ORDER

Laliet Kumar, Judicial Member. – All the above appeals filed by the Assessee against the separate orders of Ld. CIT, Appeal Addl/JCIT(A) Gwalior each dt. 12/03/2025 for the Assessment Years 2018-19, 2019-20 and 2020-21 respectively.

2. Since the issues involved in all the above appeals are common and were heard together, they are being disposed of by this consolidated order for the sake of convenience and brevity.

3. We shall takean appeal of the Assessee in ITA No. 642/Chd/2025 for the Assessment Year 2018-19 as a lead case for discussion, wherein the assessee has raised the following grounds:

| 1. |

|

That the Ld. Addl./Joint Commissioner of Income Tax (Appeals), Gwalior has erred in dismissing the appeal of the assessee and confirming the addition of Rs.31,01,954/- on account of provident fund/ESI having been deposited late. |

| 2. |

|

That the Ld. Addl./Joint Commissioner of Income Tax (Appeals), has misled himself on the basis of incorrect facts mentioned in the audit report, wherein, the employees contribution as well as employers contribution and the administrative charges have been mentioned in the audit report and whereas the only employees contribution was required to be mentioned in the audit report. |

| 3. |

|

That the addition as confirmed by Addl./Joint Commissioner of Income Tax (Appeals), is on incorrect figures mentioned in the audit report. |

| 4. |

|

That the appellant craves leave to add or amend the grounds of appeal before the appeal is finally heard or disposed off. |

4. Additionally the assessee had also raised the additional ground before us which are to the following effect:-

| 1. |

|

That the adjustment as made by the CPC on account of disallowance of EPF/ESI vide order, dated 22.06.2020 and making the addition of Rs. 31,01,954/- is bad in law and the said adjustment as made by the CPC could not have been made since at that time, the issue was debatable and not an arithmetical error. |

| 2. |

|

That the disallowance of EPF/ESI as made by CPC is bad in law, since at the time, when the disallowance was made, the issue of disallowance of deduction was highly debatable and which was pending before the Hon’ble Supreme Court in the case of ‘Checkmate Services Pvt. Ltd. v. CIT’ and it was only by way oforder,dated 12.10.2022, the judgment of Supreme Court came and, as such, the disallowance/adjustment as made by the CPC on 22.06.2020 could be not made. |

| 3. |

|

That the said view has recently been delivered in a detailed judgement of ‘Hon’ble High Court of Chhattisgarh’ at Bilaspur in the case of ‘Sh.Raj Kumar Bothra v. DCIT, Chhattisgarh’ vide order, dated 08.05.2025 and the facts being identical and, therefore, the disallowance/adjustment as made by the CPC is not in order. |

| 4. |

|

That the said adjustment/disallowance as being made by CPC is beyond the scope of procedure to process the return u/s 143(1)(a), being not an arithmetical error or other procedure as per the guidelines of the department. |

5. The brief facts of the case are that the assessee, engaged in the business of security services, filed his return of income declaring a total revenue of Rs.18,70,090/-. The return was processed under section 143(1) by CPC, Bengaluru, and an adjustment was made under section 143(1)(a)(iv) based on Form 3CD, disallowing Rs. 31,01,954/-towards the delayed deposit of employees’ contribution to PF and ESI. The assessee carried the matter before the CIT(A), who upheld the adjustment and dismissed the appeal.

6. Feeling aggrieved by the order passed by the Ld. CIT(A) the assessee is in appeal before us.

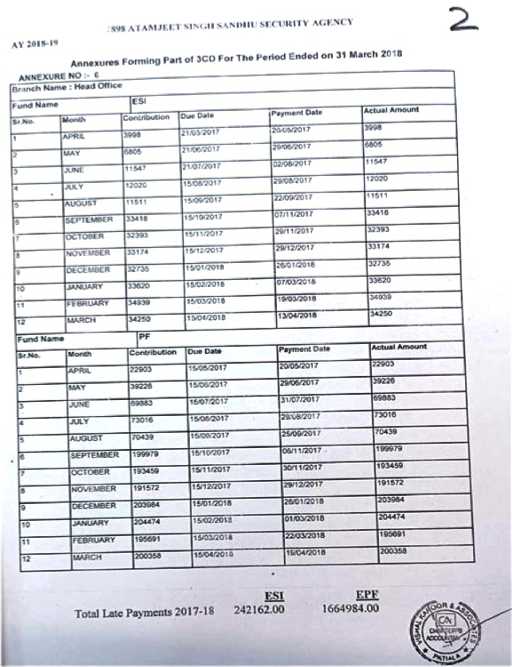

7. During the course of hearing before us, the Ld. AR submitted that the entire adjustment is legally invalid and factually incorrect. He pointed out that the CPC proceeded on the basis of figures mentioned in the audit report without appreciating that the report had erroneously clubbed employees’ contribution with employer’s contribution and administrative charges. It was submitted that under the law, only employees’ contribution falls within the mischief of section 36(1)(va), whereas employer’s contribution is separately governed by section 43B. It was emphasized that the assessee had in fact deposited the employer’s contribution before the due date for filing the return under section 139(1) and therefore no disallowance could be made in respect thereof. The Ld. AR drew our attention to the detailed chart forming part of Annexure 6 of Form 3CD, wherein month-wise details of ESI and PF contributions, due dates, and actual payment dates were furnished. On the basis of this chart, the assessee quantified the actual delayed employees’ contribution at Rs.2,42,162/- in respect of ESI and Rs.16,64,984/- in respect of PF. This position was further confirmed by the certificate dated 22.09.2025 issued by Vishal Kapoor & Associates, Chartered Accountants, who certified the total late payments of employees’ contribution for AY 2018-19 at the aforesaid figures. Thus, according to the assessee, the disallowance sustained by the lower authorities was factually inflated and not based on the correct classification of employer and employee components.

7.1 Without prejudice to the above factual contention, the Ld. AR submitted that even otherwise, the adjustment made under section 143(1)(a)(iv) was wholly unjustified because the issue of allowability of delayed employees’ contribution to PF and ESI was, at the relevant point of time, a debatable one, pending consideration before the Hon’ble Supreme Court. It was argued that the scope of adjustments under section 143(1)(a) is limited to apparent and patent errors. In contrast, in the present case, the issue involved a highly contentious question of law. Reliance was placed upon the decision of the Hon’ble Chhattisgarh High Court in Raj Kumar Bothra v. Dy. CIT 1199/476 ITR 249, wherein it was held that prima facie adjustments under section 143(1)(a) cannot be made on debatable and controversial issues and that such adjustments would travel beyond the limited jurisdiction of CPC. The Ld. AR also strongly relied upon the recent decision of the Delhi Bench of the Tribunal in Rajesh Kumar Garg v. Asstt. CIT [IT Appeal Nos. 970 and 971 (Delhi) of 2025, dated 22-8-2025], wherein the Tribunal, after an elaborate analysis of the provisions of section 143(1)(a), section 36(1)(va), and section 43B, concluded that disallowance of employees’ contribution to PF/ESI on the basis of delayed deposit is not a matter which falls within the limited compass ofprima facie adjustments under section 143(1)(a). The Delhi Bench also recognised the necessity of distinguishing between employees’ and employers’ contributions, and held that both stand on different footing and cannot be mechanically clubbed for the purpose of adjustment.

8. On the other hand, the Ld. Sr. DR placed reliance on the impugned order and submitted that the issue is squarely covered against the assessee by the authoritative pronouncement of the Hon’ble Supreme Court in Checkmate Services (P.) Ltd. v. CIT 19/[2022] 448 ITR 518 (SC)/Civil Appeal No.2833 of 2016, dated 12.10.2022. It was contended that the Apex Court has categorically held that employees’ contribution to PF and ESI, being income under section 2(24)(x), is allowable as deduction only if deposited within the due dates prescribed under the respective welfare legislations. It was further contended that section 43B has no application to employees’ contribution and therefore, once the audit report itself disclosed delay, the CPC was justified in making the adjustment and the CIT(A) was correct in confirming the same.

9. We have carefully considered the rival submissions and examined the material placed on record. It is evident from the audit annexure and the Chartered Accountant’s certificate that a factual dispute exists regarding the actual quantum of delayed employees’ contributions. The figures taken by the CPC and sustained by the CIT(A) appear to have been mechanically lifted from Form 3CD without examining whether those figures represented purely employees’ contribution or also included the employer’s contribution. The assessee has placed on record a duly certified statement showing that the delayed employees’ contribution amounted to Rs. 2,42,162/- towards ESI and Rs. 16,64,984/- towards PF, whereas the balance pertained to the employer’s contribution duly deposited before the due date under section 139(1). In our considered view, this factual aspect goes to the root of the controversy and requires proper verification at the level of the Ld. CIT(A). At the stage it may be relevant to mention that the assessee had filed the original tax report on 12/08/2018, in the said tax audit report the unpaid EPF was mentioned at Rs. 24,56,467/- and Rs. 6,45,486/- was mentioned towards ESI totaling to Rs. 31,01,953/- and thereafter a revised tax audit report was filed by the assessee on 22/09/2019. In the revised tax audit report for the A.Y. 2018-19, on page 57 of the paper book, the assessee has given the details of the payments which were delayed towards the employees’ contribution for ESI and PF, which have been corrected, albeit the same has not been considered by the authorities while passing the order.

9.1 Before us, the assessee had filed the Chart giving the details of the payment due and the date of actual payment which is to the following effect.

9.2 In support of the above the assessee had also filed the certificate from the Chartered Accountant confirming that the ESI amount not paid as per law in time was Rs. 2,42,162/- and EPF was Rs. 16,64,984/-. It was submitted that, as these amounts were specifically required to be disallowed in accordance with the applicable legal provisions, the remaining addition made by the CPC and confirmed by the Learned Authority should not stand and were required to be deleted.

9.3 On the legal aspect, we note that the Hon’ble Supreme Court in Checkmate Services (P). Ltd. (supra) has categorically laid down that employees’ contribution to welfare funds must be deposited within the statutory due date prescribed under the relevant enactments, and the operation of section 43B does not dilute or override this obligation. At the same time, it cannot be overlooked that the jurisdiction under section 143(1)(a) is restricted toprima facie adjustments and does not extend to issues which are debatable or contentious in nature. In this regard, the Hon’ble Chhattisgarh High Court in Raj Kumar Bothra (supra) has held that contentious disallowances cannot be fastened upon an assessee through a summary intimation under section 143(1). Similarly, the Delhi Bench of the Tribunal in Rajesh Kumar Garg (supra) has consistently taken the view that disallowances on account of delayed employees’ contribution, being highly litigated, fall outside the permissible scope of adjustment under section 143(1)(a).

9.4 Though it has been the case of the assessee that the judicial pronouncements relied upon reinforce the argument that the CPC exceeded its limited mandate in making the present adjustment without affording any opportunity of explanation, we refrain from making any categorical observation on the applicability of the decisions of the Hon’ble Chhattisgarh High Court and the Delhi Tribunal as referred by the Ld. AR. This is for the simple reason that the law is to be applied contextually and only upon verification of the facts. It is essential that the facts of the present case be examined in detail and a finding be recorded as to whether they are indeed parimateria with the facts in the cited precedents.

9.5 It is, however, well settled that the law declared by the Hon’ble Supreme Court under Article 141 of the Constitution is declaratory in nature and operates from the date of insertion of the statutory provision itself. Therefore, the interpretation accorded in the judgment of the Hon’ble Supreme Court in Checkmate Services (P). Ltd. (supra) binds all authorities as if it was the law from inception. The Ld. CIT(A) was thus duty-bound to apply the ratio of the Hon’ble Supreme Court as it stood on the date of his order. The subsequent decision of the Hon’ble Chhattisgarh High Court dated 08.05.2025 was not available for his appreciation at that stage. Further, the reliance placed on the decision of the Delhi Tribunal is of no assistance to the assessee since the disallowance by way of adjustment was made by the CPC on the basis of the particulars furnished in the audit report itself, which accompanied the return of income.

9.6 We may also observe that, as per Section 15 of the Income-tax Act, 1961, salary is chargeable to tax when it becomes due from the employer. The contribution towards ESI and EPF is integrally linked to the salary of the employees and becomes due at the same time as the salary itself. Such contributions are, therefore, an integral part of the employer’s salary obligation.

9.7 In view of the above discussion, we are of the considered view that the matter requires restoration to the file of the Ld. CIT(A) for a de novo adjudication. The Ld. CIT(A) shall undertake due verification of the factual position as regards the actual quantum of delayed employees’ contribution, if any. For this purpose, the Ld. CIT(A) shall segregate the employer’s and employees’ contributions on the basis of the material placed on record, including the audit annexures and the Chartered Accountant’s certificate, and confine the disallowance strictly to that portion of employees’ contribution which is found to have been deposited beyond the statutory due dates. Further, while re-adjudicating, the Ld. CIT(A) shall also take into consideration the decision of the Hon’ble Chhattisgarh High Court in Raj Kumar Bothra (supra), examine the factual matrix of the present case, and determine the applicability of the said precedents. Needless to add, the assessee shall be afforded adequate opportunity of being heard and to substantiate its claim with supporting material.

10. In the result, this appeal of the assessee is allowed for statistical purposes.

11. Both the parties fairly submitted that the facts and circumstances of other two appeals i.e ITA Nos. 643 and 644/ Chd/2025 are exactly identical to the Appeal in ITA No. 642/Chd/2025 except the amount involved in these appeals, therefore, our findings and directions given in ITA No. 642/Chd/2025 shall apply mutatis mutandis to these two appeals which are accordingly allowed for statistical purposes.

12. In the result, all the above appeals of the Assessee are allowed for statistical purposes.