AO Must Apply ‘Commercial Expediency’ to Carried-Forward Investments and Delete Disallowance.

Issue

Whether the principle of “commercial expediency,” which was accepted for an investment in a prior year, must be applied to the interest disallowance on that same (carried forward) investment in the current assessment year, or can an appellate authority set aside the entire assessment for a fresh decision?

Facts

- For the Assessment Year 2016-17, the assessee’s case was reopened, and a disallowance was proposed under Section 36(1)(iii) for interest on borrowed capital allegedly used for non-business investments.

- On appeal, the Commissioner (Appeals) set aside the entire assessment order and directed the Assessing Officer (AO) to complete a fresh (de novo) assessment.

- The assessee contended that this was incorrect, as a portion of the impugned investment was simply carried forward from a previous year.

- In that previous year, a similar disallowance had been challenged, and the claim was allowed after the “commercial expediency” of the investment was examined and accepted.

Decision

The High Court ruled partly in favour of the assessee:

- For the Carried-Forward Investment: The court held that the principle of commercial expediency, having been established and accepted in a prior year, must apply mutatis mutandis (with necessary changes) to the same investment in the current year. The AO was directed to delete the corresponding disallowance.

- For Other Investments: For any other new investments that were not covered by the prior year’s order, the issue was restored to the file of the Assessing Officer for the limited purpose of verifying the disallowance.

Key Takeaways

- Principle of Consistency: The tax department cannot be allowed to re-adjudicate an issue that has already been settled on merits in the assessee’s own case in a prior year, as long as the facts remain the same. The principle of commercial expediency, once established, carries forward with the investment.

- No Unnecessary De Novo Assessments: The Commissioner (Appeals) erred in setting aside the entire assessment. The High Court’s order was more precise, protecting the already-decided issue and remanding only the new, unverified issues.

- Commercial Expediency is the Test: This case reiterates that the primary test for allowing interest on borrowed funds under Section 36(1)(iii) is whether the funds were used for a purpose driven by business or “commercial expediency,” a decision that is based on the facts of the case.

IN THE ITAT HYDERABAD BENCH ‘B’

Kausalya Agro Farms and Developers (P.) Ltd.

v.

Income-tax OfficerVIJAY PAL RAO, Vice President

and MADHUSUDAN SAWDIA, Accountant Member

and MADHUSUDAN SAWDIA, Accountant Member

IT Appeal No. 804 (Hyd.) of 2025

[Assessment year 2016-17]

[Assessment year 2016-17]

OCTOBER 17, 2025

S. Rama Rao, Adv. for the Appellant. Dr. Sachin Kumar, Sr. DR for the Respondent.

ORDER

Madhusudan Sawdia, Accountant Member.- This appeal is filed by M/s. Kausalya Agro Farms and Developers Pvt. Ltd. (“the assessee”), feeling aggrieved by the order passed by the Learned Commissioner of Income Tax (Appeals), National Faceless Appeal Centre (NFAC), Delhi (“Ld. CIT(A)”), dated 23.01.2025 for the A.Y. 2016-17.

2. At the outset, it is noted that there is a delay of 39 days in filing of the present appeal before this Tribunal. The assessee has filed a condonation petition along with a copy of affidavit, explaining the reasons for the said delay. The Learned Authorised Representative (“Ld. AR”) submitted that during the relevant period, the Executive Director of the company, who was looking after the income tax matters, was suffering from severe neck pain radiating to both upper limbs and other related health complications. The doctor had advised him complete rest for about one and a half months, due to which the necessary steps for filing the appeal could not be taken within the prescribed period of limitation. It was further submitted that the medical certificate and supporting evidence in this regard have been filed along with the condonation petition. The Ld. AR thus contended that the delay was neither deliberate nor intentional, but occurred due to bona fide reasons beyond the control of the assessee. He, therefore, prayed that the delay may kindly be condoned and the appeal admitted for adjudication on merits.

3. Per contra, the Learned Departmental Representative (“Ld. DR”) did not raise any serious objection to the request for condonation of delay.

4. We have considered the rival submissions and perused the material on record. In the present case, the reason for delay has been duly explained by the assessee, supported by medical evidence. We find that the delay was caused due to unavoidable medical reasons and not due to any deliberate inaction or negligence. Further, the Department has not raised any serious objection to the condonation. Accordingly, we are satisfied that the assessee has shown sufficient cause for the delay in filing of the appeal. Therefore, in the interest of substantial justice, the delay of 39 days in filing the appeal is hereby condoned, and the appeal is admitted for adjudication on merits.

5. The assessee has raised the following grounds of appeal :

| 1. | The order passed by the Ld. Commissioner of Income Tax (Appeals) is erroneous both on facts and in law. |

| 2. | The Ld. CIT(A) ought to have considered the fact that the issue of disallowance of finance cost is already decided by the Hon’ble ITAT in favour of the appellant and the CIT(A) ought to have allowed the appeal following the decision of the Hon’ble ITAT. |

| 3. | The Ld. CIT(A) ought to have seen that similar additions made in the group concerns are deleted and, therefore, the CIT(A) ought to have deleted the additions made of Rs. 1,17,73,680/-. |

| 4. | The Ld. CIT(A) erred in directing the Assessing Officer to complete the assessment De novo without limiting the re assessment to the issue of disallowance of finance cost. |

| 5. | Any other ground that may be urged at the time of hearing. |

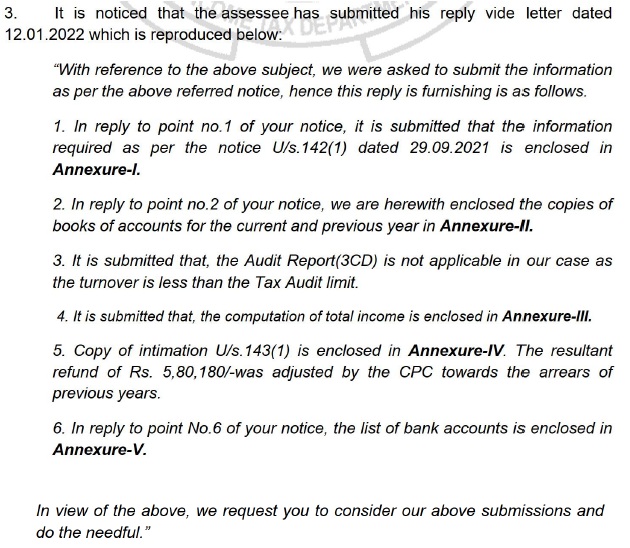

6. The brief facts of the case are that the assessee is a company which filed its return of income for the Assessment Year 2016-17 on 13.10.2016, declaring total income of Rs.2,96,250/-. The case of the assessee was reopened under section 147 of the Income Tax Act, 1961 (“the Act”), and accordingly, a notice under section 148 of the Act was issued by the Learned Assessing Officer (“Ld. AO”) on 12.03.2021. During the course of reassessment proceedings, the assessee filed its reply on 12.01.2022, enclosing copies of the books of account, computation of total income, and list of bank accounts. However, the Ld. AO was not satisfied with the explanation offered by the assessee and, accordingly, issued a show-cause notice along with a draft assessment order, proposing a disallowance under section 36(1)(iii) of the Act. Since the assessee did not furnish any response to the said show-cause notice, the Ld. AO completed the assessment under section 147 read with sections 144 and 144B of the Act on 29.03.2022, making an addition of Rs.1,17,73,680/- under section 36(1)(iii) of the Act and determining the total income of the assessee at Rs.1,20,69,930/-.

7. Aggrieved by the said assessment order, the assessee preferred an appeal before the Ld. CIT(A). The Ld. CIT(A), invoking powers under the proviso to section 251(1)(a) of the Act, set aside the entire assessment to the file of the Ld. AO with a direction to complete the assessment de novo.

8. Aggrieved by the said action of the Ld. CIT(A), the assessee is in appeal before this Tribunal. The Ld. AR submitted that the sole grievance of the assessee is that the Ld. CIT(A) erred in remanding the matter for a de novo assessment instead of restricting the remand to the limited purpose of verification of the disallowance made by the Ld. AO under section 36(1)(iii) of the Act. In this regard, the Ld. AR invited our attention to para no.3 of page no.2 of the assessment order, wherein the Ld. AO has himself recorded that the assessee had filed a reply dated 12.01.2022, enclosing books of account, computation of income, and other supporting documents. It was only in response to the final show-cause notice, proposing disallowance under section 36(1)(iii), that the assessee did not respond. Hence, the Ld. AR argued that the assessment was not fully ex parte, but only partially ex parte i.e. confined to the issue of disallowance under section 36(1)(iii) of the Act. Therefore, there was no justification for the Ld. CIT(A) to direct a complete de novo assessment.

8.1 The Ld. AR also referred to para no.22 of the Tribunal’s order in the assessee’s own case for A.Y. 2017-18 in Kausalya Agro Farms & Developers (P.) Ltd. v. Dy. CIT [IT Appeal No. 676 (Hyd.) of 2020, dated 4-9-2024], wherein the Tribunal had deleted the disallowance made under section 36(1)(iii) of the Act on the ground of commercial expediency. It was submitted that since the facts for the present year are identical, the same finding of the Tribunal should apply to the year under consideration.

8.2 Alternatively, the Ld. AR drew our attention to page no. 24 of the paper book no.2, demonstrating that the total impugned investment made by the assessee was Rs.12,72,54,000/-, whereas the interest-free funds available with the assessee was Rs.13,64,08,034/-. To substantiate the individual figure stated at page no. 24 of the paper book no.2, the Ld. AR referred to the audited financial statements placed at page nos. 7 to 12 of Paper Book no. 1. Accordingly, the Ld. AR submitted that the interest-free funds available with the assessee were more than sufficient to cover the impugned investments. Therefore, there should not be any disallowance under section 36(1)(iii) of the Act in the hands of the assessee. In this regard, the Ld. AR relied upon the order of this Tribunal in the case of Kapil Foods and Structures (P.) Ltd. v. Dy. CIT [IT Appeal Nos. 205 & 206 (Hyd.) of 2025, dated 26-9-2025] for A.Ys. 2016-17 and 2017-18, wherein, under identical facts, this Tribunal had restored the issue to the file of the Ld. AO for limited verification of the disallowance under section 36(1)(iii) of the Act. Accordingly, the Ld. AR submitted that, the case of the assessee may also be remanded to the file of the Ld. AO for limited verification of the disallowance under section 36(1)(iii) of the Act, in terms of the direction of this Tribunal in the case of Kapil Foods and Structures Pvt. Ltd. (supra).

9. Per contra, the Ld. DR strongly supported the order of the Ld. CIT(A). He submitted that the assessment was completed under section 144 of the Act and, therefore, the Ld. CIT(A) was fully empowered under the proviso to section 251(1)(a) to set aside the entire assessment for de novo adjudication. Accordingly, there is no infirmity in the order of Ld. CIT(A) and prayed that the same should be upheld.

10. We have heard the rival submissions and perused the material available on record. The undisputed fact is that the assessment was completed under section 147 read with sections 144 and 144B of the Act, with a single disallowance made under section 36(1)(iii) of the Act amounting to Rs.1,17,73,680/-. We have gone through para no.3 of page no.2 of the order of Ld. AO, which is to the following effect :

10.1 On perusal of above, it is evident that the Ld. AO himself recorded that the assessee had filed its reply dated 12.01.2022, enclosing books of account, computation of income, and other relevant details. We also note that after considering the submission of the assessee, the Ld. AO issued show cause notice to the assessee. The assessee failed to comply to the said show cause notice. Hence, while the assessment has been styled as one under section 144 of the Act, it cannot be treated as a completely ex parte assessment. The proceedings were substantially participated in by the assessee, except for the final stage relating to the proposed disallowance under section 36(1)(iii) of the Act. In this background, we find substance in the contention of the Ld. AR that the Ld. CIT(A), while exercising his powers under the proviso to section 251(1)(a) of the Act, should have restricted the remand to the specific issue of disallowance under section 36(1)(iii) of the Act, instead of directing the Ld. AO to redo the entire assessment de novo. The proviso to section 251(1)(a) indeed empowers the Ld. CIT(A) to set aside an assessment made under section 144 of the Act, but such power must be exercised in a judicious and proportionate manner, having regard to the nature of the default and the scope of the issue involved. Where the default is limited to a single issue, as in the present case, directing a full de novo assessment goes beyond what is necessary for proper adjudication. Accordingly, we are of the considered view that the Ld. CIT(A) should have restricted the remand to the specific issue of disallowance under section 36(1)(iii) of the Act, instead of directing the Ld. AO to redo the entire assessment de novo.

10.2 Further, we have gone through para no.22 of the order of this Tribunal in the assessee’s own case for A.Y. 2017-18 in ITA No. 676/Hyd/2020 dated 04.09.2024, which is to the following effect :

” 22. We have heard the rival submissions and perused the material on record and gone through the orders of the authorities below. The fact borne out from the record indicates that the assessee being in the business of real estate development, has collected advances from customers for sale of flats / commercial complexes in terms of MOU. As per the terms of MOU between the appellant and the customers, there is a provision for payment of interest ranging from 10% to 14% in case of any delay in delivery of flats to the customers. As per the contractual agreement with the customers in terms of MOU, the assessee has paid interest on customers’ advances and debited under the head finance charges. The AO has disallowed interest expenses on the ground that the appellant failed to prove utilization of advances received from customers for the purpose of business. The ld. CIT(A) went on a different footing and computed disallowance of interest for diversion of interest-bearing funds for non-business purpose. We find that the basic business of the assessee is real estate development, and in that process, the assessee collected advances from customers for sale of flats. As per the agreement with the customers, the assessee has paid interest in case of delay in delivery of flats. The assessee had also proved that the funds received from the customers in the form of advances have been utilized for the purpose of business of the assessee. In fact, it is not a case of the AO that the assessee had diverted funds for non-business purposes. Assuming for a moment that loans and advances given to group concerns are diversion of interest-bearing funds, the fact remains that, as the AO himself noted, the group companies of the assessee are also engaged in the business of real estate development and there is a business nexus between the appellant and the group concerns and thus, in our considered opinion, loans and advances given to other group companies can be said to be in the normal course of the business of the assessee and thus, there is a commercial expediency. Therefore, we are of the considered view that the AO erred in disallowing finance charges being interest paid on customers’ advances without any valid reasons. The ld. CIT(A), without appreciating the relevant facts, partly confirmed the addition made by the Assessing Officer. Thus, we set aside the order of the ld. CIT(A) and direct the AO to delete the addition sustained by the ld.CIT(A) towards disallowance of finance charges amounting to Rs.1,33,94,799/-, which was confirmed by the ld.CIT(A).”

10.3 On perusal of above, we find that the Tribunal deleted a similar disallowance after examining the aspect of commercial expediency. Since no variation in facts or legal position has been brought to our notice by the revenue for the year under appeal, the principle of consistency, as laid down by the Hon’ble Supreme Court in Radhasoami Satsang v. CIT [1992] 60 Taxman 248/193 ITR 321 (SC), mandates that similar treatment be accorded in the present year as well. Therefore, the principle of commercial expediency shall apply mutatis mutandis to the year under consideration as far as the impugned investment is concerned which has been carry forward to the A.Y. 2017-18. Accordingly, the Ld. AO is directed to apply the principle of commercial expediency to the said portion of impugned investment and delete the corresponding disallowance under section 36(1)(iii) of the Act.

10.4 As far as the other investments which are not covered in terms of commercial expediency, the assessee in his alternate plea has submitted that, the total impugned investment made by the assessee was Rs.12,72,54,000/-, whereas the interest-free funds available with the assessee was Rs.13,64,08,034/-. Accordingly, the Ld. AR submitted that the interest-free funds available with the assessee were more than sufficient to cover the impugned investments. Therefore, there should not be any disallowance under section 36(1)(iii) of the Act in the hands of the assessee. In this regard, the Ld. AR relied upon the order of this Tribunal in the case of Kapil Foods and Structures Pvt. Ltd. (supra), wherein, under identical facts, this Tribunal had restored the issue to the file of the Ld. AO for limited verification of the disallowance under section 36(1)(iii) of the Act. There is no dispute about the fact that the linkage of availability of interest free funds qua the impugned investment has not been verified by the lower authorities. In this regard, we have gone through para nos.9 to 14 of the order of this Tribunal in the case of Kapil Foods and Structures Pvt. Ltd. (supra), which is to the following effect :

9. We have heard rival submissions and perused the material available on record. As far as the admission of additional evidence is concerned, the assessee has filed audited balance sheet extracts, details of customer advances and investment statements. These documents go to the root of the matter and were not before the Ld. AO/CIT(A). In the interest of justice, we admit the additional evidences filed by the assessee.

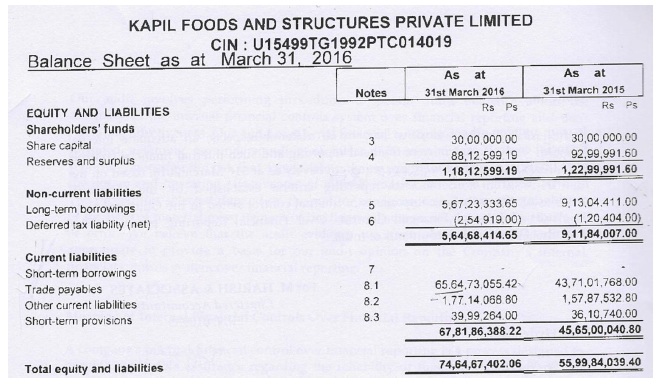

10. We have gone through the share holders funds of the audited financial statement of the assessee placed at page no.7 of the paper book which is to the following effect:

—- Space left intentionally —-

11. On perusal of above, we find that the shareholders’ funds of the assessee is Rs. 1,18,12,599/-. From page no. 10 of the paper book, we note that the assessee has secured redeemable debentures of Rs.5,49,25,000/-, which are claimed to be interest free. Further, on perusal of details of advance for sale of plots placed at page nos.2 to 24, we find that the assessee has Customer advances (interest-free in respect of registered plots) amount to Rs.4,13,70,971/-. Thus, the assessee has total interest-free funds of Rs.10,81,08,570/-(Rs.4,13,70,971/- + Rs.1,18,12,599/- + Rs.5,49,25,000/-).

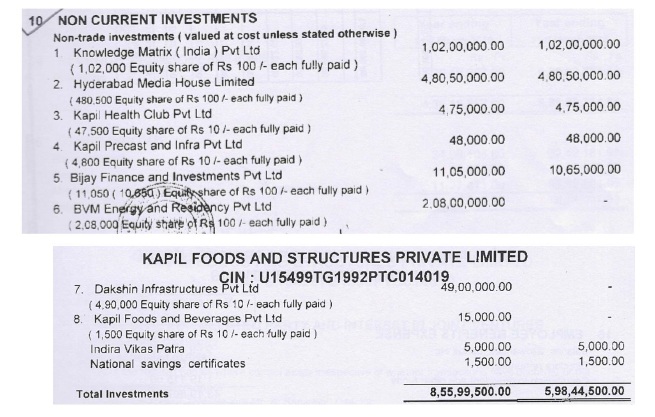

12. We have also gone through Note no. 10 regarding non-current investments of the audited financial statements of the assessee placed at page nos. 10 and 11 of the paper book which is to the following effect:

13. On perusal of above, we find that the assessee has invested in non-current investments amounting to Rs.8,55,99,500/-. We find that the assessee has total interest-free funds of Rs. 10,81,08,570/- against invested in non-current investments of Rs.8,55,99,500/-. Accordingly, it is clear that the interest free funds available in the hands of the assessee are more than the amount of investment in non-current assets.

14. We also found that, the Hon’ble Supreme Court in Reliance Industries Ltd. (supra) and South Indian Bank Ltd. (supra) has held that if interest-free funds are more than investments, presumption is that investments are made out of interest-free funds. These judgments being of the Apex Court, prevail over High Court rulings relied upon by the Ld. DR. Therefore, prima facie, the assessee had sufficient interest-free funds. However, since these documents were not before the lower authorities, proper verification is required. Accordingly, we set aside the matter to the file of the Ld. AO with the direction to verify the additional evidences. If, on verification, it is found that interest-free funds are more than the non-current investments, the disallowance made u/s 36(l)(iii) of the Act shall be deleted.

10.5 On perusal of above, we find that under the similar facts this Tribunal had restored the issue to the file of the Ld. AO for limited verification of the disallowance under section 36(1)(iii) of the Act. Therefore, respectfully following the decision of this Tribunal, as far as the other investments which are not covered in terms of commercial expediency, we restore the issue to the file of the Ld. AO for limited verification of the disallowance under section 36(1)(iii) of the Act, in terms of the direction given by this Tribunal in the case of Kapil Foods and Structures Pvt. Ltd. (supra).

11. In the result, the appeal of the assessee is allowed for statistical purposes, in terms of our above findings.