ORDER

B.M. Biyani, Accountant Member.- Feeling aggrieved by order of first-appeal dated 15.01.2025 passed by learned Commissioner of Income-Tax (Appeals)-NFAC, Delhi [“CIT(A)”] which in turn arises out of assessment-order dated 23.03.2023 passed by learned Assessment Unit of Income-tax Department [“AO”] u/s 147 r.w.s. 144 & 144B of Income-tax Act, 1961 [“the Act”] for Assessment-Year [“AY”] 2018-19, the assessee has filed this appeal on following grounds:

“Ground1. Because the very initiation of proceeding us 147 and issuance of notice u/s 148 are bad in law, invalid and therefore, the assessment is liable to be annulled.

Ground2. Because the initiation of proceeding u/s 147, 148, and completion of assessment order u/s 144 are bad in law as well as on facts and are liable to be annulled.

Ground3. The Learned A. O. has erred in computation of Long-term capital gain on fact that he has not considered the basic exemption limit of Rs. 2,50,000/-

Ground4. The Learned A.O. has erred in taking the consideration for sale of land as Rs. 1,29,73,500/- to arrive at capital gain of Rs. 1,29,73,500/-ignoring the consideration shown in documents of transfer of land and in the ITR filed by the appellant in response to notice issued u/s 148.

Ground5. The Learned Assessing Officer has erred in passing the assessment order without applying the provisions of Section 50C(2) of the Income Tax Act, 1961, regarding the valuation of the property. The Ld. AO has failed to consider the provisions allowing the taxpayer to dispute the stamp duty value by obtaining a report from a registered valuer under Section 50C(2), which was duly requested by the Appellant verbally during the course of assessment.

Ground6. The learned A.O. has erred in treating Cost of Acquisition of land to be Rs. NIL ignoring the Fair Market Value as on 01.04.2001 for the purpose of computation of long-term Capital gains.

Ground7. The learned A.O. has erred in treating Cost of improvement of land to be Rs. NIL ignoring the necessary Expenditure incurred on the plots sold.

Ground8. That the appellant craves leave to add to amend alter modify substitute withdrawal delete or rescind all or any of the above grounds of appeal on or before the final hearing if necessary, so arises.

Ground9. The appellant prays that the order passed shall be quashed, and the additions made therein be deleted, as the same are unjustified., erroneous and contrary to the applicable provisions of law. “

2. The background facts leading to present appeal are such that the AO, on the basis of information available in INSIGHT Portal of Income-tax Department revealing certain sale transactions of immovable properties done by assessee during the previous year 2017-18 relevant to AY 2018-19, issued notice u/s 148A(b) which remained uncompiled by assessee. Thereafter, the AO issued notice u/s 148 for making assessment u/s 147, followed by notices u/s 142(1) and show-cause notices. However, all notices remained uncompiled by assessee except that the assessee made limited compliance by way of filing return of income on 07.02.2022 in response to notice u/s 148 and filing a part-reply on 12.03.2023/14.03.2023 [Para 2 of assessment-order]. In the return of income so filed, the assessee declared aggregate sale proceed of Rs. 4,50,000/- of three (3) properties, cost of acquisition/ improvement of Rs. 26,49,806/- and taxable long-term capital gain of Rs. (-) 21,99,806/-. Further in his reply filed to AO, the assessee submitted that the properties sold by him were disputed and having litigation. The reply of assessee is extracted by AO in Para 6 of assessmentorder and the same is also re-produced by us in subsequent Para No. 5 of this order. As against assessee’s submission, the AO assessed aggregate sale consideration of five (5) properties amounting to Rs. 1,29,73,500/- as taxable long-term capital gain without giving any deduction of cost and completed assessment. Aggrieved, the assessee carried matter in first-appeal but the CIT(A) did not grant relief for lack of evidences/documents. Now, the assessee has come in next appeal before us.

3. We have heard learned Representatives of both sides and perused the case record including the orders of lower authorities and the documents filed in Paper-Book.

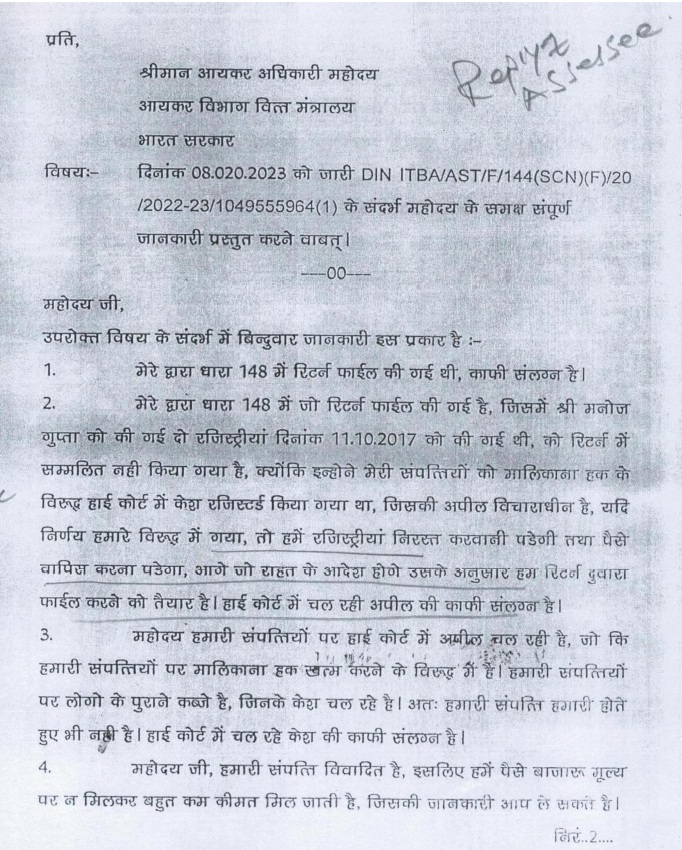

4. Ld. AR for assessee at first carried us to the reply-letter filed by assessee to AO during assessment-proceeding; Copy of same available at Pages 11-12 of Paper-Book is scanned and re-produced below for an immediate reference:

5. Thereafter, Ld. AR carried us to the assessment-order and demonstrated that the AO has considered following five (5) transactions of immovable properties for making impugned addition of Rs. 1,29,73,500/-:

| Sl. |

Date of transaction |

Name of purchaser |

Market value (Stamps duty value) |

Sale consideration received |

Taxed in assessee’s hands (% of Market Value) |

Amount |

| 1 |

11.10.2017 |

Manoj Kumar Gupta |

1,08,18,000/- |

12,00,000/- |

50% |

54,09,000 |

| 2 |

11.10.2017 |

Mo Soab |

6,84,000/- |

1,00,000/- |

50% |

3,42,000 |

| 3 |

11.10.2017 |

Manoj Kumar Gupta |

56,07,000/- |

8,00,000/- |

50% |

28,03,500 |

| 4 |

28.12.2017 |

Shakeel Ali Hasmi |

19,85,000/- |

1,70,000/- |

100% |

19,85,000 |

| 5 |

28.12.2017 |

Saeed Ajimuddin |

24,34,000/- |

2,30,000/- |

100% |

24,34,000 |

|

Total |

|

|

|

|

1,29,73,500 |

6. Finally, Ld. AR made a straightforward submission with regard to the grievances and prayers of assessee, as under:

(i) Transactions at S.No. 2, 4 & 5:

The assessee has accepted and disclosed these three (3) transactions in the return of income filed to AO on 07.02.2022 in response to notice u/s 148. Copy of the return filed by assessee is placed at Pages 13-35 in Paper-Book. Referring to Page 9 of Return [Page 21 of PaperBook], it is demonstrated that the assessee disclosed aggregate sale-proceed of Rs. 4,50,000/-, which consists of Rs. 50,000 (50% share in Rs. 1,00,000/-) for transaction no. 2 (+) Rs. 1,70,000/- for transaction no. 4 (+) Rs. 2,30,000/- for transaction no. 5. Thus, the assessee has accepted the sale transactions at S.No. 2, 4 & 5 and declared the capital gain arising therefrom in return of income. However, the assessee’s limited grievance qua these transactions is such that the sold properties were disputed and the assessee had to sell them at much lower prices due to litigation. The assessee’s submission is that the “actual” sale considerations as received by him were recorded in the registered sale-deeds and also reported in the return of income; the assessee did not receive a single penny over and above from the purchasers. These facts were clearly informed by assessee to AO in the reply-letter filed (re-produced above). However, the AO has taxed the Stamps Authority Valuations in assessee’s hands without making any reference to the Departmental Valuation Officer (DVO) and without giving benefit of section 50C(2)/(3). Therefore, the assessee prays for remanding this issue to the file of AO with a direction that the AO shall make a reference to the Departmental Valuation Officer (DVO) and finalise taxable amount of these transactions in accordance with the provisions of section 50C(2)/(3). Ld. AR relied upon (i) Ramesh Mangal v. ACIT [IT Appeal No. 461(Ind) of 2018, dated 20-11-2019], (ii) CIT v. Chandni Bhuchar (Punjab & Haryana)/TA No. 653 of 2009, order dated 07.01.2020 (P&H High), and (iii) Kiran Ashok Desai v. PCIT [IT Appeal No. 1794(Mum) of 2024, dated 21-08-2024 ], wherein the courts have given such a direction to AO in similar cases.

(ii) Transactions at S.No. 1 & 3:

These two (2) transactions of sale were made with the purchaser “Manoj Kumar Gupta” but a serious litigation cropped between assessee and purchaser due to which the deals had to be cancelled. According to Ld. AR, the assessee has already executed cancellationdocuments of transactions, therefore the transactions stand cancelled and no capital gain is taxable. Ld. AR further narrated that the assessee has also developed a dispute with the counsel involved in execution of cancellation-documents, therefore the counsel has not provided copies of cancellation-documents to assessee. The assessee is, however, making all efforts to obtain cancellation-documents and will file the same to AO. Accordingly, in the situation, the assessee prays that this issue must also be remitted to the file of AO for a fresh adjudication after examining the evidences of cancellation to be filed by assessee. Ld. AR makes a further request that in the event the assessee is unable to file the evidences of cancellation or the AO is not satisfied with the assessee’s claim of cancellation for any reason, a further direction should be given to the AO for making a reference to the DVO and finalise the taxability of these transactions in accordance with the provisions of section 50C(2)/(3).

(iii) Deduction of cost – in all five (5) transactions:

Ld. AR submitted that the AO has taxed the entire sale-consideration of properties as ‘capital gain’ without giving any deduction for cost of acquisition/improvement allowable to assessee, therefore the income assessed by AO is against the provisions of section 45(1) r.w.s. section 48 and 55(1)/(2) of the Act. Therefore, the AO must be directed to give deduction of cost to assessee. Ld. AR acknowledges that the assessee shall file required details/documents to AO in this regard.

7. Replying to same, Ld. DR for revenue though dutifully supported the orders of lower authorities yet was fair enough in accepting that the prayers made by assessee may be accepted. However, Ld. DR submitted that the bench must give stricter directions to the assessee for co-operation and filing of details/documents as and when called by AO without seeking unnecessary adjournments.

8. We have considered submissions made by learned Representatives as narrated above. Considering the totality of facts of case and the submissions of both sides, we find merit in the prayers made by the assessee/Ld. AR as narrated above. Accordingly, we remit following issues to the file of AO for a fresh adjudication:

| (i) |

|

The issues relating to the transactions at S.No. 2, 4 & 5 are restored to the file of the AO with a direction to make a reference to the DVO and re-compute taxable capital gains in accordance with provisions of section 50C(2)/(3) after affording reasonable opportunity of being heard to the assessee. |

| (ii) |

|

The issues relating to the transactions at S.No. 1 & 3 are restored to the file of the AO for fresh adjudication after examining the evidences relating to cancellation of transactions to be filed by the assessee. In case the AO is not satisfied with the claim of cancellation or in the event of non-furnishing of such evidences, the AO shall make a reference to DVO and re-compute the capital gains in accordance with provisions of section 50C(2) / (3) after affording reasonable opportunity of being heard to the assessee. |

| (iii) |

|

We further direct the AO to allow the cost of acquisition/improvement, as admissible u/s 48 r.w.s. 55(1)/(2) of the Act after carrying out necessary exercise and after verification of details and documents to be furnished by the assessee. |

9. The assessee is directed to co-operate fully in the set-aside proceedings and to file all requisite details and evidences as and when called for by the AO, without seeking unnecessary adjournments.

10. Resultantly, this appeal is allowed for statistical purpose.