ORDER

Anubhav Sharma, Judicial Member.- This appeal preferred by the Assessee against the order dated 24.03.2025 of Ld. National Faceless Appeal Centre (NFAC) (hereinafter referred to as the First Appellate Authority or ‘the ld. FAA’ for short) in DIN & Order No : ITBA/NFAC/S/250/2024-25/1074946873(1) arising out of the assessment order dated 26.12.2022 u/s 143(3) r.w.s 144B of the Income Tax Act, 1961 (hereinafter referred to as ‘the Act’) passed by the NeFAC [DEL-W-(52)(91)] for AY: 2021-22.

2. Heard and perused the records. The facts in brief are that the assessee has filed return of income on 31.12.2021 which was subsequently revised on 31.03.2022 declaring total income of Rs.194,39,080/- and claimed deduction u/s 54F of the Act to the tune of Rs.9,65,05,033/-. Statutory notices were issued and Assessing Officer examined the claim of deduction u/s 54F of the Act, with regard to eligibility and concluded that as on the date of transfer of capital asset, shares of unlisted companies, assessee was in possession/occupation of more than one residential house, thus the assessee is not eligible for deduction u/s 54F of the Act.

2.1 Further, Assessing Officer observed that assessee had invested/purchased in an apartment No. CM7184 DLF 5 and Sector 42 Gurugram worth Rs.32,95,29,561/- and has claimed deduction u/s 54F. Assessing Officer found that assessee has received a rebate of Rs.9,81,39,230/- from the developer and considering the same to be income u/s 56(1) of the Act, as income from other sources, added this amount of rebate in the income.

2.2 Assessee approached by way of first appeal before Ld. CIT(A) but failed to get any relief. The relevant findings of Ld. CIT(A) with regard to rejection of benefit of Section 54F of the Act and the addition qua rebate income are as follows:

First Issue

“10. This Appellate authority has also noted that, the appellant assessee has not provided a copy of the said purchase deed of the Flat bearing number-CM 718A The Camellias’ at Gurugram (formerly Gurgaon). As the said property is not proved registered in the name of the appellant V assessee till date the contentions of the assessing officer that, “For the purpose of exemption u/s 54F, the assessee must purchase residential house within one year before, or within 2years after, the date of transfer of original capital asset. Since the property has not yet registered in the name of the assessee deduction claimed u/s 54F is not allowable as per the Income-tax Act, 1961” carries substantial weight in the opinion of this Appellate authority. This Appellate authority has noticed that:

| a. |

|

The appellant had booked this Flat No.-CM 718A in ‘The Camellias’ on 07.12.2017 |

| b. |

|

The appellant had transferred the residential house/ Flat in The Magnolias (No.-MG-905-B, 5th Floor, The Magnolias, Gurugram) in name of his wife Mrs Ira Dash Rajguru through a gift deed on 24.10.2017. |

| c. |

|

The appellant had also transferred another residential house situated at Geetanjali Enclave, New Delhi in name of his wife Mrs Ira Dash Rajguru through gift deed on 28.03.2018. |

| d. |

|

There after appellant had sold the said shares of a Pvt. Ltd. Company in the FY 2020-21 towards which appellant has not provided any details of the said company, date of purchase and sale of the shares against which gain is said to be made and which is sought to be invested in the said Flat at The Camellia’s and for which the appellant seeks to claim the said exemption u/s. 54 of the Act. |

| e. |

|

And till date the title deed of the said Flat / property purchased by him in the Camellias – MG-905B has not been provided to this Appellate authority. |

11. The language of Section 54F of the Act (mentioned above) is clear that, the deduction u/s 54F in case of purchase of house property is available only if the house is purchased one year before or within two years after the sale of property i.e. shares of unlisted companies in your case on which capital gain has arisen.In the opinion of this Appellate authority the appellant assessee hasgrossly failed to prove the facts of his case and his contentions are not supported by the law and the provisions of Income Tax Act, 1961.

12. The appellant was also asked to submit an affidavit within the meaning of section 250(4) of the Income Tax Act, 1961 with regards to the said claim of exemption u/s. 54F of the Income Tax Act and its Registration value before the sub-registrar. The appellant filed an affidavit dated 17.03.2025 reiterating his right to claim the said exemption u/s. 54F of the Act and the Collectors circle rate, but has not submitted any copy of the purchase deed/registered purchase deed to show ownerhisop of the said Flat bearing number CM 718A ‘The Camellias’ at Gurugram or showing any registration value so paid before the sub-registrar concerned. The appellant also mentions that, he had filed a similar affidavit before the AO too dated 13.12.2022. Thus, apparently the AO had provided an opportunity to the appellant to file such proper details and to come clean, but the appellant failed to file such proper details then too.

13. The appellant assessee in its statement of facts states that, “in respect of long term capital gain on sale of shares of a private limited company.” But the appellant assessee has not provided any details or submissions regarding the sale of shares to even show as to the shares were of, which private limited company? No source has been given by the appellant assessee. The appellant assessee has also not provided any proof to show as to/ or when were these shares purchased, what was the basis on which the value of shares was taken by the assessee w.r.t. their purchase/acquiring of these unlisted shares, no proof have been provided by the appellant assessee regarding the sale of shares. The Assessee has also not provided Share Transfer Certificate/deed. The onus lies with the appellant to come clean on such basic facts whenpreferring an appeal.

14. This Appellate authority places its reliance on the judgment of the Hon. ITAT Hyderabad in case of Rachit V. Shah v. ITO in which the Tribunal has held that, “….The Assessing Officer in the paragraph reproduced above have concluded that the gift deed though exeeuted on 27.10.2014, was a colourable device as it was executed by the assessee just three days prior to entering into an agreement of sale. The conduct of the assessee, to gift the property to his father, just prior to entering into an agreement of sale raises doubt about the intention of the assessee. A perusal of clause 11 of the Gift Deed, copy of which is placed at Pages 23-28 of the paper book shows that Rs.2,20,000/-towards stamp duty and registration fee had been paid by the assessee vide Demand Draft No.317588 dt.12.01.2015 of Canara Bank, M.J. Market Branch, Hyderabad after execution of Agreement of Sale dt.03.11.2014 and just prior to purchase of asset on 30.01.2015. Quiet clearly, assessee was aware of the Income Tax provisions and was also aware that the assessee would not be entitled to the benefit of section 54F of the Act, if he had more than one residential house in his name before investing. In the present case, the assessee has shown the house property income from two houses, namely, oneself occupied (at Door No.3-6-305/43, 43/1, Avanthi Nagar, Basheerbagh, Hyderabad) and one let out (at Sy.No.52 & 53, Saheb Nagar, Khurd Village, LB Nagar, Hyderabad). However, the assessee has gifted the house at Door No.3-6-305/43, 43/1, Avanthi Nagar, Basheerbagh, Hyderabad by virtue of the gift deed Rachit v. Shah to his father, just before entering into an agreement of sale and had claimed the deduction u/s. 54F, after investing the proceeds received by him in respect to property in survey Nos. 114 & 115 situated at GaganPahad village in buying the residential house property at Road No. 47, Plot no. 946, Jubilee Hills, Hyderabad. The Assessing Officer had brought on record that the assessee had two residential properties before purchasing the residential house property at Road No.47, Plot no.946, Jubilee Hills, Hyderabad.

From the conduct of the assessee and in view of the circumstances prevailing at the time of the agreement of sale, more particularly giving gift to his father just before the date of agreement, it is clear that the act of the assessee to gift the house is nothing but a concerted effort to avoid the due payment of taxes to the Government. With a view to avoid the payment of taxes, the assessee surreptitiously gifted the house at Door No.3- 6-305/43,43/1, Avanthi Nagar, Basheerbagh, Hyderabad to his father just before entering into agreement of sale and received the consideration of RS.2,28,38,880/- on 03.11.2014 and Rs.2,11,41,120/- on 03.11.2014. Though, gift deed, on a standalone basis seems to be a natural act on the part of son to gift home to his father, but when the gift deed is to be examined in the light of the prior and subsequent acts and prevailing circumstances, then it is clear that the real intention of the assessee, was to claim the deduction u/s. 54F of the Act. Further, the assessee before and subsequent to gifting the property, continued to live with his father in the same property, which clearly shows that the gift deed executed by the assessee was merely a camouflage to claim the deduction u/s. 54F of the Act Rachit v.Shah and to avoid due payment of taxes to the Government. Undoubtedly, tax evasion connotes illegally suppressing facts, falsifying records, fraud or collusion to evade tax liability with the help of such unfair means. Whereas abusive tax avoidance involves ‘contrived’ or ‘artificial’ schemes. In the present case, the assessee was engaged in the artificial transfer of one house by way of gift deed just prior to the effective date. Further, under sections 23 and 24 of the Indian Contract Act, 1872, when the object is to defeat any provisions of law, and when consideration is of such nature that, if permitted, it would defeat the provisions of any law, the contract will be void.

In the present case, per se gift deed was not executed on account of natural love and affection but was executed by the assessee to artificially avail the deduction u/s 54F of the Income Tax Act 1961.

15. We cannot countenance the assessee’s conduct and allow the assessee to misuse and exploit the beneficial provisions of section 54F of the Act. Undoubtedly, as per the assessee, he is an individual having a high net worth and paying huge taxes. The assessee artificially created a gift deed of the property with a view to fit into the provisions of section 54F, so that he can claim the deduction against the sale of capital asset. The act of the assessee was prearranged step for execution, and it served no commercial purpose but was motivated to avoid paying taxes.

16. In view of the above, the orders passed by the assessing officer and Id. CIT(A) were within the four corners of law and do not require any interference. The decisions relied upon by the assessee are distinguishable on facts and do not apply to the facts Rachit v. Shah of the present case. Accordingly, the appeal of the assessee is dismissed.”.

15. Thus, vide the aforesaid judgment theon. Hyderabad Tribunal has clearly stated that, though the gift deed, on a standalone basis seems to be a natural act on the part of the son to gift a home to his father, but when the gift deed is to be examined in the light of the prior and subsequent acts and prevailing circumstances, then it is clear that, the real intention of the assessee, was to claim the deduction u/s. 54F of the Act. Further, the assessee before and subsequent to gifting the property, continued to live with his father in the same property, which clearly shows that the gift deed executed by the assessee was merely a camouflage to claim the deduction uls. 54F of the Act as held in Rachit v. Shah and to avoid due payment of taxes to the Government.

16. In the present case also the appellant assessee has similarly or schematically transferred his two residential units le. Plot No 8,Block F, Geetanjali Enclave, New Delhi and at MG-905-B,5thFloor, The Magnolias, Gurugram, Haryana, in name of his wife through a gift deed before buying the house/flat at The Camellias, against which assessee has claimed exemption u/s 54F of the Act.

17. The Assessee has also not provided any details/explanation, valuation regarding the unlisted shares he has sold, this also points out that, the appellant assessee is not coming out clean and has used the gift deed as a camouflage or as a colourable device to falsely claim exemption u/s 54F of the Act against the alleged Long Term Capital Gain of unlisted equity shares.”

Second Issue;

“This Appellate Authority find’s that:

i. The Ld AO finds in the assessment order that, as per the agreement for purchase of flat with DLF shows the total price payable for the said apartment is Rs.31,82,89,000/-, as against which assessee has been given a rebate by the said builder/ seller to the extent of Rs. 9,81,39,230/- towards the said flat / property ie.: CM 718A “The Camellias’ at Gurugram.

ii. The Ld AO also states that, the “.Verification of the agreement for purchase of flat with DLF shows that the total price payable for the said apartment is Rs.31,82,89,000/- as against which assessee has been given rebate by the seller to the extent of Rs. 9,81,39,230/-. As per section 56(1) the rebates earned by the assessee to the tune of Rs. 9,81,39,230/- is an income which is not to be excluded from the total income and it is chargeable to income tax under the head Income from Other Sources.

iii. The appellant assessee in its submissions claims that, everybody who gets any concession for purchasing any goods or services throughout the year right from purchasing like clothes, fruits etc. would amount to be income and taxable under Incometax Act. But the above contentions of the appellant assessee cannot be considered as correct as if the said builder/ seller/ company is giving such huge rebate @ 28% + [ie: almost 30% of the agreement value], out of the total agreed value of the said property, then the value of the property as stated by the builder/ seller/ company is Rs 31,82,89,000 – and not Rs. 22,92,28,673/-.

iv. From general trade practices it is not heard/ known commonly where the GP/NP of the builder/seller concerned is such high that, it can afford to give rebate @30% of the agreed value to the flat buyers.In such a case, one can imagine as to what kind of profits are being made by the said builder DLF who can afford to write-off / provide such huge and absurd amount of rebate to a buyer only based on early down payment. This, kind of a practice is un-heard of or is beyond preponderance of probabilities. Also the appellant has hot proved whether the said builder/ seller has given out more such flats at such huge rebate to other buyers as a practice. Whereas, it is recently heard via the news in December, 2024 across Delhi/CR that, a penthouse (flat) in DLF- the Camellias, Gurgaon (now known as Gurugram) was sold at a record breaking price of Rs. 190 croresie: approx. 1,08,000per square feet and purchased by Mr Rishi Parthi the Director of Info-x Software Tech. P. Ltd. Thus, in a colony of flats where the flats/ residences are being sold at such a ultra-high premium then such kind of rebates ie: @ Rs. 9,81,39,230/- is not only absurd but is beyond preponderance of probabilities as to why the builder/ seller would sell its prime property at such rebates and thus an arrangement cannot be denied between the buyer and builder to make such adjustment of cash or value in kind. The appellant fails to discharge the doubt and produce such valid registration papers till date to dispel the contentions of the AO.

v. The properties owned by the appellant and his spouse due to the said transfer of property discussed above at addition no.-A) at both the Camellias (ie.: CM 718A ‘The Camellias’ at Gurugram) and the Magnolia’s (i.e: The MAGNOLIAS no.-905 B, Wazirabad, Gurgaon) put together would beatleast worth over a 100-125 crores atleast in today’s terms.

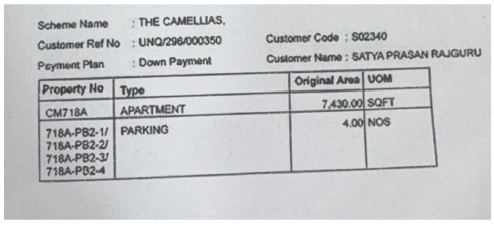

vi. The details of the property submitted by the appellant are as follows:

If seen carefully then the appellant has allegedly agreed to purchase a flat which is of 7,430 sq. feet in area with 04 car parking’s. It means that in today’s terms the said flat is worth approx. 80.24 crores in value (on date) and the cost of 04 parking’s is extra cost.Whereas, the appellant has failed to show even the registration papers of the said property.

vii. Moreover, in general trade practice also if the builder provides discounts to the individual on early payment/timely payments then that,the rebate is considered as the income of the individual and in the present case also the appellant assessee has got rebate for early down payment and timely payments. As it can be easily seen that,the appellant assessee has got the rebates of early down payment and rebate for timely payments which is the income of the appellant assessee.As per section 56(1) the rebates earned by the assessee to the tune of Rs. 9,81,39,230/- is thus an income which is not to be excluded from the total income and it is chargeable to income tax under the head Income from Other Sources.

In the light of above discussed facts at point no.-(i) to (vi) and B-1 to 3 and finding of the AO and submissions of the assessee, this Appellate authority finds substance in the contentions of the Assessing officer and the addition made by the Assessing officer amounting to Rs 9,81,39,230/- u/s 56 of the Income Tax Act, 1961 is thus found to be reasonable and thus UPHELD. The appellants grounds no. 3 are thus not allowed.”

2.4 Assessee is in appeal and has raised following grounds;

“1. That having regard to the facts and circumstances of the case, Ld. CIT(A) has erred in law and on facts in confirming the action of Ld. AO in making addition of deemed income of Rs.9,81,39,230/- in the hands of assessee under the head Income from Other Sources’ u/s 56 and that too by recording incorrect facts and findings and without observing the principles of natural justice and by disregarding the submissions and evidences placed on record by the assessee.

2. That in any case and in any view of the matter, action of Ld. CIT(A) in confirming the action of Ld. AO in making addition of deemed income of Rs.9,81,39,230/- in the hands of assessee under the head Income from Other Sources’ u/s 56, is bad in law and against the facts and circumstances of the case.

3. That having regard to the facts and circumstances of the case, Ld. CIT(A) has erred in law and on facts in confirming the action of Ld. AO in not allowing the exemption of Rs.9,65,05,033/- claimed by the assessee u/s 54F, more so when all the conditions therein have been complied with by the assessee and the said exemption has been denied by recording incorrect facts and findings and without observing the principles of natural justice and by disregarding the submissions and evidences placed on record by the assessee.

4. That in any case and in any view of the matter, action of Ld. CIT(A) in confirming the action of Ld. AO in not allowing the exemption of Rs.9,65,05,033/- claimed by the assessee u/s 54F, is bad in law and against the facts and circumstances of the case.

5. That having regard to the facts and circumstances of the case, Ld. CIT(A) has erred in law and on facts in not reversing the action of Ld. AO in charging interest u/s 234B and 234C of the Income Tax Act, 1961.

6. That the appellant craves the leave to add, modify, amend or delete any of the grounds of appeal at the time of hearing and all the above grounds are without prejudice to each other.”

3. Ground No 1 & 2: – These grounds relate to addition of Rs. 9,81,39,230/- as deemed income u/s 56(1) of the Act, made by AO on the basis that assessee purchased Flat No. 718A The Camellias at Rs. 23,13,90,331/- whereas its price was Rs. 32,95,29,561/-. Therefore, AO alleged that the rebates earned by assessee for Rs.9,81,39,230/-would be deemed income u/s 56(1) of the Act. Further, CIT(A) confirmed this addition by alleging that an arrangement cannot be denied between buyer and seller to make such adjustment of cash or value in kind.

3.1 Ld. Counsel contended that there cannot be any income on purchase of immovable property, the consideration of which is fixed by mutual bargaining. Granting discount is a routine exercise in such negotiations. Thus, the addition is bad in law.Further, the finding about the adjustment in cash or value in kind, as mentioned by CIT(A) is not backed by even an iota of evidence. Therefore, it is based on conjectures and surmises.

3.2 Then on without prejudice basis it was contended that according to section 56(2)(x) of the Act, amount of purchase of immovable property at less than stamp duty value alone can constitute income and not when property is purchased at more than stamp duty value which is evident from the plain reading of section 56(2)(x) of the Act.In this case stamp duty value was Rs. 14,68,00,000/- and flat was purchased for Rs. 23,13,90,331/-.

4. Ld. DR has however relied the impugned orders and has contended that there was no justification for rebate and it only indicates some suspicious transaction beyond what is reflected on papers. It was contended that even now there is no registration of sale deed which shows the transaction is sham.Ld. DR has relied the impugned orders and contended that huge rebate of 28% of total agreed value of the property cannot be considered reasonable as it defies normal profits declared by the builder and whether builder has given such rebate to other buyer is not known and such huge rebate indicates the arrangement to adjust cash and value in kind.

5. We have considered the material on record and it comes up that assesse has filed some relevant evidences. At PB 206-213 (relevant page 211) is the copy of assessee’s reply dated 15.12.2022 before AO stating that as per the list of collector rates applicable for AY 2021-22 in Tehsil Wazirabad, the rate mentioned at Page 6, Serial No. 3, for the disputed property is Rs. 20,000/-per square ft. Therefore, the stamp duty value of the subject property computed in accordance with Section 56(2)(x) of the Act amounts to Rs.14,68,00,000/- (i.e., Rs. 20,000x 7,340 square ft, being the total flat area.

5.1 Then at PB 248 is the copy of list of collector rates applicable for the AY 2021-22 in Tehsil Wazirabad which has been placed on record, wherein the rate for the residential project ‘The Camellias’ is specified at Serial No. 6 as Rs. 20,000/- per square foot. The said document bears the signatures and official endorsements of the Sub-Registrar, Sub-Divisional Officer, District Revenue Officer (DRO), Additional Deputy Commissioner, and the Deputy Commissioner-cum-Registrar, thereby attesting its authenticity and official character.

5. 2 At PB 259-301 (relevant page 293) is the copy of assessee’s reply dated 20.12.2022 before AO stating that the purchase consideration paid by the assessee towards the acquisition of the flat was higher than the stamp duty value as determined by the registering authority for the purposes of stamp duty under the relevant State laws. Consequently, the transaction does not fall within the ambit of Section 56(2)(x) of the Act also as no element of undervaluation or deemed income arises in such circumstances.

6. We find that both the tax authorities below have booked rebate to be an income under the head ‘income from other sources’ but it is questionable if in the absence of any specific sources invoking deeming income principles without invoking specific deeming income charging section can at all be sustained. There is actually no real income but it is the benefit by way of rebate which department wanted to cap as income, so it is only by establishing the there was deemed income department could have succeeded and thus it is rightly contended by ld. Counsel that where stamp value or circle rate is lower than actual consideration, then there cannot be any deemed income in acquiring a immovable property. On this basis alone assesse can succeed.

7. Then we find that Ld. Counsel has provided the break up of the rebate allowed under the apartment buyer’s agreement as follow:

| Nature |

Amount (INR) |

| Down payment Rebate |

4,27,83,490 |

| Move-in-Rebate |

2,22,90,000 |

| Special Rebate. |

1,82,05,740 |

| Timely Payment Rebates |

1,48,60,000 |

| Total Rebate |

9,81,39,230 |

7.1 We find that annexure IIIA providing schedule of payment copy of which is available at page 304 of the paper book as part of the apartment buyer’s agreement. The assessee has established that this rebate is not something which has come to the assessee suddenly at the conclusion of the deal but was very much part of the terms and conditions contained in apartment buyer’s agreement. Thus, it is not the case where the rebate has been earned by the assessee out of any act beyond the terms and conditions of the apartment buyer’s agreement so as to be even considered as income’earned’ rather it was very much a contractual concession given by the builder for complying with the payments schedule.

7.2 As for instance, the move in rebate @ 3000 per sq. ft. was allowable for finishing in time as per the terms and conditions of the apartment buyer’s agreement which appears to be a very prudent approach of the builder to ensure that such high price properties are not left idle or become investment subjects but rather the actual users occupy the properties.

7.3 The nature of rebates are not uncommon or unprecedented, to look pretentious, but are usually granted by builders to encourage timely repayments or early repayments and to consider it as an income u/s 56(1) of the Act is not sustainable. Ld. CIT(A) has approached the issue on the basis of common man’s perspective of such high pitched real estate transaction without acknowledging and appreciating that such high pitched real estate transactions are on high premium more because of the rich amenities and facilities provided to the occupants. Rather, questioning business prudence of the builders to give such rebates cannot be subject matter of inquiry from the end of the purchaser and thus the findings of ld. CIT(A) to sustain the additions on the basis of deemed income u/s 56 of the Act cannot be sustained and we are accordingly inclined to allow ground No. 1 & 2.

8. Ground No 3 & 4: – These grounds relate to addition of Rs. 9,65,05,033/- on the ground that exemption claimed u/s 54F of the Act was not allowable to the appellant inrespect of purchase of house at “The Camellias” as the alleged purchased property was not registered within two years from the date of sale of original asset, and that the appellant was the owner of more than one house as on the date of sale of original asset.

8.1 Ld. Counsel has submitted that the condition for claiming deduction u/s 54F of the Act is that the house must be purchased within two years as is evident from plain reading of section 54F of the Act which was so done by the appellant. He relied certain facts and evidences to claim same establish that that house at “The Camellias” was purchased within two years and aggregate amount of Rs. 23,13,90,331/- was paid for the purchase of said house. He referred to PB 102-117 (relevant page 08-109) which is the copy of assessee’s reply dated 01.11.2022 before Ld. AO stating that Occupancy Certificate in respect of the subject residential flat (i.e. The Camellia) was duly obtained on 17.12.2021, which is well within the prescribed time limit of two years from the date of transfer of the original capital asset i.e. 22.05.2020 in accordance with the provisions of Section 54F of the Act.

8.2 Then at PB 309 is the copy of possession letter dated 30.12.2020 issued by DLF Limited to the assessee. AT PB 310-312 there is the copy of detailed breakup of payments made to DLF Limited for purchase of above said flat.

8.3 It was contended that even AO himself admits at page no. 5 of the assessment order that assessee ‘purchased’ house at “The Camellias” for Rs. 23,13,90,331/- while making addition of Rs. 9,81,39,230/- u/s 56(1) of the Act, which we have considered in aforesaid discussion of ground no. 1 and 2.

9. Ld. Counsel has also submitted that moreover the law is that that registration of the purchased house is not a condition precedent for claiming exemption u/s 54F of the Act and his reliance was on the decision in CIT v. Podar Cements (P.) Ltd. (SC). It was submitted that assessee could claim exemption even on the basis of the agreement to sell only without it being registered for which reliance was placed on ITO v. Smt. Swati Oberoi [IT Appeal No. 4150(Delhi) of 2018 , dated 30-7-2021]/ITA No. 4150/Del./2018. It was then submitted that benefit of deduction u/s 54F of the Act cannot be denied to the assessee merely on the ground that conveyance deed has not yet been got registeredparticularly when the assessee is proved to be in possession of the property in question. As for this reliance was placed on ACIT v. Siva JyothiPalam, ITD 352 (Visakhapatnam – Trib.); Basheer Basheer Noorullah Khan v. CIT [IT Appeal No. 575(Bang) of 2019, dated 31-7-2019] and Nandlal Pritamdas Kishnani v. ITO (Delhi – Trib.)

10. Adverting to the allegation that the appellant is owner of more than one house on the date of transfer of original capital asset, it comes up that revenue alleges that the assessee was the owner of following three houses: –

i. C-101, Palaspally, Bhubaneshwar, Odisha

ii. MG-905B, 5th Floor, The Magnolias

iii. Geetanjali Enclave, New Delhi

10.1 Now with regarding house at Sr. no(i), above, being situated at Bhubaneshwar,assessee admits its ownership. However, with regard to house at Sr. No. (ii) in respect of “The Magnolias”, it is submitted by ld. Counsel that assessee owned ½ ownership of the property and that too was also gifted by the appellant to his wife on 24.10.2017 which is evident from the copy of registered Transfer Deed dated 24.10.2017 (PB 215-242)evidencing that the assessee had gifted/transferred his ½ undivided share in the residential property bearing No. MG-905, situated in ‘The Magnolias’ to his wife. This was done much earlier than the date of sale of shares on 22.05.2020.

10.2 As with regard to the property at Sr. No (iii) in respect of Geetanjali Enclave, New Delhi it was submitted that assessee owned ½ ownership of the property and that too was also gifted by the appellant to his wife on 27.03.2018 which is evident from the copy of registered Transfer Deed dated 27.03.2018 (PB 325-350 is) evidencing that the assessee had gifted/transferred his ½ undivided share in the residential property bearing No. F-18, Geetanjali Enclave, New Delhi in favour of his wife. He has referred to PB 214, 355-356, where there is the copy of affidavit dated 13.12.2022 and declaration on oath (notarised) dated 17.03.2025 by assessee duly affirming that as on the date of transfer of the original capital asset he was the owner of only one residential house i.e. Flat No. C-101 Pallaspalli, Bhubaneshwar, Odisha.Therefore, as per ld. Counsel, it is more than evident from the above that assessee was not the owner of more than one house on the date of transfer of original asset i.e. 22.05.2020.

11. Ld. Counsel then submitted that even otherwise the appellant was not the absolute owner of the residential properties being Magnolias &Geetanjali Enclave, in which he was having only one-half share which is clearly evident from the copy of the registered Gift Deed dated 27.03.2018 by assessee to his wife for property bearing No. F-18, Geetanjali Enclave, New Delhi showing that the previous owner Smt. ShikhaGoyal transferred the above said property jointly to the assessee and his wife on 09.05.2008 (PB 325-350 (331-333). At PB 215-242 (relevant page 217) is the copy of the registered Gift Deed dated 24.10.2017 by assessee to his wife for property bearing No. MG-905-B, The Magnolias, Gurugram showing that the assessee and his wife had purchased and were joint co-owner, seized and in possession of ½ undivided share apartment each. It was submitted that even the AO issued at notice, copy of which is at PB 204, dated 09.12.2022 stating that other than the Odisha residential house assessee is the joint owner in property no. 905B, The Magnolias, DLF Golf Links, DLF 5, Guragaon. It was contended that assessee was not the absolute owner of the residential properties i.e. Magnolias and Geetanjali Enclave and held only a partial interest specifically, an undivided one-half share therein-the said properties ought not to be considered for the purposes of determining the assessee’s ineligibility for exemption under Section 54F of the Act.Reliance was placed on P.K. Vasanthi Rangarajan v. CIT (Madras) to contend that co-ownership in a residential property does not disentitle an assessee from claiming exemption under Section 54F of the Act. It was contended that joint ownership of a second property is no bar to exemption on transfer of individual property and reliance was placed on Rajeev Vasudeva v. DCIT (Mumbai – Trib.); Anant R Gawande v. ACIT ITD 58 (Mumbai – Trib.); Smt. Savita Bhasin v. ITO ITD 195 (Delhi – Trib.); CIT v. Kapil Nagpal [2016] 381 ITR 351 (Delhi); Manoj Tekriwal v. DCIT [IT Appeal No. 4147(Mum ) of 2015, dated 13-7-2022]; Ashok G Chauhan v. ACIT (Mumbai); DCIT v. DawoodAbdulhussain Gandhi [ITA No. 3788(Mum) of 2016 , dated 31-1-2018].

12. Ld. Counsel then pointed out that CIT(A), has relied on the decision in Rachit V. Shah v. ITO. Hyderabad ITAT butthe facts of the case are clearly distinguishable as in that case the gift deed was executed three days prior to the agreement of sale. Stamp duty on the gift was paid after the sale of capital asset. These facts made the transaction to be colourable. However, the assessee had transferred his ½ shares in two abovesaid properties muchbefore the date of sale of shares. Therefore, the question of transaction of gift being colourable does not arise.

13. It is also submitted that chapter X-A deals with applicability of general anti-avoidance rule, which is applicable from AY 2018-19 and onward. Section 96(1)(b) of the Act entitles the AO to declare any arrangement to be impermissible avoidance agreement, the main purpose of which is to obtain a tax benefit, and it results directly and indirectly in misuse or abuse of the provisions of this Act. In paragraph 15, CIT(A) has recorded a finding that the gift deed executed by the assessee was merely a camouflage to claim deduction u/s 54F and to avoid due payment of taxes to the government. Such a finding requires that procedure provided in Chapter X-A ought to be followed. The same has not been done and therefore, such a finding is bad in law. It may also be submitted that the case of Rachit v Shah pertained to AY 2015-16, when Chapter X-A did not exist on the statute book. Therefore, the ratio of this case is no longer applicable.

14. Though the issue of the existence of Long-Term Capital Gain (LTCG) on the transfer of shares was neither raised by the Ld. AO nor formed a subject matter of adjudication by the Ld. CIT(A), but as ld. DR has raised the concern, ld. Counsel submitted that LTCG had arisen from the transfer of shares of V5 Global Services Pvt. Ltd., as is evident from the calculation of LTCG on the sale of shares of V5 Global Services Pvt. Ltd and at PB 10-101 are the copies of share purchase and shareholder’s agreement dated 18.04.2018 of V5 Global Services Pvt. Ltd. He pointed out that at PB 105106 is the copy of assessee’s reply dated 01.11.2022 before Ld. AO stating that 64,473 equity shares of M/s V5 Global Services Private Limited were sold to M/s First Meridian Services Private Limited on 22.05.2020 for a total consideration of Rs. 9,53,90,418/- and received Rs. 100/- on 03.12.2020 and Rs. 9,53,90,318/- on 04.12.2020 in Kotak Mahindra Bank (PB 314A).

15. Ld. DR has countered it all by relying the findings of ld. Tax authorities.

16. We have considered the rival contentions and it comes up from the impugned order the Ld. CIT(A) has heavily relied decision of Hyderabad Bench in case of Rachit V. Shah (supra) but when the facts of that case are considered in context to the issue before us we find that in that case the assessee just three days prior to entering into an agreement of sale had gifted property to his father and had also comes up as an admitted fact that after the gift assessee continue to stay in the same house with his father. Thus it was considered to be a colourable device and camouflage to claim u/s 54F of the Act.

16.1 However, here is the case before us where assessee had transferred residential house flat in the Magnolias No.MG-905-B, 5th Floor, Gurugram in favour of his wife through the gift deed on 24.l0.2017 while flat No. CN 718-A was booked on 07.12.2017. Then assessee had transferred residential house situated at Geetanjali Enclave to his wife through gift deed on 28.03.2018. While the ‘purchase’ of new asset completed in FY 2020-21.

16.2 Then we find that in MG 905 and the property situated at Geetanjali Enclave, New Delhi assessee was the co-sharer with his wife and that the gift deed with regard to MG 905 was executed on 24.10.2017 and with regard to Geetanjali Enclave property executed on 27.03.2018 only changed the status of wife as co-sharer to a full-fledged owner.

17. Further, in the case before us assessee has come up with a plea that assessee had received possession letter of the new asset on 17.12.2021. The copy of same is available at page No. 313-314 of the paper book. The copy of possession letter dated 30.12.2020 is also made available at page No. 309 the details of payment for this new asset are provided at page No. 310 – 312 and same establish that during AY: 2021-22 assessee has paid Rs.1,38,70,000/- to RB Construction for carrying out the construction work in the flat CM 718A which is a new asset. Thus, for all purposes the purchase of new asset falls during present financial year and certainly the transfer of co-sharer interest by the assessee in MG 905 and Geetanjali Enclave property on 24.10.2017 and 27.03.2018 are not so immediate so as to draw inference of colourable device.

18. Assessee while disclosing the source of payment for this new asset had claimed that apart from long term capital gain earned assessee had received Rs.89,50,000/- from his wife as a gift during AY: 2021-22. Thus, the gift executed by the husband assessee can very well be part of a family arrangement wherein assessee had withdrawn his interest in the joint properties as he was acquiring the new asset independently in his own name. We are of the considered view that gift of a property to wife specially when she is a co-sharer in the property cannot be considered to be a colourable device and camouflage transaction to taint claim of Section 54F. At the same time the co-ownership of the two properties itself makes it doubtful that same can be considered to be an embargo for claim of benefit of Section 54F of the Act. Thus, this discussion leads us to a conclusion that ld. tax authorities below have fallen in error to consider assessee not eligible for exemption u/s 54F of the Act for owning more than one residential house other than the ‘new asset’ on the date of transfer of original asset.

19. At the same time, the contention of ld. First Appellate authority that sale deed has not been executed in favour of the assessee of the new asset is also not sustainable to deny benefit u/s 54F of the Act as per ‘purchase’ of new asset is not an incident of execution of sale deed alone. The ‘purchase’ for the purpose of Section 54F of the Act has to be considered on a broader perspective and what is material is to understand if the assessee as the vendee of property has acquired right and interest in a new asset which is superior to the rights of the seller thereby giving assessee right of possession, enjoyment and even right to transfer superior to that of the seller. On payment, there is no dispute that assessee had made the complete payment of the new asset rather the addition made u/s 56(1) of the Act by the Assessing Officer as sustained by ld. CIT(A) factors in favour of the assessee that assessee has concluded that deal of purchase of new asset during the financial year because in that eventuality only revenue could have asserted deemed income arising out of rebate as income from other sources.

20. Coming up to the objection of ld. DR that the very transaction of earning of long term capital gain is doubtful for which she has relied certain observations of ld. CIT(A) we find that Assessing Officer had categorically observed at page No. 4 concluded lines as follows:

“From the above it is evident that the assessee is in possession/occupation of more than one residential house on the date of transfer of capital assets. Hence the assessee is not eligible for deduction u/s 54F over and above the reasons cited in the above paragraphs.”

20.1 Similarly, in the assessment order in para 4 Assessing Officer had observed as follows:

“In response to notice u/s 142(1) dated 14/10/2022, vide submission dated 01/11/2022, the assessee filed source of funds and nature of such credits, details of funds received from First Meridian Business Services P Ltd, the credits in assessee’s bank account from Smt. Ira Dash Rajguru(spouse of the assessee), copy of ledger maintained with various stock/share brokers, details of assets and liabilities as at 31.03.2021 and details of payments made to DLF CLin connection with acquisition of apartment.

In response to Notice u/s 142(1) dated 25/11/2022, the assessee filed reply on 29/11/2022 and furnished details such as credits and withdrawals in his bank account above Rs.5,00,000/details of payments to RB Constructions and rebate to the tune of Rs.9,81,39,230/- allowed by the DLF Limited.”

21. Thus, it is only the question of ‘eligibility’ of fulfillment of conditions u/s 54F was raised and assessing officer has not at all questioned or doubted the earning of long term capital gain. These observations also show that in fact assessee had provided the details of earning of the long term capital gain.

22. We have also gone through the copy of relevant evidences as part of the paper book and we find that assessee in his submission before the Assessing Officer dated 01.11.2022 copy of which is available at page 102 to 190 had provided coy of statement of capital gain/loss of assessee for AY: 2021-22 provided by ASK Financial Year towards portfolio, copy of statement of capital gain/loss of assessee for AY: 2021-22 provided by Burgundy Private portfolio by Axix Bank, copy of capital gains report by HSBC bank for AY: 2021-22, copy of capital gain report by Kotak Mahindra Bank for AY: 202122. Earlier by reply dated 10.08.2022 copy of which is available at page No. 2-101of the paper book assessee had provided copy of share purchase and agreement dated 18.04.2018 of V5 Global Service Pvt. Ld. Thus, the observations of NFAC as relied by ld. DR to question the earning of long term capital gain itself have no substance.

23. In the light of the aforesaid facts and circumstances as discussed we are of the considered view that tax authorities below have fallen in error in declining the claim of Section 54F of the Act. Consequently, these grounds in hand No. 3 & 4 are allowed.

24. The remaining grounds are consequential and require no separate adjudication. As a consequence of aforesaid discussion appeal of the assessee is allowed. The impugned additions and disallowance are deleted with consequence to follow.