ORDER

Girish Agrawal, Accountant Member.- This appeal filed by the assessee is against the final assessment order passed pursuant to the directions of the Dispute Resolution Panel-1, Mumbai, (DRP) vide order dated 04.09.2018 u/s. 144C(5) of the Income-tax Act, 1961 (hereinafter referred to as the “Act”), for Assessment Year 2014-15.

2. Grounds taken by the assessee are reproduced as under:

Ground 1: Determination of the arm’s length price (ALP) of the international transaction relating to processing fees received on account of guarantees issued to Indian companies based on counter-guarantee from overseas branches On the facts and in the circumstances of the case and in law, the learned AO, based on the directions of the Hon’ble DRP, erred in making a transfer pricing adjustment of Rs 56,31,605, by re-computing the ALP of the international transaction undertaken by Australia and New Zealand Banking Group Limited, Mumbai Branch (ANZ Mumbai) relating to processing fees received on account of guarantees issued by ANZ Mumbai to Indian beneficiaries [based on the corresponding back to back guarantee provided by the overseas associated enterprises (AE’s)].

Ground 2: Rejecting the Transactional Net Margin Method (TNMM) used by the Appellant and adopting External Comparable Uncontrolled Price (CUP) method as the most appropriate method

On the facts and in the circumstances of the case and in law, the learned AO. based on the directions of the Hon’ble DRP, erred in determining the ALP of the international transaction undertaken by ANZ Mumbai relating to processing fees received on account of guarantees issued by ANZ Mumbai to Indian beneficiaries (based on the back to back guarantee provided by the overseas AEs) on account of the following:

(a) In rejecting the TNMM used by the Appellant without appreciating that the Appellant provides administrative support services, by issuing local guarantees based on the instructions and counter guarantee received from the AE, without undertaking risk on the overseas third party requesting the guarantee.

(b) In adopting external CUP method as the most appropriate method to determine the ALP of the international transaction, by using information received/collected from third party Indian banks under section 133(6), and without any comparability analysis concluding that the functions performed, assets used and risks undertaken by ANZ Mumbai are comparable with the activities carried on by the banking companies from whom data was collected by the AO under section 133(6).

(c) Without prejudice to the above, in concluding that the Appellant should have charged 0.53% of the guarantee amount without any cogent and reasonable comparability exercise prescribed under Rule 10B of the Income-tax Rules, 1961 read with Section 92C of the Income-tax Act, 1961.

Ground 3: Determination of the ALP of the international transaction relating to marketing support services provided by ANZ Mumbai to its AEs in respect of derivative products

On the facts and in the circumstances of the case and in law, the learned AO. based on the directions of the Hon’ble DRP, erred in making the transfer pricing adjustment of Rs 63,93,140, by re-computing the ALP of the international transaction undertaken by ANZ Mumbai relating to marketing support services provided by ANZ Mumbai to its AEs in respect of derivative products.

Ground 4: Rejecting the Transactional Net Margin Method (TNMM) used by the Appellant and adopting revenue split under Profit Split Method (PSM) method as the most appropriate method

On the facts and in the circumstances of the case and in law, the learned AO, based on the directions of the Hon’ble DRP, erred in determining the ALP of the international transaction undertaken by ANZ Mumbai relating to marketing support services provided by ANZ Mumbai to its AEs in respect of derivative products on account of the following:

(a) In rejecting the functional, asset and risk analysis undertaken by ANZ Mumbai

(b) In not accepting the economic analysis undertaken by the Appellate in accordance with the provisions of the Act read with the Income-tax Rules, 1962 (‘Rules’) and arbitrarily applying the revenue split method under PSM as the most appropriate method without giving reason to reject TNMM adopted by the Appellate

(c) Without prejudice to the above sub-ground (b), in computing upward adjustment by considering those deals where the day end NPV is positive and ignoring those deals where the day end NPV is negative

(d) In observing that the Appellant has not maintained sufficient and appropriate documentation.

Ground 5: Reimbursement of expenses, being identifiable to ANZ Mumbai and incurred specifically for ANZ Mumbai considered to be covered within the provisions of section 44C of the Act and consequent disallowance of the said expenses

On the facts and in the circumstances of the case and in law, the learned AO, based on the directions of the Hon’ble DRP, erred in holding that the following expenses incurred by ANZ Mumbai, and which were reimbursed by ANZ Mumbai to the Appellant, are covered by the provisions of section 44C of the Act and thereby, disallowed the same being over and above the limit prescribed under section 44C of the Act:

(a) Reimbursement of telecommunication charges (Singtel leased line charges) incurred by the Appellate amounting to Rs 1,29,85,774, and

(b) Reimbursement of the cost incurred towards the expatriates personnel working as employees of the Mumbai Branch Rs 16,73,234

Ground 6: Interest received by the Appellant/ overseas branches of the Appellant from ANZ Mumbai liable to tax in the hands of the Appellant under Article 11 of the India-Australia Double Taxation Avoidance Agreement

On the facts and in the circumstances of the case and in law, the learned AO, based on the directions of the Hon’ble DRP, erred in holding that the interest received by the Appellant/ overseas branches of the Appellant from ANZ Mumbai amounting to Rs 2,98,64,616 is liable to tax in the hands of the Appellant under Article 11 of the India-Australia Double Taxation Avoidance Agreement

2.1. Assessee filed application for admission of additional grounds vide letter dated 19.04.2024 raising legal issue that the impugned assessment order has been passed beyond the prescribed time limit u/s.153. There being no objection from the other side, these were admitted for adjudication. However, in the course of hearing, at the outset, ld. Counsel for the assessee submitted that the issue raised in these additional grounds may be kept open and to adjudicate on the merits of the case. Accordingly, we deal with the merits of the case leaving open the additional grounds with the liberty to the assessee to contest on the same in case situation so demands in the future.

3. Ground No.1 raised by the assessee is with regard to determination of Arm’s Length Price (ALP) of the international transaction relating to processing fees received on account of guarantees issued to Indian companies based on counter guarantee from overseas branches. Ground No.2 raised by the assessee is on challenging the rejection of Transactional Net Margin Method (TNMM) used by the assessee and adopting external Comparable Uncontrolled Price (CUP) method as the Most Appropriate Method (MAM).

4. We have heard rival submissions and perused the materials available on record. We find that assessee is a commercial bank having its head office in Melbourne, Australia. Australia and New Zealand Banking Group (ANZ) commenced its banking operations in India with the opening of its first branch in Mumbai pursuant to the receipt of the banking license from Reserve Bank of India (RBI). During the relevant year, ANZ has a branch in India operating in Mumbai. It is involved in normal banking activities including financing of foreign trade and foreign exchange transactions.

5. During the year, assessee had issued guarantee to customer based on the counter guarantee issued by its AEs. Assessee had benchmarked this transaction using TNMM as the MAM. Assessee was asked to provide the details relating to the amount of guarantee issued by it on behalf of the clients based on counter guarantee issued by overseas branches of ANZ. Assessee was also asked to provide back-up document in respect of the above transaction and the average rate at which guarantee fees has been charged by the assessee to its AEs. All these details were submitted by the assessee. The TPO was not satisfied either with the method followed by the assessee nor the rate of guarantee fee adopted.

5.1. On the above stated facts, this issue is squarely covered by the decision of Coordinate Bench of ITAT, Mumbai in assessee’s own case for Assessment Year 2020-21, in Australia and New Zealand Banking Group Ltd. v. Dy. CIT (International Taxation) (Mumbai – Trib.)/ITA No.4778/Mum/2024, dated 28.5.2025, wherein the undersigned AM is the author. Relevant extracts in this respect from the said order are as under:

“2.1. The ld. TPO observed that assessee had earned processing fees for issuing guarantees on behalf of its AEs at an average rate of 0.02%. The ld. TPO observed that assessee had used comparables that are pertaining to support services industry which are not comparable with the activity of the assessee issuing guarantee for commission. Accordingly, the ld. TPO rejected those comparables and also TNMM method adopted by the assessee and proceeded to benchmark the guarantee transaction using external CUP method.

2.2. In order to apply the CUP method, information regarding the rates charged for giving ‘bank guarantee’ was called from various banks u/s 133(6) of the Act, which is summarized as below:

| Sr. No |

Name of the Bank |

Rate |

| 1. |

Standard Chartered Bank |

0.75% |

| 2. |

Citi Bank |

0.90% |

| 3. |

Union Bank of India |

1.20% |

| 4. |

HDFC Bank |

1.80% |

| 5. |

IDBI Bank |

2.00% |

| 6. |

State Bank of India |

2.10% |

| 7. |

ICICI Bank |

2.50% |

|

35th Percentile |

1.20% |

|

Median |

1.80% |

|

65th Percentile |

2.00% |

2.3. From the perusal of the information received from the banks, it is seen that the bank guarantee rates are 1.80%.

2.4. Accordingly, ld. TPO benchmarked the guarantee fee transaction of the assessee after taking into account the judicial precedent in the case of Hon’ble Jurisdictional High Court of Bombay in the case of CIT v. Everest Kanto Cylinders Ltd (Bom), concluded that it would be appropriate to charge 1.3% (median of bank guarantee rate charged by bank at the rate of 1.8% less 0.5% or downward adjustment) from the AE for the corporate guarantee given on behalf of assessee to third party financial institutions. According to him, since the assessee charged guarantee fee at the average rate of 0.33% per annum, the same was found to be inadequate and not meeting Arm’s Length test. He thus, computed an upward adjustment of Rs.2,25,13,339/- while passing the order u/s.92CA(3). The working for the adjustment proposed, is tabulated below:

| Particulars |

Amounl(IRR) |

| Guarantee fees based on (1.8% – 0.5%) p.a. of the guarantee amount |

3,57,65,165 |

| Less: Guarantee fees earned by the assessee |

1,12,11,826 |

| Adjustment amount |

2,25,13,339 |

2.5. The very same TP adjustment was incorporated in the final assessment order passed by the ld. AO u/s.143(3) r.w.s. 144(C) (13) of the Act dated 24.07.2024 pursuant to the directions of the ld. DRP.

3. During the course of hearing, Shri Madhur Agarwal, ld. counsel for the assessee submitted that similar issue has been decided in favour of the assessee by the Co-ordinate Bench of the Tribunal rendered in assessee’s own case.

4. On the other hand, Shri Kiran Unavekar, ld. Sr. DR vehemently relied upon the orders passed by the lower authorities.

5. We have considered the rival submissions and perused the material available on record. We find that the Co-ordinate Bench of the Tribunal in assessee’s own case in M/s. Australia and New Zealand Banking Group Ltd. v/s DCIT, in ITA No. 1106/Mum/2017, for the Assessment Year 2012-13, vide order dated 13.04.2022, had dealt with this identical issue. Further the same issue was also dealt by the Coordinate Bench in assessee’s own case for Assessment Year 2013-14 in ITA No.5129/Mum/2017, dated 10.08.2022. The Coordinate Bench in ITA No.1106/Mum/2017 for Assessment Year 2012-13, while deleting the transfer pricing adjustment made in respect of guarantee fees, observed as under:

“3.5. At the outset, we find that overseas branches of ANZ have clients who require guarantees to be issued to the beneficiaries in India. Since the beneficiaries are situated in India, the overseas branches of ANZ are situated in India. The overseas branches of ANZ request the assessee to provide such guarantees to the beneficiaries and inturn provide a back to back inter-bank guarantee / indemnity to assessee to cover any financial liability that assessee may incur in connection with guarantees issued to Indian beneficiaries on behalf of overseas ANZ branches. This is the prime function / activity carried out by the assessee with regard to the impugned international transaction. In case where the client of the overseas branch defaults and the guarantee would be invoked then, under the back to back guarantee issued to assessee, the overseas branch would make payments to assessee which would onward then make the payment to the beneficiary in India. 3.6. Hence, from the aforesaid modus operandi, it could be concluded that assessee acts as a beneficiary bank i.e. issue guarantee in India on behalf of clients of overseas branches of ANZ based on the counter guarantee issued by such overseas ANZ branches. Since assessee is acting as the beneficiary, the entire risk of discharging the bank guarantees is borne by overseas ANZ branch issuing the counter guarantee. The assessee merely provides support service in connection with processing of the guarantees, typing out the guarantee agreement based on swift message received and issuing the said agreement to the beneficiary. The aforesaid functions performed by the assessee are not disputed by the lower authorities. When assessee is fully protected by overseas counter guarantee, we are unable to comprehend ourselves as to how CUP method could be applied therein as it would be impossible to make adjustment for the differences as per Rule 10B(1)(a) of the Income Tax Rules. In effect, we find that assessee is merely providing secretarial services or which can be loosely called as carrying out administrative functions. It is not in dispute that the assessee does not bear any risk in its books as it is fully protected by overseas counter guarantee / indemnity. In fact even assessee would not have to face the foreign exchange risk in view of the fact that whenever assessee is called upon to discharge the guarantee on behalf of the overseas branches, the assessee would first receive the monies from overseas branch because of the existing counter guarantee, and then discharge the same. The assessee is receiving processing fees from its AEs in foreign currency and the said fee is received immediately after the invoice is raised for the same, thereby the risk of exchange fluctuation would be very very negligible due to reduced time span involved therein. Given these undisputed facts, it would be appropriate to consider assessee as the tested party as it would be the least complex entity and its profitability could be reliably ascertained. Admittedly, the transaction which requires to be benchmarked is the receipt of processing fees by the assessee for the guarantees issued by rendering the aforesaid secretarial services. Hence, what is to be looked into is under similar terms and conditions and under similar circumstances what is the guarantee fee charged by the third party comparables from their AEs. This is what precisely assessee has done in the instant case. The assessee had taken into account the third party comparable margins and compared the same with its margins using Transactional Net Margin Method. For this purpose, the assessee had taken the third party comparables which are engaged in providing liasoning services, managerial services, marketing services, administrative services and information services. Effectively all these services could be loosely termed as business support services. Hence, when the data under CUP method is not available and data of margins under TNMM is readily available, then it would be appropriate to apply TNMM method as the Most Appropriate Method (MAM) in the facts and circumstances of the instant case. 3.7. We find that assessee had explained the entire transactions and the modus operandi applied by it in respect of the guarantee transactions before the ld. TPO which are evident vide letter dated 09/10/2015 together with the fee charged for each type of services rendered by it. These details are enclosed in pages 316 to 322 of the paper book filed before us. We also find the assessee vide its letter dated 28/10/2015 had filed a detailed annexure enclosed in pages 328-331 of the paper book listing the guarantees issued by it based on counter guarantee received from overseas branches of ANZ. The assessee also furnished the sample documents enclosing the copy of swift message received from ANZ New York advising the assessee to issue guarantee to Indian beneficiaries like Reliance Infrastructure Ltd., and providing counter guarantee. 3.8. The assessee also placed on record the copy of the swift message from assessee to ANZ New York confirming that guarantee has been issued to Reliance Infrastructure Ltd., confirming that guarantee has been issued by ANZ Mumbai. By all these documents, the ld. AR was vociferous in driving home the point that the entire risk of discharging the bank guarantees is borne by the overseas ANZ branch issuing the counter guarantees wherein the assessee merely provides support services in connection with processing of the guarantees. The ld. AR also referred to page 380 of the paper book containing various swift messages received. The assessee also placed on record the reply letter dated 18/12/2015 filed before the ld. TPO in response to showcause notice as to why 1% guarantee fee charged by third party Indian banks should not be considered as the arm’s length price, placed reliance on the decision of the Mumbai Tribunal in the case of Asian Paints Ltd., v. ACIT in ITA Nos. 2126 & 2178/Mum/2012 wherein specifically in the context of guarantee fees, this Tribunal had deleted the adjustment made as the said judgement was rendered simply relying on certain data from the market. The facts of the case before us squarely fit into the facts prevailing in the case of Asian Paints Ltd. 3.9. The assessee before the ld. DRP made an alternative submission that the fee of 1% proposed by the ld. TPO may be applied in respect of fresh guarantees issued during the year. The details of fresh guarantees issued during the year were also furnished before the ld. DRP in pages 577-579 of the paper book vide letter dated 27/04/2016. But we find that the ld. DRP had merely brushed aside the same and grossly erred in stating that no details were filed by the assessee. 3.10. In view of the aforesaid observations, we hold that TNMM method would be the Most Appropriate Method in the facts and circumstances of the instant case and CUP could not be applied herein because of nonavailability of data. In any case in respect of adjustment made simply relying on 133(6) information from the market had been deleted by this Tribunal in the case of Asian Paints Ltd., referred to supra. It is also prudent to note that the same transactions were accepted by the ld. TPO upto A.Y.2012-13 in the case of the assessee. Hence, even going by the rule of consistency as has been held by the Hon’ble Supreme Court in the case of Radhasoami Satsang reported in 193 ITR 321, there is no need for the ld. TPO to take a divergent stand when there is no change in the facts and circumstances during the year with that of earlier years. Hence, we direct the ld. TPO to delete the adjustment made in respect of guarantee fees in the sum of Rs.10,94,55,035/-. Accordingly, the ground Nos. 1 & 2 raised by the assessee are allowed.”

6. The learned Departmental Representative could not show us any reason to deviate from the aforesaid order and no change in facts and law was alleged in the relevant assessment year. Thus, respectfully following the order passed by the Co-ordinate Bench of the Tribunal in assessee’s own case cited (supra), we uphold the plea of the assessee and delete the impugned transfer pricing adjustment. Accordingly, grounds no. 1 and 2 raised in assessee’s appeal are allowed.”

5.2. Respectfully following the above judicial pronouncement in assessee’s own case, there being no change in material facts, ground nos.1 and 2 raised by the assessee are allowed.

6. Ground nos. 3 and 4 are in respect of upward adjustment of Rs. 63,93,140/- made relating to marketing support services provided by the assessee to its Associate Enterprises (AE) for derivative products.

6.1. Nature of transaction as explained by the assessee in its transfer pricing study report placed in the paper book, is extracted below:

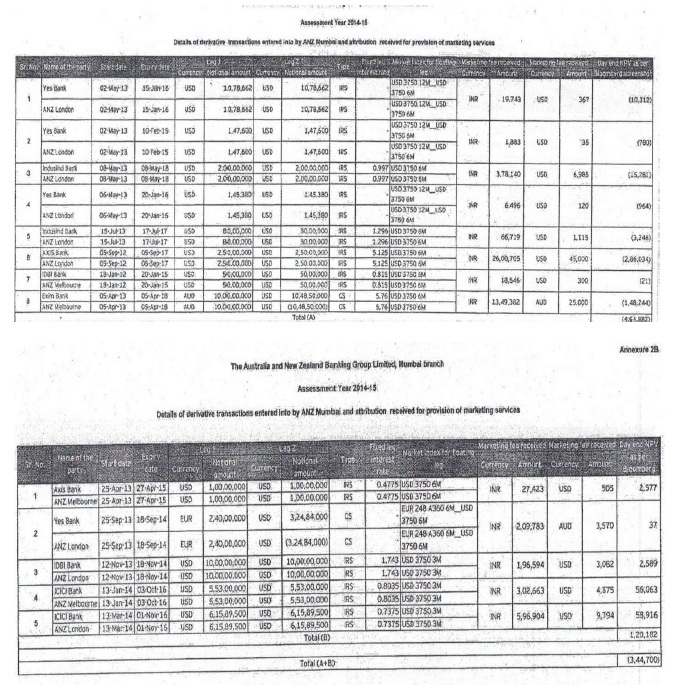

ANZ Mumbai targets customers having foreign currency liabilities and interest exposure and offers them derivative products such as interest rate swaps and cross currency interest rate contracts.

The RBI allows commercial banks operating in India (including Indian branches of foreign banks) to sell foreign currency contracts including swaps and options to its customers in India provided that they are within prescribed limits or are undertaken on a fully covered back to back basis.

ANZ Mumbai originates customer transactions from the third party end customer and then book an equal and opposite ‘back to back’ deal with its overseas AEs. Typically, a sales person from ANZ Mumbai obtains a price from the trader in the overseas ANZ office in respect of a particular derivative product. Upon receipt of the price from the overseas ANZ trader, the salesperson of ANZ Mumbai finally agrees the pricing of the trade with the customer inclusive of the mark-up of ANZ Mumbai. The entire amount of mark-up agreed by the ANZ India sales person with the customer is paid to ANZ Mumbai as fees, for the functions performed and risks assumed as outlined in para 2.5.2 and 2.5.3 below.

A total of Rs 5,774,982 has been received in relation to the activities undertaken for the year ended 31 March 2014. Details of the income attributed to ANZ Mumbai are enclosed in Appendix 11.

6.2. For benchmarking this transaction, assessee used TNMM as the most appropriate method. According to the ld. TPO/Assessing Officer, assessee had failed to furnish details in respect of these transactions and other derivative transactions entered into. Ld. AO/TPO noted that apart from the hard markup or initial spread, assessee was not getting any compensation from other deals either in the form of hard markup or share in the soft markup or trader profit or by way of recovery of cost. According to the ld. Assessing Officer/TPO, assessee has borne all the risk for the transactions and was required to be compensated adequately by the AE, which was not done. Ld. AO/TPO has dealt in detail with this issue and concluded that the assessee had not received any compensation in some of the deals and that these transactions were not benchmarked at all in its TP study report. Assessee had also failed to furnish details asked for by the AO/TPO, such as NPV or Day INPV, deal ticket, internal correspondence to show the markup, and the ALP, Further, assessee also failed to establish that 100% of the hard markup was earned by it, as claimed. It is for these reasons, ld. AO/TPO has benchmarked the transactions.

6.3. Contention of the assessee is that ld. TPO proposed to determine the arm’s length price of the remuneration received by the India Branch from the derivative transactions on the basis of the day end NPV disregarding the fact that the India Branch does not take the risk of profit/loss from the said transaction. While determining the arm’s length price, ld. TPO did not consider those deals wherein the day end NPV was negative and only considered those deals which resulted in positive day end NPV. According to the assessee, ld. TPO treated whole of the positive day end NPV as the remuneration of the India Branch from the said transaction and proposed to make an adjustment of Rs.63,93,140/- using Profit Split Method (PSM) by way of revenue split. Ld. DRP did not find any reason to interfere with the findings of ld. TPO on the said issue.

6.4. In this regard, assessee submitted the following to contest on the correctness of the method applied by Id. TPO –

| i. |

|

Not accepting the detailed benchmarking undertaken by the assessee and applying PSM without giving any reason for rejecting TNMM analysis of the assessee |

| ii. |

|

Not considering the fact that assessee does not undertake any risks of profit/loss from the transaction and therefore, ALP cannot be determined on the basis of day end NPV |

| iii. |

|

Ld. TPO erred in not splitting the profit and treating the whole of the day end NPV as attributable to the Mumbai Branch even while applying PSM. |

6.5. Assessee further submitted that even if method adopted by ld. TPO was to be considered, ld. TPO erred in computing the upward adjustments for only those deals where the day end NPV is positive and ignoring the deals where the day end NPV is negative. Assessee submitted that considering the nature of the transactions, even if the method of ld. TPO was to be applied, the same should have been applied on an aggregate basis i.e., considering both, the positive and negative day end NPV. Assessee submitted that once the deals are aggregated, there is no transfer pricing adjustment required. Assessee submitted that if it succeeds on this argument, then the other arguments on the correctness of method adopted by the ld. TPO may not be adjudicated and left open.

6.6. In relation to the rule of aggregation, assessee placed reliance on the following decisions wherein the Tribunal has consistently held that for such similar nature of transactions, the arm’s length price has to be determined on aggregate basis –

| i. |

|

Barclays Bank PLC v. ADIT (International Taxation) (Mumbai) |

| ii. |

|

Credit Agricole Corporate and Investment Bank v. Dy. CIT [IT (TP) A. No. 1479/Mum/2015, dated 10-3-2025]. |

6.7. Relevant extracts from the order of Barclays Bank PLC (supra) on the rule of aggregation are as follows:

12. The one more issue in Revenue’s appeal in ITA No. 2306/Mum/2015 for AY 2009-10 is as regards to the order of CIT(A) directing the AO/TPO to aggregate the various transaction relating to many deposits by placing reliance on IT Rules 10A(d) of the Rules. For this Revenue has raised the following ground No. 2.1 and 2.2 as under.

2.1 Whether on the facts and circumstances of the case and in law, the CIT(A) has erred in directing the AO/ TPO to aggregate the various transaction relating to money deposits by placing reliance on I.T. Rules 10A(d) without appreciating that while applying CUP method of ALP determination each such transaction could be evaluated/benchmarked separately.

2.2 Whether on the facts and circumstances of the case and in law, the CIT(A) has erred in directing the AO/TPO to aggregate the transactions and thereby directing to delete the adjustment/addition of Rs. 80,45,571/-in a case where the ALP of each transaction could be arrived at separately.”

13. Briefly stated facts are that the TPO after going through the Transfer Pricing study in the case of assessee noted that even though the assessee has used LIBOR rate as indicative rate to Bench mark the transaction on interest on money market loans and deposits received from or paid to Associated Enterprise (AE’s). According to the TPO, there is variation in the actual rate vis-a-vis the LIBOR rate. The assessee explained before the AO about variation and stated that it has worked out the interest rate arising from such fluctuations of the LIBOR rates in respect of money market deposits and loans transactions and computed the same by aggregating all the parties. However, according to AO/ TPO there is excess payment of interest by the assessee on one hand and there is short receipt of interest by assessee on the other hand. And Hence, the TPO has not accepted the explanation of the assessee and made an adjustment of amount of Rs. 80,45,51 7/-for short interest received excess interest paid on money market deposits given of accepted by the assessee. The AO has also given summary of transaction in its order. Aggrieved, assessee preferred the appeal before CIT(A), who is deleted the addition by stating that the assessee has rightly aggregating the transactions of all the parties and then reached to proper LIBOR rate. The CIT(A) deleted the addition by observing in para 7.3 to 7.5 as under: –

7.3 I have received the facts and the submissions of the appellant and the learned TPO. With regard to the aggregation, the Appellant has placed reliance on the ruling of the Mumbai Bench of the Income-Tax Appellate Tribunal (Mumbai ITAT) in the case of Essar Steel Ltd. (ITA No 3727/Mum/2011), wherein the Mumbai ITAT has drawn reference to Rule 10(A)(a) of the Income tax Rules, 1962, which defines a “transaction to include a number of closely linked transactions. In such a case, the Mumbai ITAT held that if the transactions are closely linked, then they can be aggregated for determining the ALP. In the aforementioned case, it was held that if the product remains the same and the source from which the average price has been taken remains the same, it is a fit case for aggregation. A similar view was also taken by the Mumbai ITAT has upheld the aggregation of transactions as against arbitrary selection of individual items. Separately, in the case of Boskalis International Dredging International CV (ITA 4862/Mum/2008), the Mumbai. The Mumbai ITAT noted that aggregation and clubbing of the closely linked transactions are permitted under the Income-tax Rules, 1962 and it is also supported by OECD transfer pricing guidelines.

7.4 A summary of the interest paid and received on all money market deposit transactions is provided below:

| Particulars |

Foreign Company |

INR |

| Interest paid as per transfer price |

USD 44,67,397 JPY 2,84,60,412 |

13,05,43,42,638 |

| Interest to be paid as per arm’s length price |

USD 43,53,447 JPY 2,60,55,770 |

13,04,84,54,457 |

| Interest Paid in excess of arm’s length price |

USD 1,13,950 JPY 24,04,642 |

58,88,181 |

| Interest to be received as per arm’s length price |

USD 7,87,27,213 |

3,51,81,23,621 |

| Interest received in excess of arm’s length price |

USD2,28,279 |

1,11,44,768 |

| Net transfer pricing adjustment |

NIL |

NIL |

7.5 Having taken note to the appellant’s submission, I find that while doing the addition on account of adjustment by the TPO u/s. 92CA(3), the TPO has ignored all such international transactions pertaining to this area wherein the appellant has derived excess interest in comparison with LIBOR method. I find force in appellant’s this submission that the TPO cannot do the adjustment merely on account of his personal decision to pick up one transaction and not the other. The appellant has filed a detailed chart as per ‘Annexure 7’ of Paper Book through which it is evident that if the same norms is adopted as LIBOR in working out the interest liability interest receipt, the appellant still has a better profit margin which is positive amounting to Rs. 1,11,44,768/-. The appellant has relied on the following decisions of jurisdictional ITAT, Mumbai as under:

| (i) |

|

Essar Steel Ltd. (ITA No. 3727/Mum/2011) |

| (ii) |

|

Audco India Ltd. (ITA No. 2642/Mum/2009) |

| (Hi) |

|

Boskalis International – Dredging International CV (ITA 4862/Mum/2008) |

Having taken note to the above decisions of the ITAT, Mumbai, referred by the appellant in its submission dated 22.01.2015, I find that the contention so made by the appellant is justified and hence, adjustment so made by the TPO is not correct. However, I consider it proper and appropriate to direct the AO to verify the correctness of the working done by the appellant as filed before me and before the AO as claimed by the appellant as per Annexure 7 and if the same if the same is found to be correct after making necessary verification, then the addition so made by the AO on the adjustment made by the TPO stands deleted. With this observation, the appellant’s this ground is adjudicated.”

Aggrieved, now Revenue is in appeal before us.

14. Before us, the learned Sr. Departmental Representative relied on the TPO/ APO’s order. On the other hand, the learned Counsel for the assessee stated that the issue is covered by the co-ordinate Bench of this Tribunal in the case of

ACIT v.

Audco India Ltd. (2011) 47 SOT 420 (Mum), wherein it is held as under:-

10. We have carefully considered the submissions of the rival parties and perused the material available on record. We find that the facts are not in dispute. We further find that the Id. CIT(A) has observed in paras 4.4 and 4.8 of his order as under.

“4.4 I have perused the facts of the case, Transfer Pricing Officer’s (TPO) order and assessment order thereof on this point. It is observed that the appellant had supplied the gate, globe and check valves to its AE amounting to Rs. 2,13,64,571. The primary business of the AE is sourcing of valves from the appellant company and marketing them in American markets. The appellant had the confidence to adopt CUP methodology which is the traditional method to justify its Arm’s Length. It filed full details, in this regard, before the TPO as well as the undersigned. While passing the order, the TPO ignored this data by dismissing it as general in nature.

4.8 The aggregate sale to an AE at USA is only Rs. 2,13,64,571, which is hardly 1% of the total sales of the company. It does not appear probable that for such a small turnover, which would hardly have any material affect on the income, the appellant would have tried to shift its profits.”

In para 4.9 of his order, he held as under

“4.9 More importantly, the aggregate difference of Rs. 6,94,310 between sale of L&T LLC (Rs. 2,13,64,571) Arm’s Length Price (Rs. 2,06,70,261) is only 3.35% and is well within the 5% of the tolerance limit permitted by the law. It is observed from the details filed by the appellant before the TPO as well as at the appellate stage that the prices realized from unrelated parties for an item is not uniform but higher or lower than the prices charged to related party (L&T LLC). That is to say that there are transactions for which data has been furnished, which shows that the appellant has charged higher rates from its AE as compared to third party uncontrolled transactions. The TPO while making the adjustments took only those figures in which valves were sold at the lower prices to the USA based AE while ignoring those figures and data where the same were sold at the higher price. Thus while making the adjustments, he disregarded the fact that the appellant has also sold valves to its AE at prices higher as compared to the average charged to the third unrelated parties. It would have been fair and reasonable on the part of the TPO to consider the aggregate of the sales made to the AE and then compare it with third parties as against the individual items considered by him. He has been selective in his approach and made the order arbitrary. Had the aggregate of sales made to the AE and that to the third parties been taken into account then the appellant’s case squarely falls within 5% tolerance threshold To my mind, it is appropriate to consider the aggregate sales to AE as against individual items selected arbitrarily. It is not fair for a quasijudicial authority to pick up those data, which are convenient and suitable to it and ignore the corresponding data which goes against it. Ultimately an order to stand has to have a mark of fairness, reasonableness and judiciousness. Taking all the above facts and circumstances, I am of the view that there is no case for adjustments of Rs. 7,28,865 in respect of the export price of finished valves of L&T LLC by selectively utilizing the data where the 5% limit is lower in respect of AE and ignoring those figures/data where sale of valves to the AE are at prices higher as compared to the average prices charged to third unrelated parties. The addition so made on totality of facts is, therefore, deleted.

In the absence of any contrary material placed on record by the revenue against the finding of the Id. CIT(A) and keeping in view that the difference between the sale of L&T LLC and Arm’s Length Price is only 3.35% which is well within the limit of 5%, we are inclined to uphold the finding of the Id. CIT(A) in deleting the addition made by the Assessing Officer. The ground taken by the revenue is, therefore, rejected.”

15. Similarly, in the case of ACIT v. Essar Steel Ltd. (Mumbai–Trib.), wherein it is held as under: –

“10. We have considered rival contentions and gone through the orders of the authorities below. A clear finding has been recorded by the CIT(A) to the effect that assessee has already considered all the 8 transactions with its AE in totality by aggregating the same whereas the TPO picked up two transactions where the price charge was less than the average market price. Rule 10(A)(a) defines a transaction to include a number of closely linked transaction. In case they are closely linked then they can be aggregated for determining the ALP. We found that assessee has exported hot rolled coils to its AE between 30-62005 to 10-3-2006, the price has been determined from the website whose data is not subject to challenge. The product remains the same and the source from which the average price has been taken remains the same. Accordingly, it is a fit case for aggregation. We found that if the average price is adopted for all the 8 transactions. then the average comes exactly to 420.71 which is what the price charged by the assessee to its AE. Furthermore, the detailed finding recorded by the CIT(A) at para 3.4 to 3.8 has not been controverted by learned DR by bringing any cogent material on record. Accordingly, we do not find any reason to interfere in the order of CIT(A) for deleting the addition in respect of adjustment made of Rs.5,82,41,193/”

16. After going through the facts and arguments of the both the sides, we noticed that the Tribunal is consistently taking the view that arm’s length price should be after aggregation and there was no scope for adjustment without aggregation. Taking a consistent view by following the co-ordinate benches decisions cited supra, we confirm the order of CIT(A) deleting the addition. This issue of Revenue’s appeal is dismissed.”

6.8. Ld. DR on the above issue referred to para 4.2 of the order of ld. DRP, the essence of which is already captured in the above paragraphs while narrating the nature of transaction undertaken by the assessee and observations / conclusions drawn by the ld. TPO/AO.

7. We have heard both the parties and perused the material on record. Admitted factual positon remains uncontroverted as to the impugned transactions are undertaken on back-to-back basis for which assessee does not undertake any risk of profit or loss on the said transactions. The entire amount of markup (being the difference between transaction price and the price quoted by AE) agreed by the assessee with the customer is its remuneration for the functions performed and risks assumed. Therefore, even if the transaction ultimately results in a loss, assessee will receive its remuneration being the markup. Ld. TPO has rejected TNMM adopted as the most appropriate method by the assessee and applied PSM (revenue split). Contention of the assessee is that PSM cannot be applied as InPV is a mere profit prediction and not the real profit and therefore not a correct method to be applied on the transaction undertaken by the assessee wherein it is not undertaking any risk of profit or loss from the said transaction. Arm’s Length Price (ALP) for these transactions cannot be determined on the basis of positive day end NPV. Further, ld. TPO has only considered the positive day end NPV and ignored the deals when the day end NPV is negative. Ld. TPO has not applied the same on an aggregate basis but has made a split between the positive and negative day end NPV.

7.1. In this regard, assessee furnished details to demonstrate that once an aggregation is taken into account, there would not be any transfer pricing adjustment required to be made. The working furnished by the assessee in this regard is extracted below for ready reference:

8. This issue had also come up before the Coordinate Bench of ITAT, Mumbai in the case of Credit Agricole Corporate and Investment Bank (supra). In this case, it was held that transfer pricing adjustment made by ld. TPO is not sustainable since marketing entity is not entitled to trading markup if the marketing entity is not taking trading risk of the derivative transaction. In the present case before us, ld. TPO has held that 100% of the hard markup has been earned by the assessee in all the transactions which relates to sales and marketing efforts on the part of the assessee.

8.1. Ld. TPO has resorted to PSM without providing any justification and rationality for the same on the transactions undertaken by the assessee. Even after we consider the method adopted by the ld. TPO where he has considered only positive day end NPV and ignored negative day end NPV, he ought to have applied the rule of aggregation for arriving at the bench mark. In this respect, we refer to the workings furnished by the assessee extracted above considering both positive and negative day end NPV based on aggregation which suggests that no adjustment is required even if the method adopted by ld. TPO is considered. Accordingly, in conspectus of the above discussion, we do not find any merit in the upward adjustment made for the above stated transactions and accordingly delete the same. Ground no.3 and 4 raised by the assessee are allowed.

9. Ground no.5 relates to addition in respect of reimbursement of expenses in the nature of telecommunication charges and cost incurred for expatriate personnel working as employees of India branch. Facts briefly stated in this regard are that during the year under consideration ANZ Mumbai reimbursed certain expenses to the Head Office in two categories:

| a. |

|

Reimbursement of telecommunication charges (Singtel leased line charges) amounting to Rs.1,20,65,774/-; and |

| b. |

|

Reimbursement of cost incurred towards the expatriate personnel working as employees of the Mumbai Branch Rs.16,73,234/-. |

9.1. As the said expenditure were incurred by the assessee specifically and exclusively for ANZ Mumbai, the same were claimed as a deduction by ANZ Mumbai under section 37(1) of the Act and it was submitted that the provisions of section 44C of the Act would not be applicable to the same.

9.2. Ld. Assessing Officer observed that the amounts claimed as reimbursement are covered u/s.44C of the Act. According to him, since assessee has already claimed expenditure u/s.44C towards Head Office expenses, further deduction of these expenditures is not allowable over and above the statutory limit prescribed u/s.44C. Ld. DRP upheld the contention of the ld. Assessing Officer.

10. According to the assessee, with respect to telecommunication charges, the same are towards telecom leased line which is specifically for the purpose of the assessee. It cannot be considered as general administrative expense to form part of section 44C limits. For this, assessee referred to the invoices raised on the AE which were paid on behalf of the assessee and were subsequently reimbursed by the assessee to its AE. Said invoice is placed at page 760 of the paper book wherein the particulars mention “reimbursement charges towards telecom leased line connection (Singtel connect + direct link)”. Assessee had furnished additional evidence before the ld. DRP where a remand report was called for. Claim of the assessee is that these are specific expenses relating to the business of the assessee and not in the nature of executive and general administrative expenses.

10.1. With respect to employee related expenses, these were incurred specifically for the expatriate employees working for India branch. These are in the nature of insurance charges, transfer charges and compliance cost etc. These expenses were incurred by the AE specifically for India branch and does not form part of allocation of general and administrative expenses, hence out of purview of section 44C.

10.3. In this regard, reference is made to the decision of Hon’ble Jurisdictional High Court of Bombay in the case of CIT v. Emirates Commercial Bank Ltd. (Bombay) wherein it was observed that the expenditure that was covered u/s.44C is of a common nature which is incurred for various branches or which is incurred for the head office or the branch. Hon’ble Court was concerned with the expenditure exclusively incurred for the branch and thus, held that section 44C had no application. Another decision by the Hon’ble Jurisdictional High Court of Bombay in the case of DIT (International Taxation) v. Oman International Bank S.A.O.G. ITR 151 (Bombay) held that travelling expenses incurred on travelling of head office personnel of foreign bank who had travelled to various Indian branches were allowable u/s. 37(1), section 44C would not apply in such case. Also, a reference is made to the decision of Coordinate Bench of ITAT, Mumbai in the case of Bank of Bahrain and Kuwait v. Asstt. DIT (International Taxation) (Mumbai) wherein it held that direct and exclusive NRI Desk expenses incurred by the head office are to be allowed in full under the provisions of the Act and would not be fettered by section 44C.

11. In the given set of facts and jurisprudence referred above, telecom charges and employee related cost being incurred exclusively in relation to business of India branch are out of the purview of section 44C as the same cannot be held in the nature of executive and general administrative expenses. It is thus, held that deduction of the said expenditure is allowed in entirety under provisions of section 37(1). Addition, so made is thus, deleted. Ground no.5 is allowed.

12. Facts pertaining to ground no.6 mentions that as part of its business, the overseas branches of ANZ had provided short-term loans to ANZ Mumbai. During the year under consideration, ANZ Mumbai paid interest to its overseas branches amounting to Rs.2,98,64,616/-. The said interest was not offered to tax by the assessee in its return of income filed in India given that the same are in the nature of ‘receipt from self.’ Ld. Assessing Officer, in the draft assessment order dated 26.12.2017, referred to the provisions of section 9(1)(v)(c) of the Act and held that the said section provides for a source rule for taxation and that it does not make any distinction about the payee. Further, ld. Assessing Officer held that as per Article 7(1) of the India-Australia DTAA, business income of the assessee is taxable in India only if there exists a PE of the assessee in India within the meaning of Article 5 of the said DTAA. Once the assessee opts to be governed under the beneficial provisions of the DTAA, and it is accepted that the assessee has a PE in India under the DTAA, then the single entity approach of the Act gives way to the distinct and independent entity or separate entity approach under the DTAA. Thus, the interest paid by ANZ Mumbai to the Head Office/ overseas branches of the assessee cannot be said to be payment to self. Ld. DRP vide its directions dated 04.09.2018 upheld ld. Assessing Officer’s contention and directed that interest receivable on short-term loans given to ANZ Mumbai (which is a PE of the assessee) by Head Office/ overseas branches of the assessee is chargeable to tax in India under Article 11(2) of the DTAA.

12.1. Assessee submitted that this issue is concluded in its favour by the decision of Hon’ble Special Bench and Co-ordinate Benches as under:

| i. Sumitomo |

|

Mitsui Banking Corpn. v. Dy. DIT (IT) ITD 66 (Mumbai)(SB) |

| ii. |

|

Credit Agricole Corporate and Investment Bank (supra) |

| iii. |

|

Dy. CIT (IT) v. BNP Paribas S.A. [IT Appeal No 1689/Mum/2018 (Mum), dated 17.07.2019] |

12.2. Ld. DR submitted that decision in the case of Sumitomo Mitsui Banking Corporation (supra) has not been accepted by the Revenue and is under contest before the higher appellate forum.

13. Considering the above stated facts and decision of Hon’ble Special Bench in the case of Sumitomo Mitsui Banking Corporation(supra), interest paid by ANZ Mumbai is not income in the hands of the Head Office/overseas branches of assessee and thus, not chargeable to tax. Further, while Explanation 1 to section 9(1)(v) of the Act states that interest paid by a PE in India to the head office or any other PE shall be chargeable to tax in India, the provisions of the said section are applicable only with effect from 01.04.2016, i.e., from AY 2016-17 and onwards. Ground no. 6 is thus allowed.

14. In the result, appeal of the assessee is allowed.