HC Applies Subsequent CBIC Circular to Quash GST Demand on Reinsurance Services.

Issue

Whether a taxpayer can be denied the benefit of a subsequent, beneficial CBIC circular (which grants an exemption for a past period) if the tax demand for that period was already confirmed by adjudication and appellate authorities before the circular was issued.

Facts

- The petitioner, an insurance company, faced a GST demand on reinsurance services for the period 01 July 2017 to 24 January 2018.

- The tax authorities issued a Show Cause Notice (SCN) on 27 September 2023, followed by an Order-in-Original (OIO) on 29 December 2023 and an Order-in-Appeal (OIA) on 11 July 2024, all confirming the GST levy.

- A few days later, on 15 July 2024, the CBIC issued Circular No. 228/22/2024-GST. This circular extended a GST benefit/exemption for reinsurance services, and it explicitly covered the disputed period.

- The petitioner filed a writ petition, arguing that this new, beneficial circular should be applied to their case, and the existing demand orders should be quashed.

Decision

- The High Court set aside (quashed) both the Order-in-Original (OIO) and the Order-in-Appeal (OIA).

- It held that the new CBIC circular squarely applied to the disputed period and the nature of the transaction.

- The court ruled that the assessee could not be denied the benefit of the circular simply because the lower authorities had passed their orders just days before the circular was issued.

- The High Court directly extended the benefit of the circular to the petitioner, rendering the tax demand invalid.

Key Takeaways

- Beneficial Circulars Have Overriding Effect: A beneficial circular issued by the CBIC, which clarifies the law for a past period, is binding on the department and must be applied to all relevant cases.

- Timing of Order vs. Circular: A taxpayer’s right to a benefit granted by a circular is not defeated just because the adjudicating or appellate authority passed their order before the circular’s publication.

- Writ Jurisdiction for Swift Justice: The High Court can exercise its writ jurisdiction to set aside orders that are contrary to a subsequently issued, but retroactively applicable, beneficial circular. This prevents further protracted litigation and ensures the circular’s intent is implemented.

- Finality of Law: The circular was intended to settle the ambiguity for this specific period. The court’s decision gives immediate effect to this intended settlement.

CM APPL. No.42261 of 2025

| (i) | Order-in-Appeal No. 262/Commr./Central-Tax/Appeal-I/ Delhi/2024 dated 11th July 2024 passed by the ld. Commissioner (Appeals-i), CGST, Delhi; |

| (ii) | Order-in-Original No. 58/ADC/D.N./Manish Kumar Jha/2023 dated 29th December, 2023 passed by the Respondent No. 1 and |

| (iii) | The Show Cause Notice [FORM GST DRC-01] bearing Reference No. 50/GST/2023-24 dated 27th September, 2023 issued by the Respondent No.2. |

| (1) | (2) | (3) | (4) | (5) |

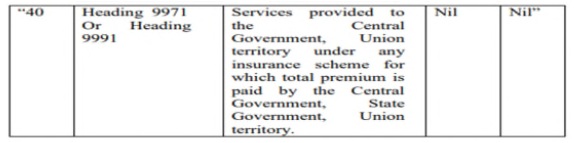

| “36A | Heading 9971 or Heading 9991 | Services by way of reinsurance of the insurance schemes specified in serial number | Nil | Nil” |

“(k) against serial number 36A, in the entry in column (3), after figures “36”, the word and figures “or 40″ shall be inserted;”

“5.46 Joint Secretary, TRU then presented the next agenda item relating to a request to clarify that reinsurance services of the insurance schemes for which total premium is paid by the Government (Sl. No. 40 of the notification No. 12/2017 CTR) are exempt from GST for the period 01.07.2017 to 26.07.2018. She stated that in the 28th GST Council meeting held on 21.07.2018, it was decided to exempt re-insurance of insurance schemes already exempt under Sl. No. 40 of Notification No. 12/2017-CTR. The said exemption was notified w.e.f. 27.07.2018. The issue was examined by the Fitment Committee and it recommended to regularize the payment of GST on reinsurance services of the insurance schemes for which total premium is paid by the Government (SI No. 40 of Notification No. 12/2017-CT(R) dated 28.06.2017) for the period from 01.07.2017 to 26.07.2018 on „as is where is” basis by way of issuance of a Circular.

Decision: The Council approved the recommendation of the Fitment Committee to regularize the payment of GST on reinsurance services of the insurance schemes for which total premium is paid by the Government (SL. No. 40 of Notification No. 12/2017-CT(R) dated 28.06.2017) for the period from 01.07.2017 to 26.07.2018 on ‘as is where is’ basis by way of issuance of a Circular. ”

“”6. GST liability on the reinsurance of specified general and life insurance schemes.

6.1 Representations have been received to either exempt or regularize the GST liability, for the period from 01.07.2017 to 24.01.2018, on reinsurance of specified general insurance and life insurance schemes, which are exempt from GST. 6.2 Certain specified general insurance and life insurance schemes are exempt from GST under Sl. Nos. 35 and 36 of notification No. 12/2017- CT(R) dated 28.06.2017. Vide entry at Sl. No. 36A of the said notification, reinsurance of the aforesaid exempted insurance schemes has also been exempted w.e.f. 25.01.2018. 6.3 GST Council in its 53rd meeting held on 22nd June, 2024 has recommended to regularize the GST liability on such reinsurance of exempt general insurance and life insurance schemes for the past period, i.e. from 01.07.2017 to 24.01.2018, on „as is where is” basis.

6.4 Thus, as recommended by the GST Council, GST liability on the services by way of reinsurance of the insurance schemes specified in Sl. Nos. 35 and 36 of notification No. 12/2017-CT(R) dated 28.06.2017 is regularized for the period from 01.07.2017 to 24.01.2018 on „as is where is” basis.”