ORDER

Narender Kumar Choudhry, Judicial Member.- This appeal has been preferred by the Revenue against the order dated 27/08/2024 impugned herein passed by the National Faceless Appeal Centre (NFAC)/Commissioner of Income Tax (Appeals), Delhi (in short, ‘Ld. Commissioner’) u/sec. 250 of the Income Tax Act, 1961 (in short, ‘Act’) for the A.Y. 2013-14.

2. Relevant facts for adjudication of this appeal are that in the instant case, M/s. Ushodaya Enterprises (Pvt.) Ltd. (in short, ‘UEPL’) was in the business of producing and telecasting entertainment/news/ information programmes under the trade name of ETV and under the scheme of demerger/arrangement under sections 391 and 394 of Companies Act 1956, which was approved vide their Order dt. 15/12/2010 w.e.f. 01/04/2010 by the Hon’ble High Court of Andhra Pradesh, merged into three companies namely:

| (1) |

|

M/s. Eenadu Television Private Ltd. (in short “ETPL”) ; |

| (2) |

|

M/s. Prism TV Private Ltd. (in short “PTVPL”) and, |

| (3) |

|

M/s. Panorama Television Private Ltd. (in short “PTPL”) |

2.1 The non-telugu channels other than Hindi and Urdu channels were clubbed together and transferred to M/s. Prism TV Private Limited (herein called “Assessee”) against whom assessment order and impugned order were passed. The Assessee company M/s. Prism TV Private Ltd. now merged with Viacom 18 Media Pvt. Ltd. w.e.f. 01-04-2015 (herein called as “Successor Assessee”) who is now contesting the orders passed by the Authorities below.

3. The assessee had declared its income at a loss of (-) Rs. 10,21,28,267 and Books Profits of Rs. 6,36,68,006 under section 115JB of the Act, by filling its return of income for the AY under consideration on dated 30.11.2013, which was initially processed u/s 143(1) of the Act and subsequently selected for scrutiny and therefore the Assessing Officer (in short “AO”) issued the statutory notices including dated 01.07.2015 u/s.143(2) of the Act, which was duly served on the assessee.

3.1 The Assessee, in response to the statutory notices issued, furnished required information and documents. The AO on perusing the information and documents and conducting assessment proceedings, ultimately passed the assessment order dated 24/03/2016 u/sec. 143(3) of the Act, making following additions/disallowances: –

| (i) |

Rs. 15,79,57,119/- |

on account of disallowance of depreciation on non-compete fee; |

| (ii) |

Rs. 134,79,41,873/- |

on account of disallowance of cost of production of TV serials and programmes claimed as revenue expenditure; |

| (iii) |

Rs. 10,13,96,329/- |

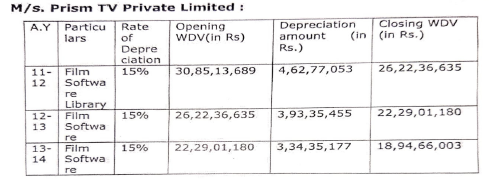

on account of disallowance of excess depreciation on “Film Software Library”; and, |

| (iv) |

Rs. 63,324/- |

on account of restriction of depreciation on computer accessories to 15%. |

4. The Assessee, being aggrieved, challenged the said additions/disallowances by filing first appeal before the Ld. Commissioner, who vide impugned order dated 27/08/2024, deleted the aforesaid additions/disallowances and, therefore, the Revenue being aggrieved, has preferred instant appeal challenging the decision of the Ld. Commissioner in deleting the aforesaid additions/ disallowances except on account of restriction of depreciation on computer accessories, by raising the followings grounds of appeal:-

“1. Whether on facts and circumstances of the case, the Id CIT(A) is correct in allowing depreciation on Noncompete fee placing reliance on the Order which was binding on the AO l.e. Order giving effect and not considering the prime reason of disallowance by the then AO Le. the necessity and genuinity of the purchase or payment of Noncompete fee.

2. Whether on facts and circumstances of the case the Ld. CIT(A) is justified in allowing the impugned claim of the whole expense of cost of TV serials and programs of Rs. 101,09,56,405/- considering the same as revenue in nature ignoring the fact that the cost incurred on production of TV Serials and programs can have enduring advantage to the business over several years and this creates long term benefits or future earning potential hence, needs to be placed under Capital Expenditure.

3. Whether on facts and circumstances of the case the Id. CIT(A) is justified in deciding the ground of disallowance of film software library without appreciating the fact that the final decision i.e. CIT(A)’s decision for appeal against the OGE order dated 31.03.2017 for AY 2007-08 from where the issue incepted is still pending and also not considering the merit of the ground.”

5. For brevity, we deem it appropriate to decide this appeal by ground-wise. Coming to ground No.1, which pertains to the depreciation on “non-compete fee” we observe from the assessment order that in the scheme of demerger, intangible asset by name of non-compete fee @ Written Down Value (WDV) of Rs. 329,76,56,250/- was distributed among ETPL, PTVPL and PTPL. The Assessee accordingly has acquired intangible asset in the name of “non-compete fee” having WDV value of Rs.112,32,50,625/- as on 01/04/2010 and for the assessment year under consideration, opening WDV worked out at Rs. 63,18,28,476/-. The Assessee thus on the said amount, worked out and claimed an amount of Rs. 15,79,57,119/- as depreciation on intangible asset namely “noncompete fee”.

6. Background of the “Non-compete Fee” is that in the A.Y. 2007-08, M/s. UEPL, which was the parent company of PTVPL has acquired Usha Kiron Television (UKT) and Usha Kiron Movies (UKM) (TV Division). Thereafter in the AY 2007-08, the erstwhile company i.e. UEPL entered into a non-compete agreement with UKT and UKM on 30/01/2008 for non-competing in the business directly or indirectly for a period of five years from the date of agreement. Accordingly, in the A.Y. 2008-09, the Assessee-company paid an amount of Rs. 670 crores towards non-compete fee and during the A.Y. 2010-11 claimed the depreciation of Rs. 109,92,18,756/-and thereafter in the AY under consideration to the tune of Rs. 15,79,57,119/- which is the subject matter or issue in question now.

7. The AO therefore, in order to examine such claim of the Assessee to the tune of Rs. 15,79,57,119/- on account of noncompete fees, examined the necessity for such non-compete fee and observed that Shri Ch. Ramoji Rao in his individual capacity is the Chairman of the Assessee-company i.e. UEPL and holds substantial shares. In the annual report, under the head “Enterprises over which shareholders, key management personnel and their relatives exercise control of significant influence”, there is a mention of “various entities of Ramoji HUF”. Two entities i.e. UKT & UKM are nothing but the business entities of HUF concern of Ch. Ramoji Rao. As such, both the payer and payees are related parties and exercise control or significant influence on each other. Thus, it is quite illogical to say that a person competes with himself. Moreover, the transaction itself is a sham transaction, inasmuch as to cover up brought forward losses of HUF (HUF as a whole is returning losses year after year), the profit making undertaking i.e. UEPL paid such huge sum under the guise of non-compete fee.

7.1 The AO further by relying on certain judgments as mentioned in para 5.2 held that it is evident that the Assessee company resorted to colourable device in the name of ‘non-compete fee’ when there was no case for competing. Without prejudice to the above, the method adopted for valuation of non-compete fee needs to be examined.

7.2 The AO further by observing “that the Assessee in the course of scrutiny proceedings, has furnished written submissions qua nature of its business carried out by UKM & UKT”, held that there is no authentic and comparable basis for the decline in revenue by 48% to 52%. The Assessee company obtained a valuation report from M/s. SSPA & Co., wherein the basis for valuation is as under: –

“Rationale for paying non-compete fees: We have been informed by the management of UEPL that substantial sum of around Rs. 787 crores was available with UKTV and UKM (the sellers of the TV software library) with which they could aggressively buy rights of block buster films, produce expensive reality and game shows and also feature films, had there been no non-compete restriction. This would have impacted the viewership of the TV channels operated by UEPL and consequently, its revenues and EBITDA. Therefore, to further secure the business that has been acquired in March, 2007, UEPL had additionally paid Rs.670 crores in January, 2008 to UKTV and UKM towards non-compete fee to ensure that these organizations do not compete for a period of 5 years from the date of agreement.

Valuation of Non-compete:

Clause 5.2: We have been informed by the Management of UEPL that if non-compete agreement is not entered, then revenue of UEPL and consequently profits might decline by 48% to 52%.

We understand that while working out the above, management has given due consideration to various factors such as strength of UKTV UKM in the business, industry dynamics and other relevant factors which could have impact on profitability of the business in case UKTV and UKM competes.

Clause 5.3: Considering the above, the valuation for non-compete has been worked out under both the situations;

(i) when there is decline in revenue by 48%

(ii) when there is decline in revenue by 52%”

7.3 The AO further by considering the valuation report, ultimately held that this valuation does not stand test of jury and as such not taken into cognizance, as there is no scientific basis for the valuation, by observing and holding as under: –

“7.2 On verification of the Valuation Report, it is seen that the Valuer has not explored any scientific method to work out the valuation for the above 48% to 52% ratio. The valuer simply worked out the non-compete for the above ratios basing on the management’s certification. Further, while working out the cost of equity, the valuer has taken only Sun TV, Zee Entertainment and Raj TV for comparative purpose when there are other comparable TV producers. Thus, there is absolutely no scientific basis for decline in revenues by 48% to 52% as submitted by the assessee-company. Accordingly, this valuation does not stand the test of jury and as such not taken into cognizance.

In the light of the foregoing discussion, it is held that there is no scientific basis for the valuation.”

7.4 The AO further by considering and examining another aspect/issue whether the Assessee is eligible for depreciation on non-compete fee or not, ultimately held that non-compete fee cannot be treated as intangible assets qualified for depreciation. The Assessee’s claim of substantial depreciation is nothing short of a colourable device in the name of ‘non-compete fee’ when there was no case for competing.

7.5 The AO thus, on the aforesaid reasons, rejected the submissions of the Assessee and disallowed the depreciation claimed to the tune of Rs. 15,79,57,119/- on the amount of “noncompete fee” by observing and holding as under: –

8. Whether non-compete fee is eligible for depreciation?

Section 32(1)(ii) prescribes for depreciation in respect of know-how, patents, copyrights, trademarks, licenses, franchises or any other business or commercial rights of similar nature being intangible assets acquired on or after the first day of April, 1998 owned fully or partly by the assessee and used for the purposes of the business or profession. There is no prescription for allowance of depreciation in respect of non-compete fees since it does not get covered under the phrase “any other business or commercial rights of similar nature”

8.1. Further, there is no explicit provision for claiming deduction on non-compete fees. Therefore, it is very obvious that all intangible assets are not eligible for depreciation allowance. The said payment does not come under either knowhow, patents, copyrights, trademarks, licenses, franchises. The only remaining category is the residual one “any other business or commercial rights of similar nature”. It is to be seen that any other business or commercial rights are not by themselves intangible assets eligible for depreciation. Those rights must be of similar nature; all similar nature to knowhow, patents, copyrights, trademarks, licenses, franchises. Any business or commercial rights not similar in nature to the above mentioned six items cannot be treated as intangible assets qualified for depreciation.

8.2. In this context, the aspects need examination:

| • |

|

that section 32(1)(ii) uses the words ‘any other business or commercial rights of similar nature’. |

| • |

|

that by using the words ‘similar nature’, the Legislature has restricted the scope of ‘intangible assets’ to the specified ones, I.e., know-how, patents, copy rights, trade marks, licences, franchises. |

| • |

|

that in the present case, the assessee had acquired ‘non-compete obligation’ which is not an asset. |

| • |

|

that the ‘non-compete obligation’ acquired by the assessee is not an asset since it has no market value, it could not be sold or assigned, and it was not a transferable right. |

| • |

|

that since the right acquired through non-competition agreement was not an asset, there was no question of discussing whether it was an intangible asset or not, or whether it was similar to, ‘know-how, patents, copy rights, trade marks, licenses, franchises’. |

| • |

|

that, without prejudice to above, even if ‘non-compete obligation’ is treated as an asset, it is not of a similar nature as ‘know-how, patents, copyrights, trade marks, licenses, franchises’. |

| • |

|

that there is no diminution in the value of these assets. |

| • |

|

that the issue is covered, in favour of the department, by the decision of ITAT, Chennai, in the case of A.B. Mauria India (P.) Ltd. [IT Appeal No. 1293 (Mad.) of 2006, dated 23-11-2007]. |

| • |

|

the decisions of the Tribunal in the following cases, where it was held that ‘Goodwill’ was not similar to the items-specified in clause (ii), and therefore, was not eligible for depreciation. |

| (i) |

|

Guruji Entertainment Network Ltd. v. Asstt. CIT [2007] 14 SOT 556 (Delhi) |

| (il) |

|

Bharatbhai J. Vyas’ case (supra). |

| • |

|

that reliance was also placed on the decision of ITAT in the case of M.M. Nissim & Co. v. Asstt. CIT [2007] 18 SOT 274 (Mum.) |

8.3. The sum and substance of the above is that the ‘right’ acquired by the assessee through the non-compete agreement, on the facts of the present case, was not an ‘asset’ at all. In order to buttress the assessee-company contention it is pertinent to mention here the definition of ‘asset’ given in Advanced Law Lexicon by P. Ramanatha Aiyer (3rd Ed. 2005), which is as under:

“An asset must be one for which a market value can be ascertained. A right to personal services under a contract of service is unassignable, it cannot be bought or sold. It cannot survive the demise of either of the parties. It can have no actual market value and so it cannot be an asset. [O’ Brien (Inspector of Taxes) v. Bensons Hosiery (Holdings) Ltd. [1978] 3 All ER -1057, 1063]

The right to trade freely and to compete in the market place is not an asset [Kirby V/s Thorn Emi Plc. [1988] 2 All ER 947, 959 (CA)].”

Further, the provisions of clause (ii) of sub-section (1) of section 32 did not need to be applied to the ‘non-compete right’ acquired by the assessee-company, because it did not fall within the definition of ‘asset’, as given in Advanced Law Lexicon (supra). The ‘non-compete obligation’ acquired by the assessee was not an ‘asset’ because it had no market value, it could not be sold or assigned, it was incapable of being transferred by the assessee to anybody else, and the agreement did not make it a transferable right. If the ‘right’ acquired through non-compete agreement was not an ‘asset’, there was no need to go into the question whether it was an ‘intangible asset’, or whether it was similar to ‘know-how, patents, copyrights, trademarks, licenses, franchises’.

8.4. In this connection, reliance is placed on the decision of the ITAT, Chennai, in the case of A.B.Mauria India (P) Limited (supra). In that case the Assessing Officer had allowed depreciation on non-compete fee and this order was set aside by the CIT under section 263, on the ground that the deduction for depreciation was allowed by the Assessing Officer without verification. The Assessing Officer was, accordingly, directed by the CIT, to redo the assessment in accordance with law. The said order of the CIT under section 263 was confirmed by the Tribunal.

Right as to knowhow, patents, copyrights, trademarks, licences, franchises, etc., can be construed to be right in them which can be claimed against the world at large. Right in restrictive covenant is ‘right in personam’ which is available against the contracting parties only. As such, right in restrictive covenant is not of similar nature. Therefore, depreciation on restrictive covenant is not allowable as per the prescription of S 32(1)(ii). Once this conclusion is arrived at, the issue whether the transaction was collusive and colourable becomes only academic.

8.5. The tenets of law are being enacted on the basis of pragmatism. Similarly, the rules relating to interpretation are also based on common sense approach. The dictum of EJUSDEM GENERIS means of the same kind, class or nature. The rule is that when general words follow particular and specific words of the same nature, the general words must be confined to things of the same kind as those specified. A word shall be interpreted with reference to the accompanying words. Words derive colour from the surrounding words. Since, non-compete fee is not a right that is acquired by the payer but a restriction on the recipient, it cannot be deemed to be covered under the residuary phrase “any other business or commercial rights of similar nature”.

8.6. It is pertinent to note that in the case of Srivatsan Surveyors (P) Ltd V/s ITO (2009) (32 SOT 268) (Chennai-Tribunal), it has been held that “Right as to know how, patents, copyrights, trademarks, licences, franchises, etc can be construed to be right in rem which can be claimed against the world at large. Right in restrictive covenant is ‘right in personam’ which is available against the contracting parties only. As such right in restrictive covenant is not of similar nature. Therefore, depreciation on restrictive covenant is not allowable as per the prescription of Section-32(1)(ii). Once this conclusion is arrived at, the issue whether the transaction was collusive and colourable becomes only academic.”

In fact, the assessment Order in which depreciation on non-compete fees was disallowed was upheld by the Ld. CIT(A).

8.7. In this regard a show cause opportunity was given to the assessee as why depreciation on non-compete fees be not disallowed, vide hearing dtd. 2/3/16. As a reply assessee has made mention of the following case laws :

| • |

|

ACIT-Vs-Real Image Tech(P) Ltd (1997)120 TTJ 983(Chennai) |

| • |

|

ITO-Vs-Medicorp Tecnologies India Ltd (2009) 21 DTR 69(Chennai) |

| • |

|

OCV Reinforcements Manufacturing Limited-Vs-ACIT (ITS 1678/Hyd/2010) |

Assessee’s contention is that in each of the above mentioned cases, depreciation on non-compete fees was allowed by the appellate authorities.

Extract from the case ACIT-vs-Real Image Tech (Pvt) Ltd (1997)120 TTJ 983(Chennai), which is also the essence of the order passed by Chennai Tribunal is given below

“When a businessman pays money to another businessman for restraining the other businessman from competing with the assessee, he gets a vested right which can be enforced under law and without that the other businessman can compete with the first businessman. When by payment of non-compete fee, the businessman gets his right what he is practically getting is kind of monopoly to run his business without bothering about the competition.

Moreover, this right (asset) will evaporate over a period of time of five years in this case because after that the protection of non-competition will not be available to the assessee. This means, this right is subject to wear and tear by the passage of time, in the sense that after the lapse of a definite period of five years, this asset will not be available to the assessee and, therefore, this asset must be held to be subject to depreciation.”

8.8. Extract from the judgement of the tribunal talks about the arrangement between two independent businessmen who have entered Into an agreement not to compete with each other for a period of 5 years. Fact of this case law is completely different from the facts involved in the present case of Prism TV Limited. The point that buyer of the asset i.e. Ushodaya Enterprises Private Limited and seller of the asset l.e. UKM and UKTV are one and the same. This point is. elaborately discussed in the earlier paragraphs which talk about lifting of corporate veil. As discussed above the assessee-company claim of substantial depreciation, is nothing short of a colourable device in the name of “Non-compete fee” when there was no case for competing. Submission of assessee is rejected.

Similarly the facts of the case ITO-vis-Medicorp as decided by Chennal Tribunal are squarely different from the facts of the present case and hence, the submission of the assessee is rejected. OCV Reinforcements Manufacturing Limited-vs-ACIT (ITS 1678/Hyd/2010).

Assessee instead of verifying the applicability of the above case laws to the present case of Prism TV Private Limited, has mere mechanically quoted the mentioned case laws. Submissions of the assessee are not valid in light of the above facts and are hence rejected.

Therefore, the depreciation claimed on non-compete fee amounting to Rs. 15,79,57,119/- is disallowed and added back.”

8. The Ld. Commissioner, on appeal, by taking cognizance of the fact that the present issue emanated from the earlier year i.e. AY 2008-09, wherein identical claim of depreciation on non-compete fees paid was disallowed by the AO and the matter travelled upto the Hon’ble ITAT, who vide order dated 22-10-2014 in Ashok Kumar Kedia v. ACIT [IT Appeal no. 26(Hyd) of 2011 and 100(Hyd) of 2012] remanded back the matter to the file of the AO for verification and examination of certain issues and to pass the assessment order afresh and thereafter consequential order has been passed by the AO allowing the claim of the Assessee on the basis of valuation report of Valuation Officer, allowed the claim lodged by the Assessee qua “Non-compete fee”.

9. We observe that the then AO without verifying and examining the issues afresh, as per directions of the Hon’ble Tribunal vide order dated 22-10-2014, referred the matter qua non-compete fee to the valuation officer, who requested further time and failed to provide the valuation report qua “Non-Compete Fee”, till the date of passing the consequential order 31/03/2017 giving effect to the Tribunal’s order dated 22/10/2014 and therefore, the AO reiterated the disallowance under consideration by observing as under: –

“10. It is clear from the above that the valuator requested further time to submit valuation report in respect of value of “Non-Compete Fee”, in spite of this office being constantly in touch with him and also bringing to his notice about the limitation of time given to him for the purpose of valuation. In view of the above facts and circumstances of the case, the assessment order passed by the then Assessing Officer with regard to necessity for Non-Compete Fee and valuation thereof, discussed in detail with respect to the issue of ‘Non-Compete Fee’ holds good.”

9.1 The AO further, in para 12 of the said order dated 31/03/2017, also noted as under: –

” 12 However, it may be noted that as and when the final report of valuator on the issue of ‘Non-Compete Fee’ is received in this office, this order will accordingly stand modified after giving due opportunity to the Assessee in accordance with the provisions of the I.T. Act, 1961.”

9.2 Somehow the Assessee challenged the said consequential order dated 31/03/2017 passed by the AO, by filing first appeal before the then CIT(A), before whom during the course of such appellate proceedings the valuation report was provided/submitted.

9.3 The then Ld. CIT(A) thus vide order dated 24/03/2023 directed the AO to allow claim of ‘non-compete fee’ as per the valuation determined by the valuation officer appointed by the AO.

10. Thus, the AO thereafter, vide order dated 19/05/2023 given effect to the order of appellate authority i.e. the then Ld. CIT(A) and allowed the claim of depreciation on ‘Non-Compete Fee’ of Rs. 618,45,51,000/- value determined by the Valuation Officer, as against the valuation arrived at by the Assessee to the tune of Rs. 670,00,00,000/-.

11. Thus, the present Ld. Commissioner in this case by perusing the order of the Hon’ble Tribunal and the then CIT(A) and corresponding orders giving effect by the AO, ultimately, came to a conclusion that this issue is now covered by the order of AO himself, as the AO has allowed the claim of depreciation @25% on the ‘noncompete fee’ as per valuation arrived at by the Departmental Valuation Officer to the tune of Rs. 618 crores as against the value of the Assessee of Rs. 670 crores. Thus, the value of the ‘non-compete fee’ as determined by the valuation officer has already been accepted by the AO in the earlier assessment year 2008-09, has to be considered for the purpose of continuing the claim of depreciation on such ‘non-compete fee’.

12. The Learned DR, therefore, being aggrieved has claimed as under: –

In captioned AY ie. 2013-14 the CIT(A) had allowed the ground of Noncompete fees stating the AO has already passed the order dt. 19.05.2023 allowing the claim of the depreciation @25%

It is pertinent to mentioned that CIT(A) in his order dated 24.08.2024 for the AY 2013-14 has taken very narrow view of the issue and allowed the claim of the assessee banking upon the order which was binding on the then AO to give effect of the CIT(A) order dated 24.03.2023. The CIT(A) has not appreciated the fact that AO has never decided this ground on merit.

It can be seen from the extract of the consequential order dated 31.03.2017 the AO has sustained the reason for disallowance. The purpose behind writing “with regard to necessity for Non-compete Fees and Valuation thereof, discussed in detail with respect to the issue of Non-compete fee holds good’ is that AO has deliberated on the fact that the core issue of the ground is the veracity of the payment of the Noncompete fees which has been subdued gradually over the time.

The UEPL has paid non-compete fees of Rs 670 crores to Usha Kiron Television and Usha Kiron Movies to restrict them to compete against him for five years On exploring the facts of the case it is found that Shri Ch. Ramoji Rao in his Individual capacity is the chairman of the Ushodaya Enterprises Private Limited and the two entities to whom the amount was being paid were the HUF units of Ramoji HUF Thus. Both the payer and payees are related parties and exercise control or significant influence on each other. Thus, it is absurd and irrational to say that person competes with himself. In addition to this, the transaction is merely a blanket/veil to cover the brought forward losses of the HUF and to reduce the profit of the UEPL.

Reference can be made to the case of M/s Indo Tech Electric Co. v. DCIT (2011) (196) CTR 0277), while deciding the genuineness of noncompete fee paid by a company to a firm, which was taken over by it on going-concern basis, the Hon’ble Madras High court held that:

“Similarly, the question of payment to be made as compensation by way of non-competing fee also would not arise, considering the fact that the assessee firm has been taken over as a going concern in its entirety by the new company. As observed earlier, the partners of the assessee firm are the new Directors of the company. The consideration was paid to the assessee firm and not the partners. There was no competition as alleged between the assessee firm and the new private limited company. There was also no control between the partners of the assessee and the new private limited company. Hence, considering above said factual position, we are of the considered view that the findings of the Tribunal in holding that in as much as there was no competition between the partners of the assessee firm and the new private limited company, coupled with the fact that the entire business of the assessee company was transferred the same cannot be found fault with.”

The facts of the case under scrutiny too are similar The members of Ramoji HUF are also on the board of directors of the assessee-company Since the entire unit of the Ramoji HUF has been taken over on a goingConcern basis, there could be no case for completion.

Also, in the case of CIT V/s Indian Express Newspapers (Madurai) Pvt Ltd. (1999) (238 ITR 70) the madras court held that:

“It is well settled that the corporate veil of a company can be lifted for the purpose of ascertaining the real character of a transaction, if that transaction was a fraudulent or sham or was intended to evade payment of tax. While legitimate tax avoidance is always permissible, devices adopted to evade payment of tax, however are not permissible though the dividing line is not always easy to draw, such a line does exist”

Therefore, in the light of the above facts and discussion it is clear that the Assessee’s company claim for depreciation is not genuine and merely a colourable device in the name of “Non- Compete fee” when there was no case for competing.

Another question which arises from the claim of the assessee is whether the “Non-compete fees” is eligible for depreciation u/s 32(1)(ii).

With regard to this it must be noted the basic definition for classifying any asset as revenue or capital in nature is that If an asset has enduring benefit to the business, then it can have capitalized and gradually amortized. In the instant case “Non-compete fees” is not a right that is acquired by the payer but a restriction on the recipient and neither it is an asset of enduring nature, thus question of claiming depreciation has no ground to stand.

“Section 32(1)(ii) prescribes for depreciation in respect of know-how, patents, copyrights, trademarks, licenses, franchises or any other business or commercial rights of similar nature being intangible assets acquired on or after the first day of April, 1998 owned or fully partly by the assessee and used for the purpose of the business or profession. There is no prescription for allowance of depreciation in respect of noncompete fees since it down not get covered under the phrase “any other business or commercial rights similar nature”

that section 32(1)(ii) uses the words ‘any other business or commercial rights or similar nature’ that by using the words ‘similar nature’, the Legislature has restricted the scope of ‘intangible assets to the specified ones, ie, know-how patents, copy rights, trade marks, licences, franchises.

| • |

|

that in the present case, the assessee had acquired ‘non-compete obligation’ which is not an asset. |

| • |

|

that the ‘non-compete obligation’ acquired by the assessee is not an asset since it has no market value, it could not be sold or assigned, and it was not a transferable right |

| • |

|

that since the right acquired through non-competition agreement was not an asset, there was no question of discussing whether it was an intangible asset or not, |

| • |

|

or whether it was similar to, ‘know-how, patents, copy rights, trade marks, licenses, franchises’. |

| • |

|

that, without prejudice to above, even if ‘non-compete obligation’ is treated as an asset, it is not of a similar nature as ‘know-how, patents, copyrights, trademarks, licenses, franchises’ |

| • |

|

that there is no diminution in the value of these assets. |

| • |

|

that the issue is covered, in favor of the department, by the decision of ITAT, Chennai, in the case of A.B. Mauria India (P.) Ltd. [IT Appeal No. 1293 (Mad.) of 2006, dated 23-11-2007 |

| • |

|

The decisions of the Tribunal in the following cases, where it was held that ‘Goodwill’ was not similar to the items-specified in clause (ii), and therefore, was not eligible for depreciation |

| (i) |

|

Guruji Entertainment Network Ltd. v. Asstt. CIT (2007) 14 SOT 556 (Delhi) |

| (ii) |

|

Bharatbhai J. Vyas’ case (supra). |

| • |

|

that reliance was also placed on the decision of ITAT in the case of M.M. Nissim & Co. v. Asstt. CIT [2007] 18 SOT 274 (Mum.) |

To sum up and in the view of above discussion and judicial precedents it is hereby stated that CIT(A) in the present case has just taken the bird eye view and not appreciated the merit of the case and made his decision on the order which was just binding on the AO to give effect and not an order of merit.

Hence, it is requested the decision of the Id CIT(A) may kindly be set aside.”

13. On the contrary, learned Counsel for the Assessee relied on the decision of the Ld. Commissioner and submitted that the then AO on being satisfying himself qua claim of the Assessee in respect of non-compete fee in the AY 2008-09 and as per the directions of the Hon’ble Tribunal, ultimately, sought for the valuation from the District Valuation Officer and on receiving the valuation report, during the appellate proceedings before the then Ld. CIT(A) and on being directed by the then CIT(A) vide order dated 24/03/2023, accepted the valuation report and/or the claim of the Assessee to the extent of Rs. 618 crores being depreciation @ 25% on the ‘non-compete fee’ and thus, the issue is squarely covered in favour of the Assessee and does not require any interference.

14. We have heard the parties and given thoughtful consideration to the facts and circumstances of the case and rival contentions raised by the parties. As observed above, an identical addition /disallowance has also been made by disallowing the claim of depreciation claimed on ‘Non-Compete Fee’ by the then AO in the case pertaining to AY 2008-09, which travelled upto the Tribunal, who vide order dated 22/10/2014 in Ashok Kumar Kedia (supra) for the AY 2008-09 remanded the issue qua ‘Non-Compete Fee’ to the file of the AO for decision afresh in view of the statutory provisions and as per the ratio laid down in the decision referred to, in the order of the tribunal, by observing and holding as under:-

“25. We have heard the submissions of the parties and perused the orders of revenue authorities as well as other materials on record and also gone through the decisions cited. A perusal of the assessment order as well as the order passed by CIT(A) would leave no room for doubt that assessee’s claim of depreciation on non-compete fee has been rejected basically for the following two reasons:

1. Genuineness of the payment made and necessity of paying noncompete fee.

2. Non-compete fee not being in the nature of an intangible asset as defined in section 32(1)(ii), depreciation is not allowable.

26. Before examining whether non-compete fee can be considered to be an intangible asset so as to entitle the assessee to claim depreciation on it, it is necessary, at the outset, to address the issue of genuineness of payment of non-compete fee and necessity to make such payment. As can be seen from the assessment order, AO has treated the agreement entered into between assessee for payment of non-compete fee as a sham transaction as Shri Ramoji Rao is not only the owner of UKT and UKM being the karta of HUF to which these concerns belong but he also in his individual capacity is the Chairman of the assessee company. As such, assessee cannot be considered to be competing with himself. As it is an arrangement between related parties, there is no necessity for payment of noncompete fee. AO further observed that the assessee has entered into agreement for payment of non-compete fee to reduce its tax burden by allowing Shri Ramoji Rao HUF to adjust the non-compete fee against the huge brought forward losses suffered by it. AO also raised doubts with regard to the value of non-compete fee at Rs. 670 crores. However, the CIT(A) has rejected assessee’s claim by holding that as Shri Ramoji Rao, who is the kartha of HUF, which owns UKT and UKM and also in his individual capacity is the Chairman of the assessee company, therefore, there is no question of paying noncompete fee as a person cannot compete with himself. Of course the CIT(A) has also held that as non-compete fee does not provide any asset of enduring nature, deprecation cannot be allowed. In this context, it is to be noted that assessee on 25/01/2008 has entered into subscription agreement and share purchase agreement with a domestic company, Viz.; Equator Trading Enterprises Pvt. Ltd. as per which the said domestic company agreed to make substantial investment in purchase of equity shares of the assessee company. However, as a precondition for making such investment, the said domestic company required the assessee company to enter into a non-compete agreement with UKT and UKM. Though, copies of the share purchase agreement and subscription agreement are not available on record before us, however, on perusal of the closing agreement dated 30/01/08 between assessee and M/s Equator Trading Enterprises Pvt. Ltd. a copy of which is at page 220 of paper book, we find a reference to such precondition in clause 2(a). Further, as it appears from the fact on record and which remains uncontroverted in pursuance to the condition imposed by the domestic investor assessee has entered into the noncompete agreement with UKT and UKM for a period of 5 years on payment of non-compete fee of Rs. 670 crores, which is also approved by the domestic investor. It is the contention of assessee that as a result of fulfillment of such condition of non-compete fee thereby excluding UKT and UKM competing with assessee company in future, the domestic company invested substantial amount by acquiring 39% of share in the assessee company.

27. From the aforesaid facts it cannot be denied that Equator Trading Enterprises Pvt. Ltd is a major stakeholder in assessee company. As can be seen from the assessment order as well as order passed by the CIT(A) before coming to their respective conclusion that the transaction entered into by parties for payment of non-compete fee is not genuine or there is no necessity for paying the non-compete fee as the same person is controlling both the assessee company and the two other companies acquired by the assessee, the role of M/s Equator Trading Enterprises Pvt. Ltd. in any decision taken by assessee company has not at all been considered. Neither the AO nor the CIT(A) has examined the effect of acquisition of 39% of equity shares by another entity and whether after such acquisition of shares, it can still be held that Shri Ramoji Rao is the controlling authority of assessee company and it is a transaction between related parties. Unfortunately, the assessment order and order of CIT(A) is totally silent on this aspect. Though in the remand report, AO has examined the issue of investment made by the domestic investor and has alleged that it as a sham transaction and a collusive agreement entered into between the parties to reduce the tax burden by claiming depreciation on payment of non-compete fee. However, such inference drawn by AO, in our view, is more on presumptions and surmises rather than on the basis of strong evidence. When two independent parties enter into an agreement on certain terms and conditions, it cannot be termed as sham or collusive without bringing sufficient evidence to prove such fact. AO cannot treat the transaction as a colourable device adopted by the parties merely on presumptions and surmises without proving the fact that either the promoters of both the companies are same or M/s Equator Trading Enterprises Pvt. Ltd. is a front company of either the assessee or the Ramoji Rao group. In these circumstances, the inference drawn on mere assumptions and presumptions that the agreement is a colourable device to reduce the tax burden cannot be accepted. Therefore, without examining the impact of investment made in equity shares to the extent of 39% by the domestic investor and condition imposed by it, the conclusion drawn by the CIT(A) that there is no necessity of payment of non-compete fee as the same person is controlling the assessee company as well as UKT and UKM, in our view, is without proper appreciation of facts and evidences brought on record, hence, cannot be sustained.

28. Even though the AO in the assessment order has also raised the issue of payment of non-compete fee for the purpose of setting off the loss sustained by the HUF and also has questioned the value of noncompete fee but the learned CIT(A) has not at all dealt with these issues. Be that as it may, it needs to be observed that so far as valuation of non-compete fee is concerned, in course of assessment proceeding, assessee has submitted a valuation report of a CA firm in support of the valuation made by it. Therefore, if the AO had any doubt with regard to the valuation made, he should have got it valued through an independent valuer instead of rejecting the valuation by simply observing that the method adopted is not correct or scientific. It is also alleged by the AO that the payment of non-compete fee was made on the one hand to enable the assessee to reduce its profit and at the same time allowing Shri Ramoji Rao HUF to adjust it against its huge brought forward losses. In this context, it is to be observed that in course of hearing before us the learned AR has submitted certain documents as additional evidence. A perusal of the said documents reveal that Shri Ramoji Rao HUF for the assessment year 2008-09 has not only shown the non-compete fee received by it as income but has also adjusted it against the brought forward losses of earlier years. AO i.e. JCIT, Range -16, while completing assessment in case of Shri Ramoji Rao HUF has accepted not only the income but also its adjustment against brought forward losses in an assessment order passed u/s 143(3) on 24/12/2010. Therefore, when the non-compete fee paid by assessee has been accepted at the hands of Shri Ramoji Rao HUF and allowed to be set off against the brought forward losses, it needs to be examined whether still the payment of noncompete fee made by the assessee to Shri Ramoji Rao HUF can be held to be either non-genuine or not necessary. Therefore, considering the totality of the facts and circumstances we are of the view that as the impact of acquisition of 39% of equity shares by M/s Equator Trading Enterprises Pvt. Ltd. has not at all been examined by AO at the time of assessment proceeding or by the learned CIT(A) while disposing of assessee’s appeal and further as the additional evidences produced before us were not examined either by the AO or by CIT(A), which certainly have a crucial bearing on the issue as to whether the payment of noncompete fee is genuine and necessary, we are inclined to remit the matter back to the file of AO for deciding afresh. Only after the issue relating to genuineness of non-compete fee paid and necessity to pay such fee is resolved, AO will decide the allowability of depreciation claimed on such non-compete fee by keeping in view the statutory provision as well as the ratio laid down in the decisions referred to hereinabove and any other decision brought to his notice. It is needless to mention that AO must afford a fair opportunity of hearing to assessee in the matter before deciding the issue. This ground is considered to be allowed for statistical purposes.

29. Before parting, we need to mention that in ground no.9, assessee has raised an alternative contention for allowing non-compete fee as deferred revenue expenditure. Though the learned AR at the time of hearing has also advanced arguments in respect of the aforesaid issue, however, considering the fact that we have remitted the issue relating to genuineness and necessity of payment of non-compete fee and assessee’s claim of depreciation on it, we are not inclined to go into the issue at this stage. However, it is open for the assessee to raise such issue before the AO at the time reassessment proceedings. If the assessee raises such an issue, AO must have to decide the same after considering the facts and materials brought on record and in accordance with law.

30. In the result, assessee’s appeal is partly allowed for statistical purposes.

15. We observe from the decision of the Coordinate Bench in the aforesaid case, in remanding the issue to the file of the AO, and the same is in consideration before us, that the coordinate Bench of the Tribunal vide order dated 22/10/2014 not only analyzed the peculiar facts and circumstances of the case but also findings of the authorities below and the additional evidence filed by the Assessee and ultimately observed “when the ‘Non-Compete Fee’ paid by the Assessee has been accepted at the hands of Shri Ramoji Rao HUF and allowed to be set of against the brought forward losses” then it needs to be examined “whether still the payment of ‘Non-Compete Fee’ made by the Assessee to Shri Ramoji Rao HUF can be held either non-genuine or not necessary”.

15.1 The Coordinate Bench by considering the peculiar facts and circumstances, was also of the view that as the impact of acquisition of 39% of the equity shares of M/s. Equator Trading Enterprises Pvt. Ltd. has not at all been examined by the AO at the time of assessment proceedings or by the CIT(A), while disposing of Assessee’s appeal and further as the additional evidences produced before the Coordinate Bench were not examined by any of the authorities below, which are clearly having crucial bearing on the issue “as to whether the payment of ‘Non-Compete Fee’ is genuine and necessary” and therefore the Hon’ble Coordinate Bench opined that the matter needs decision afresh.

15.2 The Hon’ble Coordinate Bench also directed that only if the issue relating to genuineness of ‘Non-Compete Fee’ paid and necessity to pay such fee is resolved, then the AO will decide the liability of depreciation on such ‘Non-Compete Fee’ by keeping the statutory provision as well as the ratio laid down in the decisions referred to hereinabove.

15.3 It is also a fact that before remanding the case to the file of the AO, the Hon’ble Coordinate Bench has also taken into consideration the peculiar facts and observed “that Assessee on 25/01/2018 has entered into subscription agreement and share purchase agreement with a domestic company viz. Equator Trading Enterprises Pvt. Ltd., however, as per a precondition for making such investment, the said domestic company required the Assessee company to enter into a non-compete agreement with UKT and UKM. Though, copies of the share purchase agreement and subscription agreement are not available on record before us, however, on perusal of the agreement dated 30/01/2018 between Assessee and M/s. Equator Trading Enterprises Pvt. Ltd., a copy of which is at page No. 220 of paper book, the Hon’ble Bench found a reference to such precondition I clause 2(a). Further, as it appears from the fact on record and which remains uncontroverted in pursuance to the condition imposed by the domestic investor Assessee has entered into the non-compete agreement with UKT and UKM for a period of 5 years on payment of ‘Non-Compete Fee’ of Rs. 670 crores, which is also approved by the domestic investor. It is the contention of Assessee that as a result of fulfillment of such condition of ‘Non-Compete Fee’ thereby excluding UKT and UKM competing with Assessee company in future, the domestic company invested substantial amount by acquiring 39% of share in the Assessee company. From the aforesaid facts, it cannot be denied that M/s. Equator Trading Enterprises Pvt. Ltd. is a major stakeholder in Assessee company. As can be seen from the assessment order as well as order passed by the CIT(A) before coming to their respective conclusion that the transaction entered into by parties for payment of non-compete fee is not genuine or there is no necessity for anything the ‘Non-Compete Fee’ as the same person is controlling both the Assessee company and the two other companies acquired by the Assessee. The role of M/s. Equator Trading Enterprises Pvt. Ltd. in any decision taken by Assessee company, has not at all been considered. Neither the AO nor the CIT(A) has examined the effect of acquisition of 39% of equity shares by another entity and whether after such acquisition of shares, it can still be held that Shri Ramoji Rao is the controlling authority of Assessee company and it is a transaction between related parties. Unfortunately, the assessment order and the order of CIT(A) is totally silent on this aspect. Though, in the remand report, the AO has examined the issue of investment made by the domestic investor and has alleged that it as a sham transaction and a collusive agreement”.

15.4 The Hon’ble Coordinate Bench further observed “that the AO cannot treat the transaction as a colourable device adopted by the parties merely on presumptions and surmises, without proving the fact that either the promoters of both the companies are same or M/s. Equator Trading Enterprises Pvt. Ltd. is a front company of either the Assessee or the Ramoji Rao group. In these circumstances, the inference drawn on mere assumptions and presumptions that the agreement is a colourable device to reduce the tax burden cannot be accepted. Therefore, without examining the impact of investment made in equity shares to the extent of 39% by the domestic investor and condition imposed by it, the conclusion drawn by the CIT(A) that there is no necessity of payment of ‘Non-Compete Fee’ as the same person is controlling the Assessee company as well as UKT and UKM, in our view, is without proper appreciation of facts and evidences brought on record, hence cannot be sustained”.

15.5 The Hon’ble Bench further held “that if the AO had any doubt with regard to the valuation made by the Chartered Accountant firm as submitted by the Assessee in the course of assessment proceedings, then the AO should have got it valued through an independent value instead of rejecting the valuation by simply observing that the method adopted is not correct or scientific”.

16. We observes from the order of Hon’ble Coordinate Bench that as per order and directions dated 22-10-2014 (supra) of the Hon’ble Coordinate Bench, the AO was supposed to consider all the facts and aspects as observed above, however, in absence of valuation report, which the valuator failed to file till passing the consequential order dated 31/03/2017, the then AO by observing that necessity of Non-Compete Fee and valuation thereof, as discussed in detail with respect to issue of “Non-Compete Fee”, holds good. However, the AO in the note mentioned that as and when the final report of valuator on the issue of ‘Non-Compete Fee’ is received in this office, the consequential order will accordingly stand modified after giving due opportunity to the Assessee.

16.1 Admittedly, the then AO while passing the consequential order dated 31/03/2017 failed to follow the directions of the Hon’ble Coordinate Bench in its true spirit and proper manner and without examining the issue under consideration, as per the directions of the Hon’ble Coordinate Bench and held ‘Non-Compete Fee’ as good.

16.2 However, thereafter, somehow the Assessee challenged the said consequential order dated 31/03/2017 and the then CIT(A)’s vide order dated 24/03/2023 allowed such appeal and without examining the issue and following the directions of the Hon’ble Coordinate Bench, directed the AO to allow to the claim of deprecation, as per the value determined in valuation report by the Valuation Officer, which was neither disputed nor challenged by the Assessee as it clearly appears from para 7.6 of the order dated 24/03/2023 by the then CIT(A).

16.3 Thus, the AO subsequently passed another consequential order dated 19/05/2023 and allowed the claim of depreciation to the tune of Rs. 61845.51 crores, as per the valuation report by the Valuer vide letter dated 30/06/2018 as against the valuation arrived at by the Assessee of Rs. 670,00.00 crores.

17. We further observe that this issue qua ‘Non-Compete Fee’ has also cropped up in the case pertaining to AY 2011-12, which resulted into making an identical addition /disallowance qua ‘NonCompete Fee’ by the AO and subsequently affirmed by the then CIT(A), which resulted into filing of appeal before the Hon’ble Coordinate Bench of the Tribunal at Hyderabad, who vide order dated 24/03/2016 in Prism TV (P.) Ltd. v. Dy. CIT [IT Appeal Nos. 466 & 1249(HYD) of 2015] by following the order 22/10/2014 (in IT Appeal No. 26 (HYD) of 2011, dated 22-10-2014] for the AY 2008-09) by the Hon’ble Coordinate Bench, Hyderabad, also remanded the issue to the file of the AO with a direction to give consequential effect to the decision taken by him for the AY 200809.

17.1 However, the Hon’ble Coordinate Bench in the case pertaining to AY 2007-08 Dy. CIT v. Ushodaya Enterprises Ltd. [IT Appeal No. 1265 (Hyd) of 2013, dated 16-2-2016], has recorded the finding as under:

“Similar circumstance existed in the Assessee’s own case for the subsequent A.Y. 2008-09 regarding the non-competing fee and this Tribunal has observed that the factual position has not been properly appreciated by the authorities below and has set aside the issue for reconsideration”.

18. Admittedly, both the authorities below in the case pertaining to AY 2008-09 which is the foundation of issue involved, have not examined the issues under consideration in the true spirt and right perspective and proper manner and as per the directions of the Hon’ble Coordinate Bench in the case pertaining to AY 2008-09, but in fact simply relied on and accepted the valuation report of Valuation Officer qua ‘Non-Compete Fee’, without analyzing the genesis and need of the ‘Non-Compete Fee’ in the context of the ownership and the stake-holding, as well as, without examining the additional evidences, which were directed to be examined by the Hon’ble Coordinate Bench specifically.

19. In this case, both the authorities below also failed to examine the issue involved in its right perspective and proper manner and in the context of the ownership/stake holding of Equator Trading Enterprises Pvt. Ltd. and Shri Ramoji Rao.

20. Admittedly, the Assessee before us, has also failed to establish the genesis of ‘Non-Compete Fee’. We reiterate that from the orders passed by the authorities below, it is clear that both the authorities below have not gone into genesis of the issue involved and the Ld. Commissioner simply relying on the consequential order passed in the case relevant to AY 2008-09 and without analyzing the fact that in the AY 2008-09, neither the AO nor CIT(A) examined the issue in detail and as per the specific directions of the Hon’ble Coordinate Bench vide order dated 22/10/2014 (supra), allowed the claim of the depreciation claimed, and therefore the decisions of the Authorities below are unsustainable.

21. Thus, on the aforesaid analyzations, we deem it appropriate to set aside the decisions of the Ld. Commissioner and the AO and remand the instant issue to the file of the AO for decision afresh, in view of the directions enshrined in the order dated 22/10/2014 for the AY 2008-09 passed by the Coordinate Bench (supra) and in the context of the relevant claim/stake holding and need of ‘NonCompete Fee’ in the context of relevant provisions of law.

22. Thus, the instant issue is accordingly remanded to the file of the AO for decision afresh, as per above terms.

22.1 Resultantly, issue/ground no 1 raised by the Revenue is allowed for statistical purposes.

23. Coming to the 2nd issue/ground raised by the Revenue Department, which relates to the disallowance of Rs. 134,79,41,873/- on account of cost of production of TV serials and programmes which was claimed by the Assessee as “Revenue expenditure” completely, instead of claiming depreciation on the same debiting to the profit and loss account.

23.1 The AO only allowed the depreciation @25% on the said expenditure and made addition of rest of the amount, by observing and holding as under: –

“The assessee-company debited an amount of Rs.134,79,41,873/-towards cost of production of T.V serials and Programmes. This expenditure relates to the year under consideration. Instead of claiming depreciation, the entire expenditure is claimed as revenue expenditure and debited to Profit and Loss account. Further, the cost of production of T.V serials and Programmes is not covered under Rule 9A or Rule 98.

Rule 9A states as under:

[(1) In computing the profits and gains of the business of production of feature films carried on by a person (the person carrying on such business hereafter in this rule referred to as film producer), the deduction in respect of the cost of production of a feature film certified for release by the Board of Film Censors in a previous year shall be allowed in accordance with the provisions of sub-rule (2) to sub-rule (4).

Rule 98 states as under:

(1) In computing the profits and gains of the business of distribution of feature films carried on by a person (the person carrying on such business hereafter in this rule referred to as film distributor), the deduction in respect of the cost of acquisition of a feature film shall be allowed in accordance with sub-rule (2) to sub-rule (4).

The definition of Rule 9A clearly shows that the expenditure of the assessee-company on production of T.V serials and Programmes is not covered. Similarly, the definition of Rule 9B clearly shows that the expenditure claimed by the assessee-company is not covered, as the assessee is not a film distributor. Therefore, the expenditure debited by the assessee-company on the above items is disallowed and depreciation is allowed on the above items separately as per Section 32 of the Income Tax Act.”

However, considering the Programs as intangible assets of the company, depreciation is allowed at the rate of 25% on this expenditure.”

24. We observe that the Assessee also challenged the said disallowance of Rs.134,79,41,873/- on account of cost of production of TV serials and programmes which was claimed by the Assessee as “Revenue expenditure”, before the Ld. Commissioner and more or less has claimed that an identical issue has also been cropped up in the cases pertaining to AYs 2011-12 & 2012-13, which were dealt with by the Hon’ble Coordinate Bench and allowed in favour of the Assessee vide order dated 24/03/2016 and therefore, the issue is squarely covered by the judgment of the Hon’ble Coordinate Bench.

25. On the contrary, the AO before the Ld. Commissioner has claimed that such expenditure is not covered under Rule 9A and 9B of the Income Tax Rules, 1962 (for short, ‘Rules’) and therefore, the said expense is intangible assets u/sec. 32(1)(ii) of the Act. But the AO just allowed the depreciation @25% on that assets, resulting into net disallowance of Rs. 101,09,56,405/-.

26. We observe from the impugned order that the Ld. Commissioner by taking cognizance of the fact “that the Hon’ble Coordinate Bench vide order dated 24/03/2016 (supra) has also dealt with an identical issue and allowed the deduction of cost of TV Serials and Programmes as “revenue expenditure” in favour of the Assessee by following certain decisions and therefore the issue is squarely covered in Assessee’s own cases for AYs 2011-12 & 2012-13 as there is no change in the facts”, ultimately allowed the cost of productionpurchase of TV Serials and Programmes as “Revenue expenditure” by observing and holding as under:-

“1. I have gone through the assessment order making the additions /disallowances, the detailed written submissions filed by the Appellant and the supporting documents and various judicial decisions relied on by the Appellant company and submitted in the form of Paper Book.

1. The only dispute with regards to this issue is the allowability of cost of production / purchase of TV serials and programme as revenue expenditure as against the action of the AO of considering it to be a capital expenditure eligible for claiming depreciation. The Appellant has submitted that the said issue in the present appeal is fully covered by order of Hon’ble Hyderabad Tribunal in Appellants’ (Prism TV) own case vide ITA No. 466/ Hyd /2015 for AY 2011-12 and ITA No. 1249/ Hyd /2015 for AY 2012-13, wherein the Tribunal allowed the deduction for cost of TV serials and programmes as revenue expenditure. I have perused through the Hon’ble ITAT’s order dated 24.03.2016 for AY 2011-12 and 2012-13 as relied on by the Appellant.

1. The Hon’ble ITAT while dealing with this issue before them for the preceding years have allowed the claim of the Appellant considering this issue as fairly covered in favour of the Appellant by the following decisions.

| • |

|

Hon’ble Chennai ITAT Bench order dated 31.10.2013 in the case of ACIT. Media Circle-II Chennai v M/s Sun TV Network Ltd, Chennai in ITA Nos 1515 to 1520/Mds/2013. |

| • |

|

Hon’ble Mumbai ITAT Bench order dated 12.08.2015 in the case of Zee Media Corporation Limited (formerly known as Zee News Limited), Mumbai v DCIT, Circle 7(3), Mumbai in ITA No. 1590/Mum/2015 |

| • |

|

In coming to the conclusions drawn in above cases, the Hon’ble ITAT has followed the judgement of the Hon’ble Delhi High Court in the case of CIT v Television Eighteen India Limited (364 ITR 597) (Del) |

1. Considering that the issue is squarely covered by Hon’ble ITAT’s order in Appellant’s own case for AYs 2011-12 and AY 2012-13 and there has been no change in the facts, I decide this issue in favour of the Appellant and allow the cost of production / purchase of TV serials and programme as revenue expenditure.”

27. The Learned DR, thus has claimed that cost incurred on production of TV Serials and Programmes have enduring benefit to the business over several years, it could not be treated as revenue expenditure and thus should be capitalized. If the expenditure creates asset with long term benefits or future earning potential such as the right to broadcast or exploit the TV program for a longer duration, then it needs to be placed under “capital expenditure”. The Ld. DR in support of above contentions, also relied on the judgment of Mumbai Tribunal in the case of Mukta Arts Pvt. Ltd v. ACIT [2007] 105 ITD 533 (Mumbai), wherein according to Ld. DR, expounded the applicability of Rule 9A of the Rules and unique characteristics of film production and prescribes specific guidelines for amortizing production costs over multiple years by holding as under: –

1. Rule 9A operates within the framework of the Act and does not override statutory provisions such as sections 37 & 43B.

2 Costs incurred post-certification by the Censor Board, such as promotional expenses, are governed by general provisions of the Act.

3. Capital expenditures linked to abandoned films are allowable as business losses under commercial expediency.

The Ld. DR, in view of the above, further submits that expenditure debited by the Assessee of Rs. 134,79,41,873/- has rightly been treated as “capital expenditure” and therefore depreciation on the same @25%. has rightly been allowed by the AO and thus decision of the AO on this issue, is liable to be restored.

28. On the contrary, learned counsel for the Assessee, relied on the order of the Hon’ble Coordinate Bench in AY 2011-12& 2012-13 and submitted that in view of the order of the Hon’ble Coordinate Bench, the issue is squarely covered in favour of the Assessee, therefore, the decision of the Ld. Commissioner on the issue under consideration, need no interference.

29. We have given thoughtful consideration to the peculiar facts and circumstances of the case and rival claim of the parties on the issue under consideration and observe that Coordinate Bench of the Tribunal at Hyderabad in Assessee’s own case for the AY 211-12 & 2012-13 has also dealt with an identical issue, as involved in this case and by analyzing various judgments concerning the issue, vide order dated 24/03/2016, allowed the identical claim qua expenditure as “Revenue expenditure” by allowing ground raised by the Assessee and observing and holding as under:-

“6. As regards ground No.2, against the treating of the cost of production of TV serials and programmes as capital expenditure, brief facts are that the assessee company debited an amount of Rs.123,63,94,000 towards cost of production of TV serials and programmes for the year under consideration. Instead of claiming depreciation, the entire expenditure was claimed as revenue expenditure and debited to the P & L account. The A.O. observed that the cost of production of TV serials and programmes is not covered under Rule 9A or 9B of I.T. Rules. As these Rules are applicable only to production of feature films. The A.O. treated the entire expenditure as capital expenditure and allowed the depreciation thereon. Aggrieved, the assessee preferred an appeal before the Ld. CIT(A) who confirmed the order of the A.O. and the assessee is in second appeal before us.

7. The Ld. Counsel for the assessee, while reiterating the submissions made by the assessee before the authorities below, has relied upon the decision of the Coordinate Bench of this Tribunal at Chennai and Mumbai and also the decision of Hon’ble High Court at Delhi in support of his contention that the expenditure incurred on production of television programmes should be allowed as revenue expenditure under section 37 of the I.T. Act. Copies of the said decisions are also filed before us.

8. The Ld. D.R. on the other hand, supported the orders of the authorities below.

9. Having regard to the rival contentions and the material on record, we find that the ‘A’ Bench of this Tribunal at Chennai in the case of ACIT, Media Circle-II, Chennai v. M/s. Sun TV Network Ltd., Chennai in ITA.Nos.1515 to 1520/Mds/2013 by its order dated 31.10.2013 has held as under :

“8. Now, we take up the common issue involved in all the appeals. The assessee is in the business of running satellite television channels. These channels telecast films, serials etc., through satellite channels. The rights over these films are purchased from the producers of the respective films for broadcasting through satellite television. These rights come with an embargo that the films shall not be broadcasted or aired for a specified period from the date of release in theatres depending upon the success at the box office and other factors. Till the time, such films are broadcasted, they are to be treated as stock in trade. Once the films are broadcasted, the purchase value of the films is written-off. The expenditure on purchase of films is claimed in the first year itself. The assessee has got only satellite telecasting rights and has no universal rights for airing the films or serials. Once the film or the serial is aired, its value is diminished in subsequent telecasts. The assessee earns substantial revenue in the first telecast itself. In repeat telecast, the assessee is able to generate marginal revenue. Whatever income is earned from the subsequent telecasts is offered as income without claiming any expenditure.

The assessee also generates revenue from broadcasting serials through satellite channels. The assessee gets revenue from production and broadcasting serials on the lines of feature films, the rights of broadcasting such serials are also treated as stock in trade till the time they are aired and the expenses are debited to the Profit & Loss account. The assessee treats the films and the serials at par and applied the provisions of Rule 9A and 98 of the Income Tax Rules, as are applicable in case of films on serials as well.

On the other hand, the contention of the Revenue is that the film and serial broadcasting rights acquired by assessee are perpetual in nature. After first telecast, the assessee does not discard the films but carefully store the same in digital library for airing the same again. Therefore, the assessee gets enduring benefit from the rights acquired in films and serials and they do not expire on the date of first telecast as contemplated by the assessee. The rights are intangible assets within the meaning of Explanation (iii) to Section 32 and do not fall within the purview of Section 37(1). The assessee is entitled to claim depreciation on same.

9. The issue of amortization of cost of movie and serial rights, programme production expenses, consumable and media expenses by treating them as intangible assets u/s.32(1)(ii) has been dealt in detail by the CIT (Appeals) in his order dated 23-02-2013 relevant to the A Y. 2006-07 and 2007-08. We fully agree with the detailed findings and the reasoning given by the CIT(Appeals) in his order allowing this ground of appeal of the assessee. For the sake of brevity, we are not reproducing the findings of CIT (Appeals) in accordance with the judgment of the Hon’ble Supreme Court of India in the case of CIT v. K. Y. Pillah & Sons reported as 63 ITR 411 subsequently followed by the Hon’ble Delhi High Court in the case of CIT v. Global Vantedge (P) Ltd. , reported as 354 ITR 21 (Del). The Id. DR has not been able to controvert the well reasoned order of the CIT (Appeals) on the issue. Accordingly, the findings of the CIT (Appeals) on the issue are affirmed and this ground of appeal of the Revenue in respect of all the AYs is dismissed.”

9.1. In the case of Zee Media Corporation Ltd., (Formerly known Zee News Limited), Mumbai v. DCIT, Circle- 7(3), Mumbai, the ‘G’ Bench of Tribunal at Mumbai in ITA.No.1590/Mum/2015 by order dated 12.08.2015 has held as under :

“25. We have heard both the parties and perused the orders of the Revenue Authorities as well as the cited precedents and paper book filed before us. The case of the assessee on the merits is that the assessee has a method of valuation of the news items/non fictional in nature, TV programs and the film rights. The details are given in the aforementioned ‘Note No 7’ to the financial statements. According to the same, while the news items purchased are debited to the P and L account as they do not have the repeat telecast value, other items like the TV program and the film rights constitutes ‘current assets’, which are amortised over the years and the period of such amortization is given in the said Note. Per contra, the case of the revenue on these issues is that these items constitute ‘intangible depreciable capital assets’ and provisions of section 32 of the Act apply. Considering the same, we shall now undertake to discuss the item wise adjudication as follows.

a. On the debits relating to the purchases of the News items: Regarding the nature of the news items purchased by the assessee and debited to the P and L account, we find it is in the common knowledge of every citizen that the news items do not have enduring benefit. Normally, the news items/non fictional items purchased by the assessee lose its value once they are telecast. Therefore, such items do not have repeat telecast value in terms of the revenue generation by way of advertisement from the sponsors. As such, it is a settled issue at the level of Hon’ble Delhi High Court in the case of Television Eighteen India Ltd (supra) that the claims of the assessee relating to news/non-fictional items are allowable. Even otherwise, even if some income generated, that is not criterion for describing the items as ‘intangible assets’ for the purpose of invoking the provisions of section 32(ii) of the Act. We rely on the above referred Delhi High Court’s Judgment in the case of Television Eighteen India Ltd (supra). Further, we find that the assessee has a declared method of accounting relating to accounting of these transactions. He has been consistently following the same without any change. In fact, the Revenue has consistently allowed the claim in the past. This is for the first time, AO disturbed the claim of the assessee and invoked the provisions of section 32 (ii) of the Act, without any sustainable reasoning. Therefore, considering all the points mentioned above, we are of the firm opinion that the decision of the AO/CIT(A) is unsustainable legally. Hence, the assessee is entitled to claim the purchases of news items/non-fictional items as an allowable expenditure. Accordingly, we direct the AO to delete the relevant addition.

b. On the debits relating to the purchases of the TV Programs/Film rights: Assessee amortised the ‘inventories’ as per the method of accounting consistently followed by him over the years. In fact, the Revenue has consistently allowed the claim in the past. This is for the first time, AO disturbed the claim of the assessee and invoked the provisions of section 32 (ii) of the Act without any sustainable reasoning. We have perused he judgment of Honble High Court of Delhi and the order of the Tribunal of Chennai Bench in the case of M/s Sun TV Networks Ltd (supra). We have also extracted the relevant paragraphs and already placed in this order above. We find similar issue of amortization of the TV Programs/Film rights came up before the Chennai Bench of the Tribunal wherein the issue was decided in favour of the assessee and rejected the AD’s proposal to invoke the provisions of section 32(ii) of the Act in respect of the above programs/rights. As such, the Ld DR’s argument on the applicability of the AS-26 to the TV Programs and Film rights is not supported by any precedents and therefore, the arguments raised by the Revenue are not allowed. Thus, considering the covered nature of the issue as well as the consistent method of accounting followed by the assessee in this regard and also in the absence of any contrary material to support the arguments of the Revenue against the assessee’s claim, we are of the opinion that the decision taken by the CIT (A) in the impugned order is required to be reversed. Accordingly, Ground nos. 2 and 3 raised by the assessee are allowed.

9.2. In coming to this conclusion, the Tribunal has followed the judgment of the Hon’ble Delhi High Court in the case of CIT v. Television Eighteen India Limited reported in (2014) 364 ITR 597 (Del.). The relevant portion of the judgment of the Hon’ble Delhi High Court is reproduced as under :

“The revenue has preferred this appeal claiming to be aggrieved by an order of the Income Tax Appellant Tribunal (ITAT) dated 17.03.2006. The question of law framed in this case is:-

(i) Whether the Income Tax Appellate Tribunal was right in holding that the entire expenditure incurred by the assessee on production of programmes which became part of news archives should be allowed as a revenue expense under Section 37 of the Income Tax Act, 1961 and should not be treated as incurred for creating a capital asset?

The assessee, at the relevant time, was in the business of television programme production. The assessee reflected Rs.88,83,128/- being 10% of the total expenditure incurred by it as value of “news archives” under the head of fixed assets. In the return filed by the assessee for the Assessment Year 1997, the said amount was claimed as revenue expenditure. According to the assessee this expenditure was allocated for the creation of “news achieves”, which comprised of its published or telecasted programmes. The AO capitalised this amount holding that the expenditure led to creation of an asset of enduring advantage. The CIT (Appeals) on appeal, however, reversed the findings of the AO. It was noticed that the news archives were not in the nature of plant or income generating apparatus but part of the product. It was also held that the unavailability of any objective basis, to quantify with any decree of accuracy future revenue that were likely to be generated and the proportionate cost of production that could be deferred, led to the conclusion that the 10% of the total expenditure earmarked for creation of “news archives” could not be treated as a capital expenditure.

On the revenue’s appeal, the ITAT held as follows:-

“12. It is admitted that no separate account was maintained wherein any expenditure was debited which could be earmarked towards creation of News Archives library. The assessee felt a part of footage of the news based on programmes produced has repeat value which could be used for the production of programme in future. The assessee, therefore, estimated 10% expenditure incurred as reasonable to be attributable to the News Archives library. The assessee has been engaged in the production of such programmes since assessment year 1994-95 and all along the cost of production of such expenditure has been treated as revenue expenditure and also allowed by the Department. Learned A.R. has referred to judgment of Hon’ble Supreme Court in the case of Alembic Chemical Works Ltd. v. CIT 177 ITR 377 which laid down that what is capital expenditure and what is revenue are not eternal verities but must needs to be flexible so as to respond to the changing economic realities of business. Viewed in that perspective, we are of the opinion that the estimated value assigned to the News Archives cannot be treated to be an expenditure incurred in the capital field. We, therefore, uphold the order of CIT (A) on this ground.

In this case, there is no dispute that the data base of the programmes which are utilised for the creation of “news archives” belonged to the assessee. The future likelihood of these resources being a possible source of revenue, cannot in the opinion of this Court justify its inclusion in the capital stream. Furthermore, this Court notices that the expenditure i.e. 10% Rs.88,83,128/-is a part of the entire total expenditure incurred by the assessee which is concededly treated as revenue, even otherwise.

In view of the above discussions, this Court is of the opinion that the question of law framed is answered in favour of the assessee and against the revenue.

The appeal is dismissed.”

9.3. Thus, it is seen that the issue is fairly covered in favour of the assessee by the above decision and the A.O. is directed to treat the expenditure incurred by the assessee on cost of production of TV programmes as revenue expenditure. This ground of appeal of the assessee is accordingly allowed.”