PR/Communication is an “Agency Business,” Ineligible for 44AD Presumptive Taxation.

Issue

Whether an assessee engaged in a Public Relations (PR) and communication business, which is in the nature of an “agency business,” is eligible to compute their income under the presumptive taxation scheme of Section 44AD of the Income-tax Act, 1961.

Facts

- The assessee filed an original return for AY 2018-19, computing income using a mix of Section 44AD and Section 44ADA (for professionals).

- The assessee’s TDS credits showed receipts under various heads, including Section 194J (Fees for Professional or Technical Services).

- The assessee later filed a revised return, attempting to compute income from their entire business turnover at 6% under Section 44AD.

- The department challenged this, contending that the assessee’s PR/communication activity was an “agency business.”

Decision

- The court ruled in favour of the revenue.

- It held that the assessee’s PR/communication activity constitutes an “agency business.”

- Section 44AD(6)(iii) of the Act specifically excludes a person carrying on an “agency business” from the benefits of the presumptive taxation scheme.

- Therefore, the revised return filed by the assessee, which incorrectly recomputed income under Section 44AD, was not in line with the law and was liable to be rejected.

Key Takeaways

- Specific Exclusions: The presumptive taxation scheme under Section 44AD is not available for all small businesses. It specifically excludes incomes from “agency business” and “commission or brokerage.”

- Nature of Business is Key: The nature of the assessee’s activity (PR/communication) was held to be an “agency business,” making it ineligible for the 6% presumptive rate.

- TDS as an Indicator: The receipt of payments under Section 194J (Professional Fees) often indicates a business (like PR/agency or a specified profession) that is outside the scope of the simplified Section 44AD.

- Invalid Revised Return: A revised return must be legally valid. A return that incorrectly claims the benefit of a section for which the assessee is statutorily ineligible is not a valid revision.

IN THE ITAT BANGALORE BENCH ‘SMC’

Roshan Mohan

v.

Income-tax Officer*

Laxmi Prasad Sahu, Accountant Member

IT Appeal No. 1390 (Bang.) of 2025

[Assessment year 2018-19]

[Assessment year 2018-19]

SEPTEMBER 25, 2025

Deepak Chopra, CA for the Appellant. Ganesh R. Ghale, Adv.,Standing Counsel for the Respondent.

ORDER

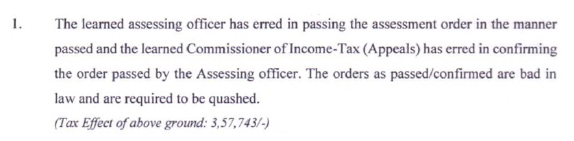

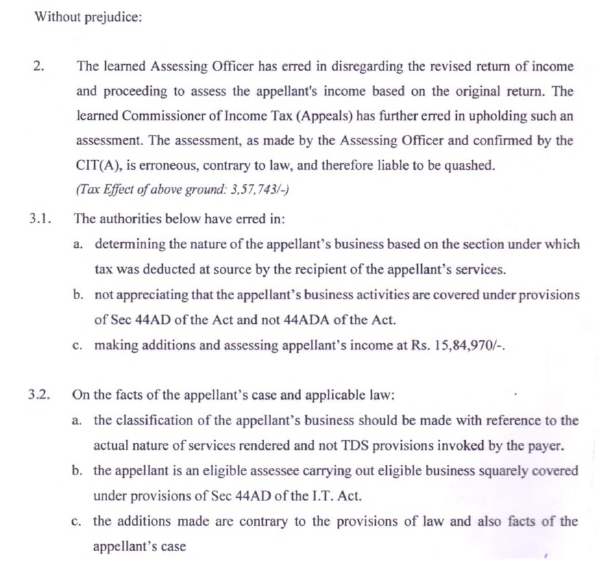

1. This appeal is filed by the assessee against the Order passed by the CIT(A) vide DIN and Order No. ITBA/N FAC/S/250/2025-26/1076128451(1) dated 08.05.2025 on the following grounds of appeal :

2. from the above grounds it is clear that sole issue raised by the assessee is regarding not accepting revised return filed by the assessee.

3. Briefly stated, the facts of the case are that assessee filed his return of income on 08.08.2018 declaring total income of Rs.16,44,968/- for Assessment Year 2018-19 and has revised return of income on 29.03.2019 declaring total income of Rs.2,47,000/-. The case was selected for scrutiny to examine the issue of reduction of income in revised income as compared to original return of income. Accordingly, during the scrutiny, the AO asked for explanation / justification as noted to substantiate such reduction of income in the revised return of income in comparison to original return of income filed. In response assessee submitted that original return of income was filed by taking the gross turnover as applicable under section 44AD of the Act partly and balance turnover as applicable under section 44ADA of the Act resulting in income of Rs.16.44 lakhs. The original return of income was filed in consequence with the TDS deducted applied on the gross turnover as applicable to provisions of sections 194C and 194A of the Act resulting in income of Rs.69.44 lakhs was the contention of the assessee. Further, he claimed that same is revised by admitting 6% as applicable under section 44AD of the Act on the entire business turnover resulting in deduction of income and accordingly contended the non-applicability of provisions under section 44AD of the Act as submitted on the part of the income covered by TDS under section 194J of the Act. During the course of assessment proceedings assessee’s contention is to hold such non-applicability of section 44ADA of the Act to the business turnover involving qualified service under section 194J of the Act as admitted in the original return of income as attributable to such business turnover. His reason is not maintainable as explained by the AO in the Assessment Order. Accordingly, AO considered original return of income and did not consider revised return filed by the assessee.

4. Aggrieved from the above Order, assessee filed appeal before the learned CIT(A) and the learned CIT(A) after considering the detailed submissions and discussions observed as follows:

“Thus, the sole motive of assesseebehind filing revised return was to present a lower income than actual, by creating a false notion about nature of work.

It was because of this reason that the assessee cleverly changed the nature of business (as mentioned earlier) in his revised return of income than as shown in original return of income, despite the fact that it is an unchangeable fact.

In view of above facts and discussion it is clear that the income declared by assessee in revised return of Rs. 2,47,000/- is not the correct income and the income declared in original return of Rs. 16,44,968/- is the correct income.

And hence the total income of the assessee is taken as Rs. 16,44,968/-as declared in original return of income.”

5. Aggrieved from the above assessment order, assessee filed appeal before the Tribunal. During the course of hearing the learned Counsel reiterated the submissions made before the lower authorities and submitted that assessee is engaged in rendering public relations services which is called PR services and it does not fall under section 44ADA of the Act. Assessee is not providing any professional services. Professional services require some specialization in the field of providing services. Therefore, as per the provision of section 44ADA of the Act, assessee does not fall under any of the services mentioned in section 44ADA of the Act and he also submitted that the Board has prescribed specified the following services which comes under section 44AD of the Act Notified professions : (a) The profession of authorized representative; and (b) the profession of film artist (actor, cameraman, director, music director, art director, dance director, editor, singer, lyricist, story writer, screen play writer, dialogue writer and dress designer) – Notification : No.SO17(E), dated 12-1-1977/profession of Company Secretary – Notification : No.SO 2675, dated 25.9.1992/profession of Information Technology – Notification : No.SO385(E), dated 4-5-2001.

6. On the other hand, learned DR relied on the Order of the lower authorities and strongly contested that revised return filed by the assessee is not acceptable because there is no omission or mistakes in the original return filed by the assessee as per section 139(5) of the Act. The original return filed by the assessee after thoughtful considerations there is no omission or wrong submission. Therefore, learned CIT(A) has rightly dismissed appeal of the assessee. He further submitted that agreement produced by the learned Counsel is not related to the impugned Assessment Year. It relates to the following Assessment Years.

7. In the rejoinder, the learned Counsel undertook that the facts, terms and conditions and contents of the agreement are same only the period is changed by mistake for the following Assessment Year’s agreement is produced and submitted that available agreement must be considered and there is no change in terms and conditions for the previous Assessment Year, just it is a renewal

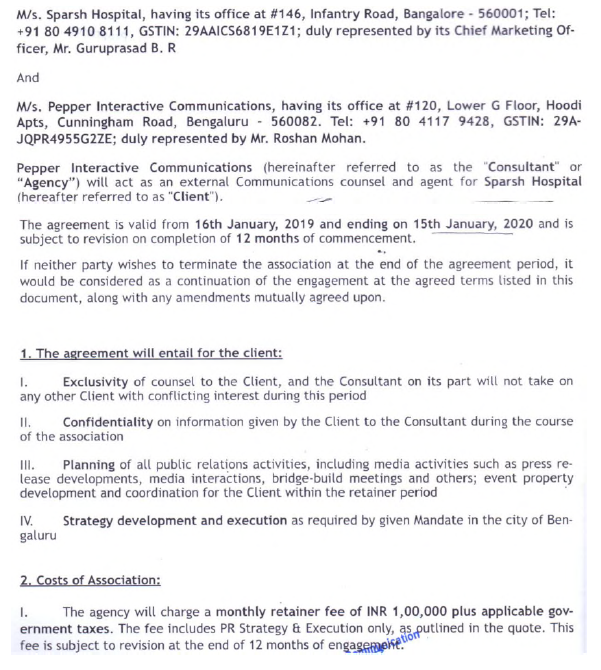

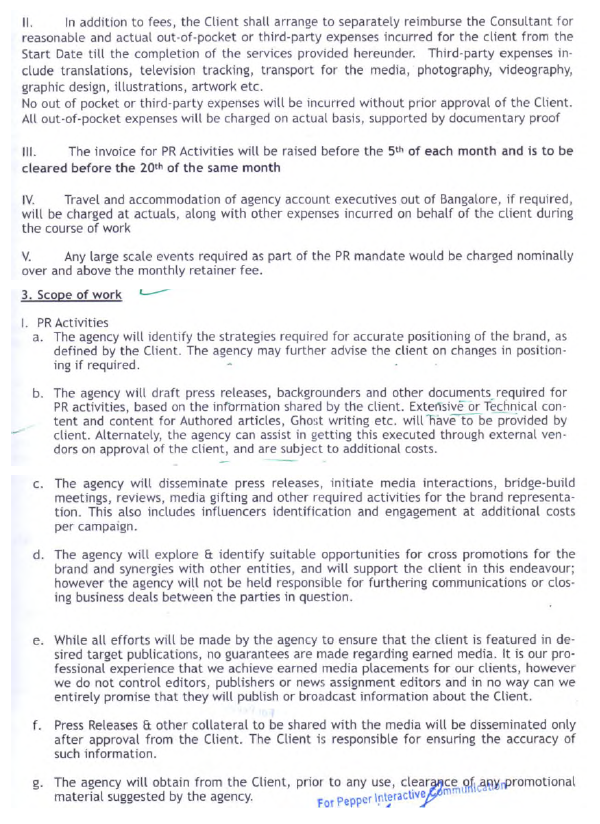

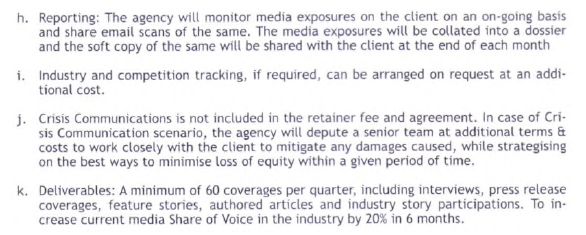

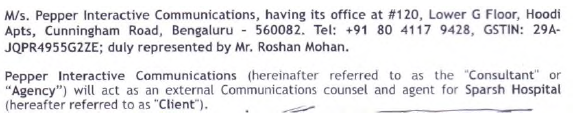

8. Considering the rival submissions, we noted that originally assessee has filed his return of income on 18.08.2018 declaring income of Rs.16,44,968/- and adjusted the TDS deducted on the payments received. On going through the computation of income filed which is placed at Paper Book Page No.44, it is noted that assessee has computed his income under section 44AD of the Act of Rs.1,82,534/- and under section 44ADA of the Act, presumptive profits of Rs.16,44,968/-. Later on 28.03.20-18, assessee has revised his return of income and computed gross total income from business / profession of Rs.3,07,001/- and the entire receipts were computed as income under section 44AD of the Act. The revised return filed by the assessee was not accepted by the AO computed under section 44AD of the Act. To decide this issue, whether the assessee will cover u/s 44AD or not, it is necessary to go to the contents of the agreement which is placed at Paper Book Page Nos.64 to 66. The relevant part of the agreement is as under:

9. On careful reading of the above agreement, the agreement itself says as under para 3. “The agreement says that business / services paid outside by the assessee is a consultant agency and he will get external communication / agent. From the above agreement it is clear that assessee is providing agency services”.

10. The agency service is out of purview of section 44AD of the Act. Section 44AD(6)(3) of the Act says as under:

44AD. [Special provision for computing profits and gains of business on presumptive basis. [Substituted by Act 33 of 2009, Section 20 (w.e.f. 1.4.2011).]

[(6) The provisions of this section, notwithstanding anything contained in the foregoing provisions, shall not apply to-

(i) a person carrying on profession as referred to in sub-section (1) of section 44AA;

(ii) a person earning income in the nature of commission or brokerage; or

(iii) a person carrying on any agency business.]

11. Assessee relied on the following judgments:

| i. | CIT v. Bhagwan Broker Agency [1993] 70 Taxman 453/[1995] 212 ITR 133 (Raj) on 11 May 1993 |

| ii. | Lakshminarayan Ram Gopal and Son Ltd., v. The Government of Hyderabad on 1 April 1954 |

| iii. | Pramod-Lele v. ITO, ITAT, Mumbai |

12. The conjoint reading of the agreement noted supra and section 44AD(6)(iii) noted supra the agency business is not covered under the provision of section 44AD of the Act. Accordingly, the revised return filed by the assessee is not in the line of section 139(5) of the Act.

13. The case laws relied on by the learned Counsel are not applicable to the facts of the present case since assessee is providing services which is clear from the agreement noted supra.

14. Accordingly, there is no omission or wrong statement in the revised return filed by the assessee. The AO not accepting the revised return is correct.

15. In the result, appeal filed by theassessee is dismissed.