ORDER

B.M. Biyani, Accountant Member.- Feeling aggrieved by order of first appeal dated 21.06.2023 passed by learned Commissioner of Income-Tax (Appeals)-NFAC, Delhi [“CIT(A)”] which in turn arises out of assessment-order dated 19.03.2021 passed by learned National e-Assessment Centre, Delhi [“AO”] u/s 143(3) r.w.s. 143(3A) & 143(3B) of Income-tax Act, 1961 [“the Act”] for Assessment-Year [“AY”] 201819, the assessee has filed this appeal on following grounds:

“1. That on the facts and in the circumstances of the case and in law, the Ld CIT(A) erred confirming the action of the Ld Assessing Officer in denying the benefit of exemption under section 11 and 12 of the income-tax Act, 1961 and assessing the total income of the appellant at Rs. 2,52,05,314/- without properly appreciating the facts of the case and submissions filed before him/her even when registration order under section 12AA of the Income-tax Act, 1961 in the case of the appellant was duly granted to the appellant on 03-02-2021 i.e. during the course of pendency of assessment proceedings for Assessment Year 2018-19 and the object & activities of the appellant remained same as compared to the year of registration and therefore, the appellant was eligible for benefit of section 11 and 12 as per section 12A of the Income-tax Act, 1961 for Assessment Year 2018-19 also.

2. That on the facts and in the circumstances of the case and in law, the Ld CIT(A) erred confirming the action of the Ld Assessing Officer in denying the benefit of exemption under section 11 and 12 of the income-tax Act, 1961 and assessing the total income of the appellant at Rs. 2,52,05,314/- by stating that the appellant has not claimed exemption under section 11 and 12 of the Act by way of filing of revised income-tax return even when the appellant had duly lodged additional claim to allow exemption under section 11 and 12 of the Act as eligible to the appellant during the course of assessment proceedings itself.

3. That on the facts and in the circumstances of the case and in law, the Ld CIT(A) erred confirming the action of the Ld Assessing Officer in denying the benefit of exemption under section 11 and 12 of the income-tax Act, 1961 and assessing the total income of the appellant at Rs. 2,52,05,314/- by stating that the appellant has not filed audit report in Form No. 10B within time even when the appellant has duly filed Form No. 10B during the course of assessment proceedings itself.

4. The appellant reserves the right to add, alter and modify the grounds of appeal as taken by it. “

2. The brief facts of the case are as under:

| (i) |

|

The assessee is a society registered in the State of Madhya Pradesh, engaged in charitable purpose of advancing education through a school named “Oxford Academy School” and a college named “Oxford International College”. For AY 2018-19 under consideration, the assessee filed its return of income on 30.03.2019 u/s 139(4C) of the Act declaring income of Rs. 3,95,65,648/-; claiming exemption of Rs. 3,95,65,648/- u/s 10(23C)(iiiad) and thus offering taxable/total income of Rs. Nil. The case of assessee was selected for scrutiny assessment. During scrutiny-proceedings, the AO issued questionnaire dated 15.12.2020 and 04.02.2021 u/s 142(1) calling various details/explanations. In response, the assessee filed letter dated 08.02.2021 (Paper-Book Pages 43-45). In the letter so filed, the assessee intimated to AO that it has wrongly claimed exemption u/s 10(23C)(iiiad). However, the assessee is holding registration u/s 12AA granted by CIT (Exemption), Bhopal vide Order dated 03.02.2021 from AY 2020-21 and consequently eligible for exemption u/s 11/12 in AY 2018-19 given by Proviso to section 12A(2) reading as under: |

“12A(2) Where an application has been made on or after the 1st day of June, 2007, the provisions of sections 11 and 12 shall apply in relation to the income of such trust or institution from the assessment-year immediately following the financial year in which such application is made.

Provided that where registration has been granted to the trust or institution under section 12AA, then, the provisions of sections 11 and 12 shall apply in respect of any income derived from property held under trust of any assessment year preceding the aforesaid assessment year, for which assessment proceedings are pending before the Assessing Officer as on the date of such registration and the object and activities of the trust or institution remain the same for such preceding assessment year:”

Further, alongwith aforesaid letter dated 08.02.2021, the assessee filed several documents including (i) a revised Computation of Total Income claiming exemption u/s 11/12 in place of exemption u/s 10(23C)(iiiad), (ii) copy of Order of registration u/s 12AA dated 03.02.2021 issued by the CIT (Exemption), Bhopal, and (iii) physical copy of Auditor’s Report (Form No. 10B) dated 04.02.2021. The assessee submitted that it satisfies all conditions prescribed in Proviso to section 12A(2) and accordingly requested the AO to give benefit of same. Subsequently, the assessee also e-filed Auditor’s Report (Form No. 10B) on 27.02.2021, copy of e-filing acknowledgement downloaded from departmental portal is filed (Paper-Book Page 48).

| (ii) |

|

The AO, however, issued show-cause notice dated 24.02.2021 to assessee, as under: |

“Kindly refer to the above

2. You have filed a return of income for A. Y. 2018-19 u/s. 139(4c) of the IT Act on 30.03.2019, declaring total income at Rs. Nil. On verification of the return of income for A.Y 2018-19, it is noticed that the aggregate income referred to in sections 11, 12 and u/s 10(23C) derived during FY. 2017-18 is Rs. 3,95,65,648/- and you have claimed exemption u/s. 10(23C)(iiiad) of Rs. 3,95,65,648/

3. During the course of assessment proceeding, you have filed Form 10B, Audit report u/s 12A(b) of the Act., dated 04.02.2021. The same have been considered but not acceptable

Section 12A(b) read as under:

“.Where the total income of the trust or institution as computed under this Act without giving effect to (Provision of section 11 and section 12 exceeds the maximum amount which is not chargeable to income tax in any previous year), the accounts of the trust or intuition for that year have been audited by an accountant as defined in the explanation below sub-section (2) of section 288 and the person in receipt of the income furnishes along with the return of income for the relevant assessment year the report of such audit in the prescribed form duly signed and verified by such accountant and setting forth such particulars as may be prescribed.”

3.1 Therefore, as per section 12A(b) of the Act, the assessee has to filed audit report in form No. 10B before the due date u/s 139(1) of the Act. As you have failed to filed the Audit report within time prescribed. The claim of exemption u/s 11 cannot be entertained.

4. Accordingly, you have hereby show cause as to why an amount received of Rs 3,95,65,648/- should not be added to your total income. In this regards, you are requested to submit your details/explanations on or before 01.03.2021. Please note that no further adjournment will be given. Failure to complied to this notice, assessment will be completed on the basis on the material available on record without given any further notice.”

[emphasis supplied]

| (iii) |

|

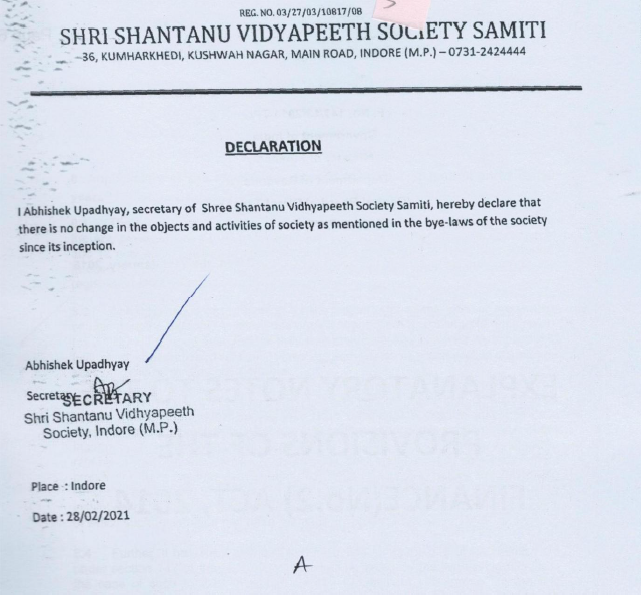

In response to show-cause notice, the assessee filed another reply dated 01.03.2021 giving a detailed explanation in support of eligibility of exemption u/s 11/12 on the basis of above-noted Proviso to section 12A(2); CBDT Circular No. 01/2015 dated 21.01.2015 and judicial rulings in favour of assessee. The assessee also filed following ‘declaration’ to AO in terms of requirement of Proviso to section 12A(2): |

| (iv) |

|

However, the AO rejected assessee’s reply by making following observations in Para 6 of assessment-order: |

“6. In response to show cause notice, the assessee uploaded letter dated 01.03.2021. The submission of the assessee is considered but the same is not acceptable. The assessee filed first time returned of income for A.Y. 2018-19 u/s 139(4C) of the Act and not filed audit report on due date. The assessee has stated that they have filed return incorrectly. They later revised computation, have uploaded/e-filed Audit report Form 10B on income tax portal on 27.02.2021 and claimed exemption u/s 11(1)(a) of the Act. Further, the assessee submitted comparative chart of income and relied on CBDT circular and has requested to consider the same. The assessee further stated that assessee society is registered u/s 12AA, has requested to condone delay in filling Form 10B and also relied on CBDT circular and case laws.

6.1 In this regards, it is submitted that the assessee has not revised return of income for A.Y. 2018-19, it is pertinent to mention here that power of condonation of delay u/s 119(2)(b) does not vest with the AO but with the Commissioner of Income Tax. Hence, plea for accepting the revised computation and Form 10B dated 04.02.2021 is hereby rejected. As stated in the show cause, as per section 12A(b) of the Act, the assessee has to filed audit report in form No. 10B before the due date u/s 139(1) of the Act electronically. The claim of assessee for exemption u/s 11 of the Act is hereby rejected as the assessee failed to file form 10B within due date of filling return u/s 139(1) of the Act and entire receipt of Rs. 3,95,65,648/- is brought to tax and hence added to total income. Penalty proceedings is being separately initiated u/s 270A of the Income Tax Act, 1961 for under-reporting of income. “

[emphasis supplied]

| (v) |

|

Ultimately, in Para 7 of assessment-order, the AO did not grant exemption claimed by assessee u/s 11/12 and thus assessed the taxable/total income of assessee at Rs. 3,95,65,648/- (rounded off to Rs. 3,95,65,650/-). |

| (vi) |

|

Aggrieved, the assessee carried matter to CIT(A). The CIT(A) decided assessee’s appeal by following order: |

“3.1 It is found that the appellant in its return of income claimed the exemption of Rs.3,95,65,648/- under section 10(23C)(iiiad) of the Income tax Act. The appellant claimed exemption u/s 10(23C)(iiiad) even for A. Y. 201920. The provisions of section 10(23C)(iiiad) before its amendment from 01.04.2022 was as under :-

Any university or other educational institution existing solely for educational purposes and not for purposes of profit if the aggregate annual receipts of such university or educational institution do not exceed the amount of annual receipts as may be prescribed; or

The prescribed upper limit for claiming exemption under section 10(23C)(iiiad) read with Rule 2BC(1) of the I.T. Rules was Rs. one crore. Since, the receipt of the appellant society exceeded Rs. 1 crore, exemption under section 10(23C)(iiiad) was not available to the appellant. If this proposition is followed, there is no violation of article 265 of the constitution of India. The appellant has taken this ground as ground no. 3. Denial of exemption under section 10(23C)(iiiad) is as per the situation authorized by law.

3.2 The Assessing Officer has relied upon the issue of non-filing of form no. 10B before the due date of section 139(1) of the I.T. Act, 1961 electronically. He is absolutely correct. This is one of the conditions to be satisfied by any trust or institution. One has to satisfy other conditions also which are being discussed in the later parts of the order. One must apply for registration u/s 12A(1)(a).

4.1 In ground no. 2 the appellant has argued that the benefit of section 12AA should be made available to this assessment year also. Copy of the order u/s 12AA of the Income Tax Act, 1961 is available in the records, as submitted by the appellant. It is specifically written in para III of the order: –

“After considering the material available on record, the applicant trust/society/nonprofit company is hereby granted registration with salient activities as Education and the provisions of section 11 and 12 shall apply in the case from the Assessment Year 2020-21”.

The appellant has not challenged this order. So, Prima facie benefits of section 12AA must not accrue to the present assessment year. Coming to the contention of the appellant in ground no. 2 that the provisions of clause (b) of proviso of sub-section 2 of section 12AA should be applied in its case as assessment proceeding was pending in its case for the present assessment year at the time of order u/s 12AA by CIT (Exemption), Bhopal. But in my opinion this proposition of the appellant is not correct as all the provisions (Proviso) of sub-section 2 of section 12AA has been made effective from 01.04.2021 and these are not retrospective in nature from any angle. So, this contention of the appellant is also rejected. Order by the CIT(Exemption), Bhopal has been passed on 03.02.2021.

4.2 The appellant should also keep in mind the provisions of sub-section 2 of section 12A. As per this section, provisions of section 11 and 12 are to be applied from the assessment year immediately following the financial year in which such application is made. Application was filed by the applicant on 24.01.2020; means F.Y. 2019-20. Assessment year immediately following the financial year in which application was made is 2020-21. So, the CIT(Exemption), Bhopal has rightly made the provisions applicable from A. Y. 2020-21. The newly introduced provisions as already stated above are applicable from 01.04.2021, i.e. A.Y. 2021-22. The provisions of sub section 2 of section 12A are reproduced below:-

[(2) where an application has been made on or after the 1st day of June, 2007, the provisions of sections 11 and 12 shall apply in relation to the income of such trust or institution from the assessment year immediately following the financial year in which such application is made:]

So the appellant does not get any relief on ground 2 and 3.

5. Ground 4 is about applicability of the CBDT circular. Appellant prays that it is the duty of the officers of the Department to assist a taxpayer and it is also his duty to not take advantage of ignorance. But the appellant must also remember and enlighten himself that even the taxpayer has also some duty to perform. A person claiming his rights must not ignore his duty. Department is providing benefits to trust, charitable institutions and institutions engaged in public activity but there are certain conditions for that. A trust has to file its return of income, get its accounts audited, apply for registration under section 12A. CBDT circular is of no help when a trust is doing genuine work but it does not register it as a society, does not maintain proper books of accounts, does not fille return of income, does not file audit report, does not apply for registration under section 12A, etc. The Income Tax Act has provided specific conditions under section 12A for applicability of section 11 and 12 and this has to be followed strictly. Actually, the appellant is stretching the intent of the CBDT circular No. 14(XL-35) of 1955 to its undeserving benefit. The circular mainly aimed at facilitating refunds to the tax payers and it also aimed at advising the taxpayer of their rights and abilities. It did not provide any absolute protection from all sorts of omissions and commissions. The content of the circular is reproduced below.

“Officers of the department must not take advantage of ignorance of an assessee as to his rights. It is one of their duties to assist a tax payer in every reasonable way, particularly in the matter of claiming and securing reliefs and in this regard the officers should take the initiative in guiding a tax payer where proceedings or other particulars before them indicate that some refund or relief is due to him. This attitude would, in the long run, benefit the department, for it would inspire confidence in him that he may be sure of getting a square deal from the department. Although, therefore, the responsibility for claiming refunds and relief rests with the assessee on whom it is imposed by law, officers should-

1. draw their attention to any refunds or reliefs to which they appear to be clearly entitled but which they have omitted to claim for some reason or other;

2. freely advise them when approached by them as to their rights and liabilities and as to the procedure to be adopted for claiming refunds and relief”.

So, this ground has no merit and it is of no help to the appellant.

6. The appellant in ground no. 1 has raised the issue of Principles of Natural Justice. The appellant has agitated against the charging of tax on Gross Receipts of Society. The claim of the appellant appears to be prime facie correct. In cases which do not enjoy exemption u/s 11 and 12 by virtue of absence of registration under section 12AA/12A; the income to be treated as taxable should be the net income i.e. after allowing the necessary expenditures incurred. The appellant has furnished form no. 10B and financial on 16.09.2021. As per the enclosed income and expenditure account the surplus income of the appellant is Rs. 2,52,05,314/-. It is settled law that even an unregistered trust or society is liable for tax on its surplus only and not on the gross receipts. So, total income of the appellant should be Rs. 2,52,05,314/- only and not Rs. 3,95,65,648/- as taken and determined by the Assessing Officer. So, the appellant gets a relief of Rs. 1,43,60,334/-. Hence, ground no. 1 of the appellant succeeds. Appeal is “Partly Allowed”.”

[emphasis supplied]

| (vii) |

|

Still aggrieved, the assessee has come in next appeal before us. |

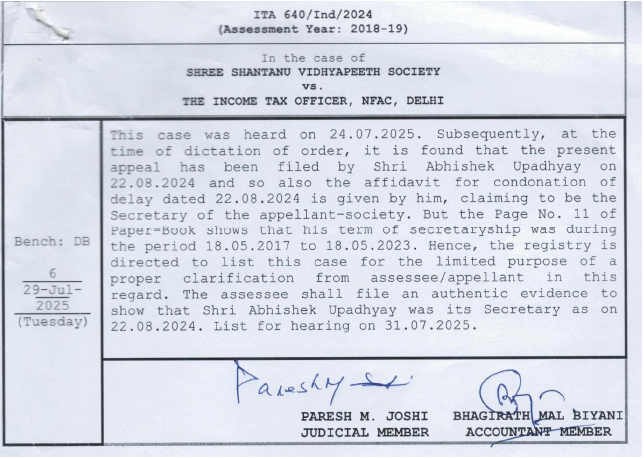

3. The appeal was initially heard by this very bench on 24.07.2025. Subsequently, vide Order-Sheet dated 29.07.2025 re-produced below, it was re-listed on 31.07.2025 for a clarification from assessee/appellant:

4. During hearing on 31.07.2025, Ld. AR for assessee filed necessary clarification and resolved the issue raised by bench. However, during such hearing, the Ld. DR for revenue submitted a “Revised Case Law Compilation” which was taken on record by bench. On next day i.e. 01.08.2025, the Ld. AR for assessee filed a letter to ITAT’s office vide Inward Entry No. 942 requesting that the assessee wants to file a detailed submission to address the revised submission filed by Ld. DR, therefore the appeal must be re-fixed for a detailed hearing. Therefore, in this situation, vide Order-Sheet dated 06.08.2025, the bench released this matter from “heard category” and directed the Registry to list the case for a fresh hearing before regular bench on 16.09.2025 after intimation to parties. Accordingly, this case has again come before this bench for a fresh hearing.

5. We have heard the learned Representatives of both sides at length and carefully perused the case-record including the orders of lower-authorities, the documents filed in Paper-Book and the Written-Submissions filed by parties.

Delay in appeal:

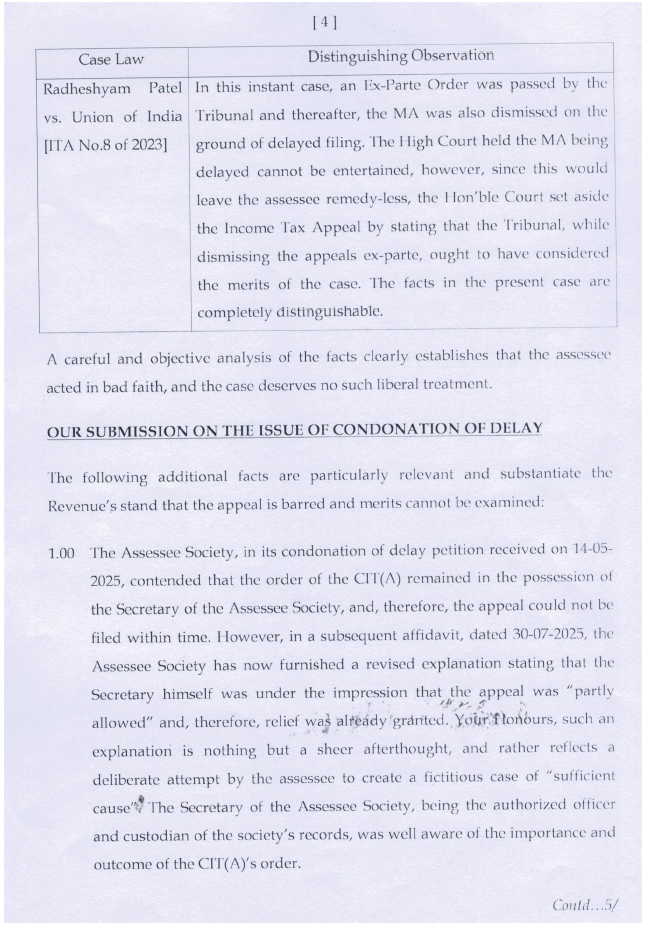

6. This appeal has been filed on 22.08.2024 against impugned order dated 21.06.2023 and accordingly there is a delay of 368 days. Ld. AR for assessee submitted that the assessee has filed an application for condonation of delay supported by two solemnised affidavits on stamp, one dated 22.08.2024 and other dated 30.07.2025. Both of these affidavits are deposed by Shri Abhishek Upadhyay/Secretary of assessee-society who has also filed this appeal and signed Form No. 36. Referring to contents of condonation-application and two affidavits, Ld. AR explained the reason of delay. He submitted that the impugned order was passed by CIT(A) on 21.06.2023 and served upon assessee on the very same day; the assessee has mentioned “date of service” as “21.06.2023” in relevant column of Form No. 36 and there is no objection of assessee against service by CIT(A). However, the impugned order remained with Shri Abhishek Upadhyay/Secretary. In so far as to why so happened, Shri Abhishek Upadhyay/Secretary has given a detailed explanation in Para No. 2 & 3 of 2nd affidavit, reading as under:

“2. The CIT(A) Order was passed in the case of M/s Shree Shantanu Vidhyapeeth Society for Assessment Year 2018-19 on 21-06-2023. On my prima-facie perusal of the Ld. CIT(A) order, wherein at the end of the order, it was mentioned that the Ground No. 1 of the appellant succeeds and the appeal is ‘partly allowed’, I was under the Bonafide impression that relief was granted and no further action was required. Screenshot of the relevant extract of the Ld. CIT(A)’s order dated 21-06-2023 is reproduced hereunder for ready reference of the Hon’ble Bench:

“6. The appellant in ground no. 1 has raised the issue of Principles of Natural Justice. The appellant has agitated against the charging of tax on Gross Receipts of Society. The claim of the appellant appears to be prime facie correct. In cases which do not enjoy exemption u/s 11 and 12 by virtue of absence of registration under section 12AA/12A; the Income to be treated as taxable should be the net income i.e., after allowing the necessary expenditures incurred. The appellant has furnished form no. 10B and financial on 16.09.2021. As per the enclosed income and expenditure account the surplus income of the appellant is Rs. 2,52,05,314/- It is settled law that even an unregistered trust or society is liable for tax on its surplus only and not on the gross receipts. So, total income of the appellant should be Rs. 2,52,05,314/- only and not Rs. 3,95,65,648/- as taken and determined by the Assessing Officer. So, the appellant gets a relief of Rs. 1,43,60,334/-. Hence, ground no. 1 of the appellant succeeds. Appeal is “Partly Allowed.”

3. Due to the aforesaid reason, I was under impression that the appeal was allowed and no further action was needed in the case of M/s Shree Shantanu Vidhyapeeth Society for Assessment Year 2018-19. Due to the said reason, the said order was remained with me and was not communicated to the counsel of the appeal for any further action.”

[emphasis supplied]

Thus, Ld. AR submitted, Shri Abhishek Upadhyay/Secretary has given a proper explanation for delay which is such that by reading of last sentence of impugned order he gained an understanding that the assessee had succeeded and no further action was required. However, when the assessee subsequently received penalty-notice u/s 270A dated 01.08.2024 for the same assessment-year [copy of penalty-notice is filed with condonationapplication], the matter was consulted with counsel who advised to file appeal against impugned order without any further delay (Para No. 3 of 1st affidavit and Para No. 4 of 2nd affidavit). Immediately, the assessee filed present appeal on 22.08.2024 as per advice of counsel. Ld. AR very humbly submitted that there is no lethargy, negligence, mala fide intention or ulterior motive of assessee in making delay and the assessee does not stand to derive any benefit because of delay. He further submitted that the sole reason of delay is as explained in the condonation-application and affidavits as narrated above. He submitted that the assessee has explained “sufficient cause” for delay. Ld. AR went ahead to submit that the assessee is a charitable institution and eligible for statutory exemption u/s 11/12 because of which the taxable/total income would be “Nil” and consequently the assessee would not have any tax liability. But at present the assessee is saddled with huge tax liability wrongly adjudicated by lower authorities in disregard to legal provisions of Income-tax Act, 1961. He submitted that the case of assessee is fully meritorious. He submitted that the delay deserves to be condoned. He relied upon certain decisions as mentioned in Condonation-Application, Paper-Book or his Written-Submissions from time to time.

7. Replying to this, Ld. DR for Revenue strongly objected. He firstly submitted that there is a delay of 368 days which is quite inordinate and cannot be considered as ordinary delay. Secondly, he submitted that there are two affidavits filed by assessee. In 1st affidavit, Shri Abhishek Upadhyay/Secretary has simply mentioned that the impugned order remained with him. This explanation itself conveys that there was a negligence on his part. Subsequently, in 2nd affidavit Shri Abhishek Upadhyay/Secretary has stated that he got an understanding that the relief was granted by CIT(A) and no further action was required, hence the impugned order was not communicated to counsel. He made a forceful submission that the averment made in 2nd affidavit is ‘after thought’. He submitted that the last sentence of CIT(A)’s order reads thus: “Hence, ground no. 1 of the appellant succeeds. Appeal is “Partly Allowed”. He submitted that the language of CIT(A) is very clear to the effect that the assessee succeeded for Ground No. 1 only and that the appeal was partly allowed, this language cannot lead to an understanding, as being claimed by Shri Abhishek Upadhyay/Secretary, that the first-appeal of assessee was allowed. He strongly opposed that the case of assessee does not have any cause” of delay much less “sufficient cause”. He submitted that the case does not have merit also because the AO has passed a judicious order as per provisions of law and the CIT(A) has already given legitimate relief to assessee. He submitted that if the delay is condoned in this case or such types of cases, the time-limit provision will become redundant and every assessee would be taking similar excuse.

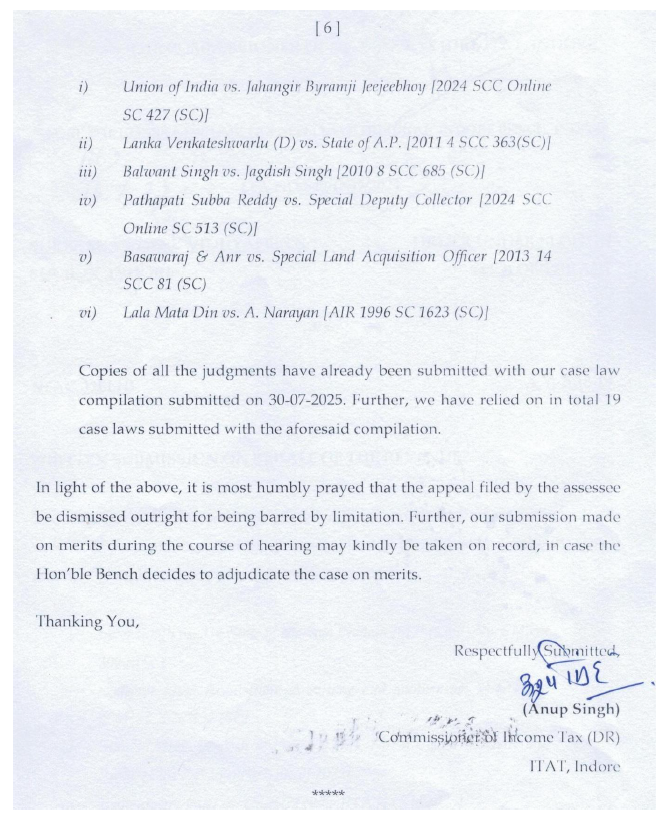

8. Ld. DR also filed a “Revised Case Law Compilation” containing as many as 19 decisions of Hon’ble Supreme Court, Hon’ble High Courts and benches of ITAT and narrated the brief ratio/key holdings in those cases during hearing. He contended that in these decisions, the Hon’ble Courts have taken significant conclusions as under:

| (i) |

|

the ‘length of delay’ is relevant meaning thereby ‘inordinate delay’ cannot be condoned. |

| (ii) |

|

the concepts such as ‘liberal approach’, ‘justice-oriented approach’, ‘substantial justice’ cannot be employed to jettison the law of limitation; |

| (iii) |

|

if the court finds that there has been ‘no negligence’ on the part of the applicant and the cause shown for delay does not lack bonafides, then it may condone the delay. If, on the other hand, the explanation given by the applicant is found to be ‘concocted or he is thoroughly negligent in prosecuting his cause’, then it would be a legitimate exercise of discretion not to condone the delay, |

| (iv) |

|

delay cannot be condoned on ‘fanciful stories’, |

| (v) |

|

‘merit of case’ cannot be considered in dealing with condonation, |

| (vi) |

|

there is no general proposition that ‘mistake of counsel’ by itself is always a sufficient ground. It is always a question whether the mistake was bonafide or was merely a decide to cover an ulterior purpose such as laches on the part of the litigant or an attempt to save limitation in an underhand way. |

9. In rejoinder, Ld. AR for assessee firstly submitted that there is no gap, contradiction or after-thought in the two affidavits of Shri Abhishek Upadhyay/Secretary. He submitted that in 1st affidavit, Shri Abhishek Upadhyay/Secretary has clearly mentioned that the impugned order remained with him. In para 3 of 2nd affidavit, he has given a detailed explanation as to why the impugned order remained with him and was not communicated to the counsel, which is such that he gained an understanding from reading of last sentence of impugned order that the assessee had succeeded in appeal and there was no necessity of taking further action. Thus, the 2nd affidavit is in continuation of 1st affidavit and gives a more detailed explanation. Secondly, he submitted that there is no question of malafide intention or ulterior motive of assessee in making delay. He submitted that the assessee was, right from AO and even before CIT(A), pursuing the claim of exemption u/s 11/12 statutorily granted by Proviso to section 12A(2). Further, there was a direct case decided way back by ITAT, Indore in Barkatullah Vishwavidyalaya v. Dy. CIT (Exemption) [IT Appeal No. 924 (Ind) of 2018, dated 30-6-2022] holding all issues in favour of assessee. When it was so, there was no reason of making delay in filing present appeal before ITAT against the orders of lower authorities. However, the delay has occurred only because of understanding (or misunderstanding) of Shri Abhishek Upadhyay/Secretary. Lastly, Ld. AR relied upon various decisions in favour of assessee wherein delay had been condoned by different courts considering the facts as well as meritorious nature of case. He particularly relied upon the landmark decision of Hon’ble Supreme Court in Collector, Land Acquisition v. Mst. Katiji (SC)/1987 AIR 1353, 1987 2 SCC 387 wherein the guiding principles for condonation of delay were laid down. He submitted that the assessee’s present case satisfies the guidelines set out by Hon’ble Supreme Court. He also referred a very latest judgement of Hon’ble Supreme Court dated 21.03.2025 Inder Singh v. State of Madhya Pradesh [SLP (Civil) No.6145 of 2024, dated 21-3- 2025].

10. Replying to re-joinder, the Ld. DR for revenue again relied heavily upon the decisions filed by him. Further, he submitted that in the case of Inder Singh (supra) relied by Ld. AR, there are some critical features to be noted by bench, namely (i) there was involvement of Covid-19 period as well, (ii) In para No. 18 of order, the Hon’ble Supreme Court has checked overall ‘circumspection’ and also observed that the court may not be liberal in futuro, and (iii) in para No. 21 of order, the Hon’ble Supreme Court also imposed a cost of Rs. 50,000/-. Hence, Ld. DR submitted, the assessee cannot derive any benefit from the said decision which is unique to itself.

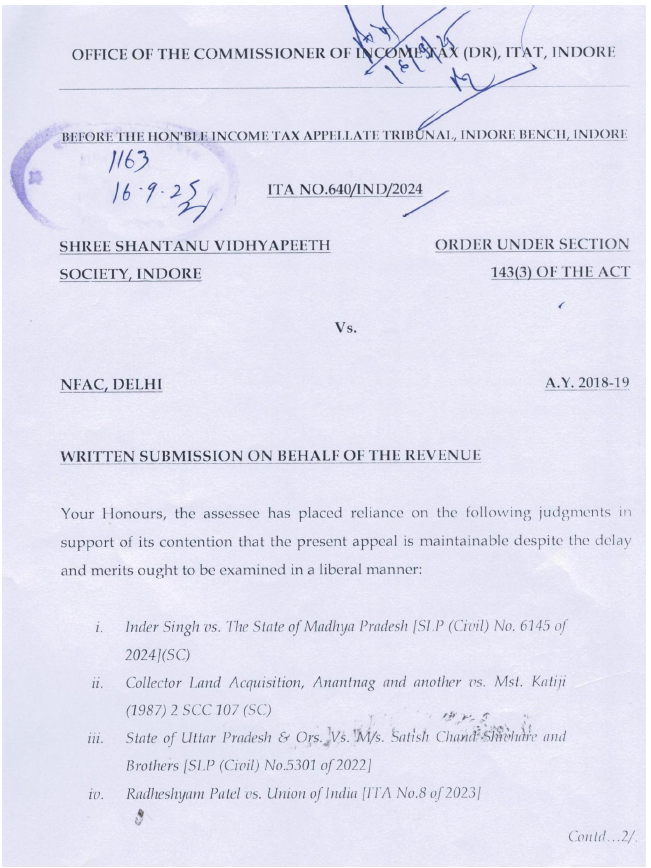

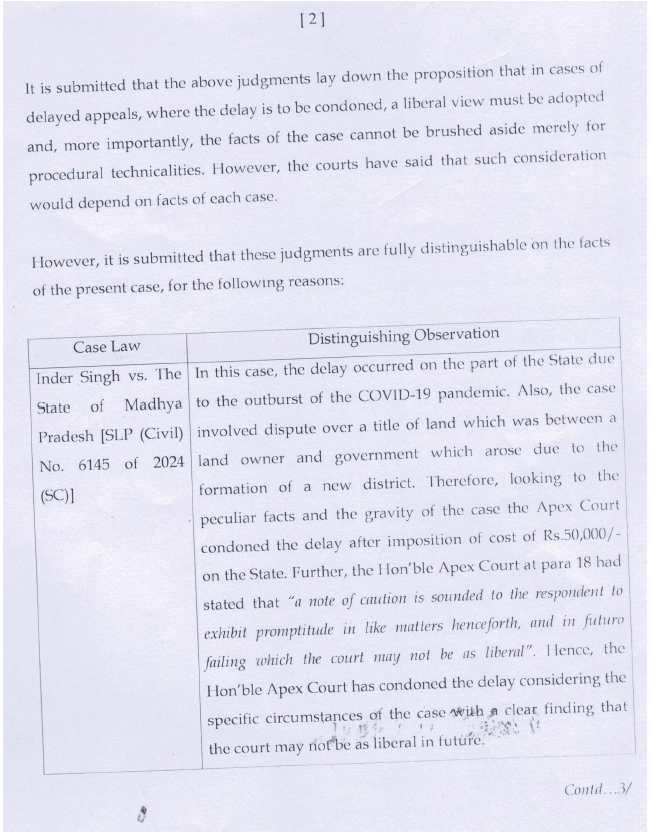

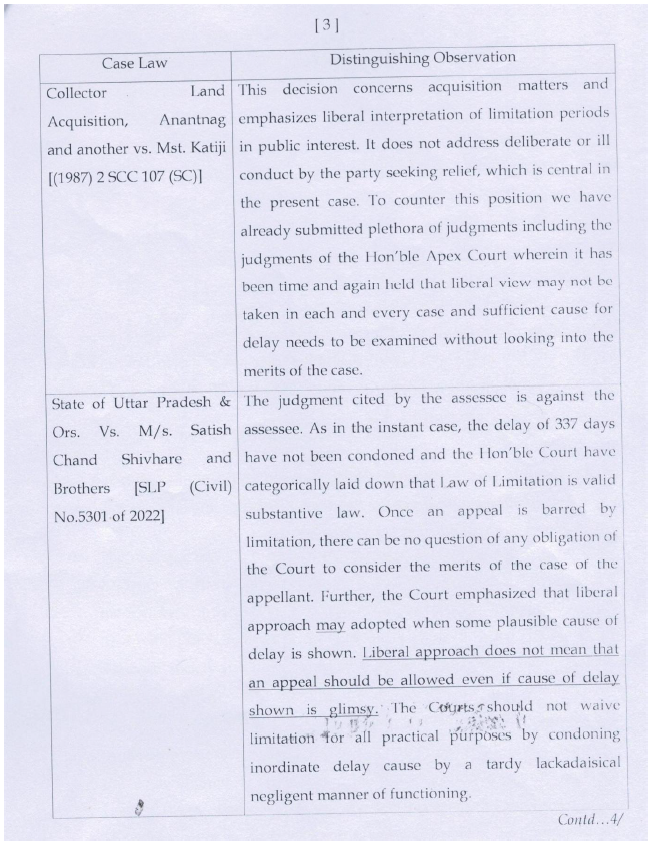

11. Yet again after conclusion of hearing, Ld. DR for revenue filed a “Written-Submission” to ITAT’s office vide Inward Entry No. 1163 dated 16.09.2025; the same is scanned and re-produced below:

12. Following same, the Ld. AR for assessee also filed his rebuttal in writing vide Inward Entry No. 1771 dated 18.09.2025 after serving a copy of same to the office of Ld. DR. The same is running over 14 pages and not being re-produced here for brevity.

13. We have considered the rival submissions and pleadings made by learned Representatives of both sides orally and in writing and also considered the documents held on record.

14. At first, we re-produce section 253(5) of the Act which prescribes:

“(5) The Appellate Tribunal may admit an appeal or permit the filing of a memorandum of cross-objections after the expiry of the relevant period referred to in sub-section (3) of sub-section (4), if it is satisfied that there was sufficient cause for not presenting it within that period.”

Thus, the section 253(5) of the Act empowers the ITAT to admit an appeal after expiry of prescribed time, subject of course that the ITAT is satisfied that there was “sufficient cause” for not presenting appeal within prescribed time.

15. Further, in the landmark decision of Collector, Land Acquisition (supra) which is followed in many cases, the Hon’ble Supreme Court has given the interpretation of “sufficient cause” and also enunciated guidelines to be followed by courts while dealing condonation in following words:

“.The expression “sufficient cause” employed by the legislature is adequately elastic to enable the courts to apply the law in a meaningful manner which subserves the ends of justice – that being the life – purpose for the existence of the institution of Courts. It is common knowledge that this Court has been making a justifiably liberal approach in matters instituted in this Court. But the message does not appear to have percolated down to all the other Courts in the hierarchy. And such a liberal approach is adopted on principle as it is realized that:-

” 1. Ordinarily a litigant does not stand to benefit by lodging an appeal late.

2. Refusing to condone delay can result in a meritorious matter being thrown out at the very threshold and cause of justice being defeated. As against this when delay is condoned the highest that can happen is that a cause would be decided on merits after hearing the parties.

3. “Every day’s delay must be explained” does not mean that a pedantic approach should be made. Why not every hour’s delay, every second’s delay? The doctrine must be applied in a rational common sense pragmatic manner.

4. When substantial justice and technical considerations are pitted against each other, cause of substantial justice deserves to be preferred for the other side cannot claim to have vested right in injustice being done because of a nondeliberate delay.

5. There is no presumption that delay is occasioned deliberately, or on account of culpable negligence, or on account of mala fides. A litigant does not stand to benefit by resorting to delay. In fact he runs a serious risk.

6. It must be grasped that judiciary is respected not on account of its power to legalize injustice on technical grounds but because it is capable of removing injustice and is expected to do so. “

[emphasis supplied]

16. Further, in recent judgement dated 21.03.2025 of Inder Singh (supra), the Hon’ble Supreme Court has held thus:

“”FACTS:

3. On 14.12.2012, the appellant filed Civil Suit No.17-A/2013 (hereinafter referred to as the ‘suit’) before the learned Second Additional District Judge, Class-1, Ashoknagar, Madhya Pradesh (hereinafter referred to as the Trial Court’) for declaration of title, possession and permanent injunction in respect of Land Survey No.8/1 having an area of 1.060 hectare (hereinafter referred to as the ‘suit property’) situated in Village Mohrirai, Tehsil and District Ashoknagar, contending that an order dated 30.08.1977 was passed in his favour, wherein he was allotted the suit property. Thereafter, by mistake, in place of the appellant’s name i.e., Inder Singh, Ishwar Singh’s name was wrongly recorded in the revenue records. Such mistake was rectified on an application filed by the appellant before the Additional Collector, Gwalior by order dated 24.08.1978. Pursuant thereto, the appellant obtained a loan from a bank for digging a well in the suit property. It is further averred in the suit that the respondent had declared the land in question to be ‘Government Land’, without any prior notice to the appellant.

4. The respondent-State countered the pleadings of the appellant before the Trial Court. The State contended that the entire area admeasuring 5.696 hectares of Land Survey No.1 was government land from the very beginning and the aforesaid land has been recorded as graze land,, out of which,, by order dated 14.09.2006 in Case No.15A6A/05-06 of the Tehsildar Ashoknagar, an area of 2.090 hectares land was reserved for the Youth Welfare Department and the remaining area of 3.606 hectares land for the Collectorate. It was denied that the appellant was ever in possession of the land.

5. The Trial Court dismissed the suit on 16.08.2013, following which the appellant filed Civil Appeal No.32A of 2015 before the Second Additional District Judge, Ashoknagar (hereinafter referred to as the ‘First Appellate Court’), which was allowed by order dated 01.10.2015, overruling the Trial Court’s judgment dated 16.08.2013. The First Appellate Court declared the appellant as the landlord of the suit property.

6. The respondent filed a Review Petition viz. Case No.92 of 2018 before the First Appellate Court, which was dismissed on the ground of delay on 30.09.2019, as the delay in filing the Review Petition was not explained with any sufficient cause from the respondent’s side. Aggrieved by the said order, the respondent, in August, 2020, filed the Second Appeal bearing No.1253 of 2020 along with I.A. No.2022/2020, seeking condonation of delay in filing the Second Appeal, in the High Court. The High Court by Impugned Order condoned the delay and ordered for listing the Second Appeal for hearing on admission as well as application for stay.

SUBMISSIONS BY THE APPELLANT:

7. Learned counsel for the appellant submitted that the High Court had failed to deal with how ‘sufficient cause’ had been shown by the respondent for condoning the delay, more so when the respondent’s Review Petition before the First Appellate Court was also dismissed on the ground of delay as they did not provide any justification for filing the review after a delay of over two years. He contended that it is settled law that ‘sufficient cause’ means that the party should not have acted in a negligent manner or failed to exercise due diligence. Therefore, the appellant’s argument that the cause of delay was due to COVID-19 cannot be accepted, as the respondent failed to remain vigilant, since the cause of action arose much before the pandemic hit.

8. With regard to the Impugned Order referring to the judgment in Sheo Raj Singh v Union of India, (2023) 10 SCC 531, where it has been observed that Courts must take a liberal approach regarding delays in appeals filed by the State, the learned counsel for the appellant drew the Court’s attention to Paragraphs no. 17 and 22 of State of Uttar Pradesh v Satish Chand Shivhare And Brothers, 2022 SCC On Line SC 2151, wherein it was held:

’17. The explanation as given in the affidavit in support of the application for condonation of delay filed by the Petitioners in the High Court does not make out sufficient cause for condonation of the inordinate delay of 337 days in filing the appeal under Section 37 of the Arbitration and Conciliation Act. The law of limitation binds everybody including the Government. The usual explanation of red tapism, pushing of files and the rigmarole of procedures cannot be accepted as sufficient cause. The Government Departments are under an obligation to exercise due diligence to ensure that their right to initiate legal proceedings is not extinguished by operation of the law of limitation. A different yardstick for condonation of delay cannot be laid down because the government is involved.

xxx

22. When consideration of an appeal on merits is pitted against the rejection of a meritorious claim on the technical ground of the bar of limitation, the Courts lean towards consideration on merits by adopting a liberal approach towards ‘sufficient cause’ to condone the delay. The Court considering an application under Section 5 of the Limitation Act may also look into the prima facie merits of an appeal. However, in this case, the CIVIL APPEAL NO. OF 2025 Petitioners failed to make out a strong prima facie case for appeal. Furthermore, a liberal approach, may adopted when some plausible cause for delay is shown. Liberal approach does not mean that an appeal should be allowed even if the cause for delay shown is glimsy. The Court should not waive limitation for all practical purposes by condoning inordinate delay caused by a tardy lackadaisical negligent manner of functioning. ‘

9. Learned counsel for the appellant further relied on the judgment in Pathapati Subba Reddy v Special Deputy Collector, 2024 SCC OnLine SC 513, wherein Paragraph no.26(v) states:

‘Courts are empowered to exercise discretion to condone the delay if sufficient cause had been explained, but that exercise of power is discretionary in nature and may not be exercised even if sufficient cause is established for various factors such as, where there is inordinate delay, negligence and want of due diligence. ‘ Hence, it was contended that this Court should not waive limitation, for all practical purposes, by condoning delay caused by the lackadaisical negligent manner of functioning of the respondent. It was urged that the appeal ought to be allowed and the Impugned Order be set aside.

SUBMISSIONS BY THE RESPONDENT-STATE:

10. Learned counsel for the respondent submitted that out of the delay of 1537 days in filing the Second Appeal, around three years was consumed in filing the Review Petition before the First Appellate Court and after its eventual dismissal on 30.09.2019, by the time the filing process could begin for the Second Appeal, the COVID-19 pandemic arose and it could only get filed in August, 2020. Therefore, the delay caused in filing the Second Appeal was unintentional, much less due to any deliberate laches, and was well-explained by the State before the High Court. It was contended that hence, rightly the delay caused in filing of the Second Appeal was condoned. The respondent further submitted that since the suit property was important and valuable government land, this Court should sustain the Impugned Order as it would entail substantial justice being done to both parties by leading to the eventual disposal of the matter on merits. Reliance was placed on the case of State of Bihar v Kameshwar Prasad Singh, (2000) 9 SCC 94.

11. It was further submitted by the learned counsel for the respondent that the interpretation of the words ‘sufficient cause’ should be such that it is construed liberally. By referring to the decision in State of West Bengal v Administrator, Howrah Municipality, (1972) 1 SCC 366, the respondent contended that a liberal interpretation should specially be taken in the present case as the State has not been negligent in pursuing the remedies available to it under law. Moreoever, the submission was that COVID-19 not being an extraneous circumstance, the State should not be punished for the delay in filing the Second Appeal.

12. With regard to the facts of the case, the respondent points out that the Trial Court had initially dismissed the suit, inter alia, on the grounds that he did not place any documentary evidence reflecting his title and there were also instances of fraud played by the appellant as he had exchanged certain vital documents. It was urged that this was the reason why it was all the more important for the underlying matter to be heard on merits by the High Court. It was canvassed that the appeal should be dismissed and the Impugned Order be upheld.

ANALYSIS, REASONING & CONCLUSION:

13. In the present case, the contentions of the appellant, on first blush appears to be attractive, in as much as the State cannot be given any undue indulgence as compared to an ordinary litigant, especially in matters of limitation. There is no doubt that all parties, whether or not State under Article 123 of the Constitution, are required to act with due diligence and promptitude.

14. There can be no quarrel on the settled principle of law that delay cannot be condoned without sufficient cause, but a major aspect which has to be kept in mind is that, if in a particular case, the merits have to be examined, it should not be scuttled merely on the basis of limitation.

15. In the present case, the filing of the Review Petition before the First Appellate Court was with a delay of two years and four months and the Second Appeal before the High Court was delayed by about a year from the date of the dismissal of the Review Petition i.e., 30.09.2019. Pausing for a moment, it is necessary to indicate that in the present case, the dispute over title of a land is not between private parties, but rather between the private party and the State. Moreover, when the land in question was taken possession of by the State and allotted for public purpose to the Youth Welfare Department and the Collectorate and has continued in the possession of the State, the claim of the State that it is government land cannot be summarily discarded. We find, upon a perusal of the record, that the appellant had, in fact, filed an execution case for taking over possession of the land, which would demonstrate clearly the admitted position that he was not in possession thereof. Thus, the matter would., in our considered view, require adjudication on its own merits due to various reasons, inter alia, the fact that a new district has been formed after the initial claim of the appellant of being allotted the land in the years 1975-1976/1977-1978. Therefore, the delay of 1537 days reckoned from 01.10.2015 i.e. when the First Appellate Court decreed the suit, includes two years and four months delay in filing a Review Petition (which was itself dismissed on the ground of delay by the First Appellate Court) and of about a year thereafter for filing the Second Appeal before the High Court, in the peculiar facts and circumstances of the case, which., at the cost of repetition relate to land claimed by the State as government land and in its possession, persuade us to not interfere with the Impugned Order. Relevantly, initially the suit was dismissed by the Trial Court, which decision was reversed by the First Appellate Court.

16. The Court in Ramchandra Shankar Deodhar v State of Maharashtra, (1974) 1 SCC 317 held

’10..There was a delay of more than ten or twelve years in filing the petition since the accrual of the cause of complaint, and this delay, contended the respondents, was sufficient to disentitle the petitioners to any relief in a petition under Article 32 of the Constitution. We do not think this contention should prevail with us. In the first place, it must be remembered that the rule which says that the Court may not inquire into belated and stale claims is not a rule of law, but a rule of practice based on sound and proper exercise of discretion, and there is no inviolable rule that whenever there is delay, the Court must necessarily refuse to entertain the petition. Each case must depend on its own facts. The question, as pointed out by Hidayatullah, C.J., in Tilokchand Motichand v. H.B. Munshi [(1969) 1 SCC 110, 116 :(1969) 2 SCR 824] “is one of discretion for this Court to follow from case to case. There is no lower limit and there is no upper limit. It will all depend on what the breach of the fundamental right and the remedy claimed are and how the delay arose”. ‘ (emphasis supplied)

17. No doubt, Ramchandra Shankar Deodhar (supra) relates to a writ petition, but the statement of law laid down is clear. Sheo Raj Singh (supra) has also considered the impersonal nature of the functioning of the State, taking note of what was observed in State of Manipur v Kotin Lamkang, (2019) 10 SCC 408. In A B Govardhan v P Ragothaman, (2024) 10 SCC 613, the Court considered as under:

’37. In Collector (LA) v. Katiji [Collector (LA) v. Katiji, (1987) 2 SCC 107], the Court noted that it had been adopting a justifiably liberal approach in condoning delay and that “justice on merits” is to be preferred as against what “scuttles a decision on merits”. Albeit, while reversing an order of the High Court therein condoning delay, principles to guide the consideration of an application for condonation of delay were culled out in Esha Bhattacharjee v. Raghunathpur Nafar Academy [Esha Bhattacharjee v. Raghunathpur Nafar Academy, (2013) 12 SCC 649: (2014) 1 SCC (Civ) 713: (2014) 4 SCC (Cri) 450: (2014) 2 SCC (L&S) 595]. One of the factors taken note of therein was that substantial justice is paramount [Para 21.3 of Esha Bhattacharjee [Esha Bhattacharjee v. Raghunathpur Nafar Academy, (2013) 12 SCC 649: (2014) 1 SCC (Civ) 713: (2014) 4 SCC (Cri) 450: (2014) 2 SCC (L&S) 595]].

38. In N.L. Abhyankar v. Union of India [N.L. Abhyankar v. Union of India, 1994 SCC OnLine Bom 574: (1995) 1 Mah LJ 503], a Division Bench of the Bombay High Court at Nagpur considered, though in the context of delay vis-a-vis Article 226 of the Constitution, the decision in Dehri Rohtas Light Railway Co. Ltd. v. District Board, Bhojpur [Dehri Rohtas Light Railway Co. Ltd. v. District Board, Bhojpur, (1992) 2 SCC 598], and held that: (N.L. Abhyankar case [N.L. Abhyankar v. Union of India, 1994 SCC OnLine Bom 574: (1995) 1 Mah LJ 503], SCC OnLine Bom para 22)

“22.. The real test for sound exercise of discretion by the High Court in this regard is not the physical running of time as such, but the test is whether by reason of delay there is such negligence on the part of the petitioner, so as to infer that he has given up his claim or whether before the petitioner has moved the writ court, the rights of the third parties have come into being which should not be allowed to be disturbed unless there is reasonable explanation for the delay. ” (emphasis supplied)

39. The Bombay High Court’s eloquent statement of the correct position in law in N.L. Abhyankar case [N.L. Abhyankar v. Union of India, 1994 SCC OnLine Bom 574: (1995) 1 Mah LJ 503] found approval in Municipal Council, Ahmednagar v. Shah Hyder Beig [Municipal Council, Ahmednagar v. Shah Hyder Beig, (2000) 2 SCC 48] and Mool Chandra v. Union of India [Mool Chandra v. Union of India, (2025) 1 SCC 625: 2024 SCC OnLine SC 1878].

40. In the wake of the authorities abovementioned, taking a liberal approach subserving the cause of justice, we condone the delay and allow IA No. 16203 of 2019, subject to payment of costs of Rs 20,000 (Rupees twenty thousand) by the appellant to the respondent. ‘

(emphasis supplied)

18. Considering the above pronouncements and on an overall circumspection, we are of the opinion that the Second Appeal deserves to be heard, contested and decided on merits. However, a note of caution is sounded to the respondent to exhibit promptitude in like matters henceforth and in futuro, failing which the Court may not be as liberal.

19. Accordingly, the present appeal stands dismissed. The Impugned Order is upheld with the imposition of costs infra.

20. No order as to costs. I.A.s No.62432/2024 4 and 62433/20245 are allowed.

21. To offset, to some extent, the hardship of the appellant in pursuing his legal remedies, we deem it appropriate that costs of Rs.50,000/- (Rupees Fifty Thousand) be paid by the respondent to the appellant, subject to which the delay in filing the Second Appeal shall be treated as condoned. Let such payment be made within one month from today. Failure to do so shall entail peremptory dismissal of the Second Appeal.

22. Further, if the payment is made within the timeline stipulated above, the High Court is requested to take up the Second Appeal on priority and endeavour to dispose it of expeditiously. “

17. Further, in a very recent judgement dated 01.04.2025 in the case titled Shri Neel Kumar Ajmera alias Nilesh Ajmera v. Pr. Commissioner of Income-tax [IT Appeal No. 924 (Ind) of 2018, dated 1-4-2025], the Hon’ble Jurisdictional High Court of Madhya Pradesh has taken cognizance of Inder Singh (supra) and condoned the delay of 1797 days, holding as under:

“8. Heard the learned counsel for the parties.

9. The Supreme Court in the case of Inder Singh Vs. State of Madhya Pradesh reported in 2025 INSC 382 has held as under:

“There can be no quarrel on the settled principle of law that delay cannot be condoned without sufficient cause, but a major aspect which has to be kept in mind is that, if in a particular case, the merits have to be examined, it should not be scuttled merely on the basis of limitation.”

10. Similarly, the Supreme Court in the case of Mool Chandra (supra), has held as under:

“It is not the length of delay that would be required to be considered while examining the plea for condonation of delay, it is the cause for delay which has been propounded will have to be examined. If the cause for delay would fall within the four corners of “sufficient cause”, irrespective of the length of delay same deserves to be condoned. However, if the cause shown is insufficient, irrespective of the period of delay, same would not be condoned.”

11. In the aforesaid case, the Supreme Court has further held as under:

“if negligence can be attributed to the appellant, then necessarily the delay which has not been condoned by the Tribunal and affirmed by the High Court deserves to be accepted. However, if no fault can be laid at the doors of the appellant and cause shown is sufficient then we are of the considered view that both the Tribunal and the High Court were in error in not adopting a liberal approach or justice oriented approach to condone the delay.”

12. In view of the aforesaid pronunciation of law as well as after going through the reasons assigned for delay in filing the appeal, this Court is of the considered opinion that although a delay cannot be condoned without sufficient cause but the merits of the case cannot be discarded solely on the technical grounds of limitation. A liberal approach should be taken in condoning delays when the limitation ground undermines the merits of the case and obstructs substantial justice.

13. Hence, this Court finds that the appellant has been able to put forth “sufficient cause” for the delay in filing the appeal before ITAT.

14. Accordingly, the order dated 23.08.2024 passed by the Income Tax Appellate Tribunal, Indore Bench, Indore in ITA No.234/IND/2024 is hereby set aside.

15. The delay in filing an appeal before the ITAT is hereby condoned.

16. The matter is remanded back to Income Tax Appellate Tribunal, Indore Bench, Indore and it is directed that the appeal shall be decided afresh in accordance with law on merits after affording reasonable opportunity of hearing to both the parties.

17. With aforesaid direction, the present ITA is hereby allowed.”

18. Now, we examine the facts of present case on the touchstone of above provisions/decisions:

| (i) |

|

The present appeal has been filed on 22.08.2024 against impugned order dated 21.06.2023 and accordingly there is a delay of 368 days. The assessee admits such delay but at the same time requests for condonation of delay on the premise of existence of “sufficient cause”. To explain such existence, the assessee has filed two affidavits of Shri Abhishek Upadhyay/Secretary. In para 2 of 1st affidavit, Shri Abhishek Upadhyay/Secretary of assessee-society has made a solemnized averment that the impugned order remained with him, however the averment does not explain further as to why the same remained with him. In para 3 of 2nd affidavit, Shri Abhishek Upadhyay/Secretary has given a detailed explanation that he got an impression that the appeal was allowed and no further action was needed. We find that Shri Abhishek Upadhyay/Secretary has given solemnized averment of the understanding (may be a misunderstanding) gained by him from order of CIT(A). This personal understanding and consequently keeping impugned order with himself, is something which is known to Shri Abhishek Upadhyay/ Secretary only and there is hardly any evidence to controvert or disbelieve same. Shri Abhishek Upadhyay/Secretary has made a solemnised averment which corroborates with the fact that the CIT(A) has allowed assessee’s appeal (though partly). Notably, the CIT(A) has not dismissed assessee’s appeal. Had it been a case of dismissal of assessee’s appeal by CIT(A) and the assessee would have filed a belated appeal claiming a bad impression of appeal having been allowed by CIT(A), certainly it would been a case of false, unacceptable explanation. But the present case is not so. In present case, the CIT(A) although the CIT(A) has mentioned success of assessee with reference to Ground No. 1 and allowed appeal partly but the fact remains that the CIT(A) has allowed assessee’s appeal. Therefore, it is quite possible that Shri Abhishek Upadhyay/Secretary got an understanding (or mis-understanding) that appeal had been allowed sufficiently and no further action was needed. Since Shri Abhishek Upadhyay/Secretary is admitting this fact and attributing the delay in filing of appeal to himself/his understanding, we do not have basis or reason to dispel or disbelieve the same. In any case, the assessee-society is an artificial person, unlike an individual who is a natural person, and its affairs have to managed through natural persons like the Chairman, Secretary, etc. Therefore, the assessee should not be allowed to suffer because of any mis-understanding generated by its Secretary in legal matters. Further, the explanation given by Shri Abhishek Upadhyay/ Secretary that when the notice u/s 270A was received on 01.08.2024, the matter was discussed with counsel who suggested for filing of appeal and immediately the present appeal was filed on 22.08.2024 is a credible explanation. The assessee has also filed penalty-notice dated 01.08.2024 for perusal. The chronology of facts is well-explained by Shri Abhishek Upadhyay/Secretary. In any case, even if it is said that the understanding of Shri Abhishek Upadhyay/ Secretary was not correct but even in that scenario, it would constitute a “sufficient cause” in so far as the assessee-society is concerned. |

| (ii) |

|

The assessee has attended the notices sent by lower-authorities and made a full participation in the proceedings of scrutiny-assessment set up by AO and the proceedings of first appellate conducted by CIT(A). Thus, the assessee has a compliant attitude and there is no signal of non-compliant approach or negligence on the part of assessee. |

| (iii) |

|

There is nothing to show that the assessee had an ulterior motive or an attempt to save limitation in an underhand way. During scrutinyassessment before AO, the assessee filed a copy of Order dated 03.02.2021 issued by CIT(Exemption), Bhopal granting registration u/s 12AA to assessee and thereby giving entitlement for exemption u/s 11/12. Further, the assessee was claiming the statutory relief granted by Proviso to section 12A(2). The AO, however, denied such benefit to assessee. Aggrieved by AO’s action, the assessee went in appeal before CIT(A) and persued its claim. The claim of assessee, as would be seen from our adjudication in subsequent paras, is meritorious and allowable. The CIT(A) also did not allow the claim of assessee but granted alternative relief and allowed appeal partly. Thus, the assessee is contending for its legitimate claim in terms of provision of law. The Ld. DR, in Para No. 2.00 of Written-Synopsis re-produced above, has mentioned “. the assessee applied for registration under section 12AA of the Income-tax Act with the ulterior motive of obtaining retroactive benefit under section 12A.”. This submission of Ld. DR does not appeal to us since the documents held on record show that the assessee filed a valid application to CIT(Exemption), Bhopal on 24.01.2020 for grant of registration u/s 12AA and the CIT(Exemption), Bhopal granted registration vide Order dated 03.02.2021 in accordance with law. Consequently, the assessee also became entitled to the benefit of Proviso to section 12A(2) which assessee pressed before AO. In such a situation, how can it be said that the assessee had an ulterior motive? |

19. We agree that there are judicial precedents on both sides. The Hon’ble Courts have condoned the delay in numerous cases and also declined to condone delay in other cases. The decision, however, depends upon facts of each case. In present case, the facts noted above satisfy the criterion followed by Hon’ble Courts in granting condonation. It is also noteworthy that the assessee is engaged charitable activity of imparting education to students. The assessee’s attempt is to claim exemption u/s 11/12 of the Act as statutorily given by Proviso to section 12A(2). Therefore, the assessee should not be deprived from its legal claim. The Hon’ble Supreme Court has, in Mst. Katiji (supra), held that whenever substantial justice and technical considerations are opposed to each other, the cause of substantial justice must be preferred by adopting a justice-oriented approach. The same tune has again been followed by Hon’ble Supreme in recent decision dated 21.03.2025 of Inder Singh (supra) and by Hon’ble Jurisdictional High Court of Madhya Pradesh in recent decision dated 01.04.2025 of Shri Neel Kumar Ajmera (supra). Respectfully following the same and having regard to the facts of case as discussed above, we are inclined to condone the delay in present appeal and we do so.

Merit of case:

20. By means of grounds raised in Form No. 36 as re-produced in the beginning, the assessee’s grievance is such that the CIT(A) has erred in confirming the action of AO in denying benefit of exemption u/s 11/12 to assessee. We have already noted the facts at length in earlier Para 2 of this order and the repetition is not required. Suffice it to say that in the return of income filed to Income-tax Department, the assessee wrongly claimed exemption u/s 10(23C)(iiiad) of the Act. However, during pendency of the assessment-proceeding, the assessee was granted registration u/s 12AA by CIT(Exemption), Bhopal vide Order dated 03.02.2021 and consequently the assessee, vide letters dated 08.02.2021 & 01.03.2021, made a claim of exemption u/s 11 & 12 on the basis of Proviso to section 12A(2). The assessee submitted to AO that all requirements of Proviso to section 12A(2) were satisfied, namely (i) the registration u/s 12AA had been granted to assessee, (ii) the assessment-proceeding of AY 2018-19 (with which we are concerned) were pending on the date of registration, and (iii) the objects and activities of assessee remained same. The assessee also filed a declaration to AO for the point no. (iii); the said declaration has already been re-produced in earlier Para of this order.

21. Ld. AR referred the assessment-order and order of first-appeal passed by AO and CIT(A) [as re-produced by us in earlier Paras 2(iv) & 2(vi) of this order] and demonstrated that there are three reasons for denial of exemption to assessee out of which first two reasons have been assigned by AO and the last reason has been added by CIT(A). These three reasons are:

| (i) |

|

The assessee has not filed revised return claiming exemption u/s 11/12. Ld. AR pointed out that although the AO has not specifically mentioned but this adverse observation may be in tune with Goetze India Ltd. v. CIT ITR 323 (SC) wherein the Hon’ble Apex Court has held that a fresh claim can be made only by filing a revised return. |

| (ii) |

|

The assessee has not filed Form No. 10B by due date for filing of return. |

| (iii) |

|

The 2nd proviso to section 12A(2) relied by assessee became effective from 01.04.2021 and the same was not applicable for AY 2018-19 under consideration. |

22. So far as the first two reasons assigned by AO are concerned, Ld. AR submitted that there are at least three orders passed by ITAT, Indore bench wherein those reasons have been rejected. These three cases are: (a) Barkatullah Vishwavidyalaya (supra), Shri Neel Kumar Ajmera alias Nilesh Ajmera (supra); (b) Madhya Pradesh Council for Vocational Education & Training v. CIT(E) [IT Appeal Nos. 176,177 (Ind) of 2024, dated 26-10-2023]; (c) Akshay Academy v. ITO, NFAC (Indore – Trib.)/ITA No. 199/Ind/2024. In Paper-Book, Ld. AR has filed a copy of order of ITAT in Barkatullah Vishwavidyalaya (supra) and made a particular reference to following paras of order:

“8. Ld. AR, thereafter, made an alternative claim that the assessee has also received registration u/s 12A(1)(aa) read with section 12AA from AY 2019-20 onwards vide Order No. ITBA/EXM/S/12AA/2019-20/ 1016373495(1) dated 17.06.2019 issued by CIT(Exemption), Bhopal. Ld. AR invited our attention to the copy of registration-order. Ld. AR then referred to the section 12A(2) which reads as under:

“12A(2) Where an application has been made on or after the 1st day of June, 2007, the provisions of sections 11 and 12 shall apply in relation to the income of such trust or institution from the assessment-year immediately following the financial year in which such application is made.

Provided that where registration has been granted to the trust or institution under section 12AA, then, the provisions of sections 11 and 12 shall apply in respect of any income derived from property held under trust of any assessment year preceding the aforesaid assessment year, for which assessment proceedings are pending before the Assessing Officer as on the date of such registration and the object and activities of the trust or institution remain the same for such preceding assessment year:”

Analyzing the above Proviso, the Ld. AR submitted that once the registration has been granted u/s 12AA, the exemption u/s 11 and 12 shall apply in respect of any preceding assessment-year for which the assessmentproceeding is pending before the AO on the date of registration. Ld. AR submitted that in the present case, the assessee has been granted registration u/s 12AA on 17.06.2019 for assessment-year 2019-20 onwards. Ld. AR submitted that the present appeal of assessee pertaining to assessment-year 2014-15 was pending on 17.06.2019 before this Bench,. Hence the benefit of the Proviso is available to the assessee. Ld. AR gainfully referred the decision of ITAT, Ahmedabad in Shri Bhanushali Mitra Mandal Trust v. ITO, ITA No. 2515/Ahd/2015 dated 22.02.2016 where it was held thus:

“7. 1 To examine the first issue, necessarily I have to analyze the relevant provision, namely, the amendment to Section 12A by Finance Act, 2014 w.e.f. 01.10.2014 by way of insertion of provisos to Section 12A(2) of the Act which is reproduced below for ready reference:

“[(2) Where an application has been made on or after the 1st day of June, 2007, the provisions of sections 11 and 12 shall apply in relation to the income of such trust or institution from the assessment year immediately following the financial year in which such application is made:

Provided that where registration has been granted to the trust or institution under section 12AA, then., the provisions of sections 11 and 12 shall apply in respect of any income derived from property held under trust of any assessment year preceding the aforesaid assessment year, for which assessment proceedings are pending before the Assessing Officer as on the date of such registration and the objects and activities of such trust or institution remain the same for such preceding assessment year:

Provided further that no action under section 147 shall be taken by the Assessing Officer in case of such trust or institution for any assessment year preceding the aforesaid assessment year only for non-registration of such trust or institution for the said assessment year:

Provided also that provisions contained in the first and second proviso shall not apply in case of any trust or institution which was refused registration or the registration granted to it was cancelled at any time under section 12AA.]”

7.2 It is also relevant to reproduce the explanatory notes to the provisions of Finance (No.2) Act, 2014 as given in CBDT Circular No.01/2015 dated 21.01.2015 in reference F.No.142/13/2014-TPL, which read as follows:

“Para 8.2

Non-application of registration for the period prior to the year of registration caused genuine hardship to charitable organizations. Due to absence of registration, tax liability is fastened even though they may otherwise be eligible for exemption and fulfill other substantive conditions. However, the power of condonation of delay in seeking registration was not available.”

This clearly goes to prove that the first proviso to section 12A(2) was brought in the statute only as a retrospective effect with a view not to affect genuine charitable trusts and societies carrying on genuine charitable objects in the earlier years and substantive conditions stipulated in section 11 to 13 have been duly fulfilled by the said trust. The benefit of retrospective application alone could be the intention of the legislature and this point is further strengthened by the Explanatory Notes to Finance (No.2) Act, 2014 issued by the Central Board of Direct Taxes vide its Circular No. 01/2015 dated 21.1.2015. Apparently the statute provides that registration once granted in subsequent year, the benefit of the same has to be applied in the earlier assessment years for which assessment proceedings are pending before the ld. A.O., unless the registration granted earlier is cancelled or refused for specific reasons. The statute also goes on to provide that no action u/s147 could be taken by the AO merely for non-registration of trust for earlier years.

7.3 In the instant case, it is not in dispute that registration was granted w.e.f. 17.12.2013 by the order ofCIT(A) dated 08.05.2014. It is also not in dispute that objects and activities of the assessee trust are charitable in nature during the relevant financial year. When Section 12A of the Act was amended by introducing new provisos to subsection (2) of Section 12A by Finance Act, 2014 with effect from 01.10.2014, the assessment orders Asst. Year 2011-12 passed by the assessing officer in respect of the present assessee were pending in appeal before the first appellate authority. During such pendency, the assessee was granted registration u/s. 12AA of the Act on 17.12.2013 w.e.f. the assessment year 2013-14. The appeal is the continuation of the original proceedings and that the power of the Commissioner of Income-tax was co-terminus with that of the assessing officer were two well established principles of law. In view of the above and going by the principle of purposive interpretation of statues, an assessment proceeding which is pending in appeal before the appellate authority should be deemed to be ‘assessment proceedings pending before the assessing officer’ within the meaning of that term as envisaged under the proviso. It follows therefrom that the assessee which obtained registration u/s 12AA of the Act during the pendency of appeal was entitled for exemption claimed u/s 11 of the Act.

7.4 The explanatory Memorandum to Finance (No.2) Bill, 2014, which sought to amend section 12A explains the objects and reasons for making such amendments. The explanation makes it clear that it was in order to provide relief to such trusts in respect of which,, due to absence of registration u/s 12AA tax liability got attached though otherwise they were eligible for exemption by fulfilling other substantive conditions that the amendment was brought in. That being so, denying such benefit to a trust like the assessee who had obtained registration u/s 12AA during the pendency of the appeals filed against the orders of the assessing authority, by narrowly interpreting the term., ‘pending before the assessing officer’ so as to exclude its pendency before the appellate authority, will be doing violence to the provisions of the Statute and, as such, liable to be interfered with,. Moreover, under the Scheme of the Act, sections 11 and 12 are substantive provisions which provide for exemptions to a religious or charitable trust. Sections 12A and 12AA detail the procedural requirements for making an application to claim exemptions under sections 11 and 12 by the assessee and the grant or rejection of such application by the commissioner. Thus, in my view, sections 12A and 12AA are only procedural in nature. Hence, it is not the registration u/s 12AA by itself that offers immunity from taxation. A receipt whether it is revenue or capital in nature is to be decided at the assessment stage. Being procedural in nature, in my view, liberal interpretation will give effect to the intention of the amendment, thereby removing the hardship in genuine cases like the present assessee under consideration.

7.5 I am also supported by the order of Kolkata Bench of ITAT in case of Sree Sree Ramkrishna Samity v. DCIT (ITA No. 1680/2012, order dated 09.10.2015) where it was held that amendment to Section 12A w.e.f. 01.10.2014 is retrospective. The relevant funding of the Hon’ble Kolkata Bench in case of Sree Sree Ramkrishna Samity v. DCIT (supra) read as follows:

“6.10. We hold that it is an established position in law that a proviso which is inserted to remedy unintended consequences and to make the provision workable, a proviso which supplies an obvious omission in the section and is required to be read into the section to give the section a reasonable interpretation, requires to be treated as retrospective in operation, so that a reasonable interpretation can be given to the section as a whole and accordingly the said insertion of first proviso to section 12A(2) of the Act with effect from 1.10.2014 should be read as retrospective in operation with effect from the date when the condition of eligibility for exemption under section 11 & 12 as mentioned in section 12A provided for registration u/s.12AA as a pre-condition for applicability of section 12A.”

Ld. AR argued that the assessee is entitled to the benefit of this decision and therefore the assessment-year 2014-15 pending before this Bench in appeal must be construed as an assessment-year for which proceeding is pending before assessing officer. For the sake of completeness, Ld. AR also submitted that the assessee is a university established under the legislation of Madhya Pradesh Govt. and since beginning it is engaged in the very same objects and activities, therefore the objects and activities remained same. With these submissions, the Ld. AR argued that the assessee fully satisfies the requirement of aforesaid Proviso to section 12A(2) and therefore perfectly eligible for exemption u/s 11 / 12. Hence the Ld. AR requested to direct the Ld. AO to allow exemption u/s 11 / 12 to the assessee, if for any reason the exemption u/s 10(23C)(iiiab) is not allowed.

XXX

11. Now we proceed to examine the alternative claim of exemption u/s 11/12 demanded by the assessee. On perusal of the Proviso to section 12A(2) and the decision of Hon’ble Co-ordinate Bench of ITAT, Ahmedabad in Shri Bhanushali Mitra Mandal Trust (supra), we agree to the proposition that the assessee is entitled to the benefit of exemption u/s 11/12 for the assessment-year 2014-15 under consideration as the requirements prescribed in the Proviso stand satisfied, viz. (i) the revenue had already granted registration u/s 12AA from assessment-year 2019-20, (ii) the assessment-year under consideration is 2014-15 which falls within “any preceding assessment year”, and (iii) the objects and activities of the assessee remain same. We also find that the Ld. DR did not make any objection to this claim argued by Ld. AR. But however we have to ascertain one important aspect i. e. can we entertain this new claim made by assessee for the first time before us? In this respect we find that the Hon’ble Supreme Court has held in Goetze India Ltd. v. CIT ITR 323 (SC) that a fresh claim can be made only by filing a revised return. But various courts have already analysed the impact of this decision and vehemently held that afresh claim before appellate authorities is not barred. It is constantly held in several decisions that a legal claim can be made by the assessee before appellate authorities even if the same was not claimed during assessment-proceedings. We also observe that the provisions of section 11/12 grant exemption to the assessee and such exemption, if not allowed, would result in illegal collection of tax from the assessee, which is never an objective of the Income-tax Act, 1961. In view of this position of law, we do not find any difficulty in accepting the alternative claim of assessee to allow exemption u/s 11 / 12. However, the claim of exemption u/s 11 / 12 involves a different type of working based on application and accumulation of income. Therefore, we feel that it would be more appropriate to refer this matter back to Ld. AO who shall give an opportunity to the assessee to provide the necessary information for computation of exemption u/s 11 / 12. Based on such information, the Ld. AO shall allow the exemption as admissible u/s 11 / 12 to the assessee.

12. In the result, this appeal of assessee is allowed for statistical purpose. “

23. Further, Ld. AR has also filed a copy of order in Akshay Academy (supra) in Paper-Book and referred following paras of same:

“2. The assesse trust has filed its return of income for the year under consideration on 18.03.2019 declaring total income at nil after claiming exemption u/s 10(23C)(iiiad) of the Act. In the scrutiny assessment the AO noted that the assesse has declared gross receipt at Rs. 7,56,19,050/- which is more than the prescribed monetary limit for claiming exemption u/s 10(23C)(iiiad) of the Act and therefore, the said claim of the assessee cannot be allowed. During the assessment proceeding the assesse’s vi.de letter dated 30.01.2021 explained that the claim of exemption u/s 10(23C)(iiiad) of the Act was wrongly made however, assessee was registered u/s 12AA and is entitled to exemption u/s 11 & 12 of the Act and accordingly requested the AO to allow the claim of exemption u/s 11& 12 of the Act. The AO denied the claim of exemption u/s 11 & 12 of the Act on the ground that the assesse has not filed revised return of income for making a new claim which is not raised in the original return of income by placing the reliance on the judgment of Hon’ble Supreme Court in case of

Goetze (India) Limited v.

CIT 284 ITR 323. The AO further observed that the assesse even not filed the audit report inform 10B within stipulated time. Aggrieved by the order of the AO, the assessee filed appeal before the CIT(A) but could not succeed.

3. Before the Tribunal Ld. AR of the assesse has submitted that in the return of income the assesse has wrongly claimed exemption u/s 10(23C)(iiiad) of the Act however, during the pendency of the assessment proceedings the assessee was granted registration u/s 12AA of the Act vide letter dated 28.09.2019 and consequently the assesse vide letter dated 29.01.2021 made a claim of exemption u/s 11 & 12 of the Act. Ld. AR has referred to the proviso to section 12A(2) of the Act and submitted that the provisions of section 11 & 12 shall apply in respect of the income derived from the property held under the trust of any assessment year preceding the assessment year for which the registration u/s 12A has been granted and the assessment proceeding of the preceding assessment year is pending before the AO as on the date of such registration subject to the conditions that objects and activities of such trust or institution remain the same. Thus, Ld. AR has submitted that when the registration u/s 12A was granted to the assessee during the pending of the assessment year under consideration then the claim of exemption u/s 11 & 12 cannot be denied by the AO on the ground of non-filing of revised return of income. Ld. AR has thus submitted that the assessee reiterated its claim of exemption u/s 11 & 12 before the CIT(A) but it was not accepted even by the CIT(A) which has no embargo for entertaining the claim not made in the return of income. Thus, Ld. AR has submitted that in view of second proviso of 12A(2) of the Act the assesse is entitled for exemption u/s 11 & 12 of the Act. In support of his contention he has relied upon following decisions:

| (i)Barkatullah |

|

Vishwavidyalaya (supra) |

| (ii) |

|

Madhya Pradesh Council for Vocational Education & Training (supra) |