ORDER

Anubhav Sharma, Judicial Member.- This appeal is filed by the assessee against the order u/s 250 of the Income Tax Act [hereinafter referred to as ‘the Act’] dated 011.09.2025 passed by the Learned Commissioner of Income Tax (Appeals)-3, Noida [hereinafter referred to as ‘the CIT(A)’] in regard to assessment order dated 30.09.2021 u/s 143(3)r.w.s 263 of DCIT, Central Circle-1, Noida[hereinafter referred as ‘the AO].

2. On hearing both the sides we find that the appellant filed his return of income on 14.09.2016 declaring total income of 16,76,97,150/. The copy of notice u/s 143(2) as enclosed at page no 126 to 129 of the PB reveals that the case was selected for compulsory manual scrutiny vide notice dated 25.09.2017 under section 143(2), purportedly in terms of para 1(i) of CBDT Instruction No. 5/2017 dated 07.07.2017.During the course of assessment proceedings, notice under section 142(1) dated 09.10.2018 was issued, and subsequently notice dated 14.11.2018 sought details regarding investments and claim of exemption under section 10(38) of the Act from capital gain of Rs. 8,74,51,109/- arising from sale of shares of M/s CCL International Ltd., which was responded by reply dated 09.12.2018.

3. The case set up by the assessee was that the shares were purchased at Rs. 31 per share (total 1,03,85,000), held in broker pool account, later transferred to demat upon payment of 1 crore on 21.03.2014 and 24.03.2014, and sold during May-June 2015 through recognized stock exchange after holding for more than 12 months. Sale consideration of 9,74,50,133/- was received through banking channel.

4. After examining these materials, the original assessment was completed on 31.12.2018 under section 143(3) without making any addition whatsoever on account of LTCG on CCL shares.

5. Subsequently, proceedings under section 263 were initiated on 22.03.2021 on the basis of an Investigation Wing, Kolkata report alleging that CCL International Ltd. was one of 84 scrips identified for providing accommodation entries of bogus LTCG. The appellant furnished detailed reply dated 25.03.2021 along with Tribunal decisions and precedents and SEBI adjudication order in the case of CCL wherein proceedings were disposed. Thereafter order under section 263 was passed on 27.03.2021 alleging that the AO failed to consider the investigation report.

6. Thereafter, the assessee preferred an appeal before the this Tribunal against the order passed under section 263 of the Act, however, the said appeal came to be dismissed vide order dated 30.05.2025.Pursuant to the findings recorded by the Tribunal, the Assessing Officer completed the assessment and made anaddition of 8,74,51,109/- under section 68 of the Act by treating the Long Term Capital Gain declared by the assessee as income arising from alleged penny stock transactions. Further, an addition of Rs. 26,23,533/- was made under section 69C of the Act on account of alleged unexplained expenditure, being commission estimated at 3% for purportedly arranging accommodation entries.

7. The appellant preferred appeal before the CIT(A). However, vide order impugned order dated 01.09.2025, the appeal was dismissed for which assessee is in appeal raising various grounds and following additional ground;

That the Ld. CIT(A) has erred in law and on facts in upholding the assessment completed by the Ld. Assessing Officer, despite the fact that the notice issued under section 143(2) of the Income-tax Act, 1961 was not in conformity with CBDT Instruction No.5/2017 dated 07.07.2017.

8. We first deal with the additional ground and the corresponding issue pertains to the validity of the manual selection of the assessee’s case for scrutiny and the consequent assumption of jurisdiction under section 143(2) of the Income-tax Act, 1961.As the same is pure legal issue it is admitted for hearing.

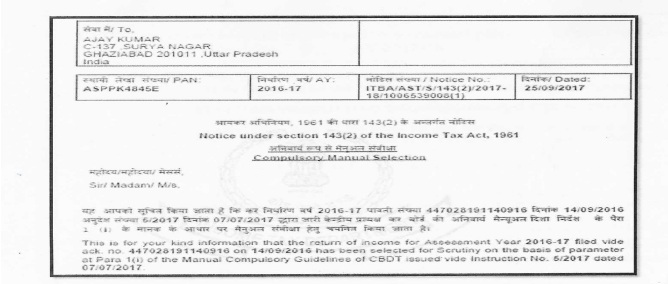

9. The case of the assessee was selected for scrutiny by issuance of a mandatory notice under section 143(2) dated 25.09.2017. In the said notice, it has been specifically mentioned that the case was selected on the basis of the return of income filed on 14.09.2016 and that the reason for selection falls under Para 1(i) of the Manual Compulsory Scrutiny Guidelines issued by the CBDT vide Instruction No. 5/2017 dated 07.07.2017. The said notice was issued by the DCIT, Central Circle, Noida, and a copy thereof is placed at page Nos. 126-129 of the Paper Book. The relevant snapshot is reproduced for your ready reference:-

10. That plain reading of Para 1(i) of CBDT Instruction No: 5/2017 dated 07.07.2017 makes it abundantly clear that manual selection for scrutiny under this clause is permissible only in cases where additions have been made in earlier assessment years on a recurring issue of law and such additions exceed 10 lakhs in non-metro charges and 25 lakhs in metro charges. Thus, the Instruction prescribes specific and mandatory preconditions for invoking manual scrutiny under the said category.

11. In the present case, the assessee falls within a non- metro charge. However, it is an undisputed fact that no addition whatsoever had been made in the earlier assessment years, nor had any order been passed sustaining any addition on a recurring issue. In support thereof, the relevant order sheet and assessment records have been placed at page No. 155-161of the Paper Book, which clearly demonstrate that no such additions existed in the preceding years. Therefore, Department could not contest and deny that the essential condition precedent for invoking Para 1(1) of Instruction No. 5/2017 was wholly absent in the case of the assessee.

12. Ld. Counsel has submitted that once the notice under section 143(2) of the Act was issued by specifically invoking Para 1(i) of the aforesaid Instruction, the validity of the selection must be examined strictly on that basis alone. The Revenue cannot subsequently improve upon or alter the reasons for selection by contending that the case could have been selected under some other clause of the Instruction. The selection must stand or fall on the reasons recorded at the time of issuance of notice.

13. It is well settled that circulars and instructions issued by the CBDT under section 119 of the Act are binding upon the Revenue authorities and reliance for this can be placed on the decision of the Hon’ble Supreme Court in Commissioner of Customs v. Indian Oil Corpn. Ltd. ITR 272 (SC). Therefore, compliance with Instruction No. 5/2017 was mandatory and not discretionary. Furthermore, the settled law is that AO is strictly liable to follow the circulars and instructions and for this proposition reliance can be placed on the decision in UCO Bank v. CIT (SC) and Keshavji Ravji & Co. v. CIT (2) TMI 1-Supreme Court.

14. Ld. Counsel has placed reliance on the decision of Coordinate Bench of the in the case of DCIT, ITO v. Raja Arora 2024 (11) TMI 158 to contend that Co-ordinate Benchhas dealt with CBDT Instruction No. 5/2017 dated 07.07.2017. The case therein had been selected under Para 1(vi) of the Manual Compulsory Scrutiny Guidelines; however, the mandatory approval as contemplated under the said Instruction was not found to have been properly accorded on record. The Coordinate Bench categorically held that the Instructions issued by the CBDT are binding on the Departmental authorities and are required to be strictly complied with. Since the procedural safeguards and mandatory conditions prescribed in the Instruction were not adhered to, the Tribunal held that the assumption of jurisdiction was invalid and the assessment was liable to be quashed. The Revenue carried the matter further before the Hon’ble High Court in the case of Pr. CIT v. Raja Arora (Delhi) and the Hon’ble High Court dismissed the appeal and affirmed the view taken by the Tribunal, thereby upholding the principle that CBDT Instruction No. 5/2017 must be strictly followed and any deviation therefrom vitiates the proceedings.

15. In the present case also the conditions prescribed under Para 1(i) of the Instruction were admittedly not satisfied. Therefore, the selection itself being contrary to the binding CBDT Instruction, the consequent notice under section 143(2) and the assessment framed pursuant thereto are liable to be held as invalid and without jurisdiction. As submitted by ld. DR, the defect in the present case is not a mere procedural irregularity but goes to the root of the assumption of jurisdiction and such jurisdictional defect cannot be cured under section 292BB of the Act. In view of the foregoing facts and settled legal position, the manual selection of the assessee’s case under Para 1(i) of Instruction No. 5/2017 being contrary to the binding CBDT guidelines renders the notice issued under section 143(2) invalid and without jurisdiction. Consequently, the assessment framed under section 263 read with section 143(3) of the Act, being founded upon such invalid notice, is bad in law and void ab initio. The addition made by the Assessing Officer pursuant to such illegal assumption of jurisdiction is, therefore, liable to be deleted.

16. The additional ground deserves to be sustained. The appeal is allowed.