ORDER

Anubhav Sharma, Judicial Member. – These are appeals preferred by both the Revenue as well as the Assessee against the orders of the Ld. Commissioner of Income-tax (Appeals)-26, New Delhi (hereinafter referred to as the ‘Ld. First Appellate Authority or ‘the Ld. FAA’ in short) in appeals filed before him against the orders dated 31.03.2022 of the ld. Asstt. Commissioner of Income-tax, Central Circle-13, New Delhi (hereinafter referred to as the Ld. AO, for short) passed u/s 153A r.w.s. 143(3)/143(3) of the Income-tax Act, 1961 (hereinafter referred to as ‘the Act’). Further details of the orders of the lower authorities are as under:-

| ITANo. & Assessment Year |

Appeal No. & Date of order of the CIT(A) |

| ITANo.3094/Del/2023, AY: 2012-13(R) |

10128/2011-12, dated 11.08.2023 |

| ITANo.3413/Del/2023, AY: 2016-17(A) |

11116/2015-16, dated 06.09.2023 |

| ITANo.3144/Del/2023, AY : 2017-18(A) |

10764/2016-17, dated 20.09.2023 |

| ITANo.3422/Del/2023,AY : 2017-18(R) |

– do – |

| ITANo.3145/Del/2023, AY : 2018-19(A) |

10558/2017-18, dated 25.09.2023 |

| ITANo.3423/Del/2023, AY : 2018-19(R) |

-do- |

| ITA No.3146/Del/2023, AY, 2019-2020 |

10612/2018-19, dated 20.09.2023 |

| ITANo.3424/Del/2023, AY : 2019-20(R) |

-do – |

| ITANo.3147/Del/2023, AY : 2020-21(A) |

10570/2019-20, dated 15.09.2023 |

| ITANo.3425/Del/2023, AY : 2020-21 (R) |

-Do – |

| ITANo.3148/Del/2023, AY : 2021-22(A) |

10021/2020-21, dated 20.09.2023 |

| ITA No.3426/Del/2023, AY: 2021-22(R) |

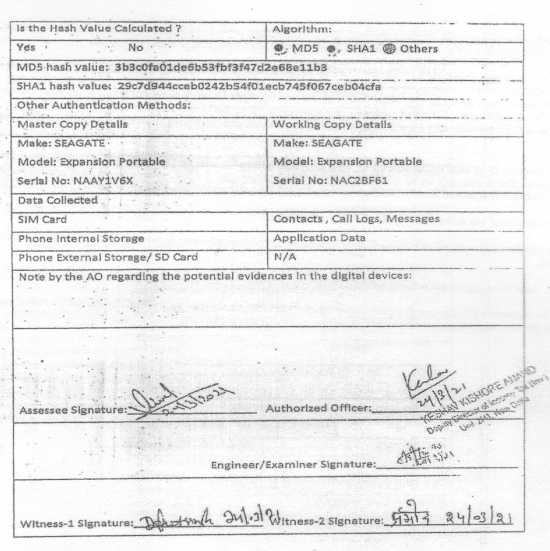

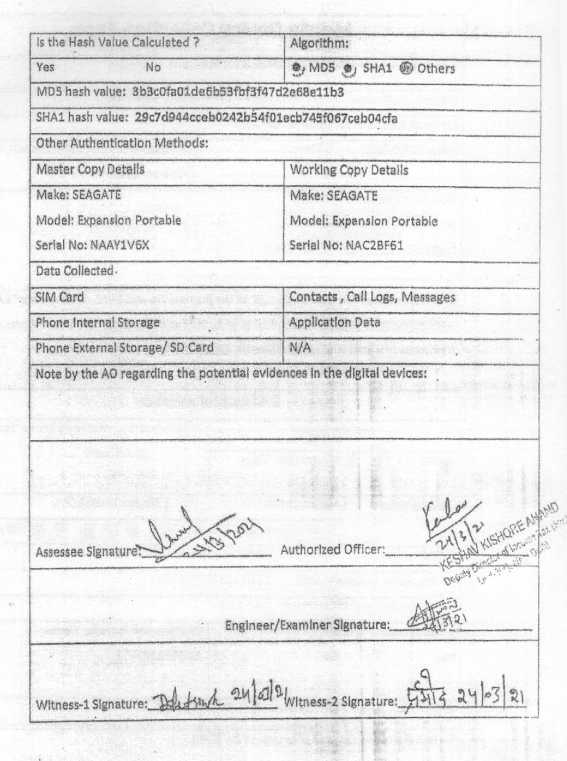

-Do – |

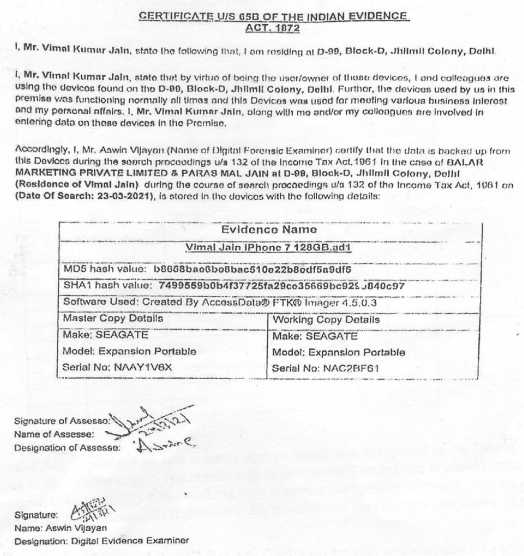

2. Heard and perused the records. The brief background of impugned assessment are that a search and seizure operation u/s 132 of the Income Tax Act, 1961 was conducted on 23.03.2021 and on subsequent dates in the case of Balar Marketing Pvt Ltd, Sh. Parasmal Jain. The group was originally into marketing and trading of copper wires and other similar goods. They were known in market by the name of Kundan Cables and now they have a brand of “Fybros”. They are manufacturing copper wires and cables and various other electrical equipment. The group companies is alleged to be involved in out of books sales, out of books purchases, bogus purchases, raising bogus share capital and share premium from dummy entities and several cash expenses. During the course of assessment AO examined the issue observing that during the course of Search Proceedings at residence premise of Sh. Vimal Jain, D-99, Block-D, Jhilmil Colony, Delhi on 23.03.2021, various electronic devices such as Hard Disk , Mobile Phone, Pendriveetc were found and seized and the same were Annexurized as A1 to A3. During examination of this Annexures A1 to A3, allegedly various incriminating evidences were found that includes the exchange of Cash Tokens through Hawala Network of M/s. Balar Marketing Private Limited with various sales and purchase parties. Shri Vimal Jain, who is working as the Administrative Head in M/s BalarMarketing Private Limited allegedly admitted in his statement that he made cash transactions for M/s Balar Marketing Private Limited which was executed through Hawala route. Sh.Vimal Jain in his statement recorded under section 132(4) and 132 (1A) has allegedly explained the modus operandi of the cash sales and has admitted that the assessee company has sold goods in cash to various parties. Further, during the course of search proceedings, digital data was extracted/cloned from the two phones of Shri Vimal Jain (iPhone 7 and Panasonic). On analysis of this digital data, allegedly Whatsapp as well as SMS chats were said to be found in the phone of Shri Vimal Jain which allegedly pertained to payment as well receipt of cash from various sale and purchase parties via exchange of Tokens. AO records that on analysis of whatsapp chat of Sh. Vimal Jain, extracted from cloned copy (working copy) of mobile (I phone 7 and Panasonic) of Shri Vimal Jain, seized during the course of search proceedings and marked as Annexure A-1, it was found that the assessee company has sold goods to 17 parties in cash. Sample Screenshot of the whatsapp chat in relation to cash sales transaction with the 17 parties has been made part of assessment order and is attached as Annexure-B. During the course of search proceedings and post search proceedings, it was also allegedly gathered that the assessee company is maintaining its parallel books of account in software namely ‘Sambhavsoftaware’, which contains the images of cash transaction undertaken by the assessee company. Further, during the post search proceedings Sh. Vimal Jain in his statement u/s 131(1A) of the IT Act,1961, in response to Q10 clarified that year mentioned in the Sambhavsoftware images are moved to 10 years back and amounts moved 2 digits back. Further cash transaction which are out of books is recorded in Sambhav Software by the name of “Bhaga”. Further out of books cash sales images which have been extracted from Sambhav software found from the mobile of Sh. Vimal Jain. Sample images are made part of assessment order and are attached as Annexure C. During the course of Post Search Proceedings, Statement of Shri Paras Mal Jain was recorded on oath under section 131(1A) of the Income Tax Act.(Copy of the above stated statements have been made part of assessment order and are attached as Annexure D) Shri Paras Mal Jain has allegedly admitted unaccounted cash transactions of Shri Vimal Jain with various parties on behalf of M/s Balar Marketing Private Limited. In his statement he has admitted that the assessee company was maintaining parallel books of accounts for recording cash transactions. Allegedly, he further confirmed the validity of the statement recorded of Sh. Vimal Jain in which he has explained the modus operndi of the cash transactions undertaken by the assessee company and identified the parties with which the assessee company has entered into cash transactions. Based on the above information, assessee was called upon to show cause but no explanation was received so an exercise was done by ld. AO to reconcile the various token found and seized during the course of search proceedings. A date wise excel sheet of token exchange by Vimal Jain with other person was prepared by AO. Accordingly various additions were made of which ld. CIT(A) has given partial relief to the assessee for which both the assessee and revenue are in appeal.

3. On appreciating the contentions of ld. representatives of both the sides, we consider it appropriate to first adjudicate on two important aspects giving rise to two different grounds of appeal, but, which somehow we find connected also. The ld. AR for the assessee has submitted that the whole case of the AO rests on alleged incriminating material extracted from two phones seized from Mr. Vimal Jain who was the administrative head of the appellant company and, apart from images of computer screen displayingSambhav Software and Whatsapp chats, no other incriminating evidence was found from any of the premises which was searched and, therefore, the evidentiary value of the seized devices phones and the extracted images should be established in accordance with the law and, more so, in accordance with the provisions of section 65B of the Indian Evidence Act, 1872 (as then applicable and hereinafter referred as Evidence Act).

3.1 Thus, the contention of the ld. AR is that in the absence of valid certificate u/s 65B, the secondary evidences in the form of images of computer screen of Sambhav software found from the mobile phone of Mr. Vimal Jain, wherein alleged out of books transactions were recorded, cannot be relied and similar is the fate of whatsapp chats.

4. Then, based on the nature of evidences relied by the AO, and various additions as made, it was submitted that the approval granted u/s 153D of the Act by the Addl. CIT, Central Range-4, New Delhi, is not in accordance with the law. The ld. AR has relied various judicial decisions of the Hon’blejurisdictional Delhi High Court in the case of Pr. CIT v. Shiv Kumar Nayyar(Delhi)/[2024] 467 ITR 186 (Delhi); Pr. CIT v. Anuj Bansal (SC)/[2024] 466 ITR 254 (SC),and the decision of the Hon’ble Supreme Court in the case of ACIT v. Serajuddin & Co.(Orissa)/[2023] 454 ITR 312 (Orissa), wherein the decision of the Hon’ble Orissa High Court quashing the assessment on the basis of mechanical approval has been sustained by the Hon’ble Supreme Court.

5. Ld. DR has defended these issues with contention that firstly provision of Evidence Act are not applicable in tax assessment proceedings. It was submitted that even otherwise necessary complia nces were made by getting E-Certificate and maintaining records of seizure of electronic evidences. As with regard to questioning approval granted u/s 153D of the Act, ld. DR has primarily asserted that its only administrative function and other wise the competent authority is always aware of all the issues involved and questionnaire raised and findings of AO, so competent authority had sufficient time to grant approval. The contentions shall be considered in detail later, where relevant.

5. 1 In regard to the first issue of extent of admissibility of electronic evidences, the order of the ld.CIT(A) is relevant to be mentioned wherein we find that as this ground was raised before the ld.CIT(A), the same was not sustained by the ld.CIT(A) by holding in para 7.3 of the order dated 20.09.202 in AY 2017-18 firstly that during the assessment proceedings the appellant assessee has never asked for such certificates and has never denied that such information was found from the mobile phone of Shri Vimal Jain, who was handling all the hawala transactions of the assessee. Further, in the opinion of the ld.CIT(A) such certificates are required in criminal proceedings and assessment being a civil proceeding, certificate u/s 65B(4) of the Indian Evidence Act is not relevant under the Income-tax Act, 1961. Accordingly, this plea of the assessee was dismissed.

6. To examine these two issues it is relevant to keep in mind as to what is the case of assessing officer and what is the material relied by him to draw conclusions. If we go comprehensivelythrough the assessment orders, we find that assessing officer has relied the electronic evidences alone for most of the additions in different AYs, which we have clubbed in the form of following issues;

Issue no. 1.

Addition on account of alleged unaccounted sales. The issue is common to AY 2016-17, 2017-18, 2018-19, 2019-20, 2020-21 and 2021-22. Both assessee and revenue are in appeal.

Issue no. 2

Addition on account of alleged bogus unsecured loans from Arham Finance and Investment Services Ltd. u/s 69C of the Act. The issue is common to AY 2017-18, 2018-19, 2019-20, 2020-21 and 2021-22

Issue no. 3

Addition on account of alleged commission paid to M/s Arham Finance and Investment Services Ltd. to obtain loan. Issue is common to AY 2019-20, 2020-21 and 2021-22

Issue no. 4.

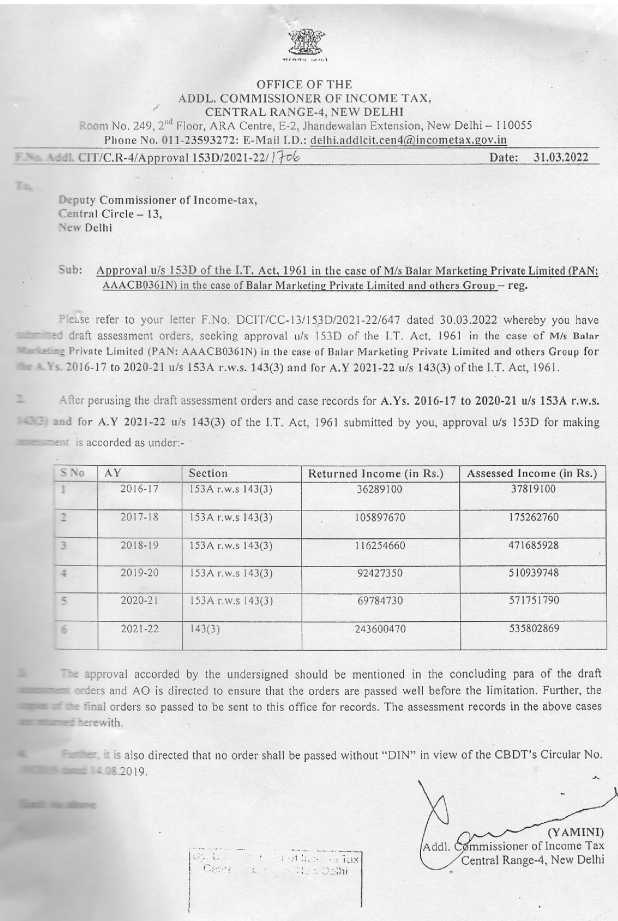

Addition on account of unexplained peak investment. Issue relates to AY 2017-18

Issue no. 5

Addition on account of unexplained peak balance of cash receipts. Issue relates to AY 2017-18

Issue no. 6

Addition on account of alleged bogus purchases from Devansh Wire and Cable Pvt. Ltd. The issue is common in AY 2017-18, 2018-19, 2019-20, 2020-21 and 2021-22. The revenue is in appeal on this issue in all the AY

Issue no. 7

Addition u/s 40A(3) of the Act on account of cash purchase. Issue is common AY 2017-18, 2018-19, 2019-20, 2020-21 and 2021-22. Revenue is in appeal on this issue.

Issue no. 8

Addition on account of alleged bogus purchase from Copoor Industries Pvt. Ltd. The issue is common to AY 2012-13. Assessee and revenue both are in appeal.

Issue no. 9

Addition on account of alleged bogus purchases from Brilliant Metals Pvt. Ltd. and ManojGarg. The issue is common to AY 2019-20, 2020-21 and 2021-22. Assessee and revenue are in appeal in AY 2019-20 while revenue is in appeal in all these years.

Issue no. 10

Addition on account of salary paid to VineetBaidRs. 75,000/- and to Vimal Jain of Rs. 14,40,000/- The issue pertains to AY 2020-21. The assessee is in appeal.

Issue no. 11

Addition made on account of sale of LED. The assessee is in appeal.

Issue no. 12

Addition on account of unexplained investment in stock. Issue pertains to AY 2021-22. The assessee is in appeal.

Issue no. 13

Addition on account of difference in rate of copper and DM water. Issue pertains to AY 2021-22. Assessee is in appeal.

Issue no. 14

Addition made on account of cash found during search. Issue pertains to AY 2021-22. The assessee is in appeal.

7. Admittedly, the alleged incriminating evidences were extracted from iPhone and a Panasonic Eluga phone recovered from Mr. Vimal Jain and, apart from that, none of the devices including phones, laptop, pen drives, HDD found from Mr. Paras Mal Jain or his family members connected with the assessee firm were found relevant and had no information relevant to the impugned additions. Not even whatsapp chats with Mr. Paras Mal or any other employee of assesseewere found which would show that Mr. Vaimal Jain was dealing with anyone on behalf of the assessee.

7.1 We are of the considered view that when the allegations are of out of books transactions then apart from so called admission of Mr. Paras Mal, some corroborative evidence must have exited to show that goods were being manufactures, sold, purchased, cash was being received.

7.2 AO mentions of the various phone numbers found in the alleged incriminating material and for which statement of Mr. Vimal Jain was relied to conclude about their identity and also as to what was the nature of transactions with these persons, but AO otherwise did not consider it necessary to make any enquiry of his own to find the identity of these persons and to see as to actually what was the possible transactions.

7.3 Then we have extensively examined the statement recorded of Mr. Vimal Jain with regard to alleged incriminating evidences in the form of images of Sambhav software and Whatsapp chats and except for mentioning in his statement repeatedly that there were hawala transactions, there is no material to corroborate independently that these transactions were not mere hawala transactions, but, were business transaction of out of books purchase and sale as no corroborating material from any books or documents are found or relied. No incriminating evidences of any sort, except the digital devices taken into possession, was found from the business premises of the assessee. No discrepancies in any of the financials have been found which will show that the assessee was indulging in any act of producing goods and transporting goods or buying goods and selling them beyond the transactions as recorded in the books of account duly maintained.

7.4 Thus the only evidence is images of ‘Sambhav software’, which is definitely a secondary piece of electronic evidence as the original software was not found in search and it seems AO had also not tried to get this software from Mr. Vimal Jain or the assesse by way of any notices.Then the other evidences are whatsapp chats of Mr. Vimal Kumar with some persons with he was exchanging ‘tokens’, which allegedly formed modus of payments of out of book purchases and sales. This too is electronic evidences. Thus we have to examine if these two electronic evidences were legally relevant, admissible and independently of any corroboration could have been basis of drawing conclusions and complete the assessment.

8. Now, as with regard to the issue of admissibility of electronic evidences, the ld. AR has heavily relied upon the Digital Evidence Investigation Manual,2014 (hereinafter called ‘the Manual’) of the Central Board of Direct Taxes to submit that a detailed procedure has been provided by the Board with regard to collection of digital evidences and the manner in which the same has to be relied during the assessment proceedings.

9. Here,at outset, we find it necessary to observe that this Manual is in the instructions though may not have been issued u/s 119 of the Act,but certainly form of atleast good practices, which Board has found fundamental and necessary to add credibility to electronic evidences. The Manual is self contained code where Board has consciously and very articulately examined various facet of collection, examining and reproducing the digital evidences in assessment orders, on the basis of judicial decisions and provisions of law as enshrined in Evidence Act or Information Technology Act, 2000, and then laid down instruction to be followed by the officers of the department.

10. To bolster this conclusion of ours, we would like to observe that the CBDT in its Manual while feeling the relevance of the question with regard to admissibility of electronic evidences and taking note of sea change in the information and technology used in the business transactionshas observed as to how inrelevant statutes, provisions have been made with regard to recognizing electronic record as admissible evidence and as for convenience we reproduce the aforesaid from para 1.1 of the Manual:-

“The law of the country has also taken cognizance of this reality.The InformationTechnology Act, 2000 has been enacted recognizing electronic records as evidence, governing access to and acquisition of digital and electronic evidence from individuals, corporate bodies and/or from the public domain. By way of this enactment, amendments were also brought in other laws like Indian Penal Code, Indian Evidence Act and Criminal Procedure Code, (Cr.PC). The Income-tax Act, 1961 has also been amended thrice by way of Finance Act 2001, Finance Act 2002 and Finance Act 2009 thereby according recognition to electronic evidence, facilitating access to them and giving when need be, powers to impound and seize them. By Finance Act, 2001, Clause (22AA) was inserted in Section 2 to provide that the term “document” in Income Tax Act, 1961, includes an electronic record as defined in clause (t) of sub-section (1) of section 2 of the Information Technology Act, 2000. By Finance Act, 2002, Clause (iib) was inserted in Sub-Section (1) of Section 132 requiring any person who is found to be in possession or control of any books of account or other documents maintained in the form of electronic record as defined in clause (t) of sub-section (1) of section 2 of the Information Technology Act, 2000 (21 of 2000), to afford the authorised officer the necessary facility to inspect such books of account or other documents; and by Finance Act, 2009, clause (c) was inserted in sub-section (1) of Section 282 providing that service of notice in the form of any electronic record as provided in Chapter IV of the Information Technology Act, 2000 (21 of 2000) will constitute valid service.”

11. In this context, it can be further observed that in para 1.5 the objectives of the Manual are mentioned which states that the aim of this Manual is to apprise the user of “basic legal provisions relating to digital evidence in Income-tax Act and other laws including Information Technology Act and Indian Evidence Act.”

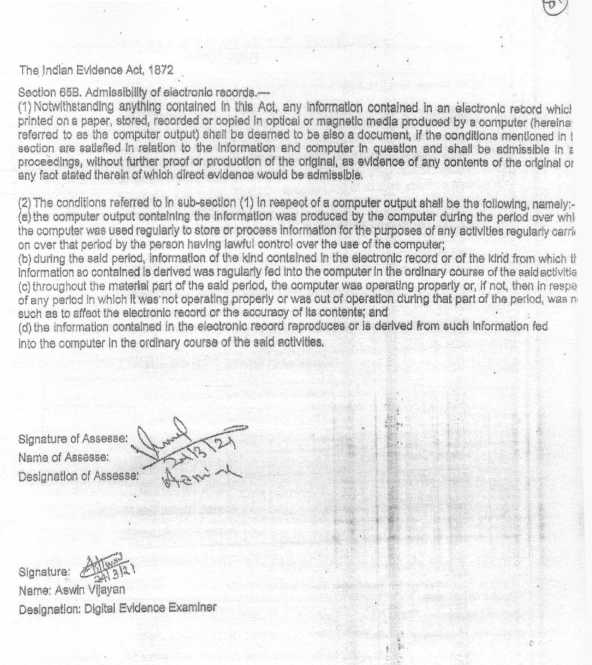

12. Then, to counter the assertion of ld. CIT(A) and ld. DR too, that provisions of Section 65B of Indian Evidence Act are not applicable to income tax assessment proceedings, we would like to reproduce from this Manual as to how the Board perceived the relevance of various provisions of the different statutes and how specifically referred to the provisions of section 65A and 65B of the Indian Evidence Act, 1872 and directed that “accordingly while handling any digital evidence, the procedure has to be in consonance of these provisions.”. The relevant part in para 2.7.3 is as follows:-

“2.7.1The Information Technology Act-2000 has been enacted to provide legal recognition to transactions carried out by means of electronic data interchange and other means of electronic communication, which involve the use of alternatives to paper-based methods of communication and storage of information. The same enactment has also brought amendments in the Indian Penal Code, 1861, the Indian Evidence Act, 1872, the Bankers’ Books Evidence Act, 1891 and the Reserve Bank of India Act, 1934.

2.7.2 As far as Income-tax Act, 1961 is concerned, it has been amended thrice by way of Finance Act, 2001, Finance Act, 2002 and Finance Act, 2009 respectively.

| • |

|

By way of first amendment, provisions of sub-section (12A) of section 2 was inserted to give legal recognition to the books of account maintained on computer and sub-section (22A) to section 2 was inserted to provide definition of ‘document’ which included “electronic record” as defined under Information Technology Act 2000. |

Under Information Technology Act 2000 an electronic record has been defined to include data, record or data generated, image or sound stored, received or sent in an electronic form or micro film or computer generated micro file. This definition of electronic record is wide enough to cover person in possession of computer, storage device, server, mobile phone, i-Pod or any such device.

The above amendment has thus specifically given recognition to electronic record as admissible evidence at par with a ‘document’. Further, the powers to impound/copy a document during a survey action u/s 133A and power to seize a document during a search and seizure operation has also been automatically extended to electronic records as a result of the amendment.

| • |

|

By way of second amendment, provisions of section 132 (l)(iib) were inserted facilitating access to the electronic devices including computer, containing document or books of accounts in the form of electronic records by making it obligatory for the person under control of such device to afford the necessary facility to inspect such records. |

By Finance Act, 2009, clause (c) was inserted in sub-section (1) of Section 282 providing that service of notice in the form of any electronic record as provided in Chapter IV of the Information Technology Act, 2000 (21 of 2000) will constitute valid service.

2.7.3 Under Indian Evidence Act there are several references to documents and records and entries in books of account and their recognition as evidence. By way of the THE SECOND SCHEDULE to the Information Technology Act Amendments to the Indian Evidence Act have been brought in so as to, incorporate reference to Electronic Records along with the document giving recognition to the electronic records as evidence.

Further, special provisions as to evidence relating to electronic record have been inserted in the Indian Evidence Act, 1872 in the form of section 65A & 65B, after section 65. These provisions are very important. They govern the integrity of the electronic record as evidence, as well as, the process for creating electronic record.

Importantly, they impart faithful output of computer the same evidentiary value as original without further proof or production of original. Accordingly, while handling any digital evidence, the procedure has to be in consonance of these provisions.

2.7.4 Under Indian Penal Code several acts of omission and commission relating to various documents and records are treated as offences. By way of the THE FIRST SCHEDULE to the Information Technology Act, Amendments to the Indian Penal Code have been brought in, so as to incorporate reference to Electronic Records along with the document.”

13. To deal with the issue further as to how far the Evidence Act is applicable or not to the assessment proceedings under the Act, in more comprehensive manner, we take note of certain provisions of the Income Tax Act 1961, which indicate as to how, though not strictly applicable, the jurisprudential concepts of law of evidence, as enshrined under the Evidence Act, find their place, in proceedings under the Income Tax Act 1961.Thereby establishing that in assessment proceedings also these jurisprudential concepts of law of evidence are relevant and need to be followed.

13.1 In this regard, the foremost thing to consider is that section 3 of the Evidence Act describes ‘evidence’ with inclusive definition by bringing in scope all statements as oral evidences and all documents including electronic records as documentary evidences. The Income Tax Act 1961, however, independently does not define ‘evidence’, relevant and admissible for assessment proceedings. So the concept of evidence as provided and interpreted under law of evidence is relevant in assessment proceedings as well.

13.2 Further Section 17 of the Evidence Act, defines, ‘Admission’ as a”statement, oral or documentary or contained in electronic form which suggests any reference as to any fact in issue or relevant fact.” However, it to keep in mind thatin the case of Pullangode Rubber Produce Co. Ltd. v. State of Kerala [1973] 91 ITR 18 (SC)andCIT v. S. Khader Khan Son (SC)/[2013] 352 ITR 480 (SC)], the Hon’ble Supreme Court, in reference to proceeding under the Act itself has held that “an admission is an extremely important piece of evidence but it cannot be said that it is conclusive.

13.3 Then Section 3 of Evidence Act, further explains the concept of ‘proved’ wherein it is said that a fact is said to be proved when after considering ‘the matters before it’, the court either believes it to exist, or considers its existence so probable that a prudent man ought, under the circumstances of the particular case, to act upon the supposition that it exists. This definition of ‘proved’ uses the words, ‘after considering the matters before it’ and does not refer to merely evidences. Thus, it is not only the evidences, but, matter as a whole on record gives the court opportunity to draw an inference about the existence or nonexistence of fact.

13.4 The ld. tax authorities likeanyotherquasi judicial authorities when entering into any inquiry to reach a conclusion on the basis of evidences, also rely the statements in the form of oral evidences or documents including electronic records called documentary evidences which form substantive material for believing a fact to exist or otherwise existing either by way of a conclusive opinion on the basis of a prudent man approach.

13.5 In this context, the provisions in section 143(2) and 143(3) of the Income Tax Act 1961 become relevant and which are reproduced below:-

“143(2) Where a return has been furnished under section 139, or in response to a notice under sub-section (1) of section 142, the Assessing Officer or the prescribed income-tax authority, as the case may be, if, considers it necessary or expedient to ensure that the assessee has not understated the income or has not computed excessive loss or has not under-paid the tax in any manner, shall serve on the assessee a notice requiring him, on a date to be specified therein, either to attendthe office of the Assessing Officer or to produce, or cause to be produced before the Assessing Officer any evidence on which the assessee may rely in support of the return:

Provided that no notice under this sub-section shall be served on the assessee after the expiry of three months from the end of the financial year in which the return is furnished.

(3) On the day specified in the notice issued under sub-section (2), or as soon afterwards as may be, after hearing such evidence as the assessee may produce and such other evidence as the Assessing Officer may require on specified points, and after taking into account all relevant material which he has gathered, the Assessing Officer shall, by an order in writing, make an assessment of the total income or loss of the assessee, and determine the sum payable by him or refund of any amount due to him on the basis of such assessment:

13.6 The aforesaid two sub-sections of section 143 of the Act, make it apparent that the AO, while taking cognizance of the return of the assessee,if finds it necessary to examine the reported income or loss, can call the assessee to produce ‘evidence’. At the cost of repetition, we observe that the word ‘evidence’ is not independently defined in the Act and, certainly, cannot mean anything more than what is defined in section 3 of the Evidence Act, which we have considered above.

13.7 It can be further seen that sub-section (3) to Section 143 of the Act, gives the scope of assessment wherein the AO has been given liberty to examine the evidences produced by the assessee and to even collect evidences by own efforts and, then, after taking into account ‘all relevant material’ which he has received from assessee or gathered in enquiry, make an assessment. Very apparently, like the use of the word ‘matter before it’ in section 3 of the Evidence Act, sub-section (3) of section 143 of the Act also uses the phrase ‘relevant material.’

13.8 Thus, to our mind, when it is said the provisions of Evidence Act are not applicable on the quasi judicial authority, what is meant is that the strict rules of proof of a fact in a particular manner only is not applicable. As for instance a Will, as per section 68 of the Evidence Act being a document required to be attested can be used in evidence only when one of the attesting witnesses at least has been examined for the purpose of proving its execution. However, in quasi judicial proceedings, like assessment, such strict mode of proof of Will is not necessary. That does not dispense with applicability of rules of fairness, prudence and natural justice which are foundation of evidence law.

13.9 As for our discussion with regard to this aspect we may mention here that under the Assessment proceedings the admission may be in the form of statements recorded at time of search and seizure under Section 132(4) of the Act and the statement have evidentiary value and can be used as evidence in any proceeding under the Act. Statement recorded during survey under Section 133A(3)(iii) unlike a statement under Section 132(4) of the Act, is not on oath and therefore has no evidentiary value, though it can still be used in proceedings being. Then during assessment proceedings u/s Section 131 of the Act, statement on oath are recorded by AO.However, statements recorded even on oath though binds the assessee cannot be independently used for making addition unless corroborated by evidences. Reliance can be placed on decision of Hon’ble Delhi High Court in Pr. CIT v. Pavitra Realcon (P.) Ltd. [2024] 340 CTR 225 (Delhi)/ 240 DTR 465 (Delhi)(HC).Thus relevant statements, including admissions or documents which are not inchoate and unimpeachable and whose veracities cannot be doubted at all should only be considered to be ‘relevant material’, permitted to be relied, u/s 143(3) of the Act for concluding the assessment.

14. This view of ours is further supported by the fact that many basic principles and rules of evidences as enshrined under evidence law, are made part of assessment proceedings. To refer to some of such instances we can see that right to cross-examination of witness examined by assessing officer stands duly recognized in case of income-tax proceedings and reliance can be placed on the decisionCIT v. SMC Share Brokers Ltd. (Delhi)/[2007] 288 ITR 345 (Delhi). Hon’ble Supreme Court in the case of C. Vasantlal and Co. v. CIT [1962] 45 ITR 206 (SC) held as under:-

“The Income-tax Office is not bound by any technical rules of the law of evidence. It is open to him to collect materials to facilitate assessment even by private enquiry. But if he desires to use the material so collected, the assessee must be informed of the material and must be given an adequate opportunity of explaining it.”

15. Principles of non-relevance and non-admissibility of hearsay evidence, as part of Section 60 of Evidence Act, is duly recognized in tax proceedings and thus suspicion how so ever strong cannot take place of proof, even in assessment proceedings. Reliance is being placed on the case of Dhakeswari Cotton Mills Ltd. v. CIT [1954] 26 ITR 775 (SC) wherein Hon’ble Supreme Court held that a suspicion remains a suspicion unless the same is established and can never take place of reality. Similarly the Hon’ble Supreme Court in the case of Umacharan Shaw & Bros. v. CIT [1959] 37 ITR 271 (SC) held that suspicion however strong, cannot take the place of evidence.Assessment cannot be made on guesswork without any reference to any material on record. The Hon’ble Supreme Court in the case of Omar Salay Mohamed Sait v. CIT [1959] 37 ITR 151 (SC) had held that no addition can be made on the basis of surmises, suspicion and conjectures. In the case of CIT v. Daulat Ram Rawatmull [1973] 87 ITR 349 (SC) the Hon’ble Supreme Court held that the onus to prove that the apparent is not real is on the party who claims it to be so.

15.1 We also find that as enshrined under Evidence Act, secondary evidences, like photocopies of a documents, are also not held be reliable for completing assessment. Reliance can be placed on decision of Hon’ble Delhi High Court in Pr. CIT v. Smt. Rashmi Rajiv Mehta (Delhi)/[2025] 474 ITR 97 (Delhi) 4 March, 2024 vide, wherein Hon’ble High Court has consider photo copy of an agreement of sale and held as follows;

“No doubt the income tax proceedings are not bound by the technical rule of evidence, but where the addition is solely based on a photocopy of alleged document and the authenticity of such photocopy which is being made basis for making addition is being challenged by the assessee, then ostensibly onus will shift upon the Revenue to first establish the authenticity of such photocopy, thereafter, the onus may shift to the assessee to establish what is stated is correct. Here is the case where Revenue has failed to establish the authenticity of the photocopy of the alleged agreement to sell and thus, we are of the view that the addition on the basis of such photocopy the authenticity of which has not been established, the same cannot be sustained.”

15.2 Then, it is also settled provision of law that illegality of search does not vitiate the evidence collected during alleged illegal search, but, at the same time, courts or the appellate authority have to be circumspect before admitting such evidences. Reliance can be placed on the decision of the Hon’ble Supreme Court in Dr. Partap Singh v. Director of Enforcement (SC)/[1985] 155 ITR 166 (SC). It can also be observed that circumstantial evidences are heavily relied by the tax authorities by drawing inferences from the facts, circumstances and material relied for making the additions. The Hon’ble Supreme Court in CIT v. Durga Prasad More [1971] 82 ITR 540 (SC), has held that courts and Tribunals have to judge the evidence before them applying the test of human probabilities. In Chuharmal v. CIT (SC)/[1988] 172 ITR 250 (SC), has held that “the rigor of rules of evidence contained in Evidence Act was not applicable, but that did not mean that the taxing authorities were not desirous??of invoking the principles of the Act in the proceedings before them, they were prevented from doing so.” In Sumati Dayal v. CIT (SC)/[1995] 214 ITR 801 (SC), the Hon’ble Supreme Court has recognized that taxing authorities were entitled to look into surrounding circumstances to find out the reality of recitals.

16. We can further see that there are various provision under the Income Tax Act 1961 akin to provision under the Evidence Act like section 131 of the Act giving powers regarding discovery, production of evidence, section 132(4A) presumption as to books of account and documents, section 132A of the Act giving power to requisition books of account, section 136 of the Act specifically mentioning that proceedings before income-tax authorities to be judicial proceedings, provision of section 250(4) of the Act and Rule 46A of admitting additional evidences, Section 278E of the Act giving rise to presumption as to culpable mental state, section 292C of the Act giving rise to presumption as to assets, books of account definitely recognize some of the basic principles of Evidence Act by specific adoptions in the Income-tax Act, 1961. The presumption attached to statements recorded u/s 143(4) of the Act.Then, though affidavits are not included in the definition of ‘evidence’ in section 3 of the Evidence Acthowever, the same are frequently called for and relied in the assessment proceedings.

17. Thus we are of considered view that certain Rules of natural justice, prudence and common sense as enshrined in the Evidence Act certainly become applicable in all quasi judicial proceedings also even if there is no strict application of Evidence Act. Based on aforesaid discussion we can certainly hold that the strict principles and Rules of ‘mode of proof’ under the Evidence Act may not be applicable to assessment proceedings but the aforesaid discussion leaves us to a conclusion that even if the Evidence Act is not made strictly applicable to the tax proceedings by the Income Tax Act 1961, the fundamental principles of law of evidence defining what constitutes evidence, the relevancy of evidence for the issues under consideration, the principles of their admissibility in terms of valid mode of proof and probative value of the evidences, cannot be ignored even by quasi judicial authorities. Thus where the initial burden of proof is on the Revenue authorities to show that the receipts constitutes income, and only real income is liable to tax and more particularly in case of search assessments that addition is on the basis of incriminating material found during the search, the burden on the Revenue is of proving that the assessee has attempted to evade tax and this burden is to be discharged by establishing facts and circumstances from ‘relevant material’ driving conclusive inference that in fact assessee evade tax lawfully payable by it. Reliance can be placed on the decision of the Hon’ble Supreme Court in the case of CIT v. Sati Oil Udyog Ltd. (SC)/[2015] 372 ITR 746 (SC). Hon’ble Supreme Court in Durga Prasad More (supra) has observed that “Now coming to the question of onus, the law does not prescribe any quantitative test to find out whether the onus in a particular case has been discharged or not. It all depends on the facts and circumstances of each case. In some cases, the onus may be heavy whereas in others, it may be nominal. There is nothing rigid about it.”

18. Now where the revenue wants to exclusively rely electronically retrieved evidences, certainly the burden on revenue is stricter as to also establish the genuineness of the electronic evidence and that too is of wholesome nature. As quasi-judicial authorities, tax authorities too are also supposed to give reasoned findings based on relevant and admissible electronic evidences coming from credible source with probative worthiness.

19. The incorporation of provision about necessity of having certificate u/s 65B of the Evidence Act is thus one of the elementary jurisprudential aspects which call for admission of only the best evidence and to ensure the electronic or digital evidence hold veracity to draw conclusive conclusions and to fasten a liability. This is fortified by the Hon’ble Supreme Court decision in Addl. Director General Adjudication v. Suresh Kumar and Co. Impex Pvt. Ltd. [Civil Appeal Nos.11339-11342 of 2018, dated 20-8-2025] where recently, the Hon’ble Supreme Court has dealt with the case of relevancy and admissibility of electronic evidences in the proceedings under the Customs Act, 1962 wherein the provisions of section 138C of the Customs Act, 1962 regarding admissibility of electronic evidences has been accepted subject to availability of certificate to be obtained in accordance with the sub-section (4) of section 138C of this Act of 1962. The Hon’ble Supreme Court observed that section 65B(4) of Indian Evidence Act is parimateria to section 138C(4) of the Act of 1962 and, further relied the decision of the Hon’ble Supreme Court in Arjun Panditrao Khotkar v. Kailash Kushanrao Gorantyal (2020) 7 SSC 1,and observed that in the said decision the Hon’ble Supreme Court, while explaining the mandatory nature of section 65B(4) of the Indian Evidence Act applied following two Latin maxims 🙁i) impotentiaexcusatlegem; (ii) lex non cogitadimpossibilia, and thereafter held that these two maxims are the foundation with regard to admissibility of electronic evidences and though section 65B(4) of the Evidence Act is mandatory, yet, it would all depend on the facts of each case, how the same could be said to have been duly complied with.

20. Accordingly, in the said case of Suresh Kumar (supra), the Hon’ble Supreme Court considered the ‘substantial compliance’ of section 138C(4) to be sufficient and, therefore, we can firmly conclude that if, in the case of the Incometax Act, 1961, there are no specific provisions with regard to admissibility of electronic evidences, then, the Manual issued by the Board would substantially hold the ground and the tax authorities are suppose to ensure that there is at least substantial compliance of the Manual to make the electronic evidence relevant and admissible under the law and thus pass judicial scrutiny in appellate jurisdictions

21. Coming to the case in hand, it can be observed that as this question of relevance of electronic evidences was raised by the ld. AR at the time of hearing and the Bench by order dated 03.05.2025 had directed the Revenue to provide records, if any, of as to how the electronic and digital evidences were handled so as to ensure that same remained unimpeached and their veracity, as admissible and reliable peace of material to conclude search remained intact and if any compliance u/s 65B of the Indian Evidence Act were made in accordance with the law. Thereafter, on 19.03.2025, certain material were filed by the ld. DR in the form of certificates taken u/s 65B of the Indian Evidence Act, 1872 and the Bench had observed as follows:-

“Ld. DR has submitted certain certificates given u/s 65B of Indian Evidence Act, 1872 and we have gone through the same. The Certificates as filed before us seem to be incomplete and Ld. DR was unable to assure that apart from the material filed before the Bench there is any other relevant material in regards to these certificates. Thus Ld. DR is directed to ensure that complete record with regard to these certificates to be produced and further to assist the bench to examine this material, a competent expert be called from the department. In any case the arguments will be concluded on the next date of hearing. Adjourned to 3rdApril, 2025. Both parties informed.”

22. Further on 24.07.2025 also court again gave ld. AO to clarify about availability of anyother material with department,specially about the chain of custody documents, and the bench had observed as follow;

“Both the sides were heard. Ld. DR was apprised that at the time of previous hearing, on behalf of the department, certain documents were filed with regard to compliances of admitting electronic evidences. However, one of the vital documents on which Ld. AR has stressed pertains to the chain of custody, a report prepared immediately at the time of search and seizure.

The chain of custody document provided to the Bench merely reflects the seizure and handing over the seized devices to the investigation wing at the time of search and seizure. However, the link evidences showing connectivity of a chain of custody to reach the Assessing officer are not there in the documents provided by the department.

Ld. DR who is present virtually, has requested that the current incumbent DR of this Bench ‘A’ be directed to procure the relevant documents/information. Accordingly, it is directed that department will ensure filing all the material establishing admissibility of the electronic evidences, specially the chain of custody document from the stage of handing over of the electronic devices to the Investigation Wing reaching the hands of the Assessing Officer.

Ld. DR is requested to forward a copy of this order for information to the present incumbent DR of ‘A’ Bench and also to the concerned Assessing Officer.

As, this Bench has considerably heard the matter at length, it is kept for further clarification on this aspect only for 14.08.2025. No further opportunity shall be granted to the department, and it will be presumed that there is no other piece of information/document available with the Assessing Officer than what has already been furnished in previous hearings.”

22.1 In response of same ld. Assessing Officer had also filed a response and for completeness the same is also reproduced below:-

“Office of The Asst. Commissioner of Income Tax Central Circle-13, New Delhi Room No-247,2nd Floor,E-2, Jhandewalan Extension, New Delhi-110055 Email:delhi.dcit.cenl3@incometax.gov.in

F.No. ACIT/CC-13/ITAT/2025-26/270 Date: 21.08.2025

To,

The Income Tax Officer,

O/o CIT(DR)-1, A Bench,

ITAT, New Delhi.

Madam/Sir,

Sub: Appeals in the case of Balar Marketing Pvt. Ltd., (PAN: AAACB0361N),assessee’s appeals ITAs 3143-3148/DEL/2023 & Department appeals in 3422- 3426/Del/2023 for A.Ys. 2016-17 to 2021-22- respectively regarding.

Kindly refer to the above and email dated 08.08.2025 vide which your office sought documents/electronic devices from the stage of handing over by the

Investigation Wing to the concerned Assessing Officer. In this regard, report is being submitted as below:

During an Income Tax search operation, technical forensics personnel is responsible for assisting the Income Tax Department in imaging and cloning digital devices found at the premises, which may contain crucial data related to the concerned party.

The procedure of seizure of electronic devices as well as imaging and cloning of digital devices is carried on in accordance with the Search and seizure manual (last updated in 2025) and Digital Evidence Investigation Manual 2014.

The forensics expert employs specialized tools while creating backups or images of the digital evidence to maintain its integrity, ensuring that no data from the original device is altered or tampered with during the cloning process. This ensures that the original evidence remains untouched throughout the acquisition process. Once the imaging/cloning is complete, the software used generates results that may vary depending on the tool; however, two consistent and critical outputs are provided by all: the forensic image of the original evidence and the hash value—a unique digital fingerprint representing all the information stored on the original device.

Hash values are generated using cryptographic algorithms through a process known as hashing. Hashing is a one-way function that transforms any amount of data into a fixed-length string of characters, known as the digest. This digest is non-reversible—meaning it cannot be decrypted or traced back to the original content—and is therefore used as a digital fingerprint for the data. Even a minor change in the original dataset would result in a completely different hash value, which makes it an effective mechanism for data integrity verification.

Hash value can be generated of any data set and it’s a data unique value. Which mean, if two data sets having exactly the same data will be having the same Hash value. This function of hashing is used for ta integrity check in case of tampering of data after a hash value is produced. Majorly two types of hashing algorithm are used i.e., MD5 and SHAI.

MD5 (Message Digest Algorithm 5): Produces a 128-bit hash value. It is efficient and widely supported across forensic platforms, and primarily used as a checksum to detect unintentional data corruption.

SHA-1 (Secure Hash Algorithm 1): Produces a 160-bit hash value, typically rendered as a 40-character hexadecimal string. It provides a higher level of uniqueness and is often used for evidence validation in legal settings.

The above procedure was duly followed in the case of the assessee, and Hash value was also recorded which remained unchanged throughout the process.

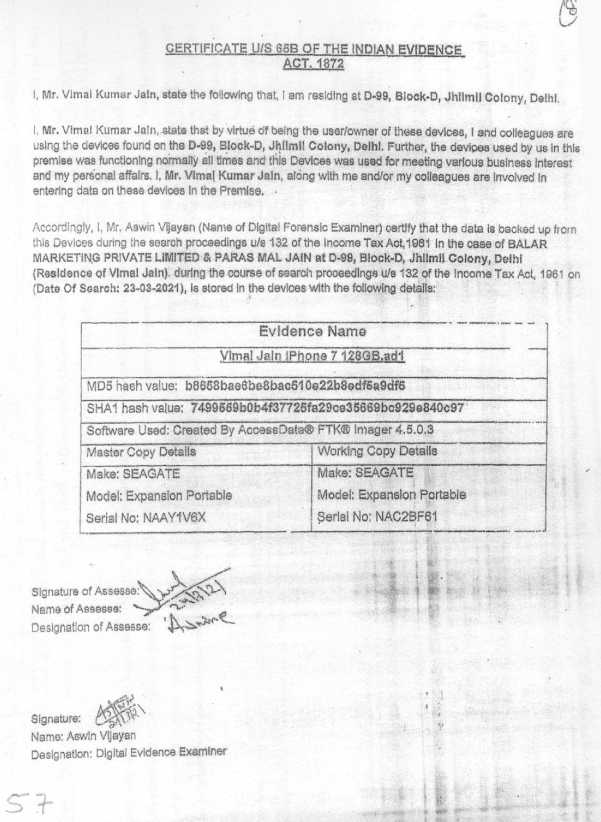

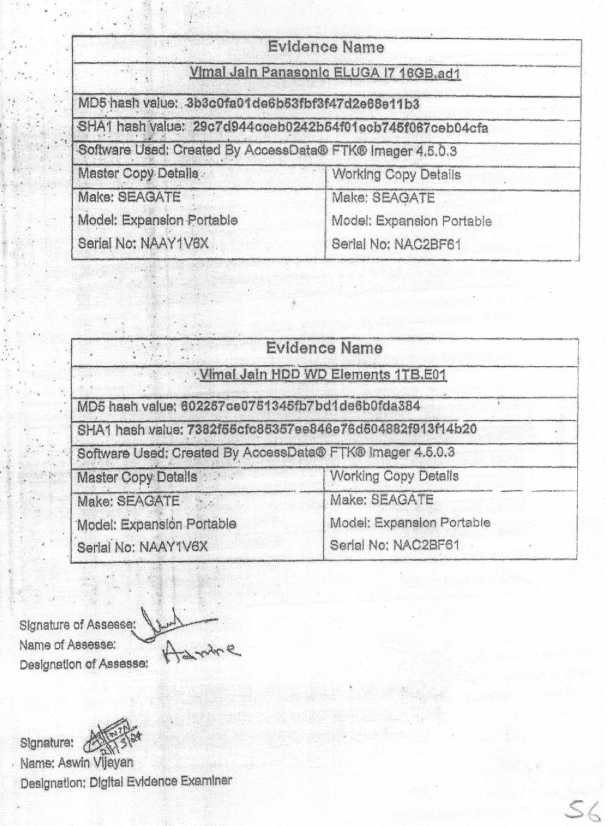

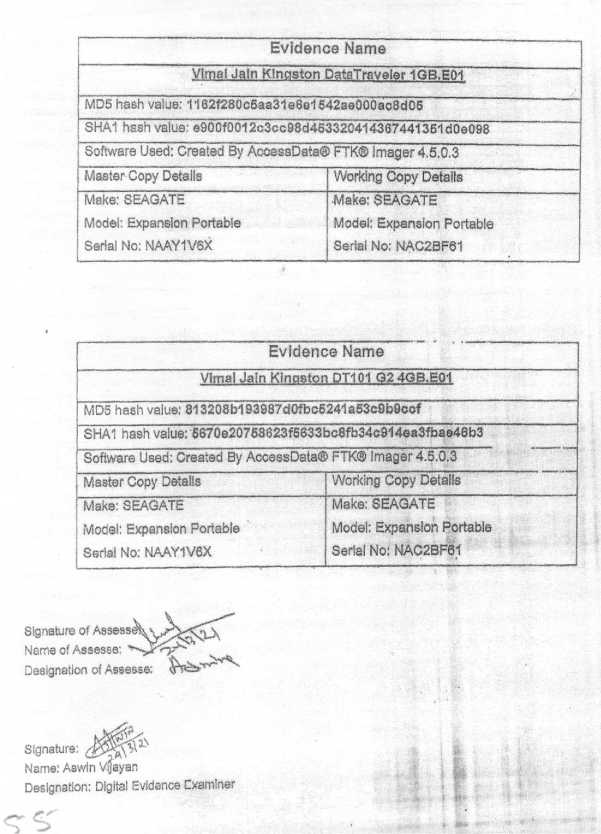

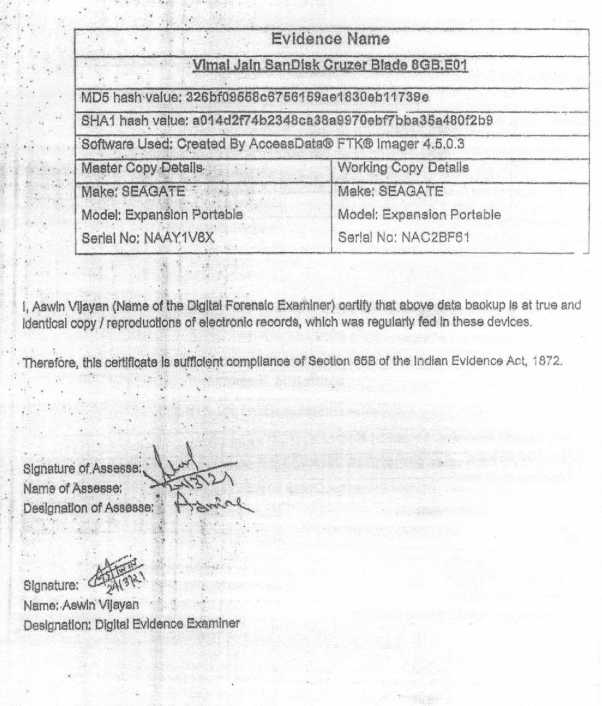

After seizure of electronic devices, Once the imaging and hashing were completed, the examiner generated a certificate under Section 65B of the Indian Evidence Act on 24.03.2021 (A sample copy of the same is attached herewith) which has now been updated to Section 63 of the BharatiyaSakshyaAdhiniyam. Form 65B includes comprehensive details about the cloned electronic evidence, party information, hash value, references to the applicable legal provision, and the signatures of the involved

parties, including the examiner. A sample copy of the Form 65B recorded in case of the assessee is reproduced below-

A chain of custody document was also signed by the Authorized officer present at the department, which indicates that the authenticity of the digital evidence was maintained at the time of seizure. A sample copy of the same in case of assessee is attached below-

The cloned data was stored on two separate storage drives: one designated as the “working copy” and the other as the “master copy.” The master copy is permanently sealed and retained by the Income Tax Department, to be used only if the working copy becomes corrupted or damaged. The master copy was sealed and the Authorized officer present at the premise and the Assessee put their signature on it as well.

Therefore, in case of the assessee as well, the Certificate u/s 65B was recorded on 24.03.2021, at the time of the extraction of data from electronic devices and thereafter cloning of data was undertaken. The Cloned data as stored in the Master copy was then sealed by the Authorised officer present on the premise and his signature were also placed on the same. The hash value was also generated at the time which remains intact and unchanged. Therefore it is clear from above that the cloning of data is undertaken after the extraction of data is done and hash value generated.

The working copy was then forwarded to the Cyber Forensics Lab (CFL), where a cyber forensics expert converted the cloned image into a readable format stored on another drive known as the “extraction copy.” The extracted copy is then used to support the ongoing investigation and, where applicable, are presented as part of the proceedings. The Digital Evidence Investigation Manual 2014 defines ‘Chain of Custody ‘ as –

“Chain of custody” is the roadmap that shows how evidence was collected, analyzed and preserved in order to be presented as evidence. Establishing a clear chain of custody is critical because electronic evidence can be easily altered. A clear chain of custody would demonstrate that electronic evidence is trustworthy. Preserving a chain of custody for electronic evidence, at a minimum, requires that-

| i. |

|

No data has been added, changed, deleted from the seized information evidence |

| ii. |

|

The seized/information evidence was duplicated exactly and completely. |

| iii. |

|

A reliable and validated duplication process was used. |

| iv. |

|

All media were secure and safe. |

Based on above, the chain of custody of the seized electronic evidence was never compromised in the process described above and followed in the case of the assessee. The cloned data is stored in 2 devices, ‘a Working Copy’ and ‘a Master copy’. And the master copy is sealed permanently and is never desealed. The hash value (i.e.—a unique digital fingerprint representing all theinformation stored ontheoriginal device) is generated which remains the same throughout the search proceedings and later on during the assessment proceedings. The unique hash value remains same for a particular electronic evidence/data set. Moreover, since the Master copy remains sealed, the question of compromise of the chain of custody does not arise.

Further, the entire seized material is handed over by the Investigation Wing to the Assessing Officer in Central Circle through a handing over note (A copy of the same in case of the assessee is attached herewith). The handing over note is the document which evidences that the entire seized material including the electronic devices and evidences is handed over to the assessing officer in the central circle. Even during this stage, the Master copy of the electronic evidence is not opened and remains sealed. Therefore, the chain of custody as well as the hash value remains intact and uncompromised.

Further, the data or evidences used from the electronic devices/evidences and which have been relied upon by the Assessing Officer for making the additions can be verified at any time by Appellate authorities through the Master copy maintained with the department.

Yours faithfully.

Sd/-

(Abhilasha Sharma)

Asst. Commissioner of Income Tax,

Central Circle -13,

New Delhi.

Encl.: as above”

23. Thus based on aforesaid response of AO, one this is crystal clear that AO admits about obligation to follow the Manual. What is also relevant is that these are forms as prescribed in the Manual meaning thereby that the search team was aware of the instruction of Board. Then it is also admitted that whatever relevant material was available to show compliance of Manual have been brought on record. Here thus it will be appropriate to give a summary the electronic evidences found in search and other material as filed by the Revenue running from page 1 to 70, by observing as to if same was found relevant and relied in assessment:-

| Sr no |

Particulars |

Page no |

Remark |

| 1. |

Email exchange between CIT[DR] and DCIT, |

|

|

|

Central Circle-13, Delhi |

1-3 |

– |

| 2 |

Mobile device collection form – Panasonic Eluga |

4-5 |

Relevant |

| 3 |

Repeat of serial no 2 |

6-7 |

Not relevant |

| 4 |

Mobile device collection form – Apple iPhone 7 |

8-9 |

Relevant |

| 5 |

Repeat of serial no 2 |

10-11 |

Not relevant |

| 6 |

Repeat of serial no 2 |

12-13 |

Not relevant |

| 7 |

Repeat of serial no 4 |

14 |

Not relevant |

| 8 |

Hash details of iPhone XS Max |

15 |

Not relevant |

| 9 |

Extraction report of Apple iPhone XS Max |

16-17 |

Not relevant |

| 10 |

Extraction report of Apple iPhone – Ms. Pooja Jain |

18-19 |

Not relevant |

| 11 |

Extraction report of Apple iPhone 11 – Bilesh |

20 |

Not relevant |

| 12 |

Verification report (Txt file)ofMs.Pooja Jain Laptop |

21-23 |

Not relevant |

| 13. |

Hash details of iPhone backup |

24 |

Not relevant |

| 14 |

Extraction report of Apple iPad |

25 |

Not relevant |

| 15. |

65B Certificate of MrParasmal Jain |

26-27 |

Not relevant |

| 16 |

65B Certificate of MrVimal Jain |

28-32 |

Relevant |

| 17 |

Repeat of serial no 16 |

33-37 |

Not relevant |

| 18 |

Repeat of serial no 16 |

38-42 |

Not relevant |

| 19 |

Chain of Custody – NAAY1V6X – MrVimal Jain |

43 |

Relevant |

| 20 |

Chain of Custody – NAC2BF61 – MrVimal Jain |

44 |

Relevant |

| 21 |

Digital evidence collection form -SanDisk pen drive |

45-46 |

Not relevant |

| 22 |

Repeat of serial no 21 |

47-48 |

Not relevant |

| 23 |

Repeat of serial no 21 |

49-50 |

Not relevant |

| 24 |

Digital evidence collection form – Kingston pen drive |

51-52 |

Not relevant |

| 25 |

Repeat of serial no 24 |

53-54 |

Not relevant |

| 26 |

Repeat of serial no 24 |

55-56 |

Not relevant |

| 27 |

Digital evidence collection form- Kingston Data Traveler |

57-58 |

Not relevant |

| 28 |

Repeat of serial no 27 |

59-60 |

Not relevant |

| 29 |

Repeat of serial no 27 |

61-62 |

Not relevant |

| 30 |

Digital evidence collection form-WD Elements HDD |

63-64 |

Not relevant |

| 31 |

Repeat of serial no 30 |

65-66 |

Not relevant |

| 32 |

Repeat of serial no 30 |

67-68 |

Not relevant |

| 33 |

Repeat of serial no 4 |

69-70 |

Not relevant |

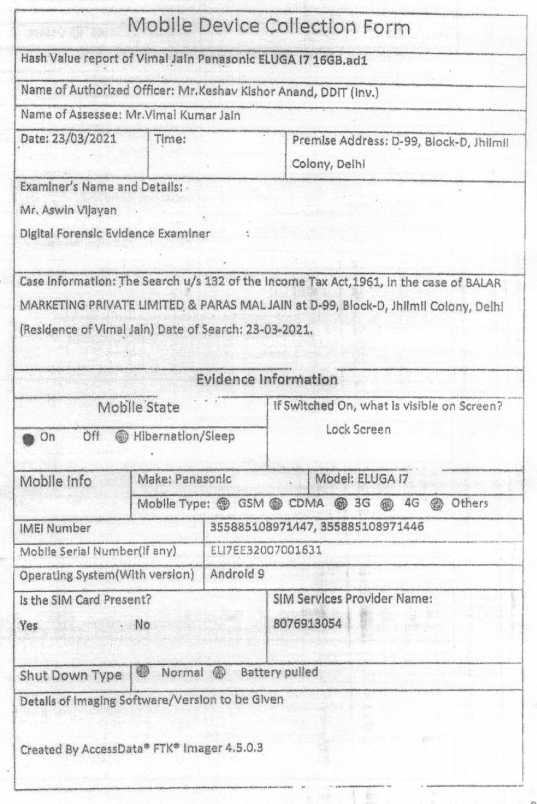

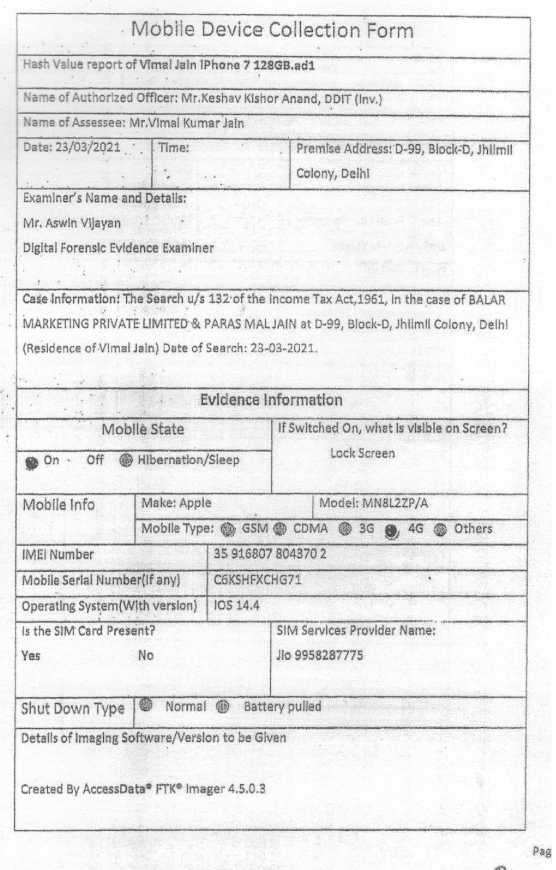

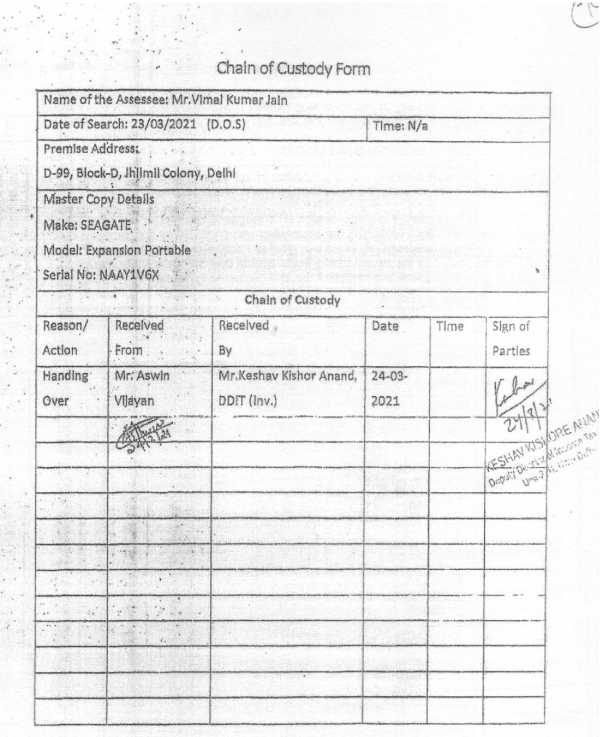

24. As from this material, it will be appropriate here to reproduce the aforesaid found material in the form of mobile device collection form of Panasonic Elugaand Apple iPhone, the two phones allegedly containing the images, the certificates u/s 65B of the Evidence Act given by Mr. Vimal Jain and copy of Chain of Custod form of two phones:-

25. We thus come to a stage where it becomes relevant to again rely the provisions of the Manual issued by the Board to find out how the Board recognizes the due procedure to be adopted to ensure the admissibility of digital evidences and we find that by virtue of para 6.8 of the Manual while giving directions as to how the forensic imaging of cloning of the devices have to be done the Manual directs that hash value should be recorded in the Panchnama and the assessee can be given the option of seeking a copy of imaged/cloned hard disk by paying the copying charges. The Manual very categorically emphasis on the importance of hash value as evidence of genuineness and completeness of the collection and examination of the digital evidences.

26. However, when we examine the Panchnama, the copy of which was file at hearing, there is absolutely no whisper of the hash value of these digital devices and evidences in the Panchnama. There is no mention of IMEI numbers of the devices shown seized in the Panchnama.

27. The Revenue has then relied mobile device collection form of two phones and they make it apparent that the mobile collection forms are dated 23.03.2021 while signatures of the Mr. Vimal Jain, authorized officer, Forensic examiner and two witnesses are dated 24.03.2021. Time column in the form is left blank. Mobile device collection form does mention MD5 hash value and SHA1 hash value of the two devices, which were impounded at the time of seizure of these devices and hash value of one external drive used to copy the content of all the digital devices seized.

28. Further, as we examine the copy of so called65B certificate said to given by Mr. Vimal Jain, the same is shown to be dated 24.03.2021. This certificate at one end merely mentions an undertaking that Mr. Vimal Jain was the owner and user of these device. At the other end, this certificate given u/s 65B of the Evidence Act is shown to be given by Mr. AshwinVijayan, Digital forensic examiner who merely certifies that the data is backed up from the seized phones and stored in the target device with relevant details of phone and target device mentioned in the certificate. This certificate is therefore just about process of collection of digital evidences and cloning being followed at time of search. It nowhere mentions of extraction of data which was used later for appraisal report or in assessment. There is no mention in these certificates not there are other certificate to show as to when and how the working copy was examined at time of preparation of appraisal report or assessment. Apart from these documents prepared on 24.03.2021, there is no document showing as to how and in what circumstances and by whom the working copy was accessed, data retrieved, extracted and reproduced for the purpose of preparing the appraisal report by the Investigation Wing and if at all the working copy was made over to the AO, to make necessary extractions and then use them for recording statement and to reproduce in the assessment order.Thus it becomes questionable as to this e-Certificate at all serves any purpose and adds to the veracity of digital evidences.

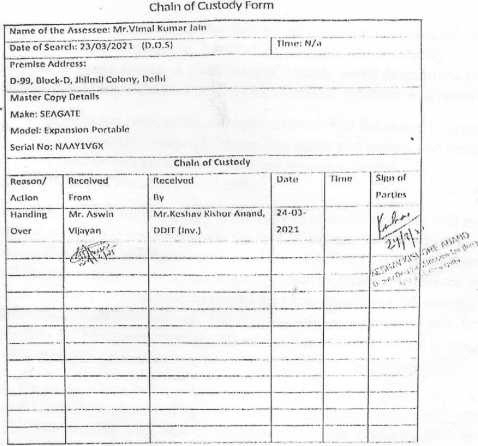

29. Thencoin got chain of custody document, same mentions only one entry of 24.03.2021 which mentions that working copy device is of Segate make and same was handed over by Mr. AshwinVijayan to Mr. Keshaw Kishore Anand, DDIT (Inv.).

30. Now, what is material is that the Manual very categorically lays down the importance of chain of custody and the Manual lays down procedure to be followed by authorities for reporting and analysis of digital evidences and as to how the AO has to deal with the digital evidences and its analyse in the assessment order and what is the importance of chain of custody of digital evidences. The relevant para 9.1 and 9.6 of the Manual which:-

“9.1 Reporting of Analysis of Digital Evidence in the Assessment Order should be done in a simple lucid manner, so that any person can understand. The report should give description of the items, process adapted for analysis, chain of custody on the movement of digital evidence, hard and soft copies of the findings, glossary of terms etc .The presentation and use of digital evidence in assessment order and presentation of the same in court of the law in matters of appeal involves stating the credibility of the processes employed during analysis for testing the authenticity of the data.

Some guidelines that assessing officer need to follow when using the Digital Evidence Analysis in the assessment order etc, are as follows:

| • |

|

Brief description of the case, details description of the objects, date and time of collection of the objects, Status of the objects when collected (On or Off), Seized from – person, organization, location etc should be included in the Assessment Order. |

| • |

|

Digital Evidence Collection Form, Mobile Phone Evidence Collection Form should be enclosed in the order to show the initial state of the Digital Evidence. |

| • |

|

Digital Forensic Report(Given by Forensic Examiner) containing details of hash value and the details of all mahazar drawn to open the digital evidence at various times to gather further evidences should be included as an annexure to the assessment order. If the chain of custody form is present, the same can be annexed to the assessment order. This will establish the integrity of the data before any court of law. |

| • |

|

The Key digital evidences retrieved if deleted along with the description of the same, in case of business application software, a note on how the business application software is and the technical details of all critical components. |

| • |

|

Whether these digital evidences have been confronted to the assessee under any section of the law? The relevant portions of the statement under various sections of Income Tax Act should be included in the order. |

| • |

|

Circumstantial evidences and other key physical evidences seized/impounded should be linked to the digital evidence. Usually the physical evidences like loose papers, sheets gives details of one particular transaction, while the .digital evidences may help in unearthing the entire consolidated data for the whole year. Such digital evidences should be linked to the physical evidences seized during the course of search to establish the genuineness of the data and also to quantify to the total unaccounted income. |

“9.6 Handling the digital evidence at a later stage

In the Income Tax Department, the digital evidence stored is used in the assessment proceedings and at later stages in case of legal tangles. In order to maintain the sanctity of data stored/seized, there is a need to maintain a chain of custody while handling the digital evidence during the course of assessment proceedings and at later stages. Due to the lengthy legal proceedings involved, it may be needed to retain evidence indefinitely.

Hence, a chain of custody of digital evidence should be created in order to know the details of who is accessing data, if anyone who accessed the data had tampered with the data etc.”

31. In regard to the chain of custody form as a part of chapter 11, in para 11.6, the Manual mentions the steps to be undertaken at the forensic lab, and it is mentioned at page No.75 of the Manual as follows:

“4. The data extracted in kept with the DDIT concerned and then transferred to the assessment units when the case is centralized. In case of this transfer, chain of custody form should be filled up and kept in safe custody for further reference.”

32. As with regard to circumstance, in the case before us, which indicate the importance of chain of custody document, we find on more careful examination of the aforesaid material provided at the time of hearing and the assessment order including the annexures in the form of statement recorded, that as mentioned above, admittedly, the date of search is 23rd March, 2021 but in the mobile device collection form has left the time of preparation of this form as blank. This mobile device collection form mentions details of imaging software/version used and also the hash value calculated. It is shown to be signed by the assessee mentioning the name Vimal, while assessee is Balar Marketing and authorized official Keshaw Kishore Anand, Dy. Director of Income-tax (Inv.), Unit-2(4), Delhi along with signature of the engineer/examiner. Two witnesses are also there, however, their signatures are dated 24th March, 2021. The list of inventory is shown to be dated 24.03.2021. The so-called certificate u/s 65B are also dated 24.03.2021. In continuity to the above, as the Panchnama document are examined they are shown to be witnessed on 25.03.2021.

33. At the same time, the statement of Shri Vimal Kumar Jain was recorded u/s 132(4) of the Act and the same is shown to be recorded on 23.03.2021 at 4 PM during the search. This statement is shown to be recorded by Shri Keshaw Kishore Anand. The statement shows that after putting 14 questions on 23.03.2021 at 8.30 PM, recording of statement was closed. This statement shows that Mr. Vimal Kumar Jain was not confronted with any of the digital devices seized or any evidence extracted at time of search. It can be observed that thereafter on 24.03.2021 the statement was continued further starting at 4.30 PM and was recorded by Shri Keshaw Kishore Anand. Therein the digital devices iPhone and Panasonic were confronted and he admitted about their ownership. It can be seen that certain questions were also put up about the whatsapp messages extracted running from pages 1 to 77 in the form of print outs and SMS messages running from page 1 to 165. As observed above the so-called certificate u/s 65B are also dated 24.03.2021, but only mention of the fact that using appropriate software working copy was prepared and nothing as such about the extracted evidences and as with regard to images of sambhav software nothing was extracted up to 24.03.21, so this e-Evidence certificate has no certification about the same. While the certificate should have been taken that the extracts taken out have been taken out in compliance of the Manual.

34. Then after four months, statement of Mr. Vimal Jain was recorded on 14.07.2021 at 11 AM by Shri Honey Patodi, Assistant Director of Income-tax (Inv.), Unit-1(2), New Delhi and after going through the same we find that it was in this statement recorded on 14.07.2021 which continued to be recorded on 22.07.2021, 26.07.2021, 09.08.2021, 10.08.2021, 12.08.2021, 25.08.2021 and the extracts taken out of working copy were individually confronted to seek an explanation as to what sort of transactions, the images and the messages connected or correlated. During the assessment proceedings, the AO has relied these statements to draw inferences. It is by way of the disclosures in the statement only the AO was claims to have drawn inference about the electronic evidences in the form of messages or images allegedly found in the two phones.

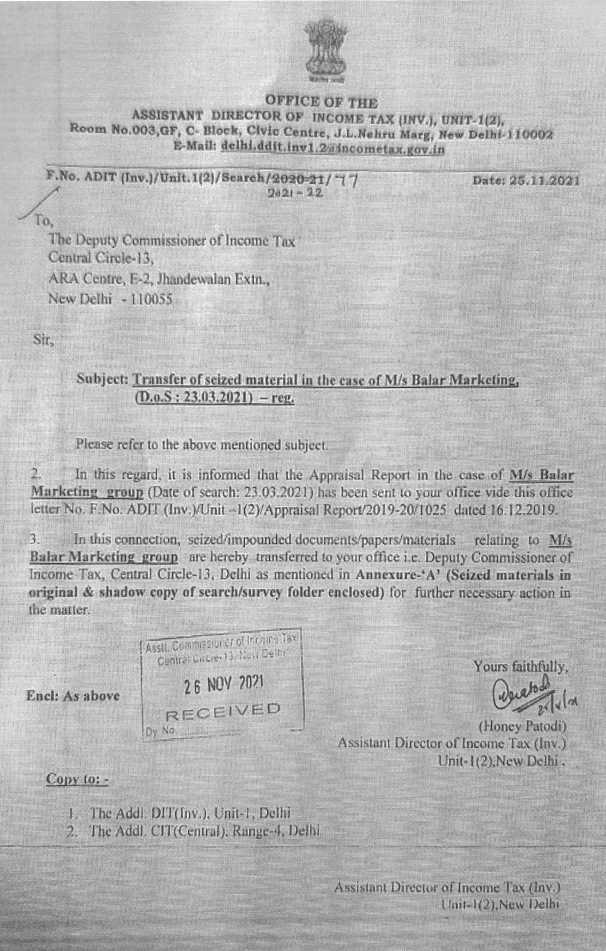

35. Thus, the discussion establishes that it is only subsequently after the search were concluded the devices or their working copy were analyzed and using necessary software extraction of electronic evidences was done which were then confronted by Mr. Honey PatodiShri, Assistant Director of Income-tax (Inv.), Unit-1(2), New Delhi. However, how the digital evidences reached him were to be established by the chain of custody form, but there is no record of same. Infact, the Bench had gone into the issue more inquisitively calling for chain of custody form and a letter dated 25.11.2021 written by Honey Patodi was placed on record and for convenience, we reproduce the same below:-

36 The aforesaid letter dated 25.11.2021 makes it crystal clear that the appraisal report prepared by the Investigation Wing was sent separately and the seized/impounded documents/papers/material which certainly included electronic devices relating to the assessee group were transferred subsequently and there is no mention of any chain of custody form or e-certificate u/s 65B being taken during the preparation of the appraisal report.

37 Then report which assessing officer has filed and we have reproduced in para 18.1 above admits that the procedure of seizure of electronic devices as well as imaging and cloning of digital devices is carried on in accordance with the Search and seizure manual (last updated in 2025) and Digital Evidence Investigation Manual 2014 and that chain of custody was not maintained subsequent to time of search. It is certainly thus not the case of department that assessing officer had any opportunity of examining the credibility of electronic evidences and then to record of same in the assessment order. Therefore, the chain of custody form as left incomplete demolishes the case of the Department that there is no reason to doubt the electronic evidences relied by the AO.

38 More importantly, as we examined the assessment order, we find that none of the directions of the Manual have been followed by the AO except for making the extracts of digital images of SambhavSoftwareor statements annexed to the assessment order. The aforesaid directions of Board in para 9.1 and 9.6 of the Manualhave been completely ignored by the AO. It appears that at time of initiation of search the process of collection of digital evidences was very much in accordance with the directions of Manual. The preparation of chain of custody document and taking E Certificate at time of making working copy, does show that authorities were conversant with the Manual or other instructions. They were aware that only evidence found in search is in the digital form so they with all caution initiated the process of collection of digital evidences form two phones in accordance with mandate of Manual and general principles of law, regulating collection of electronic evidence and to maintain its sanctity throughout, till it is ultimately relied in assessment and if needed at stage of judicial scrutiny. However, the attempt was either half hearted, if not to be presumed to be thwarted half way to prejudice of assessee. It is established that that tax authorities applied some provisions and instructions of the Manual, at time of search but, failed to maintain the records as per the instructions in Manual for Panchnama, mobile device collection form, certificate u/s 65B of the Evidence Act and most importantly the chain of custody form.

39. More particularly, and at the cost of repetition, with regard to the certificate u/s 65B, it can be observed that the same is merely a certificate of the expert about due process adopted while data was backed up from the impugned devices to the devices in which the data was cloned. However, subsequently, as to how the data was retrieved and relevant incriminating evidences were extracted from the devices by whom, have not been certified. In fact that required maintaining correct record of chain of custody, so as to show that when the data was retrieved or any extract taken during assessment proceedings the same were corroborated by hashvalues as recorded at time of making the working copy. The purpose of section 65B of Evidence Act is to provide a certificate to the computer output stating identity of the electronic record describing the manner in which the output electronic record was produced. The certificate should indicate particulars of the electronic device involved, like in the case in hand the two phones or the working copy involved for producing the output of images relied by assessing officer. The authenticity is added by the extraction reports which forms basis of issuing the certificate. There is no extraction report of these two mobiles or of working copies though of some other devices found insearch are placed in material before us. Then the certificate u/s 65B should have shown that the output to be relied as an evidence was produced from the working copy and that the same was in lawful control of the person signing the certificate and certainly the chain of custody document would have established same. However, the chain of custody document filed is completely silent about the same.

40. Then it is also pertinent to mention that the incriminating evidences relied by the AO is not the primary evidence existing in the laptop or computer wherein the alleged Sambhav software was installed, but, are merely images of Sambhav software which allegedly Mr. Vimal Jain was sharing with counterparts for acknowledging the transactions. Similarly, on going through the Whatsapp chats as part of the annexure to the assessment order, the same do not contain any message which will narrate any transaction on its own, but, only mention some figures which are allegedly to be codes. When original Sambhav software could not be retrieved from any of the electronic devices the images in the phones of Mr. Vimal Jain were, no doubt, secondary evidences only and that all the more required thatif they were to be relied the instructions given by the Board to ensure the authenticity of evidence become material directionsto be followed. The evidences extracted from the phone howsoever relevant would become admissible only once necessary compliances required as per due course of law are made. The due course here certainly is the instructions in Manual. Even if it is claimed by ld. DR to be not binding the aforesaid discussion has firmly established that the assessment though being a quasi judicial exercise had to be on the basis of evidences whose veracity can be tested in subsequent proceedings, like appeal or judicial review.This gives us an opportunity to hold that even if the case of revenue is accepted that strict principles or rules of Evidence Act are not applicable or there is no necessity of certificate u/s 65B, still in order to give and add credibility to the conclusions drawn on the digital evidences the AO should ensure that there is substantive compliances of the Manual and not just by way of eye wash.

41. Thus we have no hesitation to hold that assessment has been framed on the basis of material, allegedly retrieved from digital devices, but which are not admissible under law so as to be relied for drawing conclusions, of fact in dispute, being proved on scales of probability even. The corresponding grounds by which assesse challenges the assessment order being framed on inadmissible electronic evidences thus deserves to be sustained.

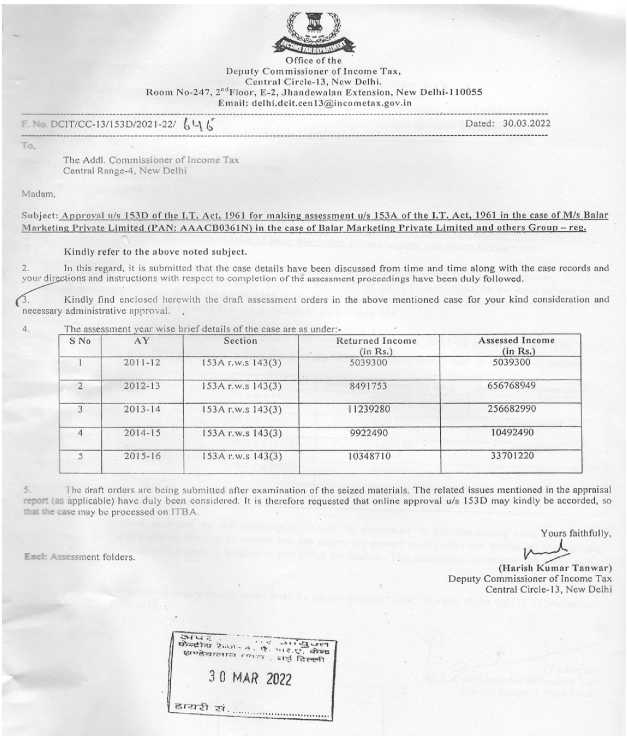

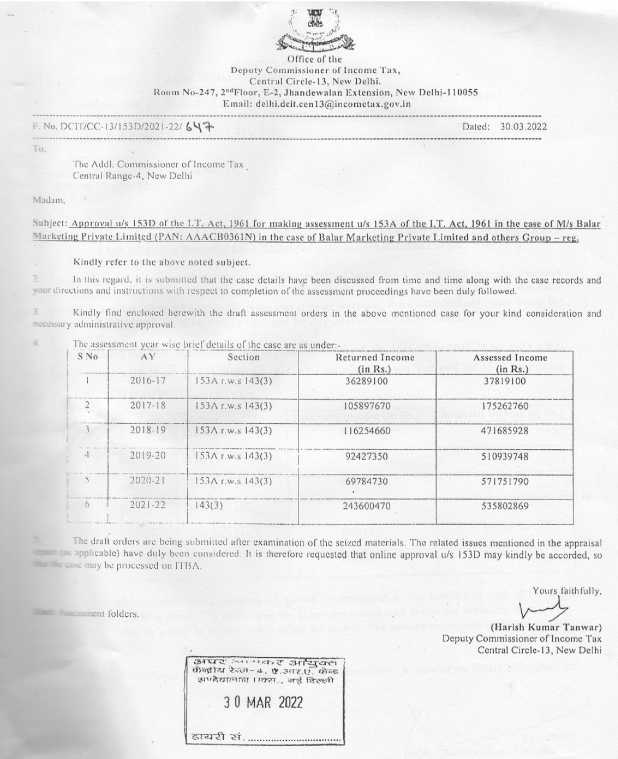

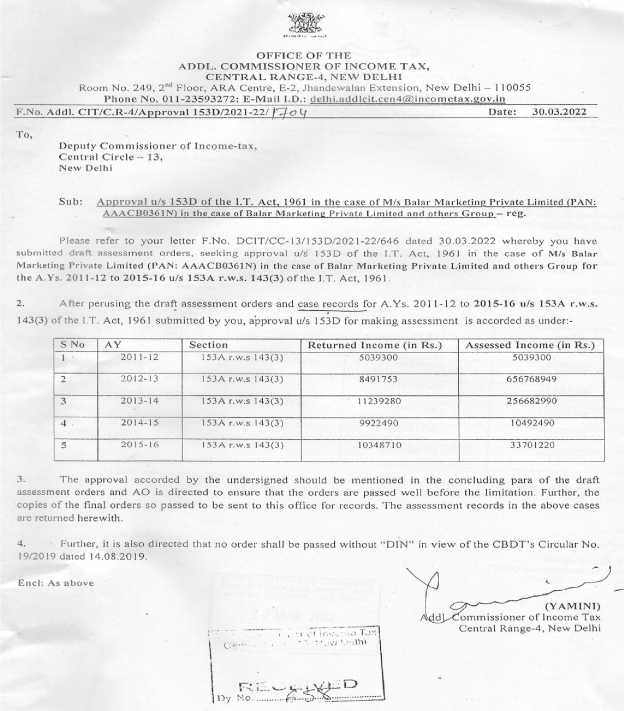

42. Connected to the aforesaid is the second issue of validity of approval granted u/s 153D of the Act and as we examine the assessment orders, we find that the same are very long assessment orders with numerous annexures and even lengthy statements of Mr. Vimal Jain and Mr. Parasmal Jain. However, what comes up is that on 30.03.2022, DCIT, Central Circle-13, New Delhi, vide letter F.No.DCIT/CC-13/153D/2021-22/646 sought approval u/s 153D of the Act. As for the sake of convenience the same are reproduced:-

43. The aforesaid letters from the AO indicate that he was merely seeking an administrative approval (para 3 of the aforesaid letter). The letter merely mentions of the seized materials and in no way mentions of the fact that the case is extensively based on electronic evidences for which necessary compliances with regard to their collection, analysis and admissibility as laid in the Manual prescribed by the Board have been made.

44. Then, on the same date, 30.03.2022, for assessment year 2011-12 to 2015-16 and AYs 2016-17 to 2021-22, by two separate letters approvals have been granted by the competent authority and for the sake of convenience the approvals so given are reproduced below:-

45. The ld. DR has relied the submission that during the assessment proceedings assessing officer from time to time discussed the issues with the senior authorities and, accordingly, the approval is sought. Relying on the judgement of the Hon’ble Supreme Court in S. Narayanappa v. CIT [1967] 63 ITR 219 (SC), it was submitted that such approval is only administrative, and is not a quasi judicial act. Reliance is also placed on the Hon’ble Karnataka High Court decision in the case Rishabchand Bhansali v. Dy. CIT (Karnataka)/[2004] 267 ITR 577 (Karnataka) to submit that approval is merely an administrative act. Then, Mumbai Tribunal decision in the case of Usha Satish Salvi v. ACIT [IT Appeal Nos.4239, 4237 & 4238/Mum/2023, dated 23.01.2025] has been relied to submit that there has to be presumption that approval has been granted with application of mind. It was also submitted that the approval letter amply makes it evident that the approving authority has applied mind in a judicious manner. The ld. DR has submitted that CBDT guidelines dated 22.12.2006 required a close coordination of all the authorities and the approving authority can be very well be presumed to have been aware of all the issues. The judgement in the case of Anuj Bansal (supra) has been distinguished by asserting that in that case, no assessment record was sent along with the draft assessment order and there were infirmities in the figure of original return of income and assessed income which was not taken note of by the Addl. CIT. Similarly, distinguishing the decision in the case of Shiv Kumar Nayyar (supra), there was no fact brought on record by the Revenue to prove that identical issues involving similar facts in different cases submitted for approval by the AO and in those circumstances granting of approval for 43 cases in a single day was not considered to be in accordance with the law. The ld. DR has also relied the decision of the Madras High Court in Home Finders Housing Ltd. v. ITO (Madras)/[2018] 404 ITR 611 (Madras) to submit that in any case if a particular procedure is not followed that does not vitiate the whole assessment order.