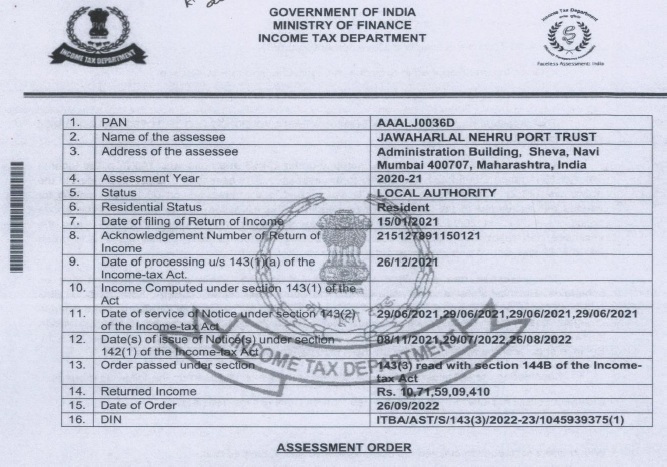

ORDER

R.K. Panda, Vice President.- The above appeals filed by the Revenue and the assessee are cross appeals and are directed against the separate orders dated 21.12.2015 of the Ld. CIT(A)-2, Aurangabad relating to assessment years 2003-04 to 2005-06 respectively. Since common issues are involved in all these appeals, therefore, these cross appeals were heard together and are being disposed of by this common order for the sake of convenience.

ITA No.543/PUN/2016 (A.Y. 2003-04) (Revenue)

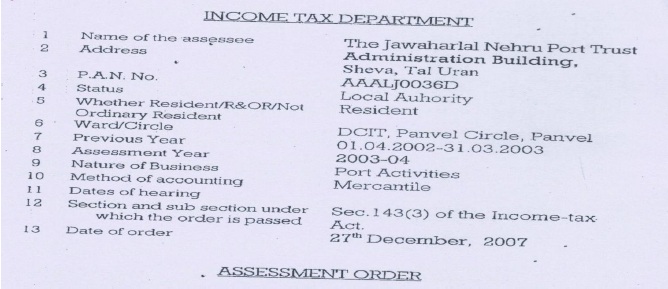

2. Facts of the case, in brief, are that the assessee is a Trust registered u/s 12A of the Income Tax Act, 1961 (hereinafter referred to as ‘the Act’). It was one of the 13 major ports operating in India. The entire income of Jawaharlal Nehru Port Trust (JNPT) was exempt under the provisions of section 10(20) of the Act upto and including the assessment year 2002-03. For the purpose of section 10(20), the term ‘Local authority’ was given a restrictive meaning by insertion of an Explanation to section 10(20) w.e.f. assessment year 2003-04. Hence, the income of the assessee became taxable. The assessee filed its return of income as a ‘local authority’ claiming no exemption u/s 10(20) for assessment year 2003-04 on 29.10.2003 declaring total loss of Rs.203,32,82,489/- and claiming refund of Rs.78,66,489/- on account of excess TDS deducted. The return was processed u/s 143(1) of the Act on 24.02.2004. After processing the return, the case was selected for scrutiny. The Assessing Officer passed the order u/s 143(3) on 31.03.2006 assessing the total loss at Rs.8,77,10,01,650/-.

3. Subsequently the CIT-2, Thane found that the assessment had become erroneous and prejudicial to the interest of Revenue for which he set aside the said assessment order and directed the Assessing Officer to frame the assessment order de novo. In the meantime the appeal filed by the assessee against the assessment order was rejected by the CIT(A)-I, Thane on the ground that the appeal of the assessee has become infructuous. Since the original assessment was set aside u/s 263 of the Act, fresh assessment order u/s 143(3) r.w.s. 263 of the Act was passed by the Assessing Officer after considering the special audit report u/s 142(2A) of the Act on 27.12.2007 computing the total income at Rs.583,06,70,963/-.

4. The assessee had filed an application for registration u/s 12AA of the Act on 10.02.2006 which was rejected by the CIT-II, Thane. Aggrieved by the order of CIT-II, Thane rejecting the application for registration u/s 12AA, the assessee had filed an appeal before the Tribunal who vide order dated 28.06.2007 allowed the appeal of the assessee. The department filed an appeal before the Hon’ble Bombay High Court which was still pending at the time of passing of the assessment order.

5. Meanwhile as per the decision of the Tribunal, certificate u/s 12AA was granted to the assessee with retrospective effect from 01.04.2002 on 27.06.2008. Pursuant to this registration u/s 12AA, the assessee filed its return of income for the impugned assessment year on 26.09.2008 claiming exemption u/s 11 and consequential refund of Rs.78,66,489/- on account of TDS credit. The assessee also took an additional ground before the CIT(A)-I, Thane for allowance of exemption u/s 11. The CIT(A)-I, Thane rejected the additional ground taken by the assessee and exemption u/s 11 had not been allowed to the assessee. Against the order of the CIT(A), Thane, the assessee preferred second appeal before the Tribunal and the Tribunal vide order 30.09.2010 allowed the assessee’s appeal vacating the orders of lower authorities and remitting the matter to the file of the Assessing Officer for framing the assessment de novo with the direction that while doing so the Assessing Officer would take into account the registration granted to the assessee u/s 12AA w.e.f. 01.04.2003 and audit reports as also other documents filed by the assessee in support of its claim of benefit u/s 11 of the Act.

6. The Assessing Officer accordingly issued and served notices u/s 143(2) and 142(1) of the Act in response to which the assessee attended before the Assessing Officer from time to time and produced the details as called for. During the course of assessment proceedings the Assessing Officer asked the assessee to explain as to why its claim of exemption u/s 11 should not be disallowed since as per law for claiming the exemption u/s 11, one should file its return of income within the time limit prescribed as per the Act and claim exemption in its return of income. Since the assessee had not filed its return of income and not claimed the exemption u/s 11 within the prescribed time limit as per Income Tax Act, 1961, therefore, the Assessing Officer, rejecting the various explanations given by the assessee, disallowed the benefit of exemption u/s 11.

7. The Assessing Officer noted that since the interest accrued / paid by the assessee on loans pertains to the period upto 31.03.2002 where the assessee’s income was exempt from tax, therefore, the provisions of section 14A are applicable in respect of the said interest expenditure and therefore, such expenses are not allowable. He further held that any claim made by the assessee otherwise than by way of filing a return cannot be accepted. Since the assessee in the present case had made a claim by way of revised computation, therefore, he disallowed the additional claim of Rs.892 crores made by the assessee during the year on account of accrued interest on loan taken from Mumbai Port Trust / Kandla Port Trust which were not paid in earlier years and not debited in the Profit & Loss Account. He further disallowed the interest of Rs.157.34 crores actually paid by the assessee during the year as deduction on the ground that it pertains to the earlier period during which the assessee’s income was exempt from tax.

8. The Assessing Officer further noticed that during the course of Special Audit U/s. 142(2A), the Auditor had found that capital expenditure to the tune of Rs.20,90,642 was claimed as revenue expenditure. Rejecting the various explanations given by the assessee and following the directions of the CIT(A)-I, Thane, the Assessing Officer allowed depreciation on the above assets and made disallowance of Rs.15,96,407/-.

9. The Assessing Officer further noticed that the assessee, during the year under consideration, has paid a sum of Rs.25.05 crores to LIC on account of employees’ superannuation fund due upto 31.03.2003 right from the date of assessee’s incorporation. He noted that the liability of the superannuation as provided in the books of account for the year under consideration was just Rs.4.65 crores on the basis of the actuarial valuations certificate dated 22.04.2002 of M/s. Charan Gupta Enterprises. He, therefore, held that the assessee has claimed an additional deduction of Rs.20.40 crores against its taxable income of the year by taking shelter u/s 43B of the Act for an amount which was an expense pertaining to earlier years when its income was exempt from taxation u/s 10(20) of the Act and should have been debited in the books of account of those years. Since the services of the employees were utilized in earning the income of the earlier periods therefore, he held that the expenses of employees’ premium for Superannuation Fund for earlier period cannot be allowed as expenditure of the year in question, in view of the clear provisions contained in section 14A of the I.T. Act, 1961. Therefore, an amount of Rs.20,39.85,000/- was added by him to the total income of the assessee.

10. The Assessing Officer observed that during the year under consideration, the assessee paid a sum of Rs.6.40 crores to LIC on account of Employee’s Gratuity Fund due upto 31/03/2003 from the date of its incorporation. However liability of the gratuity as provided in the books of account for the year was also the same at Rs.6.40 crores. The assessee also paid a sum of Rs.13.35 lakhs as gratuity over and above the payment to LIC. However, the gratuity liability for the year ended 31/03/2003 as per the Actuarial Valuation Certificate dated 23/04/2002 of M/s Charan Gupta Enterprises was just Rs.1.10 crores. Therefore, he was of the opinion that the assessee claimed deduction of Rs.6.453 crores on account of gratuity against its taxable income of the year by taking shelter u/s 43B of the Act for an additional amount of Rs.5.43 crores which was an expense pertaining to earlier years and should have been debited in the books of earlier years when its income was exempt from tax u/s 10(20) of the Act. Since, the services of the employees were utilized for earning the income of the earlier periods therefore, he held that the expenses of employee’s premium for Superannuation Fund for earlier period cannot be an expenditure of the year in question, in view of the clear provisions of section 14A of the I.T. Act. He, therefore, added an amount of Rs.5,30,36,000/- to the total income of the assessee.

11. The Assessing Officer during the course of assessment proceedings noted that the service for Wharfage was provided during the previous year relevant to assessment year 2003-04. However, the income for the same was offered in assessment year 2005-06. He, therefore, held that the income is taxable in assessment year 2003-04 itself and not in assessment year 2005-06 and accordingly made addition of Rs..37.50 lakhs.

12. The Assessing Officer similarly noted that the environment monitoring charges of Rs.10,24,800/- from NSICT has become due in assessment year 200304 and therefore, is the income for assessment year 2003-04. However, the assessee has offered the same on receipt basis in assessment year 2005-06. According to the Assessing Officer, once the income is due, the same has to be accounted irrespective of the actual receipt of such income. Since the assessee is following mercantile system of accounting, he held that this income has to be taxed in assessment year 2003-04 and not in assessment year 2005-06. He accordingly made addition of Rs.10.24 lakhs.

13. After making certain adjustments, the Assessing Officer determined the total income of the assessee at Rs.93,03,65,425/-.

14. In appeal, the Ld. CIT(A) considering the submission of the assessee, the facts of the case, findings of the AO in the assessment order, provision of the section and CBDT’s Instruction no 1/1148, dated February 9, 1978, held that the assessee is entitled to exemption u/s 11 of the I.T. Act, 1961. While doing so he noted that in the above CBDT instruction, it is stated that in cases where for reasons beyond the control of the assessee, some delay has occurred in filing the report, the exemption as available to such trust under sections 11 and 12 may not be denied merely on account of delay in furnishing the auditor’s report and the Income-tax Officer should record reasons for accepting a belated audit report. Therefore one has to examine whether the delay in furnishing the audit report was due to reasons beyond the control of the assessee. He observed that in the instant case the delay in filing of the audit report was due to circumstances beyond the control of the assessee and this case is squarely covered under the exceptions provided in CBDT’s Instruction No. 1/1148, dated February 9, 1978. He, therefore, held that the assessee is entitled to exemption u/s 11 of the Act.

15. So far as the issue of assessment completed in the status of a “Trust” instead of “Local Authority” is concerned, the Ld. CIT(A) relying upon the decision in the case of Workman of Mangalore Port Trust v. Mangalore Port Trust 1973 ILR Kar 272/KAR 272, decision of Hon’ble Bombay High Court in Ram Ugrah Singh Girjar Singh v. Board of Trustees of Port of Bombay [W.P. No. 1090 of 1983 ] with C.A. No. 1560 of 1983 and CBDT Circular No. 93, dated 26/09/1972 held that the assessee is a local authority.

16. On the issue of disallowance of expenses treated as capital in nature, the Ld. CIT(A) held that since the assessee is entitled to exemption u/s 11 of the Act, therefore, these capital expenses will be allowed as application of income for the purposes of objects of the Trust and depreciation on the same will also be allowed.

17. So far as the issue of contribution to approved superannuation fund is concerned, the Ld. CIT(A) relying on various decisions held that deduction in respect of contribution made to approved superannuation fund within limit prescribed will be wholly allowed in assessment year relating to previous year in which payment was made. He accordingly allowed the appeal of the assessee on this issue.

18. On the issue of disallowance of contribution to approved gratuity fund, the Ld. CIT(A) relying upon various decisions held that the assessee is entitled for deduction in respect of initial contribution made by it to the approved gratuity fund subject to the limitations laid down in Rule 104 of the I.T. Rules, 1962. He accordingly allowed the appeal of the assessee on this issue.

19. On the issue of deduction of Rs.43,678/- as pointed out by the Special Auditor u/s 142(2A) of the Act, the Ld. CIT(A) found the contention of the assessee to be correct and directed the AO to allow the deduction and accordingly allowed the appeal of the assessee.

20. So far as the disallowance of accrued interest of Rs.734 crores claimed on change in method of accounting and disallowance of interest expenses of Rs.157.34 crores claimed on payment basis is concerned, the Ld. CIT(A) upheld the action of the Assessing Officer on the ground that the provisions of section 14A are applicable in this case. According to him, the provisions of section 36(1)(xii) are also not applicable to the assessee as the same are applicable in the case of Corporation or Body Corporate. He further noted that section 43B allows for deduction any such sum payable by the assessee as interest on any loan or borrowing from any public financial institution or state financial corporation or in respect of a term loan from a scheduled bank in previous year in which the same is actually paid. In the instant case the assessee has taken loan from Govt. of India, Mumbai Port Trust, etc who do not fall under the category of schedule or financial institution, therefore, the provisions of section 43B are not applicable.

21. So far as the treatment of revenue expenditure of Rs.20.9 lakhs as capital expenditure is concerned, he upheld the action of the Assessing Officer. He also upheld the action of the Assessing Officer in making addition of Wharfage receipt of Rs.37.50 lakhs holding the same to be taxable in the impugned assessment year instead of assessment year 2005-06. Similarly, he also upheld the action of the Assessing Officer in making the addition of environment monitoring charges of Rs.10.24 lakhs on the ground that the said income has accrued and arisen during the impugned assessment year. Since the assessee is following mercantile system of accounting, therefore, it has to be taxed in this year.

22. Aggrieved with such part relief granted by the Ld. CIT(A) the Revenue as well as the assessee are in appeal before the Tribunal by raising the following grounds:

Grounds of appeal by the Revenue (ITA No.543/PUN/2016)

1. On the facts and circumstances of the case, the Ld. CIT(A) has erred in allowing the exemption u/s 11 of the Income Tax Act as –

| (a) | | The assessee has not claimed any such exemption in any of his return of income. |

| (b) | | The assessee has failed to get its accounts audited as required u/s 12A(b) of the Income Tax Act. |

| (c) | | The department has not accepted and filed appeal to Hon’ble High Court, Bombay against the order of ITAT dated 23/10/2013 passed in ITA No.449/Mum/2012 for AY 2008-09 directing the CIT to grant registration u/s 12AA. |

2. On the facts and circumstances of the case, the Ld. CIT(A) has erred in allowing the status of assessee as “Local Authority”.

3. On the facts and circumstances of the case, Ld. CIT(A) has erred in treating the capital expenditure as revenue expenditure.

4. On the facts and circumstances of the case, Ld. CIT(A) has erred in allowing the deduction on account of contribution towards Superannuation Funds and Gratuity Funds as the same are expenses of earlier years and further, the accounts of the assessee is not debited of any such expenses for the year under consideration.

5. The appellant crave to consider each of the above grounds of appeal without prejudice to each other and craves to add, alter, delete or modify all or any of the above grounds of appeal.

23. Ground of appeal No.1 by the Revenue relates to the order of the Ld. CIT(A) allowing the claim of exemption u/s 11 of the Act.

24. The Ld. Special Counsel for the Revenue submitted that while allowing the claim of exemption u/s 11 of the Act, the Ld. CIT(A) has not taken into consideration the fact that the assessee had failed to meet the mandatory requirements of Section 11 and 12 of the Act i.e. claiming exemption in the return of income for the relevant assessment year 2003-04 as well as getting its accounts audited. He submitted that the assessee filed its return of income only on 26.09.2008 in the status of a Trust claiming the said exemption which was well beyond the prescribed time limit provided for by the provisions of the Act. In such a scenario, the Assessing Officer was correct in rejecting the claim of the assessee.

25. Referring to the decision of a Three-Judge Bench of the Hon’ble Supreme Court in the case of CIT v. Nagpur Hotel Owners’ Association ITR 201 (SC), he submitted that it has been categorically observed that any claim for giving benefit of Section 11 on the basis of information supplied subsequent to the completion of assessment would mean that the assessment order will have to be re-opened and the Act does not contemplate such re-opening of the assessment. Therefore, in view of the decision of a Three-Judge Bench of the Hon’ble Supreme Court in the case of Nagpur Hotel Owners’ Association (supra), the order of the Ld. CIT(A) allowing the claim of exemption u/s 11 is erroneous.

26. Referring to the decision of the Hon’ble Bombay High Court in the case of CIT v. Agricultural Produce and Market Committee ITR 419 (Bombay), he submitted that the Hon’ble Bombay High Court has observed that to avail benefits u/s 11 and 12 of the Act, not only trusts/institutions must be registered under u/s 12A/12AA of the Act but they must also comply with the conditions set out in such provisions and that the trusts/institutions will not get the benefits if such conditions are not fulfilled. Moreover, mere grant of registration does not preclude the Assessing Officer to come to his own conclusion regarding claim of exemption.

27. Without prejudice to the above, the Ld. Special Counsel for the Revenue submitted that even if the benefit of exemption u/s 11 is allowed to the assessee, the assessee’s taxable income would have to be further determined and tested at the touchstone of the condition whether 85% of the same has been applied for charitable purposes or not. Referring to the provisions of Section 11(2) of the Act, he submitted that where 85% of the income of the trust is not applied for charitable purpose by the trust then the income remained to be applied to that extent will not be exempted for the income of the trust. He submitted that in the present case, the Assessing Officer has returned a finding that the assessee has neither applied 85% of its income for charitable purpose nor exercised the option in writing for the accumulation of income as per the provisions of Section 11(2) of the Act. Further, the said finding and computation by the Assessing Officer has neither been challenged before the CIT(A) nor has been challenged before the Tribunal by the assessee at any point of time. Therefore, the same has attained finality and in the said circumstances, the Assessing Officer is correct in determining the income of the assessee in accordance with law.

28. The Ld. Counsel for the assessee on the other hand while supporting the order of the Ld. CIT(A) submitted that the Revenue in its ground of appeal has basically challenged the order of the Ld. CIT(A) allowing claim of exemption u/s 11 of the Act since (a) the assessee has not claimed any such exemption in any of its return of income (b) the assessee has failed to get its accounts audited as required u/s 12A(b) of the Act and (c) the department has not accepted and filed an appeal before High Court against the order of the Tribunal dated 23.10.2013 passed in ITA No.449/Mum/2012 for assessment year 2008-09 directing the CIT to grant registration u/s 12AA.

29. He submitted that the ground raised by the Revenue is misconceived as the said issue is not the subject matter of the appeal. In so far as the third issue raised by the Revenue filing an appeal to challenge the order of the Tribunal directing the CIT to grant registration with effect from assessment year 2008-09 is concerned, he submitted that the appeal of the Revenue has been dismissed by the Hon’ble High Court vide order dated 07.11.2015 and this has become final.

30. With respect to the other two issues, he submitted that the assessment order has been passed u/s 143(3) r.w.s. 254 of the Act pursuant to the specific direction of the Tribunal vide order dated 30.09.2010, copy of which is placed at page nos.19-24 of the paper book. He submitted that the Tribunal in the said order at para 3 has observed that the Ld. CTT(A) has denied the claim of exemption u/s 11 to the assessee on the procedural grounds i.e. (i) claim not made in the return of income filed and (ii) audit report not filed along with the return. He submitted that the Tribunal has reversed the finding of the Ld. CIT(A) and held that the alleged procedural defects would not justify denying the claim of exemption under section 11 of the Act. The Tribunal directed the Assessing Officer to examine the claim on merits after considering the return and audit report filed by the assessee. He submitted that the Tribunal noted that CBDT representative have already commented in the proceedings before Committee of Disputes that such claim of the assessee may also be allowed by way of rectification request. For the above proposition, the Ld. Counsel for the assessee drew the attention of the Bench to the comments of the Committee of Disputes.

31. The Ld. Counsel for the assessee further submitted that though the Tribunal had rejected the submission of the Revenue, however, the Assessing Officer has denied the claim of the assessee on the very same procedural grounds i.e. not claiming exemption u/s 11 in the return of income and non-filing of audit report along with the return. He submitted that the said procedural grounds were already taken by the Ld. CIT(A) while denying the claim of the assessee in the original proceedings and the said decision was reversed by the Tribunal while directing the Assessing Officer to allow the claim on merits. Further, the decision of the Tribunal has not been challenged by the Revenue and therefore, the finding of the Tribunal has become final. Therefore, the finding of the Assessing Officer to deny the claim of the assessee on procedural grounds is clearly beyond the scope of his jurisdiction which was circumscribed by the decision of the Tribunal. He further submitted that no doubt on the merits of the claim and objects of the assessee has been raised by the Assessing Officer in the assessment order. This is also supported by the fact that the Assessing Officer has allowed the claim of exemption u/s 11 to the assessee in subsequent years i.e. assessment years 2006-07 to 2008-09 wherein the said claim was claimed in the return of income. He accordingly submitted that the action of the Assessing Officer in denying the claim of the assessee on procedural ground is in violation of the order of the Tribunal and accordingly the said findings are required to be rejected.

32. Without prejudice to the above, the Ld. Counsel for the assessee drew the attention of the Bench to the order of the Ld. CIT(A) wherein he has elaborately discussed the facts of the assessee and has allowed the claim of exemption u/s 11. He submitted that it is the settled position of law that once the trust is duly registered under 12A, late filing of audit report would not disentitle the assessee trust from availing the benefits of section 11 of the Act. For the above proposition he relied on the decision of Hon’ble Bombay High Court in the case of CIT v. Mumbai Metropolitan Regional Iron & Steel Market Committee ITR 103 (Bombay) wherein, dealing with identical facts, the claim of the assessee was allowed. He submitted that similar view has been taken by the Indore Bench of the Tribunal in the case of Akshay Academy v. ITO (Indore – Trib.).

33. The Ld. Counsel for the assessee submitted that as per the provision of section 11 prevailing at that time, filling of Audit report was directory in nature and not mandatory. For the above proposition, he relied on the decision of Hon’ble Punjab & Haryana High Court in the case of

CIT v.

Shahzadanand Charity Trust ITR 292 (Punjab & Haryana). He submitted that similar view has been taken by the Hon’ble Andhra Pradesh High Court in the case of

CIT v.

Andhra Pradesh State Road Transport Corporation [2006] 285 ITR 147 (Andhra Pradesh), the Bangalore Bench of the Tribunal in the case of

Sindhi Youth Association Ladies Wing v.

ITO [1994] 48 ITD 6 (Bangalore), Jabalpur Bench of the Tribunal in the case of

Shri Namiyun Parswanath Jain Swetamber Manidhari Trust v.

ITO ITD 433 (Jabalpur –

Trib.) and the Delhi Bench of the Tribunal in the case of

United Educational Society v.

JCIT (Delhi-

Trib). He submitted that there is no dispute to the fact that the return of income along with the audit report were filed during the set aside proceedings and the same were available with the Assessing Officer. Therefore, rejecting the same on procedural grounds is not correct. He accordingly submitted that the order of the Ld. CIT(A) being in accordance with law should be upheld and the grounds raised by the Revenue on this issue be dismissed.

34. We have heard the rival arguments made by both the sides, perused the orders of the Assessing Officer and the Ld. CIT (A) and the paper book filed on behalf of the assessee. We have also considered the various decisions cited before us. We find the assessee in the instant case filed its return of income as local authority without claiming any exemption under section 10(20) of the Act on 01.11.2004 declaring total loss at Rs.203.32 Crs. The assessee is a local authority notified as a Major Port by the Central Government and the entire income of the assessee was exempt under the provisions of section 10(20) of the Act upto and including assessment year 2002-03. The term “Local Authority” was given a restrictive meaning by insertion of an Explanation in section10(20) with effect from assessment year 2003-04. Hence, the assessee was no longer eligible for exemption under section 10(20). In November, 2005, the Government clarified that restoration would not be made in the case of assessee and accordingly, the assessee deemed it fit to apply for registration u/s 12A since it was engaged in activity of general public utility. We find the Assessing Officer in the order passed u/s 143(3) of the Act on 31.03.2006 determined the total loss at Rs.877.10 crores. Subsequently the said order was set aside by the Ld. CIT u/s 263 of the Act on 02.11.2006 and de novo assessment was directed. Pursuant to the said 263 order, we find the Assessing Officer passed the assessment order u/s 143(3) r.w.s. 263 of the Act on 27.12.2007 assessing the total income of the assessee at Rs.583.06 crores. Against the said order the assessee filed an appeal before the Ld. CIT(A) on 25.01.2008. In the meantime the assessee had filed an application for registration under section 12AA before CIT-II, Thane on 10.02.2006, which was rejected by the Ld. CIT vide order dated 31.08.2006. We find, in appeal, the Mumbai Bench of the Tribunal vide order dated 28.06.2007 allowed the appeal of assessee by observing as under:

“8. We have considered the submissions made by both sides, material on record and orders of authorities below. Admittedly, the assessee is registered as Major Port within the provisions of Section Indian Ports Trust Act, 1908 r.w. Major Port Trust Act 1963. All the assets and liabilities of Central Government existing at the time of creation of Trust have been vested in the Trust. It is further noted that the assessee is entitled to carry on only those activities which are permitted under the provisions of Major Port Trust Act, 1963. We have also gone through the various judicial decisions relied on by the assessee and are of the view that the issue raised in this appeal is squarely covered in favour of the assessee by these decisions. Accordingly, we conclude that the activities carried on by the assessee are of charitable nature and come within the definition of charitable purpose as defined in Section 2(15) of the Act. Thus, the decision of the learned CIT on this issue is reversed. Having stated so, we are of the view that the issue of condonation of delay for grant of registration with retrospective effect, requires fresh adjudication in view of material placed before us, hence, in the interests of justice, we set aside the order of C.I.T. and restore the issue to his file for consideration of condonation of delay in granting registration, who shall adjudicate the issue afresh after giving an adequate opportunity of hearing to the assessee. Thus, ground No.6 stands allowed for statistical purposes.”

35. We find the Ld. CIT granted registration u/s 12A only from the date of the application i.e. 10.02.2006 vide order dated 05.09.2007. The relevant observations of the Ld. CIT read as under:

“In view of ITAT’s order holding that activities of the assessee are charitable in nature, registration u/s 12AA is granted to the assessee w.e.f. 10.02.2006 i.e. F.Y. 2005-06.”

36. Aggrieved by the order of the Ld. CIT, the assessee again approached the Tribunal to grant the registration from 01.04.2002. We find, the Tribunal, after considering the plea of the assessee, vide order dated 15.04.2008 condoned the delay in filing the application and directed to grant registration u/s 12AA with retrospective effect from 01.04.2002 by observing as under:

“7. We have heard the submission of the learned Departmental Representative, who reiterated the stand taken by the Commissioner in the impugned order. We are of the view that the delay in filing the application for grant of registration has to be accepted as owing to sufficient reason. It is only because of the change in law that the assessee had to explore the possibilities of securing the benefit of exemption available to it under the provision of Income-tax Act, 1961. Till 31.3.2003, the income of the assessee was exempt under the provisions of S.10(20) of the Act. Thereafter, the assessee was exploring the possibility of reviving the provisions of S. 10(20) of the Act. It is also not disputed by the CIT that the assessee filed evidence of correspondence made to the Finance Ministry and other organisations in this regard. It is in the month of November, 2005, when the Committee did not accept the stand of the assessee and others who were affected by the aforesaid amendment, that it became clear that all efforts made by the assessee failed. Thereafter, the assessee has filed the application for grant of registration on 10.2.2006. The assessee, in the meantime, had got legal advice that its objects were charitable within the meaning of S.2(15) of the Income-tax Act and therefore, its income would be exempt under S.11 of the Act. Thereafter it filed the application seeking registration. In our opinion the plea of the assessee is bona fide. The powers of condoning the delay have to be exercised for advancing the cause of justice and unless negligence or want of bona fides is shown, normally delay should be condoned. The principles laid down in the following decisions support the pleas of the assessee:-

| (1) | | N.Balkrishnan v. M. Krishnamurty (1988) 7 SCC 125 |

| (2) | | Collector of Land Acquisition v. MST Katiji & Others (1987)167 ITR 471(SC) |

| (3) | | Mata Din v. A. Narayan (AIR 1970 (SC) 1953) |

| (4) | | Concord of India Insurance Co. Ltd. v. Smt. Nirmala Devi (118 ITR 507)-SC |

8. We, therefore, condone the delay in filing the application under S.12A of the Act, as made by the assessee in ground No.1. We accordingly direct that the registration be granted to the assessee with effect from 1.4.2002.”

37. We find pursuant to this registration u/s 12AA, the assessee filed its return of income for the subject assessment year on 26.09.2008 claiming exemption u/s 11 before the Assessing Officer. Simultaneously, since the appeals for assessment years 2003-04 to 2005-06 were pending at first appellate level, the assessee also took additional ground before Ld. CIT(A)-I, Thane for grant of exemption u/s 11 of the Act. We find the Ld. CIT(A)-1, Thane vide order dated 23.12.2008 rejected the plea of the assessee on the ground that the said exemption was not claimed in the return of income and that audit report was not filed within time prescribed under the Act. We find when the assessee preferred an appeal before the Mumbai Bench of the Tribunal against the order of the Ld. CIT(A)-1, Thane, the Tribunal, vide its order dated 30.09.2010, allowed the assessee’s appeal holding that the finding of the CIT(A)-1, Thane was not sustainable in law, thereby vacating the orders of the authorities below and remitting the matter to the file of the Assessing Officer for framing the assessment de novo with the directions that while doing so, the Assessing Officer would take into account the registration granted to the assessee u/s 12AA we.f. 1st April, 2003 and audit reports, as also other documents filed by the assessee in support of its claim of benefit under section 11 of the Act. The relevant observations of the Tribunal read as under:

“8. We find that a large number of assessees, who were covered by the wider definition of the expression ‘local authority’ before the scope of Section 10(22) was narrowed down with effect from 1st April 2003, have faced the same problem. These were the cases in which registration under section 12A was never sought earlier because the assessees were exempt from tax anyway under section 10(22), and by the time the registration under section 12AA was obtained, due to the necessity caused by this change in law, the assessees had already filed the income tax returns without complying with the procedural requirements necessary to avail benefit of tax exemption under section 11 by the virtue of registration under section 12AA. As to what should be done in such situations, we find guidance from Hon’ble Supreme Court’s judgment in the case of

CIT v.

UP Forest Corporation (

230 ITR 945). On materially similar set of facts, Their Lordships,

inter alia, observed that “Inasmuch as the respondent cannot, in our opinion, be regarded as a local authority, interest of justice would demand that the question as to whether its income is liable to be exempted under section 11(1) of the Act should be investigated and examined by a proper forum under the Act”. In our view, therefore, the prayer of the assessee is quite in harmony with the ‘interest of justice’ as viewed by Hon’ble Supreme Court.

9. The fetters on the powers of the Assessing Officer, as perceived by the learned Departmental Representative, donot restrict the scope of powers of the Tribunal in giving appropriate directions while remitting the matter to the file of the Assessing Officer, nor there is anything in the law which restricts the Assessing Officer from implementing an order passed under section 254(1). The restrictions on the powers of the Assessing Officer, therefore, donot affect our powers to issue appropriate directions to the Assessing Officer in the interest of justice. In view of the foregoing discussions, and respectfully following the guidance of Hon’ble Supreme Court in UP Forest Corporation case (supra), we deem it fit and proper to remit the matter to the file of the Assessing Officer with a direction to examine the matter, on merits, for eligibility to tax exemption as a result of the registration under section 12 AA now available to the assessee and in the light of the requisite audit report and other documents now filed by the assessee. While doing so, the Assessing Officer shall decide the matter by way of a speaking order, in accordance with the law and after giving a fair opportunity of hearing to the assessee.

10. Having held so, we may also mention that we are somewhat surprised by the hyper technical and pedantic stand taken by the learned Departmental Representative, which is in sharp contrast to very fair and reasonable stand of the CBDT representative before the Cabinet Secretariat. While the CBDT is of the view that the relief can perhaps be given even by way of a rectification order, the field authorities are fighting tooth and nail on procedural issues for even examining the claim of the assessee on merits-that too against a public sector undertaking which is fully owned by the Government of India, and when there is a direct Supreme Court decision holding that interest of justice requires such matters to be examined and investigated by a proper forum under the Income Tax Act. Such an approach of the field authorities is certainly contrary to the spirit in which Committee on Disputes in Cabinet Secretariat was formed under directions of Hon’ble Supreme Court in the case of Oil and Natural Gas Commission (supra). One can not have such a pedantic approach so as to lose sight of the very objective of the constitution of Committee on Disputes. That defeats the very purpose of the Committee and belittles the stand taken before the Committee by senior functionaries of the Government. We hope that field authorities will take note of the backdrop in which CoD functions and make genuine efforts to reduce the unproductive litigation which is so much deprecated by Hon’ble Supreme Court from time to time. We leave it at that.

11. The appeals are allowed for statistical purposes.”

38. We find the Assessing Officer in the set aside order passed on 22.12.2011 again denied the exemption u/s 11 of the Act on the same ground that the assessee has not claimed the exemption in the return of income and that the audit report required for claiming exemption has not been filed within the time prescribed in the Act. We find the Ld. CIT(A) held that reasons for delay in filling the audit report and not claiming the same in the return of income was beyond the control of the assessee. He further held that the exemption u/s. 11&12 may not be denied merely on account of delay in furnishing auditor’s report. We find the Ld. CIT(A) further stated that assessee’s case is squarely covered under the exceptions provided in CBDT’s Instruction No.1/1148, dated February 9, 1978 which prescribes condonation of delay in case where the delay was beyond the control of the assessee.

39. We do not find any infirmity in the order of the Ld. CIT(A) on this issue. We find the Assessing Officer in the instant case passed the order u/s 143(3) r.w.s. 254 of the Act on 22.12.2011 pursuant to the specific directions of the Tribunal vide order dated 30.09.2010 wherein the Tribunal at para 3 of the order has observed that the Ld. CIT(A) has denied the claim of exemption of the assessee on procedural grounds i.e. (1) claim not made in the return of income filed and (ii) audit report not filed along with the return. We find the Tribunal has reversed the finding of the CIT(A) and held that the alleged procedural defects would not justify denying the claim of exemption under section 11 of the Act. The Tribunal directed the Assessing Officer to examine the claim on merits after considering the return and audit report filed by the assessee. The Tribunal has also noted that CBDT representative have already commented in the proceedings before Committee of Disputes that such claim of the assessee may also be allowed by way of rectification request. The relevant observations of the Tribunal have already been reproduced in the preceding paragraphs.

40. We find although the Tribunal had rejected the submission of the Revenue, however, the Assessing Officer has denied the claim of the assessee on the very same procedural grounds i.e. not claiming exemption u/s 11 in the return of income and non-filing of audit report along with the return. Therefore, once the Ld. CIT(A) after considering the decision of the Tribunal in assessee’s own case has directed the Assessing Officer to allow the claim on merits, the Revenue in our opinion should not have any grievance. Further, the submissions of the Ld. Counsel for the assessee that the decision of the Tribunal has not been challenged by the Revenue and therefore, the finding of the Tribunal has become final could not be controverted by the Ld. DR. We, therefore, find merit in the arguments of the Ld. Counsel for the assessee that the finding of the Assessing Officer to deny the claim of the assessee on procedural grounds is clearly beyond the scope of his jurisdiction which was circumscribed by the decision of the Tribunal. We further find the Assessing Officer in assessee’s own case for assessment years 2006-07 to 2008-09 has allowed the claim of exemption u/s 11 of the Act. We, therefore, do not find any infirmity in the order of the Ld. CIT(A) allowing the claim of exemption u/s 11 of the Act.

41. Further once the trust is duly registered under 12A, late filing of audit report in our opinion would not disentitle the assessee trust from availing the benefits of section 11 of the Act. We find the Hon’ble Bombay High Court in the case of Mumbai Metropolitan Regional Iron & Steel Market Committee (supra) while dealing an identical issue has allowed the claim of the assessee by observing as under:

“4. We are unable to agree with Mr. Suresh Kumar. The Tribunal has found that in the light of these admitted facts, there is substance in the assessee’s arguments. The Tribunal perused its own order for the assessment year 2005-06 restoring the matter to file of the Assessing Officer and to make a de novo assessment. It held that at that time the Form 10 audit reports and documents were already on record of the Assessing Officer. If the assessee was required to file Form 10 and other documents before the completion of the assessment and in this case there is only a technical plea raised by the Revenue, then, that should not take away a benefit accruing to the assessee in law. The Tribunal has neither disregarded the judgment of the Hon’ble Supreme Court nor has misapplied it. It found that the case of the assessee is peculiar. It was not the assessee’s fault inasmuch as it got into a legal tangle. Upto assessment year 2002-03, it was enjoying a benefit under section 10(20) of the IT Act by a local authority. Later on it decided to avail of the benefit of section 11 and applied for registration. The chequered history of the case pertaining to registration has been noted by us. It is that which enabled the Tribunal to conclude that the rigors of the section have been somewhat diluted by the Revenue’s understanding and the issuance of a circular. Thus, the circular contemplates condonation of delay in filing the above documents and which would enable the assessee to avail of the benefit. Filing of Form No.10 is not dispensed with. The Commissioner is only vested with powers to accept it after the specified period. This circular No.273 dated 3rd June, 1980 which has been relied upon to hold that the assessee’s claim for benefit of exemption under section 11 of the Act deserved acceptance. It is in these circumstances and when the objects of the trust were found to be genuine that the Assessing Officer was directed to carry out a denovo assessment in terms of the Tribunal’s observations. We do not find such conclusion to be perverse or vitiated by any error of law apparent on the face of the record. No larger question or wider controversy needs to be decided.”

42. Similar view has been taken by the Hon’ble Andhra Pradesh High Court in the case of

CIT v.

Andhra Pradesh State Road Transport Corporation [2006] 285 ITR 147 (Andhra Pradesh) wherein the Hon’ble High Court has held that the provisions contained in section 12A(

b) were only directory in nature and not mandatory. The relevant observations of the Hon’ble High Court read as under:

“8. Coming to the first argument that Section 12A(b) is mandatory, learned Counsel appearing for the assessee relies on a judgment of the Bombay High Court in CIT v. Nagpur Hotel Owners Association. One of the questions, which was before the Bombay High Court was:

“Whether, on the facts and circumstances of the case, the Income-tax Appellate Tribunal is correct in holding that the application in Form No. 10 under rule 17 of the Income-tax Rules, 1962, could be filed even after the assessment is completed ?

9. The assessee in this case claimed exemption as charitable institution for the assessment years 1974-75 and 1975-76. The exemption was refused by the Income-tax Officer on the grounds that

| (a) | | it was not duly registered with the Commissioner of Income-tax under Section 12A(a) of the Act, and |

| (b) | | no notice of accumulation of income as required under Section 11(2) was filed. |

10. The court held that the Income-tax Rules could not fix a time-limit for submitting the application in Form No. 10B under rule 17.

11. Reference has been placed on some other judgments also, but in our opinion, the matter can be disposed of on the ground that there is a circular which has been reproduced hereinabove, which lays down that exemption under Section 11 of the Act should not be rejected only on the ground that there had been delay in filing the report by the accountant in terms of Section 12A(

b). There is a direct judgment of the Supreme Court in Paper Products Ltd. v. CCE

[2001] 247 ITR 128. In this case, the Supreme Court held:

“It is clear from the abovesaid pronouncements of this Court that, apart from the fact that the circulars issued by the Board are binding on the Department, the Department is precluded from challenging the correctness of the said circulars even on the ground of the same being inconsistent with the statutory provision. The ratio of the judgment of this Court further precludes the right of the Department to file an appeal against the correctness or the binding nature of the circulars. Therefore, it is clear that so far as the Department is concerned, whatever action it has to take, the same will have to be consistent with the circular which is in force at the relevant point of time.”

12. Since the Supreme Court has laid down that the Department has no right to challenge a circular issued by the Board on any ground whatsoever including the ground that it was inconsistent with the statutory provision, therefore, both questions will have to be answered in favour of the assessee and against the Department.

13. The reference is accordingly answered in favour of the assessee and against the Department.”

43. We find the Hon’ble Punjab & Haryana High Court in the case of Shahzadanand Charity Trust (supra) has also held that as per the provisions of section 11 prevailing at that time, filing of audit report was directory in nature and not mandatory. The relevant observations of the Hon’ble High Court read as under:

“7. Under Section 11, subject to certain provisions of the Act, and on fulfilling of certain conditions provided under Section 12A, income from property held for charitable or religious purpose has been exempted from payment of tax. Section 12A provides that the provisions of Sections 11 and 12 shall not apply in relation to the income of any trust or institution unless the two conditions provided in Clauses (a) and (b) of this section are fulfilled. Clause (b) of Section 12A which is relevant and as it existed at the relevant time reads :

“12A. The provisions of Section 11 and Section 12 shall not apply in relation to the income of any trust or institution unless the following conditions are fulfilled, namely : –

| (b) | | where the total income of the trust or institution as computed under this Act without giving effect to the provisions of Section 11 and Section 12 exceeds twenty-five thousand rupees in any previous year, the accounts of the trust or institution for that year have been audited by an accountant as defined in the Explanation below Sub-section (2) of Section 288 and the person in receipt of the income furnishes along with the return of income for the relevant assessment year the report of such audit in the prescribed form duly signed and verified by such accountant and setting forth such particulars as may be prescribed.” |

8. Rule 17B of the Income-tax Rules, 1962 (hereinafter referred to as “the Rules”), provides that the report of audit of the accounts of a trust or institution which is required to be furnished under Clause (b) of Section 12A, shall be in Form No. 10B. In Form No. 10B, the chartered accountant has to certify that he has examined the balance-sheet of the trust and the profit and loss account for the year ended which are in agreement with the books of account maintained by the said trust. It has to be further certified that in the opinion and to the best of the knowledge of the chartered accountant, the said accounts give a true and fair view of the accounts. The particulars (which have been prescribed) have to be annexed along with the auditor’s report.

9. Counsel appearing for the Revenue argued that furnishing of the audit report in the prescribed form duly signed and verified by the chartered accountant with the furnishing of the return is mandatory. Failure to do so is fatal disentitling the assessee to claim the benefit of exemption from tax. The audit report could not be produced at any subsequent time either before the Income-tax Officer or the appellate authority. Reliance for this was placed upon a judgment of this court in CIT v. Jaideep Industries

[1989] 180 ITR 81.

10. Counsel for the assessee has controverted the argument raised by counsel for the Revenue. It has been contended by him that furnishing of report along with the filing of the return was directory in nature in view of the circular of the Central Board of Direct Taxes issued on February 9, 1978, which provides as under :

” Charitable trust-Requirement of filing audit report in Form 10B-12A(b). Instructions regarding–The Board have considered whether the requirement under Section 12A(b) of filing audit report ‘along with the return of income’ is mandatory so as to disentitle the trust from claiming exemption under Sections 11 and 12 in case of omission to furnish such report in the prescribed form along with the return.

Normally, it should be possible for a charitable or religious trust or institution to file the auditor’s report along with the return of total income, where such trust or institution claims exemption under Sections 11 and 12. However, in cases where for reasons beyond the control of the assessee some delay has occurred in filing the said report the exemption as available to such trust under Sections 11 and 12 may not be denied merely on account of delay in furnishing the auditor’s report and the Income-tax Officer should record reasons for accepting a belated audit report. (1/1148-CBDT F. No. 267/482/77-IT(Part), dated February 9, 1978-CBDT Bulletin Tech. XXIII/582.)”

11. On behalf of the assessee, reliance was placed upon

CIT v.

Rai Bahadur Bissesswarlal Motilal Malwasie Trust [1992] 195 ITR 825 (Cal)

and CIT v.

Gujarat Oil and Allied Industries [1993] 201 ITR 325 (Guj).

12. In

CIT v.

Jaideep Industries [1989] 180 ITR 81 (P & H), the point under consideration before this court was whether the Tribunal was right in holding that filing of the audit report under Section 80J(6A) during the assessment proceedings and not along with the return of income would satisfy the requirements of Section 80J(6A). It was held that filing of audit report along with the return of income was mandatory and deduction under Section 80J(6A) would not be admissible to the assessee unless it furnished the audit report in the prescribed form duly signed and verified by the accountant along with the return. The question was answered in favour of the Revenue and against the assessee. Counsel for the Revenue argued that Section 80J(6A) was in

pari materia with Section 12A(

b) of the Act and, therefore, applying the ratio of the law laid down by this court in CIT v. Jaideep Industries

[1989] 180 ITR 81, the question referred to us in this case has also to be answered in favour of the Revenue and against the assessee.

13. The Calcutta High Court in CIT v. Rai Bahadur Bissesswarlal Motilal Malwasie Trust

[1992] 195 ITR 825 while interpreting Section 12A(

b) held that the provision was directory in nature and the Assessing Officer could allow the assessee to file the audit report, at any time before the completion of the assessment. In this case, the assessee, a charitable trust registered with the Commissioner of Income-tax, filed its return on September 17, 1984, declaring a deficit of Rs. 1,61,452. The return so filed was not accompanied by audited accounts and audit report in Form No. 10B as required under Section. 12A of the Act. The audit report dated November 12, 1984, was, however, filed by the assessee in the prescribed form on March 6, 1987, before the completion of the assessment. The Income-tax Officer, while completing the assessment, refused to allow the benefit of exemption under Section 11 of the Act to the assessee on the ground that the audit report in Form No. 10B was not filed along with the return. The income of the assessee was put to tax. The order of the Income-tax Officer was upheld by the Commissioner of Income-tax (Appeals) against which the assessee filed further appeal before the Tribunal which was accepted. On these facts, it was held that the income-tax authority had taken a hypertechnical view of the matter where the assessee has complied with the provisions of the Act in the course of the assessment by curing the defect in the return by filing an audit report. The Income-tax Officer cannot ignore such audit report or the return in completing the assessment. The delay in getting the accounts audited and in filing the return in Form No. 10B did not defeat any object of the Act and, therefore, the provision was directory in nature. It also referred to the circular of the Board dated February 9, 1978.

14. The Gujarat High Court in CIT v. Gujarat Oil and Allied Industries

[1993] 201 ITR 325 was considering Section 80J(6A). The Gujarat High Court took the view put by this court in CIT v. Jaideep Industries

[1989] 180 ITR 81. It was held that the provision about furnishing of the auditor’s report along with the return has to be treated as procedural provision and, therefore, directory in nature.

15. The provisions of Section 80J(6A) and Section 12A of the Act are pari materia. The ratio of the law laid down in CIT v. Jaideep Industries

[1989] 180 ITR 81 (P & H) would have been applicable to the facts of the present case as well had the Central Board of Direct Taxes not issued the circular dated February 9, 1978, reproduced in the earlier part of the judgment. As per this circular it is not mandatory under Section 12A(

b) to file the audit report along with the return of income. Normally, a charitable or religious trust or institution is expected to file the auditor’s report along with the return but in cases where for reasons beyond the control of the assessee some delay has occurred in filing the said report, the Income-tax Officer, for reasons to be recorded, has been authorised to condone the delay in furnishing the auditor’s report and accept the same at a belated stage. It has been clarified that the exemption available to the trust under Section 11 may not be denied merely on account of delay in furnishing the auditor’s report. The word “shall” occurring in Section 12A cannot, under the circumstances, be read as a “must” making it mandatory for the trust to furnish the auditor’s report along with the filing of the return. If for certain unavoidable circumstances, the assessee is unable to furnish the auditor’s report along with the return then the same can, be furnished at a later date with the permission of the Assessing Officer who may permit the assessee to do so after recording his reasons for so doing.

16. Counsel appearing, for the Revenue then argued that as per this circular, the auditor’s report could only be furnished up to the stage of framing of assessment as the power to condone the delay for ‘accepting the auditor’s report at a later date has only been given to the Income-tax Officer and not thereafter, i.e., at the appellate stage. We find no merit in this submission. The Central Board of Direct Taxes by issuing the circular dated February 9, 1978, has treated the provisions regarding furnishing of the auditor’s report along with the return to be procedural and, therefore, directory in nature. By showing sufficient cause, the auditor’s report could be produced at any later stage either before the Income-tax Officer or before the appellate authority.

17. In view of the Board’s circular dated February 9, 1978, the requirement of filing the auditor’s report in Form No. 10B as provided in Section 12A(

b) read with Rule 17B of the Rules, the ratio of the law laid down by this court in CIT v. Jaideep Industries

[1989] 180 ITR 81 would not apply to the present case.

18. For the reasons recorded above, the question referred to us is answered in the affirmative, i.e., against the Revenue and in favour of the assessee. No costs.”

44. The various other decisions relied on by the Ld. Counsel for the assessee also support his case to the proposition that filing of the audit report in Form No.10B is directory in nature and not mandatory and therefore, the delay in filing of the audit report cannot be a ground to deny the claim of exemption u/s 11 and 12 of the Act.

45. So far as the denial of claim of exemption u/s 11 of the Act by the Assessing Officer on the ground that the exemption has not been claimed in the return filed u/s 139(4A) of the Act within the time limit is concerned, we find merit in the arguments of the Ld. Counsel for the assessee that till the assessment year 2017-18 there was no requirement of furnishing the return within the time limit u/s 12A(b) which only required that the return was to be filed u/s 139(4A). However, no time limit was provided. It was only through the amendment made by the Finance Act, 2017 that a new clause (ba) has been inserted in section 12A to put a further condition w.e.f 01.04.2018 of furnishing return within time allowed under section 139(4A) which has been made applicable from assessment year 2018-19. However, prior to it, no time limit has been prescribed in section 12A(b) for furnishing of such return and audit report in the Act. Therefore, we find merit in the arguments of the Ld. Counsel for the assessee that once the said return and audit report in required form has been submitted before the Assessing Officer in the reassessment proceedings, the same is sufficient for the purpose of section 12A(b) of the Act. For the above proposition, we rely on the decision of the Delhi Bench of the Tribunal in the case of United Educational Society (supra) wherein the Delhi Bench of the Tribunal has held that failure to file the return u/s 139(4A) cannot be interpreted to mean that income cannot be computed in case of a charitable trust u/s 11 of the Act. It has been held that a new clause (ba) has been inserted in section 12A by the Finance Act, 2017 to put a further condition w.e.f. 01.04.2018 of furnishing return within time allowed u/s 139(4A) applicable from assessment year 2018-19. The relevant observations of the Tribunal read as under:

“19. We have heard the rival submissions and perused the relevant findings given in the impugned order. The core issues here is, whether the computation of income of the assessee society should be in accordance with section 11 or not; and whether, the filing of audit report alongwith the return filed in response to notice u/s 148 will entitle the assessee for benefit of computation of section 11. The AO has denied to compute the income in accordance with the provisions of section 11 of the Act on the reasoning that assessee has not filed the return under section 139 (4A) reads with section 12A (b) of the Act. Thus, what we have to adjudicate is, whether assessing officer was right in not applying the provisions of section 11 while computing income of the assessee. It is an admitted fact that the assessee is a society, who has been granted registration under section 12A of the Act by CIT looking to its objects of charitable purpose, i.e., it is engaged in imparting education and running various educational institutions. Thus, the registration u/s 12A is fait accompli and consequently the computation of income has to be in accordance with sections 11 to 13 of the Act. The assessee society had not filed its return of income and it was only in response to notice issued by the Assessing Officer under section 148, the assessee has filed its return of income alongwith the audited Balance Sheet and Profit & Loss Account. Now, whether the income of the assessee society is to be computed in accordance with the provisions of section 11 of the Act, as it has not filed the return as required under section 139(4A) of the Act, but has filed return in response to notice under section 148.

20. Section 139 falls under Chapter XIV-‘Procedure for assessment’ which provides procedures and conditions for filing of return of income. Section 139(1) mandates every person having income exceeding the maximum amount not chargeable to tax to file return of income. Similarly, section 139(1) (4A) mandates that every person in receipt of income derived from property held under trust, i.e., charitable trust, etc., to file its return of income in case its total income exceeds the maximum amount not chargeable to tax without giving effect to the provisions of section 11 & 12 of the Act. In case of failure to file such return of income under this section 139, penalty has been prescribed. In case of failure to file return by any person under section 139(1) penalty has been prescribed under section 271F. Similarly, in case of failure to file return by charitable society under section 139 (4A) penalty has been prescribed under section 272A (2)(e). On a plain reading of the relevant provisions, in our opinion, failure to file the return under section 139(4A) cannot be interpreted to mean that income cannot to be computed in the case of a charitable trust under section 11 of the Act. During the relevant assessment years impugned in these appeals, there is no such provision in the Act that in case return is not filed by charitable society under section 139(4A), then its income cannot to be computed in accordance with the provision of the Act.

21. Further, on going through the provisions of section 148, we further note that once the return has been filed in response to the notice issued under section 148, the provisions of this Act shall apply as if such return were a return required to be furnished under section

139. Thus, return filed under section 148 is treated as return filed under section

139, which will include sub section (4A) of section

139. Once, such return is treated as return filed under section

139, then all the provisions of Act shall apply which will, include section 11 of the Act. The phrase “so far as may be” in section 148, has to be interpreted in the manner that wherever conditions of applicability of any procedure prescribed in any section of the Act is required, then same has to be applied. If a return has been filed under section 148, then the relevant provisions of section

139 has to be applied and also the procedure of assessment and computation of income; and it cannot be interpreted in a restrictive manner to exclude any procedure. The Hon’ble Apex Court, way back in the case of

R Dalmia & Anr v.

CIT, reported in

(1999) 236 ITR 480, has clarified the interpretation of the phrase “so far as may be” used in section 148 in the following manner:-

“13. By reason of s. 148, after a notice thereunder has been served on the assessee containing the requirements which must be included in a notice under s. 139(2), “the provisions of this Act shall so far as may be applied accordingly as if the notice were a notice issued under that sub-section”. What this implies is, in our view, clear. Even after a notice is issued under s. 148, if the ITO proposes to make a variation in the income returned pursuant to such notice which is prejudicial to the assessee and the amount of such variation exceeds the amount fixed by the Board, the ITO must forward a draft of the proposed order of the assessment to the assessee. The assessee is entitled to forward objections to such variation. If he does not do so, the ITO may complete the assessment or reassessment on the basis of the draft order. If, however, the assessee does raise objections, the ITO must forward the draft order together with the objections to the IAC and the IAC must, after considering the draft order, the objections and the record, issue such directions as he thinks fit for the guidance of ITO to enable him to complete the assessment or reassessment, but no directions which are prejudicial to the assessee may be issued before an opportunity is given to the assessee to be heard. The directions issued by the IAC are binding on the ITO.

14. If, therefore, the procedure that is prescribed by s. 144B is to be applied even to assessments and reassessments under s. 147 and, as we have stated, we think it must, having regard to the terms of the provisions of the Act herein before referred to as also because the provisions of s. 144B are intended to safeguard the interest of the assessee, the extended period of limitation prescribed by Expln. 1(iv) to s. 153 must apply.

15. It was submitted on behalf of the assessee that the provisions of s. 144B were not applicable to assessments and reassessments under s. 147 because s. 144B stated that it applied only to “an assessment to be made under subs. (3) of s. 143”. The submission cannot be accepted because the words we have quoted from s. 148 cannot be ignored. A notice having been issued under s. 148, the procedure set out in the sections subsequent to s. 139 has to be followed “so far as may be”. Sec. 144B is a procedural provision. It fits into the procedural scheme as hereinbefore noted and, therefore, it cannot be excluded by reason of the use of the words “so far as may be”. Nor is there any other good reason to exclude it from the procedure to be followed subsequent to a notice under s. 148.”

22. Thus, we are of the view that, whether it is a case of a regular assessment or it is a case of an assessment consequent to issue of notice under section 148, not only the procedure of return as given in section

139 has to be applied, but also such the income has to be computed on the basis of such return in accordance with the provision of the Act, which of course will be subject to any specific provision in the Act which itself bars a claim or an exemption. Thus, section 148 provides that all the provision of the Act has to apply on such return furnished in response to notice under section 148. The Ld. CIT DR has referred to the words ‘so far as may be’ to canvass the proposition that all the provision will not apply. This contention of the Ld. DR is not correct in view of our reasoning given above. The meaning of these words ‘so far as may be’ will not mean to exclude provision of section 11 of the Act. It is only such provision which are inconsistent with the provision of section 148 as compared to section

139 regarding procedure for assessment will not be applicable so far as may be. As regards the reliance placed by the Ld. DR on the judgment in the case of

Commissioner of Incometax v.

Sun Engineering Works (P.) Ltd. 198 ITR 297 (SC), we are not in agreement with the contention of the Ld. DR that in the reassessment proceedings under section 148, no deduction can be allowed in respect of the income which has escaped assessment. In reassessment proceedings even the income which has escaped assessment has to be computed in accordance with the provisions of the Act which will include section 11 as is in the present case. It will not be correct to say that while computing income under section 148 the entire gross receipts are to be taxed. Further, it is not the case of the assessee that it is reagitating or seeking review of the issue or the deduction for which determination has already taken place. The case of the assessee is that while computing income which has escaped assessment, the computation has to be done in accordance with the provision of the Act which include section 11 of the Act. It is a case of a determination of correct escaped income as per the provision of the Act.

23. The next issue is, whether there is any such bar or limitation in the Act for claiming exemption under section 11 in the case of an assessment proceeding consequent to issue of notice under section 148 of the Act. To answer this question it may be relevant to refer to clause (b) of section 12A. As per clause (b) of section 12A where the total income of the trust/institution without giving effect to the provisions of section 11 and 12 exceeds the maximum amount which is not chargeable to income tax, a return has to be furnished along with the audit report obtained from an accountant as prescribed under the Act. However no time limit has been prescribed in this clause (b) of section 12A for furnishing of such return and the audit report in the Act. The assessing officer is trying to read a condition in clause (b) itself to hold that such return has to be filed before the due date of filing of return in this clause for claiming benefit of section 11 & 12 of the Act. On going through the clause (b) of section 12A, we are of the view that the AO is not correct in reading such condition. All that clause (b) mandates that provision of section 11 & 12 shall not apply unless the accounts are audited and a return is filed along with the audited accounts. Thus, as and when computation is to be done these conditions need to be complied with. The issue whether return has been filed in time or not is not relevant for clause (b) of section 12A. Our above view is supported by the judgment of the Chandigarh bench of the ITAT in the case of Genius Education Society v. ACIT ITA No. 238/Chd/2018 dated 20.08.2018 wherein the Tribunal has held as under:-

“…10. Undoubtedly the requirement of filing of return of income and the report of audit have been specified for being eligible for claiming exemption u/s 11 & 12 of the Act, alongwith the grant of registration u/s 12AA of the Act. In the case of the assessee, we find, that the return of income has been filed in response to notice u/s 148 of the Act. Therefore the condition offiling of return of income stands fulfilled. The section, we find, nowhere prescribes the filing of return by any due date, therefore the findings of the CIT(A) that the assessee having not filed its return within the prescribed time it had failed to comply with the requirement prescribed, is not tenable. As for the requirement of filing report of audit in the prescribed form, the said condition has been held by courts to be merely procedural and therefore directory in nature and not mandatory for the purpose of claiming exemption u/s 11 & 12 of the Act. The Hon’ble Jurisdictional High Court in the case of CIT v. Shahzadanand Charity Trust [1997] 228 ITR 292 (Punj. &Har.), has categorically held so in para 10-14 of its order as under:

“10. Calcutta High Court in Rai Bahadur Bissesswarlal’s case (supra) while interpreting s. 12A(b) held that the provision was directory in nature and the AO could allow the assessee to file the audit report, at any time before the completion of the assessment. In this case the assessee, a charitable trust registered with the CIT filed its return on 17th Sept., 1984, declaring a deficit of ^ 1,61,452. The return so filed was not accompanied by audited accounts and audit report in Form No. 10B as required under s. 12A of the Act. The audit report dt. 12th Nov., 1984 was, however, filed by the assessee in the prescribed form on 6th March, 19897, before the completion of the assessment. The ITO while completing the assessment refused to allow the benefit of exemption under s. 11 of the Act to the assessee on the ground that audit report in Form No. 10B was not filed along with the return. Income of the assessee was put to tax. Order of the ITO was upheld by the CIT(A) against which assessee filed further appeal before the Tribunal which was accepted. On these facts, it was held that the IT authority had taken hyper-technical view of the matter where the assessee has complied with the provisions of the Act in the course of assessment by curing the defect in the return by filing an audit report. The ITO cannot ignore such audit report or the return in completing the assessment. The delay in getting the account audited and in filing the return (sic-report) in Form No. 10B did not defeat any object of the Act and, therefore, the provision was directory in nature. It also referred to the circular of the Board dt. 9th Feb., 1978.

11. Gujarat High Court in Gujarat Oil & Allied Industries’ case (supra) was considering s. 80J(6A). Gujarat High Court took the view put by this Court in Jaideep Industries’ case (supra). It was held that the provision about furnishing of the auditor’s report along with the return has to be treated as procedural provision and, therefore, directory in nature.

12. Provisions of s. 80J(6A) and s. 12A of the Act are para materia. The ratio of the law laid down in Jaideep Industries’ case (supra) would have been applicable to the facts of the present case as well had the CBDT not issued the Circular dt. 9th Feb., 1978, reproduced in the earlier part of the judgment. As per this circular, it is not mandatory under. s. 12A(b) to file the audit report along with return of income. Normally, a charitable religious trust or institution is expected to file auditor’s report along with the return but in cases where for reasons beyond the control of the assessee some delay has occurred in filing the said report, the ITO, for reasons to be recorded, has been authorised to condone the delay in furnishing the auditor’s report and accepting the same at a belated stage. It has been clarified that the exemption available to the trust under s. 11 may not be denied merely on account of delay in furnishing the auditor’s report. The word “shall” occurring in s. 12A cannot, under the circumstances, be read as a “must” making it mandatory for the trust to furnish the auditor’s report along with the filing of the return. If for certain unavoidable circumstances, the assessee is unable to furnish the auditor’s report along with the return then the same can be furnished at a later date with the permission of the AO who may permit the assessee to do so after recording its reasons for so doing.”

13. Counsel appearing for the Revenue then argued that as per this circular, the auditor’s report could only be furnished upto the stage of framing of assessment as the power to condone the delay for accepting the auditor’s report at a later date has only been given to the ITO and not thereafter, i.e., at the appellate stage. We find no merit in this submission. The CBDT by issuing the Circular dt. 9th Feb., 1978 has treated the provision regarding furnishing of auditor’s report along with the return to be procedural and, therefore, directory in nature. By showing sufficient cause, the auditor’s report could be produced at any later stage either before the ITO or before the appellate authority.

14. In view of the Board’s Circular dt. 9th Feb., 1978, the requirement of filing auditor’s report in Form 10B as provided in s. 12A(b) r/w r. 17B of the Rules, the ratio of the law laid down by this Court in Jaideep Industries’ case (supra) would not apply to the present case.”

11. In view of the above therefore we find no merit in the argument of the Revenue that the assessee was not eligible for exemption u/s 11 &12 on account of not having complied with the requirements of section 12A(1)(b) of the Act.”

24. The judgment relied upon by the CIT (A) and the Ld. DR in the case of

Director of Income Tax v.

Spic Educational Foundation 257 ITR 46 (Mad), in our opinion is not applicable. In this case the issue was of not filing of audit report in Form No.10B along with the return of income for claiming exemption under section 11 and 12 of the Income Tax Act. In that case the Hon’ble Madras High Court after taking note of the provisions of section 12A (

b) and

139(9) has observed that return has to be accompanied by audit report. In this case the return was filed but audit report was not filed with the return. This audit report was also not filed later on. That is why, the High Court observed that, there is nothing on record to show that assessee had filed the audit report at any point of time and hence the exemption cannot be granted in the absence of audit report. Thus, it was a case of complete failure to file the audit report which is not the case here. In the present case the assessee society has filed the return of income and has also filed audited accounts with the audit report in response to the notice under section 148 on the basis of which AO has completed the assessment under section 148/143(3). Thus, the audit report was before the AO.