A disallowance for unverifiable creditors was restricted to 25% when sales were accepted.

Issue

When the purchases made by a business are considered genuine (because the corresponding sales are accepted), but the creditors for those purchases are found to be non-existent or unverified, should the entire amount be added to income, or should a portion of the expenditure be disallowed?

Facts

- The assessee, a fabric and garment trader, had a large amount shown as “sundry creditors” in its financial statements.

- The Assessing Officer (AO) tried to verify these creditors by sending notices, but 20 out of 27 notices were returned unserved with remarks like “non-existent” or “wrong address.”

- Based on this, the AO concluded that the creditors were bogus and added the entire closing balance to the assessee’s income under Section 41(1), treating it as a liability that had ceased to exist.

- Two key facts were on record:

- For the assessee: The goods purchased from these parties were later sold, and the revenue department had accepted these sales as genuine.

- Against the assessee: The assessee settled the dues with these creditors in later years through a suspicious pattern of multiple small cash payments, all below the ₹20,000 threshold.

Decision

The Tribunal took a middle path and ruled partly in favour of the assessee.

- It reasoned that since the sales were accepted as genuine, the underlying purchases couldn’t be entirely fake. You can’t sell goods you never purchased in the first place. Therefore, the AO’s 100% addition was incorrect.

- However, the assessee’s failure to prove the identity of the creditors, combined with the suspicious cash payment method, strongly suggested that the purchase price was likely inflated to reduce profits.

- To account for this probable inflation, the Tribunal directed that the disallowance should be restricted to 25% of the value of the purchases made from these unverifiable parties.

Key Takeways

- Can’t Deny Purchases if You Accept Sales: This is a fundamental principle. If the tax department accepts the revenue from selling certain goods, it cannot logically argue that the goods were never acquired at all.

- Estimation is a Fair Middle Ground: In cases where transactions aren’t entirely bogus but are not entirely clean either, courts often resort to a reasonable estimation of the profit element. Disallowing a percentage (like 25% for a trader) is a common way to tax the likely profit without penalizing the entire transaction.

- Your Conduct Matters: The assessee’s own actions, like making a series of small cash payments to avoid scrutiny, damaged their credibility and supported the tax department’s suspicion, ultimately leading to the partial disallowance.

- Wrong Section Used by AO: The AO’s use of Section 41(1) was likely incorrect. This section applies when a genuine liability ceases to exist. The real issue here was whether the liability was genuine from the start. The Tribunal’s approach of disallowing a part of the purchase expenditure is the more appropriate way to handle such cases.

IN THE ITAT DELHI BENCH ‘G’

Smt. Sudha Loyalka

v.

Income-tax Officer

ANUBHAV SHARMA, Judicial Member

and Manish Agarwal, Accountant Member

and Manish Agarwal, Accountant Member

IT Appeal No. 399 (Delhi) of 2017

[Assessment year 2012-13]

[Assessment year 2012-13]

SEPTEMBER 12, 2025

Dr. Rakesh Gupta, Somil Aggarwal and Deepesh Garg, Advs. for the Appellant. Narpat Singh, Sr. DR for the Respondent.

ORDER

Manish Agarwal, Accountant Member.-The present appeal is filed by assessee against the order dated 01.12.2016 passed by Ld. Commissioner of Income Tax (A)-12, New Delhi [“Ld.CIT(A)”] in Appeal No. 26/15-16 u/s 250 of the Income Tax Act, 1961 [“the Act”] arising out of assessment order dated 18.03.2015 passed u/s 143(3) of the Act pertaining to Assessment Year 2012-13.

2. Brief facts of the case are that the assessee is an individual and filed her return of income on 27.09.2012, declaring total income of INR 3,52,180/-. The case of assessee was selected for scrutiny for the reason “large amount of sundry creditors”. Assessee is engaged in the business of trading of fabrics and readymade garments under the name and style as M/s. Tirupati Industries. The assessee has shown total sundry creditors of INR 6,77,21,342/-which includes INR 3,48,88,095/- under the title “Retail Creditors Control account”. In order to examine the genuineness of these creditors, AO issued notice u/s 133(6) of the Act to 27 parties out of which notices issued to 20 parities amounting to INR 2,78,20,495/-were returned back for the reason “wrong address/incomplete address/non-existed” etc. The AO thereafter, discussed each of the parties to whom notices were sent and reached to the conclusion that these parties are non-existent and made the addition of INR 3,50,94,758/- as bogus creditors.

3. Against the said order, assessee preferred an appeal before Ld. CIT(A) who vide impugned order dt. 01.12.2016, after considering the submissions of the assessee, dismissed the appeal of the assessee.

4. Aggrieved by the said order of Ld.CIT(A), assessee filed appeal before the Tribunal where the Tribunal vide its order dated 18.07.2018 in Smt. Sudha Loyalka v. ITO 303 (Delhi – Trib.)/ ITA No.399/Del/2017 [Assessment Year 2012-13] deleted the additions and allowed the appeal of the assessee. Aggrieved by the said order, Revenue preferred appeal before Hon’ble Delhi High Court and the Hon’ble Court in ITA No.607/2019 vide order dated 30.07.2024 has set aside the order of the Tribunal and remand it to the file of ITAT for examination the issue of creditors in the line of expenditure claimed u/s 37 of the Act. The relevant observations of the Hon’ble High Court as contained from para 6 to 10 of the order are reproduced as under:-

6. “Before us and on the basis of the arguments which were addressed, we find that the invocation of Section 69C of the Act would also not sustain since the said provision concerns itself with the source of expenditure. That was clearly not an issue of dispute.

7. The appellant would contend that apart from the above, the veracity of the expenditure would have to be examined on the anvil of Section 37, and which provision had been duly pressed into aid before the ITAT. We, however find that no specific finding in that respect has been returned by it.

8. While Mr. Rai is correct in his submission that the mere nonmentioning of a provision would not invalidate an addition as long as it be otherwise sustainable under the Act, we find that the matter would merit being remitted to the ITAT which may examine the issue afresh and bearing in mind the provisions contained in Section 37 of the Act.

9. We accordingly allow the instant appeal and set aside the order of the ITAT dated 18 July 2018. The matter shall stand remanded to the ITAT for considering the appeal afresh bearing in mind the observations made hereinabove.

10. All rights and contentions of respective parties are kept open.”

5. In compliance of the directions given by Hon’ble Jurisdictional High Court, the present appeal of the assessee is taken up for hearing.

6. The assessee has raised following grounds of appeal:-

1. “That having regard to the facts and circumstances of the case, Ld. CIT(A) has erred in law and on facts in confirming the action of Ld. AO in making aggregate addition of Rs.3,50,94,758/- on the alleged ground that sundry creditors were not proved as genuine and that too by recording incorrect facts and findings and without observing the principles of natural justice.

2. That in any case and in any view of the matter, action of Ld. CIT(A) in confirming the action of Ld. AO in making addition of Rs.3,50,94,758/- on the alleged ground that sundry creditors were not proved as genuine is bad in law and against the facts and circumstances of the case.

3. That having regard to the facts and circumstances of the case, Ld. CIT(A) has erred in law and on facts in confirming the action of Ld. AO in charging interest u/s 234A, 234B and 234C of Income Tax Act, 1961.

4. That the appellant craves the leave to add, modify, amend or delete any of the grounds of appeal at the time of hearing and all the above grounds are without prejudice to each other.”

7. Since all grounds of appeal pertaining to the addition of INR 3,50,94,758/- made by the AO by alleging the creditors as non-genuine therefore, all the grounds of appeal are taken together for adjudication in the line of the directions given by the Hon’ble High Court.

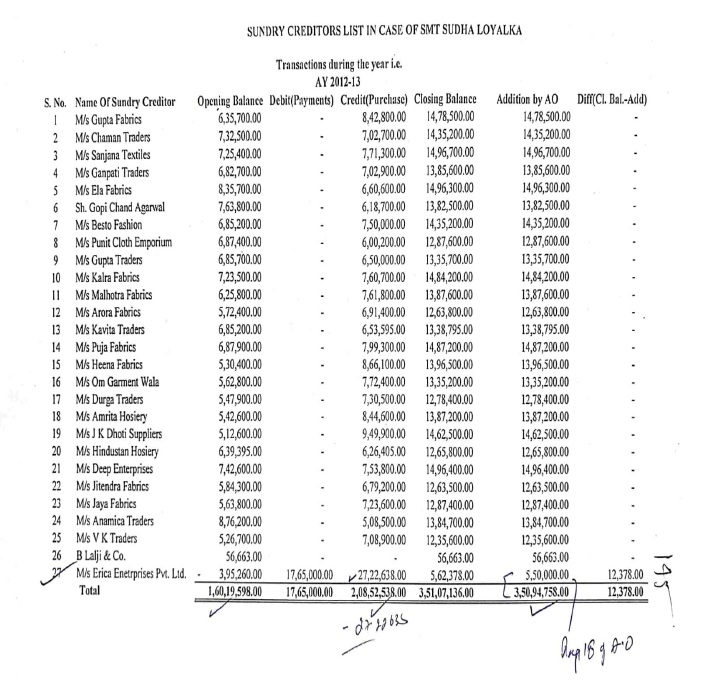

8. Before us, Ld.AR of the assessee submits that in the instant case total amount appearing as closing balances in the balance sheet was added in the hands of the assessee. It is submitted by Ld.AR that the Tribunal in its order dated 18.07.2018 observed that there were opening balances of INR 1,60,19,598/- and no expenses were claimed to the extent of this amount during the year therefore, no addition could be made. He further drew our attention to the fact that though addition was made u/s 41(1) of the Act however, since the Hon’ble High Court had directed to examine the claim of the assessee of this amount as expenditure u/s 37(1) of the Act therefore, it is to be seen what amount of expenditure was claimed against these creditors during the year under appeal. Ld.AR stated that assessee has made total purchase of INR 2,08,52,538/- from these creditors during the year under appeal as against which the addition of INR 3,50,94,758/- was made being the closing balances appearing against these parties.

9. Ld.AR stated that as per directions of Hon’ble High Court even if it is held that these creditors are non-existent / ingenuine creditors, even in such situation addition to the extent of INR 2,08,52,538/- could be made as assessee has claimed expenditure to this extent only as purchases. He further drew our attention to the chart available in paper book page 145 where at Serial No.27 of the list one creditor namely, M/s. Erica Enterprises Pvt. Ltd. from whom total purchase of INR 27,22,638/- was made during the year however, addition was made of only 5,50,000/-. He submits that this amount of purchase of INR 27,22,638/- is included in the amount of gross purchase of INR 2,08,52,538/- and since addition was made only for INR 5,50,000/- therefore, the remaining purchase of INR 21,72,638/- being accepted by the AO itself thus, no addition of this amount could be made. Ld.AR further submits that assessee has made purchase from these parties in earlier years where the purchases were accepted by the Departments and no doubts were raised in this regard in any of the preceding year and were allowed as incurred wholly and exclusively for the purpose of business. He further submits that amount of INR 1,60,19,598/- represents the opening balance for which no addition is required to be made. The chart at page 145 of the Paper Book is reproduced as under:-

10. It is submitted by Ld.AR that assessee has filed VAT returns wherein the input tax paid on such purchases was accepted by the VAT authorities therefore, the existence of these parties and claim of expenditure as purchases cannot be doubted. Ld. AR also submits that if the entire amount of purchase of INR 3,50,94,758/-is added back as unexplained expenditure, it would be resultant into impossible NP rate. Ld.AR of the assessee drew our attention to page 17 of paper book wherein trading results from FYs 2005-06 to 2014-15 are tabulated, a perusal of the same reveals that G.P rate was ranging between 1.88% to 4.13% during these years and if this purchase is added to the gross profit, the resultant GP would be impossible in the line of trade. It is further argued by Ld.AR that neither the sales were doubted nor trading results were doubted. Once sales were accepted, it cannot be said that goods were not purchased and thus, there is no question of making disallowance of purchase made. He, therefore, prayed for the deletion of the addition and submits that even no disallowance could be made u/s 37(1) of the Act.

11. On the other hand, Ld. Sr. DR supports the orders of the authorities below and filed a detailed written submissions wherein following arguments taken by the Revenue:-

Revenue’s stand

| (i) | On the Onus to Prove the Genuineness of Creditors: |

It is respectfully submitted that the addition of Rs. 3,50,94,758/- made by the Assessing Officer and confirmed by the Ld. CIT(A) is legally and factually sound. The entire addition arose from the assessee’s failure to discharge her statutory burden of proving the identity, existence, and genuineness of sundry creditors aggregating to over Rs. 3.5 crore. The creditors were shown as outstanding liabilities in the balance sheet. Despite specific notices issued under section 133(6) and show-cause notices under section 142(1), the assessee failed to file confirmations, produce addresses, or provide any third-party verification to substantiate the liabilities.

| (ii) | On Non-Compliance Despite Sufficient Opportunity: Contrary to the assessee’s allegations of violation of natural justice, the record shows that repeated and specific opportunities were provided to furnish confirmations and correct postal addresses. Notices under section 133(6) were issued to 27 creditors; 20 of these were returned unserved with postal remarks such as “no such firm,” “left,” “not known,” “incomplete address,” or “wrong address.” The AO further deputed an Inspector who conducted field inquiries and submitted a detailed report confirming the non-existence or untraceability of most of these parties. Thereafter, a notice was issued under section 142(1), but the assessee did not file a single confirmation or rebuttal from any of the 20 parties. |

| (iii) | On Admission by the Assessee During Appellate Proceedings: |

The assessee’s Authorized Representative admitted before the Ld. CIT(A) vide order sheet entry dated 27.07.2016 that addresses of the said creditors were no longer available. Further, vide submission dated 17.11.2016, it was stated that the assessee had no business transactions with these creditors in earlier years. These admissions go to the root of the matter and negate the claim that these were continuing trade payables.

| (iv) | On Cash Payments in Subsequent Years Without Evidence: |

The assessee stated that outstanding payments were made in cash in subsequent financial years. However, no ledger copies, cash book entries, or recipient confirmations were filed to substantiate these claims. In the absence of supporting documentary evidence, such vague explanations have no probative value. The use of cash for settling liabilities of this scale (over Rs. 2.78 crore) further weakens the claim of bona fide transactions and raises serious concerns about the authenticity of the alleged purchases.

| (v) | On Misplaced Reliance on VAT Returns and Audited Books: |

The assessee’s reliance on VAT returns and the fact that books were audited under section 44AB cannot substitute the requirement under the Income-tax Act to prove the genuineness of transactions recorded in the books. Similarly, acceptance of sales by VAT authorities does not imply acceptance of sundry creditors unless supported by verifiable evidence.

| (vi) | On Estimation of Profits and Rejection of Books: |

This is not a case where the AO rejected books of account and made a best judgment assessment. Instead, it is a case of specific unverified liabilities. The assessee’s attempt to invoke GP-based estimation principles is inapplicable, as the books themselves were relied upon for sales, but the liabilities shown therein lacked evidentiary support. Therefore, the claim that purchases should be estimated or accepted on profit margin consistency is legally untenable.

| (vii) | On Judicial Precedents Relied Upon by the Assessee: |

The assessee has cited several judgments relating to low GP, rejection of books, or additions made solely on the basis of non-service of summons. However, these cases are distinguishable. In the present case, the AO conducted thorough inquiries, obtained adverse postal remarks and Inspector reports, and gave multiple opportunities to the assessee to file confirmations or new addresses. In such a scenario, when both primary and secondary evidence is absent, the additions were rightly made.

| (viii) | On Legal Framework Governing the Addition: |

Under the scheme of the Act, where liabilities are claimed, the onus is on the assessee to prove that the transaction is genuine and that the liability subsists. The failure to do so, particularly in the case of liabilities which remain unpaid, unconfirmed, and unverifiable, warrants addition.

| (ix) | On CIT(A)’s Justified Findings: |

The Ld. CIT(A), in a reasoned and detailed order, has upheld the addition after confirming that neither during assessment nor appellate proceedings was any proof furnished regarding the identity or genuineness of the creditors. The appellate authority rightly held that in the absence of even a single confirmation or address, the liabilities were fictitious in nature and had to be added back to the income.

The entire pattern of non-compliance, lack of documentary evidence, absence of confirmations, vague explanations, and concession of lack of past dealings strongly supports the conclusion that the sundry creditors were non-existent and fictitious. The addition of Rs. 3,50,94,758/ made by the AO and confirmed by the CIT(A) is therefore fully justified in law and on facts.

In view of the above factual findings and legal submissions, it is respectfully prayed that the appeal filed by the assessee be dismissed in full and the order passed by the Ld. CIT(A) sustaining the addition of Rs. 3,50,94,758/-on account of sundry creditors be upheld in toto, as the assessee has failed to discharge the primary onus of proving the genuineness of the liabilities recorded in her books.”

12. Heard the contentions of both the parties and perused the material available on record. In the present case, Hon’ble Jurisdictional High Court had set aside the order of the Tribunal dated 18.07.2018 and remanded it to the Tribunal for considering the same afresh in the light of provisions of section 37 of the Act. It is further seen that Hon’ble High Court observed that no specific findings were given by the Tribunal with respect to the allowability of expenditure u/s 37 of the Act with respect to the purchase made by the assessee and disallowed by AO. However, the Hon’ble High Court has not made any adverse comments on the other observations made by the Tribunal with respect to the genuineness of the creditors.

13. From the perusal of the facts, we find that AO has not made the additions towards the purchase made during the year from the parties alleged as bogus but made additions of the closing balance of 27 creditors as is evident from the chart reproduced herein above. As per this chart, there was gross opening balance of INR 1,90,88,538/- as appearing in the accounts of all the 27 parties. In the same chart, purchases made from these parties was claimed to have been made of INR 2,08,52,538/- out of which the purchases made from M/s. Erica Enterprises Pvt. Ltd. of INR 27,22,638/- were accepted by the AO who had made the addition of INR 5,50,000/-only with respect to the difference in the balance as per assessee and as per the said party. Ld.AR submits the copy of ledger account of this parties for subsequent AY wherein INR 5,50,000/- was paid through Account Payee Cheque. Thus, total purchase made from M/s. Erica Enterprises Pvt. Ltd. could not be held as bogus/ non-verifiable and thus the expenditure booked for this purchases is genuine business expenditure incurred wholly and exclusively for the purpose of business and accordingly the addition of INR 5.50 Lakhs is hereby deleted. It is further seen that the closing balances of all remaining 26 parties was added as bogus creditors.

14. As observed above, Hon’ble Jurisdictional High Court has directed to examine the claim with respect to the application of provision of section 37 of the Act where the expenditure which is wholly and exclusively incurred for the purpose of business is to be allowed. In the instant case, as observed above, the expenses on account of purchase of goods from these parties had been sold and no doubts were raised with respect to the sales made by the assessee. All these facts lead to believe that AO has not considered the fact that goods purchased were duly accounted for and sold by the assessee in the regular course of business. Only question remained is whether these goods were purchased from the party in whose name credits are appearing or bills were obtained from theses parties for the goods supplied by other parties. From the perusal of the ledger accounts of these parties filed by the assessee as available in the Paper Book pages 76 to 134, it is seen that almost in all the cases, the payments were made in cash in subsequent years by the assessee and on every occasion, payment was below INR 20,000/- in cash on regular basis. This fact raised doubt about the genuineness of these creditor parties. Assessee is having bank account and nothing prevent to make the payments to these parties through banking channel but surprisingly, all the payments were made in cash in small sums. It is very surprising that payments were made below INR 20,000/- to these parties on daily basis, for which either the employee of assessee or of the creditor has to visit on daily basis to pay/collect the amount. As observed above, since the goods purchased were sold and sales have been accepted therefore, input of the goods cannot be doubted. From the perusal of the VAT returns filed by the assessee, it is seen that assessee has claimed input tax credit on the purchases however, the details of the parties from whose purchase input credit was claimed is not apparent/ verifiable from such returns and thus this claim cannot be verified.

15. Looking to the overall facts of the case and also considering the facts that entire outstanding balances were squared off by making payment in subsequent years in cash to these parties, we are not unable to accept the contentions of the assessee intoto and therefore, as against total addition of INR 3,50,94,758/-, we direct the AO to consider the credits to the extent of INR 2,08,52,538/-being the amount of purchase made during the year and claimed the expenditure in the light of the judgement of Hon’ble Jurisdictional High Court. It is further directed that out of the purchase made from alleged 27 parties of INR 27,22,638/- made from M/s. Erica Enterprises Pvt. Ltd. could not be doubted therefore, the remaining purchase of INR 1,81,29,900/- could be considered as purchase which was claimed as expenses and for which assessee has not able to discharge the burden of proving the genuineness of the parties. To sum up the issue and in the larger interest of justice, we hold that disallowance @ 25% of the remaining purchase of INR 1,81,29,900/- would be reasonable to meet the end of justice for any possible leakage of revenue. Accordingly, we direct the AO to disallow a sum of INR 45,32,475/-(25% of INR 1,81,29,900/-) on account of purchase made from the alleged 27 parties as unexplained expenditure. Therefore, grounds raised by the assessee are partly allowed.

16. In the result, appeal of the assessee is partly allowed.