JUDGMENT

Prathiba M. Singh, J.- This hearing has been done through hybrid mode.

CM APPLs.75278/2025 & 75279/2025 (for exemption)

2. Allowed, subject to all just exceptions. Applications are disposed of.

W.P.(C) 18204/2025 & CM APPL. 75277/2025 (for stay)

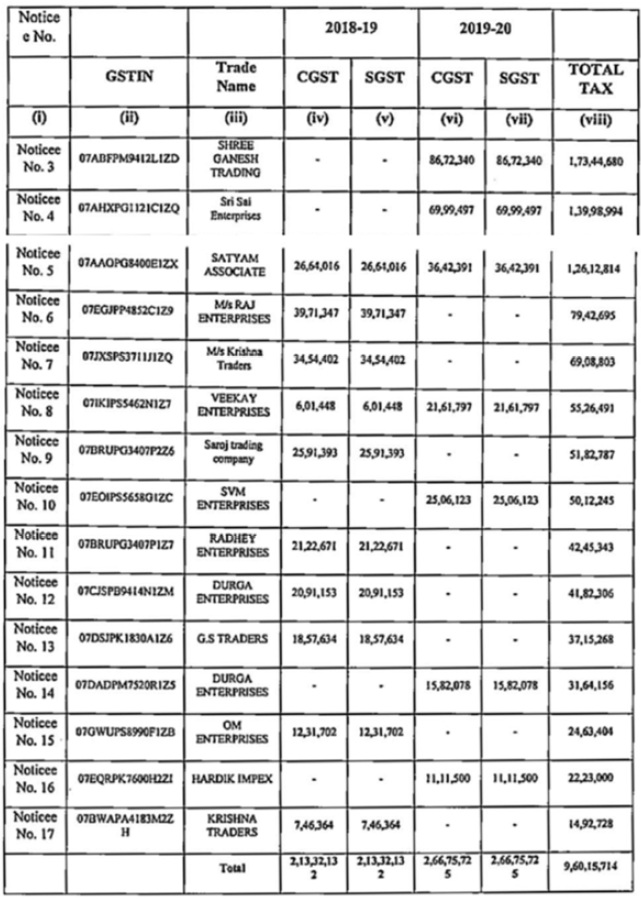

3. The present petition, inter alia, raises a challenge to the Order-in-Original dated 22nd October, 2025 by which a demand to the tune of Rs.9,60,15,714/- crores has been confirmed against the Petitioner in respect of fake ITC, which is passed on/availed by the Petitioner.

4. There are various allegations in the petition against one Mr. Parag Garg who is stated to be the master mind of the operation and involved in incorporation of several firms and non-existent entities only to avail/pass on the Input Tax Credits (hereinafter “ITC”). Shri Parag Garg, who is the partner of the Petitioner firm, has in fact filed the present petition as well.

5. The Petitioner was engaged in the business of readymade garments and leather goods at Kirti Nagar, Delhi, which is stated to be still a running business. As per the impugned Order-in-Original, searches were conducted at various premises related to Mr. Parag Garg who is also a partner in various other firms with the same addresses.

6. The Order-in-Original sets out the factual background and the manner in which ITC was availed/passed on to various entities. The total demand raised in the impugned Order-in-Original against the Petitioner and other entities is as under:

“Order

(i) I confirm the demand of ITC availed/utilized in excess, amounting to CGST=”Rs.4,80,07,857/-and” SGST=”Rs.” 4,80,07,857/-collectively Rs. 9,60,15,714/-(Rupees Nine Crore Sixty Lakhs Fifteen Thousand Seven Hundred and Fourteen Only) and I hold it recoverable from the Noticee No. 1 under Section 74(1) of CGST Act, 2017 and corresponding provisions of SGST Act, 2017 read with Section 20 of IGST Act, 2017.

(ii) I confirm the demand and order for recovery of interest, from the Noticee No. 1, on the amount demanded above, under the provisions of Section 50 of the CGST Act, 2017 and SGST Act, 2017, read with relevant provisions of the IGST Act, 2017, from the due date till the date of actual payment.

(iii) I impose and order for recovery of penalty of CGST=”Rs.” 4,80,07,857/-and SGST =”Rs.” 4,80,07,857/-collectively Rs. 9,60,15,714/- (Rupees Nine Crore Sixty Lakhs Fifteen Thousand Seven Hundred and Fourteen Only), from the Noticee No. I, under Section 74(1) of the CGST Act, 2017 read with Section 122 of CGST Act, 2017, read with relevant provisions of the SGST Act 2017 and Section 20 of the IGST Act, 2017, for their various acts of omission and commission as discussed supra.

(iv) I refrain from imposing any another penalty on the Noticee No. 1 as Section 75 (13) of the CGST Act, 2017 clearly states that Where any penalty is imposed under section 73 or section 74 [or section 74A], no penalty for the same act or omission shall be imposed on the same person under any other provision of this Act.

(v) I order appropriation of Rs. 1,66,00,000/- paid vide DRC03 by the Noticee No. 1 during the investigation against the proposed demand.

(vi) I impose and order for recovery of penalty of CGST=”Rs.” 4,80,07,857/-and SGST =”Rs.” 4,80,07,857/-collectively Rs. 9,60,15,714/- (Rupees Nine Crore Sixty Lakhs Fifteen Thousand Seven Hundred and Fourteen Only), from the Noticee No. 2, under Section 122(1A) of the CGST Act, 2017, read with relevant provisions of the SGST Act 2017 and Section 20 of the IGST Act, 2017, for their various acts of omission and commission as discussed supra.

(vii) I impose and order for recovery of penalty equivalent to Rs. 50,000/- (CGST-Rs.25,000/- and SGST-Rs. 25,000/-) from the Noticee 2, under section 122(3)(a) of CGST Act, 2017, read with relevant provisions of the SGST Act 2017 and Section 20 of the IGST Act, 2017, for their various acts of omission and commission as discussed supra.

(viii) I impose and order for recovery of penalty equivalent to amount as mentioned in column no. viii in table below, from the Noticee 3 to 17, under section 122(1)(ii) of CGST Act, 2017, read with relevant provisions of the SGST Act 2017 and Section 20 of the IGST Act, 2017, for their various acts of omission and commission as discussed supra.

(ix) I impose and order for recovery of penalty equivalent to Rs. 50,000/- (CGST-Rs. 25,000/- and SGST-Rs. 25,000/-) from the Noticee 3 to 17, under section 125 of CGST Act, 2017, read with relevant provisions of the SGST Act 2017 and Section 20 of the IGST Act, 2017, for their various acts of omission and commission as discussed supra.

(x) I impose and order for recovery of penalty equivalent to Rs. 50,000/- (CGST —Rs. 25,000/- and SGST – Rs. 25,000/-) from the Noticee 3 to 17, under section 122(3)(a) of CGST Act, 2017, read with relevant provisions of the SGST Act 2017 and Section 20 of the IGST Act, 2017, for their various acts of omission and commission as discussed supra.

(xi) I impose and order for recovery of penalty equivalent to Rs. 50,000/- (CGST-Rs. 25,000/- and SGST-Rs. 25,000/-) from the Noticee 18, under section 122(3)(a) of CGST Act, 2017, read with relevant provisions of the SGST Act 2017 and Section 20 of the IGST Act, 2017, for their various acts of omission and commission as discussed supra.

(xii) The noticees are hereby informed that in terms of the Section 74(11) of the CGST Act, 2017 read with State GST Act, 2017, Where any person served with an order issued under sub-section (9) pays the tax along with interest payable thereon under section 50 and a penalty equivalent to fifty per cent of such tax within thirty days of communication of the order, all proceedings in respect of the said notice shall be deemed to be concluded.”

7. The submission of Mr. Chinmaya Seth, ld. Counsel appearing for Petitioner is that the present writ petition is well within the limitation for filing of the appeal. However, since there was no Pre-SCN Consultative Notice in terms of Rule 142 (1A) of the Goods and Services Tax Rules, 2017, the impugned Show Cause Notice dated 12th March, 2025 (hereinafter “impugned SCN”) and the impugned Order-in-Original are not tenable. It is his submission that this stand of the Petitioner was taken up even in the reply but the same has not been considered in the impugned Order-in-Original. He also raises a challenge to the constitutional validity of Notification No.79/2022-Central Tax dated 15th October, 2020 issued by the Central Board of Indirect Taxes and Customs, by which the provisions of Rule 142 (1A) of the 2017 Rules had undergone change and ‘SHALL’ was replaced with ‘MAY’.

8. On the other hand, Ms. Nancy Jain, ld. Counsel appearing for the Respondents submits that this is again a case of fraudulent availment of ITC, and this Court, has repeatedly held in such cases that a writ petition would not be maintainable. In support of the same, she relies upon the decision in Banson Enterprises v. Assistant Commissioner CGST (Delhi)/W.P.(C) 6503/2025 (order dated 15th May, 2025).

9. In addition, it is also submitted by her that in Zeta International v. Additional Director [W.P. (C) No. 17220 of 2025, dated 13-11-2025], the Coordinate Bench of this Court under similar circumstances, considering the challenge to Rule 142(1A) of the 2017 Rules, had noticed that in view of the amendment vide the Notification No. 79/2022-Central Tax, the pre-SCN consultation notice cannot be held to be mandatory in nature.

10. The Court has heard the parties. The amended Rule 142(1A) of 2017 Rules reads as under:

“(1A) The proper officer may before service of Notice to the person chargeable with tax, interest and penalty, under sub-section (1) of Section 73 or sub-section (1) of Section 74 or sub-section (1) of section 74, as the case may be, communicate the details of any tax, interest and penalty as ascertained by the said officer, in Part A of FORM GST DRC-01A.;”

11. The same came into effect on 15

th October, 2020. Prior to the said amendment, the provision, which existed, was ‘proper officer shall’. This issue has been squarely covered and considered in the decision in

Gulati Enterprises v.

Central Board of Indirect Taxes and Customs GSTL 237 (

Delhi)/W.P.(C) No. 5407/2020, wherein the Court held that since the SCN therein was prior to the amendment, the issuance of the pre-SCN consultation notice was mandatory. This judgement brought out the distinction pre-and post-amendment.

12. Further, in Banson Enterprises (supra), this very issue has been considered by this Court. It is noticed that after the change, which has been brought about, the issuance of pre-SCN consultation notice would not be mandatory. Moreover, in the case of such large scale fraudulent availment of ITC with multiple entities, pre-SCN consultation notice may also have no impact. In the prima facie opinion of the Court such a notice would be having some bearing, only when certain simple transactions are noted. In such complex maze of transactions involving multiple parties, worth crores of rupees, pre-consultation would be meaningless due to the nature of the issues involved. In fact even when searches etc. , are conducted, parties can always tender the illegally obtained amounts, but they do not do so usually.

13. In any event, the challenge to Notification No.79/2022-Central Tax is already pending before this Court and the SCN in this case has been issued on 12th March, 2025 i.e., after the coming into effect of the said notification. The Petitioner has also deposited a sum of Rs.1.66 crores during the course of investigation, which can also be adjusted towards the pre-deposit.

14. Under such circumstances, the Court is not inclined to entertain the present writ petition. Accordingly, the following directions are issued:

| (i) | | Insofar as the Petitioner is concerned, the limitation period has also yet not expired. Accordingly, the Petitioner is free to avail of its appellate remedy under Section 107 of the CGST Act. |

| (ii) | | Insofar as the challenge to the Notification No.79/2022-Central Tax is concerned, the decision in titled Zeta International (supra) would bind the further proceedings in the appeal and thereafter. |

15. Needless to add, the observations made herein would not have any bearing on merits.

16. The petition is disposed of in the above terms. All pending applications are also disposed of.