Penalty Quashed: AO’s Failure to Specify “Concealment” or “Inaccurate Particulars” Vitiates Penalty Proceedings.

The Legal Background

Section 271(1)(c) allows the AO to levy a penalty if a taxpayer has:

-

Concealed particulars of income; OR

-

Furnished inaccurate particulars of such income.

The Procedural Error

-

The Notice: The AO issued a notice under Section 274 (read with Section 271(1)(c)) but failed to strike off the irrelevant portion. The notice essentially said the taxpayer was guilty of both concealment and furnishing inaccurate particulars.

-

The “Ambiguous Satisfaction”: At the time of initiating the penalty, the AO did not record a clear “satisfaction” as to which specific “limb” of the section the taxpayer had violated.

The Judicial Verdict

The Tribunal (and subsequently higher courts) deleted the penalty, ruling in favour of the Assessee based on the following principles:

1. Requirement of Specificity

The Court held that the taxpayer must know exactly what charge they are defending. If the AO is “unsure” under which limb the penalty is being initiated, the notice is considered vague and stereotyped.

2. Principles of Natural Justice

A penalty is a quasi-criminal proceeding. Under Section 274, a “reasonable opportunity of being heard” is mandatory. If the notice doesn’t specify the charge, the taxpayer cannot provide a meaningful explanation, thereby violating the principles of natural justice.

3. Jurisdictional Defect

Following the landmark decisions in Manjunatha Cotton and Ginning Factory and SSA’s Emerald Meadows, the courts have consistently held that the failure to strike off the irrelevant portion in the penalty notice is not a “curable defect.” It is a fundamental jurisdictional error that makes the entire penalty order void.

Key Takeaways for Taxpayers

-

Check the Penalty Notice: The moment you receive a notice under Section 274, look for the phrases “concealed the particulars of your income” and “furnished inaccurate particulars of such income.” If neither is struck out, the notice is likely defective.

-

The “Mental State” of the AO: The AO must demonstrate a clear application of mind in the Assessment Order. If the order says “penalty initiated for concealment” but the final penalty order says “penalty levied for inaccurate particulars,” the inconsistency is fatal to the Revenue’s case.

-

Transition to New Law: Note that for defaults occurring from AY 2017-18 onwards, Section 271(1)(c) has been replaced by Section 270A (Penalty for under-reporting and misreporting of income). However, the principle of “clear recording of satisfaction” remains equally relevant under the new regime.

-

Writ and Appeal Strategy: This is a “technical ground” that can win a case even if the underlying addition to income was justified. Always challenge the penalty on both technical (notice defect) and factual (merits of the case) grounds.

and Prabhash Shankar, Accountant Member

[Assessment year 2013-14]

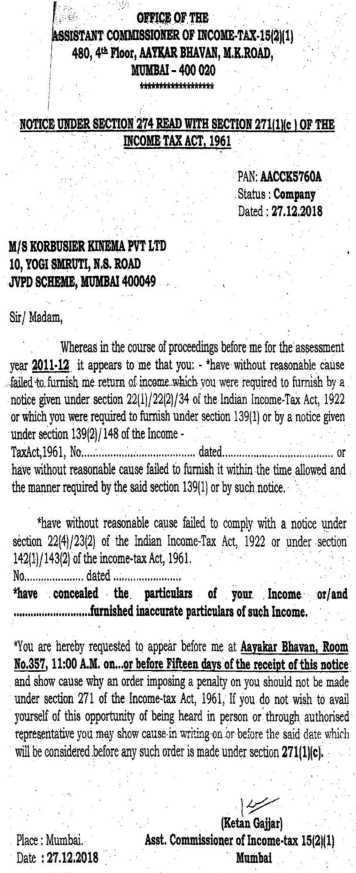

| • | Has concealed the particulars of income “OR”……………. Furnishing inaccurate particulars of such income. |

“7. We have heard the parties and perused the material available on record. As observed above, the Assessing Officer, vide assessment order dated 30.03.2014, made an addition of Rs.8,23,49,198/-, which was sustained by the then CIT(Appeals), vide order dated 09.04.2014 to the extent of 25%, i.e., Rs.2,05,87,299/-. The Hon’ble Tribunal, by order dated 03.04.2018 in ITA Nos. 4086 to 4088/M/2016, subsequently restricted the said addition to 12.5% of the total disallowance made by the Assessing Officer.

5. Thereafter, the AO issued a show cause notice dated 27.12.2008 for concealment of the particular of income or/and furnishing of inaccurate particulars of such income and ultimately vide penalty order dated 18.01.2022 u/s 271(1)(c) of the Act imposed the penalty to the tune of Rs.9.97.234/being 200% of the tax sought to be evaded on the income of Rs.14.95.851/-.

M/s. Korbusier Kinema Private Limited

6. The Assessee, being aggrieved, challenged the said levy of penalty before the Ld. Commissioner, however, of no avail, as the Ld. Commissioner vide impugned order dated 17.12.2024 affirmed the levy of penalty.

7. The Assessee, being aggrieved, challenged the decision of the Ld. Commissioner on various aspects including notice issued u/s 274 of the Act dated 27.12.2018 and by relying on the judgment passed by the Hon’ble Jurisdictional High Court in the case of Md. Farhan A Shaikh v. DCIT (2021) 434 ITR 1 (Bom.) (HC) (FB).

8. On the contrary, the Ld. D.R. refuted the claim of the Assessee by placing reliance on the judgment in the case of Veena Estate (P.) Ltd. v. CIT (2024) 461 ITR 483 (Bom.) passed by the Hon’ble Jurisdictional High Court, concerning the identical issue, wherein it was held that if an Assessee does not challenge the validity of notice during the penalty or appellate proceedings but instead responds substantially to the allegations, such objections are barred at a later stage.

9. We have heard the parties and perused the material available on record. As the issue/ground raised by the Assessee qua notice u/s 274 of the Act, goes to the root of the case, hence for the sake of brevity, we are inclined to decide this ground first. Admittedly, the AO issued the penalty notice dated 27.12.2018 u/s 274 of the Act which is reproduced herein below:

10. From the notice, it clearly appears that the AO has used or/and in between both of the limbs, which goes to show that the AO was not sure under which limb the penalty proceedings have been initiated and to be carried out. Therefore, issue emerges “as to whether the defective notice and/or not mentioning the charge/limb specifically in the notice u/s 274 r.w.s. 271(1)(c) of the Act can justify the levy of penalty”. The Hon’ble Jurisdictional High Court in the case of Md. Farhan A Shaikh (supra) has dealt with the identical issue and considered various judgments in this respect and ultimately held “mere defect in the notice non striking of the irrelevant matter – vitiate the proceedings” and therefore respectfully following the dictum laid down by the Hon’ble Jurisdictional High Court, in our considered view, the penalty under consideration is liable to be deleted.

11. Coming to the judgment relied on by the Ld. D.R. in the case of Veena Estate (P.) Ltd. (supra), we observe that in that particular case the notice u/s 274 of the Act was challenged after 23 years for the first time before the Hon’ble High Court by raising additional ground, which was not admitted and rejected by the Hon’ble High Court by interim order. Here it is not the case so, as in the instant case the Assessee has challenged the notice u/s 274 r.w.s. 271 of the Act before the second appellate authority and within a reasonable time and therefore the judgment referred to by the Ld. D.R. is factually dissimilar.

12. Even otherwise, the Hon’ble Jurisdictional High Court in the Full Bench case in the case of Md. Farhan A Shaikh (supra) has elaborately dealt with the issue and the relevant judgments and therefore respectfully following the said judgment, we are inclined to delete the penalty imposed by the AO and affirmed by the Ld. Commissioner. Thus, the penalty is deleted.

16. It is well settled that the condition precedent for levy of penalty under Section 271(1)(c) is only when the Assessing Officer, in the course of proceedings, is satisfied that an assessee has concealed the particulars of his income or has furnished inaccurate particulars of income. Thus, in applying the penalty provisions under Section 271(1)(c), it was necessary for the Assessing Officer to reached to a conclusion, that the assessee had consciously concealed the particulars of his income and/or had deliberately furnished inaccurate particulars of income to gain an undue advantage of not offering the real income to tax. A clear subjective satisfaction of these essentials is a sine qua non for the Assessing Officer to levy a penalty. Penalty proceedings are penal in nature, as the intention of such provisions is to create an effective deterrent, which will restrain the assessee from adopting any practices detrimental to the fair and realistic assessment as the law would mandate.

7.2. The Hon’ble Karnataka High Court in the case of Manjunatha Cotton & Ginning Factory, 359 ITR 565 (Kar) observed that the levy of penalty has to be clear as to the limb under which it is being levied. As per Hon’ble High Court, where the Assessing Officer proposed to invoke first limb being concealment, then the notice has to be appropriately marked. The Hon’ble High Court also held that the standard proforma of notice under section 274 of the Act without striking of the irrelevant clause would lead to an inference of non-application of mind by the Assessing Officer and levy of penalty would suffers from non-application of mind.

“21. The Respondent had challenged the upholding of the penalty imposed under Section 271(1)(c) of the Act, which was accepted by the ITAT. It followed the decision of the Karnataka High Court in CIT v. Manjunatha Cotton & Ginning Factory 359 ITR 565 (Kar) and observed that the notice issued by the AO would be bad in law if it did not specify which limb of Section 271(1)(c) the penalty proceedings had been initiated under i.e. whether for concealment of particulars of income or for hesitation to delete the penalty levied by the AO and affirmed by the Ld. Commissioner.