Late Filing of Form 10B Not Fatal if Filed Before Assessment Completion.

Issue

Can a charitable trust’s exemption under Section 11 be denied on the grounds that the mandatory audit report in Form 10B was filed after the due date of the income tax return, even if it was filed before the assessment was completed?

Facts

- The assessee-trust filed its income tax return for the Assessment Year 2017-18, claiming exemption under Section 11.

- The required audit report in Form 10B was filed after the due date prescribed under Section 139(1).

- However, the form was duly submitted before the assessment proceedings were completed by the Assessing Officer (AO).

- The AO disallowed the Section 11 exemption, holding that filing Form 10B by the due date was a mandatory and inflexible condition.

Decision

- The court ruled in favour of the assessee.

- It held that the delay in filing Form 10B was a procedural irregularity and not a fatal defect that would extinguish the right to claim the exemption.

- Since the audit report was available to the Assessing Officer before the assessment was finalized, the officer had the opportunity to verify the claim.

- Therefore, the exemption under Section 11(2) could not be denied on this purely technical ground.

Key Takeaways

- Substance Over Form: This ruling prioritizes the substantive fulfillment of conditions (i.e., being a genuine trust and applying income for charity, as certified in the audit report) over strict adherence to procedural deadlines.

- Curable Defect: The late filing of Form 10B is a curable defect. The defect is cured when the form is submitted, as long as it is done before the assessment is completed.

- Filing Before Assessment is Key: The critical timeline for a taxpayer in such cases is to ensure all required documents are on record before the AO passes the final assessment order.

Donating Accumulated Funds to Other Trusts is a Violation of Section 11(3).

Issue

Whether funds accumulated by a trust for a “specified purpose” under Section 11(2) are taxable as deemed income if they are not utilized for that purpose but are instead donated to other trusts.

Facts

- In Assessment Year 2012-13, the assessee-trust had accumulated funds under Section 11(2), declaring they would be utilized for a “specified purpose” within the subsequent five years.

- The trust failed to utilize the accumulated amount for the purpose it had originally specified.

- Instead of using the funds, the trust donated this amount to other charitable trusts.

- The Assessing Officer (AO) treated this as a violation of the accumulation conditions under Section 11(3) and taxed the amount as deemed income for the Assessment Year 2017-18.

- The Commissioner (Appeals) upheld this addition.

Decision

- The court ruled in favour of the revenue.

- It affirmed the “well-reasoned finding” of the Commissioner (Appeals).

- The court held that the act of donating the accumulated funds, rather than applying them for the declared specified purpose, constituted a clear violation of the provisions of Section 11(3).

- Therefore, the court found no reason to interfere with the order upholding the taxation of this amount.

Key Takeaways

- Accumulated Funds are Not Fungible: Funds accumulated under Section 11(2) are “specified” for a reason. They are legally tied to the purpose declared by the trust and cannot be diverted.

- Donation is Not “Utilization”: While donating to another trust is normally a valid application of current year’s income, it is not a valid utilization of past accumulated funds. Such funds must be applied directly by the trust for the purpose it had declared.

- Breach of Condition Leads to Taxation: Any misapplication or non-utilization of Section 11(2) funds within the permissible period results in the amount being treated as deemed income in the year of the breach.

IN THE ITAT MUMBAI BENCH “G”

Yuvak Pratishthan

v.

Income-tax Officer

Justice C.V. Bhadang, President

and Ms. Padmavathy S, Accountant Member

and Ms. Padmavathy S, Accountant Member

IT. Appeal No. 3347 (Mum) of 2025

[Assessment year 2023-24]

[Assessment year 2023-24]

OCTOBER 22, 2025

Ms. Kinjal Bhuta, Adv. for the Appellant. Arun Kanti Datta, CIT-DR for the Respondent.

ORDER

Ms. Padmavathy S, Accountant Member.- This appeal by the assessee is against the order of the Commissioner of Income Tax (Appeals)/ Addl. / JCIT(A)-3, Chennai [In short ‘FAA’] passed under section 250 of the Income Tax Act, 1961 (the Act) dated 20.03.2025 for Assessment Years (AY) 2023-24. The assessee raised the following grounds of appeal:

“1. The Ld Addl/Jt Commissioner of Income tax has erred in confirming the additions made in Intimation u/s 143 (1)(a)(ii) as Income chargeable to tax under section 115BBI of the Income tax Act by Rs 57,21,300/- disregarding the fact that this amount represents Amount spent out of accumulation of Year 16-17 and reported in Form 10 filed and Revised Form 10B filed by Auditor on 07/02/25.

2. The Ld Addl/Jt Commissioner of Income tax has erred in confirming the addition stated in Ground no 1 above u/s 143 (1)(a)(ii) by not considering the Revised Form no 10B filed on 07/02/25 during the course of Appeal proceedings.

3. The Ld Addl/Jt Commissioner of Income tax has erred in confirming the addition stated in Ground no. 1 above u/s 143 (1)(a)(ii) by not allowing virtual hearing as requested by the appellate in submission letter dated 10/03/25 e-filed on 11/03/25.”

2. The assessee is a Trust formed on 30.07.1980 and registered with Charity Commissioner, Mumbai. The assessee filed the return of income for AY 2023-24 on 30.11.2023 and in the return of income the assessee offered to tax the unutilized amount of earlier years accumulation amounting to Rs. 2,06,06,960/- and paid tax under section 115BBI of the Act at the maximum marginal rate. The amount offered to tax by the assessee represents the deemed income as per section 11(3) of the Act. During the year under consideration the assessee has income/receipts from activities of the Trust amounting to Rs. 2,98,66,359/- and the same was claimed as exempt under section 11. According to the assessee since the income from activities of the Trust did not exceed Rs. 5 crores the assessee filed Audit Report under Form 10BB as per Rule 17B of the Income Tax Rules, 1962 (the Rules). The relevant Rules read as under:

“Audit report in the case of charitable or religious trusts, etc.

17B. The report of audit of the accounts of a trust or institution which is required to be furnished under sub-clause (ii) of clause (b) of sub-section (1) of section 12A, shall be in—

(a) Form No. 10B where—

(I) the total income of such trust or institution, without giving effect to the provisions of sections 11 and 12 of the Act, exceeds rupees five crores during the previous year; or

(II) such trust or institution has received any foreign contribution during the previous year; or

(III) such trust or institution has applied any part of its income outside India during the previous year;

(b) Form No. 10BB in other cases.

3. The return of the assessee was processed and the an adjustment notices was issued under section 143(1)(a)(ii) stating that since the total income of the assessee exceed to Rs. 5 crore the Audit Report should have been filed in Form 10B. Out of abundant caution the assessee filed Form 10B on 16.01.2024 and in the said Form 10B the assessee has inadvertently reported the income to be taxed under section 115BBI as Rs. 57,21,300/- instead of Rs. 2,06,06,960/- which is the unutilised amount out accumulation as declared in the return of income. The CPC called for a clarification with regard to the mismatch and the assessee responded on 03.12.2024 stating that the figure was mentioned mistakenly. The CPC however issued intimation under section 143(1) on 20.12.2024 making an addition of Rs. 57,21,300/- over and above the income declared by the assessee under section 115BBI of the Act. The assessee filed revised Form 10B on 07.02.2025 rectifying the error in the income reported under section 115BBI of the Act. Aggrieved the assessee filed the appeal before the FAA. The FAA did not accept the revised Form on the ground that the assessee should have filed the revised Form 10B before the issuance of intimation under section 143(1) and not during the appellate stage. The assessee is in appeal before the Tribunal against the order of FAA.

4. The first contention of the ld. AR is that in assessee’s case the Audit Report has been correctly filed initially under Form 10BB since in assessee’s case the income during the year is not exceeding with threshold of Rs. 5 crore. The ld. AR further submitted that as per Rule 17B the income before giving effect to the provisions of section 11 & 12 should be considered for the purpose of deciding which form to be filed i.e. Form 10B in case the income exceeds to Rs 5 crores and in any other case Form 10BB. The ld. AR also submitted that the deemed income of Rs. 2,06,06,960/- is offered to tax under section 11(3) and therefore the same should not be taken into account for the purpose of the income under Rule 17B. Accordingly the ld. AR argued that the CPC should have processed the return of the assessee by considering the Form 10BB originally filed by the assessee. Without prejudice the ld. AR took the Bench through the Form 10B filed originally and the corrected Form 10B to submit that the assessee has inadvertently mentioned the actual amount applied out of earlier year accumulation as the amount offered to tax. The ld. AR argued that the CPC while processing the return did not consider the clarification provided in this regard. The ld. AR further argued that the assessee has filed the revised Form 10B after correcting the error and the same should have been considered by the FAA.

5. The ld. DR on the other hand relied on the order of the lower authorities.

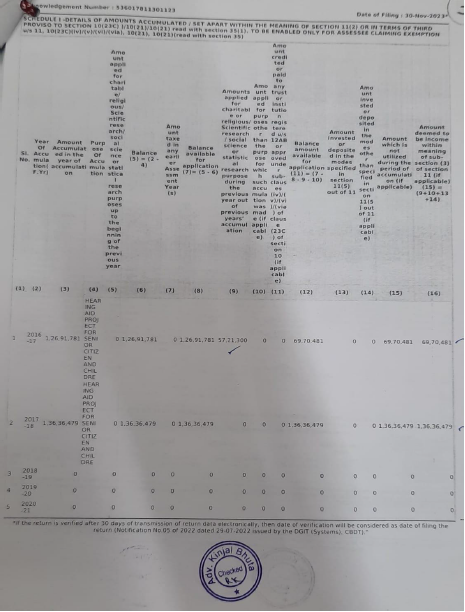

6. We heard the parties and perused the material on record. The assessee while filing the return of income offered to tax the unapplied amount accumulated in the earlier years to the tune of Rs. 2,06,06,960/-. The relevant abstract from the return of income filed by the assessee is extracted below:

7. We further notice that the assessee in Form 10BB (page 16 to 18) has declared Rs. 2,06,06,960/- as income deemed under section 11(3) of the Act.

8. We also notice that the assessee in the first Form 10B filed has stated the deemed under section 11(3) to be Rs. 57,21,300/- (page 37 of PB). The assessee filed the second Form 10B correcting the error and by offering the deemed under section 11(3) to the tune of Rs. 2,06,06,960/-. From the combined perusal of the above facts we see merit in the submission of the ld. AR that mentioning Rs. 57,21,300/- as deemed income is an inadvertent arithmetical error since the said sum is the amount actually applied by the assessee out of the accumulations of the earlier year. Accordingly, we hold that the FAA is not correct in confirming the addition made by the CPC to the tune of Rs. 57,21,300/- and the same is to be deleted.

9. Now coming to the alternate plea of the assessee that Form 10B is not applicable for the reason that the income of the assessee does not exceed Rs. 5 crore. From the perusal of Rule 17B as extracted in the earlier part of this order, we notice that the monetary limit of Rs. 5 crore is at a gross level without giving effect to the provisions of sections 11 and 12 of the Act. The receipts of the assessee during the year under consideration is Rs. 2,98,66,359/- and the ld AR argued that this is the amount that should be considered for the purpose of Rule 17B and not the deemed income under section 11(3). During the year under consideration the assessee offered deemed income to the tune of Rs. 2,06,06,960/-under section 11(3) of the Act for the reason that the said amount has not been utilised for the purpose for which it is accumulated. Section 11 contains provisions relating to mode of computation of income from property held for charitable purpose and the conditions under which the income of the trust shall not be taxable. From the plain reading of Rule 17B, it is clear that the effect of section 11 be it the deductions or the deemed income cannot considered for the purpose of considering the monetary limit of Rs.5 crores. Accordingly on this count also the assessee succeeds. The AO is thus directed to the delete the addition made considering the information declared by the assessee in Form 10BB with regard to the income applied & unapplied out of the accumulation.

10. In result, appeal filed by the assessee is allowed.