filed by the assessee has taken note that Hon’ble High Court in its para 10 has observed that so far as Affidavit of Regional Director is concerned, the petitioner companies are bound to comply with all applicable provisions of the Income Tax Act and all tax issues arising out of scheme will be met and answered in accordance with law. Ld. Assessing Officer has also taken note that ATPL and MLPL are 100% subsidiaries of Aptara Inc. USA and that MLPL is a new company not even carrying out the name of Aptara Inc. USA but when the MLPL merged with ATPL shareholders of MLPL received more shares in swap ratio which shows that valuation was made to suit the needs of the amalgamation. Further, ld. Assessing Officer referring to another transaction carried out during the year regarding buyback of 12,73,299 Equity shares by the assessee company for a consideration of Rs.4,99,98,564/- has observed that the purpose of creation of the alleged Goodwill amount is to increase the Fair Market Value of the Equity share. Ld. Assessing Officer further observed that there is no specific advantage which the amalgamating company derived from the merger and hence the claim of Goodwill and depreciation claimed thereon are not sustainable and cannot be allowed and that the company has used colourable device of amalgamation to claim Goodwill which never existed. Ld. Assessing Officer has also observed that since merger was of the two subsidiary companies and no advantage has been created on amalgamation, there is no question of Goodwill. Amortisation claimed on the Goodwill needs to be added back to the income of the company and also company will not be allowed to capitalize the Goodwill in future and therefore cannot claim any depreciation benefit in future. Accordingly, depreciation claimed on Goodwill at Rs.1,49,30,000/- has been disallowed.

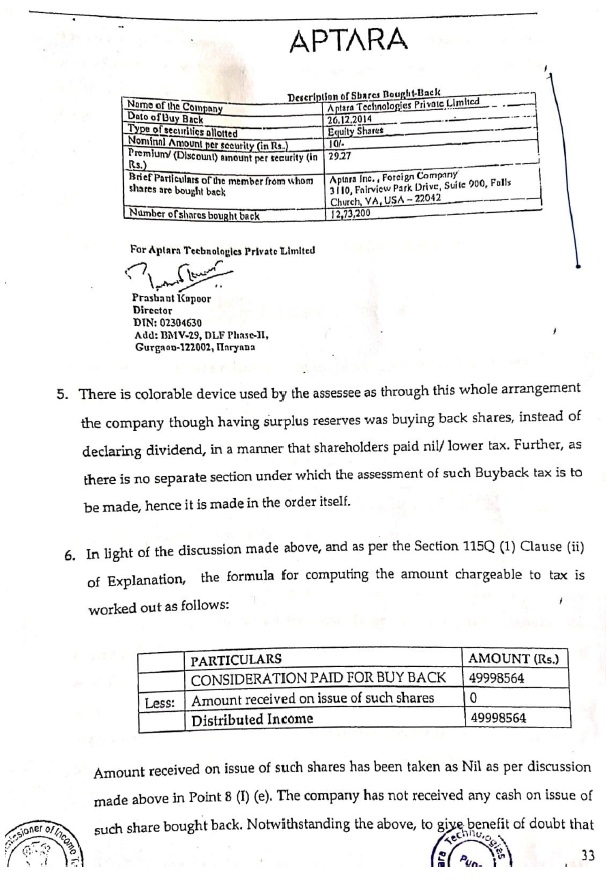

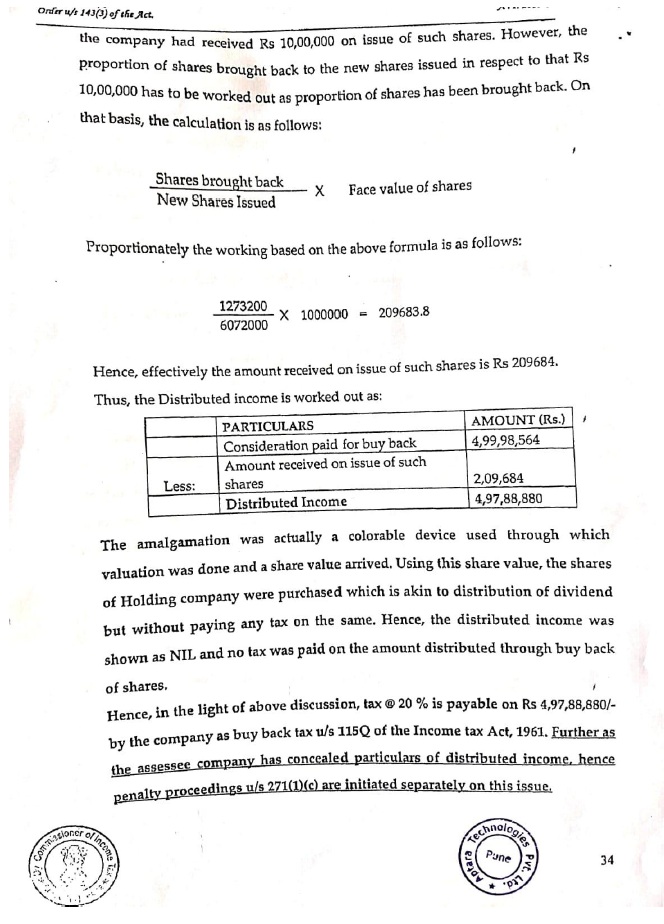

5. Next issue dealt by the Assessing Officer is regarding taxation of buyback of shares. Ld. Assessing Officer observed that Capital Reserve has been credited on the Liability side of the Balance sheet at Rs.1,27,32,000/- which when asked was stated by the assessee that it is a Capital Redemption by the company, as the assessee has brought back 12,73,200 Equity shares at a face value of Rs.10/- and the said shares have been brought back @39.27 per share thereby making payment of agreed value of buyback shares at Rs.4,99,98,564/- to Aptara Inc. USA. Ld. Assessing Officer discussed the provisions of section 115QA inserted by the Finance Act, 2013 as per which buyback of shares of unlisted domestic companies is made taxable in the hands of a company and as per section 115QA of the Act the distributed income, i.e. consideration paid by company on buyback of shares as reduced by the amount which was received by the company for issue of such shares is chargeable to tax. However, in the case of assessee the Fair Market Value as per Discounted Cash Flow (DCF) method is calculated @39.76 per share and since the buyback was made @39.27 per share, the assessee has claimed that against 39.27 price of Equity share for buyback, the assessee deserves deduction of the Equity share price @39.76 resulting into Nil taxation as per section 115QA of the Act. However, ld. Assessing Officer was not satisfied with these submissions treating it to be a colourable transaction just to avoid taxation u/s.115QA of the Act observed that the amount received by the assessee on issue of such shares which have been buyback was only Rs.2,09,684/- and therefore the distributed income is Rs.4,98,88,880/- which is liable to be taxed @20% u/s.115QA of the Act and for arriving at this conclusion the observation of ld. Assessing Officer reads as under :

6. Accordingly, Id. Assessing Officer concluded the assessment firstly disallowing the depreciation of Goodwill at Rs.1,49,30,000/, thereby assessing income at Rs.3,15,95,240/-, secondly computing tax liability u/s.115QA of the Act at Rs.99,57,776/- being 20% of distributed income of Rs.4,97,88,880/- and thirdly held that the creation of Goodwill as Intangible asset by the assessee in its books of account is mainly a colourable device and the said creation of Goodwill is not in accordance with law and that the assessee will not be eligible to claim depreciation on such Goodwill in the future years as no intangible asset in the form of Goodwill has been created in the scheme of Amalgamation.

7. Aggrieved assessee preferred appeal before ld.CIT(A) and again made detailed submissions in support of its contention that impugned addition/action of the Assessing Officer is uncalled for. Ld.CIT(A) has dealt with the arguments of the assessee at length and finally concluded that the creation of Goodwill is a colourable device so as to increase the price of Equity share of the company and thereafter pass on the consideration to the Holding Company for the buyback of Equity shares and also that the transaction has taken place between the related parties just in order to claim depreciation on the Goodwill so created and also to transfer the funds to the Holding Company without paying the tax u/s.115QA of the Act @20% payable on buyback of Equity shares.

8. Aggrieved assessee is now in appeal before this Tribunal raising the grounds extracted above.

9. Ld. Senior Counsel for the assessee Mr. Percy Pardiwalla representing the assessee first made reference to the following written submissions which have been filed before ld.CIT(A) and before this Tribunal :

“A. Facts of the Case

1. The Appellant is a private limited company engaged in the business of providing IT enabled conversion services, including elearning solutions, imaging, graphic arts and other related services. It is a wholly owned subsidiary of Aptara Inc., a company incorporated in USA. The Appellant filed its return of income for Assessment Year 2015-16 on 25 November 2015, declaring total income of Rs. 1,66,65,240. The computation of income is enclosed as Annexure-1 of Paper book-I.

2. The return was selected for scrutiny under CASS and a notice u/ s 143(2) of the Income-tax Act, 1961 (the Act) was issued to the assessee. Detailed questionnaires were issued during the course of assessment, which were duly responded to by the Appellant. Upon considering the submissions made by the Appellant, an order dated 26 December 2017 was passed u/s 143(3) of the Act, making the following adjustments to the income returned by the Appellant,

(a) In relation to the tax on income of the Appellant, disallowing the Appellants claim for depreciation on goodwill,

(b) In relation to shares bought back by the Appellant, taxing the consideration paid on buyback u/ s 115QA of the Act

B. Dis-allowance of depreciation on goodwill

B.1 Facts relevant to dis-allowance of depreciation

3. The said goodwill arose due to the amalgamation of Maximize Learning Private Limited (MLPL) with the Appellant. MLPL was a wholly owned subsidiary of Aptara Inc., USA. While the Appellant was engaged in the business of publishing services, which entails digitisation of content for third parties, MLPL was engaged in providing e-learning services, rendering services solely to Aptara Inc. The activities of the Appellant and MLPL can be explained with the following example.

4. The Finance Act amends the Income-tax Act annually. Physical copy of the Act would have to be updated with the amendments. If the Appellant is provided with a copy of the old IT Act and the amendments sough to be made, the Appellant would prepare a printable version of the amended IT Act. The Appellant was thus engaged in providing digitalisation of contents to its customers. Its customers were un-related third parties. On the other hand, if the Ministry of Finance wishes to prepare a learning module for educating tax payers to file their own income tax return, Aptara Inc would be in a position to provide the required services. Aptara Inc. would understand the IT Act, the return forms, identify the requirements of the tax payers, and prepare a video module with audio and sub-titles, navigating the whole process of filing of return by a tax payer. MLPL would provide services to Aptara Inc. in executing the assignment for the Ministry of Revenue. MLPL was undertaking assignments solely for Aptara Inc. alone.

5. The sector in which the Appellant was operating was facing significant competition from electronic medium and hence, to stay competitive in the market, the Appellant had to diverge into web based medium. Working closely with Aptara Inc. on complicated assignments, MLPL had gained significant technical expertise in providing quality e-learning services to the latter’s customers in the USA. Aptara Inc. therefore wanted MLPL to start working independently. However, MLPL did not have any expertise in marketing its products in India. In order to put together the marketing expertise of the Appellant and the technical expertise of MLPL, both of which hitherto were operating in silos, the shareholders decided to merge ML.PL into the Appellant.

6. An application was filed before the Hon’ble High Court of Bombay, to seek its approval for the amalgamation. The amalgamation was approved by the Hon’ble High Court of Bombay vide order dated 19 September 2014, w.e.f. 1 April 2014. A copy of the order of the Hon’ble Bombay High court approving the scheme of amalgamation is enclosed as Annexure- 6 of Paperbook -1. The amalgamation was projected to be beneficial to the Appellant.

7. As per the scheme of amalgamation, shareholders of MLPL got 60.72 shares in the Appellant for every share held in MLPL. The share capital of MLPL consisted of 1 lakh equity shares of Rs. 10 each, hence, the total purchase consideration for MLPL was valued at Rs. 6,07,20,000 (page 171/165 of Paper Book I). After considering the value of the assets and liabilities taken over by the Appellant from MLPL, there existed an excess of purchase consideration paid over the Net Worth of MLPL, amounting to Rs. 5,97,20,000.

8. The Appellant, in its proposed scheme of amalgamation, had chosen to follow the ‘Pooling of Interest’ method as prescribed in Accounting Standard (AS) 14 “Accounting for Amalgamations’ (para 14.2 at page 152 of Paper Book 1). Pooling of Interests Method is generally applied where object of amalgamation is as if the separate businesses of the amalgamating companies were intended to be continued by the transferee company. However, on the objections of the Regional Director of the Ministry of Corporate Affairs (para 8 at page 131 of Paper Book 1), the Hon’ble High Court approved the scheme of amalgamation subject, inter alia, to the condition that the Transferee Company would transfer the surplus or deficit arising out of the scheme to the Capital Reserve Account or Goodwill Account, respectively (para 9 at page 132 of Paper Book I). Bound by the order of the Hon’ble High Court, the Appellant recognized the excess consideration paid as Goodwill in its books of accounts, and in its return of income, claimed depreciation u/ s 32. of the Act on the said amount.

9. However, disregarding the claims of the Appellant, the learned Assessing Officer (the Ld. AO) denied the depreciation claim of the Appellant on the following grounds,

(a) Appellant had failed to follow AS 14 by recognizing the excess consideration as goodwill.

(b) The amount recognized as goodwill was just a balancing figure, and does not represent any specific asset, rights or advantages gained by the Appellant. Hence, the amount recognized as goodwill was no asset at all.

(c) Explanation 7 to Section 43(1) provides that the assets acquired under a scheme of amalgamation have to be recorded at the value at which they stood in the books of the amalgamating company. As goodwill was not recorded in the books of MLPL, the cost of acquisition in the hands of the Appellant shall also be Nil.

10. The Appellant’s submissions on each of these contentions of the AO are given below

B.2. On the facts and circumstances of the case, the Ld. AO erred in disallowing the depreciation claimed on goodwill, on the basis that the Appellant has not followed AS-14,

11. The Ld. AO has held that the Appellant is in violation of the provisions of AS 14, due to the fact that despite following the pooling of interest method, the Appellant has still recognised the excess of purchase consideration paid as Goodwill, and not adjusted the same in the Reserves of the amalgamated company. For holding so, the AO has raised the following two objections,

(a) The Ld. AO has noted that the Statutory Auditor of the Appellant had provided a Qualifying Remark regarding the ‘Accounting Treatment done on Amalgamation’.

(b) Referring to Para 16 & 35 of AS-14, the AO has held that post amalgamation, the Appellant had enough reserves to adjust the excess FMV from the combined reserves, and since the Appellant has not done so and recognized the excess amount as Goodwill, it is in violation of AS 14.

12. It is submitted that the Ld. AO has grossly erred in facts as well as in law. Firstly, the Auditors of the Appellant have issued an Unqualified Audit Report. The Ld. AO has mistaken the Notes to Financial Accounts prepared by the Management of the Appellant as the Audit Report issued by the Statutory Auditors. The Financial Statements along with the Notes to Financial Statements and the Independent Auditors’ Unqualified Audit Report have been enclosed as Annexure-2 of Paper Book 1.

13. Further, the Ld. AO has chosen to read AS-14 in bits and pieces and has disregarded Para 23 of the AS. Accounting Standard 14 has been enclosed as Annexure-1 of Paper Book -II. The said Para is reproduced below:

“Treatment of Reserves Specified in A Scheme of Amalgamation

23. The scheme of amalgamation sanctioned under the provisions of the Companies Act, 1956 or any other statute may prescribe the treatment to be given to the reserves of the transferor company after its amalgamation. Where the treatment is so prescribed, the same is followed. In some cases, the scheme of amalgamation sanctioned under a statute may prescribe a different treatment to be given to the reserves of the transferor company after amalgamation as compared to the requirements of this Standard that would have been followed had no treatment been prescribed by the scheme. In such cases, the following disclosures are made in the first financial statements following the amalgamation:

(a) A description of the accounting treatment given to the reserves and the reasons for following the treatment different from that prescribed in this Standard.

(b) Deviations in the accounting treatment given to the reserves as prescribed by the scheme of amalgamation sanctioned under the statute as compared to the requirements of this Standard that would have been followed had no treatment been prescribed by the scheme.

(c) The financial effect, if any, arising due to such deviation.”

14. Thus, where a specific treatment for reserves is specified in the scheme of amalgamation, the AS stipulates that the treatment as specified in the scheme shall have to be followed, and appropriate disclosures shall be made regarding the same. Para 23 does not apply to any scheme of amalgamation approved under the Companies Act, 2013. However, the scheme of amalgamation of the Appellant has been approved under the Companies Act, 1956 and hence the treatment of reserves specified in the scheme has to be followed by the Appellant. It is the disclosures made by the Appellant in the Notes to Financial Statements that the Ld. AO has misconstrued as Qualifying Remarks of the Auditor in the Audit Report, leading him to incorrectly believe that the Appellant has not followed AS-14.

15. Thus, the Appellant has followed AS-14 in its entirety, and the accounting treatment of the Appellant cannot be faulted.

B.3. On the facts and circumstances of the case, the Ld. AO erred in disallowing the depreciation claimed on goodwill by holding that the value of goodwill cannot merely be a balancing figure.

16. The Ld. AO has noted in his order that there are no specific advantages accruing to ATPL from the amalgamation. He states that as per the High Court Order, only general advantages are derived from the amalgamation, consequent to the fact that the both the entities are subsidiaries of a US Company. Thus, a question arises as to what constitutes goodwill, i.e., what is the definition of goodwill.

17. The term, goodwill, though finds mention in some sections in the IT Act like Section 55(2)(a) of the IT Act, is not defined in the Act. The Oxford Concise Dictionary defines goodwill as the established reputation of a business regarded as a quantifiable asset.

18. In IRC v. Muller Co’s Margarin [1901] AC 217 elaborated the meaning of ‘goodwill in the following words:

“What is goodwill? It is a thing very easy to describe, very difficult to define. It is the benefit or advantage of the good name, reputation and connection of a business. It is the attractive force which brings in customers. It is the one thing which distinguishes an old-established business from a new business at its first start. If there is one common attribute to all cases of goodwill, it is the attribute of a locality. For goodwill has no independent existence. It cannot subsist by itself. It must be attached to the business. Destroy the business, the goodwill perishes with it, though elements may remain which may perhaps be gathered up and revived again,

19. The Supreme Court in S. C. Cambatta v. Commissioner of Excess Profits Tax [1961] 2

SCR 805 explained the meaning of ‘goodwill’ in the following words:

It will thus be seen that the goodwill of a business depends on a variety of circumstances or a combination of them. The location, the service, the standing of business, the honesty of those who run it and lack of competition and many other factors go individual or together to make up goodwill’

20. Explanation 3(b) to Section 32 defines block of assets to mean tangible and intangible assets. Intangible assets include know-how, patents, copyrights, trademarks, licenses, franchises or any other business or commercial rights of similar nature. Goodwill is not separately mentioned as an asset class under intangible assets eligible for depreciation. In Areva T&D India Lid v. DCIT (Del), the expression any other business or commercial rights of similar nature has been interpreted by the Hon’ble High Court to include business contracts, business records, business information, skilled employees etc. The Hon’ble High Court applied the principles of ejusdem generis to include other intangible assets, apart from the six assets that are mentioned in Explanation 3(b) to Section 32 of the IT Act.

21. The Income-tax Tribunal in A.P.Paper Mills Limited v. ACIT [2010] 128 TTJ 496 (Hyd) held that goodwill has no independent existence and that there cannot be any sale of goodwill separately from the sale of business and that goodwill cannot subsist by itself. In the facts of that case, the Hon’ble ITAT highlighted the following factors to conclude that goodwill had existed and that it was entitled for depreciation:

a. the market share of assessee company has increased substantially;

b. the brands of the amalgamating company have become the brands of the assessee;

c. the assessee got the loyal domestic customers of the amalgamating company;

d. the assessee got various licenses and registrations on account of amalgamation like factory license, boiler operating license, pollution disposal permission, VAT registration, excise registration, export license and also got advantages due to proximity of location;

e. the assessee got various infrastructural advantages like captive power plant of 5.74 MW, coal fired boiler, DM plant, effluent treatment plant, and also benefit of sales-tax deferment loan; and

f. No gestation/ stabilization period was required when compared to new green field or brown field venture.

22. The Supreme Court in CIT v. Smifs Securities Limited (SC)/CIT v. Smifs Securities Ltd. ITR 302 (SC)/[2012] 348 ITR 302 (SC) has also specifically held that goodwill will constitute intangible asset within the meaning of Explanation 3(b) to Section 32 of the IT Act. The decision in Smifs Securities Limited (supra) was relied on by the Hon’ble Gujarat High Court in PCIT v. Swastik Industries (Guj). Similar view was taken in CIT v. Manipal Universal Learning P Limited [2013] 359 ITR 369 (Kar).

23. Over the past four years, the Appellant, post amalgamation, has achieved significant synergies in business, which has helped increase its gross revenue. Detailed in the Table below is the comparison between the projected v. the actual gross revenues of the Appellant. The projections are based on the Valuation Report obtained by the Appellant from a Chartered Accountant. The Valuation report is enclosed as Annexure-7 in Paper Book 1.

(figures in Lakhs)

| Financial Year Ended 31 March |

Gross Revenue |

| Projected |

Actual |

| 2015 |

818.24 |

1159.85 |

| 2016 |

847.36 |

920.82 |

| 2017 |

884.91 |

792.14 |

| 2018 |

924.35 |

1007.36 |

24. Every year, other than 2017, the merged entity has surpassed the projected revenue it would generate, which in itself is proof of existence of significant synergies and operations. For the FY ended 31 March 2017, there was a downturn in the entire industry, and hence the aberration in the revenues of the Appellant is seen. Comparative turnover of MLPL and the Appellant, pre and postmerger is given as Exhibit A herewith.

25. Further, the Appellant also took on its payrolls the employees of MLPL, who were highly skilled in the field of e-learning. MLPL had cleared a strong pool of talented free-lancing professionals who were in a position to provide quality development services at a very competitive price. Development of e-learning portal required the following expertise, and a team of professional

(a) Designing & Developing Content experiences & providing solutions to support the acquisition of new knowledge & skill

(b) Graphic Art & Designing, assembling images, Typography or Motion Graphics

(c) Translation, Localization & Voice over

(d) Applying principles & practices of software Quality Assurance.

(e) Images Purchase

Production of e-learning Modules

(g) Process breaking in steps to improve Quality & time Deliver

(h) Programmer specialized in development of web applications using client server model, Typically HTML, CSS, Java, PHP, Dotnet, Etc

(i) Resourcing

(j) Web graphic Design, Authoring, Standardizing Code & search engine optimization.

26. MLPL, over the period of his existence in India, had a pool of 53 resources persons who were highly skilled and training in their specialization (Exhibit B herewith). MLPL took more than half a decade to test, train and create a pool of vendor resources, which were assigned to the Appellant on amalgamation. These personnel were taken on board to also provide training to the existing employees of the Appellant, so as to increase their skill base and provide additional support in the field of e-learning, apart from their existing skills in publishing and digitization of content. As a result, the Appellant was able to tap in new customers to add on to its customer list every year.

27. With its experience in assisting Aptara Inc. in servicing overseas customers, MLPL had gained access to standard templates that would be required in the field of business. These templates, if developed on standalone basis, would have consumed significant time and efforts at the end of the Appellant. These standard templates enabled the Appellant to provide before committed time services, and thereby gaining their confidence in the otherwise new market. This also ensured that the Appellant received repeated orders from competitors, seeing the success of the initial customer. This enabled the Appellant to showcase that it had the technical expertise and skill of a company operating in the field for decades, though the entire business segment was newly established.

28. The Appellant has gained significantly from addition of new customers in its e-learning division. Post amalgamation, the Appellant has added the following customers, in its e-learning segment which has led to the generation of substantial revenue. The Appellant wishes to highlight that it was not operating in e-learning segment before its amalgamation and that it started rendering elearning services to third party customers using the resources of MLPL.

(Revenue per customer in e-learning business segment, post amalgamation)

| Customer Name (E-learning) |

2014-15 |

2015-16 |

2016-17 |

2017-18 |

| Amdocs Development Centre India Pvt. Ltd. |

– |

11,48,528 |

– |

11,48,528 |

| American Express |

3,35,197 |

10,17,019 |

72,000 |

14,24,216 |

| Apollo Munich Health Insurance Co. LTD. |

2,83,469 |

1,94,220 |

– |

4,77,689 |

| Aricent Technologies (holding) Ltd. |

– |

1,00,929 |

– |

1,00,929 |

| Jaypee Brothers |

13,48,320 |

13,56,192 |

6,72,194 |

33,76,706 |

| Philips India Ltd. |

1,00,91,597 |

2,03,37,615 |

1,20,37,096 |

4,24,66,307 |

| Reliance Corporate IT Park Ltd. |

2,00,58,733 |

1,39,29,068 |

3,993 |

3,39,91,794 |

| TATA Sky Ltd. |

2,93,23,045 |

3,27,979 |

– |

2,96,51,024 |

| Grand Total |

6,14,40,362 |

3,84,11,550 |

1,27,85,282 |

11,26,37,194 |

29. Shortly put, the Appellant gained significantly from the amalgamation, in the form of highly skilled employees, increased talent pool, significantly increased revenue, increased client and customer base, additional skills imparted to existing employees, standard templates for providing basic services, etc. apart from the general synergies of amalgamation such as reduced costs, simpler management structure, etc. The observations of the Ld. AO are therefore completely devoid of merit.

B.4. On the facts and circumstances of the case, the Ld. AO erred in disallowing the depreciation claimed on goodwill by alleging violation of Explanation 7 to Section 43(1)

30. The Ld. AO has also disallowed the claim of depreciation on goodwill on the basis that the actual cost of goodwill should be taken as Nil, following Explanation 7 to Section 43(1) of the Act.

31. Section 43(1) of the IT Act defines ‘actual cost’. Actual cost assumes relevance as depreciation in the first year is allowed on the actual cost to the assessee. Explanation 7 to the said section provides that in case of an amalgamation where the amalgamated company is an Indian company, the actual cost of the transferred capital asset to the amalgamated company shall be taken to be the same as it would have been if the amalgamating company had continued to hold the capital asset for the purposes of its own business.

32. Section 43(6) of the IT Act defines the term ‘written down value’. Written down value assumes relevance, in claiming depreciation on a year on year basis at prescribed rates. Explanation 2 to the said section provides that in case of an amalgamation where the amalgamated company is an Indian company, the actual cost of a block of assets asset to the amalgamated company shall be the written down value of the block of assets as in the case of the amalgamating company for the immediately preceding previous year as reduced by the amount of depreciation actually allowed in relation to the said preceding previous year.

33. The application of these Explanations has to be additionally seen with regard to the following factors, in the context of intangible assets such as goodwill:

A) These Explanations apply only to such assets for which a cost can be conceived in the hands of the amalgamating company.

34. Explanation 7 and Explanation 2 to Section 43(1) and Section 43(6) of the IT Act respectively deem the actual cost of the asset/ block of assets to an amalgamated company as the actual cost of the asset/ block of assets to the amalgamating company had it continued to hold the asset/block of assets.

35. For amalgamated company, the goodwill would constitute an internally generated goodwill for which it would be difficult to either ascribe a cost or arrive at the date of when it was acquired. This aspect of difficulty in valuing the goodwill was also recognized by the Apex Court in CIT v. BC Srinivasa Setty [1981] AIR 972. While the legislature, in all its wisdom, brought about an amendment in Section 55(2)(a) to deem cost of acquisition to be Nil in certain cases for certain assets, including goodwill for the purposes of computing capital gains, such a deeming provision is absent in Section 43 to deem the actual cost to be NIL with respect to goodwill which is internally generated. It is a trite law that a fiction has to be strictly construed and cannot travel beyond the text of the section which creates it [CIT v. Shakuntala 43 ITR 352 (SC)).

B) These Explanations apply only qua such assets on which the amalgamating company was claiming depreciation on.

36. Goodwill that is recorded at the time of amalgamation is not necessarily the same goodwill that was inherent in the business of the amalgamating entity. For instance, as is in the present case as well, the value of goodwill includes a loyal customer base for the amalgamating company and would include the value of future business prospects because of the amalgamation (which would consider the prospects to the transferee company in benefiting from tapping the additional customers for its existing line of business). Thus, in case of an amalgamation, goodwill arises for the first time and cannot be said to be an asset which is transferred by the amalgamating company to warrant application of Explanation 7 to Section 43(1) or Explanation 2 to Section 43(2).

37. Thus, the application of these Explanations to intangible assets such as goodwill, especially in cases wherein the cost of the asset is not determinable and where such depreciation on such assets has never been claimed by the amalgamated company is not correct. These Explanations are applicable only to tangible assets. To understand the intention of the legislature behind the introduction of these explanations, it would be relevant to trace their legislative history.

38. In cases of amalgamation, the actual cost of a capital asset and the written down values of a block of assets, for the purposes of depreciation under the IT Act, would be the same as for the amalgamating company and depreciation shall accordingly be computed for the amalgamated company.

39. Prior to the insertion of the aforesaid explanations in the Act, the computation of tax on sale of an asset was governed by Section 41(2) of the Act. Section 41(2), prior to the insertion of the explanations, i.e., prior to 01.04.1967 read as under:

“where any building, machinery, plant or furniture which is owned by the assessee and which was or has been used for the purposes of business or profession is sold, discarded, demolished or destroyed and the moneys payable in respect of such building, machinery, plant or furniture, as the case may be, together with the amount of scrap value, if any, exceed the written down value, so much of the excess as does not exceed the difference between the actual cost and the written down value shall be chargeable to income-tax as income of the business or profession of the previous year in which the moneys payable for the building, machinery, plant or furniture became due”

40. The position can be best described with the help of an example. Suppose the actual cost of an asset is Rs. 100. Till date, depreciation of Rs. 40 has been claimed on it. Thus, the written down value of the asset is Rs. 60. The asset is now sold in the following three scenarios:

a. Sale Consideration is Rs. 75

b. Sale Consideration is Rs. 50

c. Sale Consideration is Rs. 120

In Scenario (a), applying the provisions of Section 41(2), Rs. 15 (i.e. Rs. 75-60) shall be taxable as business profits. No amount shall be taxed as Capital Gains.

In Scenario (b), Rs 10 (Rs. 60-50) shall be allowable as terminal allowance.

In Scenario (c), Rs. 40 (Rs 120-60, restricted to the amount of depreciation claimed) shall be taxable as business profits. Further, an amount of Rs. 20 (the excess sale consideration received over the actual cost of the asset) shall be taxable as Capital Gains.

41. However, this method of taxation caused hardship to companies who underwent the process of amalgamation, since on transfer of assets, tax liability crystallised upon the amalgamating company. Thus, the aforesaid explanations were added to the Act.

42. The aforesaid explanations were first inserted vide Finance (No.2) Act, 1967 w.e.f. 01.04.1967. The relevant extract from the Memorandum to Finance (No.2) Bill, 1967 (Annexure-2 of Paper book-II), explaining the rationale for the amendment extracted below:

“36. ‘Under the present law, certain tax liabilities are attracted in the case of a company merging with another company under a scheme of amalgamation and also, in the case of amalgamating company who receives shares in the amalgamated company in lieu of their shareholdings in the amalgamating company. Some of these tax liabilities discourage amalgamations. For the purpose of facilitating the amalgamation of uneconomic company units with financially sound Indian companies in the interests of increased efficiency and productivity, it is proposed to make the following provisions in law:

(i) There will be no computation of any profit under Section 41(2) of the Income Tax Act in case of amalgamating company with reference to the consideration receivable by it in respect of any building, machinery, plant or Section 41(2) of the IT Act is the excess of sale proceeds or moneys receivable furniture transferred by it to the amalgamated company. The profit under by the assessee in respect of any building, machinery or plant or furniture over the written down value thereof to the extent of the depreciation of any allowance actually granted on such assets. As a corollary to this, there will terminal allowance in respect of such assets.

(ii) As a corollary to provision at (1) above, the actual cost, as also the written down value of building, machinery, plant or furniture transferred by the amalgamating company to the amalgamated company will be taken, in the amalgamating company. For the purpose of provision in Income Tax Act, the assessment of the amalgamated company, to be the same as in the case of the aggregate amount of depreciation allowed from year to year in respect of any asset will be limited to its actual cost, depreciation actually allowed to the amalgamating company on the assets transferred by it to the amalgamated company will also be taken into account. In other words, when the aggregate of the depreciation allowed to the amalgamating company and the amalgamated company in respect of such assets is equal to the actual cost of the assets in the hands of amalgamating company, the amalgamated company will not be entitled to any further depreciation on such assets.”

43. For the sake of clarity and at the cost of repetition, Section 41(2) of the IT Act, prior to 01.04.1967, is reproduced below.

“where any building, machinery, plant or furniture which is owned by the assessee and which was or has been used for the purposes of business or profession is sold, discarded, demolished or destroyed and the moneys payable in respect of such building, machinery, plant or furniture, as the case may be, together with the amount of scrap value, if any, exceed the written down value, so much of the excess as does not exceed the difference between the actual cost and the written down value shall be chargeable to income-tax as income of the business or profession of the previous year in which the moneys payable for the building, machinery, plant or furniture became due”

44. The term ‘sold’ for the purposes of Section 41(2) was ascribed the same meaning as it was defined in Explanation 2 to Section 32(1)(iii). Under the said explanation, the term sold is defined to exclude transfer of assets in a scheme of amalgamation, of any asset by the amalgamating company to the amalgamated company where the amalgamated company is an Indian company.

45. As explained in the Memorandum which is extracted above, the intention to bring in Explanation 7 to Section 43(1) and Explanation 2A (corresponding to Explanation 2 to Section 43(6) as it stands presently) to Section 43(6) was to ensure that the benefit that ensues to the amalgamating company by virtue of non-application of Section 41(2) does not result in loss of revenue to the Government by allowing depreciation on increased values to the amalgamated company.

46. The amendments made in Section 43(1) and Section 43(6) vide Finance (No 2) Act, 1967 is reproduced below for reference. It may be noted that amendment proposed in the Finance Bill was verbatim incorporated in the Finance (No 2) Act, 1967.

Explanation 7 to Section 43(1):

Where, in a scheme of amalgamation, any capital asset is transferred by the amalgamating company to the amalgamated company and the amalgamated company is an Indian company, the actual cost of the transferred capital asset to the amalgamated company shall be taken to be the same as it would have been if the amalgamating company had continued to hold the capital asset for the purposes of its own business.

Explanation 24 to Section 43(2):

Where, in a scheme of amalgamation, any capital asset is transferred by the amalgamating company to the amalgamated company and the amalgamated company is an Indian company, the written down value of the transferred capital asset to the amalgamated company shall be taken to be the same as it would have been if the amalgamating company had continued to hold the capital asset for the purposes of its business.

47. To further support the legislative intent, Circular No 5-P dated 09.10.1967 (Annexure-3 of Paper Book II) may be also be referred to which reiterates what is stated in the Memorandum.

48. On a joint reading of the Section, the Memorandum explaining the provisions and the CBDT circular (all referred supra), it can be concluded that the restriction by Explanation 7 and Explanation 2 (erstwhile contained in Explanation 2A to Section 43(6)) to Section 43(1) and Section 43(6), respectively would operate only qua building, machinery, plant or furniture Le tangible assets. The concept of block of assets and recognition of intangibles as a separate asset class eligible for depreciation, was brought into the IT Act only at a later point in time. At the time when the amendment vide Finance (No 2) Act, 1967 was made, only ships, plant, machinery, furniture and building were recognized as assets eligible for depreciation under Section 32. Hence, it is contended that intention was to apply to Explanation to only those assets which were included as an asset class eligible for depreciation at that point in time.

49. Thus, in view of the above contentions, the provisions of Explanation to Section 43(1) would not be applicable to a capital asset being goodwill and are hence not applicable at all in the present case.

50. Without prejudice to our above contention that Explanation 7 does not contemplate the transfer of capital asset being goodwill, the Ld. AO has relied on the decision of the Bangalore Tribunal in United Breweries Lad v. ACIT . It is respectfully submitted that the said decision was rendered in the context of Explanation 3 to Section 43(1), and not Explanation 7. Explanation 3 provides that if the Assessing Officer is satisfied that the main purpose of the transfer of assets is the reduction of liability to income tax by claiming depreciation on the enhanced cost, then the actual cost to the assessee shall be determined by the Assessing Officer. It is submitted that the instant case is not a case where the Ld. AO has expressed satisfaction that the transfer of assets is for the purpose of claiming excessive depreciation, and thereby reduction in income-tax liability.

51. As far as applicability of Explanation 3 to Section 43(1) of the IT Act is concerned, it may be noted that the onus is on the Ld. AO to establish that value of goodwill is lower than, the actually recognized amount. The Ld. AO cannot ignore the valuation report furnished by the Assessee in support of its claim [CIT v. Sandvik Chokshi Ltd. (Guj)). It has been already submitted earlier as well as before the Ld. AO that the value of goodwill arrived at is as per the certified valuation report issued by a Chartered Accountant obtained by the Appellant. The valuation report is enclosed as Annexure-7 of Paper book -1. Nowhere has the L.d. AO factually been able to establish that the value of the goodwill is lower than that certified by a Chartered Accountant.

52. Hence, the ratio laid down by the decision cited by the Ld. AO cannot be followed in the instant case, and hence the Appellant prays that the disallowance of depreciation on goodwill by the Ld. AO be set aside.

C. Levy of Buy back tax

C.1 Facts relevant to levy of buy back tax

53. During the relevant AY, the Appellant had bought back 12,73,200 of its own shares at a value of Rs. 39.27per share. Thus, the total buyback value was Rs. 4,99,98,564. The said buyback was carried out in compliance with the provisions of the Companies Act, 2013 and in line with Section 69 of that Act, an amount equivalent to the nominal value of shares bought back was transferred from the General Reserve to the Capital Reserve of the Company. The Ld. AO invoked the provisions of Section 115QA and disregarding the submissions of the Appellant regarding nonapplicability of the said section, treated the paid as consideration for buyback of shares as income taxable u/s 115QA.

C.2 On the facts and circumstances of the case, the Ld. AO erred in both facts and in law by assessing the Appellant u/s 1150A of the Act, without appreciating the fact that the issue price of shares was higher than the consideration paid for the buyback.

54. For reference, Section 115QA of the Act is reproduced hereunder:

“115QA. (1) Notwithstanding anything contained in any other provision of this Act, in addition to the income-tax chargeable in respect of the total income of a domestic company for any assessment year, any amount of distributed income by the company on buy-back of shares (not being shares listed on a recognised stock exchange) from a shareholder shall be charged to tax and such company shall be liable to pay additional income-tax at the rate of twenty per cent on the distributed income.

Explanation. For the purposes of this section,-

(i) “buy-back” means purchase by a company of its own shares in accordance with the provisions of any law for the time being in force relating to companies);

(11) “distributed income” means the consideration paid by the company on buy-back of shares as reduced by the amount, which was received by the company for issue of such shares, determined in the manner as may be prescribed.

55. Explanation to the Section defines distributed income to mean the consideration paid by the company as reduced by the amount received by it for the issue of shares. The calculation would thus depend upon these two amounts. As for the first part, i.e., consideration paid by the company on buyback of shares, it is undisputed that the amount paid in buyback of shares by the Appellant to Aptara Inc. is Rs 39.27 per share. The value has been calculated based on Discounted Cash Flow Method as certified by a Chartered Accountant in a valuation report of shares to be bought back. A copy of the valuation report for buyback is enclosed as Annexure-9 of Paper book – II.

56. For the second part, ie., amount received by the Appellant for issue of shares, the Appellant had issued shares to the shareholders of MLPL against purchase consideration to be discharged to them pursuant to the scheme of amalgamation between the two companies. Therefore, the Appellant has received consideration in the form of net worth of MLPL against the issue of shares. As per the valuation report obtained at the time of amalgamation of the companies, the value of MLPL was determined at Rs.24,14,23,000/. The swap ratio of shares was determined at 60.72 shares of the Appellant per share of MLPL, which had issued 1,00,000 equity shares. Thus, the total number of shares issued by the Appellant is 60,72,000. Accordingly, amount received by the Appellant for the issue of shares is worked out as under:

Amount received per share =”Value” of business of MLPL

Number of shares issued by the Appellant

=”24,14,23,000″ 60,72,000

=”39.76

57. It is thus clear that in the instant case, where the amount received by the Appellant for the issue of shares exceeds the amount paid by it for the buyback of shares, there can be no distributed income, and hence the provisions of Section 115QA cannot be applied.

C.3 Without prejudice to the ground that there is no distributed income on facts, the computation mechanism would fail, as there is no ‘amount’ received by the company’ on issuance of the shares

58. As noted earlier, the provisions of buy back tax would apply only if there exists ‘distributed income. The phrase has been defined in the following manner;

(ii) “distributed income” means the consideration paid by the company on buy-back of shares as reduced by the amount, which was received by the company for issue of such shares, determined in the manner as may be prescribed.”

(emphasis supplied)

59. The word ‘amount’ as used in this definition contemplates share application money received on issuance of the shares. The definition of distributed income thus contemplates a situation wherein a company has received certain amount for issue of the shares, and then that company itself pays some consideration for the buyback of the shares. In other words, the Section only contemplates a situation wherein the company issuing the shares as well as the company buying back the shares are the same. This inference can be easily made from a plain reading of the Section.

60. The section has not envisaged a situation where shares are issued against receipt of a business as a going concern in a scheme of amalgamation. In the facts of the present case, the amount on issue of shares was received by the amalgamating company, i.e. MLPL However, it is the Appellant which has paid consideration towards buyback of shares. The lacuna in the computation mechanism has latter been filled in by incorporation of Rule 40BB of the IT Rules. Sub-rule (5) of the Rules specifically provides that, where shares are received by a shareholders in a scheme of amalgamation, the amount received by the amalgamating company on issuance of its shares will be regarded as amount received as contemplated in Section 115QA of the Act. Evidently, the Rule is effective from 01 June, 2016 and is not applicable to shares bought back by the Appellant on 26th December, 2014.

61. It is a settled legal principle that a lacuna existing in a statute can be cured by the Legislature only and not be a means of interpretation by the Judiciary. A ‘casus omissus’ cannot be substituted by anyone other than the Parliament, as held by the Supreme Court in ACIT v. Velliappa Textiles Ltd [2003] 263 ITR 550 (SC). It is therefore submitted that, in the absence of a computing mechanism during the subject period, the Appellant could not have been regarded as having received any ‘amount’ for ‘issue of such shares”. Consequentially, the levy would not be applicable in the facts of the Appellant.

62. The Ld. AO, in his order, has held that the amount received by the Appellant Company for issue of the shares is Nil, and hence the Appellant is liable to pay tax on the buyback of the shares, on the entire value of the amount paid to the shareholders on the buyback of such shares.

63. It is respectfully submitted that the Ld. AO has grossly erred in law while interpreting the provisions of Section 115QA of the IT Act. Distributed income, as defined by the Explanation, is the difference between the consideration paid on the buyback of shares as reduced by the amount received by the company on the issue of the shares.

64. The term ‘amount received’ is not defined anywhere in the Act. The meaning of the word ‘amount’, as per the Oxford English Dictionary is “the total number, size or value of something’

Black’s Law Dictionary defines the term as:

The effect, substance, or result; the total or aggregate sum Thus, the term amount would mean the total or aggregate sum/ value of something. Applying the meaning of the word in the Section, the term ‘amount received would mean the total or aggregate value received against the issue of the shares.

65. In the facts of the present case, the Appellant Company has received the assets and liabilities of a going concern against the issue of shares. In other words, the Appellant Company has acquired a going concern against the issue of the shares. Thus, the amount received by the Appellant Company against the issue of the shares is either (a) indeterminate, or (b) the value of the business acquired by the Appellant.

66. If the amount is regarded as indeterminate, for the reasons mentioned hereinabove, the computation mechanism would fail, and hence, the tax cannot be collected from the Appellant.

67. If the amount is regarded as the value of the business acquired by the Appellant upon amalgamation, as noted in the earlier part of the submission, the consideration paid is less than the amount received by the Appellant, and hence, there can be no taxable distributable income in the hands of the Appellant. The levy would fail on this count as well.

It is thus our prayer that the additions made by the Ld. AO, being incorrect both in law as well as facts, be set aside.

We request Your Honour to kindly take this submission on record.

Yours Sincerely,

For Aptara Technologies Private Limited Authorised Signatory. “

10. Ld. Senior Counsel for the assessee also stated that the amalgamation has taken place with the purpose of taking over the running business of MLPL and pursuant to the same the Revenue and the profitability of the assessee company has increased substantially. He also submitted that by way of amalgamation the assesee has gained significantly in the form of high skilled employees, increased talent pool, significantly increased revenue, increased client and customer base along with the reduced costs, simpler management structure. He also submitted that the claim has been approved by the Hon’ble Bombay High Court and the assessee had duly complied with as per the scheme and the creation of Goodwill is also made in light of judgment of Hon’ble Apex court in the case of Smifs Securities Ltd. (supra) and there are plethora of decisions which support such creation of Goodwill by the assessee in its books. Since the consideration paid over and above the net asset of the Transferor company is Goodwill actually paid by the Transferee company, the same deserved to be created as Intangible asset and depreciation on the same is allowable as per the provisions of the Income Tax Act.

11. So far as the issue relating to buyback of shares is concerned, he submitted that the valuation of the Equity shares has been calculated as per the DCF method. Valuation report issued by Chartered Accountant has taken into consideration all the aspects as required for preparing such report. He also submitted that deduction of the consideration received by the assessee for issue of such shares bought back by assessee is as per the definition of Distributed Income u/s.115QA of the Act because the assessee had issued shares to the shareholders of MLPL against purchase of running business of MLPL which the assessee has received in the form of net worth of MLPL against the issue of shares. He therefore submitted that ld. Assessing Officer has erred in considering only Rs.10.00 lakh which is the face value of Equity shares rather than considering the amount received by the assessee company at Rs.39.78 per Equity share which has been calculated by dividing the value of business of MLPL with number of shares issues by the assessee company to MLPL. He also referred to the Oxford Dictionary defining the word “Amount” – the total of something in number, size, value, or extent and also referred to the Black’s Law Dictionary defining the word “Amount realized” – The amount received by a taxpayer for the sale or exchange of an asset, such as cash, property, services rendered, or debts assumed by a buyer. Referring to these definitions, it is contended that it is not only the face value of Equity share which the assessee company received at the time of issuing the original Equity shares but the increase in the value of Equity share on account of amalgamation of MLPL which has added to the assessee’s company’s net worth. He also submitted that the amount received by the appellant company against the issue of shares either (a) indeterminate or (b) the value of the business acquired by the appellant. If the amount is regarded as indeterminate, then the computation mechanism would fail and if the amount is regarded as value of business acquired by the assessee upon the amalgamation, the consideration paid for buyback is less than the amount received by the assessee and therefore there can be no taxable distributable income in the hands of assesssee company. Ld. Counsel for the assessee placed reliance on the following decisions :

| 1. |

|

Urmin Marketing (P.) Ltd. v. Dy. CIT (Ahmedabad – Trib.) |

| 2. |

|

Disney Broadcasting (India) (P.) Ltd. v. Pr. CIT (Mumbai – Trib.) |

| 3. |

|

Dow Chemical International (P.) Ltd. v. Dy. CIT (Mumbai – Trib.) |

| 4. |

|

Trivitron Healthcare (P.) Ltd. v. Pr. CIT (Chennai – Trib.) |

| 5. |

|

Padmini Products (P.) Ltd. v. Dy. CIT (Karnataka) |

| 6. |

|

Altimetrik India (P.) Ltd. v. Dy. CIT (Bangalore – Trib. |

| 7. |

|

Geodis Overseas Pvt. Ltd. v. DCIT – ITA No. 2305/Del/2015 dated 18.05.2020 |

| 8. |

|

Goldman Sachs (India) Securities (P.) Ltd v. ITO (International Taxation) (Mumbai) |

| 9. |

|

Capgemini India (P.) Ltd., In re (Bombay) |

12. Ld. Departmental Representative vehemently argued referring to the following written submissions :

“Brief facts of the case:

| o |

|

The assessee is a domestic company (in which public is not substantially interested) engaged in the field of providing IT enabled conversion services. |

| o |

|

During the A. Y. under consideration there was amalgamation in the nature of merger between Maximise Learning Pvt. Ltd. (MLPL) (Transferor Company) and Aptara Technologies Pvt. Ltd. (ATPL) (Transferee Company). Both the companies are wholly owned subsidiaries of Aptara Inc. (USA) (Holding Company). |

| o |

|

The amalgamation scheme was approved by the Hon’ble Bombay High Court by order dated 19/ 09/2014 with effective from 01/04/2014. |

| o |

|

As per the scheme, the shareholders of Maximise Learning Pvt. Ltd. got 60.72 shares for every 1 share held by them in Maximise Learning Pvt. Ltd. The assessee company recognized goodwill of Rs. 5,97,20,000/- (Rs, 6,07,20,000/-Rs. 10,00,000/ -) and claimed amortization of Rs. 1,19,44,000/- (Rs. 5,97,20,000/-/5)as per the Companies Act 1956. However as per 3CA, the depreciation on goodwill of Rs. 1,49,30,000/- was claimed i.e. at the rate of 25%. |

| o |

|

However, due to failure of the assessee to prove genuineness of the transaction between related parties, inability to explain the basis of quantification, non-satisfaction of recognition of goodwill and violation of AS 14 issued by the ICAI, the Ld. AO added the amount of depreciation of Rs. 1,49,30,000/- to the income of the assessee. |

| o |

|

Further there was Capital Reserve created on Liabilities side of the Balance Sheet of Rs. 1,27,32,000/- which was due to buy back of 12,73,200 equity shares of face value Rs. 10/-each at Rs. 39.27/- each. The assessee submitted calculation of Distributed Income claiming that distributed income was negative and hence no tax was paid by the assessee as per section 115QA of the Act. |

| o |

|

However, according to the computation provision given in clause (ii) of explanation to Sec 115QA of the Act, the assessee was required to pay the tax and hence the Ld. Assessing officer raised the tax demand of Rs. 99,57,776/ -u/ s 115QA of the Act. |

| o |

|

Ld. CIT(A) upheld the order of the AO and confirmed the addition and tax demand. |

After due verification of the above facts and the submissions made by the assessee before the AO and CIT(A), comments of the undersigned are as follows:

Recognition of goodwill and claim of deprecation thereon:

1. The amalgamation between Maximise Learning Pvt. Ltd. (Transferor Company) and Aptara Technologies Pvt. Ltd. (Transferee Company) was in the nature of merger and they opted for the ‘Pooling of Interest’ method.

2. From the para 4.4 page no. 11-12 of the Assessment Order, it can be observed that there is a Qualification remark put by the auditors of the assessee regarding accounting treatment done for amalgamation. The remark states that,

“Had the provisions of paragraph 16 and 35 of AS-14 Accounting for Amalgamation issued by the Institute of Chartered Accountants of India been followed, the difference would have been adjusted from the reserves. The reserves would have been lower by Rs. 4,97,66,667 and profit for the period 1 April 2014 to 31 March 2015 would have been higher by Rs. 1,19,44,000.”

The above remark clearly states that the provisions of paragraph 16 and 35 of AS 14 have not been followed by the assessee in accounting for amalgamation despite the auditor’s deviation note. Despite the approval by the Hon’ble Bombay High Court of the scheme of amalgamation on the basis of affidavit filed by the appellant on 26.08.2014, the auditor has still given a qualification remark regarding the accounting for amalgamation emphasizing on the AS 14 issued by the ICAI. The relevant para of the affidavit is reproduced below for ready reference:

Para 6(a) and (b) of Affidavit

“6. That the Deponent further submits that:-

(a) Clause 14.2 of the scheme states that the difference, if any, of the net value of assets, Inabilities and reserve of the Transferor company acquired and recorded by the Transferee company and the face value of the New Equity Shares on Merger, issued and allotted pursuant to Clause 12.1 of the Scheme, shall be adjusted in reserves in accordance with the provisions of paragraph 16 and 35 of Accounting Standard 14- ‘Accounting for Amalgamation’ issued by the Institute of Chartered Accountants of India. In this regard, it is submitted that the surplus if any arising out of the scheme shall be transferred to Capital Reserve Account of the Transferee company. If there is a Deficit, the same shall be debited in Goodwill Account of the Transferee Company.

(b) It is respectfully submitted that the tax implication, if any, arising out of the Scheme is subject to final decision of Income Tax Authorities. The approval of the Scheme by this Hon’ble Court may not deter the Income Tax Authority to scrutinize the tax returns filed by the Transferee Company after giving effect to this scheme of amalgamation. The decision of the Income Tax Authority is binding on the Petitioner Company.”

Even after the deviation note of the auditor which pointed out specifically the violation of the provisions of the AS 14 and also having the conscious knowledge of para 9 & 10 of the amalgamation scheme approved by the Hon’ble High Court of Bombay, the appellant has proceeded to ignore the observations of the auditor as the same was against the benefit of the appellant and the colourable design of the amalgamation arrangement was created.

3. Also the remark of the auditor makes it clear that the assessee company after amalgamation had enough reserves to adjust the amount to be paid on share capital issued of Rs. 6,07,20,000/ – from the combined reserves.

4. The paragraphs 16 and 35 of AS-14 Accounting for Amalgmation’ issued by the ICAI explain that:

“16. If the amalgamation is an ‘amalgamation, in the nature of merger’, the identity of the reserves is preserved and they appear in the financial statements of the transferee company in the same form in which they appeared in the financial statements of the transferor company. Thus, for example, the General Reserve of the transferor company becomes the General Reserve of the transferee company, the Capital Reserve of the transferor company becomes the Capital Reserve of the transferee company and the Revaluation Reserve of the transferor company becomes the Revaluation Reserve of the transferee company. As a result of preserving the identity, reserves which are available for distribution as dividend before the amalgamation would also be available for distribution as dividend after the amalgamation. The difference between the amount recorded as share capital issued (plus any additional consideration in the form of cash or other assets) and the amount of share capital of the transferor company is adjusted in reserves in the financial statements of the transferee company.

The Pooling of Interests Method

35. The difference between the amount recorded as share capital issued (plus any additional consideration in the form of cash or other assets) and the amount of share capital of the transferor company should be adjusted in reserves.”

The above paragraphs of AS-14 make it very clear that the difference between amount recorded as share capital issued and amount of share capital of the transferor company should be adjusted in reserves. Para 35 specifically explains accounting w.r.t. Pooling of Interest Method which is adopted by the assessee company in the present case. Hence, assessee company should have adjusted the reserves for the differential amount in compliance with the para 35 of AS-14.

The appellant has stated in his affidavit dated 26.08.2014 at para 6(a) that the surplus if any arising out of the scheme shall be transferred to Capital Reserve Account of the Transferee company and if there is a Deficit, the same shall be debited in Goodwill Account of the Transferee Company. However, the said treatment is applicable when the amalgamation is in the category of Purchase Method and not in the Pooling of Interest Method. Hence, the appellant’s contention in the affidavit is contradicting the method adopted for amalgamation by assessee company. The treatment stated in the affidavit would have been applicable if the adopted method would have been the Purchase method as specified in para 37 of AS14, which is reproduced below:

The Purchase Method

37. Any excess of the amount of the consideration over the value of the net assets of the transferor company acquired by the transferee company should be recognised in the transferee company’s financial statements as goodwill arising on amalgamation. If the amount of the consideration is lower than the value of the net assets acquired, the difference should be treated as Capital Reserve.

5. The above provisions of AS-14 explain the disclosure of reserves of the transferor company in the transferee company and adjustment of differential amount against reserves. However, the assessee in its submission as given on page 8-9 of the Assessment Order has interpreted the above provisions as beneficial to them to avoid tax liabilities by creating goodwill and claiming depreciation thereon.

6. Further, the explanation 7 to Section 43(1) of the Act shall also be considered which states that,

“Explanation 7. Where, in a scheme of amalgamation, any capital asset is transferred by the amalgamating company to the amalgamated company and the amalgamated company is an Indian company, the actual cost of the transferred capital asset to the amalgamated company shall be taken to be the same as it would have been if the amalgamating company had continued to hold the capital asset for the purposes of its own business.”

The above explanation states that if the amalgamating company is holding capital asset then after amalgamation the cost of capital asset should be taken to be the same as it would have been if the amalgamating company had continued to hold the capital asset for the purposes of its own business.

7. In the present case, the amalgamating company i.e Maximize Learning Pvt. Ltd. did not have any goodwill in its books of accounts before amalgamation. As there was no goodwill existed in amalgamating company, the same shall not form part of the amalgamated company i. e. Aptara Technologies Pvt. Ltd. Due to recognition of goodwill, there is an extra asset which is being created and which is not allowed as per the above explanation 7 to Section 43(1) of the Act.

8. The Ld. AO has referred various case laws for the definition of the term “Goodwill” (Para 4.6 page 14-16 of the Assessment Order) as it is not defined anywhere in the Act. The common underlying principle reiterates that “Goodwill” purchased represents certain specific business/commercial rights, which enable acquirer to carry on the business effectively and profitably and hence, it may be possible to claim depreciation on such goodwill.

9. In the present case, the High Court order of the approval of amalgamation scheme states that:

“3. Learned Counsel for the Petitioners states that the Transferor Company and Transferee Company are business of providing IT enabled conversion services. The proposed scheme of Amalgamation will have the benefit that The integration of the operations of Transferor Company and Transferee Company would have the benefit of eliminating duplication of processes and structures resulting in cost savings and A simplified corporate structure and improved management focus and Centralizing the activities of the two companies is expected to lead to improvement in operational and cost efficiency through economies of scale, optimization of resources, expansion of asset base and a stronger balance sheet of the enlarged company and Post the amalgamation of Transferor Company into Transferee Company, Transferor Company will be dissolved. Consequently, there would be less regulatory and legal compliance obligations including accounting, reporting requirements, statutory and internal audit requirements, tax filings etc and therefore reduction in administrative costs and The restructuring would facilitate improvement in organizational capabilities arising from the pooling of human resources with diverse skills, talent and vast experiences and The combined operations of Transferor Company and Transferee Company are expected to give rise to capital efficiency and improved cash flows.”

From the above paragraph it can be seen that there are very general advantages to both the companies from the amalgamation. The main intention of the amalgamation was ‘Cost Efficiency’ which does not satisfy the creation of goodwill. There is no specific advantage like increase in client base, superior technology, knowhow, patent, etc. which would give the transferee company any substantial benefit post amalgamation. Hence, the creation of goodwill on the basis of such general advantages is not justified.

Further, as per AS 14, “Pooling of interests is a method of accounting for amalgamations the object of which is to account for the amalgamation as if the separate businesses of the amalgamating companies were intended to be continued by the transferee company. Accordingly, only minimal changes are made in aggregating the individual financial statements of the amalgamating companies.”

Further, as mentioned in para 4, page 2 of the assessee’s paper book dated 13 June 2022 the assessee has tried to draw an analogy by stating about providing digitalised services to tax payers by updating annual amendments in the Income tax Act.

10. Further, as per para 4.6.3 page no. 17-18 of the Assessment Order, it can be observed that page 4, para 8 of the High Court Order states that, the Regional Director filed an affidavit on 26th August 2014. The main point of the same is as follows:

“8. The Regional Director has filed an Affidavit on 26th August, 2014 stating therein, save and except as stated in paragraph 6, it appears that the Scheme is not prejudicial to the interest of shareholders and public. In paragraph 6 of the said Affidavit, it is stated as under:

“6. That the Deponent further submits that:-

(b) It is respectfully submitted that the tax implication., if any, arising out of the Scheme is subject to final decision of Income Tax Authorities. The approval of the Scheme by this Hon’ble Court may not deter the Income Tax Authority to scrutinize the tax returns filed by the Transferee Company after giving effect to this scheme of amalgamation. The decision of the Income Tax Authority is binding on the Petitioner Company.”

In response to the same the High Court in its Para 10 made the following remarks:

“10. So far as the observation in paragraph 6(a) of the Affidavit of Regional Director is concerned, the Petitioner Companies are bound to comply with all applicable provision of Income Tax Act, and all tax issues arising out of Scheme will be met and answered in accordance with law.”

From the above, it can be observed that the High Court has not commented on the taxation implications of the amalgamation scheme and the assessee is bound by the decision of the Income Tax Authorities.

11. Ld. CIT(A) has discussed the above issue of goodwill in more detailed manner. In para 7.1.5 page 18 of the CIT(A) order, it is discussed that, both the companies are wholly owned subsidiaries of the Aptara Inc. (USA) before amalgamation. Hence, there exists a common control. The Ld. CIT(A) has also discussed Ind AS 103 Business Combinations’ in para 7.1.16 page no. 32-33 of the CIT(A) order. Ind AS 103 has much wider scope than AS 14. One of the most essential elements covered in Ind AS 103 is the manner of accounting in a common control transaction. Ind AS 103 has defined common control business combination as a business combination in which all the combining entities or business are ultimately controlled by the same person/persons both before and after the combination and such control is not transitory in nature. Ind AS 103 prescribes application of pooling of interest method to account for common control business combinations. Under this method:

| • |

|

All identified assets and liabilities will be accounted at their carrying amounts, i.e. no adjustment would be made to reflect their fair values unlike in case of non-common control business combinations. |

| • |

|

Balance of retained earnings in the books of acquirer entity shall be merged with that of the acquirer entity, and identity of the reserves shall be preserved. |

| • |

|

Any difference, whether positive or negative, shall be adjusted against the capital reserves (or “Amalgamation Adjustment Deficit Account” in some cases). |

| • |

|

Hence, no goodwill can be recorded in books under common control transactions under Ind AS 103. |