Earning Rental Income to Fund Charity Does Not Bar Tax Registration.

Issue

Can a charitable trust be denied registration under Section 12A of the Income-tax Act on the grounds that it earns substantial rental income from letting out shop spaces, and does this rental activity constitute a “business” that violates the conditions for a charitable purpose under Section 2(15)?

Facts

- The assessee-trust was engaged in educational and philanthropic (charitable) activities.

- To financially support these charitable objects, the trust let out shop spaces located within its premises and earned rental income.

- The Commissioner (Exemption) rejected the trust’s application for final registration under Section 12A and also cancelled its existing provisional registration.

- The Commissioner’s sole reason for rejection was that earning substantial rental income was a “business activity” and, therefore, the trust was not genuinely charitable.

Decision

- The High Court ruled decisively in favour of the assessee.

- It held that earning rental income by letting out a part of the trust’s premises to fund its main charitable objects does not attract the proviso to Section 2(15) (which restricts commercial activities).

- The court concluded that since this activity did not disqualify the trust from being charitable, the assessee could not be denied registration under Section 12A.

Key Takeaways

- Renting to Fund Charity is Not “Business”: The act of letting out property to generate funds that are then applied to the trust’s main charitable objects (like education) is not considered a “business” that would disqualify the trust.

- Motive is Key: The dominant purpose of the trust remains charitable. The rental income is merely a means to an end (funding charity), not the primary object itself.

- Proviso to Section 2(15) Not Attracted: The restriction on “trade, commerce, or business” in Section 2(15) is not intended to stop a trust from engaging in incidental activities that help it achieve its charitable goals.

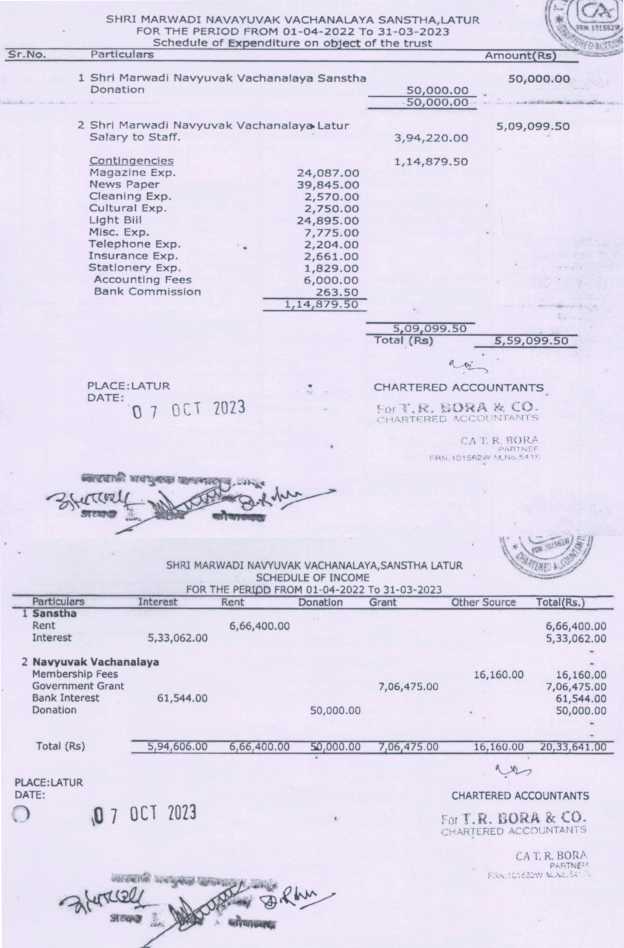

- Registration Cannot Be Denied: A trust cannot be denied registration for having an income-generating activity, provided that activity is incidental to its main charitable purpose and the income is used to further those objects.

IN THE ITAT PUNE BENCH ‘A’

Marwadi Navyuvak Vachanalaya

v.

Commissioner of Income-tax(Exemption)

Justice C.V. Bhadang, President

and R.K. PANDA, Vice President

and R.K. PANDA, Vice President

IT Appeal No. 561 (PUNE) OF 2025

SEPTEMBER 29, 2025

Bhuvanesh Kankani for the Appellant. Amol Khairnar, CIT-DR for the Respondent.

ORDER

R.K. Panda, Vice President. – This appeal filed by the assessee is directed against the order dated 27.12.2024 of the Ld. CIT(Exemption), Pune rejecting the application for grant of registration u/s 12A of the Income Tax Act, 1961 (hereinafter referred to as ‘the Act’) and cancelling the provisional registration granted earlier u/s 12AB of the Act.

2. Facts of the case, in brief, are that the assessee filed an application in Form No.10AB on 29.06.2024 for registration of the trust under clause (iii) of section 12A(1)(ac) of the Act. With a view to verify the genuineness of the activities of the assessee and compliance to requirements of any other law for the time being in force by the trust / institution as are material for the purpose of achieving its objects, a notice was issued through ITBA portal on 08.08.2024 requesting the assessee to upload certain information / clarification. From the details furnished by the assessee in response to the said notice, the Ld. CIT(E) noticed various discrepancies for which he issued another notice to the assessee on 25.09.2024 communicating the discrepancies. The assessee in response to the same filed various details. The Ld. CIT(E) noticed still certain discrepancies for which he issued another notice to the assessee on 28.11.2024. From the reply so received from the assessee the Ld. CIT(E) noticed that the assessee has received rental income of Rs.6,66,400/- on account of renting of shop spaces within its premises. The assessee in response to the query raised by the Ld. CIT(E) submitted that the shops were established as part of the trust’s premises which later on were rented and used as source to generate a sustainable source of income, which would help fund its core educational and philanthropic activities. It was submitted that every rupee of the rental income is directed towards fulfilling the trust’s objectives such as subsidizing costs for library members to keep access affordable for financially underprivileged students, covering costs related to maintenance of the library premises, ensuring it remains a conducive environment for learning, supporting community outreach programs aimed at fostering a culture of reading and education in the region.

3. However, the Ld. CIT(E) was not satisfied with the arguments advanced by the assessee. He observed from the financial statements of the assessee that the trust is earning substantial income from renting out of properties. The assessee has not clarified as to how the receipts are from the activities intrinsic with carrying out the main objectives. He noticed that no separate books of account (financial statements) are maintained since the assessee has not furnished separate account statements for the said activity. He, therefore, was of the opinion that the receipts are prima facie from an activity in the nature of advancement of any other object of general public utility wherein fees are charged for the services rendered. In absence of such books of account it was not possible to check whether such activity was with a profit motive or not. He further noted that the activity of the trust is not in line with the objects of the assessee. He also noted that out of total income of Rs.20.33 lakhs during the financial year 2022-23, the rental income is Rs.6.66 lakhs which is a substantial amount. Thus, the primary activity is letting out property on rent which is around 32.76% of income of the trust of Rs.22.33 lakhs. He also noted that the expenditure on account of expenses on charitable activities as per the Income & Expenditure account is only Rs.50,000/- as against the income of Rs.20.33 lakhs. Similar was the position in earlier financial year 2021-22. He, therefore, held that the primary activity of the trust is letting out of property on rent which is in nature of business activity and does not amount to any charity. Since despite specifically asked to furnish supporting credible evidence in respect of activities claimed to have been carried out, the assessee failed to establish undertaking of such activities by providing cogent evidences, therefore, the Ld. CIT(E) rejected the application for grant of registration u/s 12A and cancelled the provisional registration granted earlier u/s 12AB of the Act.

4. Aggrieved with such order of Ld. CIT(E), the assessee is in appeal before the Tribunal by raising the following grounds:

| 1. | On facts and circumstances prevailing in the case and as per provisions & scheme of the Income-tax Act, 1961 (‘The Act’) it be kindly held that the order passed by the Commissioner of Income Tax Exemptions [‘CIT (E)’], Pune, rejecting the Appellants application for seeking registration u/s 12AB of the Act is against the provisions of the Act. Accordingly, the order passed by the Ld. CIT (E) be held as not tenable in law and be set aside directing the Ld. CIT(E) to grant registration. The appellant be granted just and proper relief in this respect. |

| 2. | On facts and circumstances prevailing in the case and as per provisions & scheme of the Act it be kindly held that Ld. CIT(E) erred in passing the rejection order without perusing the material available on record. Accordingly, the order passed by the Ld. CIT (E) be set aside and Ld. CIT(E) be kindly directed to grant registration. The appellant be granted just and proper relief in this respect. |

| 3. | The appellant prays to be allowed to add, amend, modify, rectify, delete, raise any grounds of appeal at the time of hearing. |

5. The Ld. Counsel for the assessee submitted that the trust was created in the year 1939 and registered under the Bombay Trust Act, 1950 and also under the Societies Registration Act, 1860. It has commenced its activities from 21.04.1965. The trust operates a library under the name of ‘Marwadi Navyuvak Vachanalaya’ with the primary aim of offering a conducive and supportive environment for financially underprivileged students to focus on their studies. Referring to pages 1 to 7 of the paper book the Ld. Counsel for the assessee drew the attention of the Bench to certain photographs showing the library and the reading rooms. Referring to page 8 of the paper book, he drew the attention of the Bench to the approval letter from the government department received on 30.01.2014. He submitted that the Ld. CIT(E) denied the claim of exemption on the ground that the trust has earned an amount of Rs.6,66,400/- annually from the renting of shops within its premises which is 32.76% of income of the trust and therefore, the primary activity of the trust is in a nature of business activity. According to him, giving properties on rent is not a charitable activity. According to him, the activities of the trust are renting out properties on commercial basis and are not charitable in nature.

6. Referring to the decision of Hon’ble Bombay High Court in the case of Director of Income Tax v. Shri Vile Parle Kelavani Mandal ITR 593 (Bombay), the Ld. Counsel for the assessee submitted that the Hon’ble High Court in the said decision has held that where assessee trust generated income by giving hall and premises of its educational institution on rentals and said income was used for educational institution itself, such income could not be brought to tax.

7. Referring to the decision of Hon’ble Madras High Court in the case of CIT v. Madras Stock Exchange Ltd. [1976] 105 ITR 546 (Madras), he submitted that the Hon’ble High Court in the said decision has held that purchasing a building and letting out some surplus area was not indulging in any activity for profit and the benefit of exemption u/s 11 of the Act cannot be denied to the assessee. He submitted that when the Revenue challenged the above decision of the Hon’ble High Court, the Hon’ble Supreme Court dismissed the appeal filed by the Revenue as CIT v. Andhra Chamber of Commerce/South Indian Chamber of Commerce/South India Film Chamber of Commerce/ Madras Stock Exchange Ltd ITR 184 (SC).

8. Referring to the decision of the Pune Bench of the Tribunal in the case of Oswal Bandhu Samaj v. ITO ITD 200 (Pune – Trib.), he submitted that the Tribunal in the said decision has held that where the assessee trust, registered under section 12A and engaged in providing medical help, education help and relief to poor had let out its halls and buildings for earning rental income so as to fund its charitable objects, proviso to section 2(15) would not be attracted and the assessee could not be denied exemption under section 11. He accordingly submitted that merely because the assessee has earned certain income by letting out certain shops inside the premises of the assessee trust, the income of which has been utilized for the purpose of attaining the main objects of the trust, cannot be a ground to disentitle the assessee to claim the exemption u/s 11 of the Act.

9. So far as the allegation of the Ld. CIT(E) that the assessee has incurred only an amount of Rs.50,000/- for charitable purposes as against the income of Rs.20.33 lakhs is concerned, the Ld. Counsel for the assessee submitted that the same is factually incorrect since the assessee has spent an amount of Rs.5,59,099.50 out of the total income of Rs.20,33,641/-.

10. The Ld. DR on the other hand heavily relied on the order of the Ld. CIT(E).

11. We have heard the rival arguments made by both the sides, perused the order of the Ld. CIT(E) and the paper book filed on behalf of the assessee. We have also considered the various decisions cited before us. We find the Ld. CIT(E) in the instant case rejected the application filed by the assessee for grant of registration u/s 12A of the Act and also cancelled the provisional registration granted earlier on the ground that the trust is earning substantial income from renting out of the property, no separate books of account are maintained, the rental income of Rs.6.66 lakh is 32.76% of the total income of the trust and the assessee has spent a meagre amount of Rs.50,000/- as against the income of Rs.20.33 lakhs. According to him, all these things show that the main activity of the trust is giving properties on rent and not to do any charity. He, therefore, held that the activities of the trust are letting out the properties on commercial basis and not to do any charity. It is the submission of the Ld. Counsel for the assessee that merely because a part of the premises of the trust has been let out on rent on which certain income is earned which has been utilized for attaining the main objects of the trust, the same cannot amount to carrying on of business activity within the meaning of section 2(15) of the Act in light of the various decisions relied on by him.

12. We find some force in the above arguments of the Ld. Counsel for the assessee. We find the Hon’ble Bombay High Court in the case of Shri Vile Parle Kelavani Mandal (supra) has held that where assessee trust generated income by giving hall and premises of its educational institution on rentals and said income was used for educational institution itself, such income could not be brought to tax. The relevant observations of the Hon’ble High Court read as under:

“5. The Tribunal has held that the “”management and development program and consultancy charges”” is part and parcel of “”Narsee Monjee Institute of Management Studies”” which has been set up by the respondent assessee. The respondent-assessee is a trust and has set up 30 schools and colleges. The Commissioner as also the Tribunal has found that the element of business is missing in conducting management courses. There may be some surplus generated which itself is applied towards the attainment of the object of the educational institute. The separate books of account cannot be insisted upon because once this programme is part and parcel of the activities undertaken and carried out by the Narsee Moonjee Institute of Management Studies, then the condition precedent set out in sub-section (4A) of section 11 of the Income-tax Act, 1961, is completely satisfied. Such finding of fact cannot be termed as perverse and it is in consonance with the factual aspect regarding the activities of the trust and the object that it is seeking to achieve. Similarly, in regard to income from the hiring of the premises and advertisement rights, the said question is also not substantial question of law. Letting out of halls for marriages, sale and advertisement rights has not been found to be a regular activity undertaken as a part of business. The educational institutions require funds. The income is generated from giving various halls and properties of the institution on rentals only on Saturdays and Sundays and on public holidays when they are not required for educational activities, then this cannot be said to be a business which is not incidental to attain the objects of the trust. This being merely an incidental activity and the income derived from it is used for the educational institute and not for any particular person, separate books of account are also maintained, then this income cannot be brought to tax. This conclusion is also not perverse and given the facts and circumstances which are undisputed.”

13. We find the Hon’ble Madras High Court in the case of Madras Stock Exchange Ltd. (supra) while deciding an identical issue has observed as under:

“The object of the Chamber was clearly to promote trade and industry. The construction of a building was for the purpose of locating its office. The Chamber fulfills many functions like arranging periodical meetings of its members in promotion of its objects, receiving officials and ministers so as to make representations in order to ensure smooth flow of trade, commerce and manufacture and helping the members in other ways conceived by it. It has necessarily to keep a house in which all these functions could be carried on. When the space available in the building was found to be surplus, it naturally made it available for rent by letting out part of it. By doing so, it was not carrying on any activity for profit as conceived by the provision. A person who lets out a property and enjoys the income therefrom, is more passive than active. It is not, therefore, reasonable to call it an activity for profit. As rightly pointed out by the learned counsel for the assessee, the whole of section 11 would be rendered useless if the construction sought to be placed for the revenue is to be accepted. If merely because there is an income either from the property or from other investments sit should be held that it is an activity for profit, then the exemption under section 11 would have no scope to operate. It would be reduced to a dead letter. Any construction which would render a provision nugatory should be avoided. Therefore, it is necessary to give scope for the exemption under section 11 keeping at the same time in mind the amendment to section 2(15). It is possible to do so in the present case by holding that the assessee by purchasing a building and letting out some surplus area was not indulging in any activity _ for profit. Section 11 does not taboo the earning of profit as, unless there was profit, there would be no need for the exemption provision. It is only on the postulate of profits being there, that any exemption provision would find a place in the statute. The effect of the contention of the learned counsel for the revenue is to show that when once there was a profit, the exemption was taken away. This, in our opinion, could not be the intention of Parliament which has granted the exemption on the profits earned. A reading of section 2(15) and section 11 together shows that what is frowned upon is an activity for profit by a charity established for general objects of public utility in the course of accomplishing its objects. There is no activity here. The activity spoken of by the provision is not a mere act of purchase of a building or making an investment and getting income therefrom, but something more substantial and continuous. We are, therefore, of the opinion that the Tribunal rightly granted the exemption to the present assessee even after the definition was amended under the 1961 Act. This would answer question No. 2. The answer is in the affirmative and in favour of the assessee. “

14. We find when the Revenue challenged the above decision, the Hon’ble Supreme Court in the case of Andhra Chamber of Commerce/South Indian Chamber of Commerce / South India Film Chamber of Commerce / Madras Stock Exchange Ltd. (supra) dismissed the appeal filed by the Revenue by observing as under:

“1. This appeal by special leave is covered by the judgment of this Court in CIT v. Andhra Chamber of Commerce and in Addl. CIT v. Swat Article Silk Cloth Manufacturers Association. It is clear from the judgment in CIT v. Andhra Chamber of Commerce, that the objects of the Andhra Chamber of Commerce fell within the last head of charitable purpose denoted by the words “advancement of any other object of general public utility” and were, therefore, charitable within the meaning of Section 2(15) of the I.T. Act, 1961, unless it could be shown that they involved the carrying on of any activity for profit. The words “not involving the carrying on of any activity for profit” came up for consideration before this Court in Addl. CIT v. Surat Article Silk Cloth Manufacturers Association, and there it was held by the majority of the judges that it was only where the predominant object and the purpose of the activity carried on was to earn profit, that the object could be said to involve the carrying on of an activity for profit but if the predominant object was to subserve the charitable purpose then the inhibition of these last 9 words would not be attracted. It is clear from the facts set out in the judgment of the High Court that profit-making was not the predominant object of the activity carried on by the Andhra Chamber of Commerce but the predominant object was to promote trade and commerce which was an object of general public utility. The High Court was, therefore, right in taking the view that the objects of the Andhra Chamber of Commerce fell within the last! category of charitable purpose given in Section 2(15) of the Act and its income was exempt from tax under Section 11(1) of the Act.

2. The appeal is accordingly dismissed with no order as to costs.”

15. We find the Coordinate Bench of the Tribunal in the case of Oswal Bandhu Samaj (supra) has held that where the assessee trust, registered under section 12A and engaged in providing medical help, education help and relief to poor had let out its halls and buildings for earning rental income so as to fund its charitable objects, proviso to section 2(15) would not be attracted and the assessee could not be denied exemption under section 11. The relevant observations of the Tribunal read as under:

“13. In order to ascertain as to which activities of the nature as given under (d) above, hit by the proviso to section 2(15), were pursued by the assessee, we proceeded to examine the Income and Expenditure Account of the assssee. Total of the Expenditure side for the year ending 31-03-2010 on page 2 of the Paper book in Income and Expenditure Account is Rs.1.92 crore. Expenditure on Medical help of Rs.50.54 lakh; Education help of Rs.62.25 lakh; and Relief to the poor covered under the head ‘Education and Charity expenses of Rs.3.46 lakh, totals up to Rs.1.16 crore. There is no dispute that the assessee let out its Cultural halls and Building from time to time for earning revenue so as to fund its charitable objects. Income from such revenuegenerating activities has been recognized on the Income side of the Income and Expenditure account. In addition to Cultural hall receipts and Building rent, the assessee expressly recovered Amenity charges of Rs.20.93 lakh; Furniture and municipal taxes of Rs.56.87 lakh; Municipal receipts of Rs.11,164/-; and DG set receipts of Rs.6.74 lakh. These recoveries were made from the persons taking Cultural Hall and Building on rent basis. As against these specific recoveries, the assessee paid Municipal taxes of Rs.23.26 lakh; Repairs and maintenance of Rs.4.77 lakh; Security staff expenses of Rs.8.18 lakh; Washing and cleaning charges of Rs.4.98 lakh; Electricity charges of Rs.5.26 lakh; DG set expenses of Rs.6.37 lakh etc. Such expenses are mostly in the nature of the amounts spent by the assessee against which specific recoveries were obtained from the users of the Building and Cultural halls. Thus, these costs are identifiable with the receipts and included in the income side of Income and Expenditure Account. Total of such costs, which have no connection with the activities for advancement of any other object of general public utility, comes to Rs.52.82 lakh. If this amount is added to expenditure incurred on Medical help; Education; and Food/relief to the poor, the total comes to Rs.169.03 lakh, as against total expenses booked on the Expenditure side at Rs.192 lakh. Remaining expenses are of usual running of the trust, such as, Depreciation amounting to Rs.7.78 lakh; Salaries of Rs.4.19 lakh; and other Administrative expenses, such as, Printing and stationery; Audit fee; Professional charges, Postage etc., leaving hardly any amount for pursuing ‘advancement of any other object of general public utility’.

14. From the above discussion, it is discernible that albeit the assessee has the objects of ‘advancement of any other object of general public utility’ in its trust-deed, but none of such objects was actually pursued during the year under consideration. Whereas the objects and activities of the trust are germane at the time of grant of registration u/s 12AA of the Act, what becomes relevant for consideration at the time of assessment is to see which of the objects, having charitable purpose, were actually carried out so as to decide the question of exemption. The above discussion makes it graphically clear that the assessee actually pursued only the objects as classified in categories (a) to (c). viz., Medical Relief to the poor patients, Education to the deserving students and Relief to the needy sections of the society and hence shied away from taking up any of the objects in category (d), viz., advancement of any other object of general public utility. Once this is the position, it becomes explicitly clear that the proviso to section 2(15), which attracts only when objects of the category (d) above are pursued, did not trigger in the instant case. The sequitur is that the assessee is entitled to exemption. It is pertinent to mention that the AO did not dispute the fulfillment of any other requirements for claiming exemption u/s 11 of the Act. We, therefore, hold that the assessee is entitled to exemption. The impugned order is, therefore, set-aside.”

16. So far as the allegation of Ld. CIT(E) that the assessee has spent a meagre amount of Rs.50,000/- only on account of charitable activities as per the Income & Expenditure account is concerned, we find the same is factually incorrect. A perusal of the Income & Expenditure account shows that the assessee has spent an amount of Rs.5,59,099.50 towards its objects, the details of which are as under:

17. In the light of the above discussion and relying on the decisions cited (supra), we are of the considered opinion that the proviso to section 2(15) of the Act would not be attracted for earning rental income by letting out a part of the premises which has been utilized for the objects of the trust. Therefore, the assessee in our opinion should not be denied registration u/s 12A. We, therefore, set aside the order of the Ld. CIT(E) and direct him to grant registration u/s 12A and also restore the provisional registration granted earlier. The grounds raised by the assessee are accordingly allowed.

18. In the result, the appeal filed by the assessee is allowed.