ORDER

Anadee Nath Misshra, Accountant Member.- (A) This appeal vide I.T.A. No.131/Lkw/2024 has been filed by Revenue for assessment year 2021-22 against impugned appellate order dated 18/01/2024 (DIN & Order No.ITBA/APL/S/250/2023-24/1059905161(1) of Commissioner of Income Tax (Appeals) [“CIT(A)” for short]. In this appeal Revenue has raised the following grounds:

“1. Whether on facts and circumstances of the case and in law, the CIT(A) erred in deleting the addition of Rs.1,49,17,94,856/-made on account of disallowance of depreciation on tangible & intangible asset without appreciating the specific reasons mentioned by A. O. in assessment order for such disallowance.

2. Whether on facts and circumstances of the case and in law, the CIT(A) erred in deleting the addition of Rs.1,49,17,94,856/-without appreciating the fact that claim of the assessee for depreciation of Rs.1,49,17,94,856/- on Right to Collect Toll’ was disallowed on following facts: (a) ‘Right to Collect Toll’ does not fall under any of the categories of ‘intangible asset’ specified in clause 32(1)(ii) of the Income Tax Act, 1961. (b) The assessee is not a physical owner of the asset i.e. ‘Right to Collect Toll’ which is a pre-requisite condition for claiming depreciation in view of the CBDT Circular No. 09 of23.04.2014. (c) The claim of the assessee for allowing depreciation on the ground of ‘principal of consistency’ and sustained by the CIT(A) is not acceptable as the issue of claim of depreciation was not examined in the case of assessee in earlier years in light of CBDT circular dated 23.04.2014. This view finds support from the following case laws: Union of India & Anr. v. Radhu. “

(A.1) Grounds taken by the assessee in its Cross Objection are as under:

“1. Because Ld. CIT(A), Lucknow-3 erred on facts and law while dismissing the grounds relating to initiation of assessment proceeding u/s 143(2) of the Act, being the search assessment case, which is against the intent of amended provision of law, accordingly assessment order is liable to be quashed.

2. Because Ld. CIT(A), Lucknow-3 erred on facts and law while adjudicating the ground relating to net loss incurred in relevant year at Rs.1,30,42,77,771/-, however, considered by AO at Rs.1,20,20,10,587/- without speaking order.

3. Because Ld. CIT(A), Lucknow-3 erred on facts and law while not adjudicating the ground relating to brought forward and carry forward of business losses of Rs.5,40,48,933/- and unabsorbed depreciation of Rs.9,04,06,13,621/- as per applicable law of the Act claimed in ITR in relevant year not allowed by AO.”

(A.2) For the sake of convenience, the appeal filed by the Revenue and the Cross Objection filed by the assessee are hereby disposed of through this consolidated order.

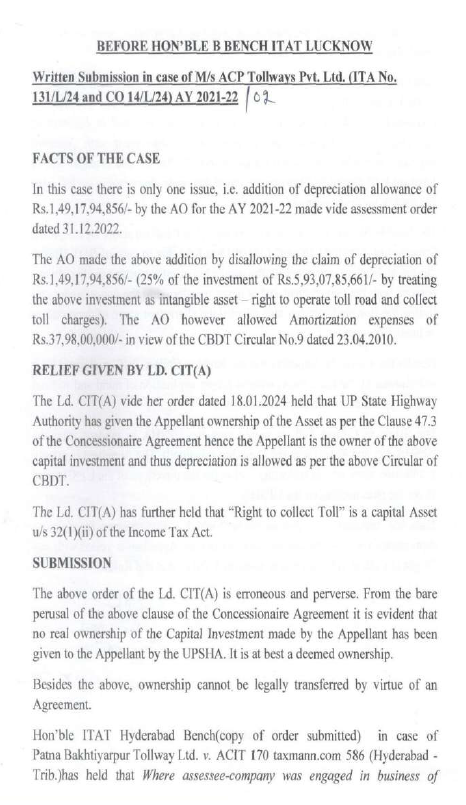

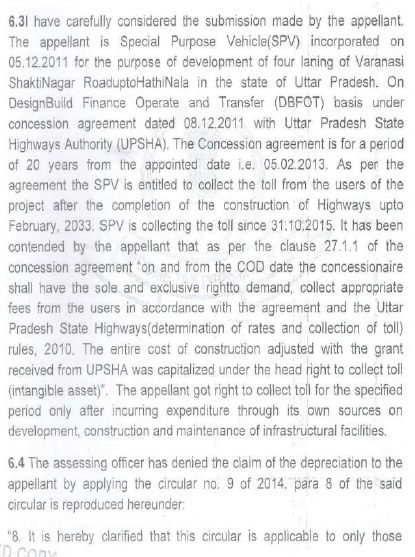

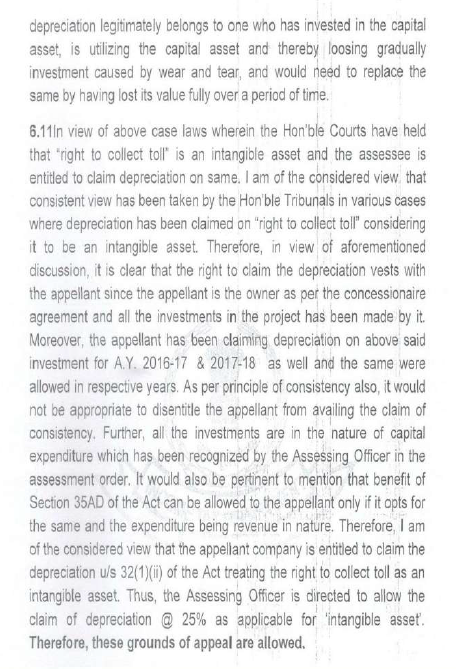

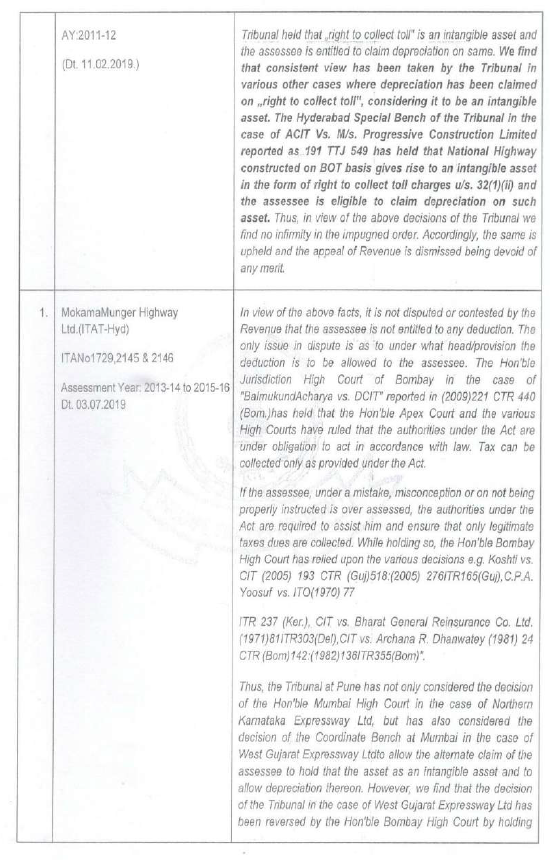

(B) The assessee company is a Special Purpose Vehicle (SPV) for the purpose of development of a portion of four lanes Varanasi Shaktinagar Road in the state of Uttar Pradesh, for which the assessee had entered into contract with UP State Highways (UPSHA) on Design, Build, Finance, Operate and Transfer (DBFOT) basis. The return of income was filed by the assessee showing loss of Rs.1,20,20,10,587/-. Under the agreement with UPSHA, the assessee has been given the right to develop and maintain the toll road and also the right to collect toll for a specified period. At page 10 of the assessment order, the Assessing Officer acknowledges that under the agreement between the assessee and UPSHA, the project was deemed to be acquired and owned by the assessee. However, the Assessing Officer has taken the view that deemed ownership, in the absence of physical ownership of asset, does not qualify the assessee to claim depreciation. The Assessing Officer took the view that CBDT Circular dated 23/04/2014, which had provision for amortization of expenses in BOT contracts (Build, Operate, Transfer) was applicable in the case of the assessee also and the assessee was not entitled to depreciation. However, in the return of income filed by the assessee, the assessee claimed that “Right to Collect” toll was a capital asset which qualified for claim of depreciation u/s 32 of the I. T. Act. The assessee opted to claim depreciation amounting to Rs.1,49,17,94,856/-and opted out of claiming amortization of the capital expenditure. The Assessing Officer disallowed the assessee’s claim for depreciation amounting to aforesaid amount of Rs.1,49,17,94,856/- and instead allowed amortization of expenses amounting to Rs.37,98,00,000/-. The assessee filed appeal in the office of learned CIT(A). Vide impugned order dated 18/01/2024, the learned CIT(A) partly allowed the assessee’s appeal. The learned CIT(A) took the view that Right to Collect Toll was an intangible asset and the assessee was entitled to claim depreciation on the same. The relevant portion of the order of learned CIT(A) is reproduced as under:

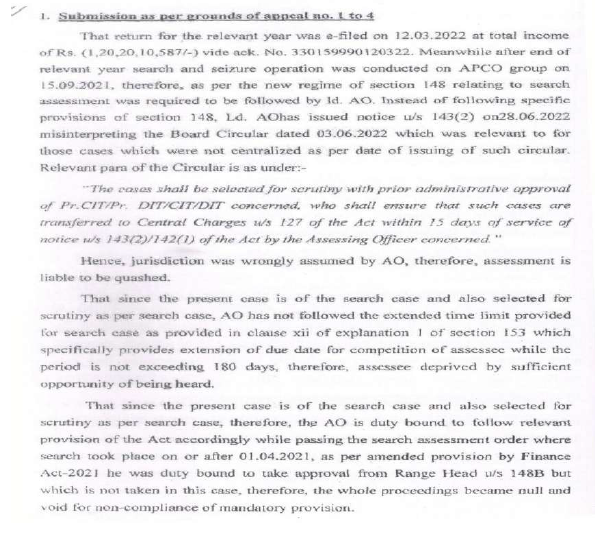

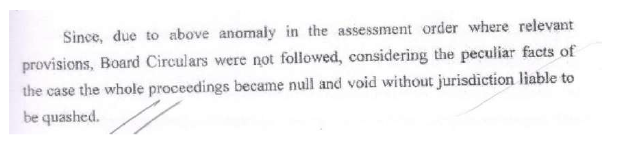

(B.1) The grounds taken by the assessee regarding validity of the assessment proceedings and jurisdiction of the Assessing Officer were dismissed by the learned CIT(A). The relevant portion of the order of the learned CIT(A) is reproduced as under:

(C) The present appeal and the Cross Objection before us have been filed by Revenue and by the assessee respectively in relation to the aforesaid appellate order dated 18/01/2024 of the learned CIT(A). In the course of appellate proceedings in Income Tax Appellate Tribunal, written submissions were filed by the office of the learned D.R., which is reproduced below for the ease of reference:

(C.1) From the assessee’s side, a paper book containing the following particulars was filed:

Moreover, the following documents were also filed from the assessee’s side:

| (1) |

|

CBDT Instruction F.No.225/81/2022/ITA-II dated 11th May 2022 |

| (2) |

|

CBDT Circular No.09/2014, dated 23rd April 2014 |

| (3) |

|

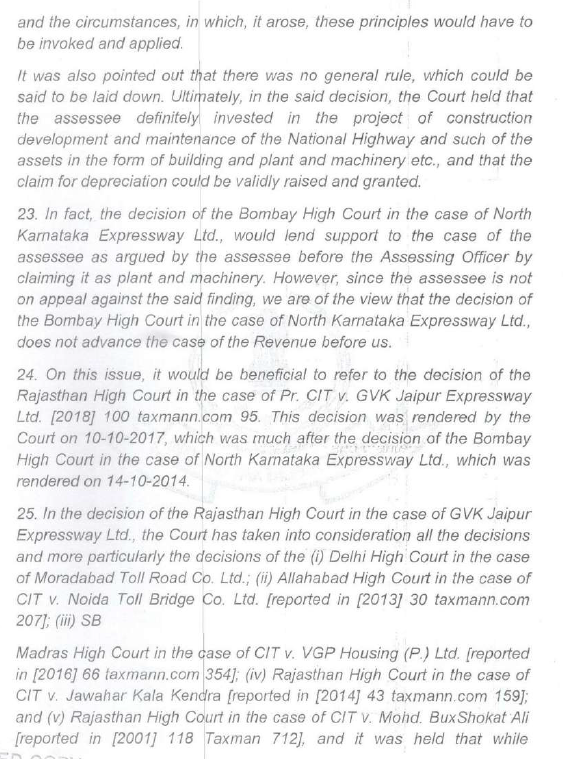

Hon’ble Allahabad High Court order dated March 15, 2023 in the case of CIT, Exemptions v. Swami Omkarananda Saraswati Charitable Trust ITR 245 (Allahabad) |

| (4) |

|

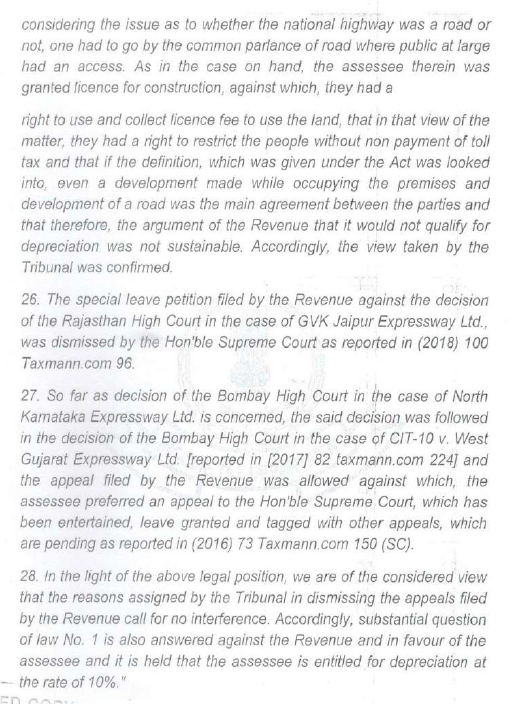

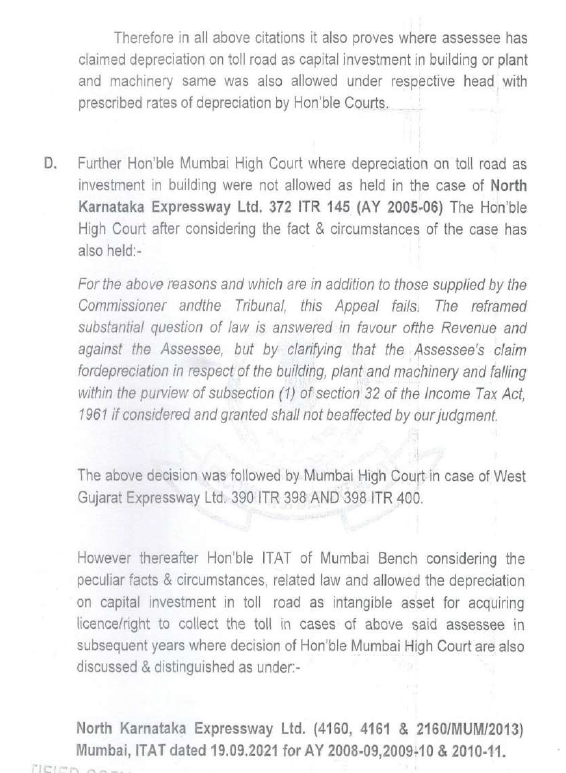

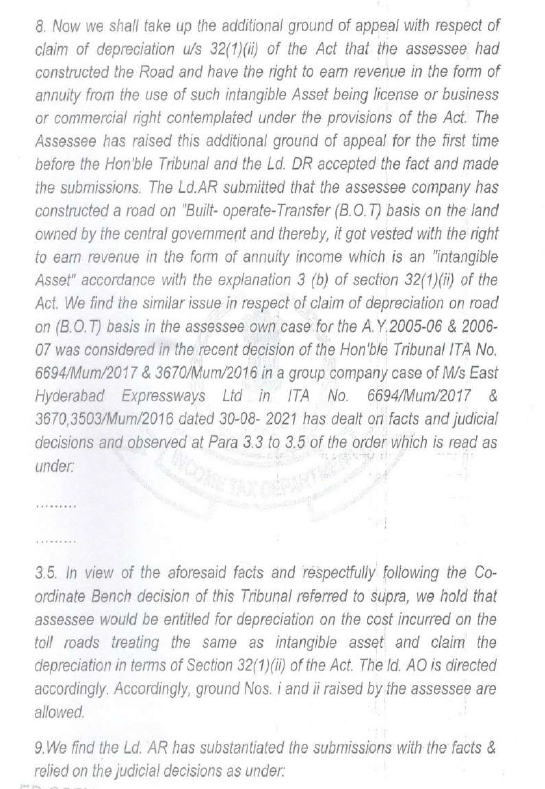

ITAT Mumbai Bench order in the case of North Karnataka Expressway Ltd. v. ACIT [IT Appeal Nos. 4160, 4161 (Mum.) of 2013 & 1230 (Mum.) of 2015, dated 20-9-2021] |

| (5) |

|

Copy of Panchnama in the case of APCO Infratech Pvt. Ltd. |

(D) At the time of hearing before us, learned Departmental Representative placed reliance on the assessment order and on the aforesaid written submissions referred to in foregoing paragraph (C) of this order. The learned A.R. for the assessee placed reliance on the paper book and other documents referred to in foregoing paragraph (C.1) of this order. He also placed reliance on the aforesaid impugned order of the learned CIT(A) as regards her order directing the Assessing Officer to allow depreciation to the assessee. Further, as regards the issues related to validity of the assessment proceedings and jurisdiction of the Assessing Officer, which were decided against the assessee by the learned CIT(A) in her aforesaid impugned order, the learned A.R. for the assessee placed reliance on submissions made in the course of appellate proceedings in the office of the learned CIT(A). These submissions are part of the paper book filed from the assessee’s side, and are reproduced below for the ease of reference:

(D.1) Further, the learned A.R. for the assessee also submitted that the Assessing Officer should be directed to allow brought forward business loss of Rs.5,40,48,933/- and unabsorbed depreciation of Rs.9,04,06,13,621/-. The aforesaid submissions covered the grounds taken in the appeal as well as in the Cross Objection before us.

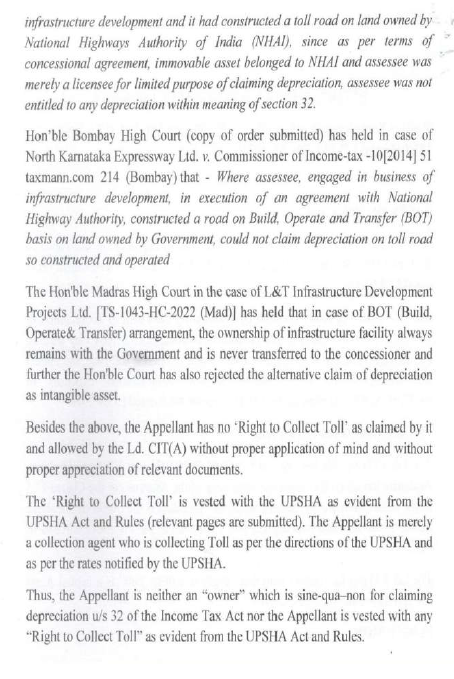

(E) We have heard both sides. We have perused materials on record. The Assessing Officer has taken the view that aforesaid CBDT Circular No. 9/2014, dated 23/04/2014 was applicable in the present case. On perusal of this circular, it is found that the circular was relevant for such cases in which the assessee was in BOT agreement for development of road public highways. In the present case before us, the assessee is in DBFOT contract and not BOT contract. A BOT contract encompasses Build, Operate and Transfer. However, the DBFOT contract is of a much wider scope as it also covers Design and Finance in addition to Build, Operate and Transfer. Since the assessee takes up additional responsibility towards design and finance in DBFOT contract, the aforesaid CBDT circular No.9/2024 dated 23/04/2014, which was issued for BOT contract is not applicable to the present case before us. Even otherwise, it is well settled and CBDT Circulars and Instructions are binding only to the extent they are beneficial for the assessee. If and when a CBDT Circular/Instruction is adverse to the assessee, it is not binding.

(E.1) Further, it is not in dispute that under DBFOT contract, the assessee entered into contract with UPSHA, the assessee was the deemed to have acquired and owned the project. Therefore, deemed ownership and acquisition of the project by the assessee is not in dispute. Moreover, the assessee was also in possession for the purpose of developing and maintaining the project and for exercising the right to collect toll. Therefore, the possession of the project by the assessee is also established. Given these facts and circumstances, the eligibility of the assessee for claiming depreciation u/s 32 of the Act is fully justified. The view taken by the Assessing Officer that physical ownership of the asset was mandatory and that the assessee was not eligible for depreciation is without any basis under the provisions of law as per section 32 of the I. T. Act, which deals with depreciation. In any case, deemed ownership and acquisition coupled with physical possession meets the requirement of physical ownership. Therefore, the stand taken by the Assessing Officer in disallowing the assessee’s claim for depreciation is patently wrong.

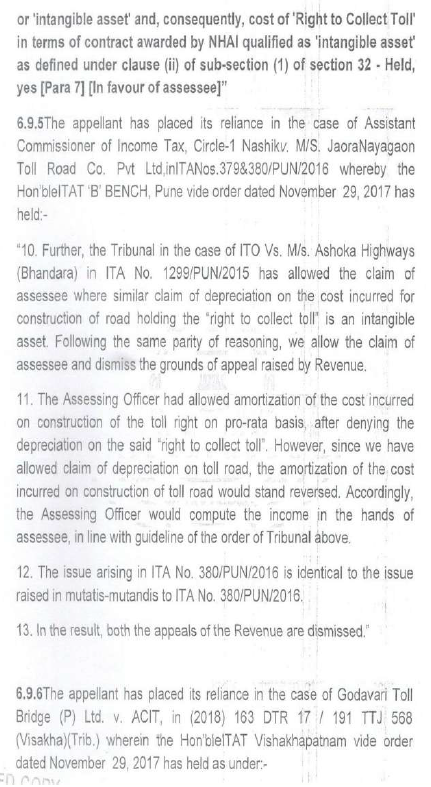

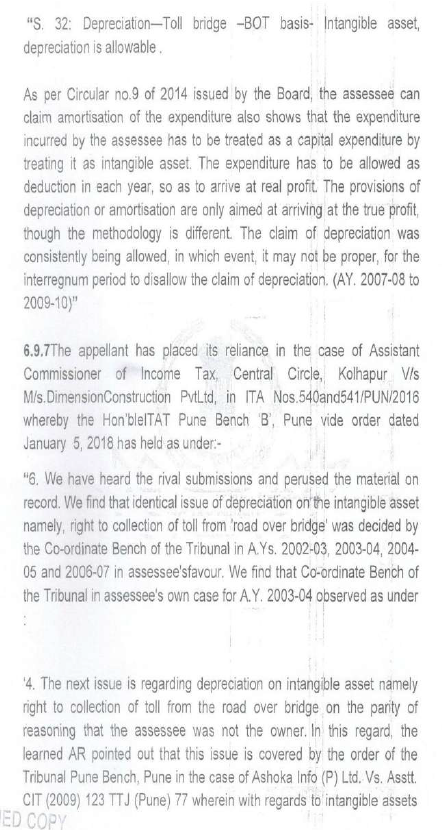

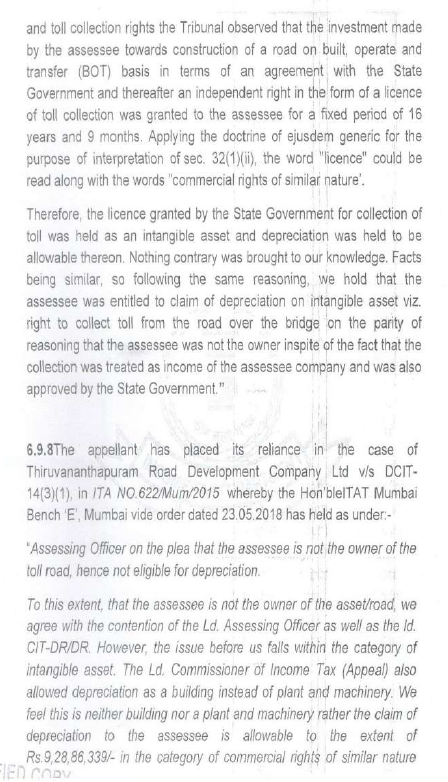

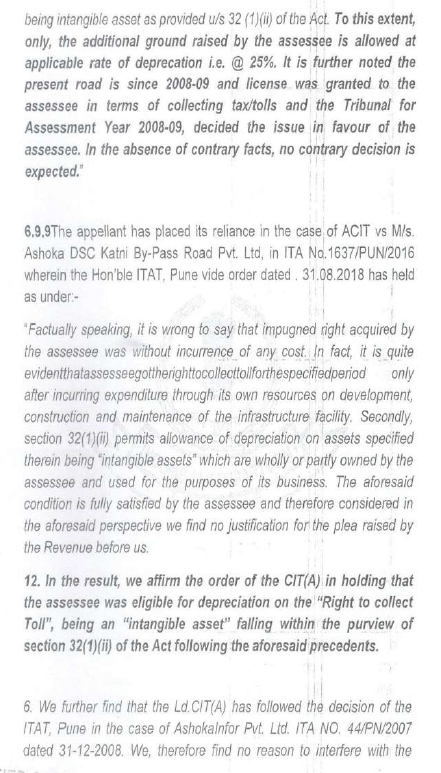

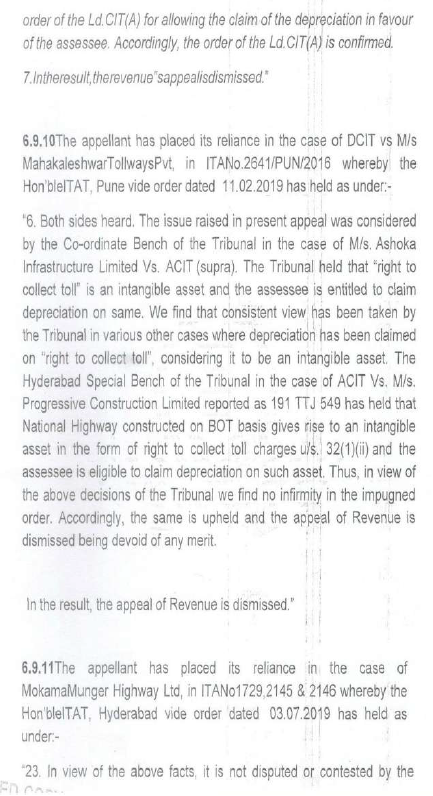

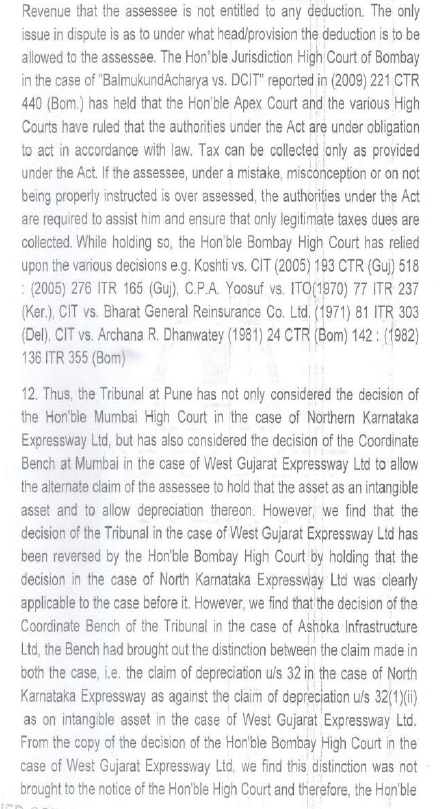

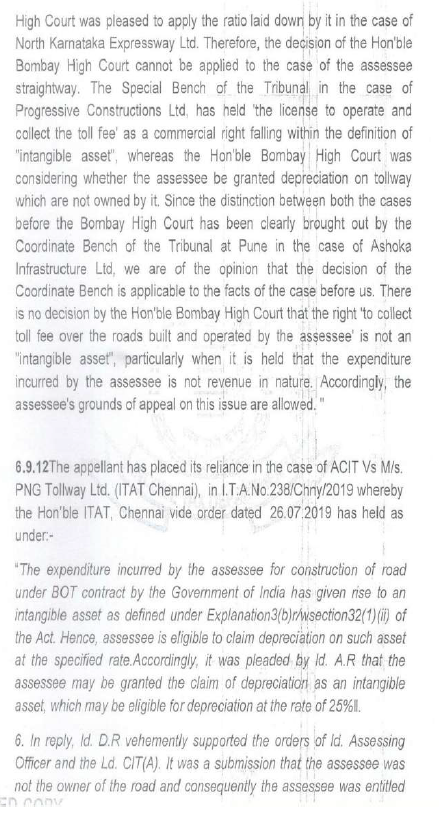

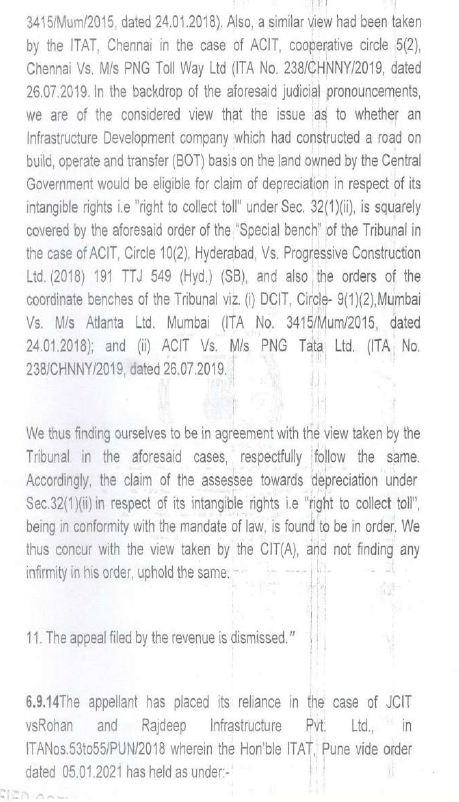

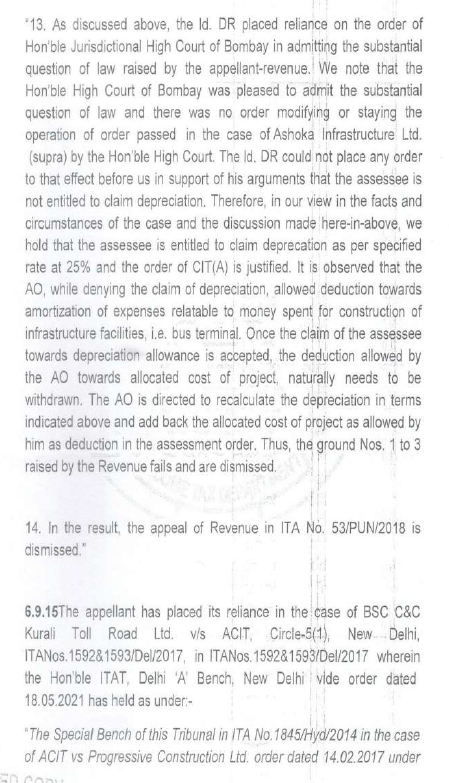

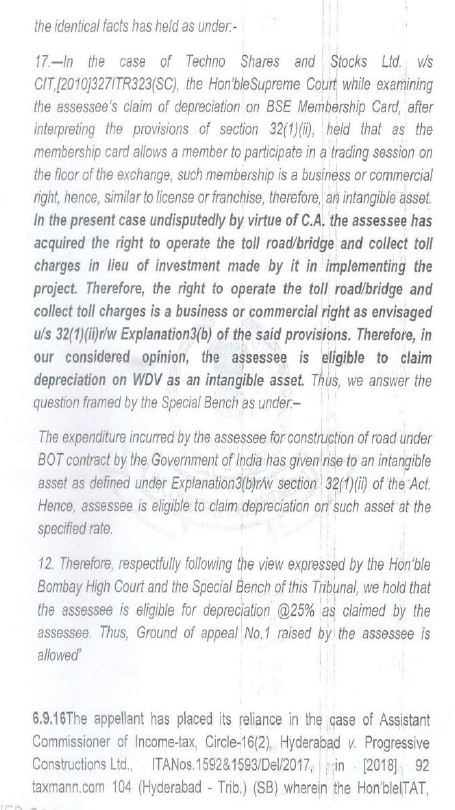

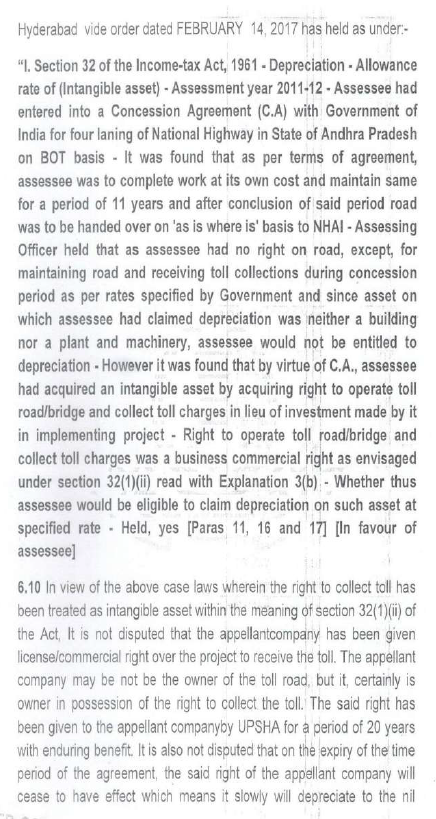

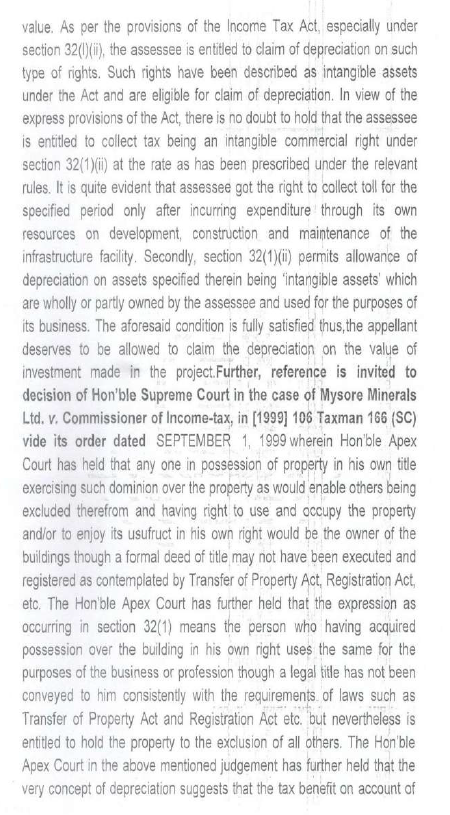

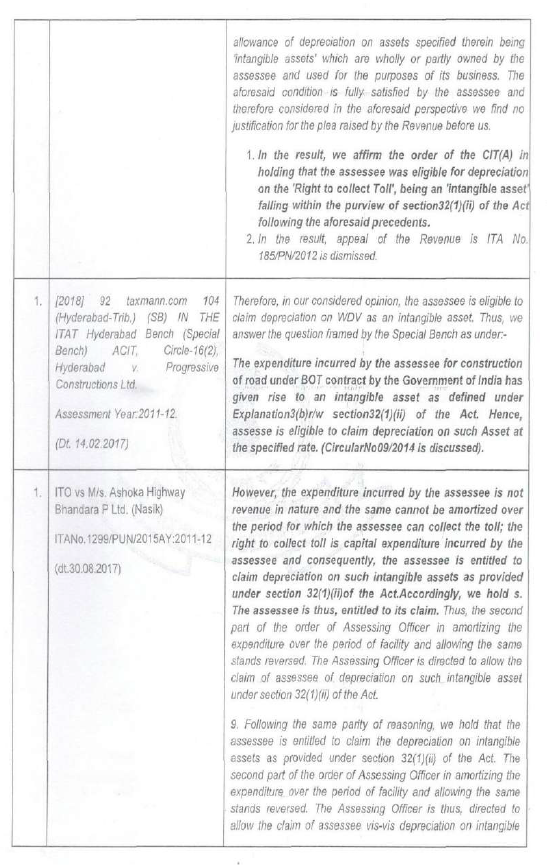

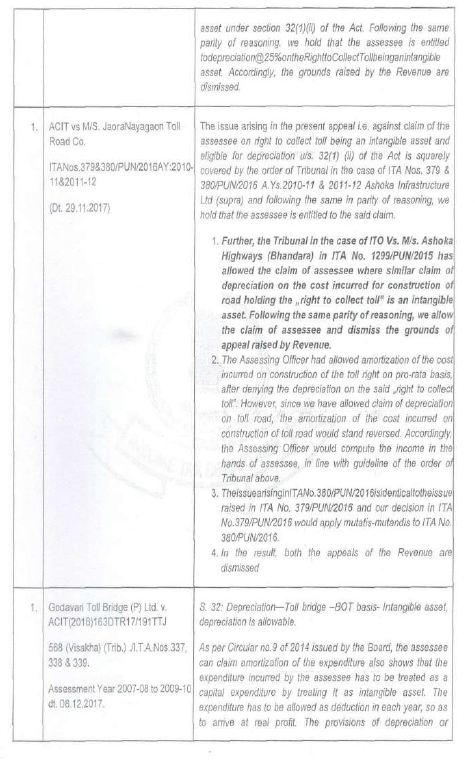

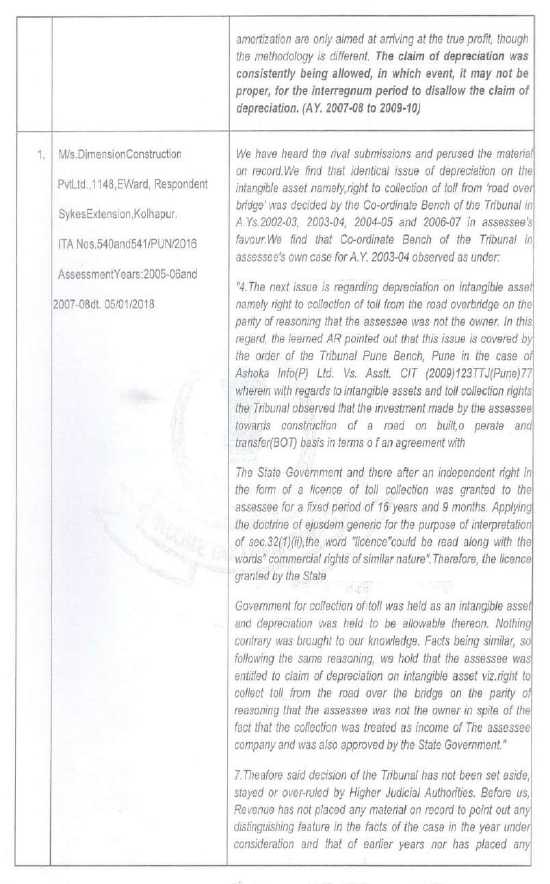

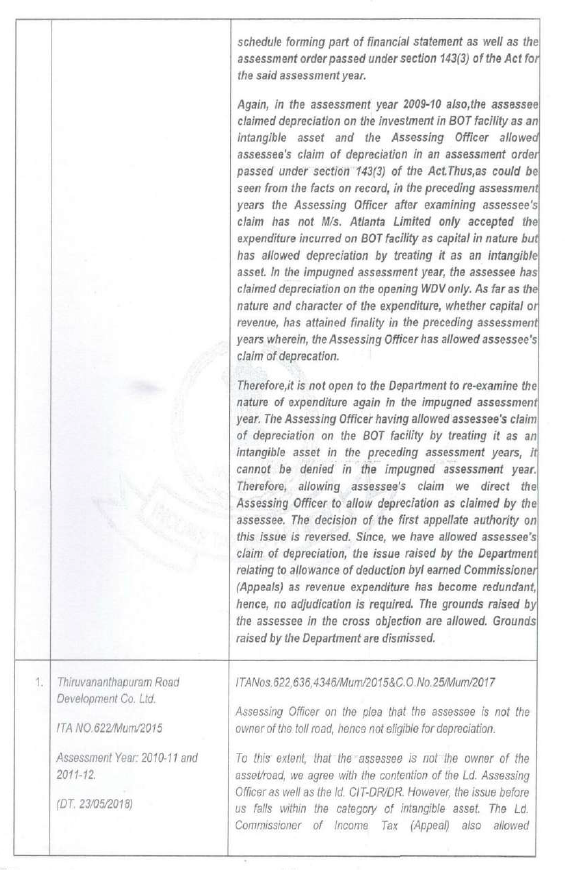

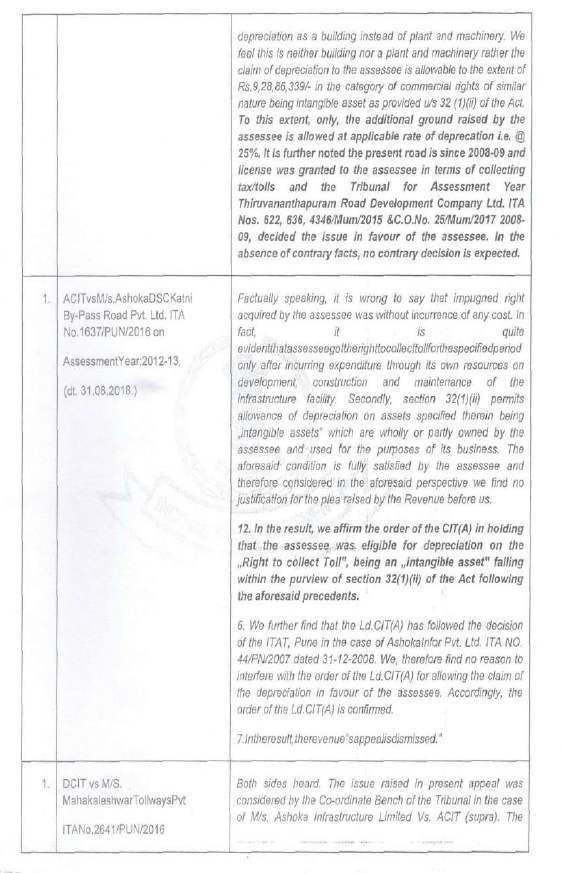

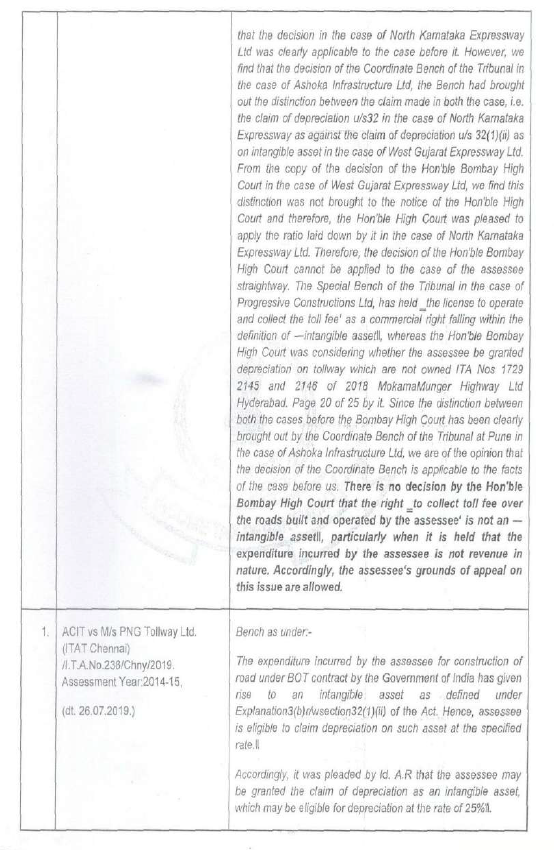

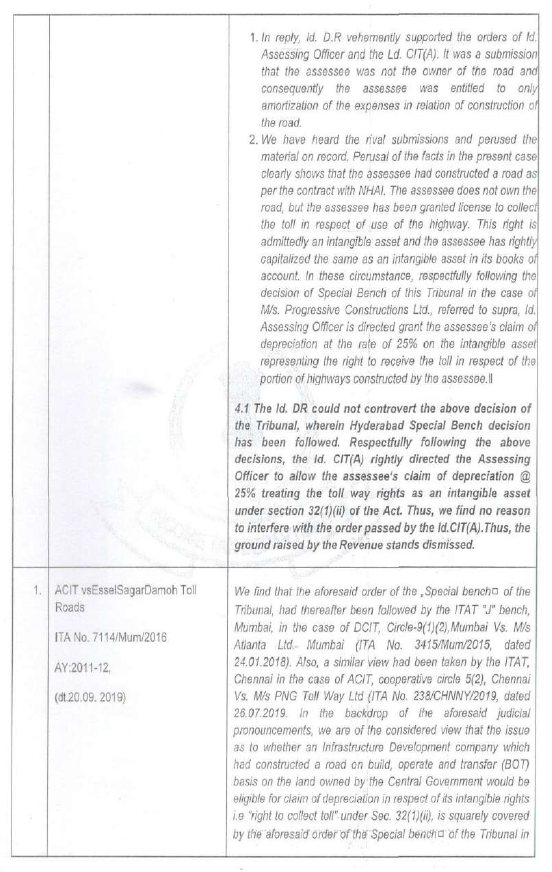

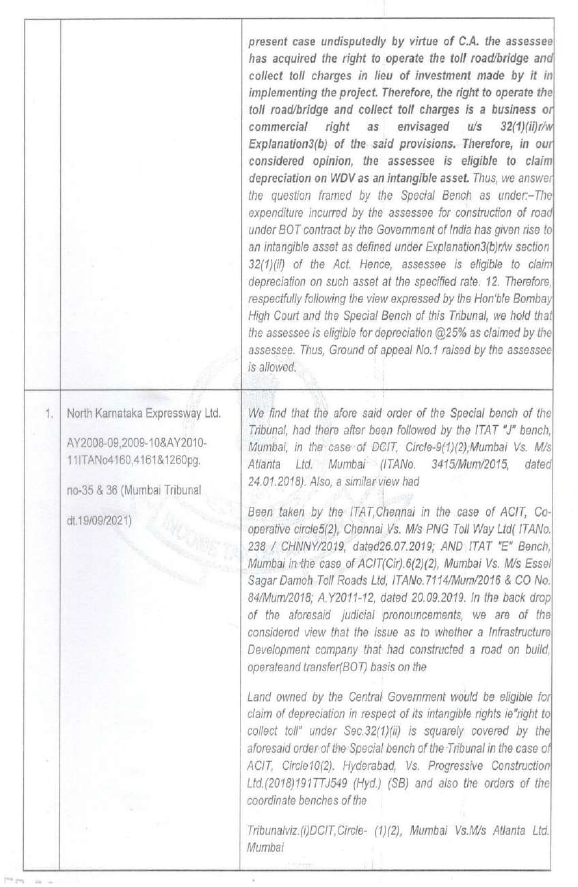

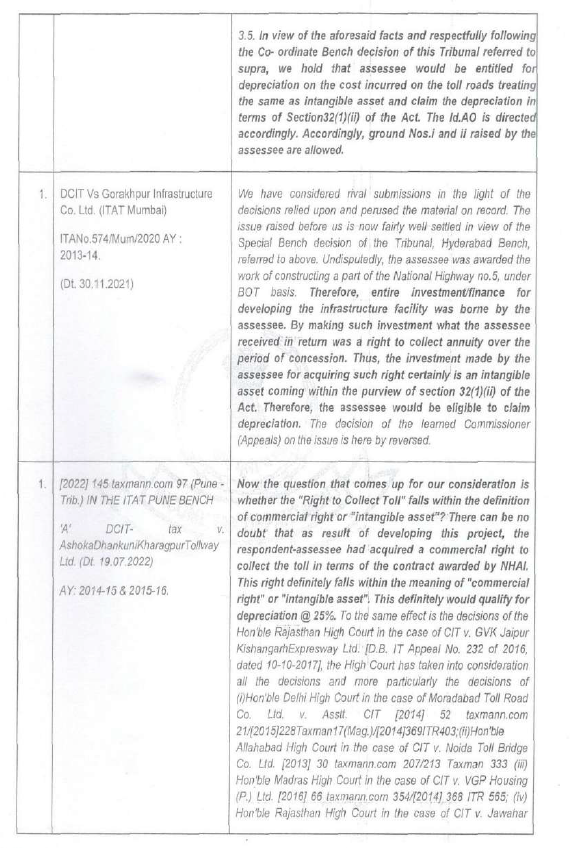

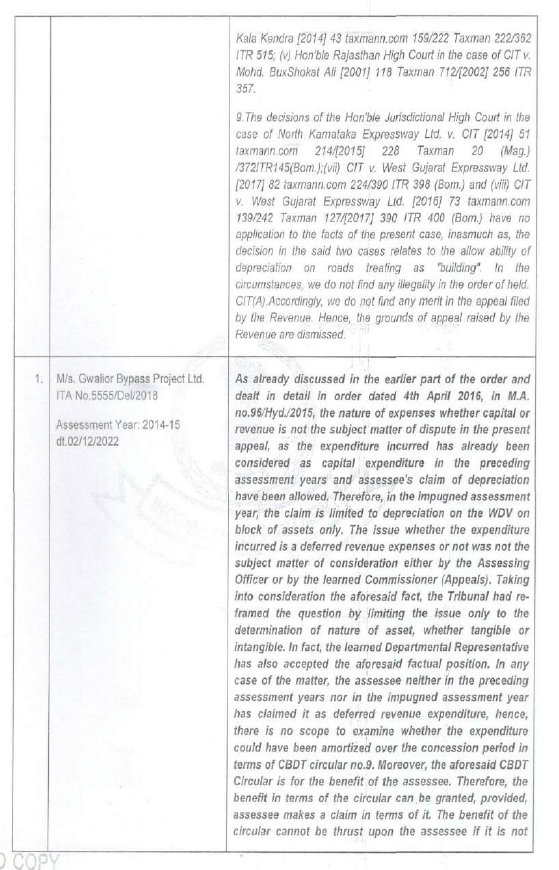

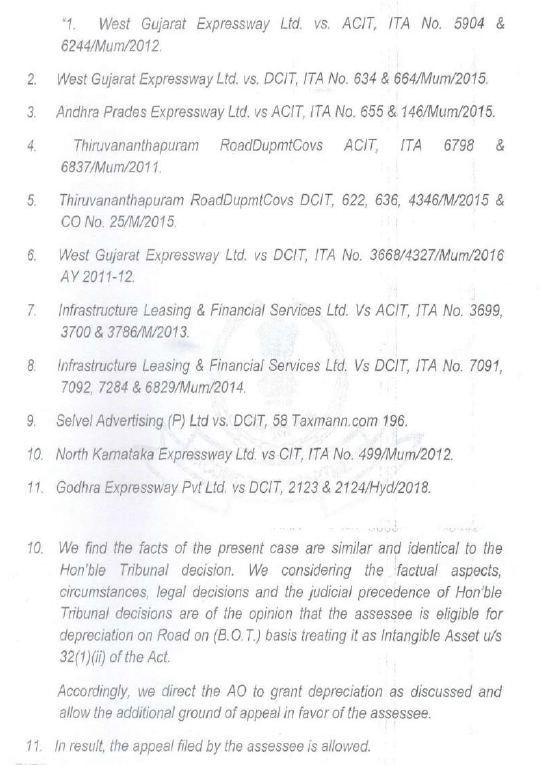

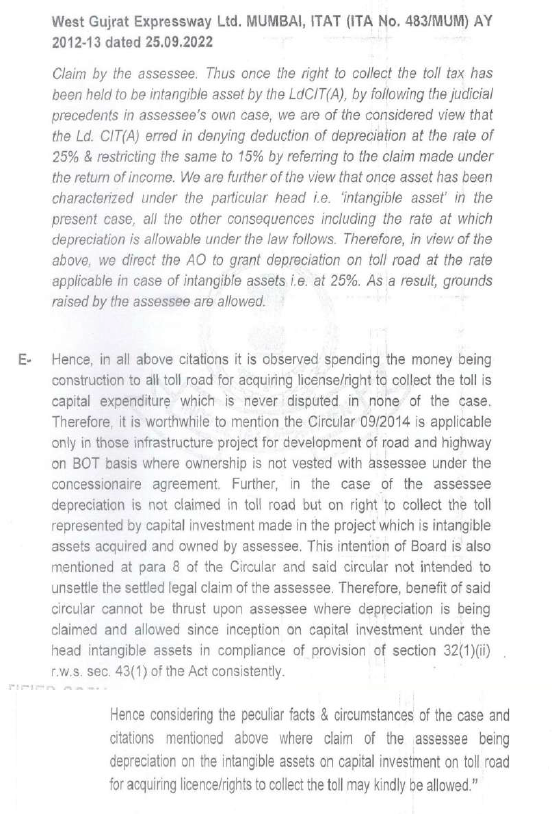

(E.2) The claim of the assessee for depreciation and the order of the learned CIT(A) directing the Assessing Officer to allow depreciation is supported by numerous precedents which have been referred to by the learned CIT(A) in the impugned appellate order 18/01/2024, contained in pages 48 to 69 of the impugned order of the learned CIT(A) and are reproduced below for the ease of reference:

(E.3) However, the Assessing Officer has failed to cite even one precedent in support of the view taken by him. Moreover, in the written submissions (referred to in foregoing paragraph (C) of this order, the learned D.R. has cited precedents, which are clearly distinguishable on facts. In the case of Patna Bakhtiyarpur Tollway Ltd. v. ACIT (Hyderabad – Trib.) on which the learned D.R. has placed reliance, the assets belonged to NHAI and not to the assessee. However, in the present case before us, as discussed in foregoing paragraph (E.1) of this order, the deemed ownership and acquisition coupled with possession of the asset is with the assessee. Further in the case of North Karnataka Expressway Ltd. (supra) and in the case of L&T Infrastructure Development Projects Ltd. (supra), on which the learned D.R. has placed reliance, the project was of BOT nature whereas in the present case before us, the contract is of DBFOT nature having much wider scope than BOT. As noted in foregoing paragraph (E) of this order, the scope of DBFOT contract, in as much as it also includes Design and Finance, is much wider than BOT contract. Moreover, as noted in foregoing paragraph (B) of this order, the project is deemed to be acquired and owned by the assessee. Further, as noted in paragraph (E.1) of this order, possession of the project by the assessee is also established. In view of these distinguishable facts and circumstances, we are of the opinion that the precedents relied upon by the learned D.R. in his written submissions have no application or relevance for the case before us. What the Assessing Officer has failed to appreciate, is that the asset on which the assessee has claimed depreciation, is “Right to Collect Toll”, which is an intangible asset. By necessary implication, it is impossible for intangible asset to be “physically owned” in the sense in which the Assessing Officer expects. When the assessee has deemed ownership of physical assets corresponding to the ‘intangible asset’ as is the case here; it meets the requirement for eligibility for depreciation, as far as requirement of ownership is concerned. It is a settled position of law; that law does not require one to perform the impossible. In situations like this, which we faced with law is to be interpreted in a manner that reasonable compliance is to be treated as adequate. What strengthens the case of the assessee, is that in addition to deemed ownership, the assessee also has acquisition and physical possession of the physical assets corresponding to the intangible asset (Right to Collect Toll). Thus, the assessee meets the requirement of law for claim of depreciation. In view of the foregoing discussion, therefore, we hold that the claim of the assessee for depreciation, while foregoing amortization, is in accordance with law in the facts and circumstances of the present case before us. Therefore, we decline to interfere with the impugned order of learned CIT(A) on this issue and accordingly, the grounds taken in appeal filed by Revenue are hereby dismissed. In effect, appeal filed by Revenue is dismissed.

(F) Since we have already dismissed the appeal filed by Revenue, the ground no. 1 taken by the assessee in its Cross Objection is rendered merely academic, hence not decided. For statistical purposes, this ground is treated as partly allowed.

(F.1) Ground no. 2 taken by the assessee in its Cross Objection is treated as allowed in view of our decision to dismiss the appeal filed by Revenue.

(F.2) As regards ground no. 3 taken by assessee in its Cross Objection, the Assessing Officer is directed to verify the records of earlier years and allow the brought forward business loss and unabsorbed depreciation in accordance with law after providing reasonable opportunity to the assessee. For statistical purposes, this ground is partly allowed.

(G) In the result, the appeal filed by Revenue is dismissed and the Cross Objection filed by the assessee is partly allowed.