Revision Order Quashed as Fee-Based Service for Member Banks is a General Public Utility.

Issue

Whether an entity, registered as a non-profit, that provides a transaction platform for its member banks in exchange for a nominal fee to cover costs is engaged in a “charitable purpose” of “general public utility,” or if this activity constitutes “trade, commerce, or business,” thereby justifying a revisionary order under Section 263 to deny its tax exemption.

Facts

- The assessee, a non-profit company registered under Section 25 of the Companies Act, provided a platform for its member banks to conduct transactions.

- It charged a nominal fee per transaction, which was intended only to cover the cost of infrastructure and operations. Any surplus was utilized for the company’s own capital expenditure.

- The Assessing Officer (AO) examined the activities, found no engagement in “trade, commerce, or business,” and accordingly allowed the assessee’s claim for exemption under Section 11.

- The Commissioner, however, invoked revisionary powers under Section 263. He held that the original assessment order was erroneous, arguing that the assessee’s fee-based activities were, in fact, in the nature of “trade, commerce, or business,” hitting the proviso to Section 2(15) and disqualifying it from the exemption.

Decision

- The High Court quashed the Commissioner’s revisionary order.

- It held that the assessee’s sole activity was recognized as a charitable purpose, falling within the category of an “object of general public utility.”

- The court found that charging a nominal fee to cover costs and passing on the benefits of economies of scale to its member banks did not convert this charitable activity into a commercial enterprise.

- Since the original assessment order was not erroneous, the Commissioner’s exercise of revisionary jurisdiction was invalid.

Key Takeaways

- Charitable Purpose Can Involve Fees: An activity of “general public utility” (like providing a shared platform for banks) does not cease to be charitable simply because a nominal fee is charged to sustain the operation.

- Motive Matters, Not Surplus: The test is not whether a surplus is generated, but what the motive of the activity is. Here, the motive was to provide a service to members at cost, not to earn a profit. Using the surplus for capital expenditure to further the object reinforces the non-profit motive.

- High Bar for Section 263: A Commissioner cannot use Section 263 to substitute their own opinion for that of the Assessing Officer. The revisionary power can only be invoked if the original order is both erroneous and prejudicial to the revenue, which was not the case here.

- Proviso to Section 2(15) Not Automatically Triggered: The proviso to Section 2(15) (which restricts commercial activities) is not attracted when the primary object is charitable and the collection of fees is merely incidental to achieving that object.

IN THE ITAT MUMBAI BENCH ‘B’

National Payments Corporation of India

v.

CIT (Exemptions)

Amit Shukla, Judicial Member

and Girish Agrawal, Accountant Member

and Girish Agrawal, Accountant Member

IT Appeal No.3652 (MUM) of 2025

[Assessment year 2020-21]

[Assessment year 2020-21]

OCTOBER 9, 2025

Niraj Sheth and Ms. Niyati Parikh, Advs. for the Appellant. Satya Prakash Singh, Sr. DR for the Respondent.

ORDER

Girish Agrawal, Accountant Member.- This appeal filed by the assessee is against the order of Commissioner of Income Tax (Exemptions), Mumbai, vide order no. ITBA/REV/F/REV5/2024-25/1075324373(1), dated 31.03.2025, passed u/s. 263 of the Income-tax Act, 1961 (hereinafter referred to as the “Act”), for Assessment Year 2020-2021.

2. Grounds taken by the assessee are reproduced as under:

“1) The Learned Commissioner of Income Tax (Exemptions) [“Ld. CIT (E)”] erred in initiating revision proceedings under section 263 of the Income Tax Act, 1961 (“the Act”). Your Appellants submit that the initiation of proceedings under section 263 of the Income Tax Act, 1961 is illegal and bad in law and the order of the Ld. CIT (E) be quashed.

2) The Ld. CIT (E) erred in stating that there is failure on part the Assessing Officer to apply correct position of law for AY 2020-21 on the ground that Ld. AO had passed the Assessment Order without making necessary inquires and verification before allowing exemption u/s 11 of Income Tax Act, 1961 since the Appellant company was hit by proviso to section 2(15) of the income tax act, 1961 for AY 2017-18 to AY 2019-20. Looking into the facts & circumstances of your Appellant it is submitted that specific queries with respect to clarification “on business income of the trust” and “detailed note on activities carried on by NPCI and explanation as to why the activities of the trust is not hit by proviso to section 2(15) of the income tax act, 1961” were already raised by the Ld. AO in his notices dated 29/06/2021 & 12/11/2021 during the course of assessment proceeding. In response your Appellant vide acknowledgement nos. 154780881140721, 239793631171221, 239970781171221 and 245265231171221 uploaded the necessary details alongwith the Annexures. Thereafter Ld. AO after due application of his mind and in accordance with law, passed the assessment order by accepting the claim of exemption. Therefore proceedings under section 263 of the Income Tax Act, 1961 is illegal, bad in law and the order of the Ld. CIT (E) be quashed.

3) The Ld. CIT (E) erred in applying deeming provision of explanation 2 to Section 263 on the ground that Ld. AO failed to examine or conduct requisite inquiries for the relevant issues. Looking into the facts & circumstances of your Appellant it is submitted that specific queries with respect to relevant issues were already raised by Ld. AO. Thereafter after due application of mind and in accordance with law, Ld. AO passed the assessment order. Therefore, assessment order passed is not erroneous & prejudicial to the interest of the revenue.

3. This issue raised by the assessee is in respect of initiation of revisionary proceedings u/s 263 and passing the revisionary order thereafter. Broadly, the assessee’s contentions are that the Ld. AO has failed to apply correct position of law as held by Ld. Commissioner of Income-tax (Exemptions) [in short ‘the Ld. CIT(E)’], since the Ld. AO did not carry out necessary inquiries and verification while allowing exemption u/s 11 as assessee is hit by proviso to section 2(15) of the Act. According to the Ld. CIT(E), claim of exemption u/s 11 was denied to the assessee for A.Y. 2017-18 to A.Y. 2019-20 since hit by proviso to section 2(15), fact of which formed the basis for taking up the impugned revisionary proceedings.

3.1. Broader contentions of the assessee are that it had made detailed submissions in the course of assessment proceedings to the specific queries and clarifications sought by the Ld. A.O. on the business of the trust and activities carried by the assessee not hit by proviso to section 2(15) of the Act. Ld. A.O. had applied his mind and after taking into consideration the provisions of law, completed the assessment by accepting the claim of exemption. Hence, the impugned revisionary proceedings and the revisionary order thereafter are bad in law, liable to be quashed.

4. Brief facts of the case are that assessee filed its regular return of income on 11.02.2021, reporting total income at Nil. Case of the assessee was taken up for scrutiny assessment by issuing notice u/s 143(2). Reasons for the said selection are listed below:

| i. | Business Income of Trust |

| ii. | Accumulation of Income by Trust |

| iii. | Receipts of Trust |

| iv. | Refund Claim |

| v. | Transaction of Trust with Specified Persons vi. Foreign Outward Remittance |

4.1. In the course of assessment proceedings, notices u/s 142(1) were issued on 12.11.2021 and 23.03.2022. Details of the notice issued and replies filed by the assessee are tabulated below:

| Sr. No. | Dates of Notices issued by AO | U/s. | Date of Online Reply filed | Acknowledgement No. |

| 1 | 29/06/2021 (Annexure 1) | 143(2) | ,14/07/2021 | 154780881140721 |

| 2 | 12/11/2021 (Questionnaire of Points) (Annexure 2) | 142(1) | 22/11/2021 | 869065191221121 |

| 17/12/2021 | 239793631171221 (Annexure 4) | |||

| 17/12/2021 | 239970781171221 (Annexure 5) | |||

| 17/12/2021 | 245265231171221 (Annexure 6) | |||

| 22/12/2021 | 320560351221221 | |||

| 3 | 23/03/2022 (Annexure 3) | 142(1) | 31/03/2022 | 564193491310322 |

4.2. In the first notice, specific query was raised vide point No. 5 which stated “brief note of activities carried out during the F.Y. 2017-18 relevant to A.Y. 2018-19. Submission of the annual report would not be treated a replacement of the brief noted”. Further, in the same notice in query at serial No. (iv) titled as “with respect to business income of the trust guideline provide the following “.(iv) your explanation regarding the above stated income of the trust with object for advancement of general public utility, within the mandatory limit mentioned in the proviso to section 2(15)”. In the second notice specific query was raised with regard to details of utilization of accumulated amount along with evidences. The assessee made detailed submissions with corroborative documentary evidences for which e-proceeding response acknowledgement dated 17.12.2021 is placed on record. Ld. A.O. completed the assessment by taking note of all these submissions. In the assessment order, he noted that statutory notices necessary for scrutiny assessment were issued and duly served on the assessee which were duly complied. Thus, he completed the assessment by accepting the income returned by the assessee.

5. Subsequent to the above, from the perusal of the records, the Ld. CIT(E) drew his preliminary consideration that from the records of the earlier years from A.Y. 2017-18, 2018-19 and 2019-20, it has been held that assessee is hit by amendment to section 2(15) made in Finance Act, 2015 w.e.f. 01.04.2016 and thus, assessee has lost its charitable character for the respective assessment years. Accordingly, claim of exemption u/s 11 or 12 was denied. Contrary to this, ld. A.O. has allowed full exemption in the year under consideration without taking into account the aforesaid position taken in the earlier years which are on same set of facts. According to him, there is a failure on the part of the Assessing Officer to apply the correct position of law and thus, he prima facie observed that the assessment so completed by the Ld. A.O. is erroneous in so far as prejudicial to the interest of Revenue.

5.1. A show cause notice u/s 263 was issued dated 04.03.2025 to which assessee made a detailed and exhaustive submission. The summary of the submissions made by the assessee in revisionary proceedings are as under:

| (i) | Assessee submitted that in response to notice u/s 142(1), issued during the course assessment proceedings, detailed submission was made before Assessing Officer. And hence the aforementioned issue has already been examined. |

| (ii) | Assessee submitted that it is prohibited by its memorandum of association (MoA) from carrying of any business activity and therefore first proviso to section 2(15) regarding commercial activity cannot not be invoked. |

| (iii) | It was submitted that on the same aforementioned issue for A.Y. 2010-11 and A.Y. 2012-13, Coordinate Bench had decided in favour of the assessee. |

| (iv) | It also placed reliance on various case laws to submit that revision proceedings u/s. 263 cannot be invoked. |

5.2-5.3. After taking into account the submission made by the assessee, ld. CIT(E) by taking note of the objects contained in MoA observed that this can at best be taken as object of advancement of any other object of general public utility as defined in section 2(15) of the Act. According to him, assessee has received income from providing services as platform in respect of transactions conducted for member banks. Assessee has also paid service tax for the services rendered to its member banks. Hence, its purpose is not a charitable purpose. He further observed that objects of the trust are in the domain of advancement of general public utility by taking into account the specific amendment brought by way of proviso to section 2(15) w.e.f. A.Y. 2009-10. He noted that nature of activity of the assessee is very much in relation to trade, commerce or business and thus, is hit by proviso to section 2(15). He then referred to Explanation 2 to section 263 introduced by Finance Act, 2015 to hold that there is a failure on the part of the AO to conduct proper inquiries and verifications which rendered the impugned assessment order erroneous and prejudicial to the interest of the Revenue. The impugned assessment order was thus, set aside for de novo assessment with a direction to make necessary detailed inquiries on the issues listed by him.

6. Before we deal on the issue, it is important to take note of the background under which the assessee was set up, the objects which are required to be fulfilled by it and the nature of activities and benefits derived by the general public from its activities. These have been elaborately dealt and discussed in the decision of the Co-ordinate Bench of ITAT, Mumbai in assessee’s own case for A.Y. 2010-11 and 2012-13 in National Payments Corporation of India v. Dy.CIT ITD 412 (Mumbai – Trib.)/ITA No. 5431/Mum/2015 and ITA No. 3382/Mum/2016, order dated 06.07.2020. These details were furnished by the assessee in the course of assessment proceedings which are placed on record in the Paper Book. The relevant details in this respect are extracted below for ready reference:

“1.1 Government of India had introduced ‘The Payment and Settlement Systems Bill 2006’ in year 2006 to facilitate the oversight of Payments and Settlements Systems in the country by Reserve Bank of India. After review of the bill by a Parliament Committee i.e. Standing Finance Committee (SFC), the said bill was introduced in the Lok Sabha and Rajya Sabha for approval. After discussion, the said Payment and Settlement Systems (PSS) bill was passed by Lok Sabha on 26/11/2007 and became an Act (Annexure -12.1). Section 2(1) (i) of the PSS Act 2007 defines a payment system to mean a system that enables payment to be effected between a payer and a beneficiary, involving clearing, payment or settlement service or all of them, but does not include a stock exchange (Section 34 of the PSS Act 2007 states that its provisions will not apply to stock exchanges or clearing corporations set up under stock exchanges). It is further stated by way of an explanation that a “payment system” includes the systems enabling credit card operations, debit card operations, smart card operations, money transfer operations or similar operations. In terms of Section 4 of the PSS Act, 2007 no person other than the Reserve Bank can operate or commence a payment system unless authorized by the Reserve Bank

1.2 The Hon’ble Finance Minister of India, while presenting the PSS Bill in Parliament, 2007 had indicated the need for setting up of a robust Payment and Settlement Infrastructure.

To quote “There are also 1068 clearing houses in this country. Today clearing is not regulated. This is being done under a contractual arrangement. So, these 1068 units will come under the National Payment Corporation of India, which will be licensed by the Reserve Bank of India and regulated by the Reserve Bank of India.” Unquote

Hon’ble Minister further committed that NPCI would be set up as a Non Profit Corporation and a Section 25 company and that no profit money will be distributed as dividend to any shareholder but will be kept with the NPCI only for improving the equipment and to cover the cost. (Extract from the speech of Hon’ble Finance Minister in the Parliament- Annexure -12.2).

1.3 RBI Deputy Governor before SFC stated in Para 32 of SFC Report, that “RBI has not been operating the clearing system to generate income. Income generation is only incidental. The profit to be generated by the new company would not be paid to the shareholders as dividend, but would be used for further development of payment system.

1.4 The Finance Ministry in reply to the SFC (Standing Finance Committee Report – Annexure -12.3 stated in Para 37 of SFC Report that NPCI (when it is set up) would be subject to the regulation and supervision of RBI under the proposed ACT and the regulations framed there under. RBI would also have a nominee in the Board of Directors of the NPCI. Though majority shareholding of the NPCI has not been explicitly stated in the Articles of Association or Memorandum of Association, public sector banks would have significant representation on the Board of NPCI (based on their percentage share in the volume of payment transactions) and would therefore have substantial powers in the decision making process. However, later PSS Act prescribed minimum Shareholding of 51% by Public Sector banks.

1.5 On the issue of exercising control, Finance Ministry, in response, informed SFC as stated in Para 38 of SFC Report”. Control through regulation and supervision can be used as effective instrument to ensure that NPCI operates in public interest. It is primarily for this reason that NPCI is going to be registered under Section 25 of the Companies Act whereby, the profit would not be distributed to the shareholders but would be utilized for ploughing back into the business of NPCI. This will financially strengthen NPCI and enable it to introduce more efficient and customer friendly payment modes and increase the reach of the payment systems to smaller towns and rural areas.”

1.6 To implement the Payments and Settlements Act, 2007, Reserve Bank of India and Indian Banks Association established NPCI as a ‘Not for Profit Company’ u/s 25 of the Companies Act, 1956 on 19/12/2008 with the certificate of commencement of business issued on 20/04/2009 by the Registrar of Companies, Maharashtra. Thus, it is established that NPCI has been established under the Payment and Settlement Systems Act, 2007 with the object of administering the activity of payment and settlement for the benefit of general public. The main objects of NPCI as per Memorandum and Articles of Association (Annexure 12.4) are:

(a) To develop a secure dedicated and robust communication backbone for the banking and financial sector and the other participant and to design, develop and implement critical payment system.

(b) To promote the activities of bankers’ clearing house, owning, establishing operating, maintaining and consolidating payment systems for promoting, sound, efficient, and cost effective clearing and payment systems and to do all such acts and deeds as are necessary to ensure deeper penetration into smaller places.

No object of the Company shall be carried out without permission of the relevant competent authorities and no object of the company shall be carried out on a commercial basis.

1.7 It may be noted that section 25 of the Companies Act, 1956, was a special provision of Companies Act 1956 which are set up for promoting commerce, arts, science, charity or any other similar useful objects to promote public good & which do not intend to distribute their profits by way of dividend & in case of dissolution or winding up the residual surplus is not distributed amongst members but were to be transferred to specified entity having similar objects.

1.8 Accordingly, the Payment and Settlement functions of RBI were divested to NPCI. It is submitted that income from Payment and Settlement functions of the RBI before transfer to NPCI were not subject to tax and not considered as business activity. Therefore, income from the Payment and Settlement functions of the RBI when divested to NPCI a “not for profit company” cannot be considered as business activity and subject to tax.

1.9 Thus on the basis of the characteristics of ‘not for profit organization, object being administering payment and settlement activity for the benefit of the general public, NPCI was granted registration u/s 12AA of the Income Tax Act, 1961 by the Director of Income Tax (Exemptions), Mumbai with effect from 1 April 2009 and its name is appearing at No 42963 in the Register of application u/s 12AA maintained by the Income tax authorities. (Certificate under section 12AA of the Income Tax Act, 1961- Refer annexure 12.5).

NON-DISTRIBUTION OF INCOME AS DIVIDEND

1.10 As per Para V (2) of the Memorandum of Association (Refer annexure 12.4), NPCI is prohibited from distribution of income or property directly or indirectly by way of dividend, bonus or otherwise by way of profits to any person/members of the company.

ON WINDING UP OF NPCI

1.11 As per Para XI of the Memorandum of Association (Refer annexure 12.4), NPCI is prohibited from distribution of net surplus, assets or property on winding up or dissolution or merger or amalgamation of NPCI among the members of NPCI but has to be handed over or transferred such other body, organization or company having similar objects or to anybody constituted mainly for the benefit of the company in the advancement of knowledge, commerce, or any other object of general public utility.

2. About NPCI

2.1 As committed by the Hon’ble Finance Minister of India in Parliament, NPCI is building Central Payment System Infrastructure which would be used by all the banks to provide modern Payment Services to general public in a very cost effective manner. For building the Technology Infrastructure, NPCI has raised Share Capital from 10 major Banks and also plans to raise debt to meet its Project expenditure. Promoter Banks were mere subscribers to NPCI’s share capital & not entities who made substantial contribution of exceeding Rs.50,000 in NPCI.

2.2 As part of implementing Payment System, NPCI at present is operating the National Financial Switch for Inter Bank ATM Switching (NFS), Cheque Truncation Services (CTS), Immediate Payment Service (IMPS), National Automated Clearing House (NACH), Aadhaar Enabled Payment System (AePS), Unified Payments Interface (UPI) and National Electronic Toll Collection (NETC). In order to meet the cost of infrastructure and operations, NPCI is charging a nominal fee per transaction to the banks as decided in consultation with RBI to cover the said cost, the surplus if any generated is being utilized to meet the huge capital expenditure. Being a ‘Non Profit Corporation’ as envisaged by the Hon’ble Finance Minister of India in Parliament, surplus if any at any point of time cannot be distributed as Dividend to its shareholders by NPCI, but is to be utilized for carrying out the objects of NPCI which are not commercial in nature. A nominal fee charged is nothing but to recover the cost incurred and not to earn profits on commercial basis.

2.3 Thus NPCI’s focus is to provide electronic mode of payments and settlement to general public at a minimum cost, all over India. It may be appreciated that electronic payment infrastructure system will enable a large section of society in India to have unparalleled access to secure and convenient payments. This fact establishes that NPCI is an institution of importance throughout India.

2.4 The role of NPCI has been articulated in RBI’s Payment Vision Document 2009-2012 and also in the draft Vision Document for 2012-15. (Important Extracts of Payments System Vision Document 2012-15 of RBI Annexure 12.6). As per the Vision Document, the new initiatives in the retail payment system will be carried forward in coordination of NPCI.

2.5 Upto 31/03/2020 NPCI has invested about Rs 765.59 crores in establishing robust payment systems and its infrastructure. Considering the way in which NPCI is introducing various innovative payment products and working with UIDAI and NIA, huge capital investment will be required to create the infrastructure to carry out the objects of NPCI for which capital alone will not be sufficient but also ploughing back of surplus is a must which will help NPCI to achieve its objectives as committed by Hon’ble Minister of Finance on the floor of the Parliament.

3. BENEFITS TO THE GENERAL PUBLIC

3.1 The benefits due to NPCI administering the Payments and Settlement Systems for the benefit of general public throughout the country and generally people of India are as follows:

Nominal Cost

(a) The system and processes being developed are in the form of utility infrastructure to be commonly used by banks at a very nominal cost which in turn would bring down the cost of transaction processing significantly and the ultimate beneficiaries will be the general public availing banking services.

(b) NPCI use to charge a Nominal fee of Re. 1 per chargeable transactions undertaken by customers upto 31st March, 2010 which was drastically reduced to Rs. 0.30 per transactions over a period of time i.e w.e.f 01st April 2019 onwards i.e the charges have been reduced by 70% (Annexure 12.7) It may be noted that despite virtually enjoying the monopoly over the payment system, the assesse company reduced the amount charged to banks for operating the payment system which shows that not only its object but also its activities were carried on without any profit motive.

Access to Affordable Payment Services

(c) A greater penetration of an e-payment set-up will not only encourage greater participation from the citizens in under banked and rural areas, it will also enable the Governments – both at Central and State level to make transfer of benefits digitally. There is a growing realization that access to affordable payment services be treated as fundamental as access to education and healthcare.

Elimination of Unaccounted Money

(d) It will also help in terms of elimination of unaccounted money by way of reduced cash transactions and also meet the global challenge to prevent money laundering and move towards cashless economy. Thus overall purpose is to achieve broad based social objectives to bring efficiency in the clearing system in India with a view to benefit society at large and therefore it can be concluded that NPCI objectives were to promote the welfare of general public.

3.2 The above are only some of the benefits. There are lot of intangible benefit in terms of operational convenience, security features, innovative solutions which will go a long way to improve the national health and standard of living of Indian citizens.

4. NPCI’S SERVICE INITIATIVES

As already stated earlier, NPCI has initiated the setting up of National financial Switch, Cheque Truncation system, Inter Bank Payment System and Automated Clearing House contributing towards consolidating and integrating various retail payment systems and also build central infrastructure that would cater to the need of all banks to provide affordable payment services to all, including the residents unbanked so far under Financial inclusion programme, NPCI has also developed domestic card payment system with an object that such an emerging market like India with growing financial transactions should not depend entirely on international card scheme like Master Card and VISA. Hence “RuPay” was developed to compete with the international schemes to save crores of foreign exchange outflows by way of commission / fees paid to such agencies.

5. NATURE OF ACTIVITY CARRIED OUT BY NPCI

As of date, NPCI has received authorization from RBI under the PSS Act to build a central infrastructure for payment systems like NFS, IMPS, CTS, National Automated Clearing House, AePS, APBS, NETC, UPI and RuPay.

In brief they are as follows;

5.1 National Financial Switch (NFS)

With a view to connect the ATMs in the country and facilitating convenient banking, the Institute of Development and Research in Banking Technology (IDRBT) conceptualized and operationalized a multilateral domestic ATM network referred to as National Financial Switch (NFS). NFS facilitates routing of ATM transactions through interconnectivity between its member institutions thereby enabling citizens to utilize any ATM of a connected entity. In October 2009, IDRBT handed over NFS to NPCI. Since the takeover, NPCI has made various improvements in technology and usage of NFS. Since NFS facilitates interbank ATM transactions, it is also used as a backbone network infrastructure for other NPCI products like IMPS, AePS, etc. With the inclusion of Scheduled Commercial Banks, Foreign Banks, Cooperative Banks, etc. as its members, NFS is the leading ATM network in the country. To take an example, if a customer of Punjab National Bank (PNB) uses an ATM of State Bank of India (SBI) to withdraw Rs. 10,000, then, SBI will claim Rs. 10,000 from PNB through the payment mechanism provided by NPCI. NPCI will recover Rs. 10,001 from PNB (including its charge of Re.

1) by debiting this amount to PNB and will credit Rs. 10,000 to SBI. Certain other charges and government levies are also recovered on actual basis on these transactions, which are pass-through costs. In this transaction, Re 1 is the income of the NPCI, which currently stands reduced to Rs. 0.30 per transaction. In case a customer of SBI uses the ATM of SBI, then, NPCI does not come into the picture.

NFS manages more than 95% of the interbank ATM transactions. As on date there are about 1199 members that includes PSU Banks, Private & foreign banks, co-operative banks, RRBs and White Label ATM Operators (WLAOs) using NFS network connected to more than 2.52 Lac ATMs.

5.2 Immediate Payment Service (IMPS)

IMPS is a 24X7, real time, cost effective, independent retail payment service introduced by NPCI empowering customers to transfer money instantly within banks and RBI authorized Prepaid Issuers (PPIs) across India. This innovative service launched as an instant mobile remittance solution in November 2010 has today evolved into a multi-channel, multidimensional remittance platform. The IMPS platform today is capable of processing P2P (Person to Person), P2A (Person to Account), P2M (Person to Merchant) and ABRS (Aadhar-based remittance system). Remittance and transactions can be initiated from Mobile, Internet, ATM as well as branch channels. In addition to banking customers, non- banking customers can also avail the IMPS facility through PPIs.

The underlying concept behind IMPS is to provide customers “any time, any place” real-time remittance access to meet their various payment needs. Using IMPS, a customer can transfer funds real-time to another person or merchant for any personal or commercial purposes.

IMPS is also emerging as a preferred mode for receiving inward cross border remittance by Banks. IMPS was launched on November 22, 2010. IMPS Ecosystem has touched new high with 637 members which includes banks & PPI. IMPS is also becoming popular in processing the domestic leg of foreign inward transaction which enables fund transfer in no time and also on holidays.

5.3 Cheque Truncation System (CTS)

An electronic image of the cheque is transmitted to the drawee bank by the clearing house, along with relevant information like data on the MICR band, date of presentation, presenting bank, etc. Thus in CTS, the physical movement of cheques from banks to clearing houses are replaced by electronic images of the cheques and the relevant data. Physical cheques are retained at the presenting bank itself.

The images and data are transmitted over the secured network. The settlement of the CTS is based on the MICR data captured from the cheques. NPCI was entrusted with the responsibility of the implementation of CTS on a PAN India level by the Reserve Bank of India.

5.4 National Automated Clearing House (NACH)

National Automated Clearing House (NACH) is a web based solution to facilitate interbank, high volume, electronic transactions which are repetitive and periodic in nature. NACH System can be used for making bulk transactions towards distribution of subsidies, dividends, interest, salary, pension etc. and also for bulk transactions towards collection of payments pertaining to telephone, electricity, water, loans, investments in mutual funds, insurance premium etc. There are 1,299 banks participating in NACH.

5.5 Aadhaar Enabled Payment System (AePS & KYC)

NPCI have gained substantial attention from the leading banks on this front. As on date, 140+ on-board entities, including RRB’s, Cooperative Banks are live on AePS platform. Banks are offering inter-bank AePS services as well. Banks have been issuing Aadhaar based RuPay debit cards. Authentication of these cards is being done basis Aadhaar number. NPCI is also offering eKYC services, wherein UIDAI shares the customer’s Proof of Identity and Proof of Address details electronically, post customers biometric authentication. NPCI is also offering demographic authentication services, wherein bank verifies demographic details provided by customer along with his/her Aadhaar number on a real time basis for account seeding purposes.

5.6 Aadhaar Payment Bridge System (APBS)

Aadhaar Payments Bridge is one of the services offered by NPCI using the Aadhaar number issued by the Unique Identification Authority of India (UIDAI). APB system is used for processing credit transactions pertaining to various Government / Government agency distribution. NPCI uses Aadhaar number as a key for electronically channelizing the Government benefits and subsidies to the Aadhaar enabled Bank Accounts (AEBA) of the intended beneficiaries.

5. 7 RuPay

RuPay has been conceived to fulfill the vision of RBI of offering a domestic, open-loop, multilateral payment system to all banks and financial institutions in India. RuPay will be instrumental in creating a less-cash economy and furthering the electronic payments system to make India a financial inclusive economy. RuPay was launched on 26th March 2012 at the hands of Late President Shri. Pranab Mukherjee.

The Major achievement of RuPay is Network to Network Agreement signing between NPCI & Japan Credit Bureau International (JCBI) on June 29th, 2015, for the purpose of Acceptance of JCB cards at ATM & POS terminals in India and Issuance of RuPay International cards. Nondisclosure Agreement and MOU has been signed between NPCI & UnionPay International (UPI) on February 03, 2015 for the purpose of Acceptance of China UnionPay (CUP) cards at ATM & POS terminals in India. RuPay issuance accounts for approximately 43% of 867million cards in circulation in the country. RuPay is now accepted on all three channels ATM, POS and e-commerce. RuPay Platinum card is now being issued by more than 40 banks. The various features available on RuPay Platinum cards is now being issued by more than 40 banks.

5.8 Unified Payment Interface (UPI)

With the increase of mobile usage and customer awareness on digitalization, mobile based APP’s were needed in the payment ecosystem for facilitating Peer to Peer & Merchant based sending and collecting payments. Unified Payments Interface (UPI) was launched with the above stated vision, which would allow sending & requesting payment as per requirement & convenience of the user.

5.9 National electronic Toll collection (ETC)

After receiving the letter of intent (LOI) from Indian Highway Management Company Limited (IHMCL) on providing a composite solution for Electronic Toll Collection. NPCI started the work of building a solution which would take care of the clearing and settlement of electronic transaction from RFID tags (FASTags). NPCI has built the scheme National Electronic Toll Collection System (NETC System) for Transaction processing, clearing & Settlement, Dispute Management and a Mapper for capturing Vehicle details. NPCI went live with NETC pilot on November 28, 2016.

6. Before us, ld. counsel for the assessee has reiterated the above factual position in respect of set up of the assessee, the objects for which it was created and the activities undertaken by it. Ld. counsel also submitted that the charitable status of the assessee still continues as it has been granted registration u/s 12AA on 22.09.2009 w.e.f. 01.04.2009 vide certificate dated 18.03.2010. The said registration still continues and has not been revoked by the Revenue. The charitable purpose for the assessee falls within the category of “advancement of any other object of general public utility” which is accepted position both, by the ld. A.O. in the assessment proceedings and by ld. CIT(E) in the revisionary proceedings. Ld. counsel also emphasized on the fact that the charitable purpose of advancement of object for general public utility has been dealt elaborately by the Coordinate Bench in assessee’s own case for assessment year 2010-11 and 2012-13 (supra). He also referred to all the aspects discussed by the ld. CIT(E) in the revisionary proceedings which have been dealt by the Co-ordinate Bench in its order for A.Y. 2010-11 and 2012-13 (supra).

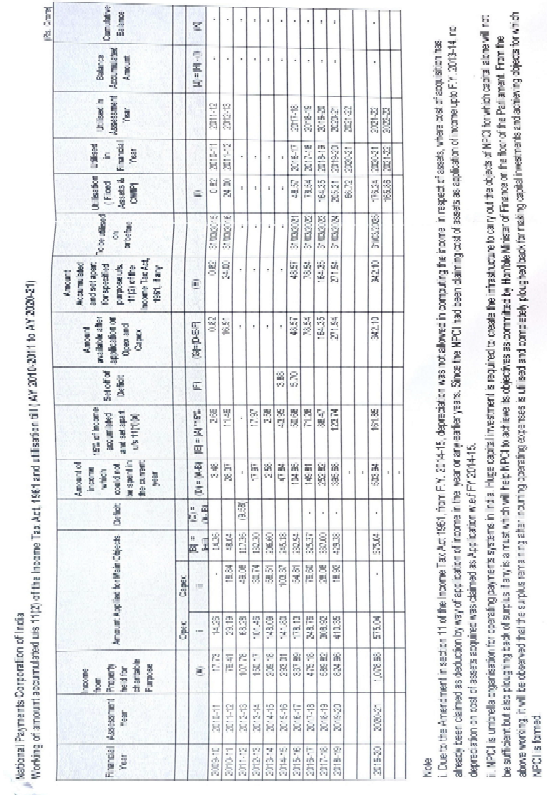

6.1. He thus, summarized that assessee is a non-profit company registered u/s 25 of the Companies Act and its income cannot be distributed by way of dividend. Assessee was granted registration u/s 12AA of the Act as it is not-for-profit organization. Also, assessee charges fee merely to meet the cost of operations and income generated is incidental in nature and not with a view to generate profit. It was submitted that the surplus remaining after incurring operating expenses are utilized and completely ploughed back in achieving objects for which it is formed. To demonstrate this factually, working of amount accumulated u/s 11(2) and its utilization from A.Y. 2010-11 to AY. 2020-21 was furnished which is extracted below:

6.2. Ld. Counsel also pointed out that Co-ordinate Bench had dealt with the decision in the case of Ahmedabad Urban Development Authority v. Assistant Commissioner of Income-tax (Exemption) ITR 323 (Gujarat), as held by Hon’ble Gujarat High Court vide order dated 02.05.2017, in its para 8.18. The views taken by Hon’ble Gujarat High Court were confirmed by the Hon’ble Supreme Court in its decision in ACIT v. Ahmadabad Urban Development Authority ITR 1 (SC).

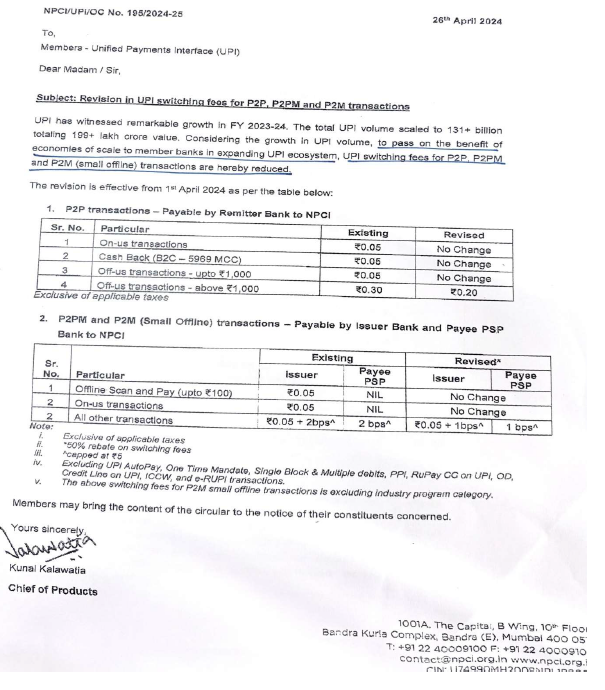

6.3. Further, ld. counsel submitted that when assessee took over the NFS operations w.e.f. 14.12.2009, its started charging a fee of Re.1 per transaction undertaken by customers of banks, using its infrastructure. This fee gradually reduced over the years despite the fact that assessee enjoyed monopoly over the payment system. For the current position of the charges, the details were furnished which demonstrates that the assessee passes on the benefits of economics of scale to its member banks and thus, there is no profit motive at the end of the assessee. The charges in the present time have come down to as low as Re.0.05 for certain categories of transactions and in certain cases, it has been reduced, for which revised details are reproduced below. It is important to note in this case that in the year 2009, when it started its operations, the charges were of Re.1 per transaction has already stated.

6.4. Thus, ld. Counsel reiterated that charitable purpose as defined in section 2(15) of ‘advancement of objects of general public utility’ is undisputed and un-distributed for the assessee. It is only the effect of decision of Hon’ble Supreme Court in the case of Ahmadabad Urban Development Authority (supra) which needs to be taken into account so as to decide whether revisional proceedings are validly undertaken or ought to be quashed. In this regard, relevant paragraphs from the decision of Hon’ble Supreme Court are reproduced below:

“206. ERNET is a not-for profit society, set up under the aegis of the Union Government. At one time, government functionaries, including the late President, APJ Abdul Kalam, were members, on account of their ex officio capacity. The objects of this assessee are to

“3.1.1 To advance the cause of computer communication in the country in all its aspects and dimensions with a view to provide rapid nationwide development of the sector and technological and economic growth of the county.

3. 1.2 To develop, design, setup and operate nationwide state of the art computer communication infrastructure with international connectivity directed towards research and development, advancement of high quality education, create and host content, express creative and academic potential via intranet and intranet peer to peer connectivity among educational and research institutions in the country and the world and make available the communication infrastructure to users in academic, research and development institutions, Govt organizations in line with national priorities. “

207. ERNET’s networks are a mix of terrestrial and satellite-based wide-area network. It provides services through its 15 Points of Presence (PoPs) located across the country. All those are equipped to provide access to Intranet, Internet and Digital Library through trial leased circuits and radio links to the user institutions. The PoP at STPI Bengaluru provides Intranet and Internet access through Satellite. ERNET provides, services, namely, Network Access Services, Network Applications Services, Hosting Services, Operations Support Services und Domain Registration Services under srnet.in, ac.in, edu.in & res.in domains. Funded through government grants, its projects support educational networks and development of internet infrastructure in numerous other segments of society.

208. Having regard to the nature of ERNET’s activities, it cannot be said that they are in the nature of trade, commerce or business, or service, towards trade, commerce or business. It has to receive fees, to reimburse its costs. The materials on record nowhere suggest that its receipts (in the nature of membership fee, connectivity charges, data transfer differential charges, and registration charges) are of such nature as to be called as fees or consideration towards business, trade or commerce, or service in relation to it. The functions ERNET performs are vital to the development of online educational and research platforms. For these reasons, it is held that the impugned judgment, which upheld the ITAT’s order, does not call for interference.

209. The Revenue has appealed the decision of Delhi High Court in which the National Internet Exchange of India (NIXI) was held to be a GPU category charity. The materials on record show that NIXI was established in 2003 under the aegis of the Ministry of Information Technology of the Union Government for the promotion and growth of internet services in India, to regulate the internet traffic, act as an internet exchange, and undertake “.in” domain name registration. Concededly, NIXI, is a not for profit, and is barred from undertaking any commercial or business activity. Its object is to promote the interests of internet service providers and internet consumers in India, improve quality of internet service, save foreign exchange, and carry on domain name operations. It is bound by licensing conditions – which include the prohibition from altering its memorandum, without the prior consent of the Union Government. According to the submissions made on NIXI’s behalf, it charges annual membership fee of Rs. 1000/- and registration of second and third level domain names at Rs. 500/- and Rs. 250/-. The finding of the ITAT and the High Court are that NIXI’s objects and functioning are by way of general public utility and thus it is a GPU category charity.

210. Having regard to the findings on record and the materials placed by the parties, it is evident that NIXI carries on the essential – crucial purpose of promoting internet services and more importantly, regulating domain name registration which is extremely essential for internet users in India. A country’s need to have a domestic internet exchange, rather than depend on an international one, cannot be overemphasized. The Union Government’s object of setting up of internet exchange is part of its essential function as a government to regulate certain segment of the communication networks. In the absence of a single entity authorized to register “.in” domain names, there is bound to be chaos or confusion.

211. In view of the foregoing discussion, this Court is of the opinion that the revenue’s contention that NIXI does not merely carry-on public purpose of regulatory activity but is involved in trade, commerce, or business or in providing service in relation thereto, cannot be accepted.”

6.5. From the above, it is noted that para 206 to 211 dealt with non-statutory bodies having similar objects falling within the category of advancement of objects of general public utility (GPU). In this category of organizations which included national internet exchange of India (NIXI) and ERNET. It was held that these are established for promotion and growth of internet services in India by the Government which was a GPU category charity and that it was not involved in trade, commerce or business. Hon’ble Court noted that these organizations have to receive fees reimbursed as cost. There receipts are not of such nature as to be called fees and consideration towards business, trade, commerce or services in relation to it.

7. Per contra, submission made by the ld. DR refers to para 4.2 of the order of the Ld. CIT(E) according to which case of the assessee is clearly hit by the proviso to section 2(15) and the factual position demonstrate that there is a profit motive at the end of the assessee breaching the threshold limit prescribed in the second proviso to section 2(15) of the Act as assessee is engaged in the activities of business, trade or commerce and services in relation thereto.

8. We have heard both the parties and perused the material on record. We have also given our thoughtful consideration to various submissions and reference made to the judicial precedents discussed above. Admittedly, the charitable activities for which the assessee falls in the category of advancement of objects of general public utility. Undisputedly, registration u/s 12AA continues and not revoked by the Revenue which was granted for the stated charitable purpose. Coordinate Bench in assessee’s own case has dealt with the claim of exemption u/s 11 and 12 by taking into account stated charitable purpose for A.Y. 2010-11 and 2012-13 (supra). It is also submitted before us that there is no stay granted by the higher forum on the operation of these decisions by the Co-ordinate Bench. In this regard, reference was made before us by the ld. Counsel of the assessee to the decision of Hon’ble High Court of Allahabad in the case of N.N. Agarwal v. CIT ITR 769 (Allahabad) wherein it was held that just because an appeal was pending, the decision of the court could not be treated as not final nor could it be ignored. It was binding upon the authorities within the territories on this state. The ITO had no option to follow this decision. Therefore, the notice issued by the Commissioner u/s 263 was not justified and the same was quashed. It was submitted that findings of the Co-ordinate Bench in assessee’s own case for A.Y. 2010-11 and 2012-13 squarely applied in the present case and ld. CIT(E) ought to have adhered to the said decision, there being no change in the material facts and stay by the higher judicial forum on their operation. We are in agreement with the submissions made by the ld. counsel to this effect to the extent that there is no stay operating on the decision of the Co-ordinate Bench (supra).

8.1. There had been subsequent development by way of decision of Hon’ble Supreme Court in the case of Ahmedabad Urban Development Authority (supra) which ought to be factored in while concluding on the issue raised before us against the revisionary order passed by ld. CIT(E). In this respect, we have elaborately referred to the said decision to understand its implication in the present case. This judgement has discussed in detail, about the charitable purpose falling in the category of ‘advancement of any other objects of general public utility’ contained in section 2(15) along with amendments made thereto. Relevant paragraphs are extracted below:

“168. If one understands the definition in the light of the above enunciation, the sequitur is that the reference to “income being profits and gains of business” with a further reference to its being incidental to the objects of the Trust, cannot and does not mean proceeds of activities incidental to the main object, incidental objects or income derived from incidental activities. The proper way of reading reference to the term “incidental” in section 11(4A) is to interpret it in the light of the sub-clause (i) of proviso to section 2(15), i.e., that the activity in the nature of business, trade, commerce or service in relation to such activities should be conducted actually in the course of achieving the GPU object, and the income, profit or surplus or gains can then, be logically incidental. The amendment of 2016, inserting sub clause (i) to proviso to section 2(15) was therefore clarificatory. Thus interpreted, there is no conflict between the definition of charitable purpose and the machinery part of section 11(4A). Further, the obligation under section 11(4A) to maintain separate books of account in respect of such receipts is to ensure that the quantitative limit imposed by sub-clause (ii) to section 2(15) can be computed and ascertained in an objective manner.

169. The conclusion recorded above is also supported by the language of seventh proviso50 to section 10(23C). Whereas section 2(15) is the definition clause, section 10 lists out what is not income. Section 10(23C) – by sub-clauses (iv) and (v) exempt incomes of charitable organisations. Such organisations and institutions are not limited to GPU category charities but rather extend to other types of charities (i.e. the per se kind as well). The controlling part of section 10(23C) along with the relevant clauses (iv) and (v) seek to exclude income received by the concerned charities. However, the provisos hedge such exemption with conditions. The seventh proviso – much like section 11(4A) and the definition – carve out an exception, to the exemptions such that income derived by charities from business, are not exempt. The seventh proviso virtually echoes section 11(4A) in that business income derived by a charity (in the present case, the GPU charities) which arises from an activity incidental to the attainment of its objective is not per se excluded.

170. Classically, the idea of charity was tied up with eleemosynary51. However, “charitable purpose” – and charity as defined in the Act have a wider meaning where it is the object of the institution which is in focus. Thus, the idea of providing services or goods at no consideration, cost or nominal consideration is not confined to the provision of services or goods without charging anything or charging a token or nominal amount. This is spelt out in Indian Chamber of Commerce (supra) where this Court held that certain GPUs can render services to the public with the condition that they would not charge “more than is actually needed for the rendering of the services, – may be it may not be an exact equivalent, such mathematical precision being impossible in the case of variables, – may be a little surplus is left over at the end of the year – the broad inhibition against making profit is a good guarantee that the carrying on of the activity is not for profit”.

171. Therefore, pure charity in the sense that the performance of an activity without any consideration is not envisioned under the Act. If one keeps this in mind, what section 2(15) emphasizes is that so long as a GPU’s charity’s object involves activities which also generates profits (incidental, or in other words, while actually carrying out the objectives of GPU, if some profit is generated), it can be granted exemption provided the quantitative limit (of not exceeding 20%) under second proviso to section 2(15) for receipts from such profits, is adhered to.

172. Yet another manner of looking at the definition together with sections 10(23) and 11 is that for achieving a general public utility object, if the charity involves itself in activities, that entail charging amounts only at cost or marginal mark up over cost, and also derive some profit, the prohibition against carrying on business or service relating to business is not attracted – if the quantum of such profits do not exceed 20% of its overall receipts.

173. It may be useful to conclude this section on interpretation with some illustrations. The example of Gandhi Peace Foundation disseminating Mahatma Gandhi’s philosophy (in Surat Art Silk) through museums and exhibitions and publishing his works, for nominal cost, ipso facto is not business. Likewise, providing access to low-cost hostels to weaker segments of society, where the fee or charges recovered cover the costs (including administrative expenditure) plus nominal mark up; or renting marriage halls for low amounts, again with a fee meant to cover costs; or blood bank services, again with fee to cover costs, are not activities in the nature of business. Yet, when the entity concerned charges substantial amounts- over and above the cost it incurs for doing the same work, or work which is part of its object (i.e., publishing an expensive coffee table book on Gandhi, or in the case of the marriage hall, charging significant amounts from those who can afford to pay, by providing extra services, far above the cost-plus nominal markup) such activities are in the nature of trade, commerce, business or service in relation to them. In such case, the receipts from such latter kind of activities where higher amounts are charged, should not exceed the limit indicated by proviso (ii) to section 2(15).

174. The insertion of section 13(8)52, the seventeenth proviso to section 10(23C) and third proviso to section 143(3) (all of which were inserted by Finance Act, 2012, but w.r.e.f. 1-4-2009), further reinforces the interpretation of this Court, of “charitable purpose”. These provisions, form the machinery to control the conditions under which income is exempt. The effect of the seventeenth proviso to section 10(23C) is to impose the same condition i.e., that that the trade, commerce or business activity or service relating to trade, business or commerce, should be part of the GPU’s activities, to achieve its object of advancing general public utility. The other condition- which is drawn in as part of the exemption condition, is that if such trading or commercial activity takes place the receipts should be confined to a prescribed percentage of the overall receipts. Section 13(8) too reinforces the same condition.

175. In the opinion of this court, the change intended by Parliament through the amendment of section 2(15) was sought to be emphasized and clarified by the amendment of section 10(23C) and the insertion of section 13(8). This was Parliaments’ emphatic way of saying that generally no commercial or business or trading activity ought to be engaged by GPU charities but that in the course of their functioning of carrying out activities of general public utility, they can in a limited manner do so, provided the receipts are within the limit spelt out in clause (ii) of the proviso to section 2(15).”

8.2. Thus, based on the above discussion, Hon’ble Court then, dealt with what kinds of income received could not be characterized as received from trade, commerce or business or in relation to such activities, for a consideration. For this, it categorized various bodies and authorities to understand the implication on each such category and one of such categories dealt by the Hon’ble Court was ‘non-statutory bodies’ which included ERNET, NIXI and GS1 India. In this respect, we have already extracted above the observations and findings of the Hon’ble Court given in para 206 to 2011.

8.3. Summary of observations and findings of the Hon’ble Supreme Court on the law prevalent and applicable prior to insertion of proviso to section 2(15) w.e.f. 01.04.2009 and amendments made thereafter is extracted below from the decision of Coordinate Bench in the case of Media Research Users Council v. Asstt.DIT ITD 170 (Mumbai – Trib.):

| i. | If at all any activity in the nature of trade, commerce or business, or a service in the nature of the same, for any form of consideration is permissible, then activity should be intrinsically linked to, or is part of the GPU category charity object. |

| ii. | Test of the charity being driven by a predominant object is no longer good law. Likewise, the ambiguity with respect to the kind of activities generating profit which could feed the main object and incidental profit-making also is not good law. |

| iii. | What instead, the definition under section 2(15) through its proviso directs and thereby marks a departure from the previous law, that if a GPU charity is to engage in any activity in the nature of trade, commerce or business, for consideration it should only be a part of this actual function to attain the GPU objective; and equally important consideration is the imposition of a quantitative standard – i.e., income (fees, cess or other consideration) derived from activity in the nature of trade, business or commerce or service in relation to these three activities, should not exceed the quantitative limit. |

| iv. | The Apex Court has further held that the idea of providing services or goods at no consideration or at cost may not be relevant factor as it has to be given a wider meaning. But now there is an inhibition against making profit though there may be a little surplus left over the end of the year. Thus, concept of pure charity i.e. the performance of an activity without consideration is not envisioned under the Act, however, as long as GPUs object involves activities which also generates profits, it can be granted exemption provided the quantitative limit under second proviso to section 2(15) for receipts from such profits, is adhered to. |

| v. | In para 171, it has been stated that if the charity involves itself in activities that entail charging amounts only at cost or marginal markup over cost and also derives profit, the prohibition against carrying on business or service relating to business is not attracted (if the quantum of such profits did not exceed 20 per cent of its overall receipts) has been adhered to.” |

8.4. By taking into account the findings of the Hon’ble Supreme Court as well as decision of the Co-ordinate Bench in assessee’s own case (supra) and keeping in juxtaposition the factual matrix of the present appeal, the question which remains to be answered is, if an institution has been granted registration u/s 12AA for a particular object of general public utility holding it to be charitable in nature then, whether the activity per se for which it has been granted registration has any element of trade, commerce or business, when it has only one source of receipt from that activity alone. Also, whether the threshold of 20% of the total receipts would still apply.

8.5. A careful reading of the proviso to section 2(15) clearly indicates that it applies only to ‘advancement of any other objects of general public utility’. The said proviso carves out an exception in the sense that advancement of any other object of general public utility shall not be regarded as charitable purpose in the following situations:

| i. | if it involves any activity in the nature of trade, commerce or business. |

| ii. | or it involves any activity of rendering of any service in relation to any trade, commerce or business, |

| iii. | the activities in item (i) and (ii) are for a fee or cess or any other consideration except when the aggregate of these receipts during the year do not exceed 20% of the total receipts of that year. |

8.6. Meaning of the word ‘trade’, ‘commerce’ and “business’ have to be understood in their ordinary sense and as known in common parlance. The word ‘trade’ would mean exchange of goods for goods or for money. The word ‘business’, though, has been defined under section 2(13) of the Act, however, is generic. ‘Business’ in its ordinary sense would mean an occupation, or profession which occupies time, attention or labour of a person and is generally undertaken with a profit motive. The word ‘commerce’ again is of same connotation as ‘trade’ or ‘business’. In the present case, as can be seen from the objects of the assessee mentioned in its MoA, it is not in any manner involved in any activity of trade, commerce or business. Further, it is necessary to see whether the second condition of any activity of rendering any service in relation to any trade, commerce or business is applicable. Since the assessee itself is not carrying on any trade, commerce or business, it cannot be said that it is involved in any activity of rendering service in relation to any trade, commerce or business.

8.7. To further elaborate on this issue, we refer to the memorandum explaining the provision of Finance Bill, 2008 which spells out the legislative intent for insertion of the proviso to section 2(15) of the Act. The relevant part of the memorandum reads as under:

“Streamlining the definition of “charitable purpose”

Section 2(15) of the Act defines “charitable purpose” to include relief of the poor, education, medical relief, and the advancement of any other object of general public utility.

It has been noticed that a number of entities operating on commercial lines are claiming exemption on their income either under section 10(23) or section 11 of the Act on the ground that they are charitable institutions. This is based on the argument that they are engaged in the “advancement of an object of general public utility” as is included in the fourth limb of the current definition of “charitable purpose”. Such a claim, when made in respect of an activity carried out on commercial lines, is contrary to the intention of the provision.

With a view to limiting the scope of the phrase “advancement of any other object of general public utility”, it is proposed to amend section 2(15) so as to provide that “the advancement of any other object of general public utility shall not be a charitable purpose if it involves the carrying on of

| (a) | any activity in the nature of trade, commerce or business or |

| (b) | any activity of rendering of any service in relation to any trade, commerce or business, |

for a fee or cess or any other consideration, irrespective of the nature of use or application of the income from such activity, or the retention of such income, by the concerned entity.

This amendment will take effect from the 1st day of April, 2009 and will accordingly apply in relation to the assessment year 2009-10 and subsequent assessment years.”

8.8. From the reading of above explanatory notes, it transpires that it was brought to the statute keeping in view the fact that in the garb of advancement of object of general public utility, many institutions/organizations are actually engaged in income generating commercial activities. Therefore, to prevent misuse of the exemption provision in the statute intended for genuine charitable institutions/organizations, the proviso was introduced.

8.9. It is further observed that as per the proviso to section 2(15), activity of trade, commerce or business or services related thereto, must be for a cess or fee or any other consideration. In the facts of the present case, admittedly, assessee recovers only a nominal charge for providing its facilities so as to recover its costs. In this respect, the factual details have been elaborately narrated in the above paragraphs which includes financial statistics as well as fees/charges recovered by the assessee. Notably, these have been reduced significantly to pass on the economies of scale to its member banks, already discussed above.

8.10. Co-ordinate Bench in the case of Media Research Users Council (supra) has also dealt with the present issue in details. Facts of this case are akin to the facts of the present case before us, where the only activity which has been carried out has been recognized for the charitable purpose in the category of object of general public utility. Coordinate Bench observed that if the very activity was in the nature of trade, commerce or business then, why it was even granted registration u/s 12AA by the Revenue which has not been revoked as of now. Thus, if from the same activities, the receipts of the assessee exceed the threshold, how can the benefit be denied and proviso be invoked when assessee carried out the activities which has been recognized as charitable, falling within the category of ‘object of general public utility’. Accordingly, the correct interpretation and the intent of brining proviso to section 2(15) will meet its end only when the assessee carried out any other activity to fulfill its general public utility objects involving element of trade, commerce or business and its receipts from such activity are found to be in excess of the 20% threshold prescribed, of the total receipts. In this context, in the present case before us, the factual position on record evidently demonstrates that assessee has been passing on the benefit of economics of scale year-on-year basis to member banks for which it started initially with charge of Re.1 and in the present time, got reduced to Re.0.05. For this, relevant circular is already extracted in the above paragraphs.

8.11. Considering the factual matrix and the judicial precedents discussed above as well as admitted position that this issue has been elaborately examined by the ld. A.O. in the course of original assessment proceeding, we do not find any justification for invocation of revisionary proceedings by the ld. CIT(E) by resorting to Explanation 2 to section 263 and basing his decision by referring to the treatment given in A.Y. 2017-18, 2018-91 and 2019-20, even though Bench had held in favour of the assessee while adjudicating for A.Y. 2010-11 and 2012-13. In the conspectus of the above discussion, we quash the revisionary proceedings and the impugned revisionary order passed by ld. CIT(E) u/s. 263. Accordingly, grounds raised by the assessee are allowed.

9. In the result, appeal of the assessee is allowed.