ORDER

Girish Agrawal, Accountant Member.- These are cross appeals filed by the assessee and the Revenue against the order of CIT(A)-6, Mumbai, vide order no. CIT(A)-6/IT-182/2013-14, dated 05.03.2014, passed against the assessment order by ACIT 2(3), Mumbai, u/s. 143(3) r.w.s. 147 of the Income-tax Act (hereinafter referred to as the “Act”), dated 07.02.2014 for Assessment Year 2008-09.

2. Grounds taken by the assessee are reproduced as under:

“1 The Learned Commissioner of Income-tax (Appeals) [” Ld. CIT(A)”] erred in upholding the –

(1) reopening of the Appellant’s assessment and

(2) the (Re) Assessment Order,

both of which are without jurisdiction and illegal.

1.1 Without prejudice to the generality of the foregoing, the Ld. CIT(A) erred, for the following reasons, in not holding that the reopening of the Appellant’s assessment and the (Re)Assessment Order were without jurisdiction and illegal:

(I) The Learned Assessing Officer (“Ld. AO”) had made an order of assessment instead of forwarding to the Appellant, a draft of the proposed order of assessment in accordance with the provisions of sub-section (1) of Section 144-C.

(ii) The sanction under the proviso to sub-section (1) of Section 151 of the Chief Commissioner to the issue of the Notice under Section 148 had not been obtained. or

(iii) The Ld. AO did not have any “reason to believe” that any income chargeable to tax had escaped assessment, within the meaning of Section 147.

(iv) The provisions of the first proviso to Section 147 were not satisfied, inasmuch as the Appellant had disclosed fully and truly all material facts necessary for its assessment for the year under consideration.

(v) In any event, the Ld. AO’s stated “reason to believe” that income chargeable to tax had escaped assessment did not constitute “reason to believe” within the meaning of that expression as employed in Section 147, inasmuch as such belief is unsupported by any reason (i.e. , cause or justification) [Ram Bal v CIT [1999] 236 ITR 696 (SC)].

(vi) Having regard to the fact that the period of four years from the end of the relevant assessment year referred to in the first proviso to Section 147 had expired on 31th March, 2013, the Jurisdiction of the Ld. AD to assess or reassess any Income chargeable to tax which had escaped assessment stood ousted by that first proviso.

(vii) Assuming whilst denying that there was any failure on the part of the Appellant to disclose fully and truly all material facts necessary for its assessment,

(a) no income chargeable to tax had escaped assessment and

(b) even assuming (whilst denying) that any Income chargeable to tax had escaped assessment, such escapement was not by reason of any such failure.

2. Disallowance of Interest Paid on Borrowed Capital Utilised for Acquisition of Equity in Corus Group plc, United Kingdom

The Ld. CIT(A) erred in upholding the Ld. AO’s disallowance of a sum of Rs.518,75,84,534, representing Interest Paid on Borrowed Capital utilised by the Appellant for acquisition during the previous year relevant to the Assessment Year 2008-09, of equity in Corus Group plc, United Kingdom, as and by way of extension of the Appellant’s existing steel business and hence claimed by the Appellant as deductible under Section 36(1)(iii).

2.1 Without prejudice to the foregoing ground, the Interest amounting to Rs. 518,75,84,534 ought to have been allowed under Section 57(iii).”

2.1. Grounds taken by the revenue are reproduced as under:

On the facts and in the circumstances of the case and in law, the learned CIT (A) has erred in allowing relief to the assessee to the extent impugned in the grounds enumerated below:

5. The order of the CIT(A) is opposed to law and facts of the case.

6. On the facts and in the circumstances of the case and in law, the Ld. CIT(A) erred in directing the Assessing Officer to delete the addition of Rs 871,17,30,496/- based on show cause notices issued by the Government of Orissa for “Excess / illegal” mining, without appreciating the detailed facts brought on the record by the Assessing Officer.

3. Before we delve on the issue, brief facts of the case are that assessee is a Public Limited Company engaged in the business of manufacturing and trading in steel. Original return of income was filed on 29.09.2008, reporting total income at Rs. 6378,97,49,808/- under the normal provisions of the Act. Assessee also reported its taxable book profit at Rs. 6893,80,27,405/- u/s. 115JB of the Act. Case of the assessee was selected for scrutiny assessment u/s. 143(3) and the assessment was completed wherein total income was assessed at Rs. 6538,90,17,034/- after making certain disallowances and additions. Subsequently, case of the assessee was reopened by invoking the provisions of section 147 r.w.s 148. For this, reasons to believe were recorded by the ld. AO alleging that income has escaped assessment.

On this account, he noted that assessee had done excessive mining during the year under consideration and the details of excess mining and resulting profit thereon were not disclosed in the course of original assessment proceedings. According to him, income relating to alleged excessive mining escaped assessment.

3.1. The other reason recorded mentions in reference to assessment proceedings of AY 2009-10 that assessee had borrowed money to invest in Corus Group PLC (‘Corus), a foreign subsidiary. According to the ld. AO, interest expense on such borrowing was claimed as business expenditure by the assessee in its profit and loss account. However, since business income of the foreign subsidiary is not assessed in India nor it is a resident in India and, therefore, interest expenditure was disallowed in the assessment proceedings for AY 2009-10. In view of this, similar disallowance needs to be made in the year under consideration as it has escaped assessment.

3.2. The reasons to believe so recorded by ld. AO are reproduced below for ready reference as contained in the impugned re-assessment order.

The assessee was issued show cause notices from Government of Orissa for excess mining. The same were asked to be produced during assessment proceedings of A.Y. 2009-10 which the assessee submitted. It is seen from the show cause notices issued to the assessee that the assessee has done excessive mining during F.Y. 2007-08 (A.Y. 2008-09) as follows:

| Sr. No. |

Location |

Date of show cause notice |

Amount in (Rs) |

| 1. |

Joda West |

30.10.2012 |

840,58,24,000 |

| 2. |

Bamebari |

30.10.2012 |

11,70,96,000 |

| 3. |

Manmora |

30.10.2012 |

83,63,936 |

|

|

Total |

853,12,83,936 |

The details of excess mining and the resulting profits were not disclosed by the assessee during assessment proceedings of A.Y. 2008-09. It is therefore obvious that income relating to above mining is not disclosed by the assessee.

It was also found during the assessment proceedings of AY 2009-10, that the assessee has borrowed money to invest in the Corus Group Ple a foreign subsidiary. The interest expense of such borrowing is claimed as business expenditure by the assessee in its P & L A/c. The business income of the foreign subsidiary is not assessed in India neither is it a resident in India. Accordingly, for the detailed reasons stated in the assessment order the interest expenditure was disallowed. Similar disallowance also needs to be made for this AY.

Hence, I have reason to believe that income has escaped assessment within the meaning of section 147 of the I.T. Act.

The escapement of income/ under assessment of income is due to the fact that the assessee did not disclose the correct facts as stated in the above paras for the purpose of assessment. Further the escapement of income/ under assessment of income is more than Rs. 1 lakh. A notice under Section 148 is therefore issued to bring to tax escaped income attributable to above excess mining as well as any other income which may be found to have escaped assessment as referred to in Explanation 3 to Section 147 of the IT Act, 1961.

Approval for the issue of notice u/s 148 is obtained from CIT-2, Mumbai, as per Section 151″

4. Both assessee and Revenue are in appeal before the Tribunal for the same assessment year, but on different issues. We first take up appeal filed by the Revenue wherein, the sole issue raised is in respect of relief granted by ld. CIT(A) for the addition of Rs. 871,17,30,496/-made by the ld. AO which was based on show cause notices issued by the Government of Odisha for excess/illegal mining.

4.1. On the ground raised by the Revenue in its appeal, fact of the matter is that assessee had been issued show cause notices by the Government of Odisha as to why penalty on excessive mining done by the assessee should not be levied. As per the said notices of the Government of Odisha, assessee had done excessive mining for the year under consideration, details of which is tabulated below:

| AY 2008-09 |

As per Government of Orissa |

|

Name of Mineral |

Actual Production |

Avg. Sale Price |

Excess production in MT |

Amount in (Rs.) (of excess production) |

|

A |

B |

C |

D |

E |

| Joda West |

Iron |

56,000 |

1,722 |

56,000 |

9,64,32,000 |

|

Mn |

7,42,000 |

12,292 |

6,76,000 |

830,93,92,000 |

| Bamebari |

Iron |

68,000 |

1,722 |

68,000 |

11,70,96,000 |

|

Mn |

|

|

|

0 |

| Monmora |

Iron |

4,800 |

1,722 |

4,800 |

82,65,600 |

|

Mn |

8 |

12,292 |

8 |

98,336 |

|

Total |

|

|

|

853,12,83,936 |

4.2. On the above, ld. AO sought explanation from the assessee as to whether the excess/illegal mining as stated by the Government of Odisha has been accounted in its books of account and taken into stock or not. Assessee furnished its detailed explanation by putting on record the factual position corroborated by documentary evidence and the applicable laws. After considering the submissions made by the assessee, ld. AO came to the conclusion that certain quantity of minerals and income thereon remained unaccounted. Details in this respect is tabulated as under:

|

Name of Mineral |

Actual Production (As per Col B of Table A) |

Avg. Sale Price (As per Col C of Table A) |

Value of unaccounted minerals [E*C] |

Quantity [MT] accounted in Assessee’s books as per auditors |

Unaccounted quantity of minerals [B-D] |

|

A |

B |

C |

D |

E |

F |

| Joda West |

Iron |

56,000 |

1,722 |

0 |

56,000 |

9,64,32,000 |

|

Mn |

7,42,000 |

12,292 |

50,762 |

6,91,238 |

849,66,97,496 |

| Bamebari |

Iron |

68,000 |

1,722 |

0 |

68,000 |

11 7,0,96,000 |

|

Mn |

|

|

|

0 |

0 |

| Monmora |

Iron |

4,800 |

1,722 |

0 |

4,800 |

82,65,600 |

|

Mn |

8 |

12,292 |

558 |

-550 |

-67,60,600 |

|

Total |

|

|

|

0 |

871,17,30,496 |

4.3. Ld. AO thus, concluded that profits on the excess/illegal materials production remained unaccounted for which he made an addition of Rs. 871,17,30,496/-.

5. Before the ld. CIT(A), extensive details were furnished along with additional evidences for which remand report was called from the ld. AO. He took note of the fact that ld. AO in his remand report had stated that quantity of production of each type of ore determined in the applicable Purported Notices (PNs) is in agreement with the quantity of production of such ore certified and/or returned in the corresponding accounting return, filed by the assessee with the Odisha mining authorities, during the relevant year, forming part of the records of the assessee. Ld. CIT(A) also took note of the decision of ld. Dispute Resolution Panel (DRP) in assessee’s own case for Ays 2009-10 and 2010-11 wherein, ld. DRP on identical facts and circumstances had deleted the addition in respect of excess mining profits proposed by the ld. AO in the draft assessment order.

5.1. He also placed reliance on the decision in assessee’s own case for Ays 2006-07 and 2007-08 wherein addition on this issue was deleted by himself at the first appellate stage. Considering similarity of the issue with the present case, ld. CIT(A) deleted the addition made by the ld. AO against which revenue is in appeal before Tribunal.

6. Before us, at the outset, ld. Counsel for the assesssee referred to the decision in assessee’s own case by the Co-ordinate Bench of ITAT, Mumbai for Ays 2006-07 and 2007-08 in ITA No. 3553 & 3554/Mum/2016 dated 22.09.2023, whereby appeal filed by the revenue was dismissed, holding it in favour of the assessee. It was pointed out that ld. CIT(A) had relied on the first appellate order for Ays 2006-07 and 2007-08 which has now been affirmed by the Co-ordinate Bench of ITAT, Mumbai (supra).

6.1. We have perused the order of the Co-ordinate Bench to take note of the similarity in the factual position and the applicable law on the issue raised by the revenue before us. Nothing has been brought on record by the revenue to controvert the finding so arrived at by the Co-ordinate Bench in assessee’s own case (supra). Relevant observations and findings of the Co-ordinate Bench as contained para 6 are extracted below for ready reference:

“6. We have heard the submissions made by rival sides and have examined the orders of authorities below. The solitary ground raised by the Revenue in appeal is against the findings of the CIT(A) in deleting addition of Rs.276,34,81,218/-, based on show cause notice issued by the Government of Odisha for excessive mining of minerals and ores. During the course of First Appellate proceedings, the assessee placed on record PN issued by the Mining Authorities, wherein quantities of alleged excessive mining were substantially reduced. The CIT(A) forwarded the additional evidence filed by the assessee to Assessing Officer for his comments. The Assessing Officer vide letter dated 28/12/2015 furnished his report wherein he after verifying the quantities and value of mineral ore production as per PN came to the conclusion that the quantity of production/mining of ores mentioned in the PN corresponds to Auditors’ Certificate and return filed by the assessee with the Orissa State Mining Authorities. For the sake of completeness relevant extract of the remand report is reproduced herein below:

2.3 it will be noted from the above Table that the quantity of production of each type of ore determined in the applicable PN is in agreement with the quantity of production of such ore certified in the corresponding Auditors’ Certificate and/or returned in the corresponding Mining Return filed by the assessee with the Odisha Mining Authorities during the relevant year and forming part of the records of the assessee. Further, Auditors have certified that the said production is recorded in the assessee’s books of account”.

The CIT(A) on the basis of remand report deleted the addition. The CIT(A) has further placed reliance on the decision of DRP in assessee’s own case for Assessment Years 2009-10 and 2010-11, wherein on identical set of facts the DRP has deleted the addition in respect of alleged profits from excessive mining. No material has been placed on record by the Revenue to controvert the findings of the CIT(A). We find no reason to interfere with the findings of CIT(A) on this issue.”

6.2. In the given set of facts and circumstances as well as the judicial pronouncement in assessee’s own case along with meritorious findings arrived at by the ld. CIT(A) based on remand report obtained from the ld. AO, we do not find any reason to interfere with the findings so arrived at by the ld. CIT(A) whereby addition made by the ld. AO was deleted. Accordingly, ground raised by the revenue in this regard is dismissed.

7. In the result, appeal of the revenue is dismissed.

8. We now take up appeal filed by the assessee, whereby it is contesting both on the legal aspect and merits of the case.

9. We have heard both the parties at length and perused the material placed on record including tabulated details, judicial precedence and paper books. We place on record our appreciation both, of the ld. Counsels for the assessee and the ld. CIT DR for their effective representation in assisting the bench to take up this matter. Submissions made by both the parties are duly considered and dealt by us while adjudicating the issue. Therefore, the same are not narrated separately for the sake of brevity and to avoid repetition.

9.1. Ld. Counsel for the assessee Sr. Advocate Shri J.D. Mistry laid more emphasis on the merits of the case than on the legal aspect of challenging the reopening and the re-assessment order passed thereafter. Within the grounds on the merits of the case, assessee has made an alternative claim without prejudice, by resorting to allowability of deduction u/s. 57(iii) of the Act.

10. Before we delve on the issue, we take note of the factual matrix of the transaction under taken by the assessee for claiming deduction of interest expenditure on borrowed capital u/s. 36(1)(iii) of the Act. During the year, assessee had debited interest expenditure of Rs. 813,64,79,407/- in its profit and loss account and claimed it as revenue expenditure in the return of income filed by it. Ld. AO noted that interest expenditure of Rs. 518,75,84,534/- out of the above stated amount was towards capital raised for investment by the assessee in its overseas subsidiary Corus Group PLC (Corus) UK, to acquire it.

10.1. In this regard, ld. AO observed that business income of the foreign subsidiary i.e. Corus is not assessed in India nor it is a resident of India. On this premise, he contended that the interest expense claimed by the assessee ought to be treated as capital expenditure and therefore, not allowable while computing the business income for the year. According to him, investment is made by the assessee only for acquiring and maintaining “controlling interest” in Corus and not with the motive of business consideration. He further observed that assessee has shown the shares so acquired of Corus as “investment” in its books of account which indicates that assessee is not in the business of investment. According to him, since assessee is not earning any income under the head “business and profession” from the said investment, the interest expense cannot be allowed as business expenditure.

10.2. He thus, formed the view that there is no connection of business in the said investment and therefore, it is not for the purpose of business. On this basis, he thus, concluded that interest expenditure claimed by the assessee is cannot be allowed as a business expenditure. He referred to the judicial precedence in the case of Tata Sons Limited for AY 2009-10 which is the parent company of the assessee to buttress his view.

10.3. In respect of the alternate claim made by the assessee for the allowability u/s. 57(iii), ld. AO’s contention is that since assessee has not invested in Corus to earn dividend, but to acquire the controlling interest and management of the said company, interest expenditure u/s. 57(iii) is not allowable. For this he placed reliance on the decision of the Hon’ble jurisdictional High Court of Bombay in the case of CIT v. Amritaben R. Shah (Bombay). He thus, concluded by taking an adverse view to make the disallowance of interest expenditure amounting to Rs. 518,75,84,534/- and added it to the total income of the assessee.

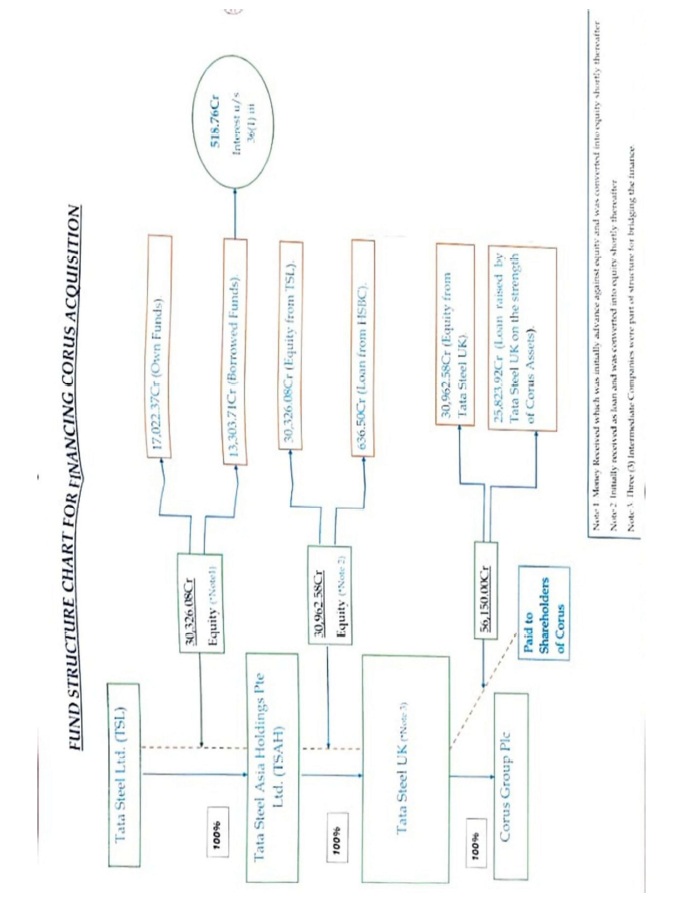

11. It is important to take note of the financing structure of the transaction undertaken by the assessee for acquiring Corus during the year. From the material on record, it is gathered that assessee for the purpose of acquiring Corus, the financing structure under taken by it was that of Leverage Financing (LF) i.e. a combination of own cash resources and syndicated loans. Assessee contributed funds as equity into its 100 percent wholly owned subsidiary “Tata Steel Asia Holding Pte Limited Singapore” (TSAH). Apart from this equity receipt by TSAH, loans were also raised in this entity without recourse to the assessee and cumulatively, all funds were invested by way of equity in Tata Steel UK Limited which acquired Corus Group PLC i.e. the target company. TSAH is the 100% wholly own subsidiary of the assessee. Tata Steel UK Ltd in turn is the 100% wholly own subsidiary of TSAH, who in turn acquired the Corus with its 100% holding. To better understand the financing structure adopted by the assessee for the purpose of acquisition of Corus, a pictorial representation is extracted below as furnished by the assessee:

11.1. From the above, it is noted that assessee infused its own funds of Rs. 17,022.37 Crores and borrowed funds of Rs.13,303.71 Crores, totalling to Rs. 30,326.08 Crores which were infused in TSAH as equity. It is on these borrowed funds of Rs. 13,303.71 Crores that assessee has claimed deduction towards interest expenditure of Rs. 518.76 Crores u/s. 36(1)(iii). This interest component is referred to as ‘Corus Interest’. On receipt of this equity capital from the assessee, TSAH further raised loans on its own accord amounting to Rs. 636.50 Crores, leading to total available funds with it of Rs. 30,962.58 Crores which was infused as equity in Tata Steel UK Limited. On receipt of this equity of Rs. 30,962.58 Crores, to meet the balance amount to Rs. 25,823.92 Crores, Tata Steel UK Limited raised loans on the strength of asset of Corus thus, totalling to Rs. 56,150 Crores for the purpose of acquiring Corus by making payments of this amount to the shareholders of the Corus.

11.2. According to the assessee, Corus interest was paid on funds borrowed for extension of assessee’s existing steel business by acquiring the shares of Corus which was in the same line of business i.e. steel. Particulars of interest paid by the assessee which has been debited to its profit and loss account for the year under consideration and claimed as a deduction while computing the total income is tabulated below:

| Particulars |

Interest (Rs.) |

| Interest in IFC Loans, Washington with swaps |

110,01,76,958 |

| Interest on USD 750 Million from SCB |

217,03,26,319 |

| Interest on USD 500 Million from SCB |

126,04,06,739 |

| Interest on SBI – Rs.2,500 Crs. |

45,30,82,191 |

| Interest on 875 Million USD – 1% CARS |

20,35,92,326 |

| Total |

518,75,84,534 |

11.3. Case of the assessee is that interest expenditure incurred by it is for the purpose of business and hence, allowable expenditure within the meaning of section 36(1)(iii). Facts relating to financing structure as detailed above and the investment made by the assessee including that by the step down wholly own subsidiaries for acquisition of equity in Corus are not in dispute. The entire issue is centered on provisions contained in section 36(1)(iii) for which relevant extracts are as under:

36. (1) The deduction provided for in the following clauses shall be allowed in respect of the matter dealt with therein, in computing the income referred to in section 28.

(i)…….

(ia)……

(b)….

(ii)….

(iia)…..

(iii) The amount of the interest paid in respect of capital borrowed for the purposes of the business or profession.

11.4. From the above provisions, we note that allowability of interest depends on utilization of the borrowed capital, that is for the purposes of business or profession or not.

11.5. The moot point which needs to be catered to for considering allowability is “the purpose of the business or profession”. In order to explain and establish that the purpose of this acquisition of Corus by the assessee is for its business, reference is made to the minutes of Board of Directors of the assessee including the presentation made therein which were all placed in the course of assessment proceedings before the ld. AO. From the minutes of the meeting of the board of directors of the assessee held on 12.10.2006, we take note of certain factual position which were considered in the said meeting whereby the Chairman informed the board that it had been contemplating and exploring the possibilities of acquisition of large size steel plants at selected location. In this regard, amongst other target companies, Corus was also considered as a probable acquisition. It is stated in the minutes whereby Chairman mentioned that if the acquisition is completed, an Integration Committee would be formed to bring synergy in operations and financial system between the assessee and the acquired company.

In this regard, Managing Director of the assessee made a detailed presentation on the overview of Corus and significant synergies which would entail between Corus and assessee, if the acquisition materializes. Minutes also include detailed discussion in respect of investment structure, financing for the acquisition and regulatory issues in this regard. In the same meeting, the board approved formation/acquisition of Special Purpose Vehicles (SPVs) as wholly own subsidiaries to address the financing structure for the acquisition of Corus.

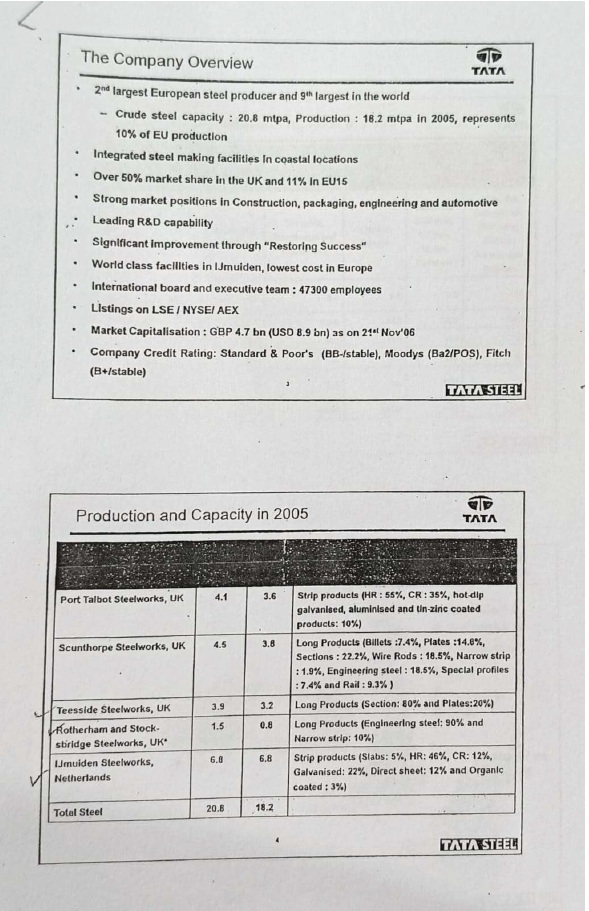

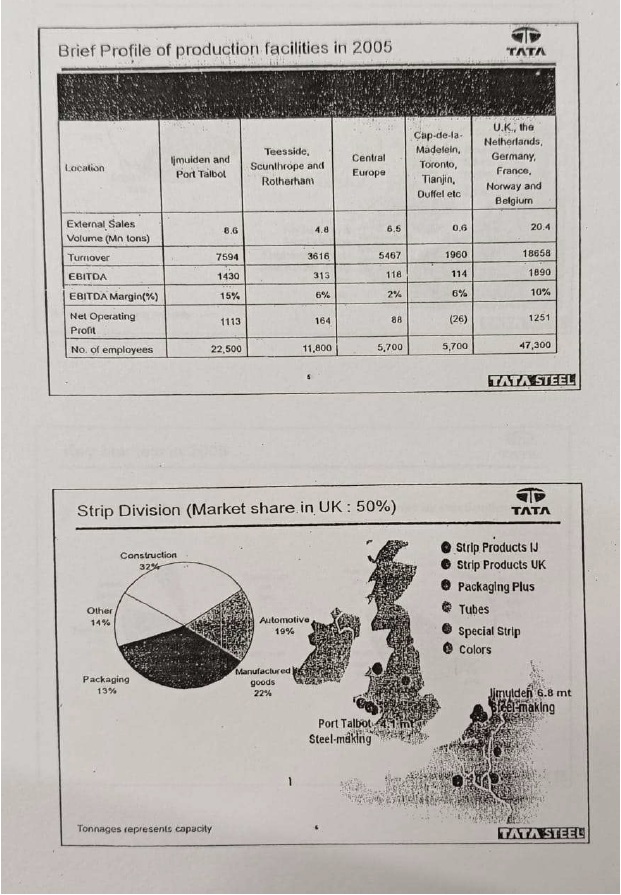

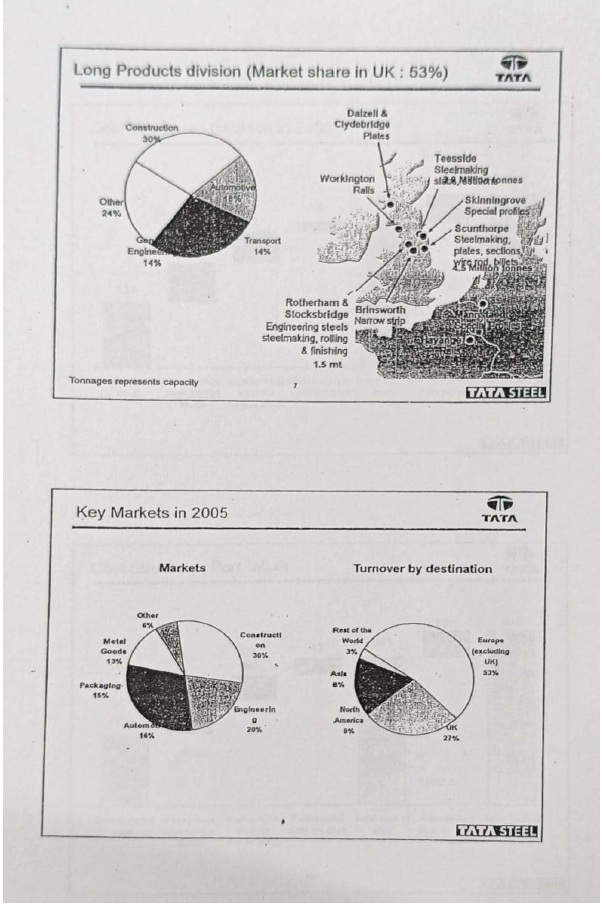

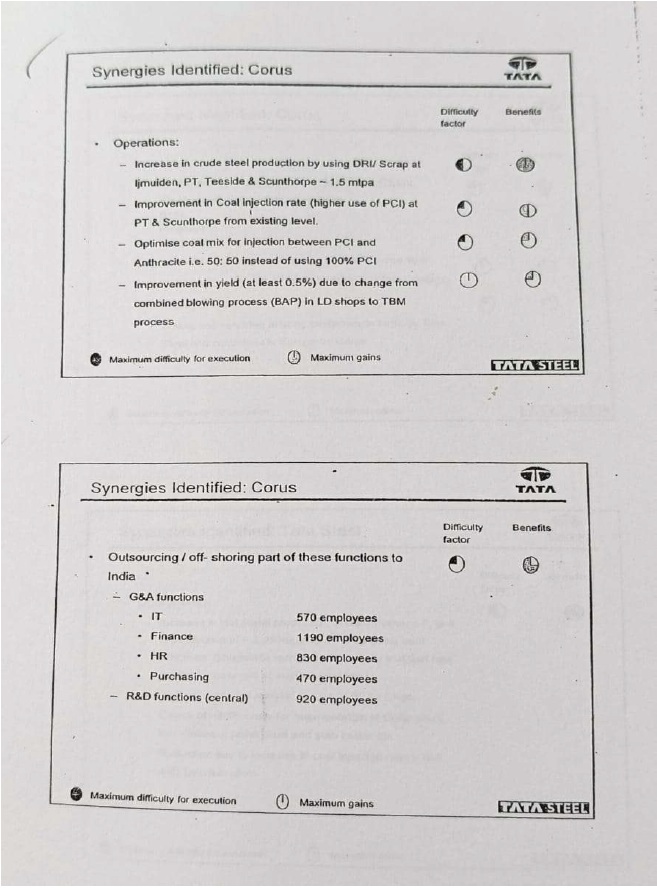

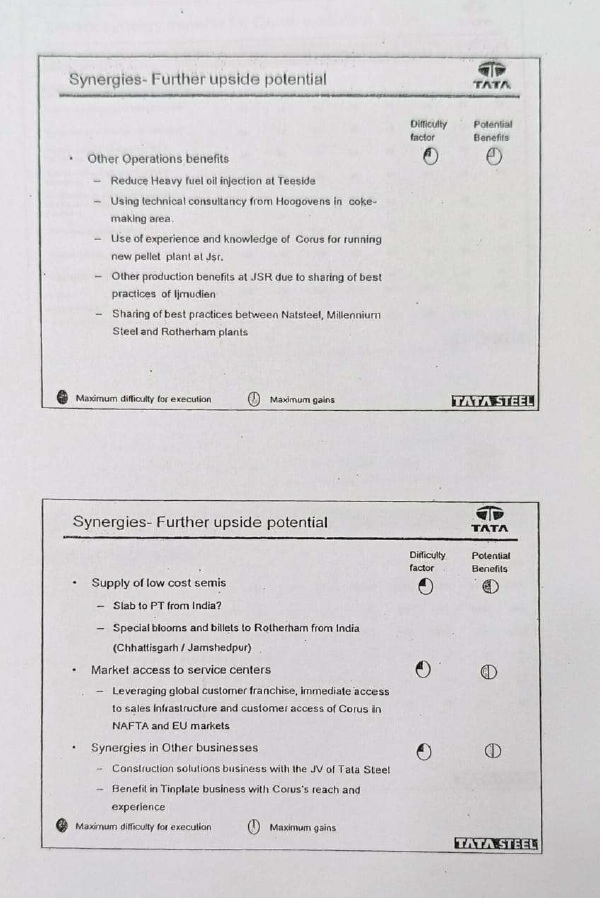

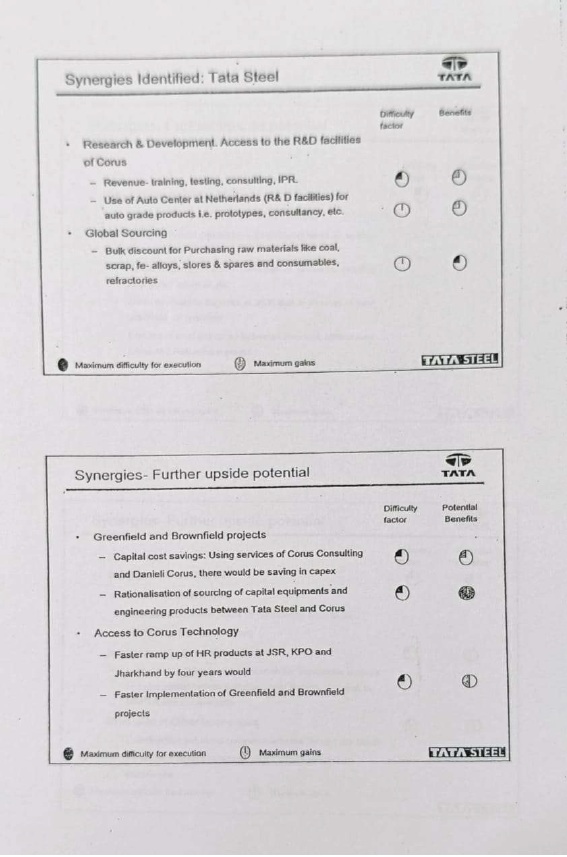

11.6. We felt necessary to go through the presentation made by the Managing Director of the assessee in its board meeting, copy of which is placed in the paper book. This was made available before the ld. AO also. From the perusal of the same, it highlights the overview of Corus which is engaged in the similar line of business in which the assessee is also operating. These highlights points out that Corus then was the 2nd largest European steel producer and 9th largest in the world. It had integrated steel making facilities in costal locations with over 50% market share in the UK and 11% in EU15. It had leading R&D capabilities and world class facilitates at certain locations with employee strength of 47,300. This presentation also highlights the production and capacity of Corus at its different locations giving breakup of market share, cost structure as well as details of sourcing of raw material. It throws light on the synergies which were identified for the purpose of acquiring Corus as to what it would bring to the business of the assessee in terms of operations and other general administrative as well as R&D functions. Some of the relevant slides of the presentation are extracted below which gives an understanding of the mind of the board of directors of the assessee for the purpose of venturing into this acquisition of Corus:

11.7. With the above stated objectives of reaching out to overseas market and for the expansion of assessee’s own existing business, assessee ventured into acquisition of Corus by acquiring its equity shares through its wholly owned step-down subsidiaries. Since assessee resorted to Leverage Financing i.e. combination of own cash resources and syndicated loans, while augmenting the syndicated loans, assessee had affront made disclosures and announcements on the purpose for which the loans were being syndicated. In this respect, a reference is made to one of the Corporate Loans Agreement entered into between the assessee and State Bank of India vide agreement dated 28.01.2008 which in its recitals at clause (A) mentions that assessee is seeking financial assistant in the form of corporate loan for the purpose of infusing funds in the form of equity or subordinated shareholders loans into TSAH, a wholly own subsidiary of assessee which in turn will use the same for repayment of the loans contracted by TSAH for acquiring Corus. Clause 2.2.2 specifically defines the draw-down and utilization of the loan proceeds on the above stated lines. Reference is also made to 1.00% Convertible Alternative Reference Securities due 2012 (CARS), convertible into qualifying securities or ordinary shares of assessee, issued by the assessee wherein also, use of proceeds is stated to be for investment in its direct or indirect wholly owned subsidiaries by way of equity investments or subordinated intercompany loans (both convertible and non-convertible) to be applied to, or towards the financing or refinancing of debts incurred in connection with the acquisition of the shares of Corus.

11.8. Thus, assessee made prior announcement while syndicating loans which was for the purpose of acquisition of Corus which would lead to avail opportunities to diversify, have access to mature markets and leverage superior technology of Corus. On the above factual position enumerated by the assessee, backed by corroborative documentary evidences placed on record, strong reliance was placed by it on the decision of Hon’ble jurisdictional High Court of Bombay in the case of PCIT v. Concentrix Services (P) Ltd. (Bombay) wherein it was held that interest incurred on loans taken for acquiring controlling interest of same line would be allowable expenditure u/s. 36(1)(iii). Substantial question of law no. 3 before the Hon’ble Court dealt with the issue before us which is extracted below:

“Whether on facts and in the circumstances of the case and in law, the Tribunal was justified in directing the AO to delete the disallowance u/s 36(1)(iii) of the IT Act, 1961 without appreciating the fact that the acquisition of business by way of investing into shares of that company through either Special Purpose Vehicle or directly cannot be considered to be ordinary event of the business and therefore, cannot be termed as expenditure incurred for the purpose of assessee’s business, which is providing ITeS services?”

11.9. While answering the aforesaid substantial question of law, Hon’ble Court took note of facts which are similar to the present case before us. It referred to the findings of the Tribunal whereby it found on facts that assessee wanted to expand its business operations and it was for the purpose of extension of its business, it acquired shares in the overseas company which was taken to be for the purpose of business. Hon’ble Court took note of the observation of the Tribunal that for the purpose of extension of business three ways available are, viz.

| (i) |

|

Set up a branch in overseas country |

| (ii) |

|

To form new companies in overseas country |

| (iii) |

|

Acquire company operating in the overseas country in the similar line of business |

11.10. Choosing one of these three options is the business decision and is the sole prerogative of the assessee. In the given case, assessee opted for the third method whereby it created a SPV to acquire the overseas entity from its existing shareholders, for which it borrowed capital and incurred interest costs, claiming deduction u/s. 36(1)(iii) of the Act. Before the Hon’ble Court, revenue had contested on similar lines as in the case before us whereby it was submitted that assessee was not in the business of investment of shares, but was in the business of Information Technology enabled Services (ITeS), BPO and call centers and therefore, interest expenditure is not allowable. Hon’ble Court took note of the factual position that business of the assessee and that of the entity to be acquired are in the similar line of business.

11.11. It noted that it is the business decision of the assessee to enhance or expand its activities and presence in the world market for which it acquired controlling interest in the overseas entity which was in the same line of the business as that of the assessee. Thus, it upheld the view of the Tribunal whereby the stand taken by the ld. AO was negatived who had held that primary object of acquiring shares was only to acquire controlling interest in the overseas entity. Hon’ble Court noted that funds were borrowed so as to expand the business activities of the assessee in the overseas country by acquiring the overseas entity which is the purpose for which the loan was taken. According to the Hon’ble Court, it is a finding of fact which has not been shown to be perverse. According to it, since it is essentially a finding of a fact, it did not give rise to any substantial question of law and therefore, the appeal by the revenue was dismissed, holding in favor of the assessee. From the above, what comes out is that the purpose of business as contemplated in section 36(1)(iii) is essentially, a finding of fact to be established in a given case.

12. Ld. CIT DR, Shri Ajay Chandra candidly submitted that the facts relating to the entire transaction in terms of borrowing of funds and its deployment through step down wholly owned subsidiaries and acquisition of equity shares of Corus are not in dispute. In his submissions, he laid emphasis on the proposition that “purpose” as contemplated in section 36(1)(iii) is not relevant in view of decision of Hon’ble Supreme Court in the case of Maxopp Investment Ltd. v. CIT (SC), though this judgement was delivered in the context of disallowance u/s.14A r.w.r. 8D. He referred to “dominant purpose test” which was analysed by the Hon’ble Court while dealing with the provisions of section 14A to decide as to what interpretation is to be given to the words “in relation to” where the dividend income on the shares is earned though the dominant purpose for subscribing in those shares of the investee company was not to earn dividend. Hon’ble Court opined that the dominant purpose for which the investment into shares is to be made by the assessee may not be relevant. According to it, dominant purpose does not appear to be a relevant factor in determining the issue at hand. In reference to the above, ld. CIT DR contended that the income which the assessee would yield out of making its investment by acquiring equity shares of Corus through its step-down subsidiaries would be only dividend in nature, falling under the head “income from other sources” only. According to him, once the income stream from such an investment made by the assessee goes under the said head of income, then the deduction can also be allowed only under the section relevant to the said head, i.e., section 57(iii). Further, by referring to the provisions of section 57(iii), he contended that since it is a case of capital financing, therefore, even under this section, no deduction would be permissible as it clearly carves out an expenditure being in the nature of capital expenditure for its allowability. He thus, emphasised that stance taken by the authorities below is a correct stance to be upheld.

12.1. He also referred to the decision of Hon’ble jurisdictional High Court of Bombay in the case of Amritaben R. Shah (supra) which dealt with the provisions of section 57(iii) for allowability of interest on loans raised by the assessee for acquiring shares in another company with the intention to acquire control over the said company. In the facts of this case, as observed by the Hon’ble Court that the shares in question were purchased by the assessee for the purpose of acquiring controlling interest in the company and not for earning dividend, the expenditure by way of interest on loan taken by the assessee for the said purpose cannot be held to be an expenditure incurred wholly and exclusively for the purpose of earning dividend income. It was, thus held that claim of interest expenditure would not be allowable as a deduction u/s.57(iii). Hon’ble Court made an observation in para 6 of this decision while comparing with the provisions of the section 57(iii) with that of section 37(1) to deal with the expressions “such income” as contained in section 57(iii) and the expression “for the purpose of business” in section 37(1). It noted that the expression “for the purpose of business” is narrower than the expression “for the purpose of making or earning such income”. According to the Hon’ble Court, for admissibility of an expenditure u/s.57(iii), it is necessary that primary motive of incurring it is directly to earn income falling under the head “income from other sources”. Such is not a case u/s.37 which allows deduction of expenditure “incurred wholly and exclusively for the purposes of business”. These observations of Hon’ble Court have significant relevance to deal with the issue before us, while adjudicating on the issue where the claim is made u/s.36(1)(iii) which also uses the expression “for the purpose of business of profession”.

12.2. Ld. CIT DR also pointed out that decision of the Hon’ble jurisdictional High Court of Bombay in the case of Concentrix Services (supra) relied upon its own earlier decision in the case of CIT v. Srishti Securities (P.) Ltd. (Bombay) wherein the ‘purpose test’ was dealt with prior to the decision of Hon’ble Supreme Court in the case of Maxopp Investment (supra). On this contention of ld. CIT DR, we observe and note that decision of Concentrix Services (supra) dated 04.09.2019 is subsequent to the judgement in Maxopp Investment (supra) which is dated 12.02.2018. Also, we note that decision relied upon by ld. CIT DR in the case of Amritaben R. Shah (supra) is of much prior period dated 20.04.1999. In the decision of Amritaben Shah, on the factual footing, the purpose identified was acquiring controlling interest in the company and not for earning dividend. It was on this fact that the Hon’ble Court held that deduction is not allowable u/s.57(iii) since expenditure was not for the purpose of earning income by way of dividends.

13. In the present case before us, claim of the assessee is u/s.36(1)(iii) for which it had announced its purpose publicly while syndicating borrowings for the purpose of acquiring the equity shares of Corus. Claim of assessee u/s.57(iii) is without prejudice and in the alternate. Also, referring to para 32 of Maxopp Investment (supra), important observation by the Hon’ble Court is taken note of for the present case before us which mentions that “if an expenditure incurred has no casual connection with the exempted income, then such an expenditure would obviously be treated as not related to the income that is exempted from tax, and such expenditure would be allowed as business expenditure”. Entire dispute in the present case before us is in reference to the expression “for the purpose of business of profession” as contained in section 36(1)(iii). Before us, it is not a case of earning passively by making investment of surplus funds or looking out for capital appreciation or earning of dividends. Further, in para 34, fact that dividend income is non-taxable is noted by the Hon’ble Court which is not a case before us wherein dividend income, if any, arising in the hands of the assessee would be a taxable income, being dividend from a foreign company, through step-down subsidiaries. In this regard, Hon’ble Court has observed in para 32 as extracted above, that if there is no ‘casual connection’ of the expenditure incurred with the exempt income then, such expenditure would be allowed as a business expenditure. Thus, what is essential is ‘the connection’. Even the decision of Amritaben R. Shah (supra) mentions that expression “for the purpose of business” is narrower as section 37 allows deduction of expenditure “incurred wholly and exclusively for the purposes of the business”. The subsequent decision in the case of Concentrix Services (supra) also held that ‘it is essentially a finding of fact’ that the loan was taken for the purpose of business with a business decision to expand the business activities in another geography.

13.1. We also refer to the decision of Hon’ble High Court of Punjab and Haryana in the case of CIT v. Majestic Auto Ltd. (Punjab & Haryana) wherein assessee manufacturing mopeds entered into negotiation with a foreign company in order to expand its business, which company insisted on equity participation and in the financial management, tribunal found that the expenses had been incurred in the course of business of the assessee and also had nexus with the existing business and rightly allowed it as revenue expenditure which was upheld by the Hon’ble Punjab & Haryana High Court.

13.2. We also refer to the decision of Hon’ble High Court of Delhi in the case of CIT v. Dalmia Cement (P.) Ltd. (Delhi) wherein it held that once it is established that there was nexus between the expenditure and the purpose of the business, the revenue cannot justifiably claim to put itself in the armchair of the businessman or in the position of the Board of Directors and assume the role to decide how much is the reasonable expenditure having regard to the circumstances of the case. Hon’ble Court noted that the authorities must look at the matter from the point of view of a prudent businessman on commercial expediency. It held in para 35 that “However, where it is obvious that a holding company has deep interest in its subsidiary, and hence if the holding company advances borrowed money to a subsidiary and the same is used by the subsidiary for some business purposes, the assessee would, in our opinion, ordinarily be entitled to deduction of interest on its borrowed loans”. This decision was considered by the Hon’ble Supreme Court in its decision of S.A. Builders Ltd. v. CIT (Appeals) (SC) wherein it observed that the transfer of borrowed funds has to be viewed from the point of view of commercial expediency and not from the point of view of whether the amount was advanced for earning profits. These two decisions were off late considered by the Hon’ble Supreme Court in a recent decision in the case of Sharp Business System v. CIT ITR 509 (SC) while dealing with the issue on allowability of interest on borrowed funds. In this case, according to the Assessing Officer, interest on money borrowed for investment can be allowed against income from investment. But, if the shares are acquired, not as an investment for earning income but to acquire controlling interest in a company, it would not be entitled to deduction of interest on borrowing. If the dominant purpose of expenditure was not for earning profit but to acquire controlling interest, it could not be allowed as a deduction. As a result, interest @ 13% on investment made in the subsidiary company was not allowed as a deduction. Total disallowance out of interest payment was worked out at Rs. 3,36,32,300/. On appeal, Tribunal observed that since the investment was made for controlling interest in the sister concern, assessee was entitled to the claim of allowance of the interest as investment was made in the shares of the sister company with a similar line of business and for commercial expediency. Thus, no disallowance was warranted under section 36(1)(iii) of the Act. Tribunal in this judgment while adjudication on the issue, by following the decision in the case of S.A. Builders Ltd. (supra) had directed the Assessing Officer to allow the claim of the assessee in respect of interest on borrowed fund since the advances were made for the purposes of commercial expediency. Hon’ble Court agreed with the finding so recorded by the Tribunal and affirmed by the High Court as the investment was clearly for commercial expediency.

14. We have already elucidated on the business decision of the assessee about acquiring Corus by referring to its minutes of Board of Director including presentation made therein, part of which is captured in the above paragraphs. Keeping these in juxtaposition, along with comprehensive disclosures to the outside world made by the assessee for its investment in Corus while syndicating finance, what emanates as the purpose of acquisition of the assessee is to reach out overseas market by expanding existing steel business. As already demonstrated through its presentation made by the assessee while contemplating acquisition of Corus that it was a leading steel company with manufacturing capabilities in different locations of Europe, post its acquisition, assessee emerged as the 6th largest steel manufacturer in the world with an advantage on its side of being lowest cost steel producer in the world which had been catering mainly to the domestic market until the said acquisition transpired.

15. It is important to deliberate on the nuances of the corporate world where business growth and expansion are led either organically or inorganically. In the manufacturing context, organic and inorganic expansion are fundamentally different in risk profile, capital structure impact, speed, and control. In our understanding, ‘organic growth’ means expanding using internal resources, without acquiring another company. Typical organic strategies in manufacturing will include, but not limiting to –

| (a) |

|

Capacity expansion (brownfield or greenfield) |

| (b) |

|

Launching new products |

| (c) |

|

Geographic expansion through new distribution |

| (e) |

|

Increasing plant utilization |

| (g) |

|

Sales force expansion |

15.1. Brownfield expansion refers to expanding the existing plant by adding new production lines or increasing capacity at current facilities. Whereas, greenfield expansion includes building new facility in a new geography, that is setting up a new plant by itself. Both approaches have their own advantages and disadvantages in terms of capex requirements, construction time required for ready to go to market, capacity utilization, logistic costs, government incentives availability, cost overruns and many more. Growing organically, in other words growing internally is funded through own reserves, accruals, retained earnings or availing incremental credit lines.

15.2. ‘Inorganic growth or expansion’ entails acquiring, merging, or partnering with another company. One expands or grows by buying capabilities, customers, capacity, or market share. Typical inorganic strategies to list a few will include –

| (a) |

|

Acquiring a competitor (horizontal acquisition) |

| (b) |

|

Acquiring supplier (backward integration) |

| (c) |

|

Acquiring distributor (forward integration) |

| (d) |

|

Buying distressed assets |

| (e) |

|

Merging with industry peer |

| (f) |

|

Joint venture with foreign manufacturer |

15.3. Financial structure for such inorganic approach requires large upfront capital also having significant debt component. This has its own set of advantages to include faster revenue scale up, opportunities to synergise, consolidate market dynamics, accessibility to new technology, new market segment, new geography. The primary challenges to encounter are on integration, cultural clashes, regulatory issues.

16. With the above understanding in perspective, we look at the growth journey and history of the assessee. Assessee having incorporated in 1907 was first to set up a steel plant in the eastern part of the country and since then, is a pioneer in steel making in Asia. Until the policy framework changed on liberalisation and globalisation in the Indian economy, production of steel was controlled and competition was limited with only two major players, namely, assessee and the Steel Authority of India Ltd. (SAIL) which is a public sector enterprise. Assessee being a local player, in order to cater to its aspirational goals of expanding its business like any other business enterprise would do, explored to encash opportunity to invest in Corus, for the same.

16.1. At this juncture, it would be important to take note of the observations of the Hon’ble jurisdictional High Court of Bombay in the case of Concentrix Services (supra) which listed three ways available for extension of business which we have already noted above. Expansion or extension of business could be in terms of geography, technology, scale of operations or even venturing into a diversified segment or could be many more such reasons, depending upon the aspirational goals of a business enterprise. Such a decision is purely a business decision. Assessee chose one of the three listed ways, to cater to its need of expansion by choosing Corus since both are in the same line of business, i.e., manufacturing of steel products, but having difference in their own individualistic operations and methodology. Assessee had a capacity of 5 million tonnes per year, whereas Corus had capacity in excess of 20 million tonnes per year. It had four plants located in UK and the Netherlands with extensive reach in matured markets of Europe and US with enviable product portfolio, with far superior basic products when compared with the products of the assessee. Thus, investment in Corus by the assessee resulted in a force multiplier which gave it economies of scale. Corus had products across segments which included automotive, aerospace, consumer goods, materials handling, energy and power, rail, engineering, ship building, packaging, security and defence. What assessee contemplated was an opportunity to diversify, have access to matured markets and leverage superior technology which would place it on the global pedestal of steel makers with these key differentiators.

16.2. Further, strong R&D set up at Corus led the assessee to gain synergy in operational improvement and process efficiencies. The key research themes included-

“Raw Materials: Research seeks to maximise the use of raw materials from captive sources. The projects include new technology to produce low ash clean coal, beneficiation of low grade iron ore and plant rejects to produce concentrates and a new coal agglomeration technology to increase the use of low-cost noncoking coal for coke production.

Market and New products: Research to develop advanced high strength steels, new forming techniques, innovative coatings, improved fatigue life of components etc.

Cost and productivity: efforts to develop cutting edge technology to become lowest steel cost producer worldwide. Many activities include research on agglomerates chemistry, blast furnace burden distribution, integrated through-process modelling, reduction in zinc consumption

Energy and Environment: Projects undertaken to reduce energy consumption, CO2 and other emissions. Construction of a pilot plant to trial the new Hisarna iron making process, which will drastically reduce the energy consumption and CO2 emissions associated with the production of iron from iron ore.

16.3. Major benefits arising out of this acquisition as summarised by the assessee are noted below:

“In Procurement, Lead Buyers have been appointed for high value items. Joint sourcing has resulted in contracts with substantial savings.

In manufacturing, knowledge exchange and synergy Identification has been driven through the Performance Improvement Teams (PITs) in 15 different areas, the most important being use of low cost coals for coke production, and increased recycling of steel plant wastes.

The synergy realised in the year under consideration comprised manufacturing, procurement, corporate centre, and tax savings. During the course of the year under consideration, the process of integration of the the Research Development & Technology (RD&T) function across the Tata Steel Group (TSG), with focus on ‘Thrust Area Projects of long-term value to the Group, was commenced.

Apart from the aforesaid, a KPI based programme was chalked out to generate mutual benefits.”

17. We also take note of the rebuttal made by the assessee on the observations of the ld. Assessing Officer while disallowance was made towards interest expenditure. The same is tabulated under:

| Sr. No. |

AO’s Observation |

Comments by the assessee |

| 1. |

Business income of the foreign subsidiary is not assessed to tax in India neither it is a resident in India. Accordingly….. (para 5.1) |

This statement of AO is factually incorrect as the income from foreign subsidiary by way of dividend is taxable in the hands of assessee and for allowability of interest under section 36(1)(iii) of the Act, residential status and taxability of foreign subsidiary is not relevant at all. This statement by AO is grossly misguided. |

| 2. |

Accordingly, the assessee was asked to explain as to why the interest expenses should not be treated as capital expenses, (para 5.1) |

The genesis of the question on allowability of deduction of interest expenses is drawn from sl. no.1 and we have already pointed that the same is baseless and hence there is no reason to doubt the allowability of expenditure under section 36(1)(iii) of the Act. |

| 3. |

However, the ultimate object was to take management of Corus. Since the assessee is not earning any income under the head business and profession from the said investment, the same cannot be treated as business expenses (para 5.2) |

The object of the company to acquire Corus was driven by business interests as the acquire was in the same line of business and because it dealt in products higher up in the value chain and catered to mature markets, provided sound business rationale to acquire the business. The management control was incidental to the act of acquiring for the sole purpose of strengthening existing Indian operations, augmenting profitability and also providing requisite insulation in times of global uncertainty due to diversification and penetration in different markets. Further, the statement to the extent that assessee is not earning any income from this investment and there is no business income, is again factually incorrect. Dividend income from this investment is taxable and the same will be offered to tax on its receipt. |

| 4. |

The interest expenditure has been incurred towards the capital borrowed to make investment in subsidiary. If investment in shares was business of the assessee, the would the have categorized investments in its books as above stock-in-trade. The fact that the assessee is showing the above shares, acquired, as investment in its books is also one of the indicators that assessee is not involved in the business of investment”, (para 5.2) |

Herein, we would like to submit that the AO has not appreciated the difference between business investment vis-à-vis other investments, and it is trite law that any expenditure for the purpose of business investment, should be allowed as revenue expenditure. The inference and conclusion drawn by AO is erroneous as he has shares categorized as stock-in-trade with mistakenly mixed the concept of investment in investments made for business purposes. It is to be noted that for manufacturing companies all investments have to perforce be categorized as The Investments and not stock-in-trade. classification of ‘Stock-intrade’ in Investment schedule is to be done for companies in the business of selling and purchasing shares. |

| 5. |

In fact it is seen that the aforesaid investment has been made only for the purpose of maintaining controlling interest in the said subsidiary company and not with the motive of business consideration, including capital appreciation.” (para 5.2) |

Herein, we would like to submit that this statement is factually incorrect. We have given our detailed submission below on the business rationale of making investment in the Corus group. Therefore, the statement made is without basis. |

| 6. |

There is no connection of business in the said investment in whatever manner.” (para 5.2) |

Herein, we would like to submit that this statement is factually incorrect. We have made detailed submission below. Considering the same, the statement as well as conclusion on the basis of this statement is incorrect. |

| 7. |

The department in the case of Tata Sons Ltd. has accepted (except share of TCS Ltd. which is part of Tata Sons Ltd.) that amounts invested for acquiring management of company is capital investment. In view of the fact that the assessee’s umbrella company/ holding company itself is contending that shares acquired with the purpose of acquiring management should be treated as capital assets, the assessee should not be allowed to take exactly the opposite position.” (end portion of para 5.7) |

The reference from the case of Tata Sons Ltd. is totally incorrect for the following reasons:

? Tata Sons Ltd. being investment company intends acquiring shares for investment purposes whereas, Tata Steel Ltd. being a manufacturing company has made Investments for its business purpose and for expansion of its business. Nature of the business undertaken by Tata Sons and Tata Steel is entirely different. One is an investment company and the other a manufacturing enterprise. Assessing Officer while drawing conclusion has not considered this basic difference while attributing similar purpose to both entities.

|

18.1. From the above, we note that reference made by ld. Assessing Officer to the case of Tata SonsLtd. (supra) is factually on a different footing since, it is an investment company whose sole objective is to acquire shares for investment purpose only. Contrary to this, assessee is a manufacturing business enterprise, dealing in production and sale of steel and its related products.

19. In the conspectus of the above detailed discussion including factual matrix of the case, provisions of the Act and judicial pronouncements, we hold that interest expenditure incurred by the assessee towards acquisition of Corus through its step-down wholly owned subsidiaries is for the purpose of business and therefore, allowable u/s. 36(1)(iii) of the Act. Disallowance so made by the ld. Assessing Officer for making an addition to the total income is deleted. Since we have allowed the claim u/s.36(1)(iii), the alternate and without prejudice ground raised by the assessee referring to section 57(iii) is rendered infructuous. Accordingly, ground no.2 is allowed.

19.1. Also, since we have allowed the appeal of the assessee on the merits of the case in terms of our above observations and findings, the legal contentions on the jurisdictional aspect raised in ground no.1 including sub-grounds are left open and not adjudicated upon, more so when, ld. Counsel for the assessee himself laid more thrust on merits as against the jurisdictional issues.

20. In the result, appeal of the Revenue is dismissed and that of the assessee is allowed.