ORDER

C.N. Prasad, Judicial Member.- This appeal filed by the assessee is directed against the order of the Ld. CIT(A)-10, New Delhi dated 26.08.2019 for the A.Y. 2012-13.

2. The assessee has raised following grounds of appeal : –

“1. That under the facts and circumstances Ld. CIT(A) erred in law as well as on merits in passing ex-parte order, although all dates of hearing were responded. CIT(A) has been incorrect in mentioning that no one attended on 20.08.19, the last date of hearing, when, CA. J. P. Sharma attended the CIT(A), requested for adjournment, it was refused, even adjournment application not accepted, then on 20.08,19, the said adjournment application had to be sent through ITBA vide Ack. No.20081911493791, thus no proper and reasonable opportunity of hearing has been allowed. In the absence of receipt of any fresh date of hearing and any fresh communication from CIT(A), the written submissions were also sent through ITBA on 30.08.19 vide Ack. No.30081911525702, which have not been considered in the impugned CIT(A) order.

2. That under the facts and circumstances, the Ld. CIT(A) erred in law in not deciding the appeal on merits substantively even while passing ex-parte asstt. order.

3. That under the facts and circumstances, the Ld. A.O. has exceeded his jurisdiction by not strictly following and working within the four corners of directions and findings in order u/s.263, hence the impugned order is not sustainable in law being without jurisdiction and illegal.

4. That under the facts and circumstances, the Ld. A.O. committed serious legal and factual errors in allowing deduction u/s.54 only for Rs.33,61,165 against correctly claimed at Rs.64,23,843, thus short by Rs.30,62,678.

4.1 That in view of the submissions, evidences furnished and the settled legal position as per case laws, the deduction u/s.54 should have been allowed for Rs.64,23,843.”

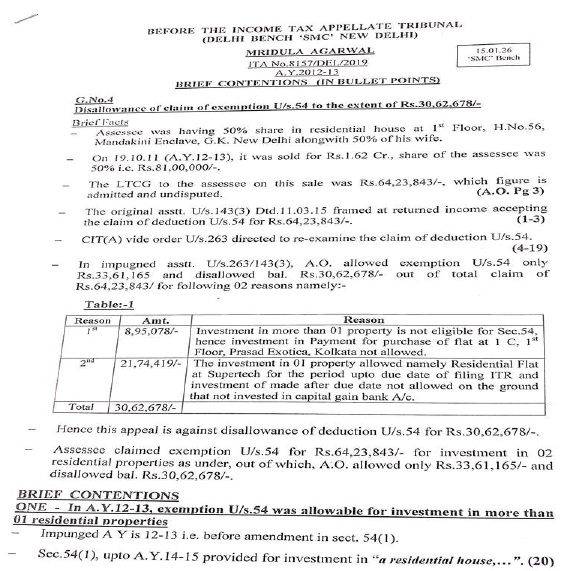

3. The Ld. Counsel for the assessee at the outset submitted that in this appeal claim for exemption u/s.54 was denied to the extent of Rs.30,62,678/- on the ground that the assessee had invested in more than one property and therefore, not eligible for exemption u/s.54 for the investment made in the property at 1C, 1st Floor, Prasad Exotica, Kolkata. The exemption was granted only in respect of property namely residential flat at Supertech for the period of up to the date of filing ITR and investment made thereafter was not allowed on the ground that assessee has not invested in capital gain account.

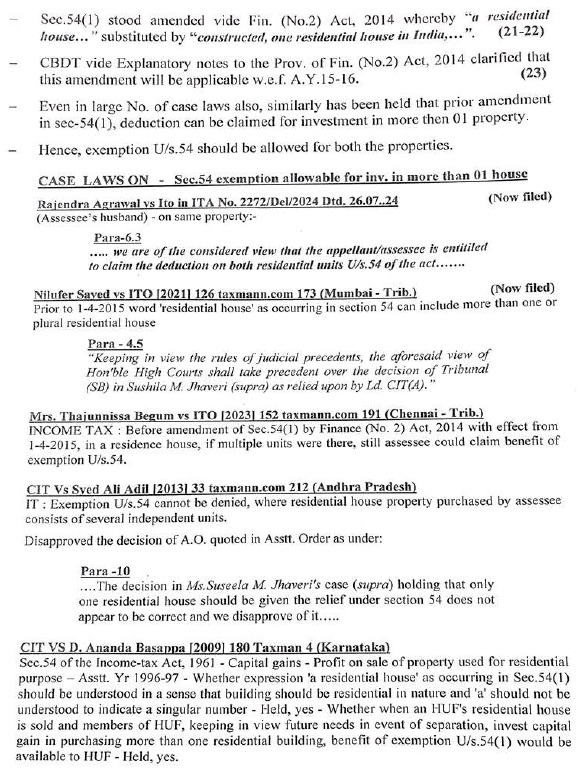

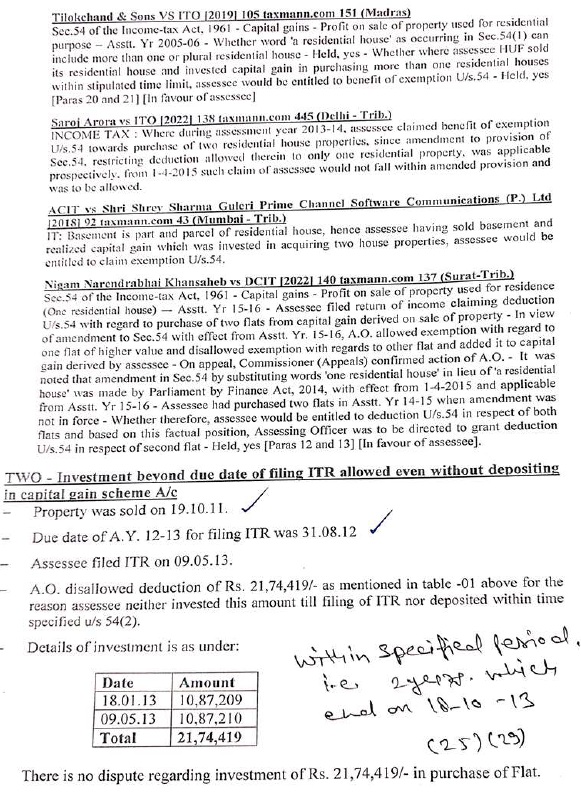

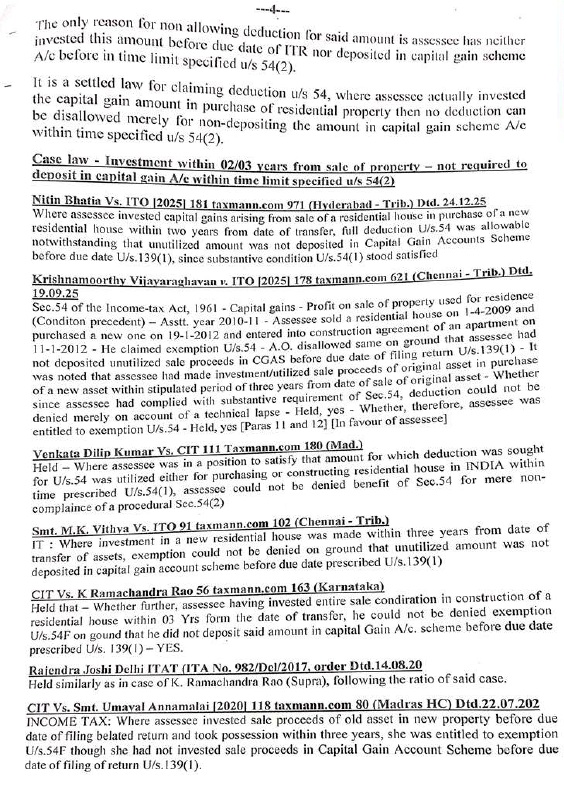

4. The Ld. Counsel for the assessee furnished the following brief note :-

5. Heard rival submissions and perused the orders of the authorities below. I find considerable merit in the submissions of the Ld. Counsel for the assessee. The issue as to whether the assessee is entitled for exemption u/s.54 in respect of investment made into two houses came up for consideration before various Tribunals and High Courts and it was interpreted the word “a” as occurring in Section 54 of the Act, that it was not the intention of the legislature to convey the meaning that it refers to only a single residential house. It is observe that the Hon’ble Delhi High court in the case of CIT v. Gita Duggal (Delhi)/ITA No.1237/2011 dated 21.02.2013 held as under:-

“5. The revenue carried the matter in appeal before the Tribunal and raised the following ground:-

“On the facts and on the circumstances of the case Ld. Commissioner of Income Tax (Appeals) has erred in law and on the facts in deleting the addition of ‘98,20,722/u/s. 54F of the IT Act, 1961 which the Assessing Officer had allowed in respect of only one unit by treating the units as two separate residential properties.”

The Tribunal confirmed the decision of the CIT (Appeals) by observing as under: –

“6. We have heard the rival contentions in light of the material produced and precedent relied upon. We find that Id. counsel of the assessee submitted that the issue is squarely covered in favour of the assessee by the decision of the Hon’ble Karnataka High Court in the case of CIT & Anr. v. Smt. K.G.Rukminiamma in ITA No. 783 of 2008 vide order dated 27.8.2010 wherein it was held as under :-

“The context in which the expression „a residential house” is used in Section 54 makes it clear that, it was not the intention of the legislation to convey the meaning that: it refers to a single residential house, if, that was the intention, they would have used the word “one.” As in the earlier part, the words used are buildings or lands which are plural in number and that: is referred to as “a residential house”, the original asset. An asset newly acquired after the sale of the original asset also can be buildings or lands appurtenant thereto, which also should be “a residential house.” Therefore, the letter “a” in the context it is used should not be construed as meaning “singular.” But, being an indefinite article, the said expression should be read in consonance with the other words „buildings” and lands” and, therefore, the singular a residential house” also permits use of plural by virtue of Section 13(2) of the General Clauses Act. CIT V. D. Ananda Bassappa (2009) 223 (kar) 186: (2009) 20 DTR (Kar) 266 followed.”

7. Upon careful consideration, we find that the contentions of the assessee that the issue is covered in favour of the assessee are correct.

7.1 Ld. Departmental Representative could not controvert the above and no contrary decision was cited before us.

8. Accordingly, we do not find any infirmity or illegality in the order of the Ld. Commissioner of Income Tax (Appeals) and hence, uphold the same.”

6. Similarly the Hon’ble Karnataka High Court in the case of Arun K. Thaiagarajan (supra) held as under :-

“11. From close scrutiny of the aforesaid provision, it is axiomatic that property sold is referred to as original asset and the original asset is prescribed as buildings and lands appurtenant thereto and being a residential house. The expression ‘a residential house’ therefore, includes building or lands appurtenant thereto. It cannot be construed as one residential house.

12. A Bench of this court case of Smt KG Rukminiamma supra dealt with the meaning of expression ‘a residential house used in Section 54(1) of the Act while taking into account Section 13(2) of the General Clauses Act, 1897 held that unless there is anything repugnant in the subject or context, the words in singular shall include the plural and vice versa. It was further held that context in which the expression ‘a residential house’ is used in Section 54 makes it evident that it is not the intention of the legislature to convey the meaning that it refers to a single residential house. It was also held that an asset newly acquired after sale of original asset can also be buildings or lands appurtenant thereto, which also should be residential house, therefore, the letter ‘a’ in the context it is used should not be construed as meaning singular, but the expression buildings and lands. Accordingly, the contention raised by the revenue was rejected. Similar view was taken by o bench of this court in Khoobchand M. Makhtia supra, B.Srinivas supra and in the case of Smt Jyothi K Mehta supra. The Madras High Court while dealing twith Section 54 of the Act as it stond prior to amendment by Finance Act No.2/2014 in the case of Tilokchand and Sons supra took the similar view and held that the word ‘a’ would normally mean one but in some circumstances it may include within its ambit and scope some plural numbers also. The Delhi High Court also took the similar view in case of Gita Duggal supra.

13. It is well settled in law that an Amending Act may be purely clarificatory in nature intended to clear a meaning of a provision of the principal Act, which was already implicit. In view of aforesaid enunciation of law by different High Courts including this court and with a view to give definite meaning to the expression ‘a residential house’, the provisions of Section 54(1) were amended with an object to restrict the plurality to mean singularity by substituting the word a residential house’ with the word ‘one residential house’. The aforesaid amendment came into force with effect from 01.04.2015. The relevant extracts of Explanatory note to provisions of Finance Act No.2/2014 reads as under:

20.3 Certain courts had interpreted that the exemption is also available if investment is made in more than one residential house. The benefit was intended for investment in one residential house within India. Accordingly, sub-Section (1) of Section 54 of the Income-Tax Act has been amended to provide that the rollover relief under the said Section is available if the investment is made in one residential house situated in India.

20.5 Applicability: – These amendments take effect from 1st April, 2015 and will accordingly apply in relation to Assessment year 2015-16 and subsequent Assessment years.

Thus, it is axiomatic that the aforesaid amendment was specifically applied only prospectively with effect from Assessment year 2015-16.

14. The subsequent amendment of Section 54(1) also fortifies the fact that the legislature felt the need of amending the provisions of the Act with a view to gwe a deforite meaning to the expression ‘a residential house’, which was interpreted as plural by various courts by taking into account the context in which the aforesaid expression was used. The subsequent amendment of the Act also fortifies the view taken by this court as well as Madras High Court and Delhi High Court. It is trite law that the principle underlying the decision would be binding as precedent in a case. In Halsbury Laws of England, Volume 22, Para 1682, Page 796, the relevant extract reads as under:

The enunciation of the reasons or principle on which a question before a court has been decided is alone binding as a precedent. This underlying principle is often termed the ratio decidendi, that is to say, the general reasons given for the decision or the general grounds on which it is based, detached or abstracted from the specific peculiarities of the particular case which gives rise to the decision.

15. This Court as well as Madras and Delhi High Court have interpreted the expression ‘a residential house’ and have held that the aforesaid expression includes plural. The ratio of the decisions rendered by coordinate bench of this court are binding on us and we respectively agree with the view taken by this court while interpreting the expression ‘a residential house’. Therefore, the contention of the revenue that the assessee is not entitled to benefit of exemption under Section 54(1) of the Act in the facts of the case does not deserve acceptance.

In view of preceding analysis, the substantial question of law framed by this court is answered in favour of the assessee and against the revenue. In the result, the order passed by the assessing officer and Commissioner of Income Tax (Appeals) and the Income Tax Appellate Tribunal insofar as it deprives the assessee of the benefit of exemption under Section 54(1) of the Act are hereby quashed and the is held entitled to benefit of exemption under Section 54(1) of the Act. In the result, the appeal is allowed.

7. Thus, respectfully following the said decision it is held that the assessee is eligible for exemption u/s.54 of the Act in respect of investment made in more than one property for assessment year under consideration.

8. Further we observed that in various decisions it was held that investment made beyond due date for filing ITR even though not deposited into capital gains scheme as referred to in the submissions of the assessee is eligible for exemption u/s.54 of the Act. Thus, respectfully following the said decisions the AO is directed to consider the investments made by the assessee even beyond due date of filing ITR as specified in section 54(2) while allowing in the exemption u/s.54 of the Act.

9. In the result, the appeal of the assessee is allowed.