JUDGMENT

Dinesh Mehta, J.- By way of the present petition, the petitioner assails the order dated 30.12.2025, whereby the respondents have rejected the petitioner’s objection regarding the jurisdiction and has decided to continue with the reassessment proceedings for Assessment Year 2012-13.

2. Before adverting to the issues that arise for consideration, it will be apposite to give, in brief, the factual backdrop giving rise to the present case.

3. The petitioner is an assessee regularly filing his return of income in Delhi and is assessed to tax within the jurisdiction of the respondents. For Assessment Year 2012-13, the petitioner filed his return of income on 26.09.2012 declaring an income of Rs. 9,39,990/-.

4. On 31.03.2019, at 11:07 pm, an e-mail was sent to the petitioner’s registered mail id from the office of the Assessing Officer, which was viewed by him on 01.04.2019. The document annexed thereto however bore the name and PAN of some other assessee, namely, M/s Paramsant Global Infratech Ltd.

5. The petitioner addressed an e-mail dated 18.04.2019 to the respondents stating that the notice received by him pertained to a third party. Thereafter, on 05.09.2019, on petitioner’s request the respondents forwarded the reasons for reopening the assessment. The petitioner raised objections vide e-mail of even date against the initiation of proceedings, on the ground that no valid notice under Section 148 of the Income Tax Act 1961 (hereinafter referred to as ‘the Act of 1961) had been issued or served upon him within the period of limitation.

6. Notwithstanding the above referred objections, a notice dated 18.10.2019 under Section 142(1) of the Act of 1961 came to be issued and, between 24.10.2019 and 10.12.2019, the objections were dealt with by a series of communications.

7. An assessment order dated 12.12.2019 was thereafter passed under Section 144 read with Section 147 of the Act of 1961, making an addition of Rs. 13,00,000/- and assessing the total income at Rs. 22,39,990/-. The petitioner carried the matter in appeal and, by order dated 12.12.2024, the Commissioner of Income Tax (Appeals) set aside the assessment order and remanded the matter to the Assessing Officer with a direction to examine the petitioner’s contention regarding the validity of the notice. Pursuant thereto, a notice dated 16.09.2025 under Section 142(1) of the Act of 1961 was issued.

8. Thereafter by way of the impugned order dated 30.12.2025, the respondents rejected the said objections and directed continuation of the reassessment proceedings which has been impugned before us.

9. Mr. Manuj Sabharwal, learned counsel for the petitioner, at the outset, submitted that though a notice under Section 148 of the Act of 1961 was issued and uploaded on the e-filing portal on 31.03.2019, no automatic email was triggered through the ITBA portal, instead, on the very same day, the Assessing Officer manually sent an e-mail enclosing a notice which was relating to an entirely different assessee, namely, M/s Paramsant Global Infratech Ltd. and it bore some other PAN number.

10. He contended that such a notice cannot constitute valid issuance or service of notice under Section 148 of the Act of 1961 in terms of Section 282 read with Rule 127 of the Income Tax Rules, 1962. In support of his aforesaid contention, learned counsel for the petitioner placed reliance on the decision of this Court rendered in the case of Suman Jeet Agarwal v. ITO ITR 517 (Delhi), and submitted that mere uploading of a notice on the ITBA portal does not amount to valid issuance under Section 148 of the Act of 1961 and unless the notice goes out of the control of the Assessing Officer in the prescribed electronic mode, i.e., by an automatic trigger from the ITBA portal, the condition precedent for issuance of notice is not satisfied.

11. He further submitted that in the case of the petitioner, since the e-mail communication itself carried a notice in the name of a third party therefore, the notice dated 31.03.2019 cannot be said to be validly issued within the period of limitation so as to conform to the provisions of Section 148 of the Act of 1961.

12. Mr. Sunil Agarwal, learned senior standing counsel for the respondents, on the other hand submitted that the notice dated 31.03.2019 mentioned PAN of the assessee and an inadvertent attachment of a wrong document with the e-mail of even date does not detract from the factum of valid issuance of the notice within the period of limitation.

13. He further submitted that even in the objections dated 25.09.2025 the petitioner has merely assailed the mode and validity of service and did not dispute the factum of issuance of the notice under Section 148 within limitation.

14. He contended that the reliance on the judgment rendered in the case of Suman Jeet (supra) is also wholly misplaced inasmuch as in the said case, on account of the regime change in limitation with effect from 01.04.2021, the Department had generated an extraordinarily large number of notices on 31.03.2021, and to prevent the ITBA system from collapsing, the notices were released in batches. In that process, some notices reached the assessees before midnight, while others were despatched shortly thereafter, giving rise to the dispute.

15. Learned senior standing counsel contended that under the unamended provision as it stood prior to its amendment on 01.04.2021, by the Finance Act, 2021, Section 148 of the Act of 1961 clearly contemplates two distinct stages, namely, issuance of notice and service thereof. While the notice must be issued within the period of limitation prescribed under Section 149 of the Act of 1961, service even after expiry of limitation does not render the proceedings invalid.

16. Heard learned counsel for the parties and perused the record.

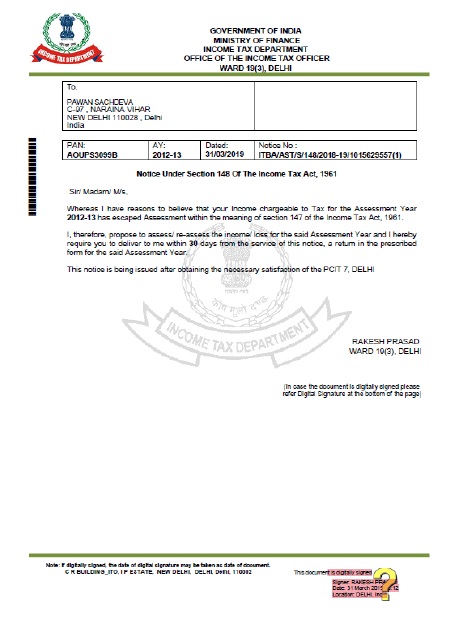

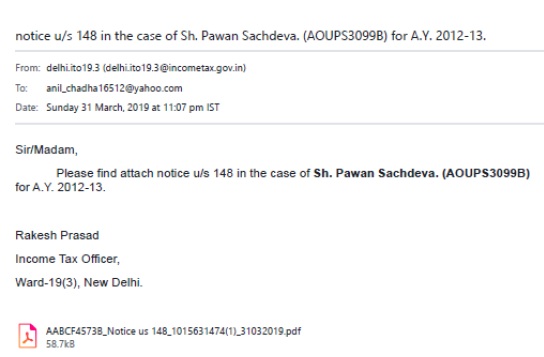

17. According to us petitioner’s objection regarding the invalidity of the notice on account of attachment of another assessee’s document is misconceived. A perusal of the e-mail dated 31.03.2019, on which reliance is placed by the petitioner, reveals that it contained the following assertion: “Please find attach notice u/s 148 in the case of Sh. Pawan Sachdeva (AOUPS3099B) for A.Y. 2012-13.”

18. We deem it apt to reproduce a copy of the notice dated 31.03.2019 and e-mail of even date that were sent to the petitioner. A scanned image of the same is pasted hereunder:

19. The e-mail, on its plain reading, clearly indicates that the statutory notice was intended for, and addressed to, the petitioner, bearing his correct name, PAN and Assessment Year. The fact that, along with the said e-mail, a notice pertaining to another assessee inadvertently came to be attached, does not efface the substance of the communication and the same, in the considered view of this Court, cannot be kept at an equal footing to a jurisdictional defect.

20. The mere fact that no real-time e-mail alert was triggered or that the petitioner did not view the same on that date i.e. 31.03.2019 cannot, by itself, lead to the conclusion that the notice was never “issued”.

21. The judgment in the case of Suman Jeet Agarwal (supra) is clearly distinguishable as the decision arose out of a wholly peculiar and timebound situation arising out of the regime change brought about by the Finance Act, 2021, where the limitation framework within the Act of 1961 itself stood altered with effect from 01.04.2021, and the controversy centred around notices generated on the last day of the old regime but despatched thereafter.

22. The instant case is governed by the pre-amendment regime i.e. prior to 01.04.2021 as the notice under section 148 of the Act of 1961 was issued on 31.03.2019. Under the un-amended provisions, the jurisdictional requirement was the issuance of notice under Section 148 within the period of limitation, and not its service within such period and service, even if effected after the expiry of limitation, cannot vitiate the assumption of jurisdiction, so long as the notice stood issued within the prescribed period of limitation.

23. In the facts of the present case, once it is found that the notice under Section 148 was issued on 31.03.2019, i.e., within the prescribed period of limitation, it was sent to and received by the petitioner on 31.03.2019 itself. Hence, even if it is taken that service was effected thereafter cannot, by itself, render the proceedings a nullify.

24. A similar view has been taken by Hon’ble the Supreme Court in the judgment rendered in R.K. Upadhyaya v. Shanabhai P. Patel (SC)/[1987] 3 SCC 96, wherein it was made clear that for the purposes of Section 149 of the Act of 1961, what is material is the issuance of the notice and not its service within the period of limitation. The date of despatch of the notice is the relevant date for determining whether the notice has been validly issued. Applying the said principle to the facts of the present case, since the notice under Section 148 was issued on 31.03.2019, i.e., within the prescribed period of limitation, it cannot be said that there is inherent lack of jurisdiction. The Assessing Officer cannot be faulted merely on the ground that attachment sent therewith contained some other assessee’s notice. In any case it was a curable defect.

25. In view of the discussion foregoing, this Court is of the considered opinion that the order dated 30.12.2025 does not warrant interference. The writ petition is, accordingly, dismissed.

26. All pending applications, also stand disposed of in the aforesaid terms.