ORDER

Ms. Madhumita Roy, Judicial Member. – The instant appeals filed by the Assessee are directed against both the orders dated 18.08.2025 passed by the Ld. Commissioner of Income-tax (Exemptions), Chandigarh [hereinafter referred to as the Ld. CIT(E)] whereby and whereunder the application filed by the assessee in Form No.10AB under Section 12A(1)(ac)(ii) of the Income-tax Act, 1961 (hereinafter referred to as ‘the Act’) has been rejected. The Registration granted u/s 12AB of the Act also stood cancelled and the grant of approval under Section 80G of the Act was also rejected.

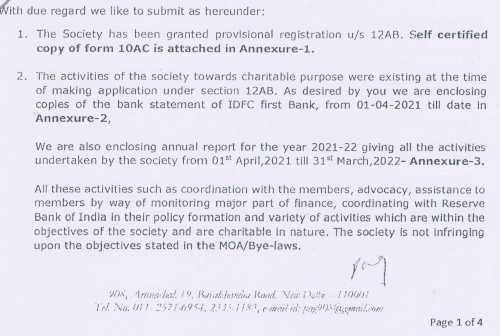

2. The assessee is having its registered office at Hyderabad and the head office and the operation office is at Gurgaon. The activities of the assessee is to coordinate with members, advocacy, assistance to members by way of monitoring major part of finance, coordinate with Reserve Bank of India in their policy formation and variety of activities which are within the objectives of the society and are charitable in nature. The assessee got the provisional registration for AY 2021-22, 2022-23 and 2023-24 under Section 12AB, the copy whereof in Form No.10AC is attached as page 1 to 3 of the paper book filed before us. The activities of the Society towards charitable purpose were existing at the time of making application under Section 12AB. Neither the assessee is infringing upon the objectives stated in the Memorandum of Association or in the bylaws. The application in Form No.10AB was filed within six months from the commencement of the activities within the extended period of time limit as provided by the CBDT. Further, that no part of the income of the assessee trust ensures directly or indirectly for the benefit of a person specified under Section 13(3) of the Act.

3. The assessee claims to be a premier institution network coordinating with the Reserve Bank of India and assisting them in the policy formulation after educating and implementing the RBI’s direction with various stakeholders in the area of micro finance. In fact various task force and committees have been formed for fulfilling the objectives of the assessee Trust. The assessee claims to help in educating various institutes in this behalf and facilitates poors of the country by making them understand their rights, facilities and advise them on reasonableness/discounting of lending rate by various institutions. The people who are suffering from natural calamities are also extended help by the society. It also has a potential in contributing to the Indian economy as reflecting from different workshops held by the assessee evidenced in the paper book filed before us.

4. In fact, it is a society registered under Telengana Societies Registration Act, 2001, recognized as a self regulatory organization for NBFC-MFIN (nonbanking finance companies operating in the micro finance sector) by the Reserve Bank of India. It is claimed to be a representative industry body engaged in the development and promotion of best practices in the micro finance sector with the additional functions for liaisoning with regulatory authorities, conducting research and capacity building for its members and publishing data and policy inputs relevant to micro-finance institutions. According to the Ld. CIT(E), the structure of the assessee is nothing, but, commercial establishment and the data from MFIN website and other sources were fetched wherefrom the structure, role and operation could be gathered and wherefrom the Ld.CIT(E) concluded that MFIN operates as an apex level industry platform not for general public, but exclusively for its members most of whom are NBFC engaged in generating profits in micro finance lending. As MFIN is recognized as a self regulatory organization for NBFC-MFIN by the Reserve Bank of India since June 16, 2014. This single lines undoes the entire premise of charitable intent. Further, all its activities include sector coordination, training, compliance audits, grievance redressal among members and policy engagement with regulators. According to the CIT(E), none of these activities are directed towards public at large. The role of the assessee is a statutory function under the delegated regulatory guidelines meant to oversee and discipline a specific class of for-profit micro finance companies. Even if it is done efficiently, the same is not charitable rather it is a regulatory duty undertaken under the RBI supervision. The claim of advancement of general public utility is, therefore, absent in the case of the assessee, it operates solely through its membership base which comprises nonbanking finance companies, micro finance institutions, most of which are for-profit entities. There is no mechanism, structure or even stated object could have been found which could suggest over reach to the general public, let alone the under privileged which is sine qua non for general public utility clause under Section 2(15) of the Act as also observed by the Ld. CIT(A). The submission of the appellant was found to be devoid of charitable content, where the legal line between service to members and service to public are quite blurred. The applicant society does not satisfy the conditions envisaged u/s 12AB of the Act and, thus, the application filed by the assessee in Form No.10AB u/s 12AB(1)(ac)(ii) of the Act was rejected. Hence, the instant appeal before us.

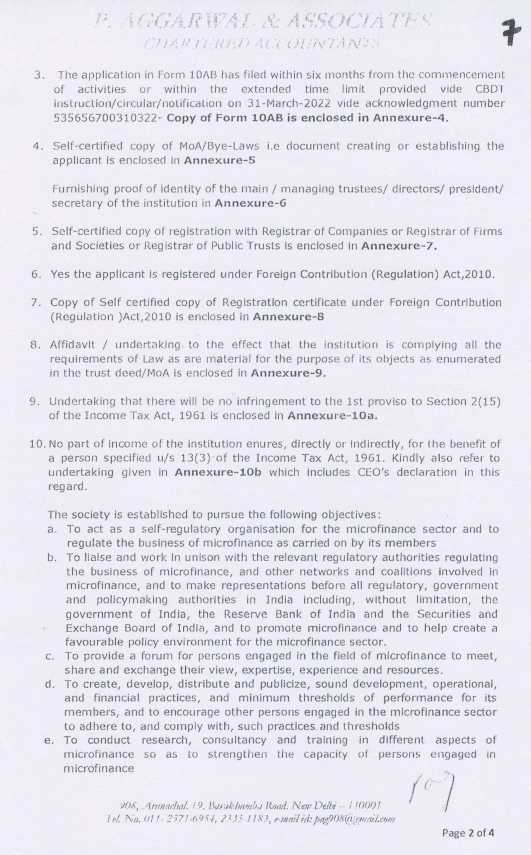

5. We find the following activities done by the assessee on the basis of which the claim of registration was sought for. In fact, such details were also made known to the order issuing authority on 28.09.2022 by the assessee appearing tt pages 6-9 of the paper book filed before us, the relevant contents whereof is as follows:-

| a. |

|

To act as a self-regulatory organisation for the microfinance sector and to regulate the business of microfinance as carried on by its members |

| b. |

|

To liaise and work in unison with the relevant regulatory authorities regulating the business of microfinance, and other networks and coalitions involved in microfinance, and to make representations before all regulatory, government and policymaking authorities in India including, without limitation, the government of India, the Reserve Bank of India and the Securities and Exchange Board of India, and to promote microfinance and to help create a favourable policy environment for the microfinance sector. |

| c. |

|

To provide a forum for persons engaged in the field of microfinance to meet, share and exchange their view, expertise, experience and resources. |

| d. |

|

To create, develop, distribute and publicize, sound development, operational, and financial practices, and minimum thresholds of performance for its members, and to encourage other persons engaged in the microfinance sector to adhere to, and comply with, such practices and thresholds |

| e. |

|

To conduct research, consultancy and training in different aspects of microfinance so as to strengthen the capacity of persons engaged in microfinance |

| f. |

|

To establish linkages between members and resource institutions, such as funding agencies, financial institutions, rating agencies and training, consultancy and research institutions. |

| g. |

|

To provide services to members, inter alia, training and capacity building; helping in achieving thresholds of performance; providing information related to legal and regulatory issues; providing availability of funding and employment opportunities; and advisory services for performance enhancement and transformation of legal forms, |

| h. |

|

To establish other bodies to support and represent microfinance |

6. The assessee was further asked to furnish an undertaking that there is no infringement to the first proviso to Section 2(15) of the Act. In response thereto the undertaking was duly given which is part of the paper book.

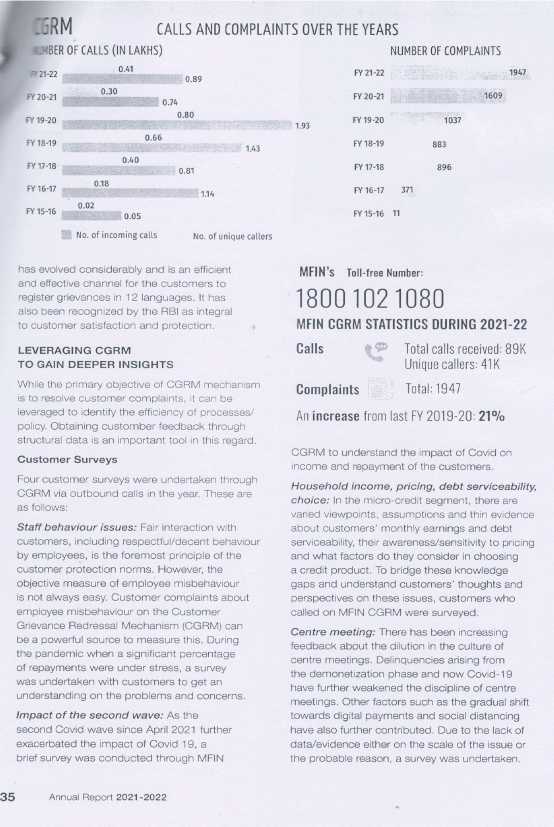

7. In fact, the assessee has further filed the following details in regard to the expenses incurred by the Assessee (‘MFIN’) towards activities involving public outreach along with the Annual report of FY 2024-25 to correlate expenses with the activities referred herein. The annual accounts for FY 2022-23 (PB-178) and FY 2023-24 (PB-260) are already part of the Paper Book as filed as further considered by us:

Customer Grievance System (Toll Free No.)

| 1. |

|

MFIN operates a customer grievance system in all major (12) vernacular languages. The free service works 24*7 and receives nearly 2 lakh queries/complaints in a year. MFIN has spent the following amounts on these activities, leading to direct benefit of 4,72,119 borrowers of microfinance sector during the captioned periods. |

| Financial Year |

Amount (INR) |

Incoming Calls |

Unique Caller |

Complaints filed |

Complaints Resolved |

| 2025-26 (till 31.12.25) |

32,07,895 |

2,10,786 |

96,236 |

1.590 |

1,517 |

| 2024-25 |

39,37,126 |

2,84,631 |

1,29,036 |

1,947 |

1,947 |

| 2023-24 |

33,28,305 |

2,11,405 |

1,03,661 |

2,045 |

2,045 |

| 2. |

|

The expenditure as tabulated above, excludes salary of senior technical staff who are employed exclusively to supervise this activity. That amount is approximately Rs. 45 lakh per year.Refer expenditure given in Note 10, 11 on page No. 64 of Annual Report 2023-24 and Note 14, 15 on page No. 84 of Annual Report 2024-25. |

Expenditure on Consumer Awareness and Capacity Building Projects.

| 3. |

|

MFIN has conducted various initiatives in this regard, details whereof are listed herein below: |

| a. |

|

Depositor Education and Awareness (DEA) Workshops – On behalf of Reserve Bank of India (RBI), MFIN is undertaking a project to conduct 2,131 workshops, with a view to educate low-income persons about financial literacy. The budget allocated towards these workshops is Rs.12,98,25,000 for 3 years. |

| b. |

|

MFIN has already conducted 723 workshops and 39,884 people have participated in these workshops till July 2025, spending Rs. 4,03,67,461/- in the first 2 phases spread over 2024-25 and 2025-26.The balance amount of Rs.8,94,57,539/- is to be spent till April 2028. These expenditures are disclosed at Note 13 on page No. 84 of Annual Report 2024-25. |

| c. |

|

Building Digital Capacity of Rural Population -This project seeks to educate and familiarize rural population with digital payments, and efficient and safe usage thereof. It is in line with the Digital India Mission. The project involved survey of population to understand their preferences and problems faced with digital transactions, development of training modules in vernacular, training to develop confidence and also development of suitable apps. It runs across ten states and wants to raise awareness of 3.38 lakh people and 1.5 lakh low-income people using digitaltransactions. While the CXO level vertical head overseas the project, a Senior VP works full time on the project and external specialized agencies are also hired. During FY 2024-25, MFIN has spent a sum of Rs.2,30,15,823/- on this project, which is disclosed at Note 13 on page No. 84 of Annual Report 2024-25. |

| d. |

|

Microfinance Awareness Program (MFAP)- Microfinance as a sector works at providing responsible lending facility largely to a population that cannot raise bank loans. As explained at Page 46 of the Paper Book, a microfinance loan is a collateral-free loan given to a household having annual income of less than Rs.3 lakhs. This chunk of India’s population is largely prey to local moneylenders. Awareness programmes are run with the objective of educating low-income segments about benefits of formal finance, regulatory architecture for customer protection, and ill-effects of taking money from moneylenders. An NCAER study in 2025 shows that share of moneylenders has declined heavily to only 1% in areas where microfinance is available, while government data states that moneylenders account for 23% of loan funds in other places. |

| e. |

|

In the current financial year, till December 2025,MFIN hasconducted 128 MFAP’s, handled by 7 technical regional heads,all of whom are senior management professionals (MBA)with 10 plus years of experience. Total expenses on these activities in FY 2024-25 by way of staff allocation, was Rs.95 lakhs, as may be referred from note 14 on page No. 84 of Annual Report 2024-25. Outlay on this count in the current financial year is projected at Rs.1.20 crore on 2025-26. This excludes travel expenses of approximately 7 experts and coordinators, who have conducted these programmes in 18 states of India. |

| f. |

|

Climate Change Adaptation Project – This project is aimed at equipping poor people to mitigate income-loss due to climate events by developing an appropriate insurance product as also building awareness and capacity. MFIN has spent Rs.81,35,596/- towards this initiative during FY 2024-25, as given in Note 14 on page No. 84 of Annual Report 2024-25. |

| g. |

|

Consumer Awareness Campaigns – MFIN has incurred substantial expenses in mass media campaigns – Ad films, Audio-visuals, newspaper advertisements, PR, posters, etc., seeking to build awareness of consumer rights, safe use of phones and digital payments, etc. Expenditure on such activities Rs.1,37, 68,554 in FY 2024-25, as may be referred from Note 14, 18 on page No. 84 of Annual Report 2024-25. |

The CIT(E)’s comments at Page 17 of the impugned order are factually rebutted in this manner.

Consumer Research & Data Analysis on RBI’s Behalf.

| 4. |

|

MFIN has conducted several research initiatives as to income, social, and welfare indicators of poor people, so as to inform RBI on government policy. RBI’s guidelines for SROs specify “Collect and share relevant sectoral information to the Reserve Bank to aid in policymaking. The SRO should also use the information to foster innovation, and coordinate on the introduction of new products within the broader regulatory framework set by the Reserve Bank. And Encourage a culture of research and development within the sector to encourage innovation while ensuring highest standards of compliance and self-governance”. This makes periodic research into the livelihood and other aspects of low income people a priority area for MFIN. |

In 2024, MFIN engaged NCAER to conduct a study on “Assessment of impact of small borrowings in India”,wherein 10,432 borrowers across 100 districts in 10 states were surveyed. Themain findings were shared with the Governor during Pre-Monetary Policy Committee meeting on 20 January 2026 and the full report will be released in February-March 2026. Total cost towards this exercise was budgeted at Rs.1,20,47,208/-, of which Rs.60,23,603/-was spent during FY 2024-25, as may be referred from Note 15 on page No. 84 of Annual Report 2024-25. The remaining sum is being spent in the current financial year.

| 5. |

|

MFIN also obtains monthly and quarterly data from credit information companies, to ensure that microfinance companies are functioning in compliance with RBI regulations, and in line with policy intent. Every month detailed district wise reports are taken from two bureaus and in addition every quarter compliance report is taken from one bureau. These reports form a crucial consumer protection tool. Against this activity, MFIN has spent sums of Rs.65,52,918/- during FY 2024-25, as may be gleaned from Note 15 on page No. 84 of Annual Report 2024-25, while a sum of Rs.40,08,982/- stands spent thus far during the current financial year. |

Regulatory Function as per RBI Mandate.

| 6. |

|

MFIN has been authorised by Reserve Bank of India to regulate the microfinance industry in India, as of 2014 onwards, with a view to overseeing protection of low-income borrowers, with the duty to submit periodic reports to RBI. While this activity is not in the nature of direct public outreach, it is undertaken for the benefit of the public – borrowers -only. MFIN’s expenditure as to its regulatory activity during the past five years, is as under. This expense does not include salary & emoluments of senior management & executives: |

| Financial Year |

Amount (INR) |

| 2025-26 (till 31.12.25) |

3,07,33,355 |

| 2024-25 |

3,22,41,017 |

| 2023-24 |

3,73,33,715 |

| 2022-23 |

2,17,85,804 |

| 2021-22 |

2,06,13,389 |

Summary Table

| Clause No. |

Particulars |

Amount (Rs. Crore) |

| F.Y 2024 25 |

F.Y 2025-26 (upto Dec 2025) |

| 2,3 |

Customer Grievance System (Toll Free No.) |

0.85 |

0.68 |

| 4(a) &(b) |

Depositor Education and Awareness (DEA) Workshop |

1.26 |

2.16 |

| 4(c) |

Building Digital Capacity of rural population |

2.30 |

– |

| 4(f) |

Climate change adaption project |

0.81 |

0.60 |

| 4 (d) & (e) |

Microfinance Awareness Program (MFAP) |

0.95 |

1.20 |

| 4(g) |

Other Activities |

1.37 |

1.89 |

| 5 |

Conduct of Pan India research studies |

0.60 |

0.60 |

| 6 |

Data cost for ensuring regulatory compliance and fair treatment |

0.65 |

0.40 |

| 7 |

MFIN as SRO (Net of Point 1) |

2.37 |

2.39 |

|

TOTAL |

11.16 |

9.92 |

This excludes senior management cost and overheads

8. The assessee was further asked as to whether it provides all the services free of cost or charges any amount by whatever name called for its activities from beneficiaries at cost or nominal margin whereupon justification of service fee charged in the light of the provision of section 2(15) of the Act was duly furnished by the assessee before the said authority. The assessee, in response to the query as to whether any part of the income of the assessee ensures directly or indirectly for the benefit of a person specified under Section 13(3) of the Act categorically submitted that no part of the income of the institution ensures the same supported by an undertaking to that effect.

9. Apart from that the assessee is not carrying out any incidental activity in the nature of trade, commerce or business as also clarified in response to the query No.11 as made by the CIT(E) dated 25.03.2025. The assessee repeated and reiterated the following objectives in support of the claim of exemption made by it as a charitable society appearing at page 21-22 of the paper book filed before us, the contents whereof is as follows:-

“The Society is established to pursue the following objectives:

1 To facilitate the evolution of a conducive ecosystem and standards for the sustainable development of a customer-centric microfinance sector.

2. To act as a Self Regulatory Organisation (SRO) for NBFC-MFIs and adoption/implementation of best practices and Code of Conduct by all members.

3. To liaise and work in unison with the relevant regulatory authorities regulating the business of microfinance, and other networks and coalitions involved in microfinance, and to make representations before all regulatory, government and policymaking authorities in India including, without limitation, the government of India, the Reserve Bank of India and the Securities and Exchange Board of India, and to promote microfinance and to help create a favourable policy environment for the microfinance sector.

4. To create, develop, distribute and publicize, sound development, operational, and financial practices, and minimum thresholds of performance for its members, and to encourage other persons engaged in the microfinance sector to adhere to, and comply with, such practices and thresholds.

5. To provide a forum for persons engaged in the field of microfinance to meet, share and exchange their view, expertise, experience and resources.

6. To conduct research, consultancy and training in different aspects of microfinance so as to strengthen the capacity of persons engaged in microfinance.

7. To establish linkages between members and resource institutions, such as funding agencies, financial institutions, rating agencies and training, consultancy and research institutions.

8. To provide services to members, inter alia, training and capacity building; helping in achieving thresholds of performance; providing information related to legal and regulatory issues; providing availability of funding and employment opportunities; and advisory services for performance enhancement and transformation of legal forms.

9. To establish other bodies to support and represent micro finance. Your Honour, the applicant is a premier network coordinating with Reserve Bank of India and assisting them in policy formation and educating and implementing RBI’s direction with various stake holders in the area of microfinance. Various taskforce and committees have been created for fulfilling the objectives. As an Industry Association and SRO, MFIN’s primary objective is to work towards the robust development of the microfinance sector. The Society helps in educating various institutes and facilitates poor’s of the country by making them understand their rights & duties and try to resolve their issues with lending institutions.

MFIN strives to create a favorable environment for the industry to deliver microfinance services with ease. To do this, MFIN invests in building strong relationships with all its stakeholders to ensure that the contribution of microfinance in the national agenda of financial inclusion is well established.

MFIN has established Task Forces for focused action on specific areas of activities that, from an overall industry standpoint, are deemed critical. The Task Forces comprise of representatives of member institutions who help drive specific initiatives with the support of the MFIN Secretariat. The Advocacy & PR Task Force is responsible for steering and guiding the advocacy agenda within MFIN. The Task Force engages with key policy makers and sector participants to create a conducive policy and business environment for the industry. MFIN engages with the key stakeholders of the microfinance Industry including Reserve Bank of India (RBI), National Bank for Agriculture and Rural Development (NABARD), Ministry of Finance (MoF). Small Industries Development Bank of India (SIDBI), Insurance Regulatory and Development Authority (IRDA), Insolvency and Bankruptcy Board of India (IBBI) and Unique

Identification Authority of India (UIDAI). MFIN is also a part of various think tanks and discussion forums including the RBI’s Financial Inclusion Advisory Committee, PSIG Think Tank, and the Access Assist Advisory Group.

Your Honour we assure you, MICRO FINANCE INDUSTRY NETWORK(“applicant”) is working towards betterment of the society and betterment of India’s economy and there is no infringement of objectives of the society. We plead before you to kindly approve the renewal application under section 12AB and oblige.

We shall be pleased to assist you, in case if any clarification/further information is required and we request you to issue show cause notice in case any adverse conclusion is being drawn and provide the assessee sufficient opportunity to clarify.

We hope you will find all the details in order, if any further information or documents as may be desired by you, we shall be obliged to submit.

Power of attorney in favor of ourselves is enclosed (Page no. 20312032)”

10. At the time of hearing of the instant appeal, the Ld. Counsel Mr. S. Krishnan vehemently argued in support of the case made out by the assessee as above and he has drawn our attention to page 58 of the paper book in order to justify that the society is giving educational, social, economic background of micro finance customers, the details whereof is as follows:-

11. He has further drawn our attention to different workshops organized by the assessee in District Forum level including medical camps in 22 flood affected districts in Bihar and Assam, micro finance radar application which is an inhouse application developed to ensure granular field level information available to member institutions in a secured and systematic form. Launched in July, 2021, Radar digitally captures four crucial parameters, repayment challenges, loan pipelining, ring leaders and disturbance created by external inciters. Both qualitatively and quantitatively, this micro level information plays a significant role in flagging ‘early warning symptoms’ to enable microfinance institutions to take timely measures to avert crisis. Skilling and financial literacy workshop has also been done in Punjab as stated by the Ld. counsel appearing for the assessee in support of which he has drawn our attention to pages 66-67 of the paper book. With their guidance, women who did exceptionally across the length and breadth of our country who made a small start and today inspiring others as also evident from different articles, annexed to the paper book from pages 68 to 74 therein. Their contribution to the Indian economy as appreciated by different government authorities are also part of the documents annexed to the paper book particularly, from pages 72 to 80 therein. We have also further considered the auditor’s report of the assessee as formed part of the paper book. Under these facts and circumstances of the matter the activities are found for the welfare of public interest at large.

12. The ld. DR, on the other hand, relied upon the order passed by the authorities below.

13. Upon perusal of the order passed by the Ld.CIT(E), it appears that the Ld. CIT(E) mainly on the following counts rejected the application made by the assessee u/s 12A of the Act:

The assessee’s eligibility for registration has never been scrutinized in the past and the assessee was enjoying the registration on the basis of the CPC’s proforma approval after 01.04.2021 as alleged by the Ld. CIT(A) as it appears from the order impugned. However, from the records, it appears that the provisional registration was granted by and under the order dated 27.01.2021 issued by the CPC appearing at page 1 of the paper book. However, notice dated 20.09.2022 was thereafter issued by the CIT(E), Chandigarh under Section 12A of the Act with the following queries:-

| “1. |

|

Whether the trust/society/company has been granted provisional registration u/s 12AB? If yes, please furnish the self-certified copy of the Form 10AC issued by CPC, Bangalore. |

| 2. |

|

Please specify the date of commencement of activities and furnish documentary evidence(s) to prove beyond doubt that the activities as mentioned in the MoA/trust deed/registration certificate under Societies Registration Act had actually commenced on the above mentioned date along- with the bank(s) statements to substantiate your claim. |

| 3. |

|

Whether the application in Form 10AB has filed within six months from the commencement of activities or within the extended time limit provided vide CBDT instruction/circular/notification, if any? |

| 4. |

|

Please furnish the self-certified copy of MoA/Trust Deed i.e. document creating or establishing the applicant. Also furnish the proofs of the identities of the main / managing trustees/ directors/ president/ secretary of the institution. |

| 5. |

|

Please furnish a self-certified copy of registration with Registrar of Companies or Registrar of Firms and Societies or Registrar of Public Trusts is enclosed? |

| 6. |

|

Whether the applicant is Registered under the Foreign Contribution (Regulation) Act, 2010 (42 of 2010). |

| 7. |

|

If yes, furnish a self-certified copy of Registration under the Foreign Contribution (Regulation) Act, 2010 (42 of 2010)? |

| 8. |

|

Please furnish an affidavit / undertaking to the effect that the institution is complying with all the requirements of law as are material for the purpose of its objects as enumerated in the trust deed/MoA. |

| 9. |

|

Please furnish an undertaking that there will be no infringement to the 1st proviso to Section 2(15) of the Income Tax Act, 1961. |

| 10. |

|

Whether any part of income of the institution enures, directly or indirectly the benefit of a person specified u/s 13(3) of the Income Tax Act, 1961. |

14. In response whereto the assessee filed reply on 28.09.2022 with the following details annexed to the paper book at pages 6 to 8:-

15. Upon considering the reply filed by the assessee and further considering the evidences adduced by the assessee in support of the reply in terms of the queries made by the ld. CIT(E), the order u/s 12A was passed on 30.09.2022 appearing from pages 10-13 of the order mentioning that “after considering the application of the applicant and the material available on record, the applicant is hereby granted registration/approval for assessment years mentioned at Sl. No.8 above subject to the conditions mentioned in Raw No.12.” The conditions imposed therein are as follows:-

| 1. |

|

The registration is being granted under section 12AB(1)(b) of the Income Tax Act, 1961. |

| 2. |

|

As and when there is a move to amend or alter the objects/rules and regulations of the applicant, prior approval of the Commissioner of Income Tax shall be sought along with the draft of the amended deed and no such amendment shall be effected until and unless the approval is accorded. |

| 3. |

|

In the event of dissolution, surplus and assets shall be given to an organization, which has similar objects and no part of the same will go directly or indirectly to anybody specified in section 13(3) of the Income Tax Act, 1961. |

| 4. |

|

In case the trust/institution is converted into any form, merged into any other entity or dissolved in any previous year in terms of provisions of section 115TD, the applicant shall be liable to pay tax and interest in respect of accreted income within specified time as per provisions of section 115TD to 115TF of the Income Tax Act, 1961 unless the application for fresh registration under section 12AB for the said previous year is granted by the Commissioner. |

| 5. |

|

The Trust/ Institution should quote the PAN in all its communications with the Department. |

| 6. |

|

The registration u/s 12AB of the Income Tax Act, 1961 does not automatically confer any right on the donors to claim deduction u/s 80G. |

| 7. |

|

Order u/s 12AB read with section 12A does not confer any right of exemption upon the applicant u/s 11 and 12 of Income Tax Act, 1961. Such exemption from taxation will be available only after the Assessing Officer is satisfied about the genuineness of the activities promised or claimed to be carried on in each Financial Year relevant to the Assessment Year and all the provisions of law acted upon. This will be further subject to provisions of section 2(15) of the Income Tax Act, 1961. |

| 8. |

|

No change in terms of Trust Deed/ Memorandum of Association shall be effected without due procedure of law and its intimation shall be given immediately to Office of the Jurisdictional Commissioner of Income Tax. The registering authority reserves the right to consider whether any such alteration in objects would be consistent with the definition of “charitable purpose” under the Act and in conformity with the requirement of continuity of registration. |

| 9. |

|

The Trust/ Society/ Non Profit Company shall maintain accounts regularly and shall get these accounts audited in accordance with the provisions of the section 12A(1)(b) of the Income Tax Act, 1961. Seperate accounts in respect of each activity as specified in Trust Deed/ Memorandum of Association shall be maintained. A public notice of the activities carried on/ to be carried on and the target group(s) (intented beneficiaries) shall be duly displayed at the Registered/ Designated Office of the Organisation. |

| 10. |

|

The Trust/ Institution shall furnish a return of income every year within the time limit prescribed under the Income Tax Act, 1961. |

| 11. |

|

Separate accounts in respect of profits and gains of business incidental to attainment of objects shall be maintained in compliance to section 11 (4A) of Income Tax Act, 1961. |

| 12. |

|

The registered office or the principal place of activity of the applicant should not be transferred outside the jurisdiction of Jurisdictional Commissioner of Income Tax except with the prior approval. |

| 13. |

|

No asset shall be transferred without the knowledge of Jurisdictional Commissioner of Income Tax to anyone, including to any Trust/ Society/ Non Profit Company etc. |

| 14. |

|

This certificate cannot be used as a basis for claiming non-deduction at source in respect of investments etc. relating to the Trust/ Institution.” |

16. Under these particular facts and circumstances of the matter, therefore, the assessee’s eligibility for registration had never been scrutinized in the past as alleged by the Ld.CIT(E) is found to be misconceived. Relevant to mention that from the said office, the impugned order of cancellation of registration has been passed on dissatisfaction on the conditions prescribed under section 12AB of the Act. The ld.CIT(E) while cancelling the registration of the assessee further alleged that the assessee’s organizational structure mimics commercial establishment, it is controlled by the senior executives and incurring heavy expenditure making payments for advertising, public relations, campaigns funding whereof are appearing from pages 7 to 23 therein whereas we find that the as the RBI appointed Regulatory entity and industry platform for the micro finance sector, the assessee is composed of economists, financial/regular experts, bankers at the highest level as it is evident from different documents annexed to the paper book filed by the assessee the contents whereof has not been able to be controverted by the Ld. DR. The activities of the assessee has already been explained hereinabove which has also formed part of the order impugned establishes the need for advertising and public expenses to raise consumer awareness and to rationalize the tenor of events and the activities conducted by the assessee. Participation in CII conclaves and Asia level conferences by the assessee cannot be at the assessee’s ipse-dixit. The Act does not determine particularly the provision of Section 12A of the Act that entities structured and working like corporate bodies cannot be held as charitable in nature. We note that the entire details of expenditure incurred by the assessee in holding such activities at highest level are on record annexed to the paper book filed before us. The organization of the assessee is comprising of economists, bankers, senior finance regulators, professionals of the highest competency level to regulate the micro finance industry, running programmes and research work for Reserve Bank of India. Further that during the scrutiny proceedings, the assessee’s application for registration, specific queries were raised by the same authority being the CIT(E), Chandigarh asked to the benefit under Section 13(3) of the Act and the instance of any activities in the nature of trade, commerce or business as it is evident from paras 8 and 9 of the notice dated 13.03.2025 appearing at page 15 of the paper book, the contents whereof is as follows:-

“8. Please furnish an undertaking that there is no infringement to the 1st proviso to Section 2(15) of the Income Tax Act, 1961. In this regard, please provide the following information:-

“Whether applicant provides all its services free of cost or charges any amount by whatever name called for its activities from beneficiary at cost or nominal margin. Please specify the amount justifying the same in the light of section 2(15). Please specify the clause no of deed in this regard or any other documentary evidence.”

9. Whether any part of income of the institution enures, directly or indirectly for the benefit of a person specified u/s 13(3) of the Income Tax Act, 1961.”

17. No adverse inference in regard to the issues as raised upon queries to the assessee is found to have been made by the Ld.CIT(E). It is the further allegation made against the assessee that application u/s 12A of the Act filed by the assessee as the activities of sector coordination, grievance reddressal and policy engagement was neither altruistic nor charitable even when the activities of the assessee is found to have been done effectively as it is evident on record. The nature of activity is of regulator duty undertaken upon supervision of RBI and there is no element of record of public benefit to non-members of the assessee network and, therefore, the general public has no stake in the organization as alleged by the Ld.CIT(E) is apparently found to be not acceptable. In the foregoing paragraph, we have already mentioned the activities performed by the assessee which is found to have been misinterpreted by the Ld.CIT(E) holding as dispute resolution between the assessee’s network members whereas evidences galore annexed to the paper book establishes the fact of performing activities inter alia through toll free grievance redressal system in 12 languages for micro finance borrowers, as a regular function for the industry as a whole, programmes for borrower education, protection, surveillance and self-help group which has direct benefit to the end users including the poorest of the poorer of the society as micro finance loan by its definition is a collateral-free loan given to a household having annual income of below Rs.3 lakhs is one of the major activities found to have been performed by the assessee. These workshops are specifically held for protection of the borrowers from micro money lenders which cannot be ignored in the present scenario. Unless the assessee is found to be carrying on the business or trade mainly the assessee is working only to serve its members’ interest, the assessee is still be entitled to registration as an entity engaged in advancement of an object of general public utility since regulation of an industry itself enures for the utility of the consumers of the said industry which is nothing, but, for the general public at large as claimed having been performed by the assessee. Reliance has been placed by the Ld. counsel appearing for the assessee on the order passed the Hon’ble Supreme Court in the case ACIT v. Ahmedabad Urban Development Authority (SC) and on the order of the ITAT in Kush Innovative Foundation v. CIT(E) (Delhi – Trib.)/ ITAs No.3456 & 3457/Del/2024 dated 12.02.2025. While deciding the issue whether the receipts are within the limit prescribed by sub-clause (ii) of Proviso to Section 2(15) of the Act, the Hon’ble Supreme Court has in the identical facts and circumstances of the matter observed as follows:-

“201. The question that arises is whether the change in definition impacts the claims of trade promotion bodies, federations of commerce, or such organizations, that they are GPU charities . The judgment in Surat Art Silk (supra) proceeded on the assumption that trade promotion was the predominant object of the GPU charity before the court, and that other objects – including procuring licences, trade etc. were incidental. The assessee in Surat Silk had clear trading objects:

“(b) To carry on all and any of the business of Art Silk Yarn, Raw Silk, Cotton Yarn as well as Art Silk floth, Silk Cloth and Cotton Cloth belonging to and on behalf of the members.

*** ***** **** *** ****

(e) To buy and sell and deal in all kinds of cloth and other goods and fabrics belonging to and on behalf of the Members.”

This court, nevertheless, held that since the predominant object of the assessee was trade promotion, while furthering it, the fact that some trading occurred, leading to income, did not preclude the assessee from claiming tax exemption.

202. In the opinion of this court, the change in definition in Section 2(15) and the negative phraseology – excluding from consideration, trusts or institutions which provide services in relation to trade, commerce or business, for fee or other 115 consideration – has made a difference. Organizing meetings, disseminating information through publications, holding awareness camps and events, would be broadly covered by trade promotion. However, when a trade promotion body provides individualized or specialized services – such as conducting paid workshops, training courses, skill development courses certified by it, and hires venues which are then let out to industrial, trading or business organizations, to promote and advertise their respective businesses, the claim for GPU status needs to be scrutinised more closely. Such activities are in the nature of services “in relation to” trade, commerce or business. These activities, and the facility of consultation, or skill development courses, are meant to improve business activities, and make them more efficient. The receipts from such activities clearly are ‘fee or other consideration’ for providing service “in relation to” trade, commerce or business.

203. The revenue has appealed to this court, in respect of two assessment years, in the case of Apparel Export Promotion Council (AEPC). The objects of AEPC, which was set up in 1978 – include promotion of readymade garment export. To achieve that end, its objects include providing training to instil skills in the workforce, to improve skills in the industry; guide in sourcing machinery; to serve as a body advising, providing information on market or technical intelligence; assisting the concerned industry in obtaining import licenses; showcase the best capabilities of Indian garment exports through the prestigious “India International Garment Fair” organised twice a year by AEPC, etc. These fairs host over 350 participants who exhibit their garment designs and patterns. Other functions are to provide information, and to provide market research. AEPC also assists in developing new design patterns and garments and to perform promotional activities in individual foreign markets. Further, AEPC sends missions and trade delegations abroad, who participate in international fairs; and conducts surveys to gather information on potential export of ready-made garments.

204. As part of its functioning, it also books bulk space, which is then rented out to individual Indian exporters, who showcase their products and services, and ultimately secure export orders. Towards these services, i.e., booking and providing space, AEPC charges rentals. Now, these rents are not towards fixed assets owned by it. They are in fact charges, or fees, towards services in relation to business; likewise, the skill development and diploma courses conducted by it, for which fees are charged, are to improve business functioning of garment exporters. Furthermore, market surveys and market intelligence, especially country specific activities, aimed at catering to specified exporters, or specified class of exporters, is also service in relation to trade, commerce or business.

205. In the circumstances, it cannot be said that AEPC’s functioning does not involve any element of trade, commerce or business, or service in relation thereto. Though in some instances, the recipient may be an individual business house or exporter, there is no doubt that these activities, performed by a trade body continue to be trade promotion. Therefore, they are in the “actual course of carrying on” the GPU activity. In such a case, for each year, the question would be whether the quantum from these receipts, and other such receipts are within the limit prescribed by the sub-clause (ii) to proviso to Section 2(15). If they are within the limits, AEPC would be – for that year, entitled to claim benefit as a GPU charity.”

18. We note that though the notice dated 13.03.2025, the Ld.CIT(E) passed specific queries as to the applicability of proviso to Section 2(15) of the Act i.e., the activity is in the nature of trade, commerce or business, etc., the provision was not found to have been invoked ultimately upon receipt of details and response from the assessee which is required to be considered in its proper perspective; the assessee involved in any trade, business or commerce has not found place in the order. Merely stating that the assessee is not involved in any public benefit programmes and unless it is engaged in trade or commerce or business is to be reckoned as a charitable entity under the ‘general public utility’ under the provision of Section 2(15) of the Act, the claim of the assessee in our considered opinion is again required to be revisited by the Ld.CIT(E) keeping in view the ratio laid down by the Hon’ble Apex Court in the matter of Ahmedabad Urban Development Authority (supra) particularly, in the light of the observations made by us hereinabove.

19. Under the facts and circumstances of the matter, judgement relied upon by the Ld. AR in the case of Ahmedabad Urban Development Authority(supra) is found to be applicable and, thus, the issue is remitted to the file of the Ld. CIT(E) to adjudicate afresh in the light of the observations made by the Hon’ble Supreme Court as explained hereinabove.

ITA No.5878/Del/2025

20. In this matter, the rejection of grant of approval under Section 80G is under challenge which is consequential to the registration under Section 12AB of the Act which has been directed to be decided by the Ld.CIT(E) in appeal No.5879/Del/2025. Thus, the issue raised in this appeal is further remitted to the file of Ld.CIT(E) to pass orders accordingly.

21. In the result, the appeals of the assessee are allowed for statistical purpose.