ORDER

Bhavnesh Saini, Judicial Member.- This appeal by the assessee is directed against the order of learned CIT(A)-II Agra dated 23.10.2013 for A.Y. 2009-10, challenging the impugned order in rejecting the claim of assessee under Section 10A of the I.T. Act before setting off of carried forward loss and unabsorbed depreciation, disallowing deduction/exemption under Section 10A of Interest on FDR, job work charges and earning from foreign exchange rate differences. Learned counsel for the assessee did not press the ground relating to exemption under Section 10A in respect of insurance account amount. This ground is dismissed.

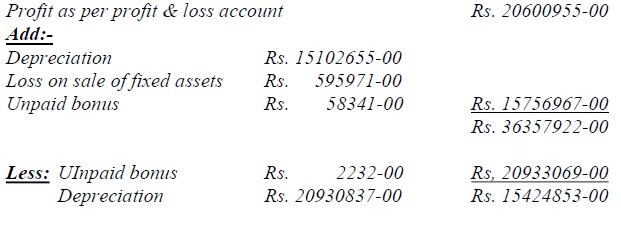

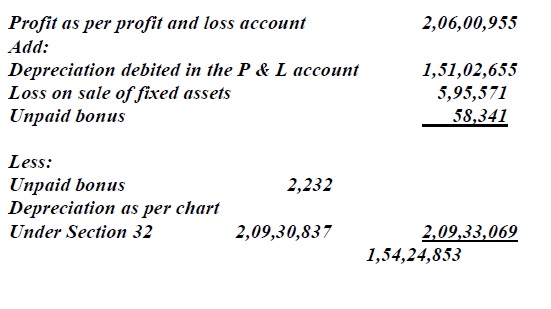

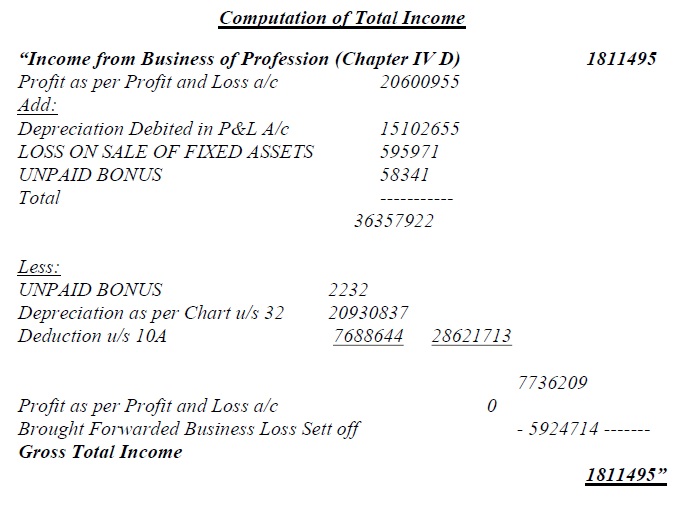

2. Briefly the facts of the case are that in this case, assessment order has been passed under Section 143(3) vide order dated 28.12.2011, determining the assessed income at Rs.93,73,120/- as against the returned income of Rs.18,11,500/- The assessee is enganged in the business of manufacturing and export of silver jewellery operating from a unit located in special Economic Zone at Plot No.94 & 99, Phase-II, Noida and therefore, claiming deduction as per the provision of section 10A of the Act. Along with the return of income, the assessee furnished computation of its total income chargeable to tax as under:-

3. On examination of the computation of total income chargeable to tax as furnished by the assessee along with the return of income as reproduced above, the AO noticed that the assessee has claimed set-off of brought forward losses amounting to Rs.59,24,714/- from the income of the year under consideration after claiming deduction u/s 10A. On examination, the AO found that the assessee is claiming deduction u/s 10A of the Act in A.Y. 2003-04 and incurred losses and also had unabsorbed depreciation in A.Ys. 2003-04 to 2005-06 and thereafter, it had income from A.Ys. 2006-07 to 2008-09 for which, it claimed deduction under Section 10A without setting off the brought forward losses and depreciation. On being questioned for not setting off the brought forward business losses and unabsorbed depreciation of earlier years against the income of A.Y. 2006-07 before claiming deduction under Section 10A, the assessee’s counsel has justified the method of computation of income adopted by the assesse stating that the judicial principle rendered in the context of section conforming deduction under chapter VIA cannot be considered while allowing deduction under Section 10A of the Act because section 10A is placed in chapter III which is as “Income which do not form part of total income”. The assessee counsel submitted before A.O. that even deduction of unabsorbed depreciation under Section 32(2) cannot be given against the income of section 10A because section 32(2) is to be given effect to after the provision of section 72 of the Act are applied and hence, deduction of unabsorbed depreciation provided under Section 32(2) is not to be provided while computing the profit of the undertaking eligible for deduction under Section 10A. In support of his argument, he also relied on sequence of columns made “ITR-6″ prescribed by CBDT for filing of return by the company in which schedule of B/F/set-off of unabsorbed business loss/ unabsorbed depreciation is appearing much after the column provided for claiming deduction under Section 10A in the schedule made for computation of business income. By quoting from the format of ‘ITR-6”, the assessee’s counsel put up his argument before the A.O. that this format is prescribed by the CBDT through its circular and hence, it is binding on Revenue Authorities.

4. After considering the arguments of assessee’s counsel, the A.O. referred to subsection (6) of section 10A which provides for determining the amount of losses and unabsorbed depreciation to be carried forward immediately succeeding the last year of the period for which deduction under Section 10A is availed by the assessee and as provided in this sub-Section for determining such amount of carried forward business loss and unabsorbed depreciation, it is necessary that the notional computation of business income and depreciation as per the provisions of the Act should be made for each year of the period covered by Section 10A by taking into account the provisions of carried forward of loss under Section 72 and unabsorbed depreciation under Section 32(2) of the Act. After discussing in paras 4 and 5 of the assessment order (Page 2 to 4) about the effect of this provision on the computation of total income of the assessee beginning from A.Y. 2003-04 till the assessment year under consideration, the A.O. held that firstly income is to be computed as per Chapter IVD by making deduction for unabsorbed depreciation under Section 32(2) and thereafter, set off of losses under Section 72(1) and then deduction as per section 10A is to be provided. On the basis of above interpretation of sub Section (6) of Section 10A, the A.O. showed that entire losses and unabsorbed depreciation from A.Ys. 2003-04 to 2005-06 (unabsorbed depreciation amounting to Rs.4646/-, Rs.17,22,986/- Rs.1,86,132/-pertaining to A.Ys. 2003- 04, 2004-05 and 2005-06 respectively and unabsorbed losses of Rs.83,360/- and Rs.39,89,128/- pertaining to A.Ys. 2003-04 and 200405 respectively) would get absorbed with the income of Rs.2,87,69,906/- declared by the assessee for A.Y.2006-07 before providing for deduction under Section 10A and hence, he held that the set off of carried forward business loss and unabsorbed depreciation as claimed in the year under consideration is not allowed.

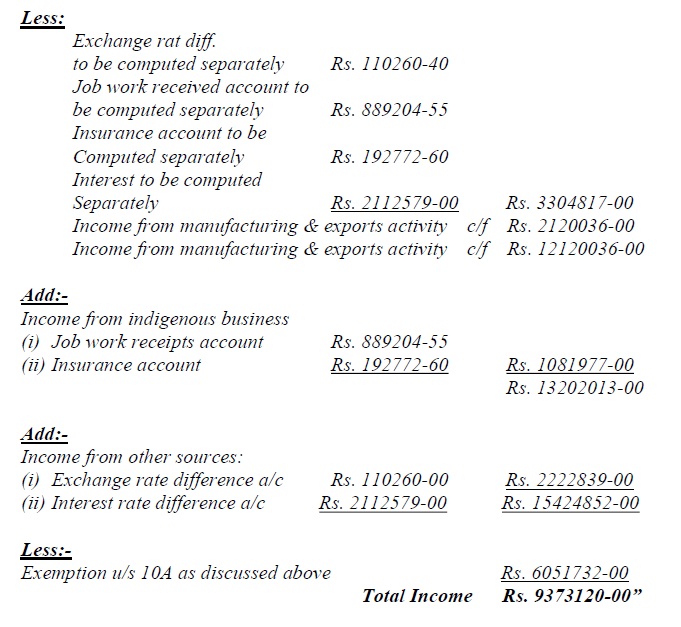

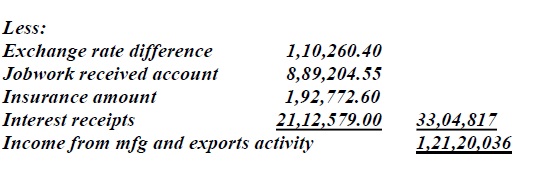

5. For the purpose of determining the income of the assessee is to be covered for deduction under Section 10A, the A.O. also examined nature of certain income viz amount earned on exchange rate difference, job work received, insurance account and interest received on which, the assessee claimed deduction under Section 10A claiming such income earned from the unit located in Special Economic Zone. After examination of nature of these income and considering the submission of the counsel for the assessee as discussed by him in Para 6 of the assessment order, the A.O. held that deduction under Section 10A would not be allowed for these income and income from interest and exchange rate difference would be assessed under the head “Income from other sources”. After excluding this income, the A.O. has computed deduction under Section 10A as under:-

“In view of above discussion, it is held that earnings on exchange rate difference of Rs. 110260-40, job work of Rs.889204-55, Insurance account of Rs.192772-60 and interest of Rs.2112579-00 do not qualify for the purpose of calculating exemption under Section 10A of the I.T. Act and same are being excluded from the manufacturing & export sales of the assessee and considered separately while computing total income of the assessee. Therefore, exempt income under Section 10A of the assessee is computed as under:-

Exemption u/s 10A of the I.T. Act as under:-

6. In view of the discussion taken by the A.O. in the assessment order as discussed above, the taxable income of the assessee is computed as under:

7. The assessee challenged the order of the A.O. before learned CIT(A). However, the learned CIT(A) confirmed the order of the A.O. and dismissed the appeal of the assessee.

8. We have heard learned representatives of both the parties, perused the findings of authorities below and considered the material available on record. The grounds of appeal are decided issue wise as under:-

Issue No.1 (Deduction under Section 10A)

9. The brief facts of the case are that the assessee is engaged in the business of manufacturing and export of silver jewellery. The claim of exemption under Section 10A has not been denied. The A.O. on the ground that set off of brought forward losses should have been adjusted by the assessee in the preceding years relevant to assessment years 2006-07 and 2007-08 has not allowed the claim of set off of brought forward losses. The assessee company claimed deduction under Section 10A of the Act from the profit eligible for the same and remaining profit has been adjusted from the unabsorbed business loss and unabsorbed depreciation brought forward. It is claimed, the working of the deduction under Section 10A is totally different from that of the deduction under chapter VIA. Leaned counsel for the assessee contended that even if it is taken deduction under Section 10A of the Act is to be given effect to after applying section 28 to 44D, the same would be without giving effect to section 32(2) of the Act. This is because Section 32(2) of the Act is to be given effect to after the provisions of Section 72 of the Act are applied. Therefore, the Section 32(2) of the Act are not to be given effect to while computing the profits of the undertaking eligible for deduction under Section 10A of the Act. It is stated, the above submission finds support from the income tax return form itself. In ITR 6 (Return Form of companies), the total of deduction under Section 10A etc. are reported in part A of the schedule BP. The business income after reducing the deduction under Section 10A etc. is reported in column 36 of part A of schedule BP. The schedule of brought forward/set off of unabsorbed business loss/unabsorbed depreciation is being reported in schedule CYLA and BFLA which is much after column 36 of part A of schedule BP and hence in respect of losses to be set of against the business income eligible for deduction under Section 10A of the Act, the starting point is the income from business which remains after allowing deduction under Section 10A of the Act as reported in column 36 of part A of schedule BP. Section 10A deduction is to be allowed separately and independent of computation profit and gains from eligible business without effect unabsorbed depreciation. The learned CIT(A), however, following the decision of Hon’ble Karnatka High Court in the case of

CIT v.

Himatasingike Seide Ltd. [2006] 156 Taxman 151/286 ITR 255 (Kar) and order of ITAT, Delhi Bench in the case of

Global Vantedge (P.) Ltd. v.

Dy. CIT [2010] 37 SOT 1 (Delhi) and considering board circular No.7/2013 dated 16.07.2013 rejected the claim of the assessee. The Hon’ble Karnatka High Court in its latest decision in the case of

CIT v.

Yokogawa India Ltd. [2012] 21

taxmann.com 154/341 ITR 385 (Kar) (dated 09.08.2011) held as under:-

“The assessee was in the business of manufacture and trading of process control instruments. The assessee filed return of income on October 31.2002, declaring a total loss of Rs.5,07,03,098/- The assessee claimed exemption of Rs. 3,95,99,100/- under section 104 for its STP unit. The exemption had been claimed before set off of brought forward losses and depreciation. According to the assessing authority, the deduction under section 10A had to be allowed from the total income of the assessee. The total income of the assessee was arrived at as per section 80B(5). Therefore, the exemption under section 10A had to be given after setting off all brought forward losses within the context of section 32(1) read with section 72(2) of the Act. Accordingly, the section 10A benefit was recomputed. After such recomputation and, after adjusting the assessee was held to be not entitled for exemption under Section 10A and hence a sum of Rs.36,575/- was treated as income from other sources. The Commissioner of Income-tax (Appeals) and the Tribunal held that the income of the section 104 unit had to be excluded before arriving at the gross total income. On appeal to the High Court:

Held, that as the profits and gains under section 10A were not to be included in the income of the assessee at all, the question of setting off the loss of the assessee from any business against such profits and gains of the under taking would not arise. Similarly, as per section 72(2), unabsorbed business loss is to be first set off and thereafter unabsorbed depreciation treated as current year’s depreciation under section 32(2) is to be set off. As the deduction under section 10A has to be excluded from the total income of the assessee, the question of unabsorbed business loss being set off against such profit and gains of the undertaking would not arise.”

9.1 Hon’ble Bombay High Court in the case of

CIT v.

Black & Veatch Consulting (P.) Ltd. [2012] 20

taxmann.com 727/208 Taxman 144 (Mag)/348 ITR 72 (Bom) held as under:-

“Section 10A of the Income-tax Act, 1961, is a provision which is in the nature of a deduction and not an exemption. The deduction under section 10A has to be given effect to at the stage of computing the profits and gains of business. This is anterior to the application of the provisions of section 72 which deals with the carry forward and set off of business losses. A distinction has been made by the Legislature while incorporating the provisions of Chapter VI-A. Section 80A(1) stipulates that in computing the total income of an assessee, there shall be allowed from his gross total income, in accordance with and subject to the provisions of the Chapter, the deductions specified in sections 80C to 80U. Section 80B(5) defines for the purposes of Chapter VI-A “gross total income” to mean the total income computed in accordance with the provisions of Act, before making any deduction under the Chapter. Therefore, the deduction under section 10A has to be given at the stage when the profits and gains of business are computed in the first instance. The Tribunal was right in holding that the deduction under Section 10A in respect of the allowable unit under section 10A has to be allowed before setting off brought forwarded losses of nonsection 10A unit.”

9.2 ITAT Delhi Bench in the case of Solutions Infosystems (P) Ltd. v. ITO [IT Appeal No. 2429 (Delhi) of 2011, dated 12-12-2013] considered the identical question of deduction under Section 10A and following the decision of Hon’ble Karnatka High Court in the case of Yokogawa India Ltd. (supra) upheld the contention of the assessee and appeal of the assessee was allowed (copy filed in the paper book).

9.3 ITAT, Banglaore Bench in the case of

KPIT Cummins Infosystems (Bangalore) (P.) Ltd. v.

Asstt. CIT [2008] 26 SOT 529/120 TTJ 956 (Bang) held as under:-

“Conclusion Sec 10A relief is to be allowed without first setting off unabsorbed depreciation of earlier years.”

10. Considering the facts of the case in the light of the above decisions it is clear that the claim of the assessee under Section 10A should have been allowed by the A.O. as it is on income shown in the return of income. Learned CII(A) Circular column No. 7/2013 (supra) in the appellate order which was considered adverse in nature against the assessee. In Para 20.2 of the said circular, provides that assessee would be entitled for the relief claimed in the appeal and it provides “with a view to rationalize the existing tax incentives in respect of such units, sub-section (6) in sections 10A and 10B has been amended to do away with the restrictions on the carry forward of business losses and unabsorbed depreciation”. We may also note here that earlier decision of the Karnatka High Court in the case of Himatasingike Seide Ltd. (supra). However, the latest decision of Hon’ble Karnatka High Court in the case of Yokogawa India Ltd. (Supra) Is dated 09.08.2011 and thus would supersede the earlier judgment of the same High Court. The decision of the Hon’ble Bombay High Court in the case of Black & Veatch Consulting (P.) Ltd. (supra) dated 09.04.2012. These judgments deal with the direct proposition involved in appeal with regard to deduction under Section10A of the Act. Conisdering the facts of the case in the light of the above judgments directly on the point, we are of the view, learned CIT(A) was not justified in rejecting the claim of the assessee. The decision of ITAT Delhi Bench in the case of Global Vantedge (P.) Ltd. (supra) cannot be given preference against the judgment of the High Courts who have also followed the earlier decision of Karnatka High Court in rejecting the claim of the assessee. Following the above decision, reproduced above, we set aside the orders of the authorities below. The A.O. is directed to allow set off of carry forward losses and unabsorbed depreciation of earlier years during the year in appeal as claimed in the return i.e. deduction under Section 10A be allowed before setting off of carry forward losses and ubabsorbed depreciation. This issue is, therefore, decided in favour of the assessee.

Issue No.2 (Exemption under Section 10A on interest of FDR)

11. The assessee challenged the decision of A.O. holding that the interest amounting to Rs.21,12,579/- earned on FDR given by the assessee to the Bank of Nova Scotia as security against the metal purchased does not quality for exemption under Section 10A of the Act. It was also contended that A.O. has erred in not providing the netting benefit of interest cost incurred by the assessee. The assessee contended before learned CIT(A) that assessee company is a manufacturer and exporter of silver jewellery. For manufacturing, the metal is taken from Bank of a Nova, Scotia for which FDR’s is given to them as security against the metal purchased on loan basis. The FDRs are given as security under compulsion to carry out the business activity, the FDRs have direct nexus with the business requirement and hence, the interest on FDRs is directly incidental to the business income. The assessee relied upon the decision of different Bench of the Tribunal in support of the contention. The A.O. in the remand report disputed the claim of assessee. The learned CIT(A) did not find any dispute on the fact that this interest income is earned by the assessee on FDR given to the Bank of Nova Scotia as security against the metal purchased by it on loan basis. The learned CIT(A), however, relied upon the decision of the Hon’ble Supreme Court in the case of

Liberty India v.

CIT [2009] 183 Taxman 349/317 ITR 218 (SC) and order of the ITAT, Delhi Bench in the case of

Global Vantedge (P.) Ltd. (supra) rejected the claim of the assessee and deduction under Section 10A was denied to the assessee. The facts are not in dispute that the assessee purchased metal from Bank of Nova Scotia for business purposes of manufacturing the jewellery. Therefore, for the purpose of export business the FDRs are given security under compulsion to carry out business activity. Ld. Counsel for the assessee relied on following decisions:

| (i) |

|

. ITAT, Mumbai Bench in the case of Livingstones Jewellery (P.) Ltd. v. Dy. CIT [2009] 31 SOT 323 (Mum-Trib). |

| (ii) |

|

. ITAT, Delhi Bench in the case of Samtex Fashions Ltd. v. Asstt. CIT [2005] 92 ITD 535 (Delhi-Trib). |

| (iii). |

|

The Hon’ble Delhi High Court in the case of CIT v. Jaypee DSC Ventures Ltd. [2012] 17 taxmann.com 257/204 Taxman 169 (Mag)/[2011] 335 ITR 132 (Delhi). |

12. It is a fact that the assessee has not provided complete details on this issue before the authorities below. Therefore, the matter requires reconsideration at the level of the A.O. We, accordingly, set aside the orders of the authorities below and restore this issue to the file of A.O. with direction to redecide this issue, in accordance with law, by discussing the complete facts and by giving sufficient opportunity of being heard to the assessee. In view of above, we are not expressing our view on above decisions.

Issue No.3 (Exemption under Section 10A on job work charges.)

13. The A.O. similarly held that income from job work charges not to qualify for deduction under Section 10A of the Act. The learned CIT(A) confirmed the order of the A.O. and dismissed the appeal of the assessee. The assessee submitted before A.O. that job work charges were received for manufacturing of jewellery for others on job work basis which were the operational income of the assessee. The assessee relied upon the decision of the Hon’ble Delhi High Court in the case of

CIT v.

Lovlesh Jain [2011] 16

taxmann.com 366/[2012] 204 Taxman 134 (Delhi) The assessee also relied upon unreported decision of Hon’ble Delhi High Court in the case of Jayshree Gems Jewellery dated 03.02.2014. The AR also relied on the order of ITAT, Mumbai Bench in the case of

Inter Classic Jewellery (I) (P.) Ltd. v.

ITO [2010] 37 SOT 4/114 TTJ 402 (Mum-Trib) (URO).

14. It is a fact that the assessee has not provided complete details on this issue before the authorities below. Therefore, the matter requires reconsideration at the level of the A.O. We, accordingly, set aside the orders of the authorities below and restore this issue to the file of A.O. with direction to redecide this issue, in accordance with law, by discussing the complete facts and by giving sufficient opportunity of being heard to the assessee. In view of above, we are not expressing our view on these decisions.

15. In the result, this ground of appeal of the assessee is allowed for statistical purpose.

Issue No.4 (Exemption under Section 10A on earning from interest rate difference)

16. It was submitted before A.O. that the exchange rate difference gain arises due to fluctuation in the dollar exchange rate, which is an integral part of export sales and eligible for deduction under Section 10A of the Act. The A.O., however, noted that a sum of Rs.1,10,260 is in respect of income related to foreign currency rate fluctuation kept by the assessee in EEFC (currency account) and not related to any sale proceed, therefore, exemption under Section 10A of the Act was denied and was considered as income from other sources. The assessee reiterated the same submissions before learned CIT(A) and relied upon the decision of Hon’ble Madras High Court in the case of

CIT v.

Pentasoft Technologies Ltd. [2013] 33

taxmann.com 570/[2012] 347 ITR 578 (Mad) in which it was held as under :-

“In order to allow a claim under section 104 of the Income-tax Act, 1961, what is to be seen is whether such benefit earned by the assessee was derived by virtue of export made by the assessee. When fluctuation in foreign exchange rate was solely relatable to the export business of the assessee and the higher rupee value was earned by virtue of such exports carried out by the assessee, the benefit of section 104 should be allowed to the assessee.”

16.1 Hon’ble High Court also noted that “therefore, when the fluctuation in foreign exchange rate was solely relatable to the export business of the assessee and the higher rupee value was earned by virtue of such exports carried out by the assessee, there is no reason why the benefit of section 10A of the Act should not be allowed to the assessee.” The authorities below, however, denied the claim of assessee because the income related to foreign currency rate fluctuation kept in EEFC (currency account) and not related to any sale proceeds received during the year under consideration. The authorities below have forgot to note that the assessee is in business of manufacturing and export of silver jewellery and deduction under Section 10A have been allowed to the assessee. The assessee would earn valid currency only on making export sales and the export sale proceeds would be kept in EEFC (currency account only). No other amount could be kept in such account. When the sale proceeds are kept in this account and there is difference in the rate, it would amount to income arises out of export business only. The authorities below were, therefore, not justified in rejecting the claim of the assessee. The issue is squarely covered in favour of the assessee by judgment of Hon’ble Madras High Court in the case of Pentasoft Technologies Ltd. (supra). We, accordingly, set aside the orders of authorities below and direct the A.O. to allow deduction under Section 10A on this amount.

17. In the result, this ground of appeal is allowed.

18. In the result, appeal of the assessee is partly allowed as indicated above.

PER PRAMOD KUMAR, ACCOUNTANT MEMBER

19. I have carefully perused the final draft order proposed by the learned judicial member and I have had the benefits of several rounds of discussions with him on this but we could not reach a consensus on the proposed order of the bench, and therefore I am writing this separate order

20. Briefly stated the relevant material facts of the case are like this. The assessee before us is engaged in the business of manufacturing and export of silver jewellery During the course of the assessment proceedings, the Assessing Officer noticed that the assessee has claimed a set off of brought forward of business losses amounting to Rs 59,24.714 after claiming the deduction under section 10A. There is no dispute that these brought forward losses were in respect of the same unit as evident from the following chart set out in the assessment order itself:

| Assessment Year |

Profit/ (-) Loss |

Business loss |

Unabsorbed depreciation |

Exemption claimed under section 10A |

| 2003-4 |

(-)88,007 |

83,360 |

4,646 |

NIL |

| 2004-5 |

(-)57,12,114 |

39,89,127 |

17,22,986 |

NIL |

| 2005-6 |

(-)1,86,133 |

NIL |

1,86,133 |

NIL |

| 2006-7 |

2,87,69,906 |

NIL |

NIL |

2,85,17,203 |

| 2007-8 |

2,92,18,044 |

NIL |

NIL |

2,76,50,745 |

| 2008-9 |

1,27,92,585 |

NIL |

NIL |

93,74,988 |

The Assessing Officer was of the view that the exemption under section 10A is to be computed after setting off his brought forward business loss and unabsorbed depreciation. He was, in substance of the view that if the assessee had done so, nothing would have remained available for set off in the present year This is evident from the following observations made at page 3 and 4 of the assessment order.

……….the unabsorbed depreciation amounting to Rs 4.646, Rs 17.22.986 and Rs 86. 132 pertaining to the assessment years 2003-04. 04-05 and 0506 should have been deducted from the income of Rs 28.76.990 shown in the assessment year 2006-07 If such an adjustment is made, there remains no unabsorbed depreciation for set off with the income of the year under consideratione 2009-10 In such circumstances, there appears to be no justification to deduct the amount of unabsorbed depreciation for the assessment year 2003-04, 2004-05 and 2005-06 amounting to Rs 19.13,764 from the current year’s income. Hence the set off of this unabsorbed depreciation is not allowed from the income of the year under consideration.

Assessee (had an) income of Rs 2.87.69.906 in the assessment year 200607. Since the loss of Rs 40.72.488 pertaining to the two years i.e. 2003-04 and 2004-05 was liable to be set off from the income of the assessment year 2006-07, there appears to be no reason to set off the same from the income of the year under consideration de 2009-10 Hence, set off of business loss, as claimed, in the year under consideration is disallowed.

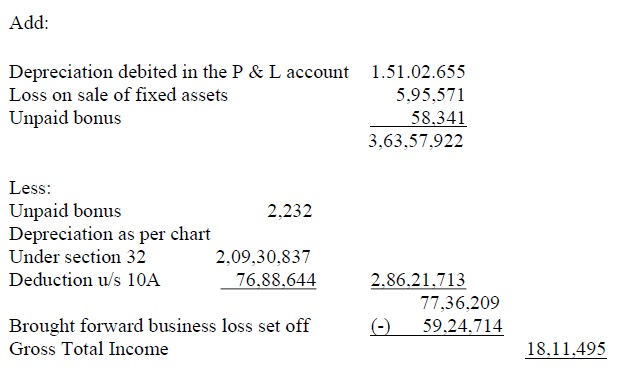

21 It was in this backdrop that correctness of the following computation of income, as given by the assessee, was called into question:

22. The Assessing Officer had also noticed that the assessee had claimed exemption under section 10 A in respect of interest income and job work income as well. The Assessing Officer was of the view that these two types of income were not eligible for exemption under section 10 A, and in support of this stand. in the assessment order, the Assessing Officer opined as follows:

Since the interest on FDR, given by the assessee to the Bank of Nova Scotia as security deposit against the metal purchase on loan basis, is not a profit earned from the business of export of silver jewellery, hence the same does not qualify for deduction under section 10A of the Act. As such, the deduction on this amount cannot be allowed to the assessee.

Similarly, income from job work charges cannot be held to be income attributable to the business of manufacturing and exports. The ssessee has done job work in respect of indigenously and it does not have any concern with export business. Therefore, exemption under section 10 A of the Act is also not available to this income It is worthwhile to mention here that the sub section 1A of Section 10A clearly speaks of the provisions of Section 10A of the Act becoming applicable only in respect of manufacturing and export of things or articles. Hence, the income under this section cannot be allowed on the income earned on account of job work

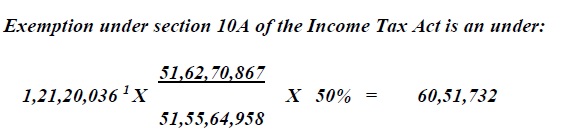

23. The Assessing Officer also did not accept assessee’s contention to the effect that the amounts received in respect of exchange rate difference (Rs 1,10, 260) and insurance claim receipt (Rs 1,92,772) was also includible in income eligible for exemption under section 10A. It was in this backdrop that the Assessing Officer recomputed the exemption under section 10A as follows:

1 As regards the quantum of business profits eligible for exemption under section 10A at Rs. 1,21,20,036, the same was computed as follows:

24. In effect thus the admissibility of exemption under section 10A was restricted to Rs 60.51.732. as against claim made by the assessee for Rs 76.88.644 In addition to so restricting the claim, set off of the business loss of Rs 59.24,714 was declined. As against a returned income of Rs 18.11.500, the assessed income was computed at Rs 93.73,120 Aggrieved by the assessment so framed by the Assessing Officer, the assessee carried the matter in appeal before the learned CIT(A) but without any success. Learned CIT(A), in a very detailed and erudite order with which we will deal a little later confirmed the assessment order The assessee is still not satisfied and is in second appeal before this Tribunal

On set off of the unabsorbed depreciation and business losses carried forward in respect of the same unit eligible for exemption under section 10 A

25. In order to deal with this issue, it could perhaps be desirable to bear in mind the fact that right now we are dealing with the year in which set off of the carried forward losses is claimed whereas what the Assessing Officer has actually ended up dealing with quantification of the losses, eligible for carry forward, in the assessment years in which these losses are claimed to have arisen. As to whether or not the Assessing Officer was indeed eligible for doing so, it is useful to take a look at the landmark judgment of Hon’ble Supreme Court in the case of

CIT v.

Manmohan Das (Deceased) [1966] 59 ITR 699 (SC) That was a case in which one of the questions which fell for consideration of Hon’ble Supreme Court was as follows

Whether the assessee could claim a set off of the loss suffered by him in the preceding year 1950-51 against his profits in the year under consideration, e. 1951-52 having failed to prefer an appeal against the refusal by the ITO making the assessment for the year 1950-51 to allow the assessee to carry forward the loss under s. 24(2) of the Act?”

26. Dealing with this question, Their Lordships, inter alia, opined as follows

The .. question presents little difficulty. In making his order of assessment for the year 1950-51. the ITO declared that the loss computed in that year could not be carriedforward to the next year under s. 24(2) of the IT Act, as it was not a business loss. The ITO has under s. 24(3) to notify to the assessee the amount of loss as computed by him, if it is established in the course of assessment of the total income that the assessee has suffered loss of profits Sec. 24(2) confers a statutory right (subject to certain conditions which are not material) upon the assessee who sustains a loss of profits in any year in any business, profession or vocation to carry forward the loss as is not set off under sub-s (1) to the following year, and to set it off against his profits and gains if any, from the same business, profession or vocation for that year Whether the loss of profits or gains in any year may be carried forward to the following year and set off against the profits and gains of the same business, profession or vocation under s. 24(2) has to be determined by the ITO who deals with the assessment of the subsequent year. It is for the ITO dealing with The assessment in the subsequent year to determine whether the loss of the previous year may be set off against the profits of that year A decision recorded by the ITO who computes the loss in the previous Year under s. 24(3) that the loss cannot be set off against the income of the subsequent year is not binding on the assessee. (Emphasis by underlining supplied by me)

27 The law so laid down by Hon’ble Supreme Court has been followed by various coordinate benches of this Tribunal from time to time, including in the cases of

Asstt. CIT v.

M.K. Chatterjee [2003] 86 ITD 90 (Kol-Trib),

Daimler Chrysler India (P.) Ltd. v.

Dy. CIT [2009] 29 SOT 202 (Pune-Trib) and a number of other decisions.

28 In the case of

CIT v.

Khushal Chand Daga [1961] 42 ITR 177 (SC). Hon’ble Supreme Court had an occasion to deal with the question whether “the assessee was competent in law to raise a question with regard to the determination of loss for the asst yr 1941-42 as finally determined in appeal. in the course of proceedings for the asst. yr. 1942-43 when the loss brought forward from 1941-42 was being set off. That was thus a case in which the assessee sought to challenge quantification of loss at the time of setting off the same against subsequent profits Hon’ble Supreme Court did decide the issue in favour of the assessee but on a technical point of lapse on the part of the Assessing Officer to have notified the quantum of loss quantified. Their Lordships, in this background observed as follows.

As regards (this) question, the only contention raised was that the loss which had been determined and ordered to be carried forward must be deemed to have become final, because no appeal was filed against the determination. But it appears that the procedure laid down by s 24(3) under which the ITO has to notify to the assessee by order in writing the amount of the loss as computed by him for the purposes of that section was not followed No doubt, under s. 30 an appeal lies. if the assessee objects to the amount of loss computed and notified under s 24, but in as much as the ITO has not notified the loss computed by him by order in writing an appeal could not be taken on that point in our opinion, the assessee was, therefore, entitled to have the loss re-determined in a subsequent year

29. Summarizing the impact of the law so laid down, Hon’ble Bombay High Court, in the case of

Western India Oil Distributing Co. Ltd. v.

CIT [1980] 126 ITR 497 (Bom), have, inter alia, observed as follows

This decision would suggest, although we express no final opinion on the point that if the quantification of loss is properly made and duly notified by following the prescribed procedure, such quantification may be impressed with the principle of finality if the matter is not carried further. However, the principle of finality as may be applicable to the question of quantification of the amount of loss does not appear to be applicable to the determination of the source of income and the decision whether the loss can or cannot be allowed to be carried forward by reason of the determination of the source. This is the clear result of the decision of the Supreme Court in Manmohan Das’ case (supra)

(Redundant portion highlighted by strikethrough characters, there does not seem to be any such statutory requirement for notification of loss at present)

30. It would thus appear to me that so far as the computation of losses to be carried forward and set off of such losses against the future profits is concerned, the scheme of the Income Tax Act is like this. The quantification of loss suffered in an year is to be determined by the Assessing Officer having jurisdiction over the assessment years in which the loss has actually arisen but it is not for him to decide whether the losses so quantified are actually eligible for set off against the profits of a subsequent year in which profits arise. That call, in accordance with the scheme of the Income Tax Act, is to be taken by the Assessing Officer having jurisdiction over the assessment year in which set off is claimed by the assessee. To illustrate, if losses are incurred in the years a, b and c and the set off of the losses so incurred is claimed in the years x, y and z, so far as the quantum of losses actually incurred in year a, b and c is to be decided in the assessment or reassessment proceedings for the respective years but whether the losses so incurred are eligible for set off against the incomes of the assessment years x, y and z, that call can only be taken in the assessment proceedings of the respective assessment years x, y and z. It appears to me that so far as quantification of business losses and unabsorbed depreciation in the respective assessment years is concerned, the matters have reached finality as the claims made by the assessee have not been disturbed. However, in my considered view, all these relevant factual aspects need to be examined and analyzed properly and there should be no scope for drawing any half baked inferences in this regard.

31. Viewed in this perspective and for this short reason alone, the very foundation of Assessing Officer’s action in denial of set off of the losses quantified and assessed in preceding assessment years, seems to be prima facie devoid of any legally sustainable merits However, as this aspect of the matter has not been taken up by any of the parties at all nor did my brother, the Presiding Officer of this bench, consider it appropriate to put this issue to the parties under proviso to rule 11 of the Appellate Tribunal Rules 1963, I am unable to do anything beyond just stating it and leaving it at that In the event, however, of this course of action being adopted, all my subsequent observations qua first issue in this appeal may end up being rendered purely academic and infructuous. However, for the sake of completeness and with this rider. I must deal with the matter on merits as well

32. On merits of the question as to whether or not the business losses and unabsorbed depreciation carried forward should be set off first and then, on the net amount so computed, the amount eligible for exemption under section 10 A should be computed, there have been many twists and turns by the coordinate benches and the legal positions is much less than, contrary to what has been concluded in the lead order, settled in favour of the assessee Of course, now that Hon’ble Supreme Court has dismissed civil appeal against Hon’ble Karnataka High Court’s decision in the case of

Himatasingike Seide Ltd. (supra), the law so laid down by Hon’ble Karnataka High Court has received finality but conflicting views were expressed by the co-ordinate benches of this Tribunal before this judicial development There is an order of the Tribunal on this issue in favour of the assessee, but as we will see a little later, in a subsequent order, the Tribunal having one of its authors in the coram, abandoned that stand and followed the jurisdictional High Court judgment, which held the issue against the assessee, and stated that perpetuating a mistake is no heroism There is also another decision on this issue in favour of the assessee but then the coordinate bench, in that case, were oblivious of and the coordinate bench stated so in so many words, any other decisions against the assessee including, it seems decision of Hon’ble Karnataka High Court in the case of

Himatasingike Seide Ltd. (supra). As to what is binding nature of these decisions from the coordinate benches, I can do no better than to refer to the following observations made by another bench in the case of

J.K.T. Fabrics (P.) Ltd. v.

Dy. CIT [2005] 4 SOT 84 (Mum-Trib).

8. As to what should be the binding effect of a per incurium decision, we can do no better than to quote the Hon’ble Andhra High Court in the case of

CIT v.

B.R Constructions (1993) 113 CTR (AP) (FB) 1

(1993) 202 ITR 222 (AP) (FB). In his inimitable style. Justice S.S.M. Quadri (as he then was) has articulated the views of the Full Bench of Hon’ble Andhra Pradesh High Court as follows:

“In a country like ours which is governed by rule of law law has to be certain and uniform which is fundamental to the rule of law In Mamleshwar v. Kanahaiya Lal AIR 1975 SC 907, Krishna lyer. J., speaking for the Supreme Court, observed.

‘Certainty of the law, consistency of rulings and comity of Courts all flowering from the same principle converge to the conclusion that a decision once rendered must later bind like cases

In this concurring judgment in State of U.P v. Synthetics & Chemicals Ltd (1991) 4 SCC 139, 163, the observation of Sahai. Jon this aspect is:

‘Uniformity and consistency are the core of judicial discipline.’

That is why the doctrine of stare decisis is part of our judicial system This doctrine means to abide by former precedents’ Blackstone elucidated the doctrine thus

‘For it is an established rule to abide by former precedents. where the same points come again in litigation as well as to keep the scale of justice even and steady and not liable to waiver with every new Judge’s opinion, as also because the law in that case being solemnly declared and determined, what before was uncertain and perhaps indifferent, is now become a permanent rule, which it is not in the breast of any subsequent Judge to alter or vary from, according to his private sentiment.

The ratio decidendi of a judgment is a binding precedent The hierarchy of authority with regard to binding precedent is summed up in para 28 at p. 158 of Salmond on Jurisprudence, Twelfth Edition, as follows

‘The general rule is that a Court is bound by the decision of all Courts higher than itself. A High Court Judge cannot question a decision of the Court of Appeal, nor can the Court of Appeal refuse to follow judgments of the House of Lords. A corollary of the rule is that the Courts are bound only by decisions of higher Courts and not by those of lower or equal rank. A High Court Judge is not bound by a previous High Court decision, though he will normally follow it on the principle of judicial comity, in order to avoid conflict of authority and to secure certainty and uniformity in the administration of justice. If he refuses to follow it, he cannot overrule it, both decisions stand and the resulting antimony must wait for a higher Court to settle.

The principles applicable to Courts in India were laid down by Subba Rao, J (as he then was) in Dr KC. Nambiar v. State of Madras AIR 1953 Mad 351 which were approved by a Full Bench of our High Court in Subbarayudu v. State AIR 1955 AP 87 (FB) (1955) 11 ALT (Cr.) 53. They are as follows

‘A single Judge is bound by a decision of a Division Bench exercising appellate jurisdiction. If there is a conflict of Bench decisions, he should refer the case to a Bench of two Judges who may refer it to a Full Bench. A single Judge cannot differ from a Division Bench unless a Full Bench or the Supreme Court overruled that decision specifically or laid down a different law on the same point. But he cannot ignore a Bench decision, as I am asked to do on the ground that some observations of the Supreme Court made in different context might indicate a different line of reasoning. A Division Bench must ordinarily respect another Divisional Bench of coordinate jurisdiction but if it differs, the case should be referred to a Full Bench. This procedure would avoid unnecessary conflict and confusion that otherwise would prevail

The effect of binding precedents in India is that the decisions of the Supreme Court are binding on all the Courts Indeed. Art. 141 of the Constitution embodies the rule of precedent. All the subordinate Courts are bound by the judgments of the High Court A single Judge of a High Court is bound by the judgment of another single Judge and a fortiori judgments of Benches consisting of more Judges than one. So also, a Division Bench of a High Court is bound by judgments of another Division Bench and Full. A single Judge or Benches of High Courts cannot differ from the earlier judgments of co-ordinate jurisdiction merely because they hold a different view on the question of law for the reason that certainty and uniformity in the administration of justice are of paramount importance. But, if the earlier judgment is erroneous or adherence to the rule of precedents results in manifest injustice, differing from the earlier judgment will be permissible. When a Division Bench differs from the judgment of another Division Bench, it has to refer the case to a Full Bench A single Judge cannot differ from a decision of a Division Bench except when that decision or a judgment relied upon in that decision is overruled by a Full Bench or the Supreme Court, or when the law laid down by a Full Bench or the Supreme Court is inconsistent with the decision.

It may be noticed that precedent ceases to be a binding precedent:

(i) if it is reversed or overruled by a higher Court.

(ii) when it is affirmed or reversed on a different ground

(iii) when it is inconsistent with the earlier decisions of the same rank.

(iv) when it is sub silentio, and

(v) when it is rendered per incuriam

In para 578 at p. 297 of Halsbury’s Laws of England, Fourth Edition, the rule of per incuriam is stated as follows

A decision is given per incuriam when the Court has acted in ignorance of a previous decision of its own or of a Court of coordinate jurisdiction which covered the case before it, in which case it must be decided which case to follow, or when it has acted in ignorance of a House of Lords decision, in which case it must follow that decision, or when the decision is given in ignorance of the terms of a statute or rule having statutory force

In Punjab Land Development & Reclamation Corpn. Ltd. v. Presiding Officer, Labour Court (1990) 3 SCC 682 (1990) 77 FJR 17 (SC), the Supreme Court explained the expression per incuriam’ thus

The Latin expression per incuriam means through inadvertence. A decision can be said generally to be given per incuriam when the Supreme Court has acted in ignorance of a previous decision of its own or when a High Court has acted in ignorance of a decision of the Supreme Court

As has been noticed above, a judgment can be said to be per incuriam if it is rendered in ignorance or forgetfulness of the provisions of a statute or a rule having statutory force or a binding authority. But, if the provision of the Act was noticed and considered before the conclusion arrived at, on the ground that it has erroneously reached the conclusion the judgment cannot be ignored as being per incuriam. In Salmond on Jurisprudence, Twelfth Edition, at p. 151, the rule is stated as follows: The mere fact that (as is contended) the earlier Court misconstrued a statute, or ignored a rule of construction, is no ground for impugning the authority of the precedent A precedent on the construction of a statute is as much binding as any other. and the fact that it was mistaken in its reasoning does not destroy its binding force

In Choudhry Bros v. CIT (1987) 60 CTR (AP) 151 (1986) 158 ITR 224 (AP) , as noticed above, the Division Bench treated the judgment in Ch. Atchaiah v. ITO (1979) 116 ITR 675 (AP) , as per incuriam on the ground that the earlier Division Bench did not notice the significant changes the charging s. 3 has undergone by the omission of the words or the partners of the firm or the members of the association individually. In our view, this cannot be a ground to treat an earlier judgment as per incuriam. The change in the provisions of the Act was present in the mind of the Court which decided Ch Atcharah’s case (supra) Merely because the conclusion arrived at on construing the provisions of the charging section under the old Act as well as under the new Act did not have the concurrence of the latter Bench, the earlier judgment cannot be called per incuriam.

Though a judgment rendered per incuriam can be ignored even by a lower Court, yet it appears that such a course of action was not approved by the House of Lords in Cassell & Co Ltd v. Broome (1972) 1 All ER 801, wherein the House of Lords disapproved the judgment of the Court of Appeal treating an earlier judgment of the House of Lords as per incurium. Lord Hailsham observed

‘It is not open to the Court of Appeal to give gratuitous advice to Judges of first instance to ignore decisions of the House of Lords in this way’.

It is recognised that the rule of per incuriam is of limited application and will be applicable only in the rarest of rare cases Therefore, when a learned single Judge or a Division Bench doubts the correctness of an otherwise binding precedent, the appropriate course would be to refer the case to a Division Bench or Full Bench as the case may be, for an authoritative pronouncement on the question involved as indicated above. The abovesaid two questions are answered as indicated above.”

9. It is thus beyond dispute that a decision which is per incuriam is not a binding judicial precedent. It is also well-settled that when it is not open to a High Court Bench to differ from the decision of a Bench of equal strength, it cannot also be open to a Bench of this Tribunal to differ from the view taken by a co-ordinate Bench of equal strength The only option in case one doubts the correctness of such a decision is to refer the matter for constitution of a larger Bench A decision ignoring this rule of precedent, which is duly approved by the Hon’ble Courts from time to time, cannot but be viewed as per incuriam. Therefore, following the Hon’ble Andhra Pradesh High Court Full Bench decision in the case of B.R. Constructions (supra), such a decision of the co-ordinate Bench has no precedence value.

33. It is not necessary for anyone to even deal with the aspect as to whether or not the two Tribunal decisions are indeed per incuriam, as learned authors themselves have been gracious enough to feel that it was an inadvertent mistake and state that there is no heroism in perpetuating a mistake in one case, and to accept that ‘no contrary decision’ on the issue was cited before them another case whereas another division bench, as we will see in the immediately following paragraph, has opined that the issue is covered against by a binding judicial precedent from Hon’ble Karanataka High Court in the case ofHimatasingike Seide Ltd. (supra) as was also the opinion of another division bench in the case of Global Vantedge (P.) Ltd. (supra) and which was confirmed in an unreported decision dated 19th September 2013 of Hon’ble Supreme Court -a fact not brought to the notice of the coordinate bench

34. The first Tribunal decision relied upon by the learned counsel is a coordinate bench decision in the case of KPIT Cummins Infosystems (Bangalore) (P.) Ltd. (supra) This decision, however, has not been followed by other coordinate benches even when one of the Members on the coram of the said bench was on the coram of the subsequent coordinate bench which disapproved the said decision In the case of Intellinet Technologies India (P.) Ltd. v. ITO [2010] 134 TTJ 744/5 ITR (Trib) 96 (Bang-Trib), a coordinate bench of the Tribunal has summed up the position as follows:-

18 It is true that Tribunal. Bangalore Benches have passed a series of orders accepting the arguments of the assessees holding that it is not necessary to set off the brought forward losses and unabsorbed depreciation of the earlier assessment years in working out the deduction available under s 10A. As rightly pointed out by the learned chartered accountant appearing for the assessee, Tribunal, Chennai Special Bench has also taken the very same view. The titles of those cases have already been mentioned elsewhere in this order

19. But de hors all these Tribunal orders, there is a binding judgment of the Hon’ble jurisdictional High Court available before us which has been rendered by their Lordships in the case of CIT v. Himatasingike Seide Ltd . (supra). Their Lordships examined the contention whether the deduction available to an assessee under s 108 has to be allowed before setting off unabsorbed depreciation and unabsorbed investment allowance. After examining the framework of law dealing with exemption under s. 108, their Lordships held that s. 108 cannot be read in isolation of other provisions. This is only an exemption provision The Court went on to explain that after taking into consideration the unabsorbed depreciation, an assessee may get exemption but to a lesser extent and nonetheless it could not take only a portion of the depreciation just to suit its income for the purpose of nil liability and adjust the balance of unabsorbed depreciation against other business income. The ratio laid down by the Hon’ble High Court of Karnataka is equally applicable to the provisions of law contained in s. 10A as well The intent and purpose of the scheme of exemption provided in ss. 10A and 10B are analogous and obviously the judgment of the Hon’ble Karnataka High Court rendered in the context of s 108 is equally applicable to s. 10A

20. The Tribunal, Delhi “C” Bench has followed the said judgment of the Karnataka High Court in deciding the matter against the assessee, in the case of Global Vantedge (P) Ltd. v. Dy. CIT (supra). While dealing with the said appeal, the Tribunal has in paras 41 and 42 of their order considered all the earlier orders of the Bangalore Bench and other decisions in favour of the assessee and has held that the relevance of those decisions do not have any binding effect when the judgment of a High Court is available on the issue

21 At the time of passing the assessment order, it is possible to argue that the decisions were available before the AO both in favour of the assessee and in favour of the Revenue Therefore, as rightly argued by the learned chartered accountant, the view adopted by the AO is one of the possible views. The general law on the question of revisional jurisdiction is that an order passed by the assessing authority cannot be held to be erroneous, if the officer has followed one of the possible views on the subject But this principle by and large applies to questions of fact When it comes to questions of law the law laid down by the competent constitutional Courts has to be invariably followed. It is a settled law that when the Hon’ble Supreme Court or a High Court declares the law on a subject, the declaration goes back to the date of enactment of that particular law so as to state that the law from the date of its enactment itself was in the manner decided by the Court subsequently When that universal rule of interpretation is accepted, we have to hold that unabsorbed depreciation and brought forward losses have to be set off against the profits while computing the deduction under s. 10A and this position of law has to be reckoned from the date of the enactment of the law itself Therefore, the necessary finding is that even when the AO was passing the assessment order, the law on the subject of exemption available under s. 10A was always the law as explained by the Hon’ble High Court in the case of CIT v. Himatasingike Seide Ltd (supra) Once the law on the subject has been declared by the High Court, the pronounced judgment dates back to the date of enactment and, therefore, by superimposition made by the judicial pronouncement, the assessment order has become erroneous It is not only erroneous, but also prejudicial to the interests of Revenue in as much as the error has contributed in granting excessive relief to the assessee.

22. We also accept the arguments of the learned CIT on the question whether the issue was sub judice before the CIT(A) at the time of passing the revision order and reject the contention of the assessee.

23. It is not out of context here. to refer to the decision of the Tribunal, Bangalore Bench rendered in the case of KPIT Cummins Infosystems (Bangalore) (P) Ltd. v. Asstt. CIT (supra) In the said decision, the Tribunal has held in favour of the assessee, accepting the argument that brought forward loss/unabsorbed depreciation need not be set off against profits eligible for deduction under s. 10A. In fact, one of us was a party to that order. But, in the course of arguments, we found that the said order might not be reflecting the correct position of law We have no hesitation to state so, as we do not believe that perpetuating a mistake is heroism

24. Therefore, in the facts and circumstances of the case, we hold that by virtue of the supervening intervention on the declaration of law, made by the Hon’ble Karnataka High Court in the case of Himatasingike Seide Ltd (supra), the assessing authority has erred in giving exemption under s. 10A before setting off the brought forward losses and unabsorbed depreciation of earlier assessment years.

35. In the aforesaid decision, as set out above, it has been said that, “It is not out of context here, to refer to the decision of the Tribunal, Bangalore Bench rendered in the case of KPIT Cummins Infosystems (Bangalore) (P.) Ltd. (supra)” in which “the Tribunal has held in favour of the assessee, accepting the argument that brought forward loss/unabsorbed depreciation need not be set off against profits eligible for deduction under s. 10A”and that “In fact, one of us was a party to that order, but, in the course of arguments, we found that the said order might not be reflecting the correct position of law. We have no hesitation to state so, as we do not believe that perpetuating a mistake is heroism”. In such a situation when that decision is abandoned by one of the authors himself it is perhaps stretching the things too far to go by that decision alone and thus ignore other binding precedents on that issue.

36. The second decision of a coordinate bench, relied upon by the assessee, is an unreported and a very brief decision in the case of Solutions Infosystems (P) Ltd. (supra). In this decision, the issue is decided in favour of the assessee by respectfully following the Yokogawa India Ltd. deicision (supra) simplictor and stating that. “No contrary decision of any High Court is brought before us on this issue. This being the sole judgement of the High Court on this issue as on the date and being the latest decision, we apply the same and uphold the contentions of the assessee. In the result ground no.1 of the assessee is allowed” (Emphasis by underling supplied by me).

The decision of Hon’ble Karnataka High Court was only on the question of carry forward and set off of business losses and unabsorbed deprecation of non 10 A units and the question regarding set off of business losses and unabsorbed depreciation of the same unit, though taken up initially, was declined to be adjudicated upon. We are, however, dealing with a situation in which the short issue before us is whether business loss and unabsorbed depreciation of the same unit, le 10A unit, can be set off against its subsequent profits

37. The approach adopted by the part of the co-ordinate bench is very fair and none can fault the same. The principle is correct but the situation that we are dealing with right now is a situation in which not only there is another decision is available such a decision, holding to the contrary to what the coordinate bench has decided, has been confirmed by the Hon’ble Supreme Court in an unreported judgment dated 13th September 2013 As it appears from a perusal of the order of the coordinate bench, this development was not brought to the notice of the bench.

38. It is interesting to note that the bench has referred to Hon’ble Karnataka High Court’s judgment in the case of Yokogawa India Ltd. (supra), as sole decision” but also as the “latest decision”. The expression “latest decision implies that there are other decisions. available on the issue, though somewhat in conflict with the earlier expression, and such a reference can only be for the decision in the case of Himatasingike Seide Ltd. (supra) but then what the coordinate bench was not informed was that this other decision, ie. in the case of Himatasingike Seide was approved by Hon’ble Supreme Court around the same time when the coordinate bench was dealing with this issue.

39. As can be noticed from observations elsewhere in this order and as opined by other division benches, but, for the detailed reasons I will set out in a short while, the question requiring our adjudication in the present case did not fell for consideration of Their Lordships in this case, and, therefore, the judicial precedent in the case of

Yokogawa India Ltd. (

supra), in the light of law laid down by Hon’ble Bombay High Court in the case of

CIT v.

Sudhir Jayantilal Mulji [1996] 84 Taxman 205/[1995] 214 ITR 154 (Bom) and by Hon’ble Supreme Court in

CIT v.

Sun Engineering Works (P.) Ltd. [1992] 64 Taxman 442/198 ITR 297 (SC), does not apply to the situation that we are dealing with In any event, no matter how persuasive a decision is from the coordinate benches, these decisions have to give way to the principles laid down by the Hon’ble Courts above. That is the strength of hierarchical judicial system that we have in our country.

40. Let us now move on to take up Hon’ble Karnataka High Court in the case of Yokogawa India Ltd. (supra) and try to understand what has been stated by Their Lordships and in what context it is necessary to appreciate the context in which the observations relied upon by the assessee have been made In the case of Yokogawa India Ltd. (supra), the questions before Hon’ble Karnataka High Court, in CIT v. Yokogawa India Ltd. [IT Appeal No. 248 of 2007, dated 9-8-2011] ie the lead case, were as follows:

(i) Whether the appellate authorities failed to take into consideration that the amendment to s. 10A by Finance Act of 2000 w.e.f 1st April, 2001, the deduction of profits and gains as earned by an undertaking from the export of articles or things or computer software is required to be allowed from the total income of the assessee and consequently the loss from the non-STP unit is required to be set off against the income of the other STP unit before allowing deduction under s. 10A of the amended Act?

(ii) Whether the Tribunal was correct in holding that the deduction under s. 10A or 10B of the Act during the current assessment year has to be allowed without setting off brought forward unabsorbed losses and the depreciation from earlier assessment year or current assessment year either in the case of non-STP units or in the case of the very same undertaking?”

41. On the first question, i.e. with respect to loss from non eligible unit, the matter was clearly decided in favour of the assesse but then that’s not the issue that we are dealing in the present case Right now, we are concerned about the losses of eligible unit in earlier years being set off against the profits of the year before us So far as this aspect of the matter is concerned it is necessary to bear in mind the fact that there was no carried forward loss of the assessee from eligible unit in this case as is evident from the following observations in the Tribunal’s order (reported in

Asstt. CIT v.

Yokogawa India Ltd. [2007] 13 SOT 470 (Bang-Trib) order dated 4th August 2006)

15. In the instant case, there is no unabsorbed depreciation or unabsorbed business loss in respect of software services division and therefore profits and gains of the software services division will be exempt under s. 10A without setting off the loss of other division or the setting off of carry forward losses of other division. In view of above discussion, we hold that learned CIT(A) was justified in directing the AO to allow exemption under s. 10A without setting off loss of non-10A unit and consequentially allowed carry forward of such losses and depreciation of non-10A unit.

(Emphasis supplied by me by underlining)

42. Their Lordships have confirmed the view so taken by the Tribunal The view so taken specifically relates to business losses and unabsorbed depreciation of non eligible units, and, as a matter of fact, it is specifically stated that since the unabsorbed depreciation and business losses pertain to non eligible units “therefore” (emphasis supplied by me) profits of eligible units “will be exempt under section 10A without setting off the loss of other division or the setting off of carry forward of the loss of other division” When appeal against this order of the Tribunal reached Hon’ble High Court, Their Lordships, inter alia, observed as follows:

31. As the income of 10A unit has to be excluded at source itself before arriving at the gross total income, the loss of non 10A unit cannot be set off against the income of 10A unit under s. 72. The loss incurred by the assessee under the head profits and gains of business or profession has to be set off against the profits and gains if any of any business or profession carried on by such assessee. Therefore, as the profits and gains under s. 10A are not to be included in the income of the assessee at all, the question of setting off the loss of the assessee of any profits and gains of business against such profits and gains ofthe undertaking would not arise. Similarly as per s. 72(2), unabsorbed business loss is to be first set offand thereafter unabsorbed depreciation treated as current year’s depreciation under s. 32(2) is to be set off. As deduction under s 10A has to be excluded from the total income of the assessee the question of unabsorbed business loss being set off against such profits and gains of the undertaking would not arise In that view of the matter, the approach of the assessing authority was quite contrary to the aforesaid statutory provisions and the CIT(A) as well as the Tribunal were fully justified in setting aside the said assessment order and granting the benefit of s 10A to the assessee. Hence, the main substantial question of law is answered in favour of the assessees and against the Revenue.

32. In view of the fact that the main substantial question of law is answered in favour of the assessee the additional question becomes purely academic and therefore is not answered.

(Emphasis by underlining supplied by me)

43. These observations, as the very first sentence of the paragraph would show, were in the context of “non 10 A units” All that Their Lordships have done is to confirm the stand taken by a coordinate bench of this Tribunal and the decision of the coordinate bench, as can be easily discerned from the facts set out above had nothing to do with the set off of the losses carried forward in respect of a 10A unit The second question which was framed by Their Lordships, and which has been reproduced earlier, has thus remained unanswered and Their Lordships stated so in so many words by observing that. “the main substantial question of law is answered in favour of the assessees and against the Revenue” and that “(i)n view of the fact that the main substantial question of law is answered in favour of the assessee the additional question becomes purely academic and therefore is not answered”. Viewed thus, it is stretching the things much beyond the permissible limits to suggest that Yokogawa’s decision is an authority for the proposition that even losses carried forward in respect of the same eligible unit cannot be set off before computing deduction under section 10A. Let us not forget the oft quoted words of Justice Dr Anand, as he then was, in the case of Sun Engineering Works (P.) Ltd. (supra), which are reproduced below:

It is neither desirable nor permissible to pick out a word or a sentence from the judgment of this Court divorced from the context of the question under consideration and treat it to be the complete “law” declared by this Court. The judgment must be read as a whole and the observations from the judgment have to be considered in the light of the questions which were before this Court. A decision of this Court takes its colour from the questions involved in the case in which it is rendered and, while applying the decision to a later case, the Courts must carefully try to ascertain the true principle laid down by the decision of this Court and not to pick out words or sentences from the judgment, divorced from the context of the questions under consideration by this Court, to support their reasoning In Madhav Rao Jivaji Rao Scindia Bahadur v. Union of India (1971) 3 SCR 9 AIR 1971 SC 530, this Court cautioned:

“It is not proper to regard a word,, clause or a sentence occurring in a judgment of the Supreme Court, divorced from its context, as containing a full exposition of the law on a question when the question did not even fall to be answered in that judgment. ”

(Emphasis by underlining supplied by me)

44. What holds good for interpreting the observations made in the judgments of Hon’ble Supreme Court, in my humble understanding, applies equally on the observations made in judgments of Hon’ble High Courts. In This view of the matter, and in view of the glaring fact that the second question i.e., with respect to set off of losses of “the same undertaking”, to use the words employed by Hon’ble Supreme Court in Sun Engineering Works (P.) Ltd.’s case (supra), “did not even fall to be answered in that judgment”, I have my serious reservation on the stand that Yokogawa India Ltd. decision (supra) is an authority for the proposition that business losses in respect of the same undertaking as brought forward from the earlier years, need not be set off before computing deduction under section 10 A That issue did not even fell for consideration in this case, and, as I have been able to understand, Hon’ble High Court did not decide that issue either. It is also important to bear in mind that, as held by Bombay High Court in the case of Sudhir Jayantilal Mulji (supra), a judicial precedent is only “an authority for what it actually decides and not what may come to follow from some observations which find place therein” In this view of the matter, the observations made in Yokogawa’s case even if these observations can be construed as in favour of the assessee, cannot dilute the binding force of binding judicial precedents on the issue before us.

45. In the case of Black & Veatch Consulting (P.) Ltd.(supra), the neatly identified question of law, which came up for consideration of Hon’ble Bombay High Court, was “Whether on the facts and circumstances of the case and law, the ITAT was correct in holding that the brought forward unabsorbed depreciation and losses of the unit the Income which is not eligible for deduction under Section 10A of the Act cannot be set off against the current profit of the eligible unit for computing the deduction under Section 10A of the IT Act.” The controversy was thus confined to carry forward and set off of business losses incurred by a unit which was not eligible for exemption under section 10A That is not the situation before us, and therefore, this decision cannot be treated as a binding judicial precedent to adjudicate on the question before us. The assessee, therefore, does not derive any advantage from this judicial precedent as well.

46. On this issue, as also held by at least two coordinate benches in the cases of ntellinet Technologies India (P.) Ltd. (supra) and Global Vantedge (P.) Ltd. (supra), there is a direct decision from Hon’ble High Court is Hon’ble Karnataka High Court’s decision in the case of Himatasingike Seide Ltd. (supra) wherein. Their Lordships were required to adjudicate on the question “Whether on the facts and in the circumstances of the case, the Tribunal is right in law in holding that the assessment order passed by the AO allowing the claim of the assessee for adjustment of the unabsorbed depreciation against the income from other sources was in order and hence cannot be considered to be erroneous or prejudicial to the interests of the Revenue and in cancelling the order under s 263”. That was a situation in which the assessee had profits from a 10 B unit which were exempt from the tax, and the assessee set off the carried forward unabsorbed depreciation from this undertaking against its income from other sources The question which thus fell for consideration by Their Lordships was whether the assessee should have first set off such unabsorbed depreciation against tax exempt profits of the same undertaking It was in this backdrop that Their Lordships observed as follows

If we see s. 108, it provides for exemption of payment of tax with reference to profits and gains derived by 100 per cent export-oriented undertaking To arrive at a profit and gain, one has to necessarily fake into consideration the total income in terms of the Act To arrive at the income one has to take into consideration, the various additions and deletions in terms of the Act. In fact, the petitioner knowing fully well has chosen to take into consideration the allowability of depreciation for the purpose of calculation of total income. But curiously an argument has now been advanced that exemption in terms of s 108 could also be on commercial basis not necessarily in terms of the calculation. We do not accept this submission. Sec. 10B cannot be read in isolation of other provisions. It is only an exemption provision Exemption cannot be fanciful and it has some rationale with other provisions of the Act. Therefore, a combined reading of the definition of exemption, total income-tax liability, deductibility, etc., one has to come to a conclusion that calculation as far as possible is to be in terms of the IT Act. That is exactly what has been done by the assessee. Having calculated in a particular manner, now it does not lie in the mouth of the assessee to contend contra in these proceedings. It cannot be argued that the calculation so provided is on a mistaken basis or that could be on commercial basis. We are not prepared to accept this argument advanced by the assessee Exemption also has to be scrutinized by the Department as otherwise there is every chance ofexemption being misused by an assessee. It may be true that even after taking into consideration the unabsorbed depreciation, the assessee may get exemption but nonetheless he cannot take only a portion of depreciation just to suit his income for the purpose of nil liability and adjust the balance of unabsorbed depreciation for other business income once again to show nil liability. When the unabsorbed depreciation could have been taken for arriving at an exempted income, the assessee cannot play with the figures for the purpose of showing nil liability as has been done in the case on hand. The intention of the legislature is only to provide 100 per cent exemption for export income and not for other income. The petitioner by dividing depreciation contrary to s 32 has virtually taken exemption from payment of tax even for other business income in the case on hand. That cannot be allowed as rightly ruled by the CIT The allowance of the depreciation by the Tribunal, in our view, is prejudicial to the interests of the Revenue as argued by the Department. The Tribunal has taken a narrow view of the matter without taking into consideration the laudable object of exemption and at the same time providing for tax liability towards other liability. The interpretation has to be meaningful and acceptable and it cannot be against the intention of the legislation Legislation never wanted the entire income to be exempted by taking advantage of s. 10B of the Act. The approach of the Tribunal to our mind is incorrect and, hence, we find substance in the argument of the Revenue.

47. The views so expressed by Their Lordships are, as opined by a coordinate bench in the case of

Global Vantedge (P.) Ltd. (

supra)

Intellinet Technologies India (P.) Ltd. (

supra), are equally applicable for the provisions of Section 10 B In any case, the issue considered by Hon’ble High Court, i.e., whether the brought forward unabsorbed depreciation etc is to be set off against the income of the same undertaking or after the grant of exemption under section 10 B is the same as before us in this view of the matter, in my considered view, the issue before us is covered against the assessee by the aforesaid judgment of Hon’ble Karnataka High Court in the case of

Himatasingike Seide Ltd. (

supra) and by coordinate bench decisions in the cases of

Global Vantedge (P.) Ltd. (

supra) and

Intellinet Technologies India (P.) Ltd. (

supra). The views so taken by Hon’ble Karnataka High Court were approved by Hon’ble Supreme Court when, in the case of

Himatsingka Seide Ltd. v.

CIT [2014] 48

taxmann.com 357/[2015] 228 Taxman 63 (Mag) (SC)/Civil Appeal No 1501 of 2008. Hon’ble Supreme Court dismissed this civil appeal, along with with a huge bench of several other connected appeals on the same issue, on merits and observed as follows:

Having perused the records and in view of the facts and circumstances of the case we are of the opinion that the Civil Appeal being devoid of any merit deserves to be dismissed and is dismissed accordingly.

48. It is also useful to bear in mind the fact that in the said case. Their Lordships were dealing with a situation in which carry forward of losses of eligible units was permitted, as is the position now and when the losses so incurred were sought to be set off against incomes other than profits of the same undertaking in the subsequent profit making years. Their Lordships disapproved that exercise. In the present legal position also, the net legal position is that carry forward and set off of the unabsorbed depreciation and business losses is permitted, and if the same cannot be permitted to be set off against other incomes, it can only be set off against the profits of the same undertaking. Any other view of the matter will render the provision of set off otiose and unworkable It is equally important to appreciate that in the subsequent assessment years, as before the Tribunal in this case, only a portion of profits of eligible undertaking is exempted under section 10 A, and, therefore, the provision for carry forward and set off provide definite advantage to the assessee. The controversy however, arises when assessee contrives to carry forward such unabsorbed depreciation and losses further so as to set it off against incomes which are effectively taxed in an altogether a different manner as in this case, taxable in the hands of the assessee though with altogether different tax implications. Such a treatment, as is canvassed by the assessee before us, is clearly incongruous and contrary to the scheme of law visualized by Their Lordships in the case of Himatasingike Seide Ltd. (supra).