A reopening of assessment is invalid if the sanction for it is not obtained from the correct, higher-level authority as prescribed by law for cases older than three years.

Issue

Is a notice for reopening an assessment valid if it’s sanctioned by an authority lower than the one specified in Section 151 of the Income-tax Act, 1961, for cases where more than three years have passed?

Facts

- The Assessing Officer (AO) decided to reopen the assessment for the Assessment Year 2016-17.

- At the time the notice was issued, more than three years had already passed since the end of that assessment year.

- The law, under Section 151(ii), mandates that in such cases, the sanction for reopening must come from a higher authority, such as the Principal Chief Commissioner of Income Tax.

- However, the AO in this case obtained the sanction from the Principal Commissioner of Income Tax, the authority prescribed under Section 151(i) for newer cases (within three years).

Decision

The Tribunal ruled in favour of the assessee.

- It held that getting the sanction from the correct authority is a mandatory jurisdictional requirement, not a minor procedural issue.

- Since the sanction was taken from a lower authority than the one legally required for a case of this vintage, the sanction itself was invalid.

- An invalid sanction makes the entire reopening proceeding void from the very beginning. The notice and all subsequent actions were therefore quashed.

Key Takeways

- Jurisdiction is Non-Negotiable: The requirement to get prior sanction from the specified authority is a jurisdictional pre-condition. Any failure to comply with this makes the entire action illegal.

- Stricter Checks for Older Cases: The law intentionally creates a higher bar (approval from a higher authority) for reopening older assessments to prevent taxpayers from being subjected to frivolous or unwarranted proceedings long after a year has passed.

- An Invalid Sanction is a Fatal Flaw: A reassessment notice issued without a valid sanction is legally dead on arrival. All proceedings that follow from such a notice are automatically null and void.

An addition for an unsecured loan under Section 68 is not sustainable if the amount has already been taxed in the hands of the lender, as it would result in double taxation.

Issue

Can an addition for an unsecured loan be made under Section 68 in the hands of the loan recipient if the same amount has already been assessed to tax in the hands of the lender, especially when the transaction is between group entities?

Facts

- The assessee-company received an unsecured loan from an individual (‘MK’) through another group entity (‘AL’).

- The Assessing Officer (AO) treated this transaction as a mere accommodation entry and added the loan amount to the assessee’s income under Section 68, alleging it was the assessee’s own unaccounted money.

- However, it was established as a fact that the lender, ‘MK’, had already been assessed to tax on the very same amount in the relevant period.

- The assessee also proved that all parties involved were assessed group entities and satisfied the three core conditions: identity, genuineness of the transaction, and creditworthiness of the creditor.

Decision

The Tribunal ruled in favour of the assessee and deleted the addition.

- It held that since the source of the fund had already been taxed in the hands of the lender, making another addition of the same amount in the assessee’s hands would result in double taxation, which is not permissible in law.

- Furthermore, the assessee had successfully discharged its initial onus under Section 68 by proving the identity, genuineness, and creditworthiness of the parties involved in the transaction.

Key Takeways

- No Double Taxation: A foundational principle of tax law is that the same income cannot be taxed twice in the hands of different persons. If the source of a credit has been identified and taxed, it cannot be treated as the unexplained income of the recipient.

- Discharging the Onus Under Section 68: To defend against a Section 68 addition, the assessee needs to prove three things about the creditor: their identity, the genuineness of the transaction, and their creditworthiness (the capacity to give the loan). The assessee did so successfully in this case.

- Group Company Transactions: While transactions between group entities are often scrutinized, the fact that all parties are assessed to tax within the same jurisdiction can help establish the identity and genuineness required to satisfy the conditions of Section 68.

and Manish Agarwal, Accountant Member

C.O. No. 106 (Del) OF 2025

[Assessment years 2016-17]

| Regime | Time limits | Specified authority |

| Sectio n 151(2) of the old regime | Before expiry of four years from the end of the relevant assessment year | Joint Commissioner |

| Section 151(1) of the old regime | After expiry of four years from the end of the relevant assessment years | frincipal fhief Commissioner or Chief Commisoioner or Principal Commissioner or Commissioner |

| Section 151(i) of the new regime | Three years or less than three years from the end of the relevant assessment year | Principal Commissioner or Principal Director or Commissioner or Director |

| Section 151(ii) of the new regime | More than three years have elapsed from the end of the relevant assessment year | Principal Chief Commissioner or Principal Director General or Chief Commissioner or Director General |

(i) If income escaping assessment was less than Rupees one lakh: (a) a reassessment notice could be issued under Section 148 within four years after obtaining the approval of the Joint Commissioner; and (b) no notice could be issued after the expiry of four years; and

(ii) If income escaping was more than Rupees one lakh: (a) a reassessment notice could be issued within four years after obtaining the approval of the Joint Commissioner; and (b) after four years but within six years after obtaining the approval of the Principal Chief Commissioner or Chief Commissioner or Principal Commissioner or Commissioner.

(i) If income escaping assessment is less than Rupees fifty lakhs: (a) a reassessment notice could be issued within three years after obtaining PART E the prior approval of the Principal Commissioner, or Principal Director or Commissioner or Director; and (b) no notice could be issued after the expiry of three years; and

(ii) If income escaping assessment is more than Rupees fifty lakhs: (a) a reassessment notice could be issued within three years after obtaining the prior approval of the Principal Commissioner, or Principal Director or Commissioner or Director; and (b) after three years after obtaining the prior approval of the Principal Chief Commissioner or Principal Director General or Chief Commissioner or Director General.

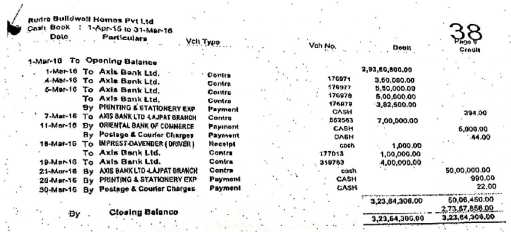

“It is seen that in entities mentioned at Serial No. 2, 4, 5, 6, 8, 9, 12 & 17in the table at Page No. 64, there is an advance given by the assessee during the earlier years/during the year which has been returned back. The copies of accounts of all the above said entities are reproduced below:

The discussion is as per table below:

| Sr. No. | Name of the entity | Remarks |

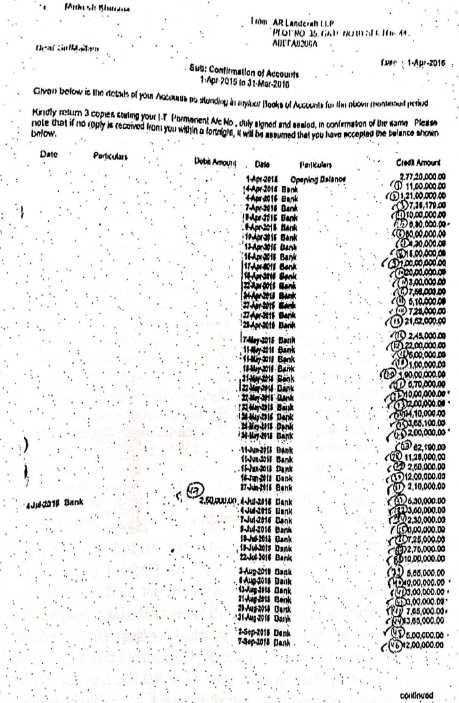

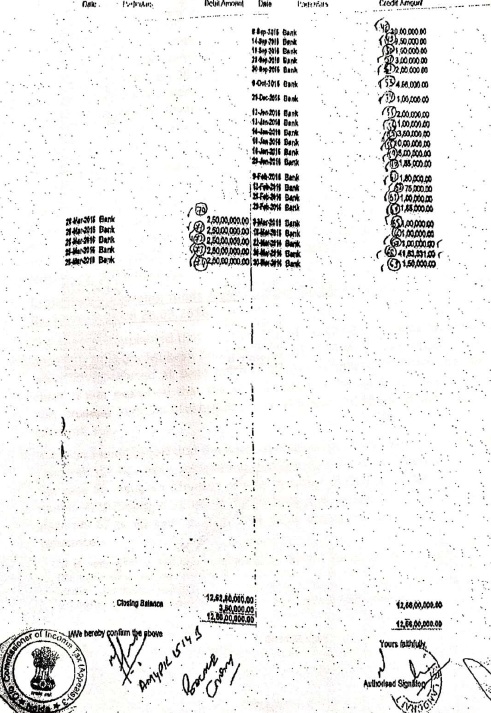

| 1 | AR Landcraft LLP | The assessee had an opening advance given to the said entity on 01.04.2015 of Rs. 2.77 crore. By the end of Financial Year, the said advance has increased to Rs. 12.56 Cr. and credits of Rs. 12.52 cr. have been received by the assessee during the year. The assessee has filed the ITR, Bank account statement and confirmation of the entity in support of the credits received. Also, the assessee has advanced more money to the said entity during the year than the amount received back, the said payments are being made through regular bank accounts of the assessee wherein, there are transfer & receipt of funds to/from the group companies. |

In all the above cases, the money was advanced by the assessee in earlier years/during the year and quantum of money received back in the current year has been added to the income by the AO. Once, the money which has been credited is the same money which has been advanced in earlier years/during the year, the same cannot be treated as unexplained money in the hands of the appellant. The AO has applied Section 69A to the case of the appellant. Once, the money has been advanced out of regular bank accounts of the assessee which are shown in the ITR, the said money once returned back or credited into the bank accounts of the assessee cannot be considered as unexplained u/s 69A of the Income Tax Act, 1961. If the AO had any doubt, then the sources of the said investments/advances in the years to which they pertained should have been investigated by the AO but the same was never done.

“SLP dismissed against order of High Court that where unsecured loans given to assessee were squared up on same date and nothing remained outstanding at end day, much less at end of financial year, Impugned reassessment proceedings to tax same under section 68 deserved to be quashed”

“Section 68 of the Income-tax Act, 1961-Cash credit (Share Capital) – Assessment year 2009-10-Assessing Officer made addition in hands of assessee-company on account of failure of assessee to prove identity and genuineness of persons who had introduced share capital and on account of failure to prove capacity of loan creditors as well as genuineness of transactions Commissioner (Appeals) found that shareholders were all private limited companies who had made investments out of their share capital and reserve through banking channels and assessee had filed a confirmation from loan creditors, regarding advancing of loan by them along with confirmation date, cheque No. and other relevant information along with PAN of companies – Accordingly, he deleted additions – Whether since question of genuineness of investors who introduced share capital and capacity of persons from whom loan was borrowed and genuineness of transactions, had been considered at length by first appellate authority and revenue had failed to point out any infirmity in fact or law, no question of law arose for consideration – Held, yes [Para 8] [In favour of assessee)”

“Section 68 of the Income-tax Act, 1961-Cash credits -Assessment year 2001-02-Whether though in section 68 proceedings, initial burden of proof lies on assessee, yet once he proves Identity of creditors/share applicants by either furnishing their PAN numbers or income-tax assessment numbers and shows genuineness of transaction by showing money in his books either by account payee cheque or by draft or by any other mode, then onus of proof would shift to revenue and just because creditors/share applicants could not be found at address given, it would not give revenue right to invoke section 68 – Held, yes”

“The assessee had produced on record the documents to establish the genuineness of the party such as PAN of all the creditors along with the confirmation, their bank statements showing payment of share application money, only because those persons had not appeared before the Assessing Officer would not negate the case of the assessee. Therefore, the addition was liable to be deleted.”

“In a case where the assessee has furnished all the relevant facts within the knowledge and offered a credible explanation, then the onus reverts to the Revenue to prove that these facts are not correct. In such a case, Revenue cannot draw inference based on suspicion or doubt or perception of culpability etc.

“Where assessee received share premium from founder promoter and had discharged its burden of proving his identity, genuineness and creditworthiness, and both lower authorities could not find any defects or fault therein, addition made under section 68 was directed to be deleted.”

“Section 68 of the Income-tax Act, 1961 Cash credit (Unsecured loans) Assessment year 2009-10 During year assessee company received an unsecured loan of certain amount from three parties Assessing Officer made addition towards said amount received on grounds that loan transactions were nothing but accommodation entries of assessee’s own unaccounted income Inform of unsecured loan It was noted that assessee had produced various details including financial statement and bank statements of creditors and their confirmation letters Assessee had also produced source of income of said creditor firms which was commission received by them from certain companies -Further, all these transactions of receiving loan by assessee were routed through proper banking channel Thus, assessee had proved identity and credit-worthiness of parties and genuineness of transactions Further, Assessing Officer had not brought on record any evidence to prove that said sum was undisclosed income of assessee Whether, on facts, impugned addition made undersection 68 on account of said amount received by assessee was unjustified and same was to be deleted – Held, yes [Paras 9 and11] [In favour of assessee)”

Section 68 of the Income-tax Act, 1961 Cash credit (Share application money) Assessment year 2010-11-Assessing Officer noted that assessee had disclosed funds from three Kolkata based companies as share application money But, since where about of above companies were doubtful and their identity could not be authenticated, Assessing Officer treated aforesaid funds as money from unexplained sources and added same to income of assessee as unexplained cash credit under section 68-However, it was found that assessee-company had furnished PAN, coples of Income tax returns of creditors as well as copy of bank accounts of three creditors through which share application money was deposited in order to prove genuineness of transactions -Further, insofar as creditworthiness of creditors were concerned, Tribunal recorded that bank accounts of creditors showed that creditors had funds to make payments for share application money and in this regard, resolutions were also passed by Board of Directors of three creditors – Thus, first appellate authority had returned a clear finding of fact that assessee had discharged its onus of proving identity of creditors, genuineness of transactions and creditworthiness of creditors which finding of fact stood affirmed by Tribunal Revenue had not been able to show any perversity in aforesaid findings of fact by authorities below Whether therefore, Tribunal was right in confirming order passed by Commissioner (Appeals) and holding that no addition could be made under section 68-Held, yes [Paras 21, 23 and 24] [In favour of assessee)

“It can never be within the exclusive knowledge of the debtor to know the sources of income of the creditor. Once he is supplied the credit that he wants, he is satisfied. Once he has furnished the true identity, the correct address and the correct GIR number of the creditor, fulfils his obligation under the Act. The assessee is not supposed to know the capacity of the money-lender or the cash creditor. It is within the exclusive domain of the creditor. It is for that specific purpose that section 131 of the Act has been introduced so that in case of any suspicion, the ITO or the authorities concerned may exercise the power of a civil court under that provision and call upon the creditor concerned to prove his capacity to pay and the genuineness of the transaction. Once the ITO or the authority concerned is satisfied that the creditor is not telling the truth, it has been left open to the assessee to discharge his subsequent onus of proving the genuineness of the transaction and the capacity of the creditor to pay, by cross-examining him.”

Where assessee-company received share capital including share premium and furnished various documentary evidences in form of confirmation from investor, statement of bank account of investor etc. so as to substantiate identity and creditworthiness of investor and genuineness of transaction and revenue falled to bring on record anything adverse to these evidences, Impugned addition made under section 68 in respect of such share capital amount was unjustified”

“The Tribunal, in our view, has correctly appreciated the position in law which is that when an unexplained credit is found in the books of account of an assessee the Initial onus is placed on the assessee. The assessee is required to discharge this oner of initial onus. Once that onus is discharged, it is for the revenue to prove that the credit found in the books of accounts of the assessee is the undisclosed income of assessee. In the circumstances obtaining in the present case, in our view, the assessee has discharged that initial onus. The assessee is not required thereafter to prove the genuineness of the transactions as between its creditors and that of the creditors source of income, i.e., the subcreditors [See Nemi Chand Kothari K v. CIT & Anr. (2003) 264 ITR 254 and judgment of this court in ITA No. 1158/2007 Mod Creations Pvt. Ltd. v. Income Tax Officer decided on 29.08.2007]”

“We find considerable force of the submissions of the leamed counsel for the appellant that the Tribunal has merely noticed that since the summons Issued before assessment returned unserved and no one came forward to prove. Therefore it shall be assumed that the assessee failed to prove the existence of the creditors or for that matter creditworthiness. As rightly pointed out by the learned counsel that the CIT(Appeals) has taken the trouble of examining of all other materials and documents viz., confirmatory statements, invoices, challans and vouchers showing supply of bidi as against the advance. Therefore, the attendance of the witnesses pursuant to the summons issued in our view is not important. The important is to prove as to whether the said cash credit was received as against the future sale of the produce of the assessee or not. When it was found by the CIT(Appeal) on fact having examined the documents that the advance given by the creditors have been stablished the Tribunal should not have ignored this fact finding.”

| i. | The assessee is under a legal obligation to prove the genuineness of the transaction, the identity of the creditors, and creditworthiness of the investors who should have the financial capacity to make the investment in question, to the satisfaction of the AO, so as to discharge the primary onus. |

| ii. | The Assessing Officer is duty bound to investigate the creditworthiness of the creditor/subscriber, verify the identity of the subscribers, and ascertain whether the transaction is genuine, or these are bogus entries of name-lenders. |

| iii. | If the enquiries and investigations reveal that the identity of the creditors to be dubious or doubtful, or lack credit-worthiness, then the genuineness of the transaction would not be established. In such a case, the assessee would not have discharged the primary onus contemplated by Section 68 of the Act.” |

Section 68 of the Income-tax Act. 1961 Cash credits (Burden of proof) A search in premises of ‘B’ Group led to survey in premises of assessee herein. Thereupon Assessing Officer completed assessment wherein addition was made to assessee’s income under section 68- Commissioner (Appeals) as well as Tribunal deleted said addition holding that relevant enquiry based upon materials furnished by assessee had not been made High Court also found that assessee had discharged onus initially cast upon it by providing basic details which were not suitably enquired into by Assessing Officer – Accordingly, High Court upheld order passed by Tribunal Whether, on facts, SLP filed against order of High Court was to be dismissed Held, yes [Para 4] [In favour of assessee]

“There is no finding that material disclosed was untrustworthy. No evidence has been brought on record, if investment made by the Investor Company actually emanated from the coffers of the assessee company so as to enable the total investments to be treated as undisclosed income of the assessee. No interference is called for in the matter. Ground No. 3 of the appeal of the Revenue is dismissed. No other point is argued or pressed.”

“The assessee during the course of proceedings has discharged its liability by submitting necessary evidence available to establish the bona fide of the transactions. Thereafter, the onus shifted on to the revenue to prove that the claim of the assessee was factually incorrect. Simply by pointing out that the applicant companies did not have sufficient income or that the bank accounts indicated credits and debits in rapid succession leaving little balance does not discharge the burden cast upon the revenue to take an adverse view in the matter.

“When the entry stands in the name of the third party and the assessee establishes the identity of the creditor and produces evidence showing that the entry is not fictitious, initial burden lying on the assessee stands discharged; the burden shifts on to the Revenue to show that the entry represented assessee’s suppressed Income.”

“Where the assessee furnished the bank statements of the loan creditors, evidencing their credit worthiness, the assessee has discharged its burden. No additions can be made unless a contrary finding is established by the AO.”

“Amounts of loan were received by cheques and repayment also made by cheques through assessee’s bankers. The creditors gave confirmation letters mentioning therein their Income-tax file numbers. ITO without making any further enquiry, disbelieving the evidence of the assesse made addition. ITAT held the addition not justified as the assessee discharged the onus. High Court held that the Tribunal was justified in deleting the addition. Similar view was expressed in the case of ACIT v. Divine (India) Infrastructure (P) Ltd. reported at [2014] 42 CCH 0022 (Del Trib.)

“Where Assessing Officer made addition on account of unexplained cash deposit in bank on ground that assessee did not have sufficient cash balance and there was no conclusive proof as to how such huge amount came into possession of assessee in form of cash, since cash was duly accounted for in cash book and audited bank accounts, impugned addition was to be deleted”

“Where Assessing Officer had made an addition treating cash deposits as income from undisclosed sources, since cash deposits were made out of cash withdrawals, impugned addition was to be deleted”

“Assessee’s explanation that cash found was out of withdrawals made by him from bank from time to time, was not accepted by Assessing Officer Cash-flow statement furnished by assessee was also rejected by Assessing Officer on basis of suspicion that assessee must have spent amount for some other purposes – Assessing Officer, accordingly, made addition by treating aforesaid cash as unexplained cash Tribunal found that as per cash book maintained by assessee, assessee had withdrawn from bank certain amount which was far in excess of cash found during course of search proceedings and that no material had been relied upon by assessing authority to support its view that entire cash withdrawals must have been spent by assessee – Accordingly, Tribunal held that addition made was not legally sustainable under section 158BC and same was ordered to be deleted -Whether order of Tribunal was justified – Held, yes”

“Once the assessee disclosed the source emanating from the withdrawal made on a given date from a given bank, the revenue was not concerned with what the assessee did with that money. Without proper investigation as to the genuineness of such deposits or documentary evidence, the ITO could not merely surmise that it would be improbable for the assessee to keep Rs. 15,000 unutilized for a period of two years. He should have given the assessee an opportunity to substantiate his assertion as to the source, of his capital outlay. Since the Commissioner also did not approach the problem in this manner, it could not be said that he exercised his revisional jurisdiction judicially and properly.”

“5. Having carefully examined the orders of the lower authorities in the light of the rival submissions, we find that the Assessing Officer has made addition on the basis AIR information. Though cash flow statement was furnished before him, but he has not looked into while making the addition; whereas the Id. CIT(A) has examined all the entries in the cash flow statement, which is available on record. In the cash flow statement, the movement of cash was disclosed and it is evident that on all dates whenever cash was deposited in the bank, the assessee was having sufficient cash balance. Nothing has been brought on record to demonstrate that the cash withdrawn by the assessee was exhausted or utilized for other purposes and the deposits were made out of undisclosed sources. In the light of these facts, we are of the considered opinion that the assessee has properly explained the source of deposits in the bank, which was properly appreciated by the Id. CIT(A). Accordingly, we find no Infirmity in the order of the Id. CIT(A) and we confirm the same.”

“8. The assessee has stated specifically that the amount was redeposited on withdrawal from the bank and sufficient cash was available. Therefore, it was the duty of the Assessing Officer to examine this fact. Further nothing is brought on record that the amount was utilized by the assessee on withdrawal from the bank account. Considering the facts of the case in the light of the decision of the hon’ble Punjab and Haryana High Court in the case of Shivcharan Dass (supra), we set aside the orders of the authorities below and restored the issue to the file of the Assessing Officer with directions to redecide this issue by giving reasonable sufficient opportunity of being heard to the assessee and the Assessing Officer shall pass a reasoned order on the submissions of the assessee.”

17. In our considered opinion, once cash flow statement is not controverted by the -Assessing Officer as well as the Id. CIT[A], when it was specifically submitted that the same is based on the entries made in the cashbook, then the source of cash deposit in the bank account cannot be discarded by the authorities below.”

5. I have considered the rival submission. I am of the view that the explanation offered by the Assessee with regard to the source of deposit of Rs. 15.00 lakhs in his bank account is satisfactory and therefore, no addition can be made on account of unexplained cash. As rightly contended by the Id. Counsel for the Assessee, the withdrawal of cash from the bank account prior to deposit of cash is not disputed by the revenue. The fact that the Assessee did not explain the reasons for withdrawal of cash from his bank account cannot be the basis to hold that the source of deposit of cash was not explained by the Assessee. The legal position in this regard is that if the deposit of money in the bank account is preceded by withdrawal of money from the very same bank account, then the source of funds is prima facie demonstrated or explained by the Assessee. The Honorable Karnataka High Court in the case of S. R. Ventakaratnam v. CIT, Karnataka- 1 & Others 127 ITR 807 has held that once the Assessee discloses the source as having come from the withdrawals made on a given date from a given bank, it was not open to the revenue to examine as to what the Assessee did with that money and cannot chose to disbelieve the plea of the Assessee merely on the surmise that it would not be probable for the Assessee to keep the money unutilized. The decision of the Hon’ble Karnataka High Court supports the plea of the assessee. It is seen that the cash deposits in the bank account are preceded by withdrawal from the very same bank account. I am of the view that the ratio laid down in the aforesaid judgment will apply to the facts of the present case. If the revenue wants to disbelieve the plea of the Assessee, then it must show that the previous withdrawal of cash would not have been available with the Assessee on the date of deposit of cash in the bank account. The AO and CIT(A) have proceeded purely on assumption and surmises that cash withdrawn was not available to the Assessee on completely. extraneous factors. In our view, the Assessee has satisfactorily explained the source of funds out of which deposit of cash was made in the bank account. I therefore delete the addition made in this regard. Consequently, the appeal of the Assessee is allowed.