ORDER

Astha Chandra, Judicial Member. – The above two appeals filed by the assessee are directed against the separate orders both dated 13.08.2025 of the Ld. Commissioner of Income Tax (Appeals)/NFAC, Delhi [“CIT(A)/NFAC”] pertaining to Assessment Years (“AYs”) 2017-18 and 2018-19. Since identical issues are involved in both the appeals, for the sake of convenience, these appeals were heard together and are being disposed of by this common order.

ITA No. 2147/pUN/2025, AY 2017-18

2. Briefly stated, the facts of the case are that the assessee is a charitable trust registered under the Bombay Public Trust Act, 1950. It is engaged in activities of providing hostel and medical facilities to needy students and awarding them scholarships. The assessee has been granted registration u/s 12A(a) of the Income Tax Act, 1961 (the “Act”) vide certificate dated 24.10.1974. It is also registered u/s 80G(5)(vi) of the Act effective from 28.11.2009. For AY 2017-18, the assessee filed its return of income on 25.07.2017 declaring total income at Rs. Nil. In its return of income, the assessee declared gross receipts of Rs.1,89,43,855/- and claimed expenditure of Rs.47,55,973/-. The assessee trust claimed exemption u/s 11(2) of the Act of Rs.1,11,00,000/-. The case of the assessee was selected for scrutiny under CASS for the reason “Form 10 filed after due date and Large amount accumulated or set apart u/s 11(2)”. Accordingly, statutory notice(s) u/s 143(2) and 142(1) of the Act along with questionnaire were duly issued and served upon the assessee. In response thereto, the assessee made requisite submissions online on e-assessment portal. The Ld. Assessing Officer (“AO”) disallowed the claim of the assessee u/s 11(2) of the Act of Rs.1,11,00,000/- on the ground that the assessee has failed to comply with any of the conditions laid down in clauses (a), (b) and (c) of section 11(2) of the Act and has also failed in filing Form 10 electronically as required under Rule 17(2) of the Income Tax Rules, 1962. The Ld. AO, therefore, completed the assessment rejecting the assessee’s claim of accumulation of Rs.1,11,00,000/- u/s 11(2) of the Act and added the same to the total income of the assessee vide his order passed u/s 143(3) of the Act dated 14.11.2019.

3. Aggrieved, the assessee preferred an appeal before the Ld. CIT(A)/NFAC who dismissed the appeal of the assessee on the ground of non-compliance with the provisions of section 11(2)(a) of the Act and nonfiling of Form 10B within the stipulated time by the assessee. The relevant observations and findings of the Ld. CIT(A)/NFAC are as under :

“6.2.2 As per above mentioned clause (a) of sec 11(2), the assessee shall furnish a statement in the prescribed form in the prescribed manner to AO stating the purpose for which the income is being accumulated or set apart and the period for which the income is to be accumulated or set apart, which shall in no case exceed five years.

6.2.3 Thus, the accumulation of income is allowed only for the purpose stated, it means that there must be a specific purpose whereas in the case on hand, as noted by the AO in the assessment stating that accumulation of fund as one of its object is not a specific purpose as stated in provisions of sec 11(2)(a). therefore the claim of exemption u/s 11(2) (a) with such purpose is not eligible for exemption u/s 11(2).

6.2.4 Since, the appellant has failed to comply with provisions of sec 11(2)(a), the claim of the grounds of appeal 1 to 3 made is not allowable.

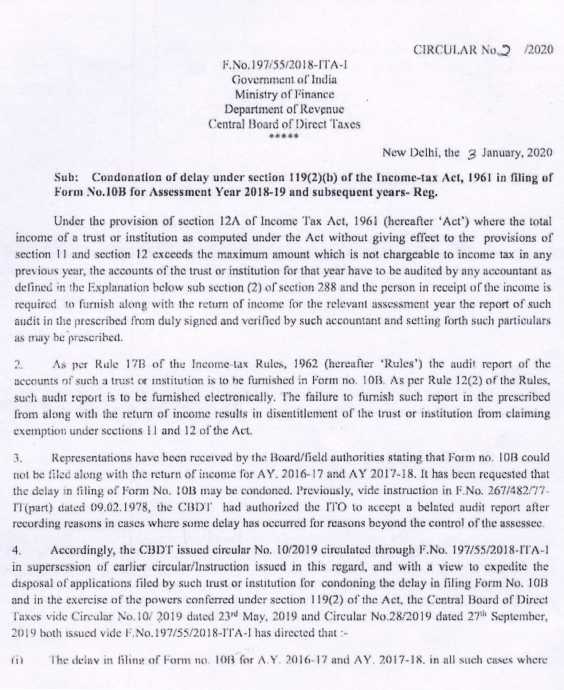

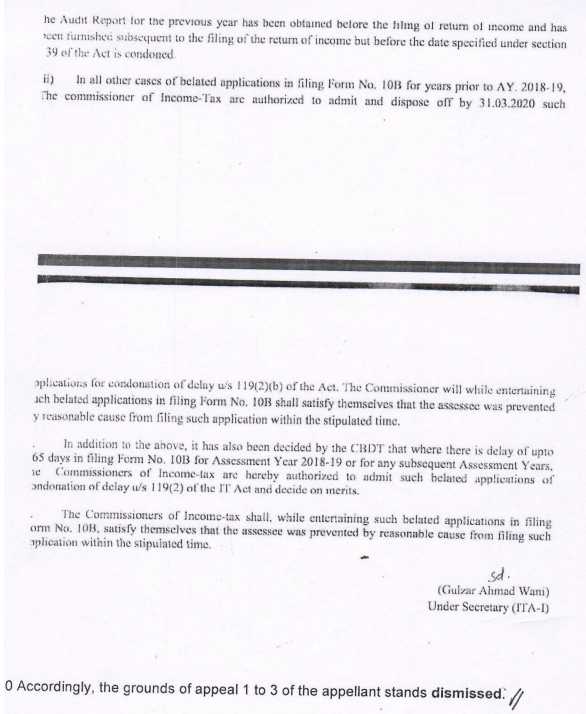

6.2.5 lt is also pertinent to note that filing of the Form 10B is mandatory to avail exemption u/s 11 from AY 2017-18 onwards. Therefore, denial of exemption on the count of non-filing of Form 10B within the stipulated time holds good. However, it is brought to the notice of the appellant that such delay in filing of Form 10B might have been condoned on application to learned CIT/Exemption as per the CBDT circular cited below for easy reference.

4. Dissatisfied, the assessee is in appeal before the Tribunal raising the following grounds of appeal :

| “1. |

|

On the facts in the circumstances of the case and as per the law the learned CIT(A) erred in confirming addition of Rs.1,11,62,306/- on the ground that the provisions of Section 11(2)(a) are not complied. |

| 2. |

|

The Ld. CIT(A) had erred by not considering the resolution passed |

| stating |

|

the specific purpose of accumulation and further failed to appreciate that the accumulation is made u/s 11(2) as per the law. |

| 3. |

|

The appellant craves leave to add, alter, amend or delete any of the grounds of the appeal.” |

5. The Ld. AR submitted that Form 10 does not specify any specific purpose to be stated for accumulation of income. She submitted that admittedly the assessee trust had delayed to comply with clause (a) of section 11(2) of the Act in the prescribed manner, however, a proper resolution has been passed by the assessee trust for specifying the funds for accumulation stating therein the specific purpose of accumulation. The Ld. AR submitted that mere failure to file Form 10 in due time does not disentitle the assessee trust to claim benefit of exemption u/s 11(2) of the Act. She submitted that under similar set of facts, the Courts/Tribunals have allowed the claim of exemption u/s 11(2) even if there is delay in filing Form 10. She, therefore, submitted that the delay in filing Form 10 should be condoned and benefit of exemption u/s 11 should be allowed to the assessee. In support of the above proposition, the Ld. AR relied on the following cases :

| i. |

|

Joy of Sharing Foundation-Charitable Trust v. ITO, Exemptions (Chennai – Trib.); |

| ii. |

|

Bible Fellowship Centre Wagholi v. ITO Pune – Trib.); |

| iii. |

|

ITO (E) v. Takshshila Foundation (NGO) ITD 677 (Ahmedabad – Trib.) and |

| iv. |

|

Gyandeep Charitable Trust v. ADIT [IT Appeal No. 555 (AHD) of 2023, dated 3-1-2024]. |

6. On the proposition that non-mentioning of specific purpose for accumulation in Form 10B would not disentitle the assessee trust to claim exemption u/s 11(2) of the Act, the Ld. AR relied on the following cases :

| i. |

|

CIT (Exemptions) v. Bochasanwasi Shri Akshar Purshottam Public cable Trust (SC); |

| ii. |

|

CIT (Exemptions) v. Bochasanwasi Shri Akshar Purshottam Public Charitable Trust (Gujarat); |

| iii. |

|

DIT, Exemptions, Bangalore v. Envisions (Karnataka); |

| iv. |

|

Bharat Kalyan Pratisthan v. DIT (Exemption) (Delhi); |

| v. |

|

DIT v. Mitsui & Co. Environmental Trust (Delhi); |

| vi. |

|

CIT v. Hotel & Restaurant Association (Delhi); |

| vii. |

|

ITO v. Yogakshema Trust ITD 408 (Cochin – Trib.); |

| viii. |

|

Dy. CIT (Exemption) v. State Institute of Health & Family Welfare 1 ITD 480 (Jaipur – Trib.) and |

| ix. |

|

Arhatic Yoga Ashram Management Trust v. ITO (Exemptions) Ward – 1, Chennai ITD 14 (Chennai – Trib.). |

7. The Ld. DR, on the other hand, relied on the order of the Ld. AO and the Ld. CIT(A)/NFAC.

8. We have heard the Ld. Representatives of the parties and perused the material on record as well paper book filed by the Ld. AR on behalf of the assessee. We have also perused the decisions cited by the Ld. AR. The facts of the case are not in dispute. Admittedly, there was delay in filing Form 10/10B by the assessee trust for the relevant AY 2017-18 under consideration. The Ld. AO has denied assessee’s claim of exemption to the assessee for the reason of non-compliance with the provisions of section 11(2)(a),(b)&(c) of the Act on account of non-filing for Form 10/10B within the prescribed time limit. The Ld. CIT(A/NFAC has dismissed the appeal of the assessee for the reasons reproduced in the preceding paragraphs which is mainly on account of non-compliance to the provisions of section 11(2)(a) and filing of Form 10 being barred by limitation. It is the submission of the Ld. AR that the Resolution passed by the assessee trust (placed on pages 07 and 17 of the paper book) clearly states the objects for which the funds were set apart, however, both the Ld. AO as well as the Ld. CIT(A)/NFAC has failed to take cognizance of the said Resolution specifying the specific purpose of accumulation therein. It is further contented that the accumulation has been made u/s 11(2) of the Act as per law. The assessee trust had deposited funds under the specified mode(s) prescribed u/s 11(5) of the Act and hence the claim of accumulation u/s 11(2) is a bonafide claim made by the assessee. The Ld. AR submitted that Form 10 (placed at pages 30-32 of the paper book) specifies the purpose as the object of the trust for the accumulation done by the assessee trust and one of the object is renovation and extension of the trust building. Placing reliance on the various judicial precedents (supra), the Ld. AR argued that even otherwise lack of declaration in Form 10 regarding specific purpose for which funds were being accumulated by the assessee trust would not be fatal to the exemption claimed u/s 11(2) of the Act.

9. We find some force in the arguments advanced by the Ld. AR. We find that the Hon’ble Gujarat High Court in the case of Bochasanwasi Shri Akshar Purshottam Public Cable Trust (supra) under the similar set of facts as that of the assessee in the present case, has allowed the assessee’s claim of exemption u/s 11(2) of the Act holding that non-specification of specific purpose for accumulation in Form 10 would not be fatal to the exemption u/s 11(2) of the Act. We further observe that the Hon’ble Supreme Court has dismissed the SLP filed by the Department in the above case (reported in (SC)) upholding the findings of the Hon’ble Gujarat High Court. This view has also been upheld by various decisions of the Hon’ble Courts/Tribunals (supra) cited by the Ld. AR.

10. As regards the assessee’s contention that mere failure to file Form 10/10B in due time would not disentitle the assessee to claim benefit of exemption u/s 11(2) of the Act, we find that Chennai Bench of the Tribunal in the case of Joy of Sharing Foundation-Charitable Trust (supra) has upheld this view by observing as under :

“6. We have heard both the parties and perused the material available on record. It is noted that the assessee is a public Charitable Trust formed in the year 2010 and was enjoying registration u/s.12AB of the Act and carrying on charitable activities. The assessee Trust is noted to have filed its RoI for AY 2022-23 on 07.09.2022 u/s.139(1) of the Act admitting ‘Nil’ income along with mandatory Form 10B i.e. Audit Report. In the RoI filed on 07.09.2022, the assessee Trust is noted to have duly disclosed under Schedule-I, the details of amount accumulated as per sec.11(2) of the Act as well as the same was duly disclosed in Form No.10B (Audit Report) at Column Nos.5 & 6 [refer Annexure-B] wherein we note that the sum of Rs.54 lakhs has been clearly mentioned therein as amount accumulated as per sec.11(2) of the Act. It is further noted that the assessee Trust while filing the ITR on 07.09.2022 has uploaded the Audit Report in Form No.10B [which was well before the due date u/s.139(1) of the Act] but the CPC in its intimation u/s.143(1) of the Act on 31.03.2023 has disallowed the accumulation of income of Rs.54 lakhs, only on the reason that assessee Trust didn’t file Form No. 10 [accumulation of income].

7. According to the assessee, while uploading RoI & Audit Report [Form 10B], the assessee also uploaded Form 10 [accumulation of income] and was of the bona fide belief that it has uploaded the Form 10 in the Income Tax Portal, but to its dismay when the return was processed by the CPC, and intimation dated 31.03.2023 was passed, it came to know that accumulation of income of Rs.54 lakhs has been denied, for not uploading the Form 10. The assessee Trust is noted to have re-filed/uploaded Form No.10 on 02.06.2023; and during the appellate proceedings before the Ld.CIT(A), has brought to his notice that the assessee Trust had filed/uploaded return as well as Audit Report in Form No.10B before the due date u/s.139(1) of the Act i.e. on 07.09.2022 as well as Form No.10 was uploaded, but due to technical glitches, it was unsuccessful and since, there was heavy load server got hung and which resulted in CPC rejecting the accumulation of Rs.54 lakhs. And assessee had again re-filed/uploaded on 02.06.2023 and a copy of Form No.10 has been filed before us. However, we note that the Ld.CIT(A) has dismissed the appeal of the assessee albeit on a different reason that for claiming exemption u/s.11 of the Act, it is mandatory to file Form No.10B before the due date of filing of return or should have got condonation of delay for belated filing of Form No.10B from the CIT (Exemption). However, we find that this findings of fact recorded by the Ld.CIT(A) is erroneous for the simple fact that the assessee had filed the Form 10B (audit-report) before the due date u/s.139(1) of the Act i.e. on 07.09.2022 and the CPC has refused accumulation of income u/s.11(2) of the Act only on the reason that Form No.10 [accumulation of income] has not been filed. Thus, we find that the Ld.CIT(A) has misdirected himself on the erroneous assumption that assessee Trust didn’t file Form No. 10B [i.e. Audit Report] when the correct fact is that assessee Trust had filed the Audit Report in Form No.10B along with the RoI on 07.09.2022. Thus, impugned action of the Ld.CIT(A) cannot be countenenced and need to be interfered with.

8. As discussed, the Ld.CIT(A) erred in rejecting the appeal on the ground which was not raised/flagged by the CPC i.e. non-filing of Form 10 [accumulation of income of a Trust] whereas the Ld.CIT(A) has denied the accumulation of income only on the ground that the assessee Trust didn’t file the Form No.10B [i.e. Audit Report]. We find that the assessee Trust has filed the RoI along with Audit Report before the due date u/s.139(1) of the Act and in the RoI as well as the Audit Report has clearly shown the accumulation of income u/s.11(2) of the Act to the tune of Rs.54 lakhs. In such a scenario, we are of the view that the Income Tax Authorities while processing the return for assessment/appellate order ought not to have rejected the accumulation of income on the aforesaid facts and circumstances of the case. In this regard, we refer to the decision of the Hon’ble jurisdictional High Court in the case of CIT v. SPIC Educational Foundation (TCA No.1593 of 2008 dated 12.12.2018), wherein the Hon’ble High Court has held that filing of Form 10 for accumulation of income u/s.11(2) of the Act which was filed beyond due date couldn’t disentitle the trust from exemption claimed u/s.11 of the Act. The Hon’ble Court directed the AO to examine the benefit of admissibility rather than to foreclose the claim of assessee on technicalities. Therefore, respectfully taking note of the binding decision of the Hon’ble High Court (supra), we hold that the Ld.CIT(A) erred by misdirecting on an issue which wasn’t raised by CPC; and since the TAR had been filed along with RoI filed within due date u/s.139(1) of the Act, and Form No.10 was again uploaded by the assessee on 02.06.2023, we are of the view that the First Appellate Authority erred in passing the impugned order, which we set aside and direct the CPC/AO to allow the accumulation of income claimed by the assessee u/s.11(2) of the Act to the tune of Rs.54 lakhs.”

11. Similar view has been taken by the Ahmedabad Bench of the Tribunal in the case of Takshshila Foundation (NGO) (supra) wherein it has been held as under :

“6.2. It has been held by various Courts that the requirement offiling Form 10/10B is merely directory in nature and failure to furnish Form 10/10B before due-date prescribed u/s 139(1) of the Act cannot be so fatal so as to deny they very claim of exemption u/s.11(2) of the Act. The following judicial precedents have reiterated the aforesaid principal:

| I. |

|

Association of Indian Panelboard Manufacturer v. Dy. CIT – TA 655 of 2022 (Guj.); |

| II. |

|

II. Dy. CIT v. Croygas Equipments (P.) Ltd. [IT Appeal No. 415 (Ahd.) of 2020, dated 16-6-2023]; |

| III. |

|

III. True Sparrow Systems (P.) Ltd. v. Pr. CIT [IT Appeal No. 765 (Ahd.) of 2019, dated 22-4-2022]; |

| IV. |

|

IV. Shardaben Education Trust v. ITO [IT Appeal No. 2312 (Ahd.) of 2018, dated 16-11-2022]; |

| V. |

|

V. CIT v. Xavier Kelavani Mandal (P.) Ltd. (Mag.) (Guj.); |

| VI. |

|

VI. Zenith Processing Mills v. CIT [1996] 219 ITR 721 (Guj.); |

| VII. |

|

VII. CIT v. Mayur Foundation [2005] 274 ITR 562 (Guj.); |

| VIII. |

|

VIII. CIT v. Gujarat Oil & Allied Industries [1993] 201 ITR 325 (Guj.); |

| IX. |

|

IX. CIT v. G. M. Knitting Industries (P.) Ltd. ITR 456 (SC); |

| X. |

|

X. CIT v. Web Commerce (India) (P.) Ltd. ITR 135 (Delhi); |

| XI. |

|

XI. CIT v. Contimeters Electricals (P.) Ltd. ITR 249 (Delhi); |

| XII. |

|

XII. Pr. CIT v. Surya Merchants Ltd. ITR 105 (All.); |

| XIII. |

|

DIC Fine Chemicals (P.)Ltd. v. Dy. CIT ITD 672 (Kol.). |

6.3. In light of the above facts and judicial pronouncements, we find that the delay in filing Form 10B was due to technical issues and was beyond the control of the assessee. The procedural requirement should not deny the substantive claim of exemption under section 11 of the Act. Therefore, we direct the Assessing Officer to grant the exemption under section 11 as claimed by the assessee. Hence, the Cross Objection filed by the assessee is accordingly allowed.”

12. Based on the facts and circumstances of the case and legal position enumerated above, we set aside the order of the Ld. CIT(A)/NFAC and direct the Ld. AO to allow the assessee’s claim of exemption u/s 11 of the Act. The grounds raised by the assessee are accordingly allowed.

13. In the result, the appeal of the assessee is allowed.

ITA No. 2148/pUN/2025, AY 2018-19

14. Both the sides are unanimous in stating that the facts and the grounds of appeal in ITA No. 2148/pUN/2025 are identical to the grounds raised in ITA No. 2147/pUN/2025 except the variance in amounts. Thus, in view of the fact that the issue(s) raised in both the appeals are identical and are arising from same set of facts, the finding given by us while adjudicating the appeal in ITA No. 2147/pUN/2025 would mutatis mutandis apply to the appeal in ITA No. 2148/pUN/2025 as well. Accordingly, the grounds of appeal raised by the assessee in ITA No. 2148/pUN/2025 are allowed in the same terms.

15. To sum up, both the appeals of the assessee in ITA Nos. 2147 & 2148/pUN/2025 are allowed.