ORDER

Ms. Padmavathy S, Accountant Member.- These cross appeals by the revenue and the assessee for Assessment Years (AY) 2017-18 & 2018-19 and the appeals of the revenue for AY 2014-15 to 201617 are against the separate orders of the Commissioner of Income Tax (Appeals) / National Faceless Appeal Centre, Delhi, [In short ‘CIT(A)’] passed under section 250 of the Income Tax Act, 1961 (the Act) dated 26.06.2023 for (AY) 2014-15, dated 19.06.2023 for AY 2015-16 & 2016-17, dated 11.07.2023 for 2017-18 & 2018-19. The common issues contended by the assessee and revenue in all these appeals are listed as under:

Revenue’s Appeal — Issues contended

| (i) |

|

Learned Commissioner of come Tax (Appeals) erred in deleting the addition made by the A.O. u/s 36(1)(vii) without considering the fact that assessee has been allowed deduction u/s. 36(1)(viia)(c) and assessee has credit balance in provision for bad a doubtful account allowed us. 36(1)(viia) (c) of the Act. – AY 2014-15, AY 2015-16, AY 2016-17, AY 2017-18 and AY 2018-19 |

| (ii) |

|

Learned Commissioner of Income Tax (Appeals) erred in directing the learned Assessing Officer to restrict the disallowance us. 14A, relying upon the Judgement of the case pertaining to the A.Y. 2004-05, ignoring the fact that during the current A. Y provisions of Rule 8D are applicable. – AY 2014-15, AY 2015-16, AY 2016-17, AY 2017-18 and AY 2018-19 |

| (iii) |

|

Learned Commissioner of Income Tax (Appeals) was not justified in allowing the appeal of the assessee on the issue of claim of deduction u/s. 36(1) (viii) without appreciating that deduction has been calculated after making deductions under all other clauses of section 36(1) which includes the claim of deductions u/s 36(1) (viia)(c) also. – AY 2016-17, and A Y 2017-18 |

Assessee’s Appeal — Issues contended

| (i) |

|

Learned CIT(A) has erred in confirming the disallowance u/s. 14A of the Income Tax Act, 1961 to the extent of an adhoc amount over and above the disallowance made by the assessee – AY2014-15, AY2015-16, AY2016-17, AY2017-18 and AY 2018-19 |

| (ii) |

|

Learned CIT (A) has erred in confirming the action of Learned assessing officer in disallowing the claim of proportionate amortized amount of lease premium paid to MMRDA in respect of leasehold land. – AY 2017-18 and AY 2018-19 |

2. Since the issues contended are common across all these appeals they are heard together and disposed of by this common order. For the purpose of adjudication, we will consider the appeal for AY 2016-17 as lead case.

3. The assessee is a company functioning as Principal Financial Institution for promotion, financing and development of Micro, Small & Medium Enterprises and to co-ordinate the functions of Institutions engaged in similar activities. The assessee filed the return of income for AY 2016-17 on 29.09.2016 declaring a total income of Rs. 1552,64,02,200/- under the normal provisions of the Act and book profit of Rs. 1861,94,44,229/- under section 115JB of the Act. The case was selected for scrutiny and the statutory notices were duly served on the assessee. The Assessing Officer (AO) made the following disallowance while assessing the income at Rs. 1646,52,55,744/- under the normal provision of the Act and recomputed the book profit after adjusting the disallowance under section 14A of the Act at Rs. 1867,45,30,421/-.

| (i) Disallowance to bad-debts u/s 36(1)(vii) – Rs. |

84,46,95,341/- |

| (ii) Disallowance of amortized rent – Rs. |

60,79,783/- |

| (iii) Disallowance under section 14A – Rs. |

5,50,86,192/- |

| (iv) Restricting the deduction claimed u/s 36(1)(viii) to Rs. |

71,75,94,432/- |

4. Aggrieved assessee filed further appeal before the CIT(A). The CIT(A) gave relief to the assessee with respect to disallowance made towards bad-debts under section 36(1)(vii) and towards restricting the deduction under section 36(1)(viii). With regard to the disallowance made under section 14A, the CIT(A) gave partial relief to the assessee by upholding the disallowance to the extent of Rs. 50,00,000/-. The CIT(A) rejected the contentions of the assessee with regard to the amortization of rent claimed on the leasehold land towards premium paid to MMRDA. Both the assessee and the revenue are in appeal against the order of the CIT(A) before the Tribunal.

Disallowance of deduction under section 36(1)(vii)

5. During the year under consideration, the assessee has claimed bad-debts amounting to Rs. 175,65,10,683/- under section 36(1)(vii) r.w.s. 36(2) of the Act. The assessee also claimed an amount of Rs. 81,73,55,929/- as provision for doubtful debts under section 36(1)(viia)(c) of the Act at 5% of total income. The AO held that the claim of bad-debts under section 36(1)(vii) is subject to the restriction as per the proviso to the said section where it cannot exceed the credit balance in the provision for bad & doubtful debits under section 36(1)(viia). The AO noticed that the assessee in the AY 2015-16 has claimed a deduction of Rs. 84,46,95,341/- under section 36(1)(viia)(c) and therefore held that the said amount ought to have been carried as credit balance in the current AY i.e. AY 2016-17. The AO accordingly disallowed deduction claimed to the extent of. Rs. 84,46,95,341/- stating that the bad-debts claimed should be reduced to the extent of the credit balance as per the proviso to section 36(1)(vii). The CIT(A) deleted the addition made by the AO by placing reliance on the decision of the Co-ordinate Bench in assessee’s own case for AY 2005-06 Small Industries Development Bank of India v. Addl. CIT [IT Appeal No. 4046(Mum) of 2011, dated 25-09-2018 ].

6. The ld. DR submitted that the CIT(A) has not factually examined the impugned issue but has simply followed the earlier years decision of the Tribunal to allow the claim of the assessee. Accordingly, the ld. DR supported the order of the AO.

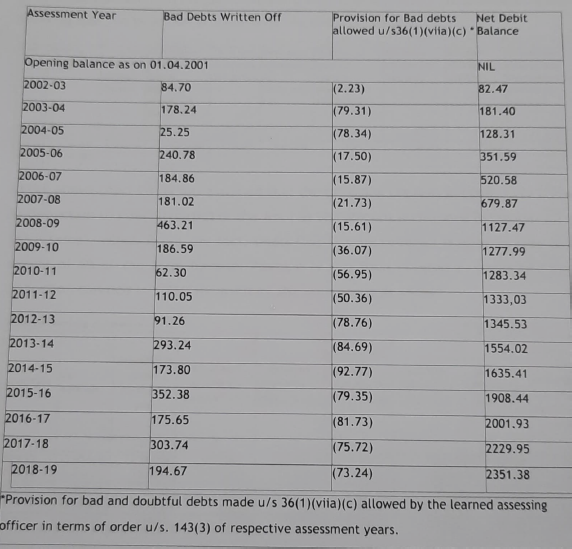

7. The ld. AR on the other hand submitted that the impugned issue has been consistently held in favour of the assessee by the Co-ordinate Bench from AY 2004-05 and that the Department has not preferred further appeal against the order of the Tribunal. The ld. AR accordingly submitted that the issue has reached finality. The ld. AR on merits submitted that the ground on which the AO made the disallowance is that the bad-debts claimed under section 36(1)(vii) cannot exceed the credit balance in the provision for bad and doubtful debts under section 36(1)(viia)(c) of the Act. The ld. AR further submitted that the assessee in earlier years has established the fact that there is no credit balance in the provisions account and therefore the question of applying the proviso to section 36(1)(vii) does not arise. In this regard the ld. AR drew our attention to the following table which includes the details pertaining to the year under consideration also –

8. We heard the parties and perused the material on record. We notice that the Co-ordinate Bench in assessee’s own case for AY 2004-05 Dy. CIT v. Small Industries Development Bank of India [IT Appeal No. 7143(Mum)2008 dated 15-02-2012 ] has considered the identical issue where it has been held that

“28. Even on merits of the claim of the Assessee, we are of the view that the same deserves to be accepted. The relevant provisions under which the deduction has been claimed by the Assessee are as follows:

36. Other deductions (1) The deductions provided for in the following clauses shall be allowed in respect of the matters dealt with therein, in computing the income referred to in section 28-

(vii) subject to the provisions of sub section (2), the amount of any bad debt or part thereof which is written off as irrecoverable in the accounts of the assessee for the previous year:

Provided that in the case of a bank to which clause (viia) applies, the amount of the deduction relating to any such debt or part thereof shall be limited to the amount by which such debt or part thereof exceeds the credit balance in the provision for bad and doubtful debts account made under that clause;

(viia) in respect of any provision for bad and doubtful debts made by-faj a scheduled bank not being a bank incorporated by or under the laws of a country outside India or a non-scheduled bank, an amount not exceeding five per cent, of the total income (computed before making any deduction under this clause and Chapter (VIA) and an amount not exceeding ten per cent, of the aggregate average advances mode by the rural branches of such bank computed in the prescribed manner:

From a reading of the aforesaid provisions, it would be clear that the Assessee is thus entitled to claim deduction both under Sec. 36(l)(vii) and Sec, 36(l)(viia) of the Act. The only limitation is that the amount of deduction shall not exceed the amount by which such debt or part thereof exceeds the credit balance in the provision for bad and doubtful debts account. In the present case there is no dispute that provisions of Sec. 36(1)(viia) applies to the Assessee and also the fact the amount of deduction relating to bad debts written off is limited to the amount by which such debt or part thereof exceeds the credit balance in the provision for bad and doubtful debts account. In the case of the Assessee there is no dispute that there was no credit balance in the provision account and therefore whole of the bad debts written off would in effect be in excess of the credit balance (which is nil) in provisions account. Therefore, the whole of the bad debts written off would be deductible u/s.36(1) (vii) of the Act. The fact that this sum has been omitted to be claimed in the return of income has been amply demonstrated by the Assessee. Even in the reassessment proceedings the AO has no answer to the claim of the Assessee in this regard and has merely observed in his order that there is no evidence produced by the Assessee. The book entries and the return of income before the AO are enough evidence to come to the conclusion that the amount in question was not claimed in the return of income though the Assessee could have claimed it legitimately. In the given circumstances, we are of the view that there is no merit in the ground raised by the Revenue. Consequently, the ground of appeal of the revenue is dismissed and the order of CIT(A) in this regard is upheld.”

9. The interplay between the deduction claimed under section 36(1)(vii) and 36(1)(viia) has been explained by the Hon’ble Supreme Court in the case of Catholic Syrian Bank Ltd. v. CIT ITR 270 (SC). The relevant observations are extracted below –

” Under Section 36(1)(vii) of the ITA 1961, the tax payer carrying on business is entitled to a deduction, in the computation of taxable profits, of the amount of any debt which is established to have become a bad debt during the previous year, subject to certain conditions. However, a mere provision for bad and doubtful debt(s) is not allowed as a deduction in the computation of taxable profits. In order to promote rural banking and in order to assist the scheduled commercial banks in making adequate provisions from their current profits to provide for risks in relation to their rural advances, the Finance Act, inserted clause (viia) in subsection (1) of Section 36 to provide for a deduction, in the computation of taxable profits of all scheduled commercial banks, in respect of provisions made by them for bad and doubtful debt(s) relating to advances made by their rural branches. The deduction is limited to a specified percentage of the aggregate average advances made by the rural branches computed in the manner prescribed by the IT Rules, 1962. Thus, the provisions of clause (viia) of Section 36(1) relating to the deduction on account of the provision for bad and doubtful debt(s) is distinct and independent of the provisions of Section 36(1)(vii) relating to allowance of the bad debt(s). In other words, the scheduled commercial banks would continue to get the full benefit of the write off of the irrecoverable debt(s) under Section 36(1)(vii) in addition to the benefit of deduction for the provision made for bad and doubtful debt(s) under Section 36(1)(viia). A reading of the Circulars issued by CBDT indicates that normally a deduction for bad debt(s) can be allowed only if the debt is written off in the books as bad debt(s). No deduction is allowable in respect of a mere provision for bad and doubtful debt(s). But in the case of rural advances, a deduction would be allowed even in respect of a mere provision without insisting on an actual write off. However, this may result in double allowance in the sense that in respect of same rural advance the bank may get allowance on the basis of clause (viia) and also on the basis of actual write off under clause (vii). This situation is taken care of by the proviso to clause (vii) which limits the allowance on the basis of the actual write off to the excess, if any, of the write off over the amount standing to the credit of the account created under clause (viia). However, the Revenue disputes the position that the proviso to clause (vii) refers only to rural advances. It says that there are no such words in the proviso which indicates that the proviso apply only to rural advances. We find no merit in the objection raised by the Revenue. Firstly, CBDT itself has recognized the position that a bank would be entitled to both the deduction, one under clause (vii) on the basis of actual write off and another, on the basis of clause (viia) in respect of a mere provision. Further, to prevent double deduction, the proviso to clause (vii) was inserted which says that in respect of bad debt(s) arising out of rural advances, the deduction on account of actual write off would be limited to the excess of the amount written off over the amount of the provision allowed under clause (viia). Thus, the proviso to clause (vii) stood introduced in order to protect the Revenue. It would be meaningless to invoke the said proviso where there is no threat of double deduction. In case of rural advances, which are covered by the provisions of clause (viia), there would be no such double deduction. The proviso limits its application to the case of a bank to which clause (viia) applies. Clause (viia) applies only to rural advances. This has been explained by the Circulars issued by CBDT. Thus, the proviso indicates that it is limited in its application to bad debt(s) arising out of rural advances of a bank. It follows that if the amount of bad debt(s) actually written off in the accounts of the bank represents only debt(s) arising out of urban advances, the allowance thereof in the assessment is not affected, controlled or limited in any way by the proviso to clause (vii)”

10. From the above observations of the Hon’ble Supreme Court, it is clear that the assessee is entitled to claim of deductions under both the sections i.e. section 36(1)(vii) and section 36(1)(viia). However, the legislature wanted to restrict the claim of deduction towards bad-debts so that it does not exceed the provision made towards bad and doubtful debts and the same is achieved by the proviso to section 36(1)(vii). It is relevant to notice that the restriction under the proviso is to be applied by comparing the actual bad-debts claimed under section 36(1)(vii) with the provision made and claimed under section 36(1)(viia)(c) so that there is no double deduction claimed by the assessee in an AY. In assessee’s case from the perusal of the table containing details of bad debts under section 36(1)(vii) and provision for bad and doubtful debts under section 36(1)(viia)(c) claimed in various AYs including the year under consideration (refer table extracted in the earlier part of this order), we see merit in the claim of the assessee that the deduction claimed under section 36(1)(vii) is not in excess of the credit balance in the provision account. Further in assessee’s case from the perusal of the table above it is clear that there is no duplication of claim between deduction under section 36(1)(vii) and section 36(1)(viia) and this fact has been consistently confirmed by the orders of the coordinate bench in assessee’s case. Accordingly, we hold that there is no infirmity in the decision of the CIT(A) in allowing the issue in favour of the assessee by following the decision of the Co-ordinate Bench in assessee’s own case for earlier years.

Disallowance under section 14A

11. The assessee during the year under consideration has earned exempt income from dividend, tax free bonds and Long Term Capital Gains (LTCG). The assessee in the computation has made a suo-motu disallowance of Rs. 1,16,75,281/- under section 14A of the Act towards administrative expenditure on pro-rata basis of number of employees in the Investment Department vis-a-vis the total number of employees. The AO held that the assessee has not maintained separate set of account with regard to the exempt income / the expenditure attributable to earning of such exempt income. The AO further held that the assessee has disallowed on estimation basis and not on actual basis which is not acceptable. Accordingly the AO considered 0.5% of the investments earning exempt income to make a disallowance of Rs. 5,50,86,192/- after reducing the suo-motu disallowance made by the assessee. On further appeal the CIT(A) upheld the disallowance to the extent of adhoc amount of Rs. 50,00,000/-. Both the assessee and the revenue are contesting the decision of the CIT(A).

12. The ld. AR submitted that the AO has not recorded dissatisfaction with respect to the books of accounts and therefore the disallowance without recording satisfaction by the AO is not tenable. The ld. AR further submitted that the assessee has computed the suo-motu disallowance based on a scientific method which has been consistently followed by the assessee. The ld. AR relied on the decision of the Co-ordinate Bench in assessee’s own case for AY 2008-09 Small Industries Development Bank of India v. Addl. CIT [IT Appeal No. 3708(Mum) of 2012, dated 23-03-2018 ] where it has been held that

“46. We have carefully considered the rival submissions. In this case, the dispute between the assessee and the Revenue pertains to the quantification of disallowance envisaged u/s 14A of the Act. Pertinently, Sec. 14A of the Act prescribes that no deduction shall be allowed in respect of expenditure incurred by the assessee in relation to an exempted income, i.e., an income which does not form part of the total income under the Act. Sec. 14A(2) of the Act empowers the Assessing Officer to determine the amount of expenditure incurred in relation to the exempt income in accordance with such method as may be prescribed, which is contained in Rule 8D of the Rules. In the present case, the Assessing Officer has applied Rule 8D(2)(iii) of the Rules to determine the amount of such administrative/overhead expenditure. However, the case set-up by the assessee is that resort to Rule 8D(2)(iii) of the Rules by the Assessing Officer is circumscribed by a caveat in Sec. 14A(2) of the Act itself. The phraseology of Sec. 14A(2) of the Act itself prescribes that resort to Rule 8D of the Rules can be made only if the Assessing Officer is not satisfied with the correctness of the claim of assessee in respect of such expenditure, having regard to the accounts of the assessee. Notably, in the present case, assessee has made a suo moto disallowance of Rs.21,69,490/- out of proportionate establishment expenditure. Before the lower authorities as well as before us, assessee has referred to the basis of such calculation and pointed out that the proportionate cost of employees working in the Investment Department to the total number of employees of the assessee-company has formed the basis for such calculation. We find that what is contemplated u/s 14A(2) of the Act is that the Assessing Officer has to record his satisfaction with respect to the incorrectness or otherwise of the claim made by the assessee before applying Rule 8D(2)(iii) of the Rules; and, such satisfaction has to be arrived at, having regard to the accounts of the assessee. We have perused the assessment order and find that such an approach is conspicuous by its absence and the Assessing Officer has proceeded to determine the disallowance in terms of Rule 8D(2)(iii) of the Rules in a mechanical fashion. Moreover, the order of CIT(A) suggests that according to him the factum of suo moto disallowance made by the assessee is enough a cause to empower the Assessing Officer to resort to Rule 8D of the Rules. In our view, the said reasoning weighing with the CIT(A) is contrary to the stated legal position inasmuch as the satisfaction contemplated u/s 14A(2) of the Act is not only in a situation where the assessee claims no expenditure having been incurred in relation to exempt income, but also where a particular quantum of expense is claimed to have been incurred in relation to the exempt income. The aforesaid understanding of the mechanics of Sec. 14A of the Act is clear from the reading of Sub-section (2) & (3) thereof and also from the judgment of the Hon’ble Delhi High Court in the case of Maxopp Investment Ltd., 347 ITR 272 (Delhi) and also the judgment of the Hon’ble Supreme Court in the case of Godrej & Boyce Mfg. Co. Ltd., 111 (SC), which has approved the judgment of the Hon’ble Bombay High Court reported in the case of Godrej & Boyce Mfg. Co. Ltd., 328 ITR 81 (Bom) on the aspect of recording of satisfaction contemplated in Sec. 14A(2) of the Act. The Assessing Officer ought to have recorded his satisfaction in an objective manner as to why the expenditure determined by the assessee as being incurred in relation to the exempt income is incorrect, having regard to the accounts of the assessee. In the absence of such a satisfaction, the Assessing Officer could not have straightaway resorted to Rule 8D(2)(iii) of the Rules in order to compute the disallowance u/s 14A of the Act. Moreover, we find that the assessee has explained the basis of computing the disallowance of Rs.21,69,490/- before the Assessing Officer as well as the CIT(A), and we do not find any reasons advanced by them to doubt its veracity. Therefore, considered in this light, in our view, resort to Rule 8D of the Rules made by the Assessing Officer to enhance the disallowance u/s 14A of the Act is not merited in the instant case. Thus, the enhancement of disallowance made u/s 14A of the Act by the Assessing Officer by a sum of Rs.1,80,96,335/- is not tenable and is hereby directed to be deleted.”

13. The ld. AR argued that the above findings of the Co-ordinate Bench are relevant for the year under consideration also since the AO has not recorded proper satisfaction specifically with regard to the workings of suo-motu disallowance of the assessee. The ld. AR further argued that the adhoc disallowance confirmed by the CIT(A) is without any basis and there is no provision under the law to make adhoc disallowance under section 14A.

14. The ld. DR on the other hand submitted that the assessee has made the suo-motu disallowance based on estimation and therefore the AO has correctly rejected the same stating that he is not satisfied with the suo-motu disallowance.

Accordingly, the ld. DR supported the order of the AO. The ld. DR further submitted that the CIT(A) has followed the order his predecessor to sustain the disallowance to the extent of Rs. 50,00,000/- without recording any specific finding with regard to the substantial relief given to the assessee.

15. We heard the parties and perused the material on record. During the course of hearing the ld. AR drew our attention to the workings of the suo-motu disallowance done by the assessee as extracted below:

| Computation of disallowance u/s 14A of the Income Tax Act, 1961 |

| No. of employees in Investment department |

5 |

| Total no of employees |

1060 |

| Establishment expenditure |

2,10,12,55,994 |

| Prorata establishment expenditure in respect of exempt income |

99,11,585 |

| Direct Expenditure on TCO |

63,677 |

| Proportionate administrative expenditure (disallowed) |

17,00,019 |

| Expenses disallowed under section 14A of Income Tax Act, 1961 |

1,16,75,281 |

16. We notice that the AO has rejected the above workings of the assessee by holding that

“33 The assessee, in the instant case, has not maintained any separate account relevant for exempt income investments and other activities to support its claim that they have incurred an expenditure of 1,16,75,281 only attributable to earning of the exempt income. The assessee is under obligation to establish the extent of expenditure out of all the accounts debited to the Profit and Loss Account as such assessee would not make investment in isolation. The assessee however has not established with the help of its books of account that working of expenses attributable to earning of exempt income and/or holding of its investments are correct and not mere estimation.

34 In view of the above discussions, it is held that the Prorata working of disallowance u/s. 14A of the Act furnished by the assessee is not satisfactory and as a result provisions of section 14A(3) of the Income Tax Act, 1961 are invoked in this case..”.

17. From the above observations of the AO, we notice that the basis for rejecting the suo-motu disallowance is that it is based on estimation and not on actual. However, it is noticed that the AO while rejecting the suo-motu disallowance has not given any specific finding with regard to the books of accounts based on which the assessee has arrived at the disallowance. The AO has also mentioned that the assessee has not maintained separate set of books towards exempt income which in our view is not a requirement under the law. In view of this discussion, we see merit in the submission of the ld. AR that the findings of the Co-ordinate Bench in AY 2008-09 is applicable for the year under consideration also. Respectfully following the above decision of the Co-ordinate Bench, we direct the AO to restrict the disallowance under section14A to the suo-motu disallowance made by the assessee. The ground raised by the assessee is allowed and the ground raised by the revenue is dismissed.

Claim of deduction under section 36(1)(viii)

18. The assessee in the computation has claimed deduction under section 36(1)(viii) to the extent of the least of 20% of profits derived from the eligible business and the amount transferred to the special reserve amounting to Rs.80,00,00,000. The AO during the course of assessment proceedings re-worked the claim of deduction under section 36(1)(viii) by the assessee for the reason that he has made changes to the claim of deduction under section 36(1)(viia) by the assessee in the computation. The AO recomputed the income of the assessee from the business of long term financing activities to arrive at the deduction under section 36(1)(viii) and while doing so the AO reduced the revised deduction under section 36(1)(viia)(c) allowed. Accordingly the AO arrived at an amount of Rs. 71,75,94,432/- and since the amount transferred to the special reserve was Rs. 80,00,00,000/- restricted the amount of deduction to Rs. 71,75,94,432/-. On further appeal the CIT(A) has held that the AO is not correct in reducing the deduction claimed under section 36(1)(viia)(c) while reworking the profit from the eligible business to allow deduction under section 36(1)(viii). In this regard the CIT(A) placed reliance on the decision of the Co-ordinate Bench in assessee’s own case for AY 2004-05 (supra).

19. The ld. DR submitted that the deduction under section 36(1)(viia)(c) is calculated at 5% of the total income and the deduction under section 36(1)(viii) is calculated at 20% of the profits from the eligible business. The ld. DR further submitted that there is an overlapping between these two sections since the profits from eligible business are part of the total income and to this extent there may be a double deduction claimed by the assessee. The ld. DR therefore claimed that the AO is correct in reducing the deduction under section 36(1)(viia)(c) before computing the profits for the purpose of deduction under section 36(1)(viii).

20. The ld. AR submitted that both the sections are independent of each other since the wordings in both the sections use the phrase “computed before making any deduction under this clause” for the purpose of computing the deduction under the said clause. The ld. AR further submitted that the Co-ordinate Bench in assessee’s own case for AY 2004-05 (supra) has considered similar issue and held that the revenue has been consistently accepting the claim and therefore cannot take a different view. The ld. AR also relied on the decision of the Hon’ble Madras High Court in the case of Infrastructure Development Finance Company Ltd. v. ACIT ITR 115 (Madras) where it has been held that

“Question No. 2: Claim for deduction under Section 36(1)(viia)(c) after reducing from the appellant’s income deduction under Section 36(1) (viii) of the Act:-

19. The issue which arises is whether deduction should be firstly allowed in terms of Section 36(1)(viii) for the application of the deduction under Section 36(1)(viia)(c).

20 Section 36(1)(viia)(c) is as follows:-

“Section 36 deals with other deductions

Section 36(viia) (c) deals with in respect of any provisions for bad and doubtful debts made by

(c) a public financial institution or a State financial corporation or a State industrial investment corporation, an amount not exceeding five percent of the total income (computed before making any deduction under this clause and Chapter VI-a).”

21. Section 36 is included in Chapter – IV of the Act relating to Computing of Business Income Chapter VI-A relates to “Deductions in respect of certain Payments”

Section 36 (1)(viii) is as follows:-

“in respect of any special reserve created and maintained by a financial corporation which is engaged in providing long-term finance for industrial or agricultural development of development of infrastructure facility in India or by a public company formed and registered in India with the main object of carrying on the business of providing long-term finance for construction or purchase of houses in India for residential purposes, an amount not exceeding forty per cent of the profits derived from such business of providing long-term finance (computed under the head “profits and gains of business or profession” before making any deduction under this clause) carried to such reserve account.”

22. In the explanation, eligible business had been stated to be business in respect of the specified entity referred to in sub-clause (1) or sub-clause (ii) or sub-clause (iii) or sub-clause (iv) of clause (a), namely the business of providing long-term finance for-

(a) industrial or agricultural development;

(b) development of infrastructure facility in India, or

(c) development of housing in India.

23. It is an admitted fact that the appellant comes within the definition of a ‘specified entity and is carrying on ‘eligible business as provided under Section 36(1)(viii) of the Act.

24. It is the contention of Mr. Karthik Ranganathan, learned Standing Counsel for the respondent that the deduction should be made only on the total income. However, before the amendment, introduced under the Finance Act 1995, the deduction to be allowed under Clause (vii)(a)(c) and Clause (viii) were placed on par. The amendment did not change the character of the deduction but changed the method of computation. By the amendment, an Assessee was permitted to compute deduction at 40% of the profits derived out of business and not 40% of the total income. This was a significant shift in the method of computation. This interpretation is borne out by the Memorandum explaining the provisions in the Finance Bill 1995 whereunder the amendment was introduced. The relevant portions of the Memorandum reads as follows:-

“Under Clause (viii) of sub-section (1) of Section 36 of the Income Tax Act, 1961, an approved financial corporation engaged in providing long-term finance for industrial or agricultural development in India, or an approved public company formed and registered in India with the main object of carrying on business of providing long-term finance for construction or purchase of residential houses, is entitled for a deduction of an amount not exceeding 40 per cent of its total income carried to a special reserve. The deduction is allowed on the “total income” and not with reference to the income from the activities specified in Section 36(1) (viii).

These organisations have diversified their activities and are claiming deduction under this Section even in respect of their income from activities other than those specified in this section. There is no justification for allowing the deduction with reference to income from other activities or from sources other than business. It is, therefore, proposed to limit the deduction of 10 per cent only to the income derived from providing long-term finance for the activities specified in Section 36(1)(viii). It will thus take outside the purview of deduction, income arising from other business activities or from source other than business.”

25. The above must be given harmonious and purposive interpretation that each one of the Clauses under sub-section (1) of Section 36 is independent in its operation and each one of them does not depend upon the other for the extension of the benefit.

26. The learned counsel for the respondent relied on CIT. H.P. Housing Board ITR 388 (HP). The facts in that case are as follows:-

“The Assessee-housing board had floated a self financing scheme for sale of houses/flats wherein the allottees were required to deposit some amount with the assessee and construction was to be carried out of these amounts. One of the conditions of the terms of allotment was that in case the possession of the house/flat was not given to the allottee within a particular time frame, then the assessee-board was liable to pay interest to the allottees on the money received by it. There was delay in construction of the houses and therefore, the Housing Board paid interest at the agreed rate to the allottees in terms of the letter of allotment. The ITO (TDS) held that the amount paid by the assessee to the allottees was in the nature of interest within the meaning of Section 2(28A) and in terms of Section 194A, tax had to be deducted at source. On appeal, the Commissioner (Appeals) allowed the same holding that the amount paid by the Board was not really interest within the meaning of Section 2(284) but actually compensation for the delay in construction of the house and handing over possession of the same to the allottees. The revenue filed an appeal against the said Judgement, which was dismissed.”

27. The High Court of Himachal Pradesh held as follows:-

“8. In the case in hand it stands proved that in case the houses were ready within the stipulated period the Board would not be liable to pay interest. When construction of a house is delayed there can be escalation in the cost of construction. The allottee looses the right to use the house and is deprived of the rental income from such house. He is also deprived of the right of living in his own house. In these circumstances, the amount which is paid by the Board is not payment of interest but in our view is payment of damages to compensate the allottee for the delay in the construction of his house/flat and the harassment caused to him. It may be true that this compensation has been calculated in terms of interest but this is because the parties by mutual agreement agreed to find out a suitable and convenient system of calculating the damages which would be uniform across the Board for all the allottees.

10. In the present case the allottees had not given the money to the Board by way of deposit nor had the Board borrowed the amount from the allottees. The amount was paid under a self financing scheme for construction of the flat and the interest was paid on account of damages suffered by the claimant for delay in completion of the flats.”

28. The facts in the present case are distinguishable and different. A provision had been made for deduction of provisions for Bad and Doubtful debts under Section 36(1)(viia)(c) independent of Section 36(1)(viii) which provide for deduction upto 40% for special Reserve created by Assessee providing long term finance for development of infrastructure facility. The Tribunal in the present case had actually not applied its mind on this issue. They had simply reaffirmed the earlier order dated 05.09.2003 for the Assessment Year 2000-2001, and the order dated 19.01.2004 for the Assessment Year 2001-2002 and followed the same principles. However, as pointed out above, the appeals against the said orders had been allowed by a Coordinate Bench of this Court and the answer has been given in favour of the Assessee. If Section 36(1) is examined, it is clear that sub-section (1) gives the list of matters in respect of which deduction can be allowed while computing the income referred under Section 28. Clause (i) to (xi) of sub-section 1 of Section 36 do not imply that those deductions depend on one another. If an Assessee is entitled to the benefit under Clause (i) sub-section (1) of Section 36, the Assessee cannot be deprived of the benefit the other Clauses. This is how the provisions have been ayed. The computation of amount of deduction under both these clauses has to be independently made without reducing the total income by deduction under clause (viii) of Section 36 of the Act.

29. In view of the above reasons, we hold that this substantial question of law has to be answered in favour of the appellant and against the respondent.”

(emphasis supplied)

21. We heard the parties and perused the material on record. The deduction under section 36(1)(viia) allows deduction not exceeding five per cent of the total income (computed before making any deduction under this clause and Chapter VIA) and deduction under section 36(1)(viii) provides for deduction not exceeding twenty per cent of the profits derived from eligible business computed under the head “Profits and gains of business or profession” (before making any deduction under this clause) carried to such reserve account. In other words, the deduction under section 36(1)(viia)(c) is restricted to a certain percentage on total income whereas the deduction under section 36(1)(viii) is restricted to a percentage on the Profits & Gains from the eligible business. If we are to interpret that deduction under section 36(1)(viii) is a subset of 36(1)(viia)(c) and vice versa then the claim of deduction under these two section may get into a loop and any change to one deduction will distort the other which would not be the intention of the legislature. Further the plain interpretation of the wordings used in both these sections i.e. “computed before making any deduction under this clause” in our view would mean not to consider the deduction under the respective clauses while computing the restriction applicable as a percentage of either total income or profits from the eligible business. Our view is strengthened by the ratio laid down by the Hon’ble Madras High Court in the above case where it is held that the deductions under various clauses to sub section (1) of section 36 are independent of each other and the deduction under a particular clause is to be claimed without reducing the total income by deduction under any other clause. Therefore in our considered view the same corollary is applicable to the issue under consideration also where the reverse situation is contended i.e. whether deduction under section 36(1)(viia)(c) is to be reduced for the purpose of deduction under section 36(1)(viii). Further we notice that the coordinate bench in assessee’s own case for earlier years has held the impugned issue in favour of the assessee on that ground that the revenue has accepted the deduction and the principle of consistency should be applied. In view of these discussions and considering the judicial precedence we hold that there is no infirmity in the decision of CIT(A). The ground raised by the revenue is dismissed.

Disallowance of amortized rent

22. The AO disallowed the claim of deduction towards lease premium paid to Mumbai Metropolitan Regional Development Authority (MMRDA) on proportionate basis. The CIT(A) confirmed the said disallowance. The ld. AR during the course of hearing submitted that the disallowance made in earlier years had been confirmed by the Co-ordinate Bench i.e. the issue has been decided against the assessee in the earlier years. The ld. AR further submitted that the assessee has challenged the orders passed by the Tribunal in the earlier year by filing an appeal before the Hon’ble Bombay High Court and the substantial question of law raised by the assessee has been admitted by the Hon’ble High Court. The ld. AR in this regard placed before us the copy of the order of the Hon’ble Bombay High Court in Small Industries Development Bank of India v. Dy. CIT [IT APPEAL No. 792 OF 2012, dated 18-3-2013] where the following question of law had been admitted.

“Whether on facts and in circumstances of the case and in law the amount paid by the appellant to MMRDA as lease premium constituted revenue expenditure and the appellant was entitled to claim a proportionate part of the said premium as deduction in the current AY.”

23. The ld. AR submitted that the assessee is filing a declaration under section 158A in Form-8 before the Tribunal since identical question of law is pending before the Hon’ble Bombay High Court. The ld. AR further submitted that the assessee shall not raise the above said question of law before any of the appellate authority, if the above said declaration is not objected to by AO and accepted by the Tribunal. The ld. AR also submitted that similar declaration has been filed by the assessee in earlier years and that in those years the AO has furnished the report stating that the claim made in the declaration filed by the assessee under section 158A was found to be correct and had further stated that the order of the Hon’ble High Court is awaited. Accordingly, the ld. AR prayed that the declaration for the years under consideration may be forwarded to the AO for obtaining a similar report and that the revenue shall not take any action against the assessee until the decision by the Hon’ble High Court on the impugned issue.

24. We heard the parties and perused the material on record. Considering the facts as narrated hereinabove, we are setting aside the issue back to the AO with a direction to consider Form-8 in the light of section 158A of the Act and pass an appropriate order after giving a reasonable opportunity of being heard to the assessee.

25. We have listed the issues contended by the assessee and the revenue through various grounds in the earlier part of this order. From the perusal of the same it is clear that the issues contended in AYs 2014-15, 2015-16, 2017-18 and 2018-19 are identical to AY 2016-17. Therefore in our considered view our decision in AY 2016-17 are mutatis mutandis applicable to AYs 2014-15, 2015-16, 2017-18 and 2018-19 also.

26. In result, the appeals of the revenue for AYs. 2014-15 to 2018-19 are dismissed and the appeals of the assessee for AY 2017-18 and 2018-19 are partly allowed to the extent as indicated above.