ORDER

C.N. Prasad, Judicial Member.- All these appeals are filed by the revenue for the A.Y’s 2009-10, 2011-12 and 2012-13 to 2015-16. The assessee filed appeal for the A.Y.2011-12 in ITA No.989/Del/2017.

2. First we take up the appeal of the revenue for the A.Y.2009-10 in ITA No.5095/Del/2014. The revenue in its appeal raised the following grounds of appeal : –

| 1. |

|

Whether on the facts and circumstances of the case & in law, the Ld. CIT(A) erred in rejecting the Transfer Pricing approach of the TPO on short charge by the assessee to its US AE? |

| 2. |

|

Whether on the facts and circumstances of the case & in law, the Ld. CIT(A) erred in rejecting the internal comparison made by the TPO wherein both the segments were involved in performing similar functions and utilizing same assets and undertaking similar risks? |

| 3. |

|

Whether on the facts and circumstances of the case & in law, the Ld. CIT(A) erred in accepting the transfer pricing approach of the assessee on short charge by Assessee from its US AE whereas in A.Y. 2007-08 the CIT (A) has upheld the adjustment albeit to the extent of Rs. 50000/-? |

| 4 |

|

Whether on the facts and circumstances of the case & in law, the Ld. CIT(A) erred in deleting the addition u/s 37(1) made by the AO by grossly ignoring the reasons advanced by the assessing officer and totally relying upon the submissions of the assessee? |

| 5. |

|

Whether on the facts and circumstances of the case & in law, the Ld. CIT(A) erred in holding that the assessee was not under no obligation to deduct tax on the payment of gateway charges made to City Bank & Amex Bank as order u/s 195/197 is valid only for the Indian branches of the above bank and not for the payments received on behalf of the Head Office. The commission payments are not received by the branches of the above banks located at various places in India but by the Head Office of the above Banks. Hence, the above order is not valid for the payment gateway charges and giving relief amounting to Rs. 41346192/- |

| 6. |

|

Whether on the facts and circumstances of the case & in law, the Ld. CIT(A) erred in deleting the addition made by the AO on account of Deferred Revenue Income by grossly ignoring the findings of the AO and by merely relying upon the submissions of the assessee company and giving relief amounting to Rs. 154237532/-7 |

| 7. |

|

Whether on the facts and circumstances of the case & in law, the Ld. CIT(A) erred in deleting the disallowance made by the assessing officer for payments made to MMT US by ignoring the findings of the AO that the said payments are not in the nature of reimbursement of expenses, as claimed by the assessee, but are fees for technical services as per the provision of Section 9(1)(vii) of the Income Tax Act, 1961 therefore liable for deduction of TDS as per provisions of section 195 as there is clement of income embedded in these payments and allowing relief of Rs. 333245829/- to the assessee? |

| 8. |

|

Whether on the facts and circumstances of the case & in law, the Ld. CIT(A) erred in allowing relief to the assessee by relying upon the addition evidence accepted and without giving opportunity to the assessing officer as per provisions Rule 46A? |

| 9. |

|

That the order of the Ld. CIT(A) is erroneous and is not tenable on facts and in law. |

| 10. |

|

That the grounds of appeal are without prejudice to each other. |

3. The Ld. Counsel for the assessee at the outset submitted that ground No.1 to 3 are in respect of transfer pricing adjustment made by the TPO rejecting the transfer pricing approach of the Assessee in respect of Advertisement, Marketing & Promotion Expenses (AMP) approach adopted by the assessee.

4. The Ld. Counsel for the assessee submitted that the issue is covered in favour of the assessee by the order of the Tribunal for the A.Y. 2005-06 to 2009-10 and the copies of the orders of the Tribunal are placed in paper book pages-1 to 103 and also the judgment of the Hon’ble High Court which is placed at pages 104 to 110 in assessee’s own case for the A.Y. 2009-10. Referring to page 63 para 8 of the paper book which is order of the Tribunal for the A.Y.2007-08 and 2008-09 in ITA No.2692 and 4974/Del/2013 dated 22.06.2020 submitted that the Tribunal deleted the adjustment made by the TPO in respect of AMP expenses. The Ld. Counsel for the assessee further referring to page 75 para -20 submitted that the transfer pricing adjustment made in respect of ticketing charges and tours and travels packages services the Tribunal upheld the order of the Ld. CIT(A) in restricting the addition to Rs.50,000/- as against the addition made by the TPO.

5. The Ld. DR strongly supported the orders of the authorities below.

6. Heard rival submissions and perused the orders of the authorities below. In so far as the TP adjustment in respect of AMP expenses and ticketing charges and tours and travel packages services are concerned we observed that the issue is a recurring issue from the year to year starting from A.Y. 2005-06 to 2009-10 and we observed that the Tribunal for the A.Y. 2007-08 and 2009-10 vide order dated 26.02.2020 in ITA No.2692 and 4974/Del/2013 which is placed at pages -57 to 84 deleted the transfer pricing adjustment by observing as under :-

| “8. |

|

Ground Nos.1 to 7 by the Revenue and ground No.1 by the assessee relate to the order of the CIT(A) in deleting the addition of Rs.31,81,07,110/- on account of adjustment of AMP expenses and restricting the addition of Rs.1,47,93,024/- for ticketing services and tours and travel services packages to Rs.50,000/-. |

| 9. |

|

The ld. DR strongly supported the order of the TPO. He submitted that the assessee had spent Rs.31,36,22,787/- on AMP out of which Rs.3,60,01,993/- has been reimbursed to it by the subsidiary MakeMy Trip Inc. This was 50.40% of assessee’s operating income of Rs.62.22 crores. The assessee had selected nine comparable companies from the ITES sector for benchmarking the charge received by it from MMT US for its back office activity for rendering ticketing services and tours and travel related services to MMT US. Out of the nine companies selected by the assessee, financials of six companies for F.Y. 2006-07 were available. The remaining three companies had spent 40.0583% of the sales as AMP expenses as against 50.40% in case of the assessee. Therefore, applying the same benchmark, the TPO had determined the excess AMP expenses by the assessee at Rs.313,259,999/-. The ld. DR submitted that the TPO has rightly made the addition of the above amount to the total income. He submitted that because of the development of brands in India, the US company is capitalizing that brand building and developing brand in US. Therefore, to some extent, the AMP expenses has to be considered for the purpose of TP adjustment. However, the TPO has not done any adjustment. Further, the CIT(A) has accepted certain additional evidences and given relief to the assessee. Therefore, he submitted that the matter should be restored back to the file of the TPO for fresh adjudication of the issue. So far as the short charge of Rs.1,47,93,024/- on account of ticketing and tours & travel packages is concerned, he submitted that the TPO has given justifiable reasons while proposing upward adjustment. Therefore, the same should be upheld. |

| 10. |

|

The ld. Counsel, on the other hand, heavily relied on the order of the CIT(A). He submitted that the ld.CIT(A) has given a categorical finding that the brand is owned by the assesseee and not by the US company. Further for the A.Y. 2010-11 the Department has accepted that it is not an international transaction. So far as the additional evidences filed before the CIT(A) are concerned, he submitted that these are only for the AMP expenditure and the documents are vital. Referring to the decision of the Hon’ble Delhi High Court in the case of CIT v. Virgin Securities and Credits P. Ltd. , reported in 332 ITR 396, he submitted that the Hon’ble High Court in the said decision has held that before admitting the additional evidences, the CIT(A) had obtained a remand report from the AO. The additional evidence was crucial to the disposal of the appeal and had a direct bearing on the quantum of the claim made by the assessee. Rule 46A of the Income-tax Rules, 1962 permits the CIT(A) to admit additional evidences if he finds that the same is crucial for disposal of the appeal. He submitted that the ld.CIT(A) in the instant case has obtained a remand report from the AO. Therefore, the Revenue should not have any grievance since the AO was given due opportunity of being heard before admission of the additional evidence which is vital for determination of the case in hand. |

| 10.1. |

|

Referring to the decision of the Hon’ble Bombay High Court in the case of Prabhavati S. Shah, reported in 231 ITR 1, he submitted that the Hon’ble High Court in the said decision has held that if prima facie information is necessary for the claim of the assesseee, the CIT(A) should consider the necessary evidence in exercise of his power u/s 250(4) of the Act. It has been held that when a statutory authority has the powers to do something, then, it has a corresponding duty to exercise such powers whenever circumstances warranting exercise of such powers exist. |

| 11. |

|

He also relied on various other decisions filed in the case law compilation and synopsis. |

| 12. |

|

So far as the argument of the ld. DR that AMP expenses was not incurred by the assessee wholly and exclusively for the business of the assessee and was capital in nature is concerned, the ld. Counsel for the assessee, referring to the decision of the Hon’ble Delhi High Court in the case of CIT v. Salora International Ltd. , 308 ITR 199, submitted that the Hon’ble High Court in the said decision has held that where the assesseee incurred advertisement expenditure for launching products and the Tribunal had given the finding that the assessee had to incur such expenditure to meet the competition in the market for selling the product, then, the entire expenditure is allowable as revenue expenditure and the finding of the Tribunal does not call for any interference and, therefore, no substantial question of law arises. |

| 12.1 |

|

Referring to the decision of the Hon’ble Delhi High Court in the case of CIT v. Monto Motors Ltd., vide ITA No. 978/2011, order dated 12th December, 2011, he submitted that the Hon’ble High Court has upheld the decision of the Tribunal where the Tribunal has held that the advertisement expenses when incurred to increase the sales of products are usually treated as revenue expenditure. Since the memory of purchaser or customer is short, advertisements are issued from time to time and the expenditure is incurred periodically, so that the customers remained attracted and do not forget the products and its qualities. Advertisement and sales promotion are conducted to increase the sale and their impact is limited and felt for a short duration and no permanent character or advantage is achieved and is palpable, unless special or specific factors are brought on record. |

| 12.2 |

|

Referring to the decision of the Hon’ble Delhi High Court in the case of CIT v. Jubilant Food Works India Pvt. Ltd. , reported in 271 CTR 227, he submitted that the Hon’ble High Court in the said decision has held that expenditure incurred by the assessee on advertisement expenses is revenue in nature since no permanent character or advantage is achieved via the same and such expenses for advertising the consumer products generally are a part of the process of profit earning and not in the nature of capital outlay. So far as the order of the CIT(A) in restricting the addition on account of transfer pricing adjustment in regard to ticketing and tours & travel package services to Rs.50,000/- is concerned, the ld. Counsel submitted that the same addition was sustained by the CIT(A) on the basis of and without prejudice to the arguments taken by the assessee before the CIT(A). However, no addition is called for. |

| 13. |

|

We have considered the rival arguments made by both the sides, perused the orders of the AO the CIT(A) and the paper book filed on behalf of the assessee. We have also considered the various decisions relied upon by both the sides. We find, the TPO, in the instant case, has made transfer pricing adjustment of Rs.33,29,00,134/- which comprises of two additions, i.e., on account of AMP services of Rs.31,81,07,110/- and ticketing and tours & travel package services of Rs.1,47,93,024/-. So far as the addition on account of AMP services of Rs.31,81,07,110/- is concerned, it is the case of the TPO that the assessee has less charged the above amount from its AE. According to the TPO, the assessee had spent Rs.31,36,22,787/- on AMP out of which only Rs.3,60,01,993/- had been reimbursed to it by its subsidiary MakeMy Trip.com Inc. This was 50.40% of the assessee’s operating income of Rs.62.22 crores. Since, according to the TPO, out of the nine comparables selected by the assessee, the financials of six companies for A.Y. 2006-07 were available and the remaining three companies had spent only 0.05% of sales as its AMP as against 50.40% in the case of the assessee, the TPO concluded that the assessee had spent excessively of AMP of Rs.31,32,51,999/- meaning thereby that as against Rs.31,36,22,787/- spent by the assessee on AMP, only Rs.3,62,788/- should have been spent. The TPO, therefore, treated this excess AMP expenses as international transaction and inferred that it was for promotion of MakeMy Trip brand only for which the assessee should have been compensated. It is also the case of the TPO that the beneficiary of this excess AMP was parent company MMT Mauritius since, later on, MMT Mauritius had listed 50 lakh shares at USD 15 each totaling to USD 70 million on Nasdaq, USA on 13th August, 2010. According to the TPO, MMT Mauritius has been benefitted by the listing of the company in the US at a premium. According to the TPO, when the assessee MMT India was in losses, the shares of its parent MMT Mauritius were being quoted at a premium at Nasdaq IN USA. Therefore, the beneficiary of excess AMP expenses by MMT India was MMT Mauritius. Therefore, MMT Mauritius should have compensated MMT India for services rendered in connection with promotion of marketing intangibles which accrued to the benefit of MMT Mauritius. It is also the case of the TPO that even otherwise also such huge expenditure of AMP should have been capitalized since the assessee derives an enduring benefit. |

| 14. |

|

We find, the ld.CIT(A) after obtaining a remand report from the AO had given a finding that the assessee is the owner and sole beneficiary of MakeMy Trip or MMT brand since the trade mark ‘MakeMy Trip’has been registered in the name of MakeMy Trip (India) Pvt. Ltd., w.e.f. 25th April, 2006. Event the TPO himself at various places of his order has accepted that MMT India is the owner of MMT brand. We find the ld. CIT(A) had also given a finding that neither the share premium received from incoming shareholders upon IPO listing nor steady value creation in the hands of founder/existing shareholders be deemed to qualify as any kind of benefit accruing to MMT Mauritius under the provisions of the Act. Further, he has also given a finding that the AMP expenses incurred by the assessee is wholly and exclusively for the purpose of business and not capital in nature. While admitting the additional evidence, he had also given justifiable reasons as to why he has accepted the same under Rule 46A of the IT Rules. The relevant findings of the CIT(A) from para 7 onwards read as under:- |

“7.0 Finding:

7.1 During the course of appellate proceedings, the appellant furnished a copy of agreement dated 01.04.2006 between appellant and MMT Mauritius. It also furnished a list of 3 new comparables viz. Thomas Cook, Cox & King, Shree Raj Travels & Tours for tire purpose of application of bright line test, Since these documents were not furnished before AO, these were sent to AO requiring him to furnish his remand report u/r 46A. The AO furnished his remand report vide letter dated 03.12.2012, The appellant also furnished a rejoinder to it vide letter dated 28.12.2012. I have considered both remand report and the rejoinder in context, of factual matrix of the case. The AO has argued that adequate opportunities were provided to the appellant during assessment stage and therefore there is no case u/r 46A for admission of these additional evidences. The appellant has argued that intercompany covenant has been furnished to substantiate its claim that the brand is owned by the appellant, a fact which even the AO has not explicitly denied. Further, financials of 3 new comparables have been furnished because the AO has wrongly taken comparables of ITES companies which were taken by the appellant for the purpose of bench marking its receipts from provision of ticketing & tour and package services to MMT Inc. US. It is seen that the appellant has taken this plea before the AO also but it was not considered. The AO did not ask for copy of intercompany agreement during assessment stage to verify the actual ownership of the brand. Therefore, considering the fact that these additional evidences are vital to decide the relevant issue, I hereby admit the additional evidence u/r 46A.

7.2 After considering the TPO/AO’s orders and the arguments of the appellant, 1 am of the considered view that appellant is the owner and sole beneficiary of the MakeMyTrip or MMT brand. The trademark ‘MakeMyTrip’ has been registered in name of MakeMyTrip (India) Pvt. Ltd. w.e.f. 25.04.2006 as evidenced by registration certificate dated 29.10.2008 issued by Government of India, Registrar of Trade marks. Further, Para 2 of the intercompany covenant dated 01.04.2006 establishes beyond all doubt that MMT India is the owner and sole beneficiary of MMT brand. Even the TPO himself has indicated at various places of his order his acceptance that MMT India is the owner of MMT brand. Therefore Blight Line Test or Arm’s Length AMP Expenditure Test suggested in the OECD Guidelines/Australian Tax Office Guidelines/ US case laws, which is relevant only in the context of promotion of brand owned by the foreign AE, is not applicable in the appellant’s case. The said bright line test comes into operation in a situation where a business enterprise is incurring excessive AMP expenditure for promoting a brand owned by its foreign AE. Based on appellant’s submissions and evidences placed on record, it is explicitly clear that the appellant is the sole beneficiary of the AMP expenses. A Special Bench of Hon’ble Delhi Tribunal in case of LG electronics India Pvt. Ltd. v ACIT ITA No. 5140/Del/2011 (judgment dated 23.01.2013) has taken a view that a tacit understanding could be assumed between brand owner and brand licensee regarding excess AMP spend by the licensee, but that assumption is applicable only in cases where the Indian entity promotes brand owned by its foreign affiliate. In appellant’s case, it is the appellant who owns the brand. Therefore, provisions regarding arm’s length price would not apply to the appellant’s case. It has been found that MMT Mauritius has also got ‘MakeMyTrip’ mark registered in its name in Mauritius w.e.f. 19.07.2011 vide registration certificate dated 14.10.2011. The appellant has explained that it has been done to protect future business interests of the appellant’s planned business operations in Mauritian territory. Even this future event has no bearing on the fact that the appellant is both legal and economic owner of the brand ‘MakeMytrip’. The MMT Mauritius is only an investment company as its audited financial statements for the year ending 31.03.2007 shows only interest income and nothing else. It is pertinent to mention that MMT Mauritius had been granted a Category 1 Business licence w.e.f. 05.05.2000 and conditions as mentioned in said licence certificate mention that the stated purpose of the company is to engage in investment holding activities.

7.3 Further, I concur with the contentions of the appellant that neither share premium received from incoming shareholders upon IPO listing nor steady value creation in the hands of founder / existing shareholders be deemed to qualify as any kind of ‘benefit’ accruing to MMT Mauritius under the provisions of the Act. Share issue at a premium does not give any benefit to the company. If the company decides to buy back these shares, the premium has to be returned to the shareholders who sell the shares. And if the shareholders sell the shares in the market, the premium is earned by the shareholder & not by the company. In any case, if because of robust economic growth of a company, there is appreciation in market value of capital investment of its shareholders, then the company has no legal, economic or moral right to get reward/compensation from its shareholders out of such appreciation.

7.4 Lastly, in view of a plethora of case laws on the subject including those cited by the appellant in paragraph 6.3 above, I have no hesitation to hold that the AMP expense of appellant is wholly and exclusively for the purposes of its business and further it is not capital in nature. The AO has not given any reasons in his order to substantiate his observations that AMP expense of the appellant are not wholly and exclusively for the purpose of its business and these are in nature of capital expenses.

7.5 Since, it has been held that the appellant does not render any services in connection with promotion of marketing intangibles which accrue to the benefit of MMT Mauritius; there is no question of applying a mark up for determining the compensation.

7.6 Therefore, addition of Rs 31,81,07,110 made on account of AMP expense is deleted. This disposes of grounds of appeal no. 8 to 15.”

15. We further find from the submissions made by the ld. Counsel that from A.Y. 2010-11 onwards, the Department has accepted that such AMP expenses is not an international transaction and no addition has been made by the AO. From the various details furnished by the assessee, it is seen that the following AMP expenses were incurred by the assessee from A.Y. 2010-11 to 2016-11 and the TPO has not considered the same as an international transaction:-

| Assessment Year |

AMP expenses |

Whether it was considered international transaction by TPO? |

| 2010-11 |

461,907,373 |

No |

| 2011-12 |

577,466,197 |

No |

| 2012-13 |

807,126,413 |

No |

| 2013-14 |

604,210,658 |

No |

| 2014-15 |

811,585,225 |

No |

| 2015-16 |

690,400,000 |

No |

| 2016-17 |

4,741,800,000 |

No |

16. So far as the ground raised by the Revenue relating to acceptance of additional evidence is concerned, we find that the ld.CIT(A), in the instant case, has called for a remand report from the AO and, thereafter, only has admitted the same and has given his finding on the basis of such additional evidence. The Hon’ble Delhi High Court in the case of Virgin Securities and Credits P. Ltd. (supra) has held that when the additional evidence was crucial to the disposal of the appeal and had a direct bearing on the quantum of the claim made by the assessee, Rule 46A of IT Rules, 1962 permits the CIT(A) to admit the additional evidence if he finds that the same is crucial for the disposal of the appeal. The various other decisions relied on by the ld. Counsel for the assessee also support his case that when the evidences are very important for effective adjudication of the grounds raised by the assessee in the appeal and when the CIT(A) forwards these additional evidences to the AO for his comments in the shape of a remand report, then, the same is required to be admitted. It has also been held in various decisions that if the evidence goes to the very root of the matter and essential for rendering substantial justice, then, the same is required to be admitted. Since, in the instant case, the ld.CIT(A) has forwarded those additional evidences to the AO for his comments in the shape of a remand report and since the additional evidence goes to the root of the matter and are essential for rendering substantial justice, therefore, we do not find any merit in the grounds raised by the Revenue for admission of such additional evidence in violation of Rule 46A of the IT Rules.

17.So far as the grievance of the Revenue that the AMP expenses incurred by the assessee is capital in nature is concerned, we find the Hon’ble Delhi High Court in the case of Salora International Ltd. (supra) has observed as under:-

“3. The first issue that is sought to be raised in this appeal pertains to advertising expenditure of approx. Rs. 3.08 crores. According to the AO, the expenditures was incurred for launching of its products. The AO was of the view that such expenditure was of an enduring nature and, therefore, treated one-third as “capital expenditure” and only allowed the two-thirds of the said amount as “expenditure, to the assessee”. The CIT(A) allowed the entire amount after treating the expenditure as “revenue expenditure”. The findings of the CIT(A) were confirmed by the Tribunal by virtue of the impugned order. Particularly, the Tribunal held that there was a direct nexus between the advertising expenditure and the business of the assessee and that the assessee had to incur such expenditure to meet the competition in the Indian market for selling its products in India. A finding was returned that unless the assessee made its products known to the market, its business would suffer. Consequently, the Tribunal held the entire expenditure on advertising to be of a revenue nature and allowed the same. The Tribunal also noted the decision of the Supreme Court in the case of Empire Jute Co. Ltd. v. CIT (1980) 17 CTR (SC) 113 : (1980) 124 ITR 1 (SC) wherein the Supreme Court held that there could be cases where the expenditure even if it was incurred for obtaining of a benefit of an enduring nature may, nevertheless, be on the revenue account and, in such cases, the test of “enduring benefit” may breakdown.”

18.We find the Hon’ble Delhi High Court in the case of Jubilant Foodwork Pvt. Ltd. (supra) has held that the expenditure incurred by the assessee on advertisement expenses is revenue in nature since no permanent character or advantage is achieved via the same and such expenses for advertising consumer products generally are a part of the process of profit earning and not in the nature of capital outlay. Similar view has been taken by the Hon’ble Delhi High Court in the case of CIT v. Monto Motors Ltd. (supra).

19.In view of the above discussion and in view of the detailed order passed by the CIT(A) on this issue and considering the fact that the Revenue in assessee’s own case for AYs 2010-11 onwards has not considered such AMP expenses as international transaction, therefore, we do not find any infirmity in the order of the CIT(A) in deleting the addition of Rs.31,81,07,110/- on account of adjustment of AMP expenses as computed u/s 92CA(3) of the IT Act.

20.So far as the order of the CIT(A) in restricting the adjustment of Rs.1,47,93,024/- on account of short charge to MMT US for ticketing charges and tours and travel package services to Rs.50,000/- is concerned, we find the ld.CIT(A) while deciding the issue has observed as under:-

“10.0 Finding;

I have carefully gone through various submissions of the appellant. I find force in the appellant’s contention that comparison of gross profit mark ups earned by the appellant from “Ticketing” and “Tour Management Services” rendered to MMT US can not be compared with the corresponding mark ups earned from rendering of similar services to other customers because the efforts made by MMT US for acquisition of customers, marketing and business development expenditure etc and the business risks assumed by MMT US would not be factored in such comparison. If at all this comparison has to be made, then corresponding expenses incurred by MMT US ought to be factored in, as was accepted by my predecessor in appeal for AY 2005-06. The appellant has worked out that approximately 16.44 percent of AE’s operating expenses will be allocated to the appellant since the appellant will receive 16.44 percent of the total gross profit of AE if the TPO’s approach is applied. Accordingly, Rs. 1.474 crores (being 16.44 percent of the AE’s operating expenses amounting to Rs. 8.965 crores) is required to be allocated to the appellant. After such factoring in, the addition to be made on this account would remain Rs.50,000 only as per working furnished by the appellant. Therefore, following the reasoning of then CIT(A) given in appellate order for AY 2005-06, out of Rs 1,47,93,024 added by the AO, addition of only Rs 50,000 is upheld and the balance Rs 1,47,43,024 is deleted. The grounds of appeal no. 3 to 7 are therefore partly allowed.”

21. We do not find any infirmity in the order of the CIT(A) on this issue. We find, while restricting the addition to Rs.50,000/- as against Rs.1,47,43,024//- added by the AO/TPO, he has upheld the order of his predecessor for A.Y. 2005-06. The assessee had also given the break-up on the basis of the finding given by the CIT(A) in A.Y. 2005-06. Nothing substantial was brought to our notice either by the Ld. AR or by the ld. DR against the finding given by the ld.CIT(A) on this issue. We, therefore, uphold the same and the ground raised by the assessee and the Revenue on this issue are dismissed. Accordingly, ground of appeal Nos.1-7 filed by the Revenue and ground No.1 raised by the assessee are dismissed.

7. Respectfully following the order of the Tribunal in asssessee’s own case we reject ground No. 1 to 3 of the revenue’s appeal.

8. Ground No. 4 and 5 are in respect of disallowance made u/s. 40(a)(ia) of the Act on payment to banks for payment gateway charges.

9. The Ld. Counsel for the assessee submitted that these grounds are also covered by the decision of the Tribunal for the A.Y. 2007-08 and 2008-09 in ITA No.2307 and 4757/Del/2013 dated 22.06.2020/Make My Trip (India) (P.) Ltd. v. Dy. CIT (Delhi – Trib.) in para 27 to 34 of the order.

10. The Ld. DR fairly accepted that the issue was decided in favour of the assessee by the Tribunal.

11. Heard rival submissions and perused the orders of the authorities below. In so far ground Nos. 4 and 5 are concerned we observed that the Tribunal in assessee’s own case in ITA No.4757/Del/2013 and in ITA No.4974/Del/2023 for A.Y. 2008-09 by order dated 26.02.2020 decided the issue in favour of the assessee by observing as under :-

ITA No.4757/Del/2013 (By the assessee) & ITA No.4974/Del/2013 (by the Revenue) (Assessment Year: 2008-09) 27.Grounds of appeal of the assessee read as under:-

The appellant respectfully submits as under:

Disallowance under section 40(a)(ia) of the Act of Payment Gateway Charges-

INR 10,93,40,316

1. Under the facts and circumstances of the case and in law, the Ld. CIT (A) erred in upholding the disallowance of INR 10,93,40,316 under section 40(a)(ia) of the Act, being the aggregate amount paid by the Appellant to the banks for availing Payment Gateway facilities.

2. Under the facts and circumstances of the case and in law, the Ld. CIT (A) erred in holding that the amount paid to the banks for availing Payment Gateway facilities, which are standard facilities provided by Banks to its customers, are in the nature of ‘commission or brokerage’ within the meaning of Section 194H of the Act and consequentially TDS should have been deducted on such payments.

3. Under the facts and circumstances of the case and in law, the Ld. CIT (A) has failed to appreciate that the banks in providing Payment Gateway facility, act on Principal to Principal basis with the Appellant and they are neither agent nor do they act on behalf of the Appellant and the provisions of Section 194H of the Act are not applicable.

4. Under the facts and circumstances of the case and in law, the Ld. CIT (A) has failed to appreciate that, CBDT vide Notification No. 56/2012 [F. NO. 275/53/2012-1T(B)] dated December 31, 2012 has notified that no TDS shall be deductible on credit/debit card commission between the merchant and the acquirer bank with effect from January 1, 2013. The Payment Gateway facility charges being similar to credit/debit commission, the aforesaid beneficial notification equally applies to the transactions, prior to the effective date of notification,

5. Under the facts and circumstances of the case and in law, the Ld. CIT (A) failed to appreciate that the Appellant has been making payments to various banks on account of Payment Gateway charges from Financial Year 2000-01 onwards and no adverse inference has been drawn by the Income-tax department in this regard in the past and therefore payment made to banks should not be disallowed following the principles of Hon’ble Mumbai Bench of the Income-tax Appellate Tribunal in the case of CIT v. Kotak Securities Limited (Appeal No 311 of 2009).

The above grounds of appeal are without prejudice to and independent of one another.

The appellant craves leave to add, supplement, amend, vary, withdraw or otherwise modify the grounds mentioned herein above at or before the time of hearing.

The appellant prays for appropriate relief based on the said grounds of appeal and the facts and circumstances of the case.”

27.1 Grounds of appeal filed by the Revenue read as under:-

“1. Whether in the facts and circumstances of the case, the Ld. CIT (A) erred on the facts and circumstances of the case, in accepting the additional evidence u/s 46A when adequate opportunity was already provided to the assessee during the TP/assessment proceeding.

2. The Ld. CIT (A) has erred on the facts and circumstances of the case, in rejecting the Transfer Pricing approach of the TPO.

3. The Ld. CIT (A) has erred on the facts and circumstances of the case, in rejecting the internal comparison made by the TPO, wherein both the segments were involved in similar business.

4. The Ld. CIT (A) has erred on the facts and circumstances of the case, in accepting the Transfer Pricing approach of the assessee.

5. The Ld. CIT (A) has erred on the facts and circumstances of the case, in accepting the additional evidence u/s 46A when adequate opportunity was already provided to the assessee during the TP/assessment proceedings.

6. The Ld. CIT (A) has erred on the facts and circumstances of the case, in concluding MMT to be an Indian brand without appreciating the business model of the assessee.

7. The Ld. CIT (A) has erred on the facts and circumstances of the case, in concluding that the AMP expenditure of the assessee rendered in the nature of service to its AE is not international transaction.

8. The Ld. CIT (A) erred in holding that the assessee was not under an obligation to deduct tax on the payment gateway charges made to Citi Bank and American Express Bank as order u/s 195/197 is valid only for the Indian branches of the above bank and not for the payments received on behalf of the Head Office. The Credit Card Commission payments are not received by the branches of the above bank located at various places in Indian but by the Head Office of the above bank. Hence, the above order is not valid for the payment gateway charges.

9. That the order of the Ld. CIT (A) is erroneous and is not tenable on facts and in law.

10. That the grounds of appeal are without prejudice to each other.

11. The appellant craves leave to add, supplement, amend, vary, withdraw or otherwise modify the grounds mentioned herein above at or before the time of hearing.”

28 .Grounds No.1 to 7 filed by the Revenue are identical to grounds of appeal No.1 to 7 in Revenue’s appeal for A.Y. 2007-08 in ITA No.2692/Del/2013. We have already decided the issue and the grounds raised by the Revenue have been dismissed. Following similar reasonings, the above grounds raised by the Revenue are dismissed.

29 .Grounds No.1 to 5 filed by the assessee and the ground No.8 filed by the Revenue relate to part relief granted by the CIT(A) on account of addition made by the AO for non-deduction of TDS on payment of gateway charges paid to HDFC and ICICI Bank.

30 .Facts of the case, in brief, are that during the course of assessment proceedings, the AO noted that the assessee has claimed bank charges of Rs.12,52,49,946/- in the P&L Account. From the details furnished by the assessee, the AO noted that the assessee has paid the following charges:-

| Nature of Expenses |

Amount (Rs.) |

| Payment of Gateway Charges |

11,99,39,901/- |

| Bank charges – General |

53,10,044/- |

31 .It was further stated that no tax has been deducted on the above two payments on account of the following:-

“1. that the assessee is a e-commence company and is using automated facility to charge a customer through its website using his debit/credit/prepaid card or bank account (Net banking) on-line.

2. that TDS provisions are not applicable to its case.

3. that the services provided by bank do not fall under the definition of ‘Technical Services’ as given in explanation 2 to section 9(l)(vii) of the I.T. Act.

4. that since the services provided by bank do not fall within the purview of technical services as defined in the Income Tax Act, no tax was liable to be deducted on these services.”

32 .Relying on various decisions, it was submitted that neither the provisions of section 194H nor the provisions of section 194J are applicable to the assessee and, therefore, the payment gateway charges are not liable for tax deduction at source either u/s 194H or u/s 194J. However, the AO was not satisfied with the argument advanced by the assessee. Rejecting the various explanations given by the assessee and observing that the payments made to bank in respect of payment gateway services is commission on which tax was liable to be deducted u/s 194H of the IT Act and the AO made an addition of Rs.11,99,39,901/-to the total income of the assessee.

33 .In appeal, the ld.CIT(A) held that the assessee had furnished nil TDS certificate obtained from Citi Bank and American Express Bank u/s 195 of the IT Act. The certificates furnished from Citi Bank and American Express Bank shows that gateway charges were received by the Indian Branches on their own account and payments have been duly declared in their respective return of income only in India. He, therefore, held that the assessee was under obligation to deduct tax while making payment of gateway charges to Citi Bank and American Express Bank. After going through the process involved in payment gateway facility, he held that there is no human intervention involved at the time of clearance of the payments through gateway facility. Following the ratio of the decision in the case of Bharti Cellular Ltd. (supra), he held that no technical services within the meaning of Explanation-2 to section 9(1)(vii) of the Act are provided by the banks when the payment is cleared through gateway facility. He, thereafter, held that the provisions of section 194H would be applicable to payment gateway charges paid to banks. Since the assessee has not made TDS as per provisions of section 194H on these payments, he upheld the action of the AO in disallowing these payments u/s 40(a)(ia) of the Act. He, however, held that payments made to Citi Bank and American Bank are not considered for the purpose of disallowance u/s 40(a)(ia) of the Act. Aggrieved with such order of the CIT(A), both the Revenue and the assessee are in appeal before us.

34 .We have heard the rival arguments made by both the sides and perused the record. It is the submission of the ld. DR that provisions of Explanation (2) to section 195 are applicable to the assessee according to which tax is required to be deducted from any payment made to a non-resident outside India. The assessee has the option to obtain a No-deduction Certificate from the AO which he has not done in the instant case. It is the submission of the ld. Counsel for the assessee that identical issue had come up before the Tribunal in assessee’s own case for A.Y. 2009-10 and the Tribunal, vide order dated 26th September, 2017, has decided the issue pertaining to non-deduction of taxes on payment gateway charges in favour of the assessee with certain directions/observations. Further, the appeal filed by the Revenue was dismissed by the Hon’ble High Court. Under these circumstances and considering the totality of the facts of the case, we deem it proper to restore this issue to the file of the AO with a direction to decide the issue afresh in the light of the decision of the Tribunal in assessee’s own case for A.Y. 2009-10 and decide the issue as per fact and law. Needless to say, the AO shall give due opportunity of being heard to the assessee while deciding the issue. We hold and direct accordingly. The grounds of appeal No.1 to 5 by the assessee and ground of appeal No.8 by the Revenue are accordingly allowed for statistical purposes.

12. respectfully following the said decision we reject the ground Nos 4 and 5 of the revenue’s appeal.

13. Coming to ground No.6 which is in respect of deferred revenue income. We find that the Ld. CIT(A) at pages -48 to 51 and para 25.16 to 26.7 considering the submissions and evidences on record held that based on the agreements entered into by the assessee with various parties and the services rendered proportionately the income was recognized as per accounting standard- 9 and deleted the addition by observing as under :-

24.0 Issue 6-Advance income received from Amadeus of Rs 12,23,95,833 and Apollo DKV Rs 3,18,41,669 taxed in the year of receipt

25.0 Appellant’s Case

25.1 During the year, the Appellant entered into an agreement (‘Amadeus Agreement”) on February 1, 2009 with Amadeus India Pvt. Ltd., India (“Amadeus” or “AIPL”) for obtaining access to and use of internetbased reservation services for airlines and other travel related products and services (Amadeus System/GDS System of Amadeus) which provides travel content including reservation facility on airlines interlaced with MMT’s website.

25.2 During the year, the Appellant has received INR 12,50,00,000 as loyalty signing bonus from Amadeus which is contingent and conditional upon it using the Amadeus System as its exclusive service provider for its reservation business for a period of four years. Also, in the event of termination of the agreement the entire amount of loyalty signing bonus shall be refundable.

25.3 The key conditions of the agreement between Amadeus and the Appellant are as follows:

| • |

|

The Amadeus Agreement has been entered for a period offour years; |

| • |

|

The Appellant has received one time loyalty signing bonus as per clause 6.3 of the Amadeus Agreement for exclusively using the GDS system of Amadeus for the period of four years. |

| • |

|

The Appellant shall solely and exclusively use the GDS system of Amadeus for the period of 4 years. |

| • |

|

The essence of the Amadeus agreement is uninterrupted, continuous and exclusive use of the GDS system of Amadeus for four years with the expected business of sale of 6 million tickets. The agreement also provides for short fall recovery in case MMT books less than 4.5 million segments/tickets during the term of the Amadeus Agreement. |

| • |

|

The loyalty signing bonus is paid in two installments INR 6.25 crores on signing of the Amadeus Agreement and the balance INR 6.25 crores on or before March 31, 2009, subject to the Successful Migration of the Amadeus GDS. Successful Migration of the Amadeus GDS, includes the condition that 100% of the tickets booked through appellant’s website shall be booked through Amadeus GDS on or before March 31. 2009 and for the remainder of the term i.e. till the end of the period of the Amadeus Agreement i.e. till February 28, 2013. Thus the disbursement of installment of loyalty signing bonus subject to fulfillment of above condition is merely timing of payment and cannot be equated to the accrual of income as the obligation against above receipt is to be discharged over a period of 4 years in future. |

| • |

|

If the Amadeus Agreement is terminated the Appellant shall be required to refund the entire one time loyalty signing bonus to Amadeus. |

25.4 As disclosed in the audited financial statements for the year, INR 26,04,167 being the proportionate amount upto March 31, 2009 has been treated as income for the AY 2009-10 by the Appellant and the balance amount INR 12,23,95,833 being the proportionate amount for the unexpired period of the agreement has been treated as current liabilities. The Appellant has included the balance amount of INR 12,23,95,833 as income of the respective Assessment years from AY 2010-11 to AY 2011-12 proportionate to the sale of tickets/ the term of agreement.

25.5 Ld. AO has made an addition of INR 12,23,95,833 being part of amount received from Amadeus, proportionate to the unexpired period of the agreement without appreciating that suc income has not accrued to the Appellant during the current year.

25.6 Similarly, the Appellant has also entered into an agreement with Apollo DKV wherein Appellant undertakes to provide all the commercial assistance and facilities for issuance Apollo’s travel insurance products (policies) to Appellant’s customers through its website which the Appellant has received Rs 4,00,00,000 as sign up fees.

25.7 The key features of the agreement are as follows

| • |

|

The Apollo Agreement has been entered for a period of three years, |

| • |

|

The Appellant has received the signing up fees for issuance of Apollo’s travel Insurance products (policies) to Appellant’s customers through its website, |

| • |

|

The Appellant shall solely and exclusively sell Apollo’s travel insurance products through its website; |

| • |

|

If the Apollo Agreement is terminated, the Appellant shall be required to repay the pro rata sign up fee from the Appellant for the unexpired period. |

25.8 As disclosed in the audited financial statements for the year, INR 8,158,331 being the proportionate amount upto March 31, 2009 has been treated as income for the AY 2009-10 by the Appellant and the balance amount INR 3,18,41,669 being the proportionate amount for the unexpired period of the agreement has been treated as current liabilities. The Appellant has included the balance amount of INR 3,18,41,669 as income of the respective Assessment years.

25.9 The Appellant submitted that as per the provisions of section 5 of the Act, income which accrues to an assessee shall be chargeable to tax in that particular year. An income is said to be accrued when a person acquires a legally vested right in it. It has been held in various case laws that mere receipt of an amount which has not accrued to the assessee in a given assessment year would not be considered as income for the year and cannot be subject to tax.

25.10 The Appellant has relied on the following rulings:

| • |

|

CIT v. Bank of Tokyo (CAL.) |

| • |

|

CIT v. Govind Prasad Prabhunath (171 ITR 417) (Allahabad High Court) |

| • |

|

Amar Nath Khandelwal v. CIT (126 ITR 322) (Delhi) |

| • |

|

ED Sassoon & Co. Ltd. v. CIT (26 ITR 27) (SC) |

| • |

|

CIT v. M/s Shoorji Vallabhadas & Co. (46 ITR 144) (SC) |

| • |

|

Shri Kewal Chand Bagri v. CIT (183 ITR 207) (Calcutta High Court) |

The analysis of the various rulings clearly establishes the following principles on accrual of income :

| • |

|

No sum shall accrue as income until a legally vested right is acquired by the occurrence of all the events on which the remuneration depends. |

| • |

|

Where such consideration is contingent upon the happening of an event, the said consideration would become income of the payee only on the happening of that event and not before. |

| • |

|

If no income has materialized, there can be no liability to tax on a hypothetical income. |

| • |

|

Where the amount is inchoate and has not accrued or crystallized into income, but is only in the process of accrual, the stage of income is not reached. |

25.11 The Appellant submitted that the loyalty signing bonus is contingent upon successful migration to Amadeus GDS which can only be said to have been done when the Appellant makes 100% reservation of tickets through Amadeus GDS for a span of four years upto February 28, 2013. Similarly, in context of the Apollo agreement, the Appellant is required to provide commercial assistance and facilities for issuance of Apollo’s travel insurance products (policies) to Appellant’s customers through its website for a span of 3 years. In light of continuous provision of service by the Appellant a sign up fees of INR 3 crores has been granted to the Appellant.

The aforementioned loyalty signing bonus/sign up fees is repayable on complete/pro rata basis to Amadeus/Apollo on not honoring the conditions of the contract for 4/3 years.

Since the amounts received from Amadeus and Apollo is contingent upon successful migration/rendering of services for a period of 3/4 years, the income cannot be said to have been accrued to the Appellant. Owing to this contingency the Appellant has recognized the receipts from loyalty signing bonus/sign up fee as income over the period of the sole and exclusive contracts with Amadeus and Apollo.

25.12 The Appellant has also placed reliance on Calcutta High Court judgment in the case of CIT v. Bank of Tokyo (supra) wherein deferred guarantee commission received by a bank was spread over the period to which it pertained rather than taxing the same in the year of receipt a done by the AO. Calcutta High Court has observed that in case of receipt of guarante commission for a period shall be spread over the period of the guarantee as full commission though payable at the outset does not crystallise into perfect right to receive so far as unexpired period is related because the payability or receivability from the view of the assessee-bank is Counter-balanced by the refundability, diluting the right to receive into contingent right as regards the unexpired period of the guarantee.

In the given case, the Appellant is in receipt of the loyalty signing bonus/sign up fees which is contingent/conditional upon the fact that the Appellant should continue to use GDS system of Amadeus/exclusively assist in issuance of Apollo’s travel insurance products for the period of 4/3 years. In case of non-compliance with this condition, the Appellant would be required to refund the entire/ pro-rata loyalty signing bonus/sign up fees to Amadeus/Apollo.

25.13 The Appellant also submitted that being a company, it is required to maintain its books of accounts on mercantile basis and is also required to comply with Accounting Standards issued by Institute of Chartered Accountants of India. The loyalty signing bonus received by the Appellant has been recognized in the books of accounts following mandatorily applicable Accounting Standard 9 (‘AS 9’) which provides that when recognition of revenue is postponed due to the effect of uncertainties, it is considered as revenue of the period in which it is properly recognized.

Following the principles of AS 9, the loyalty signing bonus/sign up fees has been spread over the period of the entire agreement with AIPL/Apollo i.e. 4/3 years as per AS 9. Hence, in the case of Amadeus, Rs 2,604,167, being income pertaining to FY 2008-09, was recognised as income during the year and consequently offered to tax. Moreover, in the case of Apollo, Rs 8,158,301 has been offered to tax during FY 2008-09.

The Appellant has also placed reliance on the ruling of ACIT v. ITD Cementation India Ltd, Mumbai ITAT which observed that as per Sec 145(2) any accounting standard notified by the Central Government in Official Gazette was to be mandatorily followed by the respectiva class of the assessee as provided in those standards. AS-7 has not been notified by the Centra Government. However ITAT observed, “But this does not mean that the assessee cannot follo the other Accounting standard issued by ICAL. ICAI being the highest accounting body of country, created by an Act o Parliament, Accounting Standards issued by it cannot be brushed avide lighaly. On the contrary, if a avessee is following the Accounting Standards xwed by ICAL it would give more credibility and authenticity to its account”

25.14 The Appellant submitted that the LAAO has taxed the entire receipt of loyalty signing bonus in the year of receipt alleging that the Appellant has successfully migrated to the GDS system ignoring that successful migration has been defined as 100% reservations through

Amadeus system for the period of 4 years coupled with various other conditions about sale to be achieved during the term of Agreement and subject to the condition of proportionate refund/recovery in case of default/short fall.

25.15 The Appellant also submitted that in case of any cancellation/revocation of the agreement, the entire/pro-rata amount of the bonus was refundable to Amadeus/Apollo DKV.

25.16 The Appellant submitted that, the Appellant had entered into a similar agreement in AY 2008-09 with Abacus wherein a signing bonus of USD 2 million was received by the Appellant against which proportionate amount of INR 4,555,556 was treated as income for AY 2008-09 and balance amount was to be treated as income over the term of the agreement. In AY 2009-10 the agreement with Abacus was terminated, thus the total amount received from Abacus was refunded. On refund of the signing bonus the amount of INR 4,555,556 treated as income in AY 2008-09 was debited to the profit and loss account for AY 2009-10 and claimed as deduction. The Ld.AO accepted the aforesaid system of recognizing income on accrual basis for AY 2008-09 and also allowed the deduction in completing the assessment for AY 200910.

25.17 Further, the Ld. AO has not given any direction for providing any consequential relief in subsequent years wherein the proportionate amount of income has been offered to tax in the respective assessment years by the Appellant.

26.0 Findings:

26.1 I have carefully gone through the submissions made by the Appellant and other material placed on record. My finding in respect of two agreements is as under.

Amadeus Agreement

2.62 From perusal of the Amadeus agreement dated February 1, 2009, it is clear that the Appellant has received the entire amount of loyalty signing bonus during the year. As per clause 4, period of agreement shall be 4 years. As per clause 5.1, the MMT shall use Amadeus GDS as sole and exclusive GDS for its reservations requirements for a minimum period of 4 years. The Appellant has received one time loyalty signing bonus per clause 6 of the Amadeus

Agreement. The loyalty signing bonus is paid in two installments INR 6.25 crores on signing of the Amadeus Agreement and the balance INR 6.25 crores on or before March 31, 2009, subject to the Successful Migration of the Amadeus GDS. Successful Migration of the Amadeus GDS, includes the condition that 100% of the tickets booked through appellant’s website shall be booked through Amadeus GDS on or before March 31, 2009 and for the remainder of the term ie. till the end of the period of the Amadeus Agreement i.e. till February 28, 2013. Further as per clause 9.3, if the Amadeus Agreement is terminated, the appellant shall be required to repay the entire one time loyalty signing bonus to Amadeus. In other words, the loyalty cum signing bonus is contingent/conditional upon the aforementioned conditions,

26.3 The appellant is following the accrual system of accounting and INR 26,04,167 being the proportionate amount upto March 31, 2009 has been treated as income for the AY 2009-10 by the appellant and the balance amount INR 12,23,95,833 being the proportionate amount for the unexpired period of the agreement has been treated as current liabilities. The appellant has included the balance amount of INR 12,23,95,833 as income of the respective Assessment years from AY 2010-11 to AY 201112 proportionate to the sale of tickets/the term of agreement.

26.4 It is seen that the entire amount of loyalty signing bonus received by the Appellant in AY 2009-10 as per the agreement is subject to condition of exclusive & continuous use of GDS system of Amadeus over the term of agreement which is 4 years and also linked to sale of certain number of ticket’s over the period of the agreement. It is well established that the advance receipts cannot partake the character of income till the happening of the underlying contingency or conditions subject to which such amounts were received. Further, the agreement clearly provides for refund of entire amount of loyalty signing bonus in the event of breach of any of the above conditions of the agreement. The Appellant has also consistently followed the accrual basis of accounting in recognizing such income over the period of the agreement in case of Abacus which has been accepted by the department in the past. Further, it is undisputed that the amount is taxable. The only issue involved is timing of taxation. In view of these facts, I hold that the balance amount of INR 12,23,95,833 being a proportionate amount for the unexpired period of the agreement is not in the nature of accrued income for AY 2009-10. The amount of loyalty signing bonus is to be treated as income over the period of the agreement and happening of the conditions subject to which such amounts were received. The Appellant has correctly offered INR 26,04,167 as income for AY 2009-10 and the balance amount of INR 12.23.95,833 has been included as income for subsequent AYs. As a result, the addition made by the AO of INR 12,23,95,833 stands deleted.

Apollo DKV Agreement

26.5 As per Apollo DKV agreement dated April 30, 2008, the Appellant has received the amount to provide all the commercial assistance and facilities for issuance of Apollo’s travel insurance products (policies) to Appellant’s customers through its website for a period of 3 years. The sign up fees has been received subject to the following conditions:

| • |

|

The Apollo Agreement has been entered for a period of three years; |

| • |

|

The Appellant has received the signing up fees for issuance of Apollo’s travel insurance products (policies) to Appellant’s customers through its website, |

| • |

|

The Appellant shall solely and exclusively sell Apollo’s travel insurance products through its website; |

| • |

|

If the Apollo Agreement is terminated the Appellant shall be required to repay the pro-rata sign up fee from the Appellant for the unexpired period. |

| • |

|

As per clause 12 of the agreement, in case of noncompliance with any of the conditions as mentioned above, the pro rata amount of the sign up fees shall be refundable to Apollo. In other words, the sign up fees is contingent/conditional upon the aforementioned conditions. |

26.6 The Appellant is following the accrual system of accounting and INR 8,158,331 being the proportionate amount upto March 31, 2009 has been treated as income for the AY 2009-10 by the Appellant and the balance amount out of INR 3,18,41,669 being the proportionate amount for the unexpired period of the agreement has been treated as current liabilities. The Appellant has included the balance amount of INR 3,18.41,667 as income of the subsequent respective Assessment years.

26.7 It is seen that the entire amount of sign up fee received by the Appellant in AY 2009-10 as per the agreement is subject to condition of solely and exclusively selling Apollo’s travel Insurance products through its website over the term of agreement for a period of 3 years. It is well established that the advance receipts cannot partake the character of income till the happening of the underlying contingency or conditions subject to which such amounts were received. Further, the agreement clearly provides for refund of pro rata amount of sign up fee in the event of breach of any of the above conditions of the agreement. The material facts in case of this agreement are essentially similar to those in case of Amadeus agreement. Accordingly. I hold that the balance amount of INR 3,18,41,669 being a proportionate amount for the unexpired period of the agreement is not in the nature of accrued income for AY 2009-10. The amount of sign up fee is to be treated as income over the period of the agreement and happening of the conditions subject to which such amounts were received. The Appellant has correctly offered INR 8,158,331 as income for AY 2009-10 and the balance amount of INR 3,18,41,669 has been included as income in subsequent Assessment years. Therefore, the addition made by the AO of INR 3,18,41,669 stands deleted.

14. On careful perusal of the order of the Ld. CIT(A) we do not find any infirmity in the order passed by the Ld.CIT(A).

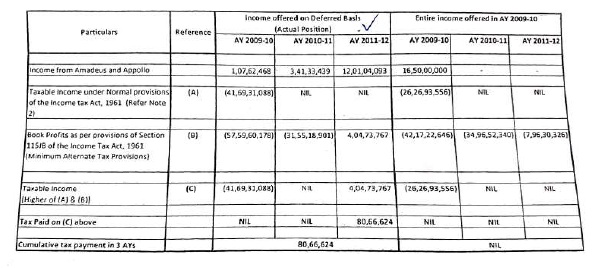

15. We further find the impact on taxes if entire income received from Amadeus and Apollo is recognized in A.Y. 2009-10 viz-a-viz recognized on deferred basis in subsequent years would be as under :-

16. As could be seen from the above table as a matter of fact when the income is offered on deferred basis based on actual position of rendering of services during each assessment years the assessee ended up paying taxes in the assessment year 2011-12. However, if the entire income is offered to tax in the assessment year 2009-10 it would result in loss due to set off of losses.

17. Coming to ground No.7 of grounds of appeal which in respect of disallowance u/s. 40(a)(i) for non deduction of TDS on reimbursement of ticketing cost we find that the Ld. CIT(A) at page -27 held that provisions of section 195 are not applicable to the said transaction as the payment made for purchase of ticketing cost by the assessee to MMT US is not chargeable to tax in India and therefore, no tax is deductable u/s. 195 of the Act as under :-

“27.0 Issue 7 Non-deduction of TDS on Purchase of International Air Tickets (INR 33,32,45,829)

28.0 Appellant’s Case

28.1 During the year, the Appellant purchased air tickets amounting to INR 33,32,45,829 for sale to third party customers. These tickets were purchased by the appellant through its Group Company, Make My Trip Inc. (‘MMT US’) and subsequently such amounts were paid to MMT US for onward payment to the respective foreign airlines.

28.2 The cost of air tickets amounting to INR 33,32,45,829 was collected by MMT US from the appellant on behalf of foreign airlines and passed on at actual to the foreign airlines. In effect, the amount of INR 33,32,45,829 represents income of foreign airlines towards sale of air tickets to third party customers in US. The Appellant submits that the typical arrangement for tickets purchased by a US customer for travelling to India is as follows:

28.3 The flow of transaction is as follows:

| • |

|

Customers in the US, when log in for online purchase of tickets, get access to the MMT US website. |

| • |

|

When tickets are purchased by such customers the revenue is received by MMT India directly through online banking channel and the ticket gets issued though MMT US. |

| • |

|

MMT India includes the net amount of income, being amount of revenue collected less cost of tickets paid to MMT US as net income, being the commission income of sale of tickets to customers in US from sale of such tickets. |

| • |

|

As the revenue is received by MMT India the cost of tickets issued to customers in US which tantamount to purchase of such tickets by MMT India is also required to be accounted for by MMT India. |

| • |

|

As the tickets have been booked through MMT US, MMT India pays the cost of tickets to MMT US which in turn is passed on by MMT US to the foreign airlines |

| • |

|

MMT US is separately compensated by ticketing service fees of 2% of the ticket cost for purchase of tickets. |

28.4 MMT US acts as an agent of foreign airlines while selling tickets on behalf of such foreign airlines to be sold to third party customers in US. In effect, the amount of INR 33,32,45,829 represents income of foreign airlines in respect of sale of air tickets to think party customers in US.

28.5 The Ld.AO has disallowed the entire amount of INR 33,32,45.829 being purchase cost of tickets of foreign airlines purchased through MMT US alleging it is Fees for Technical Services (‘FTS’) and stating that TDS should have been deducted and disallowed the purchase cost of tickets invoking section 40(a)(1) of the Act.

28.6 The Appellant has contended that no tax is deductible on purchase cost of airline tickets as the payment of Rs 33,32,45,829 to MMT US is towards cost of airline tickets purchased and does not amount to FTS under the Act or FIS under DTAA with USA.

28.7 Appellant contended that the expression Fee for technical services [FTS] for the purpose of taxability under section 9(1)(vii) of the Act, has been defined as follows:

Explanation-For the purposes of this clause, “fees for technical services” means any consideration (including any lump sum consideration) for the rendering of any managerial, technical or consultancy services (including the provision of services of technical or other personnel) but does not include consideration for any construction, assembly, mining or like project undertaken by the recipient or consideration which would be income of the recipient chargeable under the head “Salaries”.

In the given case, the transaction involves mere purchase of air tickets to be sold to the third party customers. There is no element of services involved in the given transactions, leave alone managerial, technical or consultancy services while purchasing these air tickets.

Further, provisions of explanation to section 9(2) of the Act, introduced by the Finance Act 2007 are as follows:

For the removal of doubts, it is hereby declared that for the purposes of this section, where income is deemed to accrue or arise in India under clauses (v), (vi) and (vii) of sub-section (1), such income shall be included in the total income of the nonresident, whether or not the non-resident has a residence or place of business or business connection in India

The Appellant submitted that while relying upon the above amendment, the Ld.AO failed to appreciate the fact that even before the idea of considering a transaction chargeable to tax under section 9(1)(vii) can be conceived, the transaction in question has to qualify as managerial, technical or consultancy services which is not possible in case of mere purchase of air tickets.

28.8 The Appellant also contended that purchase of tickets cannot be considered as FIS under the India US DTAA as ticket cost purchase does not satisfy the “Make Available’ condition in the Restrictive FIS definition in the India-US DTAA. The definition of FIS as per Article 12 of India-USA DTAA is as follows:

For purposes of this Article, “fees for included services” means payments of any kind to any person in consideration for the rendering of any technical or consultancy services (Including through the provision of services of technical or other personnel) if such services:

(a) are ancillary and subsidiary to the application or enjoyment of the right, property or information for which a payment described in paragraph 3 is received; or

(b) make available technical knowledge, experience, skill, know-how, or processes, or consist of the development and transfer of a technical plan or technical design.

The meaning of ‘make available’ has been interpreted by Memorandum to the India-USA DTAA and various judicial authorities. The MOU states as follows

“Generally speaking, technology will be considered ‘made available’ when the person acquiring the service is enabled to apply the technology. The fact that the provision of the service may require technical input by the person providing the service does not per se mean that technical knowledge, skills, etc., are made available to the person purchasing the service, within the meaning of paragraph 4(b). Similarly, the use of a product which embodies technology shall no per se be considered to ‘make the technology available”.

This view also gets support from numerous judgments from various judicial authorities:

| • |

|

Cushman and Wakefield Pre Lad (305 ITR 208 (AAR)) |

| • |

|

Anapharm Inc [2008] 305 ITR 394 (AAR) |

| • |

|

Intertek Testing Services India Pvt. Ltd. [2008] 307 ITR 418 (AAR) |

| • |

|

CESC Lid v DCIT (2003) 87 ITD 653 |

| • |

|

Ernst & Young (P) Ltd [2010] 230 CTR 355 (AAR) |

| • |

|

Worley Parsons Services (Private) Limited 313 ITR 74 (AAR) |

| • |

|

Raymond Lid v. Deputy CIT (86 ITD 791, Mumbai ITAT) |

| • |

|

Cable and Wireless Networks India (P) Ltd., In re.n m(AAR) |

| • |

|

Bharati AXA General Insurance Co Ltd vx. DIT 845 of 2009 (AAR) |

| • |

|

R.R. Donelley India Outsource Private Lid (AAR) |

| • |

|

Guy Carpenter & Co. Lid. v. ADIT [2011-T11-190-ITAT-DEL -INTL) |

| • |

|

DCIT v. Dr. Reddy’s Laboratories Limited [ITA No. 867 & 868/Hyd/03) (Hyderabad ITAT) |

| • |

|

ITO v. Veeda Clinical Research Pvt. Lid. [2013] [ITA No. 1406/Ahd/2009) (Ahmedabad ITAT) |

In the given set of facts, there is no acquiring or application of technical know-how, skill etc. MMT US acts as a mere agent on behalf of the airlines for issuing tickets to third party customers of the Appellant. Hence, the payments made by the Appellant to MMT US for cost of tickets purchased does not fall within the purview of FIS as contemplated by Article 12 of the India-USA DTAA. Accordingly, no TDS is deductible on payments made by the Appellant to MMT US under section 195 of the Act.

28.9 Appellant has also contended that MMT US does not have any PE in India, thus even business income of MMT US is not taxable in India under the India US DTAA.

28.10 Alternatively, the Appellant has also contended that MMT US is just a commission agent; ticket income is the income of Foreign Airlines which is not chargeable to tax in light of the provisions of Article 8 of the US Treaty. A separate service income of INR 66,57,356 has been paid to MMT US by the Appellant for such tickets.

28.11 Hence, in the given case, as there is no income chargeable to tax in India, the Appellant submitted that there is no liability to deduct TDS u/s 195 of the Act on payments amounting to INR 33,32,45,829 in respect of sale of air tickets to third party US customers. The Appellant also contended that the judicial principles laid down by the Apex Court in the case of GE India Technology Centre Private Limited v. CIT (327 ITR 456) have been completely disregarded as no disallowance can be made on account of non-deduction of tax under section 195 of the Act, when the amount is not chargeable to tax in India in the hands of the recipient in the first place.

29.0 Findings:

29. 1 I have considered the elaborate submissions of the Appellant. From the facts stated above it is clear that the customers in the US, when log in for online purchases of tickets, get access to the MMT US website. Accordingly, when tickets are purchased by such customers, the revenue is received by MMT India directly through online banking channel and the ticket gets issued though MMT US. As the revenue is received by MMT India, the cost of tickets issued to customers in US which tantamount to purchase of such tickets by MMT India is also required to be accounted for by MMT India.

29. 2 Consequently, MMT India paid Rs 33,32,45,829 during AY 2009-10 to MMT US for tickets purchased on cost to cost basis. In addition to the said cost of tickets small amount of ticketing services charges of Rs 66,57,356 was paid to MMT US separately. MMT India has included the net amount of income being amount of revenue collected less cost of tickets paid to MMT US as net income being the commission income of sale of tickets to customers in US from sale of such tickets.

29. 3 As per provisions of section 195 of the Act, any person responsible for making a payment to a nonresident which is chargeable to tax in India is required to withhold tax at the time of payment of such sum or credit of that sum to the account of the non-resident, whichever is earlier. The issue to be decided in present case is whether the payment made by the appellant to MMT US towards cost of tickets is taxable in India as FTS/FIS.

29. 4 The expression ‘Fee for technical services’ [FTS] is defined in Explanation 2 to section 9(1)(vii) of the Act as a consideration for rendering any managerial, technical or consultancy services. Services can be considered of a ‘technical’ nature only when some special skill or knowledge related to a technical field is required for the provision of the services. Mere use of technology in providing a service may not be indicative of whether the service is of a technical nature or not. Further, the expression ‘consultancy service’ means services of advisory nature provided by a professional expert. In the given case, the transaction involves mere hooking of air tickets by MMT US to be sold to the third party customers of the appellant. Mere purchase of tickets does not involve any service element. The AO has also relied upon the amended explanation to section 9(2) wherein it has been provided that the services shall qualify as FTS irrespective of the fact whether the service provider has a residence or place of business in India. The AO has not appreciated the fact that even before the idea of considering a transaction chargeable to tax u/s 9(2) can be conceived, the transaction in question has to qualify as managerial, technical or consultancy services which is not possible in case of mere purchase of air tickets.

29. 5 Further, payment of cost of tickets by the Appellant can not be considered as FIS under Article 12(4) of the India-USA DTAA. In present case, simple purchase of air tickets does not entail acquiring or application of technical know-how, skill etc. MMT US is in business of booking tickets and acts as a mere agent on behalf of the airlines for issuing tickets to third party customers of the Appellant. No technical or consultancy service is being provided in the process. Further, even if it is assumed that there is any element of technical or consultancy service, “make available clause needs to be satisfied. From conduct of the parties concerned, it can not be said that these is transfer of any technical knowledge, experience, skill, know-how, or processes from MMT US to the appellant.

29. 6 Impugned payments in hands of MMT US are undoubtedly in nature of business income which is not taxable in India as MMT US does not have PE in India.

29. 7 In light of the discussion above, I hold that the payment made for purchase of ticket cos by the appellant to MMT US is not chargeable to tax in India in the hands of MMT US and r tax is deductible u/s 195 of the Act on such payments made by the appellant to MMT US. Hen no disallowance u/s 40(a)(i) of the Act is warranted in this case. Thus, the addition made by the AO of INR 33,32, 45, 829/ stands deleted. Hence, ground 39 to 46 are decided in favour of the appellant.

18. On careful perusal of the order of the Ld. CIT(A) we do not see any valid reason to disturb the findings of the Ld. CIT(A). Ground No.7 of appeal is dismissed.

19. In the result, the appeal of the revenue is dismissed.

ITA No.989/Del/2017 for A.Y. 2011-12

20. Coming to assesee’s appeal for the A.Y.2011-12, the assessee has raised following grounds of appeal :

1. That on the facts and circumstances of the case and in law, the order passed by the Ld. The CIT(Appeals) is erroneous to the extent it upholds the additions/ disallowance made by Ld. DY. Commissioner of Income Tax (‘Ld. AO’) in the assessment order.

Disallowance on account of rate of depreciation on computer peripherals.

2. That on the facts and circumstances of the case and in law, Ld. CIT (Appeals) erred in upholding a partial disallowance of depreciation on computer peripherals, by allowing depreciation at the rate of 15 per cent as “Plant and Machinery” instead of 60 per cent as “Computers including computer software” claimed by the Appellant on certain additions to depreciable assets made during the year.

3. That on the facts and circumstances of the case and in law, Ld. CIT (Appeals) erred in directing the Ld. AO to identify items like digital call logger board, soft protection, Nortel equipment, headsets, time attendance system etc. and holding that same are eligible for depreciation @ 15 per cent on a premise that these items do not qualify as computer peripherals.

Advertisement and publicity expenses amounting to Rs. 271,000,394.

4. That on the facts and circumstances of the case and in law, Ld. CIT (Appeals) erred in holding that a portion of Advertisement and publicity expenditure, amounting to Rs. 271,000,394 (out of total Advertisement and publicity expense of Rs. 577,466,196), are for generating enduring benefits to the Appellant.

5. That on the facts and circumstances of the case and in law, Ld. CIT (Appeals) erred in not appreciating the fact that the above “Advertisement and Publicity expenditure of Rs. 271,000,394 were incurred in the normal course of business of the Appellant and allowable under section 37 of the Act.

6. That on the facts and circumstances of the case and in law, the Learned CIT(A) has erred in upholding the levy of interest under section 234D of the Act and withdrawal of interest under section 244A of the Act.

The above, grounds of appeals are without prejudice to and independent of one another.

The appellant craves leave to add, to amend, modify, rescind, supplement or alter any of the grounds stated herein above, either before or at the time of hearing of this appeal.

The appellant prays for appropriate relief based on the said grounds of appeal and the facts and circumstances of the case.