ORDER

Anikesh Banerjee, Judicial Member.- Instant appeal of the revenue was preferred against the order of the National Faceless Appeal Centre (NFAC), Delhi [hereinafter referred to as “Ld. CIT(A)”] order passed u/s. 250 of the Income Tax Act, 1961 (hereinafter referred to as “Act”) order passed for the Assessment Year 2020-21 date of order 16.09.2025. The impugned order emanated from the order of the Assessment Unit Income Tax Department (hereinafter referred to as “Ld. AO”), order passed u/s. 143(3) r.w.s. 144B of the Act date of order 28.09.2022.

2. Brief facts of the case are that the assessee is an individual and carrying on business commission agent related to chemical distribution. During the impugned assessment year, the return was filed and declaring total income of Rs. 4,87,280/-. The assessee claimed capital gain exemption under section 54F amounting to Rs. 11,68,89,000/-. The assesses’s case was selected for scrutiny under cash or verifying the capital gain deduction claim in the return of income. The Ld. AO found that the assessee had received amount to Rs. 11,68,99,000/- on surrender of tenancy rights. The said property was jointly owned by his family. The assessee with his brother Shri Vivek Jaisingh Asher were the tenant of the said property. After a long-standing RAE suit, on the first floor was vacated in 2013. The old tenant vacated on 31 March 2013 for a consideration of Rs. 2.75 crore. To meet the families bonafide residential needs, the assessee and his brother started occupying the vacated portion by paying rent of Rs. 5000/- per month. Though no formal agreement was executed initially, the rent receipt and electricity bills evidenced for tenancy.

Since the property would remain within the family the family did not find it necessary to make any formal agreement in 2013. Both the sons were paying rent of Rs. 5000 per month and assessee has submitted rent receipts and electricity bills to evidence the tenancy. Later on the property was proposed to be redeveloped. The redeveloper required a formal agreement and therefore tenancy agreement was registered on 05/08/2014. The Ld. AO considered the tenancy agreement as a sham matter of arrangement a colourable device which does not really bestow any legitimate and genuine tenancy rights without appreciating the fact the tenancy agreement was between assessee and his own immediate family members and the Income Tax Act per se exempt transaction between assessee and his relatives from any tax on transaction.

The owners entered into joint development agreement on 11/08/2014. Permanent Alternate Accommodation Agreement was entered by tenants with the builder in March 2017 after which the tenant gave the possession of the property. The OC of redeveloped building was received in February 2020 after which the assessee received possession of one flat of 1550 sq.ft in lieu of surrendering tenancy rights. Finally, a registered tenancy agreement was letter executed in 2014 to facilitated the redevelopment. The assessee claimed exemption U/s 54F of the related to surrender of tenancy right.

The Ld. AO disregarded the tenancy agreement, and treating it as a colourable devise and tax the value of flat receipt under section 56(2)(x)(b) as income from other sources. Ignoring the nature as considering for surrender of tenancy rights being a capital asset. Ld. AO also denied the benefit of section 54F related to acquisition of new flat. Aggrieved assessee filed an appeal before Ld. CIT(A). The Ld. CIT(A) after considering the submissions of the assessee deleted the addition. Being aggrieved revenue filed an appeal before us.

3. The Learned Departmental Representative (Ld. DR), argued and stated that the agreement and all the documents related to the proof of tenancy is nothing, but a colourable device for avoidence of the tax. Ld. DR stands in favour of the impugned order of Ld. AO

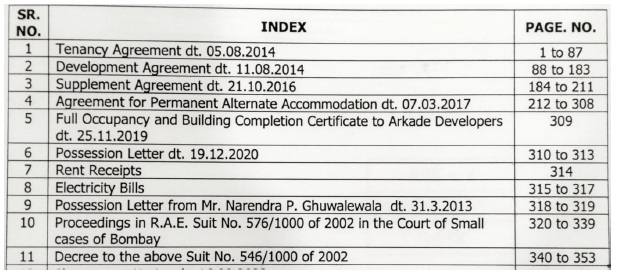

4. The Learned Authorised Representative (Ld. AR) submitted that the assessee had filed a paper book comprising pages 1 to 443, which has been taken on record. The Ld. AR drew our attention to the index of the paper book, wherein the assessee has placed various documents before the revenue authorities as well as before this Bench in support of the claim of tenancy. The list of such documents evidencing the tenancy rights of the assessee is as follows:

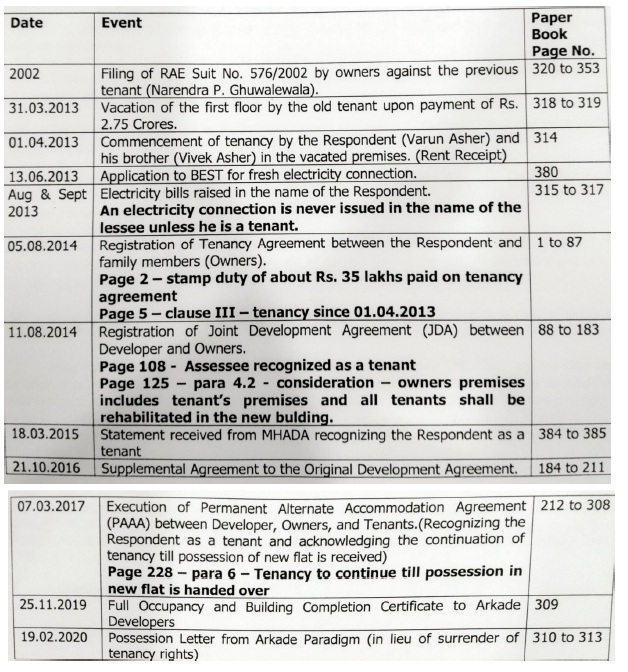

5. The Learned Authorised Representative (Ld. AR) also filed a written note explaining the sequence of events, along with the relevant facts and documents, which are reproduced as under:

The above chronology clearly establishes uninterrupted tenancy rights of the Respondent from 01.04.2013 up to 19.02.2020, duly evidenced by rent receipts, electricity records, registered agreements, statutory recognition by MHADA, and culminating in allotment and receipt of permanent alternate accommodation on 19.02.2020 (almost 7 years later) in lieu of surrender of tenancy rights.

It is important to note that even stamp duty of Rs. 35 lakh was paid on registration of tenancy agreement.

These are all government records or records which are registered. Such documents cannot be disregarded.

The tenancy agreement and other documents registered in the year 2014 and prior years cannot be disputed and disregarded in the year 2020.

There cannot be tax avoidance or tax evasion on transfer from father (or close relative) to son. Reliance on the decision of the Hon’ble Supreme Court in case of Mahendra Gala v. ITO (tendered in the Court).

There are four co-owners. They received 3 flats. If they had received this one more flat, still they would have been able to claim benefit of section 54F of the Act.

Therefore, there is no tax savings as such.

If AO disregards the tenancy, then he should also disregard the receipt of new property in the hands of the assessee.

Even Maharashtra Housing and Area Development Authority (MHADA) had verified the tenancy. The assessee was listed as a tenant in the redevelopment scheme approved by MHADA. This independent government verification negated the AO’s claim that the tenancy was a sham.

Since, in lieu of tenancy the assessee has received new flat on ownership basis, therefore, in the year of possession of new flat, the tenancy is extinguished. There will be transfer and the assessee would be entitled to take benefit of section 54F of the Act as allowed by Ld. CIT(A).”

6. The Ld. AR respectfully, relied on the order of the Ld. CIT(A). The relevant para 9 from page 35 to 36 of the impugned appellate order are reproduced below:

“9. All the grounds of appeal are concerned with the action of the AO in treating Tenancy Arrangement as Sham after rejection of Documentary Evidence which resulted into disallowance of Section 54F exemption claimed by the appellant.

The AO concluded that the tenancy agreement dated 05.08.2014 between the assessee and his family members was a colourable device, executed solely to claim exemption under section 54F. He held that the assessee had no independent or legitimate tenancy rights and that the arrangement lacked commercial substance. Despite the assessee submitting rent receipts, electricity bills, and MHADA verification, the AO disregarded these documents, citing that they were self-serving and did not establish genuine tenancy. The AO relied on Sumati Dayal v. CIT and McDowell & Co. Ltd. v. CTO to apply the “test of human probabilities” and strike down what he considered a tax avoidance scheme. The AO also argued that the flat received by the assessee in the redeveloped building was not against any genuine consideration. Thus, he treated the receipt of the flat as gratuitous and invoked section 56(2)(x), taxing the stamp duty value of Rs.11.68 crore as income from other sources.

From review of documentary evidence it is seen that Tenancy Agreement is Registered and notarized. As per tenancy agreement, tenancy was given w.e.f. 01.04.2013 immediate after vacation of the property by outgoing tenant in pursuance of a decree in terms of consent terms arrived at and substantial payment of Rs.2,75,00,000/- was paid to outgoing tenant as documented at para 1(III) of the tenancy agreement. Mere fact that registration of the Tenancy agreement was done at a later date, doesn’t render the tenancy agreement invalid/non-existent. Rent Receipts are on monthly payment basis and acknowledged by landlords. Electricity Bills are in appellant’s name since 2014. During MHADA Verification appellant was listed as tenant in redevelopment scheme. Permanent Alternate Accommodation Agreement was found executed with developer. Thus, the appellant has valid tenancy rights. Argument of the AO that the appellant was not a genuine tenant and had no independent tenancy rights, is not correct.

The AO relied on decision given in the case of Sumati Dayal v. CIT [1995] 214 ITR 801 (SC) to justify rejection of documentary evidence based on surrounding circumstances and decision given in the case of McDowell & Co. Ltd. v. CTO [1985] 154 ITR 148 (SC) to argue that tax planning through colourable devices should be struck down. Facts of these case laws are different from the facts of the appellant. Case Laws relied on by the AO pertain to unexplained cash credits and tax avoidance but the appellant’s case is of documented tenancy and transactions are supported by registered agreements and third-party verification.

Since, tenancy rights are capital assets under section 2(14) and surrender constitutes transfer u/s 2(47), flat received in exchange for tenancy right is a valid consideration. There is nothing on record to show that any other residential property held by the appellant on date of transfer. As, flat qualifies as investment in residential house, conditions to claim exemption u/s section 54F stands satisfied. As flat received in exchange for surrender of tenancy rights which is a valid consideration and transaction is not gratuitous, invoking provisions of section 56(2)(x) by the AO is not correct.

In view of the above findings, the addition of Rs.11,68,99,000/- made under section 56(2)(x) is hereby deleted and the claim of exemption under section 54F is held allowable. In the result, appeal is allowed in full.”

7. The Ld. AR further contended that an identical issue had arisen in the case of the assessee’s brother, who was the co-tenant of the property. In respect of the same assessment proceedings, the legal issue was challenged and subsequently adjudicated by the Hon’ble Bombay High Court in the case of the assessee’s brother, Vivek Jaisingh Asher v. ITO (Bom)/Writ Petition No. 4370 of 2022, vide order dated 16.04.2024.

The relevant observations of the Hon’ble Jurisdictional High Court are reproduced as under:

“8. Admittedly, no notice has been issued to assessee/petitioner calling upon assessee to show cause whether the entire stamp duty value be treated as unexplained investment under Section 69 of the Act. In the affidavit in reply, the answer given to this allegation of petitioner that no notice was given to show cause under Section 69 of the Act is that the assessment was getting barred by limitation on 30th September 2022 and there was no time for further show cause notice and hence the Faceless Assessing Officer (FAO) has passed the assessment order after considering all the submissions and possible aspect of the case and agreement value of the new purchased property at Rs.11,68,99,000/- is treated as unexplained investment under Section 69 of the Act and added to the total income of assessee. In the assessment order though there is reference to Section 56(2)

(x) of the Act and the reply/objections filed by petitioner in response to the show cause notice, in the operative part there is no reference to Section 56(2)(x) of the Act.

9. The courts have time and again held that issuance of show cause notice is not an empty formality. Its purpose is to give reasonable Purti Parab 5/6 449-WP-4370-2022.doc opportunity to the affected persons to effectively deal with the allegations in the show cause notice. In our view, even the show cause notice dated 23 rd August 2022 is defective in as much as even though it had reference to Section 56(2)(x) of the Act, it did not mention whether the Assessing Officer proposed to treat the stamp duty value as deemed income of assessee under clause (a) or clause (b) of Section 56(2)(x) of the Act. This is because both are separate provisions and under either of these two clauses the stamp duty value could be treated as deemed income. By not specifying whether Section 56(2)(x)(a) or Section 56(2)(x)(b) of the Act was applicable, the A.O. first of all has not given reasonable opportunity of showing cause to the assessee. Assessee would be totally unaware of the grounds which had prompted the A.O. to arrive at a prima facie conclusion and issue show cause notice.

The power that the A.O. had was required to be executed properly. Moreover in the assessment order dated 29 th September 2022 that is impugned in the petition, the A.O. has chosen to give Section 56(2)(x), a go by and treat the stamp duty value of the flat at Rs.11,68,99,000/- as from unexplained source under Section 69 of the Act. There is no reference to Section 56(2)(x) of the Act in the operative part of the order dated 29th September 2022.

10. In the circumstances, the impugned order dated 29 th September 2022 cannot be sustained. The allegations in the affidavit in reply that assessee has claimed tenancy rights as colourable device in order to get an Purti Parab 6/6 449-WP-4370-2022.doc exemption under the provisions of the Act and evade the tax liability also cannot be accepted because if the A.O. had evidence to that effect the same should have been stated in the show cause notice dated 23rd August 2022.”

8. He further argued that, the identical issue was duly examined and adjudicated by the Co-ordinate Bench of ITAT, Mumbai in the case of Vasant Nagorao Barabde v. Dy. CIT (Mum–Trib) the relevant para 8 to 9 is reproduce as below:

“8. We have heard both the parties and perused the material on record. We have given our thoughtful consideration to the submissions made before us and the factual matrix as demonstrated by the documentary evidences placed on record and submissions made before the authorities below. It is an undisputed fact that both the assessee and his daughter are tenants in the registered agreement for PAA dated 21.09.2017 under which flat no. 1103 in the new building has been allotted by the developer against surrender of tenancy rights. Existence of tenancy is not in dispute. Primarily, the claim is that the surrender of tenancy rights is by the daughter of the assessee for which letter of allotment issued by Sandu Developers dated 26.03.2013 is placed on record which records the said transaction in the name of the daughter of the assessee. Ld. AO has resorted to make the addition in the hands of the assessee by taking note of the fact that agreement for PAA bears first name as that of the assessee. Since there was no consideration for having the impugned flat registered in the name of the assessee, the entire stamp duty value of the said flat was taken as income in the hands of the assessee u/s. 56(2)(x)(b)(B) of the Act.

8.1. In the given set of facts, it is important to note that there is a surrender of tenancy rights against which a new flat has been allotted for which a registered deed is placed on record, contents of which are not in undispute. Once it is disputed that there is a surrender of tenancy rights, the factual position which emerges is that tenancy right is a capital asset which has been transferred and is liable to be taxed u/s. 45 of the Act for capital gain r.w.s 48 of the Act. The moot point arises is as to in whose hands this capital gain is to be taxed depending upon who owned the tenancy rights and who transferred the same to the builder against which the new flat was allotted. in present set of facts, it could be either the assessee or his daughter Ms. Ashwini Barabde. In either case, deduction u/s, 54F is available against the capital gain so computed since, there is an investment by way of PAA residential flat allotted by the builder of equivalent stamp duty value of Rs. 2,88,85,600/-. Thus, in either hands, the capital gain so computed will be eligible for deduction u/s. 54F in toto.

8.2. We are in agreement with the contention raised by the Ld. Counsel that once an income from a source falls within a specific head, the fact that it may indirectly be covered by another head will not make the income taxable under the later head. In our considered view, applicability of Section 56 is ruled out in the present fact of the case. Respectfully following the principle laid down by the Hon’ble Supreme Court in the case of D.P. Sandu Bros. Chembur (P.) Ltd. (supra) and in the given set of facts as narrated above, the addition made by the Ld. AO in the hands of the assessee u/s. 56(2)(x)(b)(B) of the Act is deleted. Further, claim of the assessee for deduction u/s. 54F against the capital gain on the impugned transaction is an allowable claim by taking into account the observation of Hon’ble Supreme Court in the case of Goetze (India) Ltd. (supra) whereby Hon’ble Court held that (“nothing impinges on the power of the appellate authorities to entertain such a claim of the assessee). Accordingly, grounds raised by the assessee are allowed.

9. In the result, appeal of the assessee is allowed.”

9. We have heard the rival submissions and perused the material available on record, including the documentary evidences placed in the paper book and the judicial precedents relied upon by the parties. The primary issue involved in the present appeal is whether the tenancy arrangement entered into by the assessee was a sham transaction and whether the value of the flat received by the assessee on surrender of tenancy rights was liable to be taxed under section 56(2)(x) of the Act, or whether the same constituted consideration for transfer of a capital asset entitling the assessee to claim exemption under section 54F of the Act. From the record, it is evident that the assessee has placed substantial documentary evidence to establish the existence of tenancy rights, including rent receipts, electricity bills, registered tenancy agreement dated 05.08.2014, MHADA verification records, and the Permanent Alternate Accommodation Agreement executed with the developer. These documents clearly demonstrate that the assessee had been occupying the premises as a tenant since 01.04.2013 and that the tenancy rights continued until their surrender in the course of redevelopment of the property. The fact that the tenancy agreement was formally registered in 2014 does not invalidate the existence of tenancy, particularly when the surrounding documentary evidence corroborates continuous occupation and payment of rent.

We further observe that tenancy rights constitute a capital asset within the meaning of section 2(14) of the Act and the surrender thereof amounts to a transfer under section 2(47) of the Act. The allotment of a residential flat by the developer under the redevelopment scheme represents consideration received in exchange for such surrender of tenancy rights. Therefore, the transaction squarely falls within the ambit of capital gains and cannot be brought to tax under the residuary provisions of section 56(2)(x) of the Act. In this regard, we find support from the decision of the Coordinate Bench of the Tribunal in Vasant Nagorao Barabde (supra), wherein it has been held that once a transaction falls under the specific head of capital gains, it cannot be taxed under the head “Income from Other Sources”. We also note that the Hon’ble Bombay High Court, in the case of the assessee’s brother and cotenant Vivek Jaisingh Asher (supra), has observed that allegations of colourable device cannot be sustained in the absence of cogent material and proper show cause notice specifying the applicable statutory provision. The observations of the Hon’ble Jurisdictional High Court further lend support to the assessee’s contention that the tenancy arrangement cannot be disregarded merely on the basis of suspicion.

In light of the above factual and legal position, we find no infirmity in the order of the Ld. CIT(A), who after detailed examination of the documentary evidence rightly concluded that the assessee possessed valid tenancy rights and that the flat received on redevelopment constituted consideration for surrender of such rights. Consequently, the addition made by the Assessing Officer under section 56(2)(x) of the Act was rightly deleted and the assessee’s claim of exemption under section 54F was correctly allowed. Accordingly, we uphold the order of the Ld. CIT(A) and dismiss the grounds raised by the revenue.

Hence, the appeal filed by the revenue is dismissed.

10. In the result, the appeal of the revenue bearing ITA No. 8251/Mum/2025 is dismissed.