Section 54 Deduction is Based on Actual Investment, Not Joint Ownership Share

Issue

Whether an Assessing Officer (AO) can restrict a taxpayer’s capital gains exemption claim under Section 54 to 50% of the cost of a new property, merely on the ground that the property was purchased jointly with a relative, even if the taxpayer’s actual, proven investment was significantly higher.

Facts

- The assessee sold two residential properties and claimed a capital gains exemption under Section 54.

- She invested her capital gains in a new residential house, which was purchased jointly with her son-in-law.

- The total cost of the new property was ₹4.18 crores.

- The assessee provided proof that her actual, personal contribution to this purchase was ₹3.68 crores.

- The Assessing Officer (AO) disregarded the actual contribution and restricted the assessee’s exemption claim to 50% of the total cost (approx. ₹2.09 crores), solely on the basis of the 50% joint ownership.

Decision

- The court ruled decisively in favour of the assessee.

- It held that the AO’s action of restricting the claim to 50% merely due to joint ownership was incorrect.

- The court affirmed that the assessee was entitled to the Section 54 deduction to the full extent of her actual investment (₹3.68 crores), which she had verifiably contributed.

Key Takeaways

- Investment is the Key, Not Ownership Share: The quantum of deduction under Section 54 is determined by the amount of capital gains invested by the assessee, not by the percentage of legal title they hold in the new property.

- Proof of Contribution: A taxpayer claiming more than their proportionate share in a joint property must be able to provide clear documentary proof (like bank statements) that their personal funds were used for the investment.

- Joint Ownership is Not a Bar: Purchasing a property jointly with another person (even a relative other than a spouse) does not automatically limit the Section 54 claim, provided the taxpayer’s own funds are used for the investment.

AO Cannot Reject Valuer’s Report Backed by Stamp Authority’s Certificate

Issue

Whether an Assessing Officer (AO) can arbitrarily reject a detailed valuation report from a registered valuer (for determining the Fair Market Value (FMV) as of 01.04.2001) and substitute it with a lower ready reckoner rate, especially when the valuer’s report is corroborated by a certificate from the Stamp Valuation Authority itself.

Facts

- The assessee sold two properties and, for computing Long-Term Capital Gains (LTCG), adopted the FMV as on April 1, 2001, at ₹1.72 crores.

- This valuation was based on a detailed report from a Government-approved registered valuer, which considered comparable sale instances.

- To further support this, the assessee also submitted a certificate from the Stamp Valuation Authority showing the FMV as of that date to be ₹1.71 crores (a nearly identical value).

- The AO rejected the assessee’s valuation and the valuer’s report. Instead, the AO adopted the ready reckoner rate, determining a much lower FMV of ₹91.71 lakhs, thereby increasing the taxable capital gain.

Decision

- The court ruled in favour of the assessee.

- It held that the assessee’s adopted valuation was not only supported by a registered valuer’s report but was also corroborated by the Stamp Valuation Authority’s own certificate.

- This proved compliance with the proviso to Section 55 (which caps the FMV at the stamp duty value).

- The court found that the AO had no valid reason to deny the valuation adopted by the assessee, as it was well-supported by evidence, and the AO’s own adoption of the ready reckoner rate was arbitrary.

Key Takeaways

- AO is Not a Valuation Expert: An AO cannot simply reject a detailed report from a registered valuer and substitute their own opinion or a general ready reckoner rate without providing cogent reasons.

- Corroborating Evidence is Key: The assessee’s case was made exceptionally strong by providing two independent, expert reports (a registered valuer and the stamp authority) that both arrived at a similar valuation.

- Stamp Duty Value vs. Ready Reckoner: The value certified by the Stamp Valuation Authority for that specific property was accepted over a generic ready reckoner rate, highlighting the importance of obtaining specific valuation certificates where possible.

IN THE ITAT MUMBAI BENCH ‘B’

Income-tax Officer

v.

Neelam Shamsher Kashyap*

Amit Shukla, Judicial Member

and Ms. Padmavathy S., Accountant Member

and Ms. Padmavathy S., Accountant Member

IT APPEAL No. 2053 (Mum.) OF 2025

[Assessment year 2021-22]

[Assessment year 2021-22]

OCTOBER 27, 2025

Leyaqat Ali Aafaqui, Sr. AR for the Appellant. Ajay R. Singh and Akshay Pawar, Advs. for the Respondent.

ORDER

Ms. Padmavathy S., Accountant Member.- This appeal by the revenue is against the order of the Commissioner of Income Tax Appeals/National Faceless Appeal Centre (NFAC), Delhi (in short “CIT(A)”) passed u/s. 250 of the Income Tax Act, 1961 (the ‘Act’) dated 30.01.2025 for AY 2021-22. The revenue raised the following grounds of appeal.

“1. Whether on the facts and circumstances of the case and in laws, Ld. CITA) has erred in directing the AD to accept the cast acquisition as per the valuer’s report or, at the very least, restrict it to the value certified by the Stamp Valuation Authority, without conducting proper verification. The AO had correctly adopted the stamp duty valuation rate as of 01:04 2001 at Rs 5,078 per sq. ft., as determined in the registered valuer’s report submitted by the assessee. In contrast, the certificate issued by the Sub-Registrar, relied upon by the Ld. CIT(A), reflects a valuation significantly higher than the Ready Reckoner Rate adopted by the registered valuer of the assessee and mentions the market rate instead of the stamp duty value.

2. Whether on the facts and circumstances of the case and in low, Ld. CIT(A) has erred in incorrectly allowing the assessee’s full claim under section 54 of the Act, disregarding the fact that the property was jointly held with her son-in-law. As per section 54, deduction is available only for the assessee’s share in the new property, and the AO had rightly restricted the deduction to 50% based on joint ownership.

3. Whether on the facts and circumstances of the case and in law, Ld. CITIA) has erred in passing the order without waiting for the AO’s remand report, despite the fact that a request for the same was made on 24.11.2024. No follow-up reminder was issued, and the order was passed hastily on 30.01.2025, without granting the AO sufficient time to respond, which resulted into an erroneous conclusion based on unverified claims?”

4. Whether on the facts and circumstances of the case and in law, Ld. CITIA) has erred in allowing the deduction under section 54 of the Act, based on an amended sale deed, which was not presented during the original assessment proceedings. This amendment appears to be an afterthought and was not considered by the AO during scrutiny, rendering the decision of the Ld. CII(A) unsustainable.

5. Whether on the facts and circumstances of the case and in law, Ld. CIT(A) has erred in allowing the deduction under section 54 of the Act, by relying on the Stamp Valuation Authority’s certificate without properly considering its discrepancies with the valuation adopted by the registered valuer of the assessee. The FMV as per the certificate of Sub-Registrar was significantly higher than the Ready Reckoner Rate adopted by the registered valuer of the assessee, which raises doubts about its authenticity and reliability?”

6. The appellant craves leave to amend or alter any grounds or add a new ground which may be necessary.”

2. The assessee is an individual and filed the return of income for AY 2021-22 on 17.12.2021 declaring a total income of Rs. 89,08,020/-. The case was selected for scrutiny and statutory notices were duly served on the assessee. The Assessing Officer (AO) noticed that the assessee as earned Long Term Capital Gains (LTCG) from sale of two properties and has claimed the deduction u/s. 54 to the tune of Rs. 4,00,84,000/-. The AO further noticed that the property towards which the assessee has claimed deduction u/s. 54 is bought by the assessee along with her son in law and that the son in law has paid an amount of Rs.50,00,000/- towards the purchase. The AO though has accepted the fact that the assessee has paid the balance consideration towards purchase of the new property did not allowed the claim for the reason that the ownership of the property is divided at 50% between the assessee and her son in law and, therefore, restricted the deduction u/s. 54 to the tune of 50% of the amount invested amount into Rs. 2,00,42,000/-. The AO also considered the cost of acquisition as of 01.04.2001 based on the ready reckoner value thereby rejecting valuation considered by the assessee based on the valuation report of the Government Valuer.

3. Aggrieved the assessee filed further appeal before the Ld. CIT(A). The assessee submitted before the Ld. CIT(A) that the ground of which the AO allowed only 50% of deduction is not supported by any evidence since the purchase agreement of the new property does not specify any percentage of ownership between the assessee and her son in law. Assessee further submitted the out of the total consideration of Rs. 4,00,84,000/- the assessee has invested Rs. 3,67,94,500/-which is more than 85% of the cost of the new asset and, therefore, the assessee should be allowed deduction u/s. 54 for the amount actually invested. With regard to the AO substituting the stamp duty value of the property sold as on 01.04.2001 as the cost of the acquisition, the assessee submitted before the Ld. CIT(A) that the AO should have made a reference to Department Valuation Officer (DVO). The assessee in this regard further submitted that, the valuation report is obtained from the government registered valuer by the assessee and that the AO rejected the said valuation report to substitute the same with the ready reckoner value. The assessee also submitted that the AO cannot summarily reject the valuation report without referring to the DVO by placing reliance on various judicial pronouncements. The Ld. CIT(A) after considering the submissions of the assessee deleted the addition made by the AO by holding that:

“5.3.3. On perusal of the assessment order, the AO observed that the investment in the new asset of Rs.4,17,94,500/- with investment of Rs.3,67,94,500/- by the appellant and Rs.50,00,000/- by her son-in law. Though, the appellant claimed the proportionate investments made by her in the new asset as deduction u/s.54 and such investment was sourced out of the capital gains earned from the sale of original assets, the AO presumed that the new asset was purchased jointly by the appellant along with her son-in -law with equal share and restricted the claim of deduction u/s. 54 to the extent of only 50% of investment made in the new asset. The AO had examined all the documents, bank account statements etc. filed by the appellant but not accepted the claim of deduction by the appellant to the extent of investment made by her in the new asset and instead restricted the claim to 50% of the value of the new asset. Further, the AO had re-computed the capital gains earned from the sale of properties (original assets) by adopting Rs.5078/- per square feet as the reckoner value while computing the FMV as on 01.04.2001. The AO had arrived the fair market value as on 01.04.2001 at Rs.91,70,868/- (before indexation) and Rs.2,76,04,312/- (after indexation) as the cost of the original asset as on 01.04.2001, whereas the appellant on the other hand adopted the FMV value/cost of acquisition of the original asset as on 01.04.2001 at Rs.1,71,57,000/-(before indexation) and Rs.5,16,42,570/- (after indexation) as the cost of original asset. The only difference in computation of LTCG of the original asset by the AO and the appellant was on account of adoption of cost of acquisition of the original asset as on 01.04.2001, which resulted difference in the taxable LTCG.

5.3.4. The observations of the AO and the appellant’s submission were considered carefully. In the instant case, the appellant had sold properties (original asset) and invested in the new asset. The appellant had claimed the deduction u/s. 54 out of the LTCG earned from the sale of original asset. There is no dispute in the sale consideration of the original asset, whereas the only contention was on the adoption of cost of the original asset as on 01.04.2001 by the appellant and the AO. Similarly, there was a difference between the AO and the appellant on the quantum of deduction claimed u/s. 54 of the Act on the proportionate investment made in the new asset. The appellant claimed the entire amount invested by her in the new asset as deduction u/s. 54, whereas the AO allowed only 50% of the investment since the property (new asset) was purchased by the appellant along with her son-in-law. The AO had not raised any dispute in the purchase consideration, associated expenditure and the amount of investment made by the appellant in the new asset. Further, the appellant had also submitted a copy of registered rectification deed executed reflecting the proportionate share in the new asset and also submitted a copy of certificate issued by the Stamp Valuation Authority (SRO, Andheri, Mumbai) mentioning the FMV of the original asset as on 2001 at Rs.1,70,61,370/-during the appeal proceedings. After accepting the additional evidences, the submissions and the additional evidences filed by the appellant were forwarded to the AO calling for his comments and a remand report. Even after giving sufficient opportunities, the AO neither responded nor submitted the remand report.

5.3.5. As far as the claim of deduction u/s. 54 by the appellant is concerned, the section 54 of the Act mandates for the eligible deduction that there should be an investment in the new asset by an individual or HUF and the profit on sale of original asset is eligible for deduction to the extent of investment made in the new asset. In the instant case, there is no dispute on the amount of investment made by the appellant in the new asset and there is no dispute that the new asset came in to existence within the period stipulated (purchase /construction) as per section 54. However, the AO presumed that the appellant is eligible for only 50% of the investment made by her as the new asset was purchased jointly. Whereas, the provisions of Section 54 stipulate mainly two conditions that there should be a new asset and the profit from sale of original asset is eligible to the extent of investment made in the new asset. In the instant case, the appellant had rightly claimed the entire amount of investment made in the new asset as it was sourced out of the profit earned from sale of original asset. Hence, the appellant is eligible to claim deduction u/s. 54 to the extent of investment made in the new asset of Rs.3,67,94,500/-. On the other hand, the appellant had also filed a registered rectification deed specifically mentioning the proportionate of interest/ share in the new asset between the appellant and the co-owner, though without such documents too, the appellant is eligible to claim the entire investment made by her in the new asset (to the extent of profit earned out of sale of original asset), as deduction u/s. 54. Accordingly, the appellant succeeds on this ground and the appellant’s ground is allowed.”

4. The Ld. DR submitted that, the Ld. CIT(A) has given relief to the assessee without waiting for the remand report and that the Ld. CIT(A) should have issued final reminder to the AO before proceeding allow the appeal in favour of the assessee. The Ld. AR further submitted that the Ld. CIT(A) failed to considered the proviso to Section 55(2)(b) introduced from AY 2021-22 that mandates that the fair market value as on 01.04.2001 shall not exceed the stamp duty value whereas in assessee’s case the valuation considered as cost of acquisition as on 01.04.2001 is more than the stamp duty value as per ready reckoner. The Ld. DR further submitted that, the AO has correctly adopted the ready reckoner value and that the Ld. CIT(A) has heavily relied on the certificate from stamp valuation authority submitted as additional evidence by the assessee. The Ld. DR also submitted by the certificated relied on by the Ld. CIT(A) was not verified by the AO and therefore, the Ld. CIT(A) accepting the valuation based on the certificate is not correct. With regard to the ground of deduction u/s. 54 allowed by the Ld. CIT(A), the Ld. DR submitted that the exemption is intended for the assessee to invest in new residential property for her own benefit and not if she buys property for somebody else. The Ld. DR further submitted that, the Ld. CIT(A) has accepted the amended purchase deed the submitted for the first time before which is an afterthought, by the assessee to claim full deduction u/s. 54. The Ld. DR submitted a detailed written submission in support of the above contentions which has been taken on record.

5. The Ld. AR on the other hand, submitted that the assessee has lawfully claimed the deduction u/s. 54 to the extent of the amount invested by her in the purchase of new property. Our attention in this regard, is drawn to the capital gain working submitted by the assessee while filing the return of income (Page 3 and 4 of paper book). The Ld.AR further submitted that the AO has assumed 50% ownership without any basis since there is no such mention in the purchase deed of the new property. The Ld. AR also submitted that the assessee subsequently, modified the purchase deed mentioning the share of ownership which has been examined and accepted by the Ld. CIT(A) while giving relief to the assessee. The Ld. AR argued that the AO has not disputed the amount contributed by the assessee, but has restricted the deduction u/s. 54, merely on the assumption that the assessee owns only 50% in the new property. With regard to the cost of acquisition the Ld. AR drew our attention to a valuation report submitted before the Ld. CIT(A) where the valuation officer has considered various factors along with sale instances which justifies the cost of acquisition adopted by the assessee (page 47 to 69 of paper book). The Ld. AR also drew our attention to the stamp duty valuation (page 194 of paper book) were the market value of the property is stated to be Rs.1,70,61,370/-. Accordingly, the Ld. AR argued that the cost of acquisition adopted by the assessee has been rightly allowed by the Ld. CIT(A).

6. We heard the parties perused the material on record. During the year under consideration the assessee has sold two properties and has claimed exemption u/s. 54 of the Act, towards, purchase of new property. The AO noticed that the assessee has purchased the new property along with her son in law. The AO though has admitted the fact that assessee has paid a sum of Rs. 3,67,94,500/- towards purchase in the property, restricted the exemption to 50% of the cost of acquisition of the new property for the reason that the assessee has jointly acquired the new property with the son in law. In this regard, it is relevant to note that in the purchase agreement of the new property share of ownership between the assessee and her son in law has not been specifically mentioned in the documents. The AO also considered the cost of acquisition of the property as on 01.04.2001 at Rs. 5,078/- based on the ready reckoner value as against the valuation adopted by the assessee. Before the Ld. CIT(A) the assessee submitted a modified purchase deed where the shares of the assessee and her son in law have been explicitly mentioned. The assessee also submitted the, valuation before of the property substantiating the value as on 01.04.2001. The Ld. CIT(A) gave relief to the assessee after considering the various submissions made by the AO along with the documentary evidences. The Ld. CIT(A) before concluding the appellate proceedings called for a remand report from the AO and since the AO did not submit any response the Ld. CIT(A) decided the issue in favour, of the assessee after considering the merits. As already mentioned the AO in his finding has not disputed the fact that the assessee has paid majority of the consideration towards acquisition of the property, but has restricted the deduction for the only reason that the assessee co-owns the property with her son in law. Section 54 provides for deduction from the capital gains if the assessee purchases or constructs a new property and the quantum of deduction is amount of capital gain or the cost of the new residential house whichever is lower. From the perusal of the findings of the Ld. CIT(A) it is clear that the Ld. CIT(A) has examined the various documentary evidences including the amended purchase deed before giving relief to the assessee. Accordingly, in our considered view there is no infirmity in the finding with the Ld. CIT(A) since the only reason for restricting the deduction u/s. 54 by the AO is not substantiated more so when the amount of investment is not disputed.

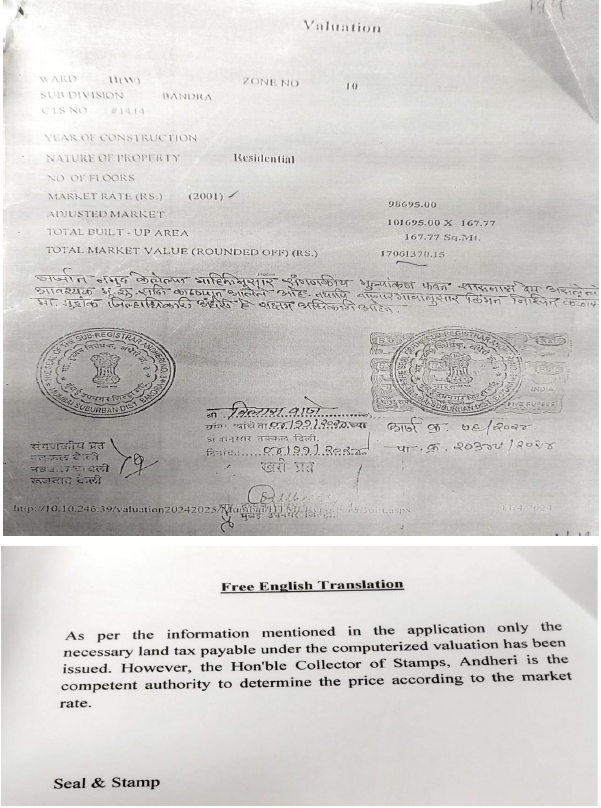

7. Now coming to the cost of acquisition adopted by the AO. We notice that as per the stamp duty valuation submitted by the assessee in page 194 of paper book the value of the property as on 01.04.2001 is stated to be Rs. 1,70,61,370/- and the assessee has adopted a value of Rs.1,71,57,000 as per the valuation report for the purpose of computing the capital gains. The relevant extract of the valuation by the stamp duty authority along with English translation is extracted below:

8. Further the assessee has submitted a valuation report and on perusal of the same we notice that the valuer has considered various aspects including the sale instances during the same period in other cases and also the justification for the valuation adopted has compare to the ready reckoner value. We also notice that the valuation as per the stamp duty authorities is matching with the valuation as of 01.04.2001 adopted by the assessee and therefore there is no violation of the proviso to section 55(2)(b) as contented by the revenue. In view of these discussions we are of the view that there is no reason to deny the valuation adopted by the assessee and accordingly we see no reason to interfere with the decision of the Ld. CIT(A).

9. In the result, the appeal of the revenue is dismissed.