ORDER

Vimal Kumar, Judicial Member. – The appeal filed by the Revenue is against order dated 25.08.2023 of Learned Commissioner of Income-Tax (Appeals)/National Faceless Appeal Centre (NFAC), Delhi (hereafter referred to as “Ld. CIT(A)”) under Section 250 of the Income-Tax Act,1961 (hereinafter referred to as “the Act”) arising out of assessment order dated 30.12.2018 under Section 143(3) of the Act by the Assistant Commissioner of Income Tax, Circle 53(1), Delhi (hereinafter referred to as “the AO”) for assessment year 2016-17.

2. Brief facts of case are that assessee having income from business and profession, house property, capital gains and other sources, filed return of income on 16.10.2016 declaring income of Rs.21,63,53,810. The return was processed under Section 143(1) of the Act. The case was selected for scrutiny assessment through CASS for limited scrutiny based on following reasons:

| 1. |

|

“Substantial increase in capital in a year”. |

| 2. |

|

“Large deduction claimed u/s. 54B, 54C, 54D, 54G, 54GA”. |

| 3. |

|

“Large long term capital gain”. |

3. Notice under Section 143(2) of the Act dated 22.06.2016 was served on assessee. Subsequently, notices under Section 142(1) dated 10.07.2018 and 06.09.2018 were served on assessee. In response to notices under Section 143(2) and 142(1) of the Act, Learned Authorised Representative of assessee made submissions through e-assessment module. On completion of assessment proceedings, Ld. AO vide order dated 30.12.2018 made addition of Rs.41,71,72,652/-. Against order dated 30.12.2018 of Ld. AO, assessee filed appeal before Ld. CIT(A) which was allowed vide order dated 25.08.2023.

4. Being aggrieved, the appellant/revenue preferred present appeal.

5. Learned Authorized Representative for the Revenue submitted that Ld.CIT(A) failed to consider that the addition of Rs.41,71,72,652/- on account of deduction under Section 54B of Rs.78,54,42,491/- as claimed by assessee minus unutilized amount of Rs.36,82,69.839/- in capital gain account on which tax is paid during assessment year 2018-19 claimed by the assessee on purchase of land does not fall within the ambit of section 54B of the Act ignoring the basic facts of the case. Ld. CIT(A) wrongly held that no evidence of film shooting etc. by Ld. AO was collected. The Inspector had visited the place without notice to the assessee.

6. Learned Authorized Representative for the assessee stated that the order passed by the Ld. AO is bad in law violating the provisions of section 142(3) of the Act and put his reliance on the following points:

“Ld. CIT(A)’s order, Inspector’s report and not confronted with the assessee violation of section 142(3);

ITAT orders vide ITA No.3523/Del/2013 dated 13.12.2013 in the case of M K Chabbra v. ITO No. 3523/Del/2013 and ITA No. 1026/Del/2016 dated 06.02.2018 in the case of Kamla Devi Sharma v/s ITO Jaipur.”

6.1 Reliance was placed on ITAT’s order in the case of ITO v. Babita Gupta (Delhi–Trib)/ITA 5313/Del/2019 as under:

“In this case assessee purchased agricultural land against GPA and agreement to sell such agreements are not allowed as per judgment of SC of Suraj Lamp and Industries. GPA and agreement to sell were allowable by CIT(A) and ITAT delhi for exemption u/s 54B in this case since the requirement of the said section is complied. The allow ability of section 54B has been accepted against GPA and agreement to sell but in my case the assessee has all the documents much more reliable in comparison to the one accepted in the above case”.

6.2 The assessee had submitted all relevant documents etc. in support of land transaction. Ld. CIT(A) has also accepted all relevant evidences after proper verification. He placed reliance on the decision of Hon’ble High Court of Madras in S. Sundaramurthy v. Pr. CIT (Madras)/W.P.No.26957 of 2019andW.M.P.Nos.26342, 26344 & 32232 of 2019. The contents of the said judgment are as follows:

“In this case, it is stated that after the sale, the petitioner has purchased agricultural lands within two years. However, the dispute in this case is not with regard to the second condition. On the other hand, the dispute is that the petitioner did not use the land for agricultural purposes two years immediately preceding the date on which the sale took place. Though, the Revisional Authority while rejecting the revision under Section 264, has stated so, perusal of the order passed by the Assessing Officer would show that he was carried over by the fact that the land was sold to a person, who is a developer and therefore, the petitioner is not entitled to benefit under Section 54B. Apart from saying so, the Assessing Officer has given a finding that the assessee could not show that there has been an agricultural activity. The first respondent has also reiterated the very same contention. On the other hand, it is stated by the petitioner that he has produced chitta, adangal etc., for the relevant period in support of his contention that the subject matter land were used for agricultural purposes two years immediately preceding the date on which the transfer took place.

Therefore, this Court is of the view that the factual aspects raised in this writ petition, need to be considered once again by the first respondent and to decide the matter as to whether the petitioner has satisfied the requirement contemplated under Section 54B, while seeking deduction. Certainly, the reason stated by the Assessing Officer that the purchaser is the builder and therefore, the land is not an agricultural land, cannot be a reason which is in consonance with the requirement made under Section 54B of the said Act. Therefore, it is for the first respondent to consider and decide the matter afresh”.

7. From examination of record, in light of aforesaid rival submission, it is crystal clear that vide order dated 30.12.2018, Ld. AO held deduction of Rs.41,71,72,652/- (deduction under Section 55B of the Act). “.I hold that the deduction of Rs.41,71,72,652/- [Deduction u/s. 54B of 78,54,42,491/- as claimed by assessee minus unutilized amount of Rs.36,82,69,839/- in Capital gains account on which tax is paid during A.Y. (18-19) claimed by the assessee on purchase of land doesn’t within the ambit of sec.54B of the income tax act, 1961. The same is brought to tax accordingly under Section 45 of the Income Tax Act, 1961.”

8. Ld. CIT(A) vide order dated 25.08.2023 held as under:

“Adjudication

Grounds 1 to 6:- The grounds of appeal are inter-related and are being adjudicated together. The facts of the appeal are that the appellant had sold his agricultural land in Village Asola, New Delhi on 07/12/2015 for a consideration of Rs 100 crores. The proceeds of the sale of this land resulted in capital gains of Rs 19,59,57,813/- after claiming deductions u/s 54B for Rs 78,54,42,491/- and 54EC for Rs 50,00,000/-

In net effect the appellant claimed deduction of Rs 41,71,72,652/- under section 54B after purchasing three properties from Ms. Latika Dutt, Ms. Charu Dutt and Sh. Mafresh Aggarwal. The Ld. Assessing Officer examined the claim of deduction u/s 54B of the appellant and found the same to be untenable.

According to the findings of the Ld. A.O. from the perusal of the ITRs, it was clear that very nominal agricultural income was being earned for the vast stretch of landholding. The DDA master plan though described the land as Agricultural, the master plan envisaged the same to be residential in near future and the appellant has purchased the land for these considerations. The Ld. A.O with the use of Google Pictures concluded that there were no signs of any agricultural activity on the property. The field inquiries from support staff and guards of the properties by the Inspectors of the A.O further revealed that marriage ceremonies and film shootings were being carried out at the farm houses purchased from Ms./s Latika Dutt and Charu Dutt whereas the property purchased from Sh. Mahesh Aggarwal was being used as a godown for business purposes and was sealed for violations. The A.O. recorded the statement of the assessee u/s 131 wherein it was stated by him that the lands were being used for agricultural purposes. In view of the findings, the Ld. A.O. disallowed the deduction of Rs 41,71,72,652/- to the appellant and added the same to his income vide order u/s 143(3) dated 31/12/2018.

During the appellate stage, additional evidence under Rule 46A was filed by the appellant before my predecessor on 21/08/2019. The appellant has submitted the following additional evidences to support his contentions:

1. Copy of order u/s 81 of Revenue Department sold during the year

2. Google Earth Pictures of the property sold during the year

3. Tube Well Sanction of the Property sold during the year under appeal

4. Khasra/Gidawari of Assessee after Purchase

5. Website snapshot of SDMC

6. SDMC approval of Dwelling Unit for Latika Dutt Property

7. Tube Well Sanction for Latika Dutt property

8. RTI reply regarding DDA Master Plan for Asola Village

The Ld. A.O replied to the evidences on 03/10/2019. The appellant replied to the rejoinder on 30/10/2019. The additional evidence was admitted by my predecessor on 08/11/2019 stating that the Inspector’s Report and Google images were not confronted to the appellant. A final report to CIT(A) was submitted by the A.O on 10/01/2020 in this respect. The Ld. A.O preferred to reiterate the findings of the assessment order.

The sole question for determination is whether the assessee is entitled to relief under Section 54B of the Act or not. Sub-section (1) of Section 54B of the Act, which is relevant for our purposes, reads as under:-

Capital gain on transfer of land used for agricultural purposes not to be charged in certain cases.-

(1) Subject to the provisions of Sub-section (2), where the capital gain arises from the transfer of a capital asset being land which, in the two years immediately preceding the date on which the transfer took place, was being used by the assessee or a parent of his for agricultural purposes (hereinafter referred to as the original asset), and the assessee has, within a period of two years after that date, purchased any other land for being used for agricultural purposes, then, instead of the capital gain being charged to income-tax as income of the previous year in which the transfer took place, it shall be dealt with in accordance with the following provisions of this section, that is to say,-

(i) if the amount of the capital gain is greater than the cost of the land so purchased (hereinafter referred to as the new asset), the difference between the amount of the capital gain and the cost of the new asset shall be charged under Section 45 as the income of the previous year; and for the purpose of computing in respect of the new asset any capital gain arising from its transfer within a period of three years of the purchase, the cost shall be nil; or

(ii) if the amount of the capital gain is equal to or less than the cost of the new asset, the capital gain shall not be charged under Section 45; and for the purpose of computing in respect of the new asset any capital gain arising from its transfer within a period of three years of its purchase, the cost shall be reduced, by the amount of the capital gain.”

From a plain reading of the above, It is clear that to claim the benefit of this provision, the following conditions are required to be satisfied:-

(i) the capital gain arises from the transfer of land which, in the two years immediately preceding the date on which the transfer took place, was being used by the assessee or his parent for agricultural purposes; and

(ii) the assessee has purchased the land within a period of two years after the sale of the above land for being used for agricultural purposes.

The Ld. A.O has disputed the use of the land for agricultural_purposes and hence disallowed the deduction u/s 54B. It is important to mention that land classifications in Delhi are done by DDA as per its master plan. The three lands under consideration have been classified as Agricultural by the DDA in its master plan. The same is mentioned in the respective Sale Deeds as Agricultural Land. Further land records of the Delhi Govt such as Khasra/Gidawari as submitted show that cultivation/agricultural activity has been taking place on these land properties. The appellant has also an order of DM, South Delhi dated 07/09/2015 settling the dispute between Gram Sabha, Asola and Latika Dutt wherein it has been ordered by Govt Authority that the land in question is being used for agriculture purposes and there is no violation of section 81 of Delhi Land Reform Act, 1954. The appellant has also submitted the tube well plans as well as the sale bills of agriculture bills to buttress his contentions. The electricity bills submitted at the time of appellate proceedings also show the capital asset to be Agricultural Land. Even the Income tax Returns of Department also show that the assessee had declared agricultural income from this land in his returns of the preceding two years.

In view of the above, it is evident that the assessee had claimed the deduction u/s 54B in a bona fide manner and that all the conditions thereof were fulfilled.

It is important to mention the decision of Hon’ble ITAT, Delhi in the matter of Income tax Officer v. Babita Gupta 100 ITR(T) 252 (Delhi Trib.) wherein it has been inter alia stated that:-

“Where assessee claimed capital gains arising on sale of an agriculture land as exempted under section 54B on purchase of another agriculture land, since assessee had furnished all sales documents viz. agreement to sell & purchase, receipt, possession letter, GPA and affidavit, along with copy of returri filed by land owner, from whom new land was purchased wherein she had declared capital gains arising from sale of its land to assessee, benefit of exemption u/s 548 was allowable.”

The facts of this case to this extent match with those of the appellant.

The Ld. A.O has contended that the lands purchased from Latika Dutt, Charu Dutt were being used for non-agricultural purposes. It is pertinent to mention that at the best the evidence collected through any inquiry has to be confronted to the assessee which were not done. Further, ample evidences have been adduced by the appellant under Rule 46A to prove that the lands purchased are agricultural. The A.O has not controverted the evidence hence adduced.

It is also important to mention that judicial precedents have held that once the requirements under section 54B are satisfied, the deduction cannot be denied.

The Hon’ble High Court of Madras in S. Sundaramurthy v. Principal Commissioner of Income-tax, Chennai reported in (Madras) has held as under-

“Where the A.O rejected assessee’s claim for deduction under section 54B in respect of capital gain arising from sale of agricultural land on ground that purchaser of land was a builder and thus, sald piece of land was not agricultural land, since view taken by Assessing Officer while rejecting assessee’s claim was not in consonance with requirements made under section 54B, Impugned order passed by him was to be set aside.”

Hence, once conditions for section 54B are satisfied, the other contentions like land being utilized for non-agricultural purposes are totally irrelevant considerations.

In view of the facts and circumstances narrated above, the appellant is eligible for deduction u/s 54B. The disallowance made by the A.O is hereby deleted.

Ground Nos 1 to 6 are hereby allowed.

Grounds nos 7 & 8

Since, ample opportunity has bee opportunity has been granted to the appellant, the grounds raised in Ground No 7 and 8 are herewith addressed. Hence, this ground stands allowed.

Ground no 9

The issue of levy of penalty is premature and does not require adjudication. Ground No 10 Is general in nature and does not require any adjudication.

Additional Ground

The appellant has also taken an additional ground vide submission dated 13/08/2023. I have perused the documents and the grounds thereof. To meet the ends of justice, the additional ground is hereby allowed taking recourse to various judicial precedents including Kedarnath Jute Mfg. Co. Ltd. v. CIT (1971) 82 ITR 363 (SC), NTPC Ltd. v. CIT (1998) 229 ITR 383 (SC) and Pruthvi Brokers and Share holders (2012) 349 ITR 336 (BOM).

The appellant vide the additional ground has contended that the A.O has not rectified a mistake committed at the time of filing of the ITR amounting to Rs 59.67 lakhs, the same being not considered at the time of passing of the assessment order. It is held that the Ld. A.O. could not have granted the relief to the assessee as the same could have only have been claimed vide a revised return which was not filed.

To support his contention, the appellant has claimed that in ITR has claimed Indexed Cost at Rs 13,177,336/- which should have been Rs 19,164,284/-. The appellant has filed purchase deeds for F.Y 1988-89 and 1993-94 vide his submissions before the Ld. A.O. It has been contended by the appellant that the sale of property in the F.Y. 1993-94 was out of exchange and not a financial sale finance the cost of the said property is equal to indexed cost of the F.Y. 1993-94. A detailed working of the actual calculation of indexed cost thereof has also been provided by the appellant vide his submissions. The appellant has stated the difference in indexed cost is due to a clerical error.

I find merits in the submissions of the appellant in view of the fact that relevant calculations have been submitted which can be corroborated from documents. The human error in these calculations by the appellant may not be ruled out.

In view of these observations, the Ld. A.O while giving the appeal effect may consider cost of index of the said property at Rs 19,164,284/- after due verification of records.

The additional ground of appeal is allowed for statistical purposes.

In the end, the appeal is Allowed.”

9. From perusal of finding of Ld. CIT(A) in light of grounds of appeal, it is apparent on record that Ld. AO disputed the use of land for agriculture purpose and disallowed deduction under Section 54B of the Act. Ld. AO had considered:

| (a) |

|

Sale deed pertaining to land sold by assessee and sale deeds of land purchased from Ms. Latika Dutt (pages 137 to 150 of the paper book), Ms. Charu Dutt (pages 151 – 169 of the paper books) and Mr. Mahesh Aggarwal (pages170-178 of the paper books); |

| (b) |

|

ITRs of assessee mentioning agricultural income; |

| (c) |

|

DDA land searched on public domain; and |

| (d) |

|

verification by team of inspectors. |

10. However, Ld. CIT(A) found that the three sale deeds of lands purchased by assessee mentioned as land agriculture. He further observed that the land purchased by assessee was classified agriculture by DDA in its Master Plan. As per RTI Replies, pages 202 & 203 of paper book Master Plan of DDA has not being notified. The DDA’s Master Plan is not in paper books. It is a material fact established on record that three sale deeds of the land purchased by the assessee from Ms. Latika Dutt, Ms. Charu Dutt and Mr. Mahesh Aggarwal mention the land as “agriculture land”. Land records of Delhi Government as such Khasra girdawari at page nos. 179 to 190 of paper books state land as agriculture under cultivation. Section 81 Order of Revenue Department in case of Ms. Latika Dutt at page nos. 191-193 of the paper book, mention land use for agriculture purposes. Assessee submitted, tube well plan, sale bills and bills of agriculture etc. Ld. CIT(A) accepted additional evidence page nos. 281 to 282 of paper books and asked the Ld. AO to verify which were not controverted. After considering the above facts, Ld. CIT(A) deleted the addition made by Ld. AO. The discussion, reasons and findings of Ld. CIT(A) are sustainable in law and liable to be upheld. The ground of appeal being de void of merit is untenable.

11. In the result, the appeal of Revenue is dismissed.

BRAJESH KUMAR SINGH, Accountant Member:- I am unable to persuade myself with the findings of learned Brother, regarding his decision in upholding the decision of the Ld. CIT(A) in allowing the deduction of Rs.41,71,72,652/- claimed u/s 54B of the Income Tax Act, 1961 (hereinafter referred as ‘the Act’) by the assessee and dismissing the appeal of the Revenue filed against the said deletion. The facts of the case are not in dispute as stated by my Ld. Brother. However, my findings differ from my Ld. Brother in view of the facts as discussed hereinafter.

2. The assessee is an individual having income from business and profession, house property, Capital Gains and other sources. The assessee filed his return of income on 16.10.2016 declaring income of Rs. 21,63,53,810/-. The return was processed u/s 143(1) of the Act. The case was selected for scrutiny through CASS for Limited Scrutiny based on the reasons:

| 1. |

|

Substantial increase in capital in a year” |

| 2. |

|

Large deduction claimed u/s. 54B, 54C, 54D, 54G, 54GA” |

| 3. |

|

Large long term capital gains”. |

3. During the assessment proceedings, on perusal of Income tax return and computation of income as submitted by the assessee on the ITBA Portal, the AO found that assessee had sold Agricultural land of area 37 Bighas 15 Biswas bearing Khasra No. 1893/623, 1892/623.624 Etc. in village Asola, New Delhi 110074 on 07/12/2015 for a value of Rs. 100 Crores to M/s Radha Soami Satsang Beas. The details/ computation as claimed by the assessee as per ITR for AY (1617) as noted by the AO are as follows:

| Total consideration |

100,00,00,000/- |

| Less expenses on sale of property |

4,22,360/- |

|

99,95,77,640/- |

| Less Indexed Cost |

1,31,77,336/- |

| Balance |

98,64,00,304/- |

| Deduction u/s. 54B |

78,54,42,491/- |

| Deduction u/s, 54EC 50,00,000/- |

79,04,42,491/- |

| Capital Gains. |

19,59,57,813/- |

3.1. Further, the AO noted that the assessee had purchased three properties as per details below for a sum of Rs.38,97,99,000/- and offered capital gains amounting to Rs.19,59,57,813/- for taxation as per the above computation.

| I. |

|

From Latika Dutt: Purchase of land property on 03/10/2016 from Latika Dutt of 12 Bigha 14 Biswa bearing Khasra Nos. 298/1 (7-0) 298 MIN (2-09), 1820/297 MIN EAST (2-11) and 1819/297 MIN WEST (0-14) in Asola Tehsil Saket, New Delhi 110074 for a consideration of Rs.25,26,74,000/- (excluding stamp duty and registration charges) on 03.10.2016. |

| II. |

|

From Charu Dutt: Purchase of land on 04/01/2017 from Charu Dutt amounting to Rs. 13,56,25,000/- (excluding stamp duty and registration charges) of 13 Bigha 5 Biswas bearing Khasra Nos. 1820/297 Min West(1-8),1819/297 MIN WEST (0-8), 261, 261, 263, 260, 259. 267 etc village Asola, New Delhi 110074. |

| III. |

|

From Mahesh Aggarwal: Purchase of land on 26/12/2016 from Mahesh Aggarwal amounting to Rs. 15 Lakh of 9 Biswas bearing Khasra No. 2004/1461 Etc. village Bhati, New Delhi 110074. |

3.2. Further, the AO on perusal of the IT return of the assessee observed that it cast a doubt about any substantial agricultural activities being carried out by the assessee on the above lands. The said observation of the AO in para-4 on page no.6 & 7 of the assessment order is reproduced as under:-

Perusal of the TR of the assessee : It has been observed from the ITs that assessee has been claiming a very nominal agricultural income for his vast stretch of landholding. A summary of the agricultural income declared over the years is as follows:

| AY |

Agricultural Income Declared (in Rs.) |

| 2011-12 |

277864 |

| 2012-13 |

287136 |

| 2013-14 |

50000 |

| 2014-15 |

50628 |

| 2015-16 |

25500 |

| 2016-17 |

15000 |

| 2017-18 |

328000 |

| 2018-19 |

443188 |

The observation cast a doubt about any substantial agricultural activities being carried out by the assessee on the above mentioned lands.

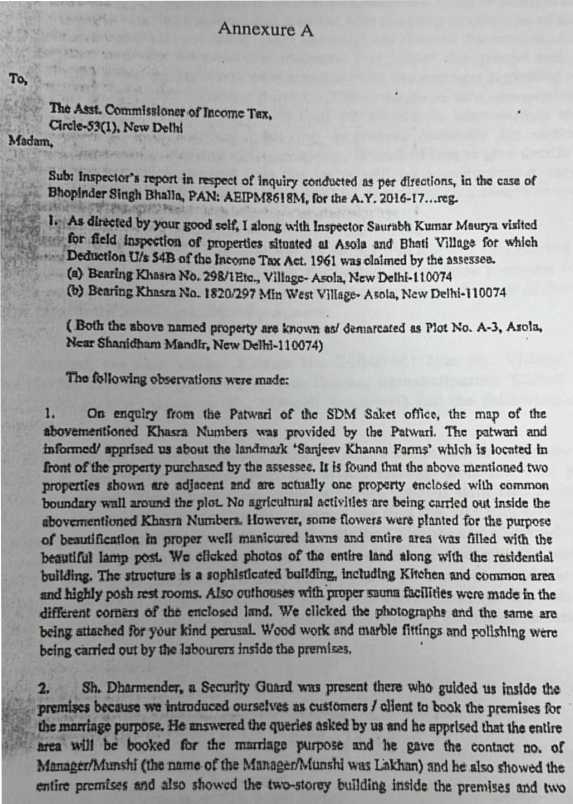

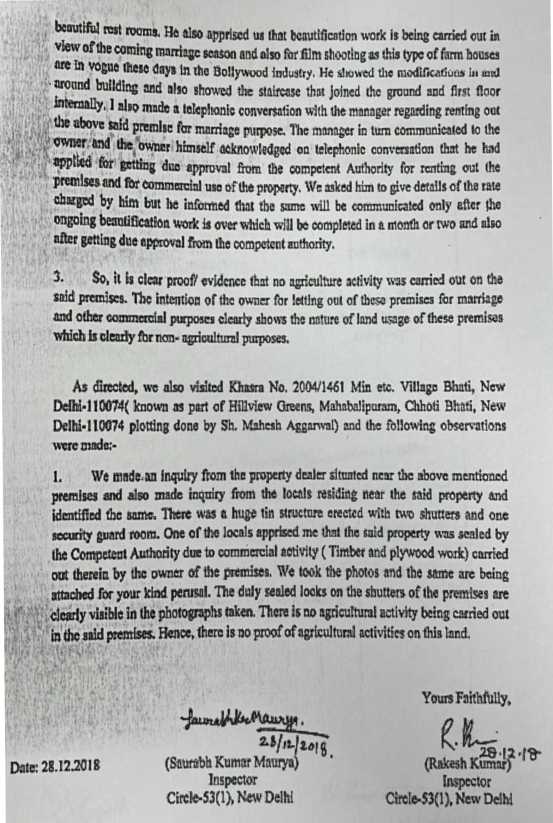

3.3. The AO thereafter conducted a field enquiry through her Inspectors, whose report dated 28.12.2018 has been made as part of the assessment order as per Annexure-A. On the basis of the said Inspectors’ report, the AO held that the property purchased from Ms. Charu Dutt and Ms. Latika Dutt was a farm house consisting of posh house with well manicured lawns, out houses and swimming pools and there was no trace of any agricultural activity on the said property. The AO also reproduced the picture of the house and of the premises taken by the Inspectors on page no.10 and 11 of the assessment order. Further, the AO noted on the basis of the Inspectors’ report that the property purchased from Shri Mahesh Aggarwal showed that buildings were constructed by the assessee on this site for commercial purposes. The AO relying upon the enquiry made by the Inspectors noted that the assessee had been using this site for his plywood and timber business as the assessee was a proprietor of M/s Hindustan Timber Store. The AO also noted that this site had been sealed by the competent authority on account of violations of laws. The AO also reproduced the picture of the site taken by the Inspectors on page-12 of the assessment order.

3.4. As stated above, the above findings of the AO were based upon the report of two inspectors dated 28.12.2018, who visited the above sites. The said report of the Inspectors forming part as Annexure-A of the assessment order is reproduced as under:-

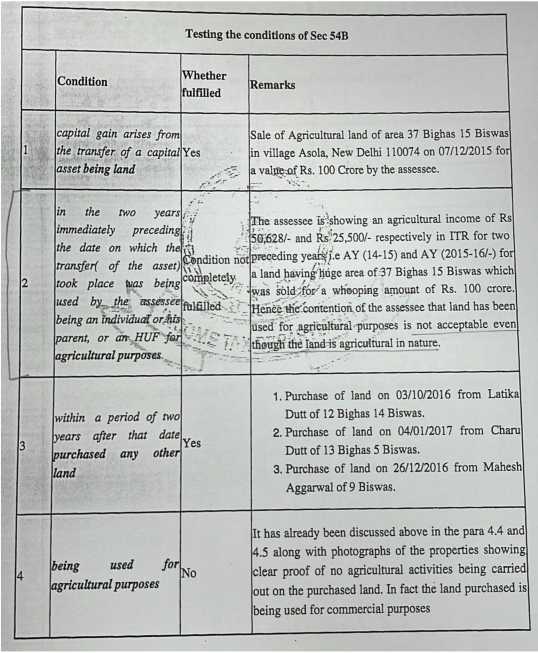

3.5. Thereafter, the AO prepared a tabular chart under the title ‘Testing the conditions of section 54B’, which is reproduced as under:-

3.6. In view of the above facts, as referred in column no.2 and 4 of the above table that in view of the nominal agricultural income shown by the assessee for the preceding two AYs 2014-15 and 2015-16, the land was not used for

agricultural purposes and in fact the land purchased was being used for commercial purposes, the AO held that the deduction of Rs.41,71,72,652/-[Deduction u/s 54B of Rs.78,54,42,491/- as claimed by assessee minus unutilized amount of Rs.36,82,69,839/- in Capital gains account on which tax is pad during AY 2018-19] claimed by the assessee on purchase of land doesn’t fall within the ambit of Sec. 54B of the Act and the same was brought to tax accordingly under section 45 of the Act.

4. Aggrieved with the said order, the assessee filed an appeal before the Ld. CIT(A), who allowed the appeal of the assessee and the Department is in appeal before us by raising grounds of appeal:-

“Whether on facts and circumstances of the case, the Ld.CIT(NFAC) has not considered the addition of Rs.41,71,72,652/- on account of the deduction of Rs.41,71,72,652/-[Deduction u/s 54B of Rs.78,54,42,491/- as claimed by the assessee minus unutilized amount of Rs.36,82,69,839/- in Capital Gains account on which tax is paid during AY 2018-19] claimed by the assessee on purchase of land does not fall within the ambit of Section 54 of the IT Act, 1961 without considering the basic facts of the case.”

5. The relevant extract of the Ld. CIT(A) allowing the appeal of the assessee has been reproduced by my learned Brother in para no.8 of his order. Thereafter, my learned Brother, based upon his findings in para no.9 and 10 of his order upheld the decision of the Ld. CIT(A) deleting the disallowance of deduction u/s 54B of the Act amounting Rs,,41,71,72,652/-. The para no.9 and 10 of the order of my ld. Brother is reproduced as under:-

“9. From perusal of finding of Ld. CIT(A) in light of grounds of appeal, it is apparent on record that Ld. AO disputed the use of land for agriculture purpose and disallowed deduction under Section 54B of the Act. Ld. AO had

| (a) |

|

Sale deed pertaining to land sold by assessee and sale deeds of land purchased from Ms. Latika Dutt (pages 137 to 150 of the paper book), Ms. Charu Dutt (pages 151 – 169 of the paper books) and Mr. Mahesh Aggarwal (pages 170-178 of the paper books); |

| (b) |

|

ITRs of assessee mentioning agricultural income; |

| (c) |

|

DDA land searched on public domain; and |

| (d) |

|

verification by team of inspectors. |

10. However, Ld. CIT(A) found that the three sale deeds of lands purchased by assessee mentioned as land agriculture. He further observed that the land purchased by assessee was classified agriculture by DDA in its Master Plan. As per RTI Replies, pages 202 & 203 of paperbook Master Plan of DDA has not being notified. The DDA’s Master Plan is not in paper books. It is a material fact established on record that three sale deeds of the land purchased by the assessee from Ms. Latika Dutt, Ms. Charu Dutt and Mr. Mahesh Aggarwal mention the land as” agriculture land”. Land records of Delhi Government as such Khasragirdawari at page nos. 179 to 190 of paper books state land as agricultureunder cultivation. Section 81 Order of Revenue Department in case of Ms. Latika Dutt at page nos. 191-193 of the paper book, mention land use for agriculture purposes. Assessee submitted, tube well plan, sale bills and bills of agriculture etc. Ld. CIT(A) accepted additional evidence page nos. 281 to 282 of paper books and asked the Ld. AO to verify which were not controverted. After considering the above facts, Ld. CIT(A) deleted the addition made by Ld. AO. The discussion, reasons and findings of Ld. CIT(A) are sustainable in law and liable to be upheld. The ground of appeal being de void of merit is untenable.”

6. My Ld. Brother has inter alia relied upon the fact that the three sale deeds of the land purchased by the assessee from Ms. Latika Dutt, Ms. Charu Dutt and Mr. Mahesh Aggarwal mention the land as “agriculture land”, Land records of Delhi Government as such Khasra girdawari at page nos. 179 to 190 of paper books state land as agricultural under cultivation and that Section 81 Order of Revenue Department in case of Ms. Latika Dutt at page nos. 191-193 of the paper book, mention land use for agriculture purposes. Further, my ld. Brother also noted that the assessee submitted, tube well plan, sale bills and bills of agriculture etc. and the Ld. CIT(A) accepted additional evidence at page nos. 281 to 282 of paper books and asked the Ld. AO to verify which were not controverted. In view of these facts, my ld. Brother upheld the order of the Ld. CIT(A) and dismissed the appeal of the Revenue.

7. For analyzing the issue regarding the claim of the assessee on deduction u/s 54B of the Act, the relevant provision of section 54B(1) is reproduced as under:-

“Capital gain on transfer of land used for agricultural purposes not to be charged in certain cases.

54B. (1) Subject to the provisions of sub-section (2), where the capital gain arises from the transfer of a capital asset being land which, in the two years immediately preceding the date on which the transfer took place, was being used by the assessee being an individual or his parent, or a Hindu undivided family for agricultural purposes (hereinafter referred to as the original asset), and the assessee has, within a period of two years after that date, purchased any other land for being used for agricultural purposes, then, instead of the capital gain being charged to income-tax as income of the previous year in which the transfer took place, it shall be dealt with in accordance with the following provisions of this section, that is to say,—

7.1. As per the provisions of above section, for claiming the deduction on the capital gains on the sale of the land, the first requirement is that capital gain should arise from the transfer of a capital asset being land which, in the two years immediately preceding the date on which the transfer took place, was being used by the assessee being an individual or his parent, or a Hindu undivided family for agricultural purposes and thereafter the assessee has, within a period of two years after that date, purchased any other land for being used for agricultural purposes.

7.2. In this case, as per the computation of capital gains filed by the assessee (placed at page no.2 of the paper book) and reproduced earlier in my part of this order, it is seen that the assessee sold land having area of 37 Bighas 15 Biswas for a sum of Rs.100 crores to M/s Radha Soami Satsang Beas. From the above computation, it is seen that the indexed cost of this land has been claimed at Rs.1,31,77,334/-. However, the agricultural income shown by the assessee on the above land (as reproduced in para 3.2 on page no.15 & 16 of this combined order) is very nominal and the realization value of the said land on its sale almost appreciated 100 times from the year 1989 to 1993 during the period in which the above lands were purchased by the assessee(details of the said purchase deeds are placed at page no.68 to 134 of the paper book). The agricultural income declared by the assessee amounts to Rs.50,628/- and Rs.25,500/- for the AYs. 2014-15 and 2015-16, two assessment years prior to its sale in AY 2016-17 for a property which was purchased between 1989 to 1993. It is reasonable to expect that on such a huge tract of land over this period, there should have been substantial agricultural income if the land was being used for agricultural purposes in its true sense and not as a token activity as has been done by the assessee. These facts show the unreasonableness of the claim of the assessee that the land sold was being used for agricultural purposes over the period of its purchase and also in AY 2014-15 and 2015-16 two years prior to the date of sale in AY 2016-17. The deduction u/s 54B of the Act is for a land which is used for agricultural purposes which will result in earning agricultural income by the assessee and to earn the agricultural income, the assessee has to use the land for agricultural purposes. It has to be borne in mind that the deduction u/s 54B of the Act is given for the sale/purchase of ‘land being used for agricultural purposes’ and not for a ‘land for agricultural purposes’. The evidences submitted by the assessee by way of purchase agreements categorizing the said lands as agricultural, tube well connection on the said land and electricity connection on the said land at best supports the claim of the assessee that the land was agricultural land but it does not establish the claim of the assessee that the land was being used for agricultural purposes. In fact, in the given facts of the case, it will be reasonable to conclude that the assessee is a investor in land who as a strategic investor invested in the land sold during the year in an urban setting or nearby an urban setting expecting an increase in the prices of the said land upon its sale and claiming to use the land for agricultural purposes for claiming deduction u/s 54B of the Act on the capital gains arising on the eventuality of the sale of the said land. An argument may be taken that the land was purchased as early as between 1989 to 1993 and therefore such a conclusion arrived will not be correct in view of the huge time gap between the said land being purchased and the land being sold in FY 2015-16 i.e. on 07.12.2015 and no reasonable person could have anticipated such a huge appreciation of about 100 times in the sale price of the said land. However, as discussed above, the assessee had again purchased agricultural land from three persons at the investment cost of Rs.38,97,99,000/- but again on such a huge investment, the agricultural income earned by the assessee in AY 2017-18 and 2018-19 amounts to Rs.3,28,000/- and Rs.4,43,188/-, which again is found to be unreasonable compared to the investment made and for his claim that the land being purchased was for agricultural purposes. Further, it is seen that the assessee claims to grow vegetables, flowers and grass on the said land but given the very nominal agricultural income shown by the assessee, it can be safely concluded that the main purpose in declaring the said agricultural income was merely a ploy to claim the deduction of capital gains u/s 54B of the Act, where the land purchased and sold has to be shown that it was being used for agricultural purposes as per the stipulated time period provided u/s 54B(1) of the Act. As discussed above, it cannot be said that the main purpose of the assessee is to buy the land for agricultural purposes and once the land is not bought for using it for agricultural purposes then the assessee will not be entitled for deduction u/s 54B of the Act as claimed by him.

7.3. The above declared agricultural income by the assessee in respect of the land sold and purchased by him shows that the assessee’s rate of return on its capital invested for the purchase of the said land by way of the agricultural income shown in AY 2014-15 and 2015-16 (prior to sale by the assessee) and 2017-18 and 2018-19 (post purchase by the assessee) was very negligible. On perusal of the sale deeds of the various properties purchased by the assessee between 1989 to 1993 (placed at page no.68-136 of the paper book) the total cost of purchase amounts to Rs.25,70,000/- (the cumulative value of the land as available on page no.68, 73, 77, 81, 86, 91, 95, 103 (except of the property- which is the exchange deed of property placed at page no.135-136 of the paper book, where the agreement or the agreement or the exchange value is not mentioned).On the said investment value of Rs.25,70,000/- (which in real value terms will be much higher during the period 1989 to 1993 than in AY 2014-15 to AY 2018-19 the material period for claiming deduction u/s 54B in this case)the agricultural income of Rs.50,628/- and Rs.25,500/- for AY 2014-15 and 2015-16 comes to 1.96% and 0.99% respectively. Similarly, the agricultural income of Rs.3,28,000/- and Rs.4,43,188/- for AYs 2017-18 and 2018-19 respectively, comes to 0.084% and 0.113% on the total purchase cost of Rs.38,97,99,000/-(Rs.25,26,74,000/- paid to Ms. Latika Dutt, Rs.13,56,25,000/- paid to Ms. Charu Dutt and Rs.15,00,000/- paid to Shri Mahesh Aggarwal) from a land area of 25 Bigha, 28 Biswas. Such low return on capital invested and such nominal agricultural income from as such a huge area of land does not stand the test of reasonableness in the hands of any prudent person, be he being a businessman or a farmer or an agriculturist if the said land was purchased for being used for agricultural purposes, which was sold by the assessee during the year and also the same situation remains in respect of the three parcels of land purchased by the assessee being claimed to be used for agricultural purposes during the stipulated period as mandated u/s 54B of the Act. Therefore, this data also negates the claim of the assessee that the land sold by him was used for agricultural purposes during AYs 2014-15 & 2015-16 and the land purchased by him was being used for agricultural purposes or was being used by the assessee till AY 2018-19 for agricultural purposes in terms of the requirement of section 54B of the Act as discussed above.

7.4. Further, in my humble opinion, for claiming the deduction u/s 54B of the Act, the land in question being sold/purchased should be used for productive agricultural purposes on substantive basis, commensurate to its size and the suitability of the land for agricultural purposes (the suitability of the land for being used for agricultural purposes is implicit or a pre-requirement for claiming the deduction u/s 54B of the Act in the case of the assessee at least in assessment year 2014-15 and 2015-16 since no expenses has been claimed to be incurred for any improvement on the said land, meaning that the land was fit for agricultural purposes from the initial purchase of the land between 1989 to 1993) and grow the agricultural crops by engaging agricultural labourers and contributing in the wealth/GDP of the nation rather than its dormant use for agricultural purposes in the case of the assessee as discussed above. On the allowance of deduction u/s 54B of the Act as claimed by the assessee, the public exchequer will forego tax amounting to Rs.9,62,50,074/- (as per the figure given by the Department in the column of ‘Total Tax Effect’ in Form No.36 of the appeal filed by the Department), on the said capital gains of Rs.41,71,72,652/-, which again in my humble opinion, cannot be allowed merely by a symbolic or token activity of using the said land for agriculture purposes by the assessee as discussed above.

7.5. Further, the assessee in support of his claim that the land was being used for agricultural purposes, the assessee has submitted the Khasra/Girdawri of the land sold and the land purchased by the assessee on the following page nos. of the paper book as under-:

| Sl. No. |

Particulars |

Page No. |

| 1 |

Copy of the sale deed of the property sold during the year under appeal |

13-21 |

| 2 |

Khasra/Girdawri of Latika Dutt before purchase |

179-181 |

| 3 |

Khasra/Girdawri of Assessee after purchase (Latika Dutt & Charu Dutt) |

182 & 194 |

| 4 |

Khasra/Girdawri of Charu Dutt before purchase |

183-187 |

| 5 |

Khasra/Girdawri of Mahesh Aggarwal before purchase |

188-190 |

| 6 |

Khasra/Girdawri of Assessee after purchase |

194 |

7.6. The same has been carefully perused. However, on its perusal, it appears that the same has been issued for all the years around the same time without any serial number and whether the due process for issuing the said Khasra/Girdawri has been followed or not is not evident i.e. whether the same is based on any application or any return filed by the assessee and the sellers of the said land. In absence of any verification by the AO, the authenticity of the data in the said Khasra/Girdawri is not tested. It is true that the AO has not made any enquiry about the correctness of the above Khasra/Girdawri and has not controverted the entries therein but even if considering the facts mentioned therein to be correct but in view of the discussion made earlier in para 7 to 7.4 as above in my order, these documents showing such nominal income does not establish the claim of the assessee that the land was being used for agricultural purposes as required under the provisions of section 54B of the Act.

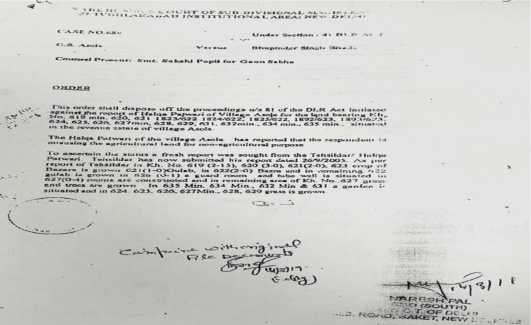

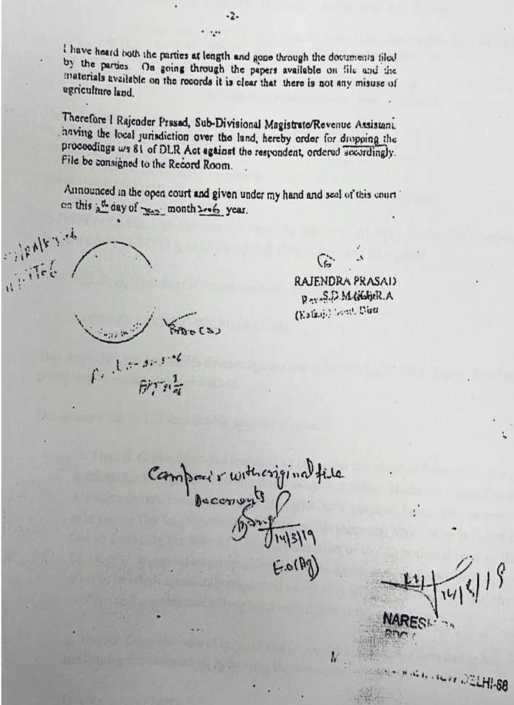

7.7. Further, the assessee has placed reliance on the order u/s 81 of the DLR Act by Sub-divisional Magistrate, Kalkaji District, dated in the month of January, 2006 (as date of order is not very legible) in respect of the property sold by the assessee and placed at page no.34 and 35 of the paper book in support of his claim that the land sold by the assessee was being used for agricultural purposes. The same is reproduced for ready reference:-

7.8. Further, on perusal of the said order, it is stated that crop of Bajra, Gulab and grass and trees are grown and the specifications of the quantity and the area grown is mentioned in the above order.

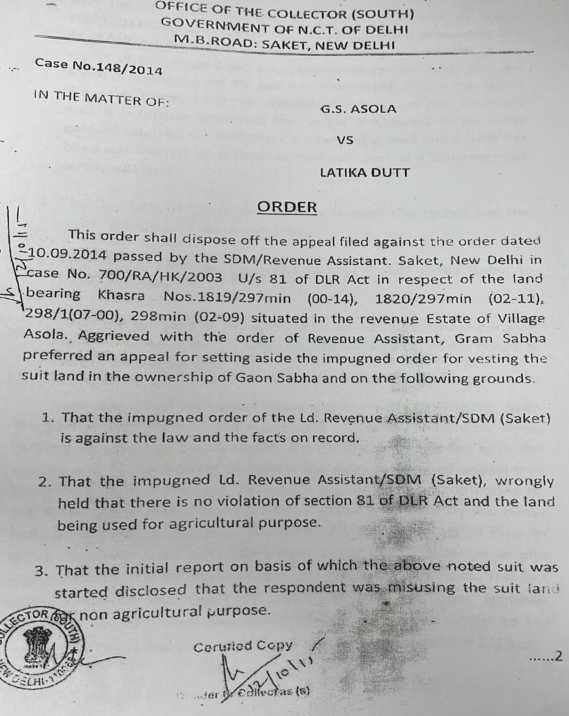

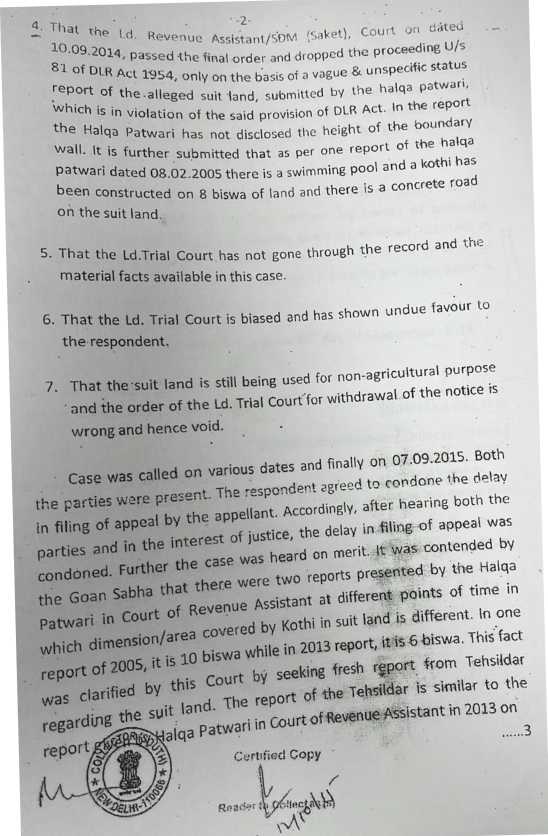

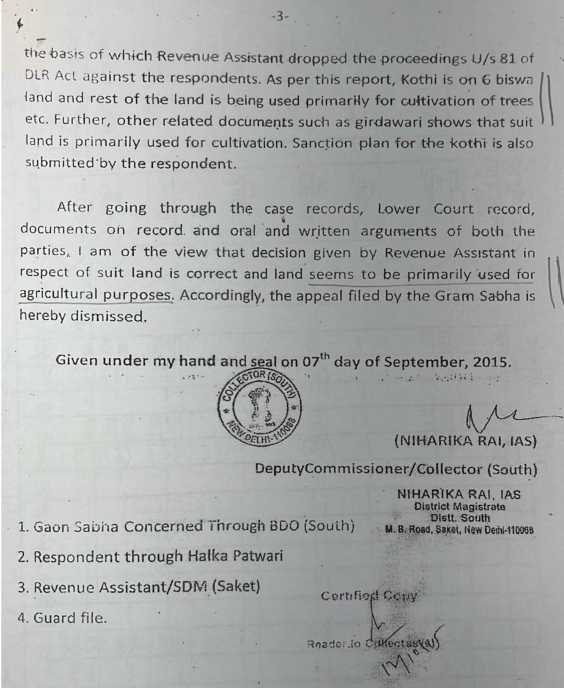

7.9. Further, the assessee has also placed reliance on the order dated 07.09.2015 passed u/s 81 by the Dy. Commissioner/Collector(South) Saket in support of his claim that the land purchased from Ms. Latika Dutt was being used for agricultural purposes. The said order is reproduced as under:-

7.10. On perusal of the said order, it is stated that land was being used primarily for cultivation of trees and the girdawari shows that suit land is primarily used for cultivation of trees and seems to be primarily used for agricultural purposes. The said order is placed at page no.191 to 193 of the paper book.

7.11. However, on perusal of both the orders, it is seen that the same have been passed u/s 81 of DLR Act and not considering the provisions of section 54B of the Act, where the deduction on capital gains for the land being used for agricultural purposes is allowed on the capital gains arising to the assessee on sale of the land as per the conditions laid down in the said section. The order in the case of the assessee passed in January, 2006 relates to AY 2006-07and is not for the AY 2014-15 and 2015-16, which are the relevant years for the determination of the land being used for agricultural purposes for determining the deduction u/s 54B of the Act as claimed by the assessee. Even though the second order dated 07.09.2015 in the case of Ms. Latika Dutt is just prior to the date of purchase of the land by the assessee on 07.12.2015 but in view of the reasons given by me earlier in this order in para no.7 to 7.4 the findings in the said two orders u/s 81 of the DLR Act cannot be relied upon for allowing deduction u/s 54B of the Act as claimed by the assessee.

7.12. Therefore, in the given facts of the case and as per above discussion particularly in para no.7 to 7.4, 7.6 and 7.11 of my order, it is held that the land which has been sold by the assessee during the year and land purchased by the assessee from Ms. Latika Dutt, Ms. Charu Dutt and Shri Mahesh Aggarwal have not been used for agricultural purposes as per the requirement of section 54B of the Act to make the assessee eligible for claiming deduction of Rs.41,71,72,652/-u/s 54B of the Act as claimed by him.

7.13. Therefore, in view of the facts and discussion, I do not agree with the findings of my ld. Brother in upholding the order of the Ld. CIT(A) in deleting the deduction of Rs.41,71,72,652/- disallowed by the AO and it is held that the disallowance of Rs.41,71,72,652/- claimed by the assessee u/s 54B of the Act by the AO is justified and the same is confirmed. Ground of the appeal filed by the Revenue is allowed.

8. In the result, the appeal filed by the Revenue is allowed.

MAHAVIR SINGH, VICE PRESIDENT (AS THIRD MEMBER): –By the order of President, ITAT vide U.O. No.F.28-Cent.Jd(AT)/2025 dated 18th July, 2025, the undersigned has been nominated to adjudicate the difference of opinion between the learned Judicial Member and learned Accountant Member on the following question:-

“1. Whether in facts and circumstances and in Law, the order of the Ld. CIT(A) deleting the disallowance of Rs.41,71,72,652/- claimed by the assessee under Section 54B of the Act should be confirmed/reversed?”

2. Brief facts of the matter are that the assessee sold land admeasuring 37 Bighas 15 Biswas bearing Khasra No.1893/623, 1892/623, 624 etc. in Village Asola, New Delhi 110074 on 7th December, 2015 for a total consideration of ‘100 crores. This land was purchased by the assessee during the year 1988-89. The assessee claimed deduction under Section 54B of the Income-tax Act, 1961 (hereinafter referred to as ‘the Act’) for the relevant assessment year 2016-17 for a sum of ‘78,54,42,491/- and a deduction under Section 54EC of the Act of ’50 lakhs. The assessee submitted the details of all the three properties purchased and claimed deduction under Section 54B of the Act. The details of properties purchased are as under:-

From Latika Dutt : Purchase of land property on 03/10/2016 from Latika Dutt of 12 Bigha 14 Biswa bearing Khasra Nos.298/1(7-0) 298 MIN (2-09), 1820/297 MIN EAST (2-11) and 1819/297 MIN WEST (0-14) in Asola Tehsil Saket, New Delhi 110074 for a consideration of Rs.25,26,74,000/- (excluding stamp duty and registration charges) on 03.10.2016.

From Charu Dutt : Purchase of land on 04/01/2017 from Charu Dutt amounting to Rs.13,56,25,000/- (excluding stamp duty and registration charges) of 13 Bigha 5 Biswas bearing Khasra Nos.1820/297 Min West (1-8), 1819/297 MIN WEST (0-8), 261, 261, 263, 260, 259.

267 etc village Asola, New Delhi 110074.

From Mahesh Aggarwal : Purchase of land on 26/12/2016 from Mahesh Aggarwal amounting to Rs.15 Lakh of 9 Biswas bearing Khasra No.2004/1461 Etc. village Bhati, New Delhi 110074.

3. The balance unutilized amount on which the assessee paid tax is ‘36,82,69,839/-. In net effect, the assessee claimed deduction of ‘41,71,72,652/-under Section 54B of the Act after purchasing above three properties (which is now in dispute). The Assessing Officer, while framing assessment, examined the conditions as prescribed under the provisions of Section 54B of the Act for allowing deduction under this provision and, according to him, the land sold by the assessee i.e., agricultural land of area 37 Bighas 15 Biswas in Village Asola, New Delhi, is not used for agricultural purposes and, in fact, land has been purchased in 1988 and is being used for commercial purposes. This fact is noted by the Assessing Officer at page 14 of his order, which reads as under:-

| 1. |

|

Purchase of land on 03/10/2016 from Latika Dutt of 12 Bighas 14 Biswas. |

| 2. |

|

Purchase of land on 04/01/2017 from Charu Dutt of 13 Bighas 5 Biswas. |

| 3. |

|

Purchase of land on 26/12/2016 from Mahesh Aggarwal of 9 Biswas. |

| Testing the conditions of Sec 54B |

|

Condition |

Whether fulfilled |

Remarks |

| 1 |

capital gain arises from the transfer of a capital asset being land |

Yes |

Sale of Agricultural land of area 37 Bighas 15 Biswas in village Asola, New Delhi 110074 on 07/12/2015 for a value of Rs.100 Crore by the assessee. |

| 2 |

in the two years immediately preceding the date on which the transfer (of the asset) took place was being used by the assessee being an individual or his parent, or an HUF for agricultural purposes. |

Condition not completely fulfilled. |

The assessee is showing an agricultural income of Rs.50,628/- and Rs.25,500/-respectively in ITR for two preceding years i.e. AY (14-15) and AY (2015-16) for a land having huge area of 37 Bighas 15 Biswas which was sold for a whooping amount of Rs.100 crore. Hence the contention of the assessee that land has been used for agricultural purposes is not acceptable even though the land is agricultural in nature. |

| 3 |

within a period of two years after that date purchased any other land |

Yes |

|

| 4 |

being used for agricultural purposes |

No |

It has already been discussed above in the para 4.4 and 4.5 along with photographs of the properties showing clear proof of no agricultural activities being carried out on the purchased land. In fact the land purchased is being used for commercial purposes. |

Therefore, in light of the above discussion, I hold that the deduction of Rs.41,71,72,652/- [Deduction u/s. 54B of 78,54,42,491/- as claimed by assessee minus unutilized amount of Rs.36,82,69,839/- in Capital gains account on which tax is paid during A.Y. (18-19) claimed by the assessee on purchase of land doesn’t fall within the ambit of Sec 54B of income tax act, 1961. The same is brought to tax accordingly under section 45 of the Income tax Act, 1961.

Aggrieved, assessee preferred appeal before the learned CIT(A).

4. Learned CIT(A) allowed the claim of the assessee, which is reproduced in the order of learned Judicial Member at paragraph 8 from pages 5 to 10, which need not be reproduced again for the sake of duplicity and brevity.

5. Before me, learned Counsel for the assessee filed copies of sale deed pertaining to land sold by the assessee to Radha Soami Satsang of Beas in Village Asola and land purchased by the assessee from Ms. Latika Dutt, Ms. Charu Dutt and Mr. Mahesh Aggarwal. Learned Counsel pointed out that in all the three sale deeds of the land sold &purchased by the assessee, it is clearly mentioned that the land is agricultural land. This fact is neither disputed by the learned Accountant Member, rather, he noted this fact in his order at pages 23 & 24 paragraph 7.2, and the relevant fact noted is being reproduced for the sake of brevity as, “The evidences submitted by the assessee by way of purchase agreements categorizing the said lands as agricultural, tube well connection on the said land and electricity connection on the said land at best supports the claim of the assessee that the land was agricultural land but it does not establish the claim of the assessee that the land was being used for agricultural purposes”. Learned Accountant Member, however, has noted that the above documents do not support or establish the claim of the assessee that land was being used for agricultural purposes. Learned Counsel for the assessee Dr. Rakesh Gupta pointed out from the assessment order Paragraph 4 at pages 6 & 7, wherein the summary of the agricultural income declared by the assessee over the years is noted as under:-

| AY |

Agricultural Income Declared (in Rs.) |

| 2011-12 |

277864 |

| 2012-13 |

287136 |

| 2013-14 |

50000 |

| 2014-15 |

50628 |

| 2015-16 |

25500 |

| 2016-17 |

15000 |

| 2017-18 |

328000 |

| 2018-19 |

443188 |

6. Learned Counsel stated that the assessee has filed Khasra/Girdawri of the land sold by the assessee, as well as the Khasra/Girdawri of the land purchase from Ms. Latika Dutt, Ms. Charu Dutt and Mr. Mahesh Aggarwal. In these Khasra/Girdawri, on the entire land, the land sold by the assessee as well as the land purchased by the assessee, agricultural income has been declared for the reason that crops grown are disclosed as bajra, gulab and grass. Learned Counsel for the assessee also drew my attention to the order passed by the Sub-Divisional Magistrate, Kalkaji District under Section 81 of the Delhi Land Revenue Act dated January, 2006, which is reproduced in the order of learned Accountant Member at pages 29 to 30 at paragraph 7.7, which need not be reproduced again. According to learned Counsel, this order clearly establishes on the basis of Halqa Patwari report that the land is used for agricultural purposes. A particular finding based on the report of the Tehsildar/Halqa Patwari reads as”To ascertain the status a fresh report was sought from the Tehsildar/Halqa Patwari. Tehsildar has now submitted his report dated 26/9/2005. As per report of Tehsildar in Kh. No.619(2-15), 620 (3-0), 621 (2-0), 623 crop of Bazra is grown 621 (1-0) Gulab, in 622 (2-0) Bazra and in remaining 622 gulab is grown in 626 (0-1) a guard room and tube well is situated in 627 (0-4) rooms are constructed and in remaining area of Kh. No.627 grass and trees are grown. In 635 Min. 634 Min. and 631 a garden is situated and in 624, 625, 626 Min. 628, 629 grass is grown.” In challenge to the above order, the SDM, Kalkaji District has categorically held that the land is not misused and it is used for the purpose of agricultural. The relevant finding reads as “I have heard both the parties at length and gone through the documents filed by the parties. On going through the papers available on file and the materials available on the records it is clear that there is not any misuse of agriculture land.”

7. Learned Counsel further drew our attention to the order of Deputy Commissioner/Collector (South) Saket under Delhi Land Revenue Act under Section 81 dated 7th September, 2015, which is reproduced in the order of learned Accountant Member at paragraph 7.9. Learned Counsel for the assessee specifically drew my attention to the finding of fact recorded by the Deputy Commissioner/Collector (South) Saket, and the same is being reproduced again for the sake of brevity and clarity, as under:-

“Case was called on various dates and finally on 07.09.2015. Both the parties were present. The respondent agreed to condone the delay in filing of appeal by the appellant. Accordingly, after hearing both the parties and in the interest of justice, the delay in filing of appeal was condoned. Further the case was heard on merit. It was contended by the Goan Sabha that there were two reports presented by the Halqa Patwari in Court of Revenue Assistant at different points of time in which dimension/area covered by Kothi in suit land is different. In one report of 2005, it is 10 biswa while in 2013 report, it is 6 biswa. This fact was claimed by this Court by seeking fresh report from Tehsildar regarding the suit land. The report of the Tehsildar is similar to the report given by Halqa Patwari in Court of Revenue Assistant in 2013 on the basis of which Revenue Assistant dropped the proceedings u/s 81 of the DLR Act against the respondents. As per this report, Kothi is on 6 biswa land and rest of the land is being used primarily for cultivation of trees etc. Further, other related documents such as girdawari shows that suit land is primarily used for cultivation. Sanction plan for the kothi is also submitted by the respondent.

After going through the case records, Lower Court record, documents on record and oral and written arguments of both the parties, I am of the view that decision given by Revenue Assistant in respect of suit land is correct and land seems to be primarily used for agricultural purposes. Accordingly, the appeal filed by the Gram Sabha is hereby dismissed.”

8. Learned Counsel for the assessee also stated that even the DDA master plan has categorized the land sold and land purchased by the assessee as agricultural land and this fact came to the light when the information was obtained from DDA under Right to Information Act and the same is enclosed at assessee’s paper book page 202 and 203.

9. On the other hand, learned CIT-DR heavily relied on the assessment order and also on the order passed by learned Accountant Member. He argued that practically, there is no agricultural activity carried on by the assessee and the alleged agricultural income shown by the assessee from the above lands is nominal and the realization value of the above said land on its sale almost appreciated 100 times during the period 1989 to 1993, in which the above lands were purchased by the assessee. He argued that on such a huge tract of land over this period, the assessee has declared a token activity of agriculture and a token income as against the value of the land. Therefore, he argued that in the given facts of the case, it would be reasonable to conclude that the assessee is an investor who, as a strategic investor, invested in the land sold during the year in an urban setting or nearby an urban setting expecting an increase in the prices of the land whenever it is sold. Further, it was argued by the learned CIT-DR that such nominal agricultural income from such a huge tract of land does not stand the test of reasonableness in the hands of any person, particularly he being a businessman or a farmer or an agriculturist if the said land was purchased for the purpose of agriculture use. As far as the orders passed under Delhi Land Revenue Act by Sub-Divisional Magistrate, Kalkaji District and Deputy Commissioner/Collector (South) Saket, he stated that it is not the determining factor for the claim of deduction under Section 54B of the Act. Learned CIT-DR also relied on the findings of Report submitted by the two Inspectors dated 28th December, 2018, wherein it is categorically admitted by the Manager of the property regarding renting out the above said premises for marriage purposes and this fact is also confirmed by the owner. Learned CIT-DR relied on the Inspectors’ report.

10. In reply, learned Counsel for the assessee, apart from other arguments, confronted the Revenue on Inspectors’ report and stated that the very language of the report clearly says that the Inspectors have gone as ordinary persons and this is not the report of the Inspectors, may be it is a discreet inquiry. It is clear from paragraph 2 of the report, which is reproduced by the learned Accountant Member at page 17 and 18 as Annexure ‘A’. The relevant portion of paragraph 2 highlighted by the learned Counsel for the assessee reads as under:-

“2. Sh. Dharmender, a Security Guard was present there who guided us inside the premises because we introduced ourselves as customers/client to book the premises for the marriage purpose. He answered the queries asked by us and he apprised that the entire area will be booked for the marriage purpose and he gave the contact no. of Manager/Munshi (the name of the Manager/Munshi was Lakhan) and he also showed the entire premises and also showed the two-storey building inside the premises and two beautiful rest rooms…………………..”

11. In view of the above, learned Counsel stated that the Inspectors visited the premises as a common man and the report has not been confronted to the assessee or no further examination was carried out by the Department. Hence, this report has no evidentiary value.

12. The facts are very clear and admitted by both sides. The only disputed point remains for adjudication is, Whether the land sold by assessee is used for the purposes of agricultural or not? Admittedly, the assessee, from the above sold land, has disclosed agricultural income. This is evident from the assessment order and the order of learned CIT(A) and even the orders of learned Judicial Member and learned Accountant Member. I noted that the Sub-Divisional Magistrate, Kalkaji District has passed order under Section 81 of the Delhi Land Revenue Act dated January, 2006 and the order was challenged before Deputy Commissioner/Collector (South) Saket, who, vide order dated 7th September, 2015, affirmed, rather held, that the land is primarily used for agricultural purposes. This is the finding of a Revenue authority who is the final authority to decide the nature of land and its usage. I have gone through the provisions of Section 54B of the Act and noted the conditions for applicability of Section 54B(1), which are – (i) a capital gain arises from the transfer of land by the assessee, (ii) of a capital asset being land, and (iii) such land was being used by the assessee or his parents, the assessee being an individual or his parents or a HUF for agricultural purposes, in the two years immediately preceding the date of the transfer, and (iv) the assessee has, within a period of two years after the date of the transfer, purchased any other land for being used for agricultural purposes, the assessee is eligible for claim of deduction under this provision. There are various criterions which may applied to find out if the land in a particular case is agricultural or not and some of them are (i) classification and assessment of land to land revenue, (ii) whether agricultural operations are carried on, (iii) intention of the owner, a temporary user of the land either for agricultural or non-agricultural purposes is not important but the real intention of the owner is to be ascertained, and (iv) character of adjoining land. If the surrounding lands are agricultural lands, the presumption would be in favour of holding that the land in question was also agricultural land. Once the assessee establishes that the land in question was assessed to land revenue and was continuously used for agricultural purposes, a prima-facie presumption arises from such user is that the land in question continued to be agricultural land. The price paid or received and/or the situation of the particular land in a well-developed area do not displace that presumption. The presumption can be rebutted only by showing that the land was not agricultural land and the current user of the land was a stop-gap arrangement pending some other user. Even the effect of the amendment i.e., amendment in Section 47(viii) of the Act with effect from 01.03.1970 is that the transfer of urban agricultural land will make the gains thereby earned exigible to the levy of capital gains tax but, in order to mitigate the hardship, capital gains on transfer of such urban agricultural land enjoys exemption under Section 54B of the Act if the conditions specified therein are fulfilled.

13. In the present case before us, the assessee has established that the land is assessed to land revenue as is evident from the Khasra/Girdawri and Halqa Patwari report. Even the land is assessable to Delhi Land Revenue Act and the competent authorities i.e., the matter was brought to the notice of Sub-Divisional Magistrate, Kalkaji District and consequent orders of user was passed under Section 81 of Delhi Land Revenue Act in January, 2006. Consequently, the matter was also challenged before the Deputy Commissioner/Collector (South) Saket, who passed order dated 7th September, 2015 accepting that the suit land is agricultural land and land is primarily used for agricultural purposes. It is also a fact that the assessee is consistently declaring agricultural income from land sold by him at least for last 10 years as is noted by the AO.

14. I have also noted that the Assessing Officer and learned CIT-DR relied on the report of the Inspectors who visited the premises and reported that there is no agricultural activity carried out and the property is a farm house consisting of a posh house with well-manicured lawns, out-houses and swimming pools. The Inspectors clicked photographs of the property but these Inspectors never informed the assessee about the visit and it looked like that this is a discrete enquiry conducted by them without informing the party. The photographs clicked by the team of Inspectors do not give any clear picture, whether the same is being used for any purpose. Even the authenticity of this report and the photographs reproduced in the assessment order are specifically discarded by the assessee. Even otherwise, the Inspectors’ Report is dated 28th December, 2018, which is not at the point of time of transfer of land, which is dated 7th December, 2015. Clearly, there is a gap of three years. Hence, the report of the Inspectors and consequent photographs cannot be taken into consideration while adjudicating this issue as it is without any evidence contrary to the facts on record.

15. In view of the above facts and discussions carried out, the character of this land, as on the date of transfer i.e., 7th December, 2015, is agricultural land and the revenue records also prove that the agricultural land was put to use. Moreover, this has another support that the assessee is consistently declaring agricultural income and the quantum of agricultural income cannot the reason for disallowing the claim of deduction under Section 54B of the Act. The assessee is able to prove that the nature of land is agricultural and it is being used for agricultural activity as per records. The Revenue has not discharged the onus of disproving the same.

16. The lands purchased by the assessee from Ms. Latika Dutt on 3rd October, 2016, from Ms. Charu Dutt on 4th January, 2017 and from Shri Mahesh Aggarwal on 26th December, 2016, in the given facts and circumstances and discussion carried out above, the character of these lands purchased as per revenue records, sale deed, etc., is agricultural land. The revenue records i.e., Girdawri of the land clearly states that there was agricultural produce and land was put to agricultural activity. Clearly, the assessee, in assessment year 2017-18 and 2018-19, has declared agricultural income of these purchased lands at ‘3.28 lakhs and ‘4.43 lakhs respectively. The only presumption of the Assessing Officer was that there is meagre agricultural income, but, quantum of agricultural income cannot decide the character of the land. In such circumstances, the assessee is able to prove the nature of land purchased as agricultural land, and it is being used for agricultural activities as per the revenue records and as per the records of the Income-tax Department. It is also to be pointed out that Assessing Officer has nowhere treated the income declared by the assessee as business income or income from other sources, rather, it is accepted as agricultural income. Accordingly, I am of the view that the assessee is entitled for claim of deduction under Section 54B of the Act in the given facts and circumstances of the case.

17. Now, in view of the above discussion and legal position, I answer the question referred to me as under:-

| Question framed by the Bench |

Answer to the Question |

| Whether in facts and circumstances and in Law, the order of the Ld.CIT(A) deleting the disallowance of Rs.41,71,72,652/- claimed by the assessee under Section 54B of the Act should be confirmed/reversed? |

In the given facts and circumstances of the case and discussion carried above, this question is answered in favour of assessee as the CIT(A) has rightly allowed the claim of deduction under Section 54B of the Act and consequently, the order of CIT(A) is to be confirmed. |

18. The matter shall now be placed before the regular Bench for passing appropriate order in accordance with the majority opinion.

PER VIMAL KUMAR, JUDICIAL MEMBER:

The appeal filed by the Revenue is against order dated 25.08.2023 of Learned Commissioner of Income-Tax (Appeals)/National Faceless Appeal Centre (NFAC), Delhi (hereafter referred to as “Ld. CIT(A)”) under Section 250 of the Income-Tax Act,1961 (hereinafter referred to as “the Act”) arising out of assessment order dated 30.12.2018 under Section 143(3) of the Act by the Assistant Commissioner of Income Tax, Circle 53(1), Delhi (hereinafter referred to as “the AO”) for assessment year 2016-17.

After hearing the appeal, the Judicial Member dismissed the ground of Revenue raising in appeal and consequently upheld the order of CIT(A). The Accountant Member opined otherwise and wrote a separate order allowed ground of appeal of the Revenue. On account of difference of opinion between the Members constituting the Bench, a reference was made to the Hon’ble President ITAT u/s. 255(4) of the Act. The Hon’ble President vide order dated 18.07.2025 nominated Third Member to decide the reference. The ld. Third Member vide order dated 04.02.2026 concurred with the view of Judicial Member. Consequent to the opinion of Third Member, appeal of the revenue is dismissed.