Validity of Section 37(1) Disallowance on Transactions Covered by Advance Pricing Agreements

Reference: Section 37(1) read with Section 92CC

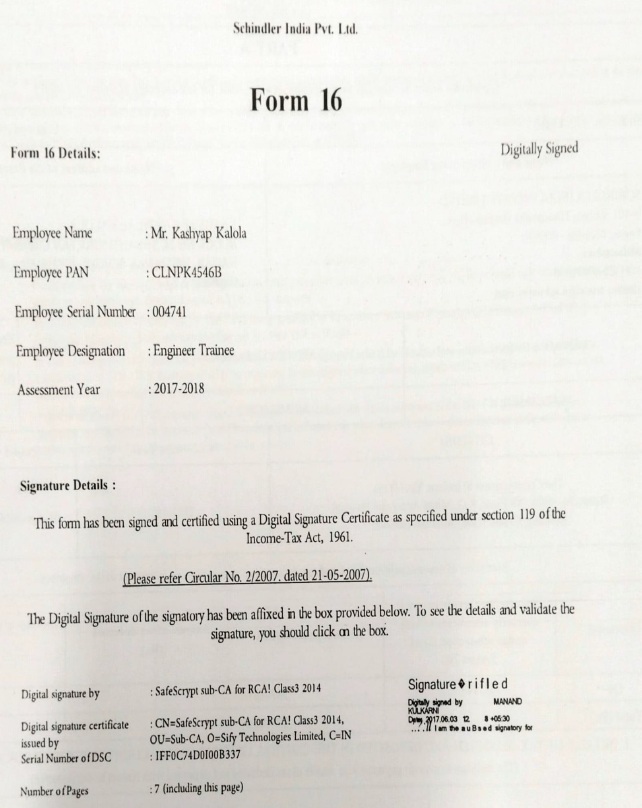

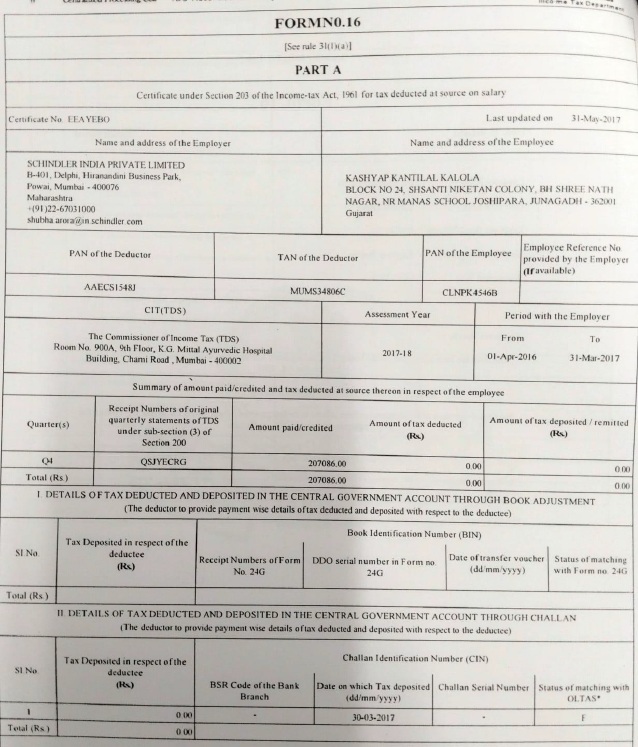

Assessment Year: 2017-18

Status: In Favor of Assessee

Legal Issue: Can the Revenue disallow intra-group payments under Section 37(1) if the same transactions are covered by a unilateral Advance Pricing Agreement (APA)?

Summary of Facts: The assessee paid royalty, management charges, and IT support fees to its Associated Enterprises (AEs). The TPO determined the Arm’s Length Price (ALP) at “Nil,” and the AO/DRP further disallowed the costs under Section 37(1) claiming the “benefit test” was not met. However, the assessee had already entered into a unilateral APA with the CBDT covering these specific transactions.

Final Holding: NO. The Court held that since the CBDT, while concluding the APA, had already examined the need, rendition, and benefit tests, as well as the cost allocation methodology, the AO cannot re-examine the commercial expediency under Section 37(1). The APA effectively validates the business nature of the expenditure.

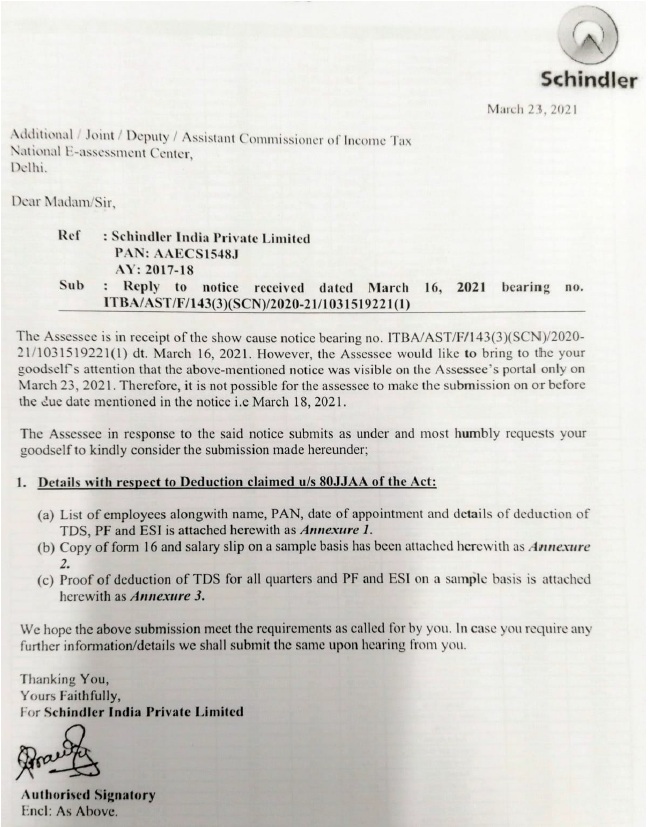

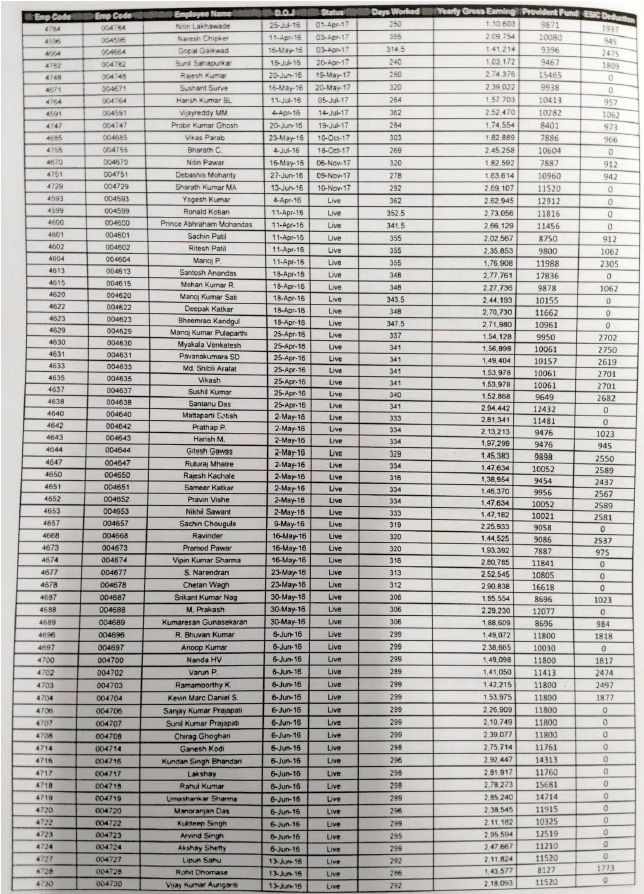

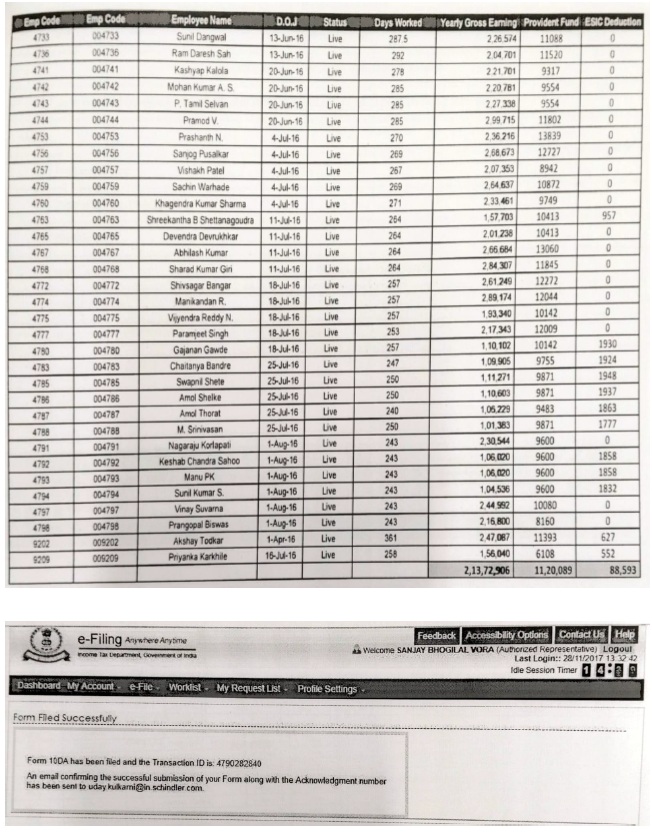

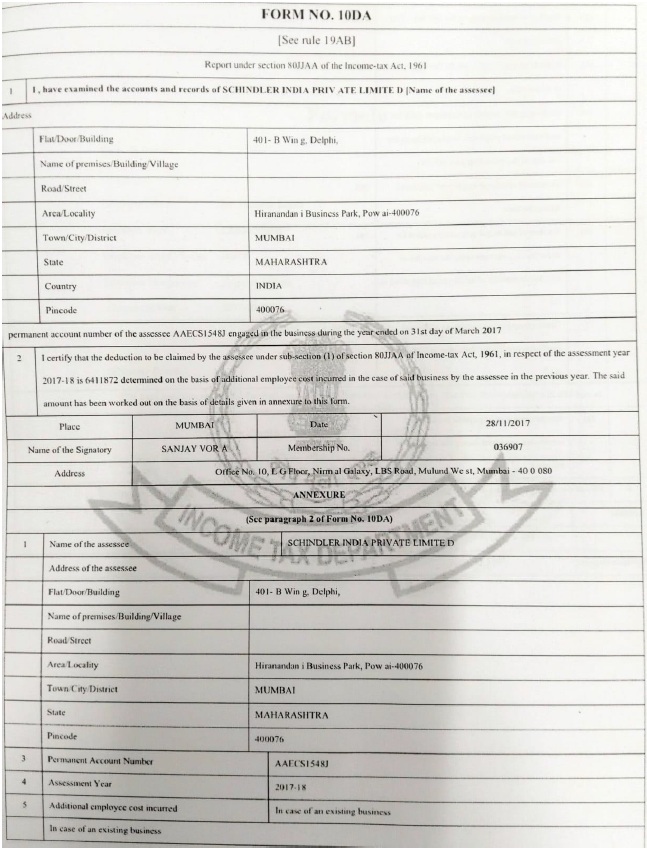

Sustainability of Section 80JJAA Deduction Based on Certified Accountant Reports and Form 10DA

Reference: Section 80JJAA read with Rule 19AB

Assessment Year: 2017-18

Status: In Favor of Assessee

Legal Issue: Can a deduction for new employment be disallowed if the assessee has submitted the prescribed Form No. 10DA?

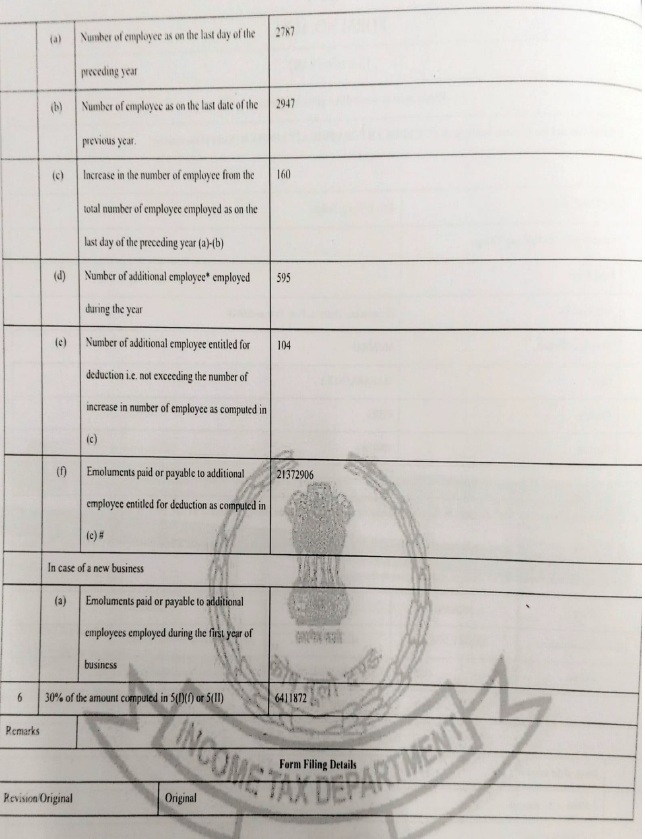

Summary of Facts: The assessee claimed a deduction under Section 80JJAA for the employment of new workmen. The AO disallowed the claim, asserting a lack of supporting documents. However, the assessee had filed the mandatory Accountant’s Report in Form No. 10DA along with the return and provided further details during the assessment.

Final Holding: YES (In favor of Assessee). The Court held that since the assessee had discharged its onus by providing the prescribed certification from an independent accountant and submitted the required data, the authorities were not justified in ignoring the evidence and disallowing the claim.

AND GIRISH AGRAWAL, ACCOUNTANT MEMBER

[ASSESSMENT YEAR 2017-18]

1. On the facts and in the circumstances of the case and in law, the learned AO/TPO erred and the Hon’ble DRP further erred in upholding/confirming the action of the learned AO/TPO in not stating any reasons to show that either of the conditions mentioned in clauses (a) to (d) of Section 92C(3) of the Act were satisfied before making an adjustment to the total income of the Appellant.

2. On the facts and circumstances of the case and in law, the transfer pricing order passed by the learned TPO under section 92CA(3) of the Act further considered by the learned AO and confirmed by the Hon’ble DRP is bad in law, illegal, unsustainable and ought to be deleted, as the learned AO/Id. TPO has not applied any of the methods for determination of arm’s length price as prescribed under section 92C of the Act, read with rule 100 of the rules being the most appropriate method.

3. On the facts and in the circumstances of the case and in law, the learned AO/TPO erred and the Hon’ble DRP further erred in upholding/confirming the action of the learned AO/TPO in determining the arm’s length price of the international transactions relating to Payment of License Fees / Royalty, payment of management recharge cost and payment of IT support and SAP systems recharge at NIL, without appreciating that as per the provisions of the Act, the Id. TPO’s role is merely to determine the arm’s length nature of the transactions referred to him by the Id. AO.

4. On the facts and in the circumstances of the case and in law, the learned AO/TPO erred and the Hon’ble DRP further erred in upholding/confirming the action of the learned AO/TPO whereby they have exceeded their jurisdiction in questioning the commercial expediency of the Appellant and in applying the need-evidence-benefit test in relation with the international transactions carried out by the Assessee the in determining the arm’s length price of the international transactions relating to Payment of License Fees/Royalty, payment of management recharge cost and payment of IT support and SAP systems recharge.

5. On the facts and in the circumstances of the case and in law, the learned AO/TPO erred and the Hon’ble DRP further erred in upholding/confirming the action of the learned AO/TPO in disallowing the aforesaid international transactions without disputing or pointing out any specific deficiency/errors in the benchmarking analysis conducted by the Appellant in accordance with the transfer pricing regulations.

6. On the facts and in the circumstances of the case and in law, the learned AO/TPO erred and the Hon’ble DRP further erred in upholding/confirming the action of the learned AO/TPO in issuing notices requiring the Assessee to show cause as to why the last year’s adjustments should not be made in the current year thereby failing to appreciate that the principle of res judicata is not applicable to the assessment proceedings.

7. Without prejudice to the above ground, in relation with the international transactions pertaining to payment for IT support and SAP System charges:

a. The Hon’ble DRP has erred in concluding that the facts in the current year are similar to the facts in earlier years without considering the observations of the learned TPO as captured in the remand report whereby the learned TPO has satisfied himself on the need-evidence-benefit test and cost allocation mechanism for the services availed.

b. Without prejudice to the above, on the facts and in the circumstances of the case and in law, learned AO/TPO erred and the Hon’ble DRP further erred in upholding/confirming the action of the learned AO/TPO in:

i. Making an adjustment to the total income of the Appellant, without disputing/rebutting or providing an explicit findings/observations on the voluminous / plethora of evidences filed by the Appellant in support of the claim that the aforesaid international transactions have been carried out at an arm’s length standard and to substantiate need, receipt and benefits arising from the aforesaid international transactions.

ii. Seeking documentation in relation with payment made by the AE to third party for which Assessee is not in privy to such documentation thereby causing undue hardships to the Assessee in resulting in assessment made by the Ld. AO / TPO to be arbitrary and unreasonable.

iii. Deviating and following different benchmarking approach vis-avis approach adopted in the Appellant’s own case in preceding assessment years (prior to AY 2016-17), wherein consistently, the said international transactions have been held to be at arm’s length.

8. Without prejudice to the above ground (Group 1), on the facts and in the circumstances of the case and in law, the learned AO/TPO erred and the Hon’ble DRP further erred in upholding/confirming the action of the learned AO/TPO in:

a. Disallowing the royalty payments made to the AEs without considering the business/commercial reality of the business of the Assessee.

b. Making an adjustment to the total income of the Appellant, without disputing / rebutting or providing an explicit findings/observations on the voluminous/plethora of evidences filed by the Appellant in support of the claim that the aforesaid international transactions have been carried out at an arm’s length standard and to substantiate need, receipt and benefits arising from the aforesaid international transactions.

c. Restricting the royalty payout by the applicant based upon several subjective presumptions, without taking due cognizance of the commercial / business rationale justifying the payment; documents demonstrating availing of technology/trade name/trade mark; and the benefit test documentation.

d. Rejecting the benchmarking analysis as undertaken by the Appellant merely for a reason the comparables selection are the foreign comparables which is based on the selection of tested party, However, the learned AO/TPO erred by not providing any reasons to reject the AE as the tested party

e. In concluding that the Appellant should not pay royalty as the IPs are used since inception of the company i.e. the IPs lose their value over the time and cannot be used for payment of royalty. The Ld. AO/TPO erred in disregarding the agreement submitted by the Assessee and concluding that the agreement is mostly for license of trademark and patents, which the Assessee has been using for last 16 years.

f. In concluding that payment of royalty is not warranted as the AEs has certain obligations towards the Assessee as shareholder activities.

g. In concluding that the payment of royalty is not warranted in case where the Assessee has appointed a Managing Director, two Directors, and a Company Secretary, without appreciating the facts that such key managerial persons are fundamental for operating and running a business for any entiy.

h. In concluding that there are consistent and increasing sales promotion expenses (in the form of commission and incentives) given by the Assessee and therefore the Assessee’s sales are continuously increasing due to its own efforts.

9. Without prejudice to the above ground (Group 1), on the facts and in the circumstances of the case and in law, the learned AO/TPO erred and the Hon’ble DRP further erred in upholding/confirming the action of the learned AO/TPO in:

a. Making an adjustment to the total income of the Appellant, without disputing / rebutting or providing an explicit findings/observation on the voluminous / plethora of evidences filed by the Appellant in support of the claim that the aforesaid international transactions have been carried out at an arm’s length standard and to substantiate need, receipt and benefits arising from the aforesaid international transactions.

b. Concluding that the allocation details in relation aforesaid transaction as submitted by the Assessee and further supported by certification from an independent consultant certifying the cost allocation methodology, as inappropriate without finding out any discrepancies in the allocation workings provided. The Learned AO/TPO erred in making an adjustment without considering the fact that the cost allocation methodology is uniformly and consistently followed by the Schindler Group for charging Management charges to all the group companies globally.

c. Seeking documentation in relation with payment made by the AE to third party for which Assessee is not in privy to such documentation thereby causing undue hardships to the Assessee in resulting in assessment made by the Ld. AO/TPO to be arbitrary and unreasonable.

d. In concluding that certain services are duplicative in nature/in nature of shareholder activities, merely on the basis of nomenclature of these services and ignoring the actual nature of services.

e. In concluding that the Assessee is incurring the sales promotion expenses (in form of Commission and Incentives) which indicates that its sales are continuously increasing due to its own efforts. Therefore, there is no requirement of availing the management services from SMAG.

10. On the facts and in the circumstance of the case and in law, the learned AO/TPO erred and the Hon’ble DRP further erred in confirming the action of the AO/TPO in ignoring the fact that there was no intention by the Appellant to shift profits outside India.

11. The Appellant submits that the above grounds are independent and without prejudice to one another.

12. The Appellant craves leave to add, alter, amend or withdraw all or any of the grounds of appeal herein above and to submit such statements, documents and papers as may be considered necessary either at or before the hearing of this appeal as per the law.

a. the payment made by the Appellant towards royalty, management recharge and IT support & SAP systems recharge services are wholly and exclusively for the purpose of its business;

b. the documents and evidence submitted by the Appellant clearly establish that the services are actually received by the Appellant;

c. the Appellant has derived various qualitative and quantitative benefits from the services so received,

d. the commercial expediency behind an expenditure is entirely the Appellant’s prerogative and cannot be questioned.

a. the Appellant claimed the deduction u/s 80JJAA towards additional employee cost after fulfilling the conditions and requirements provided in section 80JJAA,

b. the documents and evidence submitted by the Appellant along with Form 10DA clearly establish that the Appellant is eligible to claim deduction u/s 80JJAA,

c. the Appellant has provided details/documents/evidence as asked for during the assessment proceedings.

d. disallowance of deduction without providing reasonable adequate opportunity to be heard is violation of principle of natural justice

| Sr. No. | Nature of Service | Amount (Rs.) | TPO’s Contentions |

| 1 | Payment of Royalty | 52,38,81,571/- | Ld. TPO computed the Arm’s Length Price (ALP) for all 3 transactions as NIL by holding that rendition, need for such services and benefits received by the assessee were not demonstrated adequately. |

| 2 | Payment of information Technology (IT) support and SAP system charges | 29,28,69,883/- | |

| 3 | Payment of Management charges | 26,16,88,811/- | |

| Total | 107,84,40,265/- |

| • | hold meetings with the applicant on such time and date as it deems fit; |

| • | call for additional documents or information or material from the applicant; |

| • | visit the applicant’s business premises; and |

| • | make such inquiries as it deems fit in the circumstances of the case. |