ORDER

Sandeep Gosain, Judicial Member.- The present appeal has been filed by the assessee challenging the impugned order dt. 24.04.2025 passed under section 263 of the Income Tax Act, 1961 (‘the Act’), by the Pr.CIT(A) for the assessment year 2022-23. The assessee has raised the following grounds of appeal:

1. The Learned Principal Commissioner of Income-tax has erred in law and on facts in not appreciating that where the A.O. after detailed verification of record and making enquires had framed the assessment, the revision powers conferred on the Principal CIT under section 263 of Act, cannot invoked only based on a change of opinion.

2. The Principal Commissioner of Income-tax has erred in passing Order u/s.263 of the Income-tax Act, 1961 dated 24.04.2025, without appreciating the fact that the order passed by the A.O. is neither erroneous nor prejudicial to the interest of revenue.

3. The Principal Commissioner of Income-tax has erred in passing Order u/s.263 of the Income-tax Act, 1961 dated 24.04.2025, and issuing directions that exemption u/s.54F was not admissible and the amount of Rs. 16,83,33,702 was taxable in A.Y.2022-23 without considering that A.O. had considered the investment was in multiple flats that were interconnected with a single access point, common living space and internal stairways qualifying it as a single residential unit, and after application of mind held that the provisions of Section 54F was available to the Assessee and hence the directions of Principal Commissioner of Income-tax were on account of change of opinion.

4. The Principal Commissioner of Income-tax has erred in passing Order u/s.263 of the Income-tax Act, 1961 dated 24.04.2025, and issuing directions that Long term Capital gains of Rs.16,83,33,702 was taxable in A. Y.2022-23, on the grounds that Assessee had contravened the provisions of proviso a(ii) to sub- section (1) of Section 54F of the Act, even though the same was considered as taxable in A.Y.2021-22 vide his Order dated 27.03.2025, passed u/s.263.

5. The Principal Commissioner of Income-tax has erred in passing Order u/s.263 of the Income-tax Act, 1961 dated 24.04.2025, and issuing directions that exemption u/s.54F was not admissible and the amount of Rs.39,96,80,216 was taxable without considering that A.O. had considered Assessee has not more than one residential flat, other than the new flat on the date of transfer of the original asset.

6. The Appellant prays that, the Order u/s.263 of the Incometax Act dated 24.04.2025 passed by Principal Commissioner of Income-tax be annulled, squashed and set aside.

7. The aforesaid Grounds of Appeal are independent, alternative and without prejudice to one another.

8. The Appellant craves leave to add, and / or alter, and / or modify, and / or delete the aforesaid Grounds of Appeal before or at the time of hearing.

2. All the grounds raised by the assessee are interrelated and interconnected and relates to challenging the order of PCIT in passing the order u/s 263 of the Act. Therefore, we have decided to adjudicate these grounds through the present consolidated order.

3. We have heard the counsels for both the parties, perused the material placed on record, judgments cited before us and also the orders passed by the revenue authorities. From the records we noticed that assessee had earned long term capital gains by selling unquoted shares and shown Long term Capital gain of Rs. 81,39,22,970/-crore and thus claimed deduction of Rs. 39,96,80,216/-u/s 54F of the Act on account of the purchase of flat No. 501 in building known as “Samparpan” at Bandra vide registered agreement on 20.08.2021. It was observed by Ld. PCIT from return of income of the assessee for A.Y 2021-22 that the assessee had purchased six residential flats / house on 23.12.2020 i.e flat Nos. 1402, 1403, 1502, 1503, 1602 & 1603in the residential building known as “Apas Valmark” in Bangalore for a purchase consideration of Rs. 20,00,64,750/- and against the same the assessee had also claimed deduction u/s 54F of the Act. Therefore reasons recorded by Ld. PCIT for revision of the order of assessment dated 20.03.2024 was that since the assessee had purchased six residential flats in Bangalore before purchase of residential flats in “Samparna” at Bandra, Mumbai therefore assessee was not eligible for deduction u/s 54F of the Act amounting to Rs. 39,96,80,216/- as assessee had failed to adhere to the conditions laid down in proviso (a)(i) to sub section (1) of Section 54 of the Act which prescribes that assessee could not “own more than one residential house other than the new asset on the date of transfer of the original asset”

4. In this regard the assessee categorically mentioned that with regard to deduction of Rs. 39,96,80,216/- u/s 54F of the Act, the assessee had submitted that he had „single residential unit’ in Bangalore on 23.12.2020 i.e. “Apas Valmark” and had no ownership of any other property in Bangalore. It was further submitted that six flats described by Ld. PCIT at “Apas Valmark” at Bangalore owned by assessee is a ‘single residential unit’. It was submitted that on similar facts the case of the assessee for A.Y 2021-22 was revised by order u/s 263 of the Act by Ld. PCIT and the said order was challenged by the assessee consequently, the Coordinate Bench of ITAT in its order Sidhardha Bhaskar Shah v. Pr. CIT [IT Appeal No. 2169/Mum/2025, dated 29-9-2025] under the similar set of facts considered the six flats at “Apas Valmark” at Bangalore has alleged by the Ld. PCIT in the present case and held the same as one residential unit. Therefore the issue of considering six flats as one unit is not res-integra in view of the decision of the Coordinate Bench of ITAT in assessee’s own case titled Sidhardha Bhaskar Shah(supra), therefore when once the Coordinate Bench has already considered the flats at Bangalore and held as one unit therefore the very basis for invoking the provisions of Sec. 263 of the Act for the year under consideration is not sustainable. The operative portion of the order of the Coordinate Bench in Sidhardha Bhaskar Shah (supra), the operative portion of the same is reproduced herein below:

5. We have heard both the parties and perused the material on record and given our thoughtful consideration to the orders of the authorities below. We have also perused the paper book containing factual documents in 72 pages and also the paper book containing judicial precedents. At the outset, we note that ld. Assessing Officer had made detailed enquiry and verification in respect of the reason for which the case was taken up for scrutiny assessment namely, “for verification of deduction claimed by the assesseeu/s. 54F”. Assessing officer had issued show-cause notice comprising of 21 pages, covering every aspect of the claim of deduction made by the assessee, for which even the assessee made detailed submission, supported by relevant documentary evidences, all of which are placed on record. Thus, it is not a case of lack of enquiry or inadequate enquiry on the part of the Assessing Officer in arriving at a view, taken while completing the assessment.

6. The moot point before us in respect of the present appeal vis-a-vis revisionary order passed by the ld. PCIT is to adjudicate upon whether the view taken by the Assessing Officer in accepting the claim of deduction u/s. 54F is a plausible view or otherwise. The issue raised by the ld. PCIT in the revisionary order of assessee violating the provisions of section 54F by making investment in multiple flats i.e. six flats, two each on three different floors and converting the same into one triplex residential house, has been enquired into detail by the ld.Assessing Officer in the course of assessment proceeding itself. Replies given by the assessee along with documentary evidences are found to be satisfactory as recorded by the ld.Assessing Officer in Para 6 of his assessment order.On the very same issue, ld. PCIT has another view of assessee being not entitled to claim of deduction u/s. 54F having invested into multiple flats i.e. six flats on three different floors, two on each floor and thus, has held the assessment order to be erroneous insofar as prejudicial to the interest of revenue.

6.1. To understand the factual position, we perused the registered agreement to sell, placed in the paper book at page 36 and onwards ,whereby the details of the property sold by the Vendor/Developer to the assessee is detailed in Para J of the said agreement. The said Para is extracted below for ready reference.

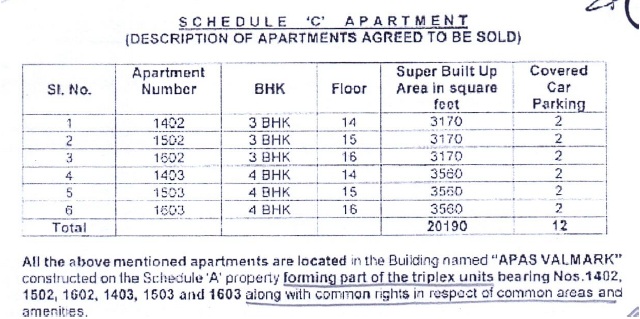

“J. WHEREAS the Vendor/Developer herein has agreed to sell to the Purchaser/s the SCHEDULE ‘B’ PROPERTY and SCHEDULE ‘C’ PROPERTY for a valuable consideration and on certain mutually agreed lems and conditions as mentioned hereinafter a proportional undivided share night title and interest in the Schedule A Property being 696.57 sq.ft, 696.57 sq.ft., 696.57 sq ft, 782.27 sq.ft., 782.27 sq.ft. and 782.27 sq.ft. all aggregating to 4436.52 sq.ft. which is more fully described in the Schedule B hereto and for the sake of brevity is hereinafter collectively called and referred to as the SCHEDULE B PROPERTY and a 3 and 4 BHK Apartment forming part of the triplex units bearing Nos. 1402, 1502, 1602, 1403, 1503 and 1603 respectively on the Schedule A property on the Fourteenth, Fifteenth and Sixteenth Floors, individually measuring 3170 sq.ft., 3170 sq.ft., 3170 sq.ft., 3550 sq.ft. 3560 sq.ft. and 3560 sq ft. of Super Built up area, along with 2 (two) covered car parking space reserved for each apartment referred to above which is more fully and particularly described in the Schedule ‘C’ hereto and for the sake of brevity is hereinafter collectively called and referred to as the SCHEDULE ‘C’ APARTMENT in accordance with the sanctioned plan and on the terms, conditions and specifications as mentioned in the SCHEDULE D’ hereunder.”

(emphasis supplied by us by bold and underline)

6.2. From the above Para, it is noted that the scheduled property is a “triplex unit” comprising of the six flats. We also take note of the Schedule C containing description of the apartments agreed to be sold by the developer vide this registered agreement. The same is extracted below.

6.3. From the above, we note that there are six flats, one 3BHK flat and another 4BHK flat on floor 14 and similarly on floor 15 and floor 16 thus, comprising of six flats on three floors, two each with two parking for each flat. The total super built up area covered by the six flats is 20,190 square feet and which forms part of the “one triplex unit”. Assessee also gets proportionate undivided share in the land in respect of the said property comprising of one triplex unit having six flats.

7. The issue of considering multiple flats on different floors of an apartment to be considered as one residential house had come up before the Hon’ble High Court of Delhi in the case of PCIT v. Lata Goyal (Del), wherein on similar fact pattern, the claim of deduction u/s. 54F was allowed to the assessee. Facts of this case as noted in Para 4 of the order are that “assessee filed her return of income declaring income of Rs. 70,87,301/-.She claimed a deduction of Rs. 90 crores u/s. 54F asserting that the consideration received from the sale of shares of FITTJEE Limited, an unlisted company, the gains from which would otherwise be chargeable to tax as capital gains, was invested in acquiring a residential house property bearing the address E-27, Vasant Vihar, New Delhi, i.e., the new asset”. In the assessment completed by the ld. Assessing Officer u/s. 147, he noted that assessee owned more than one residential property on the date of the transfer of shares, being basement and second floor of the property. According to him, the basement and second floor were required to be considered as two separate residential houses, and therefore, the provisions of section 54F were not complied with. Revenue was in appeal before the Hon’ble High Court on the relief granted by the Tribunal in allowing the claim of deduction u/s. 54F by treating the different units at different floors as one single residential house.

7.1. Hon’ble Court referred and relied on the decision of Hon’ble High Court of Karnataka in the case of CIT v. D. Ananda Basappa [2009] 309 ITR 329 (Kar), whereby it held that the expression “a residential house’ should be understood in a sense that ‘a’ should not be understood to indicate a singular number. Hon’ble Court noted that the two apartments had been joined to make one unit by opening a door between the two apartments and therefore, the same could be construed as one unit. Hon’ble Delhi High Court referred to the decision of its own Coordinate Bench in the case of CIT v. Geeta Duggal [2013] 357 ITR 153 (Del), wherein the issue relating to ‘a residential house’ visa-vis ‘a residential unit’ was elaborately dealt with. In para 11 of this order, in the case of Geeta Duggal (supra), Hon’ble Court noted that section 54 and 54F uses the expression ‘a residential house’. What ld. Assessing Officer has referred to is ‘a residential unit’ which is not an expression found in the said sections.

7.2. According to the Hon’ble Court, section 54 and 54F requires the assessee to acquire a residential house and so long as the assessee acquires a building which may be constructed for the sake of convenience in such a manner as to consist of several units, which can, if the need arises, be conveniently and independently used as an independent residence, the requirement of the section should be taken to have been satisfied. Hon’ble Court also noted that there is nothing in these sections which require the residential house to be constructed in a particular manner. The only requirement is that it should be for the residential use and not for commercial use. Thus, if there is nothing in the section which requires that the residential house should be built in a particular manner, the Income-tax authorities cannot insist upon such a requirement. Hon’ble Court further elaborated that a person may construct a house according to his plans and requirements. Hon’ble Court thus, concluded that how or why the physical structuring of the new residential house, whether it is lateral or vertical, should come in the way of considering the building as residential house. According to the Hon’ble Court, the fact that the residential house consist of several independent units, cannot be permitted to act as an impediment to the allowance of the deduction u/s. 54 and 54F.

7.3. Hon’ble Delhi High Court further referred to the decision of another Hon’ble High Court of Madras in the case of CIT v. Gumanmal Jain [2017] 394 ITR 666 (Mad). This decision was also rendered in the context of construing whether the new asset purchased is a residential house, an expression used in section 54 and 54F of the Act. Hon’ble Court noted that this decision would be equally applicable for construing the term ‘one residential house’ as used in clause (i) of the proviso to section 54F. Thus, Hon’ble Court after placing reliance on several decisions of other High Courts, namely Hon’ble High Court of Karnataka, Hon’ble High Court of Madras and of its own Coordinate Bench in another case, found no infirmity with the decisions of the Tribunal in holding that the assessee could not be denied the deduction u/s.54F on the ground that she held more than one residential unit. While concluding, Hon’ble Court also took note of the fact that configuration of ownership of the property as recorded in South Delhi Municipal records does not lead to the conclusion that there is any failure on the part of the assessee in disclosing the material facts relevant for claiming the deduction sought by the assessee.

7.4. Relevant paragraphs of this decision from para 20 to para 28 are extracted below for ready reference:-

“20. In CIT v. D. Ananda Basappa (Karnataka), the Karnataka High Court considered the admissibility of exemption under Section 54 of the Act in a case where the Assessee had sold a residential house and purchased two adjacent apartments. The Court held that “the expression ‘a’ residential house should be understood in a sense that building should be of residential in nature and ‘a’ should not be understood to indicate a singular number”. However, in the facts of the said case, the court noted that two apartments had been joined to make one unit by opening a door between the two apartments and therefore, the same could be construed as one unit.

21. In Pawan Arya v. CIT (Punjab & Haryana)/2010 SCC OnLine P&H 12590, the court distinguished the decision in D. Ananda Basappa (supra) and stated that the exemption under Section 54F of the Act would not be applicable where the units are located at two different locations. In the aforesaid context, the court observed as under:-

“4. As regards claim for exemption against acquisition of two houses under Section 54 of the Act, the same is not admissible in plain language of statute. In the judgment of Karnataka High Court in CIT v. D. Ananda Basappa [2009] 309 ITR 329 (Kar), referred to in the impugned order, exemption against purchase of two flats was allowed having regard to the finding that both the flats could be treated to be one house as both had been combined to make one residential unit. The said judgment, thus, proceeds on a different fact situation. “

22. It is also relevant to refer to the decision of the coordinate bench of this court in CIT v. Gita Duggal (Delhi)/2013 SCC OnLine Del 752 where this court has held as under: –

“11. There could also be another angle. Section 54/54F uses the expression “a residential house”. The expression used is not “a residential unit”. This is a new concept introduced by the Assessing Officer into the section. Section 54/54F requires the assessee to acquire a “residential house” and so long as the assessee acquires a building, which may be constructed, for the sake of convenience, in such a manner as to consist of several units which can, if the need arises, be conveniently and independently used as an independent residence, the requirement of the section should be taken to have been satisfied. There is nothing in these sections which require the residential house to be constructed in a particular manner. The only requirement is that it should be for the residential use and not for commercial use. If there is nothing in the section which requires that the residential house should be built in a particular manner, it seems to us that the Income-tax authorities cannot insist upon that requirement. A person may construct a house according to his plans and requirements. Most of the houses are constructed according to the needs and requirements and even compulsions. For instance, a person may construct a residential house in such a manner that he may use the ground floor for his own residence and let out the first floor having an independent entry so that his income is augmented. It is quite common to find such arrangements, particularly postretirement. One may build a house consisting of four bedrooms (all in the same or different floors) in such a manner that an independent residential unit consisting of two or three bedrooms may be carved out with an independent entrance so that it can be let out. He may even arrange for his children and family to stay there, so that they are nearby, an arrangement which can be mutually supportive. He may construct his residence in such a manner that in case of a future need he may be able to dispose of a part thereof as an independent house. There may be several such considerations for a person while constructing a residential house. We are therefore, unable to see how or why the physical structuring of the new residential house, whether it is lateral or vertical, should come in the way of considering the building as a residential house. We do not think that the fact that the residential house consists of several independent units can be permitted to act as an impediment to the allowance of the deduction under section 54/54F. It is neither expressly nor by necessary implication prohibited.”

23. This court in Mrs. Kamla Ajmera v. Pr. CIT Mrs. Kamla Ajmera v. Pr. CIT (Delhi)/Neutral Citation No.: 2024:DHC:9342-DB, referred to the decision in Geeta Duggal (supra), and held that in certain circumstances, multiple residential units may be considered as a single residential house for the purposes of exemption under Section 54F of the Act. The court observed as follows: –

“39. This assumes significance in the backdrop of our opinion that the word ‘a’ used in Section 54F of the Act denotes one singular residence, along with the caveat that in case the floors or houses are so constructed as to be used as one singular unit or capable of being used as such, they may fall within the definition of a residential house.”

24. The Madras High Court also held a similar view in CIT v. Gumanmal Jain ITR 666 (Madras)/2017 SCC OnLine Mad 13653.

25. The aforesaid decisions were rendered in the context of construing whether the new asset purchased is ‘a residential house’ – an expression used in Section 54 and 54F of the Act. However, the said decisions would be equally applicable for construing the term ‘one residential house’ as used in clause (i) of the proviso to Section 54F of the Act. We say so because in Pawan Arya (supra) as well as in Gita Duggal (supra) and Mrs Kamla Ajmera (supra), the term ‘a residential house’ has been construed to mean ‘one residential house’. We find it difficult to accept that, in the given facts, different floors of a house are required to be considered as multiple residential houses.

26. In view of the above, we find no infirmity with the decision of the learned ITAT in holding that the Assessee could not be denied the deduction under Section 54F of the Act on the ground that she holds more than one residential unit.

27. We also find that there has been no failure on the part of the Assessee to truly and fairly disclose all the material facts in her return. The Assessee had fairly disclosed about the sale of the original asset, in respect of which capital gains had arisen as well as about the house property purchased from the said sale proceeds.

28. The configuration of ownership of the property, as recorded in the South Delhi Municipal Corporation records for D-6/ 5, does not lead to the conclusion that there was any failure on the part of the Assessee in disclosing the material facts relevant for claiming the deduction sought by the Assessee. 29. In view of the above, we find that no substantial question of law arises for consideration of this court. Accordingly, the appeal as well as the pending application is, accordingly, dismissed. “

8. It is important to take note of the fact that assessee has relied upon these judicial precedents of various Hon’ble High Courts which were placed before the ld. Assessing Officer in the submissions made in the assessment proceedings. Ld. Assessing Officer had taken cognizance of all the submissions including the factual position corroborated by documentary evidences based on which he found the submissions satisfactory and dropped the variation proposed in his show cause notice. He thus, took one of the plausible view, based on the factual position and the judicial precedents placed before him. Ld. PCIT has taken a contrary view of treating the triplex residential house as multiple flats owned by the assessee, which is not in conformity with the provisions of section 54F, so as to render the assessment made by the ld. Assessing Officer as erroneous and prejudicial to the interest of Revenue.

8.1. It is a settled position of law, where the view taken by ld. Assessing Officer after due deliberation and examination of factual position as well as the judicial precedents, cannot be subjected to revisionary proceedings by adopting the other view. For this, we draw our force from the decision of Hon’ble High Court of Delhi in the case of CIT(A) v. Sunbeam Auto Ltd. [2011] 332 ITR 167 (Del), wherein it held that on facts and law, view taken by Assessing Officer was one of possible views and, therefore, assessment order passed by Assessing Officer could not be held to be prejudicial to the interest of Revenue. We also place our reliance on the decision of Hon’ble Supreme Court in the case of CIT(A) v. Max India Ltd. [2007] 295 ITR 282 (SC) which also covers the case of the assessee.

8.2. Considering the facts on record and the discussion made above vis-a-vis the judicial precedents relied upon, we hold that the revisionary proceedings invoked by ld. PCIT and the revisionary order passed thereafter, is not in accordance with the provisions of section 263 and is liable to be quashed. Accordingly, the impugned order is set aside and quashed. Grounds raised by assessee in this respect are allowed.

9. In the result, appeal of the assessee is allowed.

5. Since the facts are similar in the year under consideration therefore applying the principles laid down by the decision of Hon’ble Supreme Court in the case of Radhasoami Satsang v. CIT , we are also of the view that the fundamental aspect or a core finding of the fact as already been established in the earlier decision of the Coordinate Bench of ITAT and the factual position in the year under consideration is also same therefore we are bound to follow the “Doctrine of Binding Precedents” which demands that the decision of Coordinate Bench is binding therefore following judicial consistency emanating in assessee’s own case, we are of the view that invocation of provisions of Sec. 263 of the Act in the present case in view of the fact that assessee was holding more than one residential house other than new asset on the date of transfer of original asset is not sustainable in the eyes of law.

6. Even otherwise the case of the assessee was selected for scrutiny for following reasons:

| a. |

|

Salary income shown under Part B-TI is less than salary income per Annexure II of TDS return filed by all the employer |

| b. |

|

Large Capital Gains set off with large Capital Loss. |

During the course of original assessment a detailed verification of facts was already done by the AO with regard to the said issue. A detailed show cause notice dated 06.03.2024 and 07.03.2024 was issued upon the assessee wherein in response thereto assessee had filed reply dated 18.03.2024 and also filed all the required documents which were duly examined by the Ld.AO.

7. And after considering the detailed submissions and after conducting a detailed enquiry into the facts of the case, the AO accepted the claim of the assessee in the return of income filed for the year under consideration as “satisfactory” and thus made no additions which goes to show that the observation of Ld. PCIT that the order passed by AO was not based on detailed enquiries and finding of facts is not correct, whereas the AO had taken a conscious and reasonable view therefore no proceedings u/s 263 of the Act could have been initiated as had been held in the cases of:

Delhi HC in Pr. CIT, Central v. Lata Goel (Delhi),

Delhi HC in CIT v. Gita Duggal (Delhi)

Karnataka HC in CIT v. D. Ananda Basappa (Karnataka)

Madras HC in CIT v. Gumanmal Jain (Madras)

Delhi HC in Mrs. Kamla Ajmera v. Pr. CIT (Delhi)

8. Therefore considering the totality of the facts as discussed by us above and also taking into consideration the decision of the coordinate Bench in assessee’s own case, wherein the facts owned by the assessee at ‘Apar Valmark’ Bangalore were considered as ‘one residential unit’. Hence, in view of the above facts, the invocation of the provisions of Sec. 263 of the Act and orders passed thereafter are not sustainable in the eyes of law and are thus quashed. Accordingly, the grounds raised by the assessee stands allowed.

9. In the result, the appeal filed by the assessee stands allowed.