TDS Credit Allowed on Bond Maturity Even When Income Was Taxed on Accrual.

Issue

Can the tax department deny a taxpayer credit for Tax Deducted at Source (TDS) in the year of maturity of a bond, on the grounds that the taxpayer had already offered the corresponding interest income to tax on an accrual basis in prior assessment years?

Facts

- The assessee had invested ₹4 crores in RBI bonds.

- Over the life of the bonds, the assessee consistently offered the interest income to tax on an accrual basis in the respective assessment years (as required by Section 145) and paid taxes on it.

- In the Assessment Year 2023-24, the bonds matured, and the assessee received the maturity proceeds.

- On this maturity, TDS of ₹24 lakhs was deducted (as TDS is deducted on a payment basis).

- The assessee claimed this ₹24 lakh TDS credit in their return for AY 2023-24.

- The Assessing Officer disallowed the TDS credit, creating a mismatch, as the income had already been taxed in previous years.

Decision

- The High Court (implied) ruled decisively in favour of the assessee.

- It held that the assessee was entitled to claim the TDS credit in the Assessment Year 2023-24, the year in which the tax was actually deducted.

- The court’s reasoning was that the assessee had already properly offered the income to tax on an accrual basis in the earlier years and paid taxes thereon. Denying the credit for the TDS now, when it was finally deducted, would be unjust.

Key Takeaways

- Accrual of Income vs. Deduction of TDS: This case highlights a common mismatch in the tax system. Income from certain instruments (like bonds) may be taxed on an accrual basis, while the corresponding TDS is deducted on a payment basis at maturity.

- Credit Must Be Allowed: The tax department cannot deny the TDS credit. The assessee is entitled to claim the credit in the year the TDS is actually deducted (as per the TDS certificate).

- Prevention of Double Disadvantage: The assessee correctly paid tax on the income as it accrued. Denying the TDS credit when the tax is finally deducted would result in a “double whammy”—the assessee would have paid tax on the income and would also lose the benefit of the tax deducted on that same income.

- AO’s Duty to Reconcile: The AO’s role is to reconcile the facts, not to disallow a legitimate credit. The proper procedure would be to allow the TDS credit in the year of deduction.

IN THE ITAT AGRA BENCH ‘DB’

Surbhi Anand

v.

ACIT*

Sunil Kumar Singh, Judicial Member

and BRAJESH KUMAR SINGH, Accountant Member

and BRAJESH KUMAR SINGH, Accountant Member

IT APPEAL No. 258 (Agr) of 2025

[Assessment year 2023-24]

[Assessment year 2023-24]

OCTOBER 9, 2025

Sahib P. Satsangi, CA for the Appellant. Anil Kumar, Sr. DR for the Respondent.

ORDER

Brajesh Kumar Singh, Accountant Member.- This appeal filed by the assessee is directed against the order dated 15.03.2025 of the National Faceless Appeal Centre, Delhi, Addl/ JCIT(A), Kochi, relating to Assessment Year 2023-24 arising out of intimation u/s 143(1) of the Income Tax Act, 1961 (hereinafter referred to ‘the Act’) dated 11.12.2023.

2. Brief facts of the case: – In this case, the assessee had filed her return of income declaring a total income of Rs. 1,88,12,590/-. The assessee had claimed TDS amounting to Rs. 34,37,842/- in the return of income filed, whereas, in the order u/s 143 (1) of the Act, dated 11.12.2013, TDS was allowed to the assessee to the extent of Rs. 8,19,493/-. The assessee submitted that he had invested in various Government bonds, (hereinafter referred to as 8% RBI Bond) through M/s Stock Holding Corporation of India Ltd. (hereinafter referred to as SHCIL) as under:

| 8% RBI Bond | Cumulative option | 4,00,00,000 |

| 8% RBI Bond | Non- Cumulative option | 4,00,000 |

2.1 Further, it was submitted that the assessee had invested in 7.75% taxable Government of India Bonds (non-cumulative option) through M/s HDFC Bank Ltd.

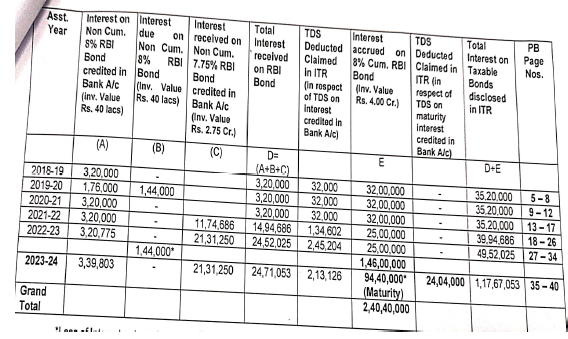

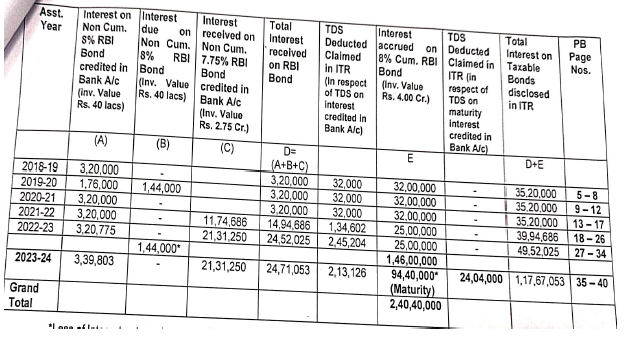

2.2 Further, it was submitted that the assessee had declared the interest on accrual basis in the returns filed for the earlier years and had deposited her tax liability on such interest income in different Assessment Years whose assessments have been completed under section 143(1) as under. A.Y. 2018-19 -Rs.32,00,000 A. Y. 2019-20 – Rs. 33,44,000 A.Y. 2020-21 – Rs. 32,00,000 A. Y. 2021-22 – Rs. 25,00,000 A. Y. 2022-23 -Rs.25,00,000 Total – Rs. 1,47,44,000 Further, it has been submitted that out of the Interest received on maturity of Rs. 2,40,40,000 during the year (on which TDS has been deducted u/s 193 of the I.T. Act, 1961) the income relatable to the year under consideration of Rs. 92,96,000, declared in the return after reducing the interest accrued stated as above, has been accepted.

2.3 The assessee submitted that, on the maturity of the said bonds, the RBI credited to proceed including interest of Rs. 2,40,40,000/- on maturity and deducted TDS u/s 193 of the Act amounting to Rs. 24,04,000/-. The assessee further submitted that she had disclosed the interest income on an accrual basis in her Income Tax Returns for Assessment Years 2018-19 to 202223, in accordance with section 145 of the Act, and paid due taxes thereupon, and therefore, the interest income having already been offered for taxation in those years, were again not offered during the year, even though the entire interest amount was received during the year. It was further submitted that the assessee had declared interest income on accrual basis to the tune of Rs. 1,47,44,000/- for A.Ys. 2018-19 to 2022-23 and hence offered the balance amount of Rs. 92,96,000/-, (Rs. 2,40,40,000/- – (Rs. 1,47,44,000/-). It was submitted that while processing the return u/s 143 (1) of the Act, the CPC accepted the returned income but disallowed TDS credit of Rs. 24,04,000/-, and submits that the assessee is very much entitled to the TDS credit, and by not allowing the same would result in computation of tax liability beyond and against the scheme of the Act.

3. Against the denial of the TDS claim, the assessee filed an appeal before the ld. CIT (A) as well as a rectification petition u/s 154 of the Act before the CPC. The ld. CIT (A) dismissed the appeal of the assessee and it was submitted by the assessee that the ld. CIT(A) passed the impugned order without issue of any notice, holding that on account of subsequent rectification orders under section 154 passed by CPC the present appeal got merged with those orders and the remedial option available to the appellant was to file appeal against the rectification order u/s 154 dated 08.04.2024.

4. Aggrieved by the said order, the assessee is in appeal before us, on the following grounds of appeal: –

“1. Because the learned Addl./JCIT (A), Kochi has erred both on facts and in law in dismissing the appeal of the appellant filed against order passed under section 143(1) as infructuous holding that on account of subsequent rectification orders under section 154 passed by the CPC the present appeal merged with those orders and the remedial option available to the appellant was to have filed appeal against the rectification order u/s 154 dated 08.04.2024.

2. Because the learned authorities below have erred both on facts and in law in not allowing the claim of the credit of TDS of Rs.24,04,000 reported in Form 26AS-Annual Tax Statement of the appellant by the M/s Stock Holding Corporation Ltd. in respect of the TDS deducted on the interest received on maturity of 8% Taxable Gol Bond. The disallowance made is liable to be

3. Because in any view of the case, the appellant having declared the interest on accrual basis in the returns filed for the earlier years deposited his tax liability on such interest income in different Assessment Years whose assessments have been completed under section 143(1) as under. A.Y. 2018-19 – Rs.32,00,000 A. Y. 2019-20 – Rs. 33,44,000 A.Y. 2020-21 – Rs. 32,00,000 A. Y. 2021-22 – Rs. 25,00,000 A. Y. 2022-23 – Rs.25,00,000 Total – Rs. 1,47,44,000 Thus, out of the Interest received on maturity of Rs. 2,40,40,000 during the year (on which TDS has been deducted u/s 193 of the I.T. Act, 1961) the income relatable to the year under consideration of Rs. 92,96,000, declared in the return after reducing the interest accrued stated in the above table, has been accepted.

4. Because the learned authorities below have erred both on facts and in law by not allowing the credit of the TDS of Rs.24,04,000 claimed without appreciating that the appellant had declared his income chargeable under the head ‘income from other sources’ on mercantile system/accrual basis of accounting regularly employed by him in terms of section 145 of the I.T. Act, 1961 and deposited tax thereon himself resulted in payment of tax twice on the same income.

5. During the hearing before us, the Ld. AR submitted that the aforesaid decision of the Ld. CIT(A) is bereft of the situation where the appeal is filed against order passed under section 143(1) and nothing precludes the assessee to seek remedial action by raising online rectification request before CPC seeking redressal of her grievance under section 154. It was further submitted that had the grievance been resolved by CPC the appeal filed before CIT(A) could have been withdrawn. It was further submitted that it was not a case that the appeal filed against the Intimation u/s 143(1) was absolutely barred in the scheme of Act. Thereafter, the Ld. AR had relied upon various case laws to submit that the said action of the Ld. CIT (A) was not correct. 6. The Ld. AR also relied upon a written submission filed, which is reproduced as under:

” The appellant is an individual earning income from House Property, Business, Capital Gains and Other sources consisting of Interest and Dividend on investments. During the A.Y. 2018-19 the appellant made investments in 8% Taxable Government of India Bonds (herein after referred to as 8% RBI Bond) through Mis Stock Holding Corporation of India Ltd. (herein after referred to as SHCIL) as under:

| 8% RBI Bond | Cumulative option | 4,00,00,000 |

| 8% RBI Bond | Non- Cumulative option | 4,00,000 |

In the A.Y. 2021-22 the appellant invested in 7.75% Taxable Government of India Bonds (Non-Cumulative option) (herein after referred to as 7.75% RBI Bond) through M/s HDFC Bank Ltd.

During the impugned year, appellant’s investments in 8% RBI Bonds got matured and redeemed into her bank account. In respect of the cumulative option on the maturity of these 8% RBI Bonds M/s SHCIL, custodian of the GOI Bonds issued by the Reserve Bank of India, credited the proceeds including interest of Rs. 2,40,40,000 on maturity and deducted Tax Deducted at Source (TDS) u/s 193 of the I.T. Act, 1961 of Rs. 24,04,000 thereon, which was reported by SHCIL in the Annual Tax Statement – Form No. 26AS for the impugned year i.e. A.Y. 202324 (PB Page Nos. 42-62, relevant page 47)

That the appellant has disclosed the interest earned on 8% Taxable Government of India Bonds both cumulative and non-cumulative in her ITR filed for various years. The tax was paid on the interest under cumulative option on accrual basis in terms of section 145 of the I.T. Act, 1961, the detail of the interest earned is as under.

Loss of interest not received in Bank in A.Y. 2020-21 Rs. 1,44,000 adjusted from Maturity hence net income of Rs 02,00,000 considered in A.Y. 2023-24 on account of maturity of bond the bonds

Therefore, the interest income earned on afore stated 8% Cumulative RBI Bond was disclosed in the ITRs on accrual by the appellant to the tune of Rs. 1,47,44,000 filed for the A.Ys. 201819 to 2022-23 and tax thereon stands paid. Hence, there is no question of taxation of the same interest again in the year of maturity. The balance interest income of Rs. 94,40.000 pertaining to the year on account of maturity is the income for the impugned year ie. A.Y. 2023-24. Since the 8% Non-Cumulative RBI Bond also matured during the year and the appellant did not receive the interest of Rs. 1,44,000 for the A.Y. 2019-20 the same was adjustment from the interest on maturity and the appellant paid tax on the net interest income of Rs. 92,96,000 in the impugned year

The Id. CPC processed the return under section 143(1) on the returned income but disallowed the claim of the TDS credit of Rs. 24,04,000 reflected in Form 26AS for the impugned year resulting in appellant filing an appeal before the Ld. CIT(A) and also an online rectification under section 154 of the I.T. Act, 1961.

The Id. CIT(A) passed the impugned order without issue of any notice, dismissing the appeal in limine, holding that on account of subsequent rectification orders under section 154 passed by CPC the present appeal merged with those orders and the remedial option available to the appellant was to file appeal against the rectification order u/s 154 dated 08.04.2024.

The aforesaid decision of the Id. CIT(A) is bereft of the situation where the appeal is filed against order passed under section 143(1) and nothing precludes him to seek remedial action by the appellant by raising online rectification request before CPCseeking redressal of his grievance under section 154. Had the grievance been resolved by CPC the appeal filed before CIT(A) could have been withdrawn, it is not a case that the appeal filed against the Intimation u/s 143(1) is absolutely barred in the scheme of Act.

It is respectfully submitted that the appellant has two remedies against the Intimation u/s 143(1), viz (i) file appeal u/s 246A, or (ii) file rectification application u/s 154. Accordingly, the appellant filed appeal and a rectification-application u/s 154 which is not only one of the available remedies but also a simpler remedy and practically resorted to by many of the assessees, particularly in the matter of the adjustment involved in the present appeal.

Your honours kind attention is invited to the decision of ITAT, Jodhpur Bench in the case of Akbar Mohammad, Nagaur v. ACIT, CPC, Bangalore ITA No. 108 & 109/Jodh/2021 order dated 31.01.2012 in which the Hon’ble Co-ordinate Bench has resolved the controversy, where the appeal was not filed against intimation order passed u/s 143(1) but under section 154. by holding as under “6.1 Of course, it is a case in point that the assessee did not file any appeal against the intimations passed us 143(1) of the Act and the Ld. Sr. DR is right to the extent that the assessee cannot be given relief for that reason. However, it is also a settled law that the assessee cannot be taxed on an amount on which tax is not legally imposable. Although, the assessee might have chosen a wrong channel for redressal of his grievance, all the same, it is incumbent upon the Tax authorities to burden the assessee only with correct amount of tax and not to unjustly benefit at the cost of tax payer Therefore, in the interest of substantial justice, we deem it expedient to restore the issue to the file of the Assessing officer with a direction to pass appropriate orders deleting the addition/disallowance after duly considering the settled judicial position in this regard, which have been decided in the three cases as enumerated above in Para 5.”

It is further submitted that CPC having rejected to online application for rectification did not allow the claim of credit of the TDS to the appellant and thus the grievance of the appellant remained unresolved and there would have been no help to the appellant in filing appeal against the subsequent order passed u/s 154/143(3) by CPC.

In this context it can be observed that the scope and ambit of power of rectification u/s 154 came to be considered and decided by the Hon’ble Supreme Court in T. S. Balaram, ITO v. Volkart Brothers [1971] 82 ITR 50 (SC). It was held in that case that the power of rectification of mistakes under section 154 of the Act is a very limited power which is restricted to rectification of mistakes apparent from the record. Besides, it must be a mistake which is patent on the face of the record and does not call for detailed investigation of the facts or require an elaborate argument to establish it. Itdoes not cover any mistake which may be discovered by a complicated process of investigation, argument or proof. The mistake sought to be rectified must be manifest and self-evident on the face of the record. It must be one which is apparent and not lurking, which is visible and not dormant, which can be seen and not hidden. It cannot be demonstrated to exist by relying upon materials outside the record. A decision on a debatable point of law or failure to apply the law to a set of facts which remain to be investigated cannot be corrected by way of rectification.

The appellant is very much entitled to the TDS credit and by not allowing the same, the same would result in computation of tax liability beyond and against the scheme of the Act. Hence it is prayed that the lower authorities be directed to accept the claim of appellant on merit.”

7. On the other hand, the Ld. DR supported the order of the Ld. CIT (A).

8. We have heard both the parties and perused the material available on record. We note that the Ld. CIT(A) dismissed the appeal of the assessee, on the ground that the correct recourse for the assessee was to file an appeal against the subsequent rectification order dated 08.04.2024 passed by the CPC, as the present appeal had merged in the subsequent rectification orders u/s 154 of the Act dated 30.01.2024 and 08.04.2024. The relevant finding of the Ld. CIT (A) in para no. 4 & 5 of the order is reproduced as under: –

“4. It is seen from the above and as stated by the appellant, that the Intimation u/s 143(1) dated 11.12.2023, against which the appellant has filed the present appeal has been subsequently rectified by Rectification orders u/s 154 dated 30/01/2024 and 08/04/2024, determining the total income of Rs. 1,88,12,590/-which is the same total income admitted by the assessee as Rs. 1,88,12,590/-, but raising demand of Rs. 29,92,530/-, by restricting the TDS based on Rule 37BA of the IT Act, 1961. which is reproduced in the previous para no.3 above. The remedial option available to the assessee was, to have filed an appeal against the said rectification order u/s 154 dated 08/04/2024.

5. In view of all the above, on merits of the case and also as the Intimation u/s 143(1) dated 11.12.2023, against which the present appeal has been filed, has merged in the subsequent rectification orders u/s 154 dated 30.01.2024 and 08/04/2024, the present appeal filed against the intimation u/s 143(1) dated 11/12/2023 is treated as infructuous and accordingly, the present appeal is dismissed.”

8.1 We have considered the above view of the Ld. CIT (A), and we do not agree with the decision of the Ld. CIT(A) in dismissing the appeal of the assessee for the reasons stated in the said order. The passing of the order u/s 143(1) of the Act, dated 11.12.2023 by the CPC is a separate order giving rise to a grievance to the assessee, against which the present appeal was filed. Therefore, it was the duty of the Ld. CIT(A) to adjudicate the said grievance, by passing an order and giving reasons either accepting the claim of the assessee or rejecting the claim of the assessee instead of dismissing it merely on technical ground, which is not sustainable in the eyes of the law. In this case, the assessee claims to offered the interest income received on maturity of the RBI bonds over the years i.e. from A.Y. 2018-19 to 2023-24, on accrual basis in terms of section 145 of the Act, and paid taxes thereupon, as per the chart submitted by the assessee and reproduced as under.

8.2 Apparently, the offering of such income and payment of due taxes, accordingly, by the assessee has been accepted by the Department. In this regard, the Rule 37BA(3) of the Income Tax Rules 1962, is reproduced as under:

“37BA.

(3) (i) Credit for tax deducted at source and paid to the Central Government, shall be given for the assessment year for which such income is assessable.

(ii) Where tax has been deducted at source and paid to the Central Government and the income is assessable over a number of years, credit for tax deducted at source shall be allowed across those years in the same proportion in which the income is assessable to tax.

41[(3A) Notwithstanding anything contained in sub-rule (1), subrule (2) or sub-rule (3), for the purposes of section 194N, credit for tax deducted at source shall be given to the person from whose account tax is deducted and paid to the Central Government account for the assessment year relevant to the previous year in which such tax deduction is made].”

8.3 On perusal of the computation of income filed by the assessee for A.Ys. 2018-19 to 2022-23, it is seen that the assessee has already paid taxes over the respective assessment years, as per the interest income offered by it on accrual basis on the aforesaid RBI bonds, after claiming proportionate credit of the TDS received from Stock Holding Corporation of India Limited and HDFC Bank Limited, as the case may be. Therefore, after giving thoughtful consideration, we are of the considered view that in the given facts of the case, the A.O. is directed to allow the TDS credit of Rs.34,37,842/- including Rs. 24,04,000/-, on the said bonds, as claimed by the assessee in the assessment year 2023-24 after due verification in term of Rule 37BA(3) (ii) of the I.T. Rules, 1962, and determine the tax payable or refundable, and pass the order accordingly. In terms of the above directions, the appeal of the assessee is allowed.

9. In the result, the appeal of the assessee is allowed.