Software License Renewal and AMC Fees Held Deductible as Revenue Expenditure u/s 37(1); No Creation of Capital Asset or Enduring Benefit

1. Core Dispute: Capital vs. Revenue Classification

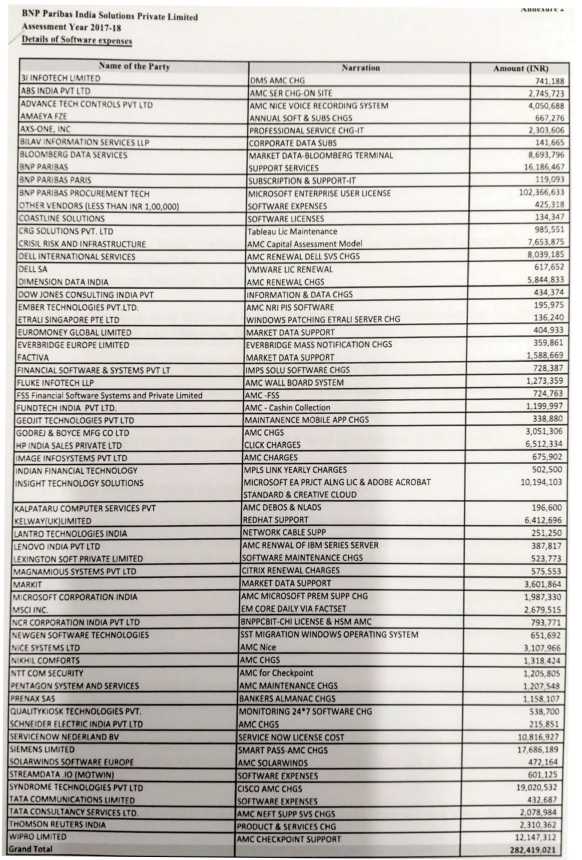

The assessee, a service provider, incurred various software-related costs including Annual Maintenance Charges (AMC), database support fees, and license renewal costs. The assessee claimed these as a business expense under Section 37(1).

-

Assessing Officer’s (AO) Stand: The AO disallowed the claim, arguing that the software provided an “enduring benefit” to the business and should therefore be treated as a capital expenditure (eligible for depreciation but not a 100% deduction).

-

Assessee’s Stand: The expenses were “period costs” (recurring annually) required to keep the existing business systems running. No new asset or ownership was created.

2. Legal Analysis: The “Enduring Benefit” and “Ownership” Tests

The Tribunal/Commissioner (Appeals) scrutinized the nature of the software spend by applying established judicial tests to determine if the cost was for “profit-earning apparatus” (Capital) or “facilitating trading operations” (Revenue).

I. No Creation of an Asset or IPR

The court observed that by paying renewal and maintenance fees, the assessee did not acquire any Intellectual Property Rights (IPR) or ownership of the software. The vendor remained the owner, and the assessee was merely a licensee.

-

The Ruling: Since no tangible or intangible asset came into existence, the expenditure cannot be capitalized.

II. The “Functional Test” & Period Cost

Software licenses for a fixed period (typically 12 months) are considered period costs.

-

Recurring Nature: These expenses are incurred periodically to maintain the efficiency of existing operations.

-

Facilitation: The software merely facilitates the conduct of business more profitably/efficiently without affecting the “profit-making functions” (the core capital base) of the business.

3. Final Verdict: Deduction Upheld

The ITAT concluded that the software expenses did not bring any enduring benefit or new capital asset into existence.

-

Verdict: Software expenses were held to be revenue expenses, deductible under Section 37(1).

-

Outcome: The AO’s disallowance was set aside, and the assessee was granted the full deduction.

Key Takeaways for Businesses

-

Subscription Models (SaaS): Modern SaaS renewals and annual license fees are classic examples of revenue expenditure. They provide “annual benefit” only and must be renewed to maintain access.

-

Application vs. System Software: While “system software” (like an OS) might sometimes be capitalized, “application software” and its maintenance/upgrades are generally treated as revenue expenditures by various High Courts.

-

Enduring Benefit is Not Absolute: Even if software lasts more than a year, it is not a capital asset if it only improves the efficiency of the existing business rather than creating a new line of business.

and Girish Agrawal, Accountant Member

[Assessment year 2017-18]

| a. | It is in the business of providing support services to its group entities. Software expenses incurred are in the nature of annual maintenance charges, fees for database support, license renewal cost, etc, which are necessary to carry on its regular business and are in furtherance of its business activities. |

| b. | The said software expenses are annual, recurring in nature, which are paid towards usage of software and do not create any asset or intellectual property. No ownership of the same is transferred to the assessee. Accordingly, software expenses are debited to its profit and loss account, being revenue expenditure in nature. The said treatment is also supported by commercial principles of accounting and in absence of any contrary provision under the Act, such commercial accounting treatment followed by the assessee in its books of account and as certified by the statutory auditor are uncontroverted. |

| c. | The said software expenses have a direct nexus with the business of the assessee and have been incurred wholly and exclusively for its business, allowable u/s. 37(1). |

| d. | Ld. AO erred in holding that the software expenses are capital in nature by relying on general proposition of law without having regard to the actual facts of the case and without appreciating the real nature of expenses incurred by the assessee. |

| i. | Asstt. CIT v. Matrix Publicities and Media India (P.) Ltd. (Mumbai – Trib.)/[2025] 213 ITD 463 (Mumbai – Trib.) |

| ii. | ACIT v. First Advantage (P.) Ltd. (Mumbai – Trib.) |

| iii. | Asstt. CIT v. Boots Piramal Health Care Ltd. (Mumbai) |

| iv. | Ratilal Becharlal & Sons v. Jt. CIT (Mumbai)/[2014] 148 ITD 628 (Mumbai) |

| v. | CGI Information Systems and Management Consultants (P.) Ltd. v. ITO (Karnataka)/[2023] 455 ITR 270 (Karnataka) |

| vi. | CIT v. G.E Capital Services Limited [IT Appeal No. 560 (Mum) of 2007, dated 10-07-2007] by Hon’ble High Court of Delhi |