State Government Grants for Infrastructure are Promoter’s Capital Contribution, Not Taxable Income.

Issue

Whether grants received by a state-owned infrastructure undertaking from the State Government, for the specific purpose of infrastructure development, are taxable revenue receipts or are non-taxable capital contributions from a promoter.

Facts

- The assessee, a wholly-owned undertaking of the Government of Maharashtra, was engaged in infrastructure development under Build-Operate-Transfer (BOT) arrangements.

- It received grants and contributions from the State Government, which were specifically for infrastructure development projects.

- The assessee treated these grants as capital receipts (a promoter’s contribution) and credited them to a capital reserve account.

- The Assessing Officer (AO) disagreed, treating the grants (both received and accrued) as revenue receipts and added them to the assessee’s total income.

- It was noted that the assessee was merely a contractor executing projects for the State, not the owner of the projects.

Decision

- The court held that the grants received by the assessee were capital in nature and could not be treated as income.

- It was ruled that the grants were not provided to support the assessee’s day-to-day business activities or to supplement its profits.

- The funds were determined to be a capital contribution by the State Government (as the promoter), specifically earmarked to cover the capital costs of the infrastructure projects.

Key Takeaways

- Purpose of the Grant: The tax treatment of a grant is determined by its purpose. Grants given to meet the capital cost of specific projects are “capital receipts,” whereas grants to assist with daily operations or supplement profits are “revenue receipts.”

- Promoter’s Contribution: When a promoter (in this case, the State Government) provides funds to its undertaking for the creation of capital assets, such funds are treated as a capital contribution and are not taxable as income.

- Ownership vs. Execution: The fact that the assessee was merely an executing contractor and not the owner of the assets further supported the conclusion that the funds were not its income but were capital investments in the projects themselves.

AO Cannot Tax Gross Toll Revenue Without Allowing Estimated Maintenance Costs.

Issue

Whether an Assessing Officer (AO) can make an addition by “grossing up” the revenue from a long-term toll contract without simultaneously allowing a deduction for the estimated future costs (like maintenance and improvement) that are an integral part of the same contract.

Facts

- The assessee was awarded a 15-year contract for the collection of toll, as well as the operation, maintenance, and improvement of a section of a highway.

- In its books, the assessee recognized the net consideration from the contract as its income.

- The Assessing Officer (AO) challenged this method and made an addition by considering only the gross revenue of the assessee.

- However, while making this upward adjustment to the income, the AO failed to consider or allow a corresponding deduction for the estimated costs of maintenance and improvement that the assessee was contractually obligated to incur.

Decision

- The court deleted the addition made by the Assessing Officer.

- It held that the AO’s approach of considering only the gross income, without accounting for the associated costs, was incorrect.

- The court ruled that if the income is to be recognized on a gross basis, then a corresponding reduction for the estimated expenditure must also be allowed.

Key Takeaways

- Matching Principle: In taxation and accounting, the “matching principle” is essential. An AO cannot recognize the gross revenue from a long-term contract without also recognizing the estimated costs that are contractually required to earn that revenue.

- One-Sided Adjustments are Invalid: An assessment cannot be framed by only considering the income side of a transaction while ignoring the corresponding and contractually-mandated expenditure side.

- True Income: The goal of an assessment is to tax the true income. In a BOT contract, the true income is the net figure after accounting for the contractual obligations of maintenance and improvement, not just the gross toll collection.

IN THE ITAT MUMBAI BENCH ‘B’

Maharashtra State Road Development Corporation Ltd.

v.

Income-tax Officer*

Amit Shukla, Judicial Member

and Ms. Padmavathy S., Accountant Member

and Ms. Padmavathy S., Accountant Member

IT Appeal No. 3484 (Mum) OF 2014

[Assessment year 2006-07]

[Assessment year 2006-07]

OCTOBER 27, 2025

Mukesh Butani, Pratik Poddar, Ms. Shruti Agarwal and Yash Ranglani for the Appellant. Pravin Salunkhe and Aditya M. Rai, Sr. DRs for the Respondent.

ORDER

Sandeep Singh Karhail, Judicial Member.- The assessee has filed the present appeal challenging the impugned final assessment order dated 29/10/2024, passed under section 143(3) r.w.s. 144C(13) of the Income-tax Act, 1961 (“the Act”), pursuant to the directions dated 30/09/2024 issued by the learned Dispute Resolution Panel-2, Mumbai [“learned DRP”], for the assessment year 2021-22.

2. In its appeal, the assessee has raised the following grounds: –

“Based on facts and circumstances of the case and in law, the Appellant respectfully craves leave to prefer an appeal under section 253(1) of the income-tax Act, 1961 (the Act) against the order dated 29.10.2024 passed under section 143(3) r.w.s 144C(13) rwis. 1448 of the Act by the Assessment Unit, Income Tax Department, on the following grounds, which are independent and without prejudice to each other:

General

1. On facts and circumstances of the case and in law, the learned Assessing Officer (‘AO’)/the learned Transfer Pricing Officer (TPO) under the directions of the Hon’ble Dispute Resolution Panel (‘DRP”) has erred in computing the total income of the Appellant at INR 42,11,15,313/-as against returned income of INR 31,63,85,208.

2. On facts and circumstances of the case and in law, final assessment order dated 29 October 2024 is barred by limitation, thus bad-in-law and is liable to be quashed in-limine.

3. On the facts and in the circumstances of the case and in law, the notice issued under section 143(2) of the Act is without jurisdiction, bad in law and thus the entire proceedings initiated by the learned AO are void-ab-initio.

Transfer Pricing-INR 10,47,30,105

4.On facts and circumstances of the case and in lww, the leamed AO/TPO, under the directions of the Hon’ble DRP, erred in making an adjustment of INR 10,47,30,105 in relation to the intemational transaction for payment of bareboat charter hire fees.

5. On facts and circumstances of the case and in law, the learned AO/TPO under the directions of the Hon’ble DRP erred in arbitrarily rejecting the economic analysis undertaken by the Appellant in accordance with the provisions of the Act read with the Income-tax Rules, 1962 (‘the Rules’) and various submissions made by the Appellant before lower authorities, considering none of the conditions mentioned in section 92C(3) of the Act is satisfied.

6. On facts and circumstances of the case and in law, the learned AO/TPO, under the directions of the Hon’ble DRP, erred in not appreciating the contractual structure, in general, and in particulars, the function performed by the appellant and its AE, to whom the bareboat charter hire fee is payable.

7. On facts and circumstances of the case and in law, the learned AO / TPO erred to distinguish the contractual arrangement and facts as per the directions of the Hon’ble DRP and in not following DRP directions for AY 2016-17, thereby violating the principle of consistency and res-judicata.

8. On facts and circumstances of the case, and in law, the learned AO/TPO under the directions of the Hon’ble DRP, erred in alleging that a 2.5% brokerage/facilitation fee should be deducted to determine the arm’s length price of the international transaction for payment of bareboat charter hire fees, despite there being no understanding agreement nor act of parties suggesting such consideration.

9. Without prejudice, on facts and circumstances of the case and in law, the learned AD/TPO, under the directions of the Hon’ble DRP, erred in determining the arm’s length price of the international transaction of payment of bareboat charter hire fees on an ad-hoc basis without applying any of the prescribed methods as per section 92C(1) of the Act.

10. Without prejudice, on facts and circumstances of the case and in law, the learned AO/ TPO, under the directions of the Hon’ble DRP, erred in not granting benefit of second proviso to section 92C(2) of the Act basis which the ALP determined by the learned AO/TPO is within the +/-3% range and thus no adjustment is warranted.

Corporate Tax

11. On facts and circumstances of the case and in law, the learned AO erred in not allowing credit of tax deducted at source of INR 5,09,51,916.

12. On facts and circumstances of the case and in law, the learned AO erred in levying interest under section 234A and section 234B of the Act.

13. On facts and circumstances of the case and in law, the learned AO erred in levying interest under section 234C of the Act.

14. On facts and circumstances of the case and in law, the learned AO erred in initiating penalty proceedings under Section 270A of the Act.

The Appellant prays that the additions made by the learned AO/TPO under the directions of the Hon’ble DRP be deleted and consequential relief be granted.

The Appellant craves for leave to add, amend, vary, omit or substitute any of the aforesaid grounds of appeal at any time before or at the time of hearing of the appeal, so as to enable the Hon’ble Income tax Appellate Tribunal to decide this appeal according to law.

Tax Effect:

Ground 1: is not calculated. This is a general ground, hence separate tax effect

Ground 2: This ground is in relation to limitation, hence separate tax effect is not calculated.

Ground 3: This ground is in relation to validity of the proceedings, hence separate tax effect is not calculated.

Grounds 4 to 10: These grounds relate to a single transfer pricing addition of INR. 10,47,30,105/- and its tax effect is INR 2,63,58,473/-, separate tax effect is not provided in relation to each of these grounds.

Ground 11: This ground relates to non-grant of credit of TDS and its tax effect is INR 5,09,51,916.

Ground 12: This ground relates to charging interest under section 234A and 234B which is consequential in nature, hence separate tax effect is not calculated

Ground 13: This ground relates to charging interest under section 234C of the Act and its tax effect is INR 24,33,595.

Ground 14: This ground relates to initiation of penalty proceedings, hence separate tax effect is not calculated

3. Ground no.1 is general in nature. Therefore, it requires no specific adjudication.

4. Grounds no. 2 and 3, raised in the assessee’s appeal, challenging the validity of the final assessment order, were not pressed during the hearing. Accordingly, the said grounds are kept open.

5. Grounds no.4-10, raised in assessee’s appeal, pertains to the transfer pricing adjustment on account of bareboat charter hire fees paid to the associated enterprise.

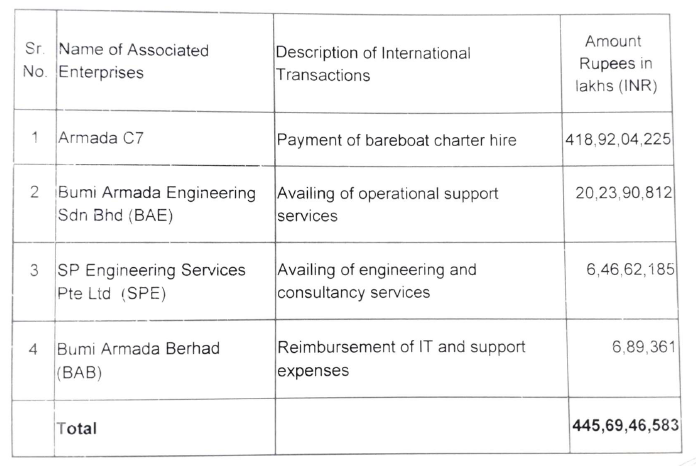

6. The brief facts of the case pertaining to this issue, as emanating from the record, are: The assessee was awarded the contract by Oil and Natural Gas Corporation Ltd (“ONGC”), an Indian Public Sector Company, operating in oil and gas, for supplying a Floating Production Storage and Offloading (“FPSO”) vessel and providing, inter alia, Operations and Maintenance (“O&M”) services to ONGC for a period of 9 years. As the assessee did not own any FPSO vessel, nor did it possess the expertise relating to the construction and mobilisation of an FPSO vessel, it obtained the vessel on a bareboat charter hire basis from its associated enterprise, Armada C7 Pte filed its return of income on 15/03/2022, declaring a total income of INR 31,63,85,208. The return filed by the assessee was selected for complete scrutiny, inter alia, on the issue of the large value of international transactions in the nature of technical service fees (TP risk parameter). Accordingly, the case was referred to the Transfer Pricing Officer (“TPO”) under section 92CA(1) of the Act for the determination of the arm’s length price of the international transaction entered into by the assessee. During the year under consideration, the assessee entered into the following international transactions with its associated enterprises: –

7. During the transfer pricing assessment proceedings, it was observed from the audited financial statements of the assessee that INR 41,892.04 lakhs were paid to the associated enterprise, during the year under consideration, as bareboat charter expense against the FPSO vessel. It was further observed that the amount was the same as shown by the assessee in its books of accounts to have been received from ONGC for the sub-leasing of the FPSO. Further, no margin was retained by the assessee while acting as a sub-lessor, and the entire amount received from ONGC for the vessel was passed on to the associated enterprise by the assessee. Accordingly, the assessee was asked to explain why the benchmarking adopted for the payment of bareboat charter expenses should not be rejected, and the arm’s length price of the same should not be determined, leaving a 2.5% commission for the assessee for acting as a sub-lessor of the FPSO vessel. In response, the assessee submitted that ONGC remunerates it on a daily basis for the charter hire and O&M services. It was further submitted that, of the amount received from the third party, the assessee reimbursed the associated enterprise with bareboat charter hire fees, after retaining an arm’s length markup for the O&M activities performed by the assessee. The assessee also submitted that, considering the functional and risk profile of these transactions, the assessee is merely a passthrough entity as it performs no role and bears no risk associated with the performance of the vessel, as its role is limited to the performance of the O&M services to ONGC for which the assessee has earned a markup of 38.09% on the cost incurred. Accordingly, the assessee submitted that the payment of charter hire fees was merely a pass-through cost, and the said transaction was benchmarked using the “Other Method” as the most appropriate method. The assessee further submitted that the FPSO vessel, Armada Sterling II, is a one-of-a-kind vessel that is highly customised and built according to the customer’s specifications, i.e., ONGC. It was also submitted that the FPSO vessel is not an ordinary, over-the-counter product that can be bought, sold, or traded like a routine finished product. Thus, the assessee submitted that it is not undertaking any sales activity on behalf of the associated enterprise or acting as an agent of the associated enterprise for selling its products. Furthermore, the assessee submitted that it entered into a contract with ONGC on a principal-to-principal basis for the provision of time charter services, which included bareboat charter hire and O&M activities. Additionally, it acquired the FPSO vessel on a bareboat charter (dry lease) basis from its associated enterprise. Thus, it was submitted that without the FPSO vessel, the assessee would not have been able to enter into a contract with ONGC.

8. The TPO, vide order dated 27/10/2023 passed under section 92CA(3) of the Act, disagreed with the submissions of the assessee and held as follows:-

| (a) | As per the contract with ONGC, the assessee was bound by the contract to supply a FPSO vessel, install it as required in the FPSO facility, provide project management services, provide design and engineering services, operate the FPSO vessel, provide marine warranty services and provide all the elements of the work in accordance with the execution schedule. Thus, the TPO rejected the assessee’s contention that it was merely a pass-through entity and performed no role, bearing no risk associated with the performance of the vessel. |

| (b) | The associated enterprise of the assessee is earning revenue on a transaction just because the contract from ONGC was granted to the assessee. Therefore, the TPO held that it was the effort of the assessee that secured him the contract, not the other way around. |

| (c) | There are significant differences in the specification of the FPSO vessels and therefore the cost of O&M services for the vessels considered for benchmarking by the assessee cannot be in the same proportion to the bareboat hire charges. Thus, the TPO rejected the assessee’s benchmarking of the transaction. |

| (d) | The TPO also rejected the submission of the assessee that both parties are operating on a principal-to-principal basis and provide the requisite expertise to execute the composite contract with ONGC, on the basis that the internal arrangement between the parties is not material for transfer pricing proceedings, for which the assessee is a single entity, who has won the contract from ONGC which is a composite and inseparable contract. |

| (e) | It is only because of the assessee the associated enterprise has earned revenue from ONGC and it should accordingly compensate the assessee. |

| (f) | The assessee has not brought on record as to what negotiations it had with the associated enterprise for hiring the vessel on a bareboat charter basis, and whether the assessee obtained quotes for FPSO leasing from other parties. |

| (g) | The fact that FPSO hire charges are approximately 80% of the total revenue and the associated enterprise did not directly bid for the contract with ONGC proves that the assessee had additional strength while bidding for the contract. Therefore, the assessee should be remunerated for the value it created for the associated enterprise. |

| (h) | Distinguishing the facts of the case from the assessment year 2016-17, the TPO held that there is nothing on record to show that in the assessment year 2016-17, the assessee was transferring the amount received from ONGC for bareboat charter hire charges to the associated enterprise on a back-to-back basis without retaining any margin. |

| (i) | The TPO held that no independent party will sub-lease an asset to any other party without keeping a margin for itself. |

9. Accordingly, the TPO determined the arm’s length margin at 2.5% for the back-to-back arrangement by the assessee with its associated enterprise for providing the FPSO vessel to ONGC. Consequently, the TPO computed the arm’s length price of the international transaction of bareboat charter hire charges at INR 408,44,74,120 instead of INR 418,92,04,225 paid by the assessee and made a downward transfer pricing adjustment of INR 10,47,30,105. In conformity with the order passed by the TPO under section 92CA(3) of the Act, the AO passed the draft assessment order dated 18/12/2023 under section 144C(1) of the Act, determining the total income of the assessee at Rs. 42,11,15,317 after making the transfer pricing adjustment of INR 10,47,30,105.

10. The learned DRP, vide its directions dated 30/09/2024 issued under section 144C(5) of the Act, rejected detailed objections filed by the assessee against the findings of the TPO. The learned DRP agreed with the TPO’s conclusions that, in the assessment year 2016-17, there was no evidence to suggest that back-to-back transfers were made to the associated enterprise for the entire amount received from ONGC in respect of the FPSO vessel. Thus, the learned DRP held that the findings made in the assessment year 2016-17 are distinguishable on facts. The learned DRP held that the action of the TPO in attributing over 2.5% as brokerage/facilitation fees to be retained by the assessee from the fees paid to the associated enterprise for bareboat charter hire is reasonable and correct. In conformity with the directions issued by the learned DRP, the AO passed the impugned final assessment order assessing the total income of the assessee at INR 42,11,15,313. Being aggrieved, the assessee is in appeal before us.

11. During the hearing, the learned authorised Representative (“learned AR”) submitted that the contract with ONGC and the associated enterprise was entered into for a period of 9 years and following the approach accepted by the learned DRP in assessee’s own case for assessment year 2016-17, the assessee used “Other Method” as the most appropriate method and the proportion of bareboat charter hire day rate to the time charter day rate in case of the assessee was compared with the similar ratios in the case of third parties. The learned AR submitted that a similar arrangement also existed even in the assessment year 2016-17, and the assessee recorded the entire time charter revenue received from the ONGC as its income in the profit and loss account, while the bareboat charter hire fees paid by the assessee to the associated enterprise were shown as an expense. The learned AR submitted that, in the year under consideration, in compliance with the requirements of Indian Accounting Standard (“Ind AS”) 116, the assessee was required to disclose the lease transaction in a particular manner. Thus, what was considered a back-to-back transfer to the associated enterprise with respect to the FPSO vessel was merely due to changes in reporting methods, as the fundamental nature and substance of the transaction remained unchanged. It was further submitted that what is back-to-back is a function performed by the assessee and the associated enterprise, and not the amount, as the billing to ONGC does not provide a split between bareboat charter hire fees and O&M. The learned AR further submitted that assessee entered into the agreement with ONGC on principal-to-principal basis and not as an agent of the associated enterprise, i.e. Armada C7 Pte Ltd. By referring to the agreement, the assessee submitted that the contract with the ONGC acknowledged the fact that the associated enterprise will provide the vessel, and in this regard, the ONGC also required a commitment letter from the vessel owner, which was provided by the associated enterprise to the assessee as well as the ONGC. Without prejudice, the learned AR submitted that even after imputing 2.5% commission for the bareboat charter hire fees, the transaction would still be at arm’s length. Thus, the learned AR submitted that there is no basis for making the impugned transfer pricing adjustment by the TPO/AO.

12. On the contrary, the learned Departmental Representative (“learned DR”) submitted that the assessee in its books has shown the bareboat charter hire charges separately received from ONGC and the same were being paid to the associated enterprise as it is, without keeping any margin. The learned DR submitted that, as per the FAR analysis, the assessee assumed various risks separately or jointly with the associated enterprise in the execution of the contract with ONGC. Therefore, the assessee is entitled to a certain margin besides the O&M charges, which is nothing but a pure domestic transaction carried out individually by the assessee with ONGC. The learned DR, by referring to the clauses of the agreement entered into by the assessee with ONGC, submitted that it is the assessee’s responsibility to maintain it in a stable condition. The learned DR further submitted that it is only due to the efforts of the assessee that the bid was successfully secured, and therefore, the assessee is entitled to a separate margin in that regard. Disputing the selection of comparables, the learned DR submitted that it is clearly stated in the TPO/learned DRP’s order that the vessels leased in those cases are significantly different from the vessel leased in the instant case. Accordingly, the learned DR vehemently relied upon the order passed by the lower authorities.

13. We have considered the submissions of both sides and perused the material on record. The assessee is an Indian Joint Venture Company held by Shapoorji Pallonji Energy Private Limited and Bumi Armada Berhad to the extent of 51.002% and 48.998%, respectively. Bumi Armada Berhad is one of the most prominent FPSO players in the world, an established offshore service vessel owner and operator with extensive experience across Asia, Europe, Africa, and Latin America.

14. Pursuant to the bidding process, the ONGC entered into an agreement with the assessee on 13/03/2013 for bareboat charter hire of FPSO vessel and O&M services for Cluster 7 Marginal Field. From the perusal of the agreement entered into between the assessee and ONGC, which forms part of the paper book from pages 503-694, we find that the said agreement was entered into for a period of 9 years, with an option to extend the operational period for a further period of 7 years. Further, the ONGC, in the agreement, has acknowledged that the assessee will take on lease the FPSO vessel from Armada C7 Pte Ltd upon completion of conversion of the designated vessel for the duration of this agreement, and the assessee will perform such operations with the FPSO and its personnel as per the scope of work and tender conditions set forth in the bidding documents. We find that, in this regard, the associated enterprise of the assessee, i.e., Armada C7 PTE Ltd, also issued letters to ONGC committing to make the FPSO vessel available and to deploy it at the designated location of ONGC. These commitment letters issued by the Bumi Armada Group are annexed as Annexure-E to the agreement entered into between the assessee and ONGC.

15. Subsequently, vide agreement dated 11/10/2014, entered into with Armada C7 Pte Ltd, the assessee agreed to take on lease the FPSO vessel, namely Armada Stelling II, from Armada C7 Pte Ltd for deploying it under the ONGC agreement for the purpose of extracting/producing mineral oils for ONGC. Under this agreement, the scope of work of Armada C7 Pte Ltd is as follows: –

“1. The Owner shall be responsible for constructing/converting the FPSO as detailed in the basis of design, Scope of Work and technical specifications and all functional/technical specifications set out in the ONGC Charter.

2. During the Construction Phase, the Owner shall be responsible for carrying out all alterations in the designs and Drawings of FPSO as required by ONGC.

3. The Owner shall be responsible for Mobilization of the FPSO to the C7 oilfield offshore, Mumbai, India

4 The Owner shall be responsible for providing design, engineering, procurement and equipment as well as sub-sea designs for the successful Construction of FPSO as set out in the ONGC Charter.

5. The Owner shall be responsible for installation of the sub-sea structures and the mooring system for the FPSO as set out in the ONGC Charter.

6. The Owner shall be responsible for the start-up of the FPSO and for obtaining the final Acceptance Certificate from ONGC certifying the performance of the FPSO and all systems.

7. The Owner shall following grant of the Final Acceptance Certificate, hand over to the Company all documentation, records, vendor data, technical manuals required for the operations and maintenance services as required under the ONGC Charter.

8. The Owner shall provide all insurances for the FPSO including and not limited to construction all risks, protection and indemnity, hull and machinery as required for the duration of the ONGC Charter and shall name the Company as the co-insured along with ONGC.

9. The Owner shall be responsible for Demobilization of the FPSO and all sub-sea equipments belonging to the Owner as set out in the ONGC Charter.”

16. On the other hand, the assessee was responsible for all operations and maintenance activities with regard to the FPSO vessel as envisaged in the ONGC agreement, which are summarised as follows: –

“(a) Safely operate and maintain the FPSO to process the well fluid to ONGC specifications and store the crude oil in cargo tanks;

(b) Safely operate and maintain the FPSO to process the sea water to ONGC specifications and supply to ONGC for injection in the wells;

(c) Safely operate and maintain the FPSO for the production and processing of gas and export thereof to ONGC’s pipeline;

(d) Safely operate and maintain the captive power production plant to produce power for captive consumption;

(e) Safely conduct the crude offload, including mooring and unmooring operations of the ONGC tanker,

(f) Ensure that the FPSO Facility including the machines and the equipment are operated and maintained in line with good industry practice and in accordance with the guidelines and procedures which are applicable to the FPSO Facility.

(g) Ensure safety of all personnel and maintain integrity of physical assets.”

17. From the perusal of both agreements, it is evident that Bumi Armada Berhad, through its subsidiary Armada C7 Pte Ltd, provided the FPSO vessel. On the other hand, the assessee provided O&M services along with additional functions and risk-taking capabilities. According to the assessee, the Shapoorji Pallonji Group partnered with the Bumi Armada Berhad Group and formed the joint venture entity to leverage the latter’s rich experience in the FPSO sector. Thus, as evident from the combined perusal of the aforementioned agreements, two companies with different areas of expertise came together to form a joint venture to bid for the project and jointly agreed to undertake the project. In such a case, it cannot be said that the roles and responsibilities of one company can be performed by the other company. The purpose of forming the joint venture is only to jointly bid for the project and win the mandate to perform the contract. At this stage, it is pertinent to note that the contract entered into between the assessee joint venture and the ONGC is a composite contract for the supply of the FPSO vessel and the provision of O&M services. Furthermore, it is equally imperative to note that without the unconditional commitment letters issued by Bumi Armada Berhad Group and Armada C7 Pte Ltd for the provision of the FPSO vessel after its conversion to meet the specification and technical requirements of the tender documents, the ONGC would not have signed the contract with the assessee, as the FPSO vessel was a very important aspect of the entire bidding process, which the ONGC required for production, storage and offloading of oil and gas operations conducted in the offshore waters of India. The fact that the contract was entered into between the assessee joint venture and the ONGC does not undermine the expertise of each partner of the joint venture, due to which the bid was assigned to the joint venture. Therefore, each party was responsible for its own scope of work, as agreed upon among them. The joint venture can at best be for the purpose of completion of the contract for which the bid was made. Further, the revenue from the contract shared by each partner is also not relevant, as the bid was made by the joint venture, considering the scope of the contract. It is also worth noting that in such a scenario, neither party acts as an agent of the other. In the contract dated 13/03/2013 entered into between the assessee and the ONGC, clause 12 clarifies explicitly that the assessee acts as an independent contractor. Therefore, we agree with the submissions of the assessee that it entered into an agreement on a principal-to-principal basis and not as an agent of its associated enterprise, i.e. Armada C7 Pte Ltd.

18. As regards the findings of the TPO that the assessee has not established what negotiations it had with the associated enterprise or what quotes for hiring the FPSO vessel were taken, it is pertinent to note that the entity providing the FPSO vessel is none other than one of the joint venture partners. Therefore, such a question doesn’t arise. On one hand, the TPO held that the associated enterprise would not have earned any revenue from the FPSO had the ONGC contract not been awarded to the assessee, however, on the other hand, the TPO did not dispute the fact that the assessee also would not have been able to earn on account of undertaking O&M services under the ONGC contract without obtaining the FPSO vessel from the associated enterprise on a bareboat charter hire basis. Therefore, it is evident that both parties jointly benefited from the contract with ONGC for which they came together to form a joint venture. Hence, we do not find any basis in the various findings of the TPO recorded in the foregoing paragraphs.

19. Insofar as the benchmarking of the international transaction of payment of bareboat charter hire charges to the associated enterprise, the assessee, considering itself as the tested party, adopted “Other Method” as the most appropriate method. Further, by comparing the proportion of bareboat charter hire day rate paid to the associated enterprise to the time charter day rate received from ONGC, with similar ratios in the case of contracts entered into by the sister concerns with third parties for bareboat charter hire of FPSO vessels and O&M activities, the assessee in its transfer pricing study report claimed that the international transaction of payment of charter hire fees to associated enterprise is at arm’s length.

20. It is the consistent plea of the assessee that the benchmarking approach of revenue split adopted by the assessee has been accepted by the learned DRP, in the assessee’s own case, for the assessment year 2016-17. In this regard, reliance was placed on the following findings of the learned DRP, rendered vide its directions dated 03/11/2020 for the assessment year 2016-17, which forms part of the paper book from pages 91-224: –

“It transpires that each offshore oil and gas field is different because of seabed topography, geology, depth etc. Therefore, to explore/produce/store/offload oil and gas from each of them would require separate/ different technically specific set of FPSO equipment/machinery and associated facilities. We have two examples before us, one, the FPSO in the instant case named as Armada Sterling II’ and the FPSO for the oil and gas field named as ‘D1’in the case of the sister concern of the assessee, ie., M/s Shapoorji Pallonji Bumi Armada Offshore Pvt. Ltd named as ‘Armada Sterling. Both FPSO are deployed off the Indian western coast. Perusal of the two agreements reveal that. although, the FPSOs and associated facilities are as per the unique requirements of the two different oil and gas fields with regard to their seabed topography, geology, depth etc. yet there is similarity in the purpose, operations and management and business activities of the exploration/production/storage/offloading of oil and gas. This would hold true in other instances also where offshore exploration/production/storage/offloading of oil and gas are undertaken through FPSO vessels. The businesses of FPSO vessels for offshore exploration/production/storage/offloading of oil and gas, are similar in nature/character The dictionary meaning of the word similar is ‘having a resemblance in appearance, character or quality without being identical. The business activities of making FPSO vessels, its hiring/ leasing, its operations and management and consequent/ related transactions, with consideration of all the relevant facts can be termed as transactions under the similar circumstances u/r 10AB because all FPSOs are deployed for offshore exploration/ production/storage/ offloading of oil and gas. Therefore, data of similar uncontrolled transactions under similar circumstances, having considered all the relevant facts, from other FPSO vessels can reasonably be termed as ‘similar uncontrolled transactions with or between the nonassociated enterprises as required u/r 10AB Therefore, we are inclined to invoke ‘other method under rule 10AB for determination of ALP of the hire/lease charges paid to the AE. We are of the considered view that the comparable uncontrolled transaction available/ provided by the assessee being similar FPSO hining/ leasing business for gas and oil exploration/ operations by the M/s Bumi Armada Offshore holdings Ltd (AE) to third party being Husky- CNOOC Madura Ltd, which is unrelated to the AE group company, need to be considered for TP benchmarking, because, one, it is similar in nature/character and it is with an unrelated third party. It can be treated as acceptable internal.comparable due to similarity in services, economic factors, management factors, finance involvement etc. We find support for acceptance of internal comparables in the cases of Mattel Toys (1) (P.) Ltd. 144 ITD 76 (Mum.- Trib.), Birla Soft (India) Ltd 59 SOT 156 (URO) (Delhi-Trib.), Pino Bisazza Glass (P.) Ltd. (2014) 146 ITD 644 (Ahd.-Trib.)

We have perused the additional evidence the certificate and the affidavit accompanied by the relevant and redacted (carefully edited to remove confidential references) version of agreement in this regard. The date of agreement is 08.08.2014. The agreement is for 10 years. The hire/lease day-rate paid for the FPSO is USD $ 2,30,000 against the total charter hire/ lease day-rate received for the FPSO and agreed operations at USD $ 2.79.972. Remaining USD $ 49,972 retained towards O & M services. Thus 82.15% (USD $ 2.30,000/ USD $ 2,79,972 x 100) of the total charter hire/lease day-rate received was paid towards hire/ lease day-rate of the FPSO, In the instant case the same payment for hiring/ leasing day-rate of the FPSO works out at 70.97% (USD $1,57,383/ USD $ 2.21.739.0892 x 100) (USD $ 1,57,383 is average day rate] of the total charter hire/lease day-rate received. In the instant case, the outgo for the hiring/ leasing dayrate of the FPSO is lower than the comparable transaction between AE and third party. The transaction is reasonable on this count.”

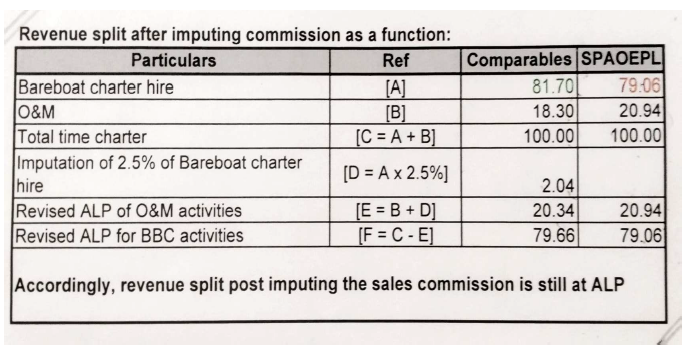

21. However, the TPO rejected the reliance placed by the assessee on the findings of the learned DRP on the basis that there is nothing on record to show that it was discussed in the assessment year 2016-17 that the assessee is transferring the amount received from ONGC for bareboat charter hire charges to the associated enterprise on a back-to-back basis, without retaining any margin. On the contrary, according to the assessee, the only change in the instant year is the presentation in the financial statements, which is a result of adopting Ind-AS 116, effective from the financial year 2019-20. According to the assessee, Ind-AS 116 requires the disclosure of lease transactions in a particular manner. At this stage, it is pertinent to note that the Revenue has not brought any material on record to show that the O&M services rendered to ONGC and the supply of the FPSO vessel in the year under consideration were under a contract different from the contract considered in the assessment year 2016-17. Therefore, such being the facts, it is amply evident that the entire edifice of rejecting the reliance placed by the assessee on the findings of the learned DRP in the assessee’s own case for the assessment year 2016-17 is based on the recording of transactions in the books of account. It is well settled that mere entry in the books of account is not determinative of liability towards income tax for the purpose of the Act. Therefore, given the facts, we do not find any merit in the submissions made on behalf of the Revenue that the findings made in the assessment year 2016-17 are distinguishable on the facts. Since the contract with ONGC and the associated enterprise was entered into for a period of 9 years, and the assessee has followed the benchmarking approach accepted by the learned DRP in the assessment year 2016-17, thus, in the absence of any change in facts or arrangement between the parties, we are of the considered view that a different stand cannot be taken in the year under consideration. In this regard, gainful reference can be made to the decision of the Hon’ble Supreme Court in Radhasoami Satsang v. CIT ITR 321 (SC). From the perusal of the aforesaid findings of the learned DRP, it is also evident that the aspect of difference in FPSO and associated facilities, qua the seabed topography, geology, depth, etc., was also considered by the learned DRP in the assessment year 2016-17.

22. As regards the without prejudice submission made during the hearing that even after imputing 2.5% commission for the bareboat charter hire, the transaction would still be at arm’s length, the learned AR placed reliance upon the following computation: –

23. Having perused the aforesaid computation, we find that even after imputing 2.5% commission payable to the assessee for the bareboat charter fees paid to the associated enterprise, the assessee is still paying less than the comparable instances. Therefore, we are of the considered view that, in any case, the international transaction resulted in an arm’s length outcome, even after considering that the assessee should have been paid a commission of 2.5% for the bareboat charter hire transaction.

24. Accordingly, in view of our aforesaid findings in the facts and circumstances of the present case, we do not find any merit in the transfer pricing adjustment of INR 10,47,30,105 made by the TPO/AO. Hence, the same is directed to be deleted. As a result, grounds no.4-10 raised in assessee’s appeal are allowed.

25. Ground no.11 raised in the assessee’s appeal pertains to the non-grant of credit of tax deducted at source. As the adjudication of this ground requires verification of the basic facts, we deem it appropriate to restore this issue to the file of the jurisdictional AO for de novo consideration after necessary verification/examination of the facts qua this issue. As a result, ground no.11 is allowed for statistical purposes.

26. Ground no.12, raised in assessee’s appeal, pertains to the levy of interests under section 234A and section 234B of the Act, which are consequential in nature. Therefore, this ground needs no separate adjudication.

27. Ground no.13, raised in assessee’s appeal, pertains to the levy of interest under section 234C of the Act.

28. The AO vide impugned final assessment order levied interest amounting to INR 24,33,595 under section 234C of the Act.

29. During the hearing, the learned AR submitted that the interest under section 234C of the Act should be computed on the returned income filed by the assessee instead of the assessed income. On the other hand, the learned DR vehemently relied on the computation made by the AO.

30. We have considered the submissions of both sides and perused the material available on record. As per provisions of section 234C of the Act, the interest is levied either on failure to pay the advance tax by the assessee or on shortfall in payment of advance tax as compared to tax due on the returned income. Thus, it is pertinent to note that section 234C refers to the term “returned income” in comparison to section 234B, which refers to the term “assessed tax” for levying interest. Accordingly, we direct the jurisdictional AO to compute the interest under section 234C of the Act, as per law, after taking into consideration the returned income of the assessee. Accordingly, ground no. 13 raised in assessee’s appeal is allowed for statistical purposes.

31. Ground no.14, raised in assessee’s appeal, challenges the initiation of the penalty proceedings under section 270A of the Act, which is premature in nature. Therefore, this ground is dismissed.

32. In the result, the appeal by the assessee is partly allowed for statistical purposes.