ORDER

1. The petitioner is before this Court against the impuged Order in Original No.15/2025-GST-ADC dated 08.01.2025 passed by the respondent, whereby, the proposal in Show Cause Notice No.115/2024-GST(ADC) dated 25.07.2024 has been confirmed against the petitioner for the tax period 2017-2018 to 2022-2023. The Operative portion of the impugned order reads as under:-

“ORDER”

i. I confirm the demand of Rs.22,65,05,082/- (IGST Rs.22,65,05,082/-) (Rupees Twenty-two Crore sixty-five lakh five thousand and eighty two only) as discussed in Para 7 above in terms of Section 74(9) of the CGST Act, 2017 read with similar provision of the TNGST Act, 2017 made applicable to IGST vide Section 20 f the IGST Act, 2017.

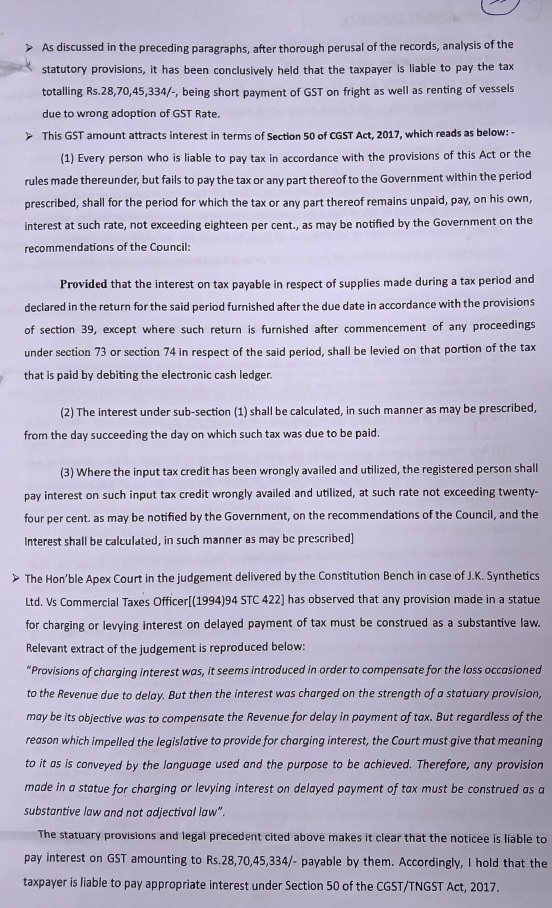

ii. I confirm the demand of appropriate interest on the demand confirmed under Sl.No.(i) above and order for recovery of the same in terms of Section 50 of the CGST Act, 2017, read with similar provision of the TNGST Act, 2017 and made applicable to IGST vide Section 20 of the IGST Act, 2017.

iii. I impose penalty on the taxpayer for an amount of Rs.22,65,05,082/- (Rupees Twenty-two Crore sixty-five lakh five thousand and eighty two only) on the demand confirmed under Sl.No.(i) above in terms of Section 74(9) of the CGST Act, 2017, r/w Section 122(2)(b) of the CGST Act, 2017 along with similar provision of the TNGST Act, 2017 and made applicable to IGST vide Section 20 of the IGST Act, 2017.

iv. I confirm the demand of Rs.6,05,40,252/- (IGST Rs.6,05,40,252/-) (Rupees Six Crore five lakh forty thousand two hundred and fifty two only) as discussed in Para 7 above in terms of Section 74(9) of the CGST Act, 2017 r/w similar provision of the TNGST Act, 2017 made applicable to IGST vide Section 20 of the IGST Act, 2017.

v. I confirm the demand of appropriate interest on the demand confirmed under Sl.No.(iv) above and order for recovery of the same in terms of Section 50 of the CGST Act, 2017 read with similar provision of the TNGST Act, 2017 and made applicable to IGST vide Section 20 of the IGST Act, 2017.

vi. I impose penalty on the taxpayer for an amount of Rs.6,05,40,252/-(Rupees Six Crore five lakh forty thousand two hundred and fifty two only) on the demand confirmed under Sl.No.(iv) above in terms of Section 74(9) of the CGST Act, 2017 r/w Section 122(2)(b) of the CGST Act, 2017 along with similar provision of the TNGST Act, 2017 and made applicable to IGST vide Section 20 of the IGST Act, 2017.

2. The breakdown of the above demand confirmed by the impugned Order-in-Original is as under:-

| FY |

Taxable Value @ 5% as per Sale register (A) |

IGST Payable @ 18% (B) |

IGST Paid @ 5% (C) |

Diff. IGST to be Paid (B-C) |

| 2017-18 |

21377600 |

3847968 |

1068880 |

2779088 |

| 2018-19 |

269113870 |

48440497 |

13455694 |

34984803 |

| 2019-20 |

1182376314 |

212827737 |

59118816 |

153708921 |

| 2020-21 |

269478997 |

48506219 |

13473950 |

35032270 |

| 2021-22 |

0 |

0 |

0 |

0 |

| 2022-23 |

0 |

0 |

0 |

0 |

| Total |

1,74,23,46,781 |

31,36,22,421 |

8,71,17,339 |

22,65,05,082 |

3. A part of the demand covered by Clauses I, II and III is as under:

“i. I confirm the demand of Rs. 22,65,05,082/- (IGST Rs. 22,65,05,082/-) (Rupees twenty-two crore sixty-five lakh five thousand and eighty-two only) as discussed in Para 7 above in terms of Section 74(9) of the CGST Act, 2017 read with similar provision of the TNGST Act, 2017 made applicable to IGST vide Section 20 of the IGST Act, 2017.

ii. I confirm the demand of appropriate interest on the demand confirmed under Sl. No. (i) above and order for recovery of the same in terms of Section 50 of the CGST Act, 2017 read with similar provision of the TNGST Act, 2017 and made applicable to IGST vide Section 20 of the IGST Act, 2017.

iii. I impose penalty on the taxpayer for an amount of Rs. 22,65,05,082/- (Rupees twenty-two crore sixty-five lakh five thousand and eighty-two only) on the demand confirmed under Sl. No. (i) above in terms of Section 74(9) of the CGST Act, 2017 read with read with Section 122(2)(b) of the CGST Act, 2017 along with similar provision of the TNGST Act, 2017 and made applicable to IGST vide Section 20 of the IGST Act, 2017.”

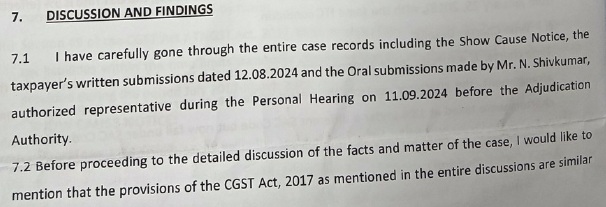

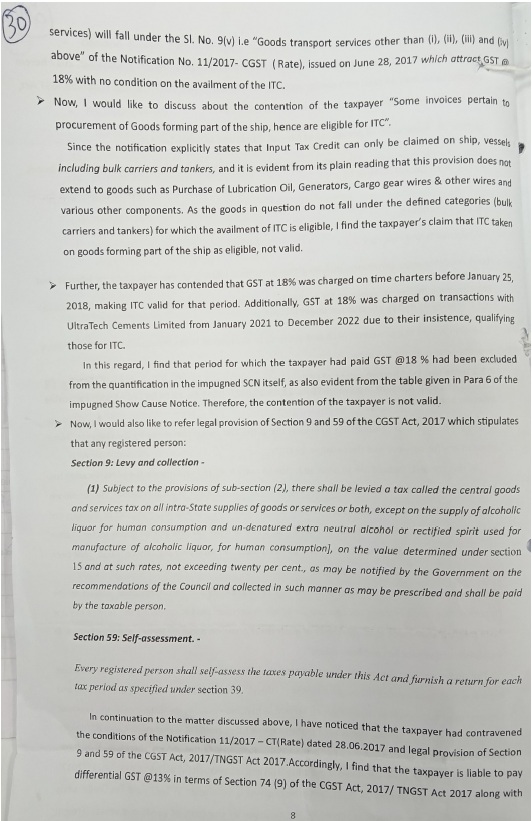

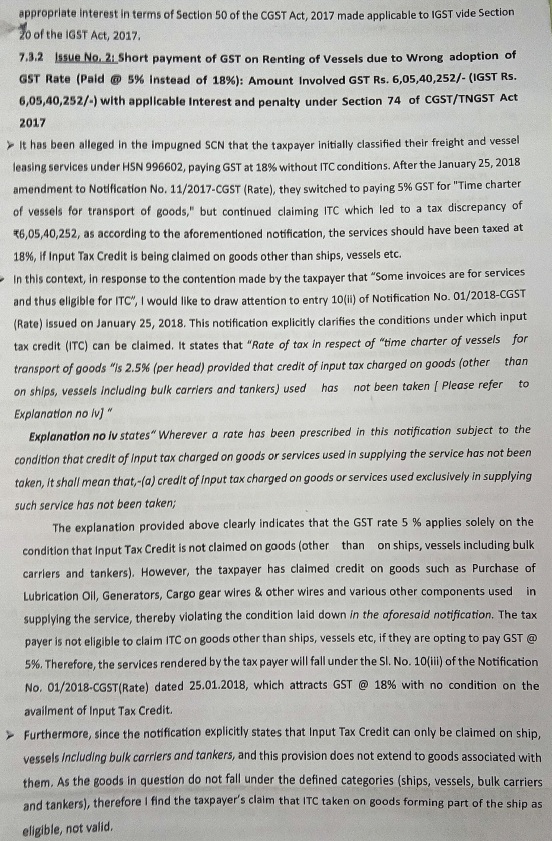

4. As far as Clauses IV, V and VI are concerned, the allegation against the petitioner was that during the period from July 2017 to January 2018 (up to 25.01.2018), the petitioner made a supply of services viz. Freight and Leasing / Renting of the Vessels with Crew Members by classifying the services under HSN 996602 and paid 18% GST without availing ITC as per Serial No.10(ii) of Notification No.11/2017-CGST (Rate) dated 28.06.2017.

5. However, by amendment to the above notification with effect from 25.01.2018, the petitioner started discharging tax at 5% for renting vessels as per Serial No.10, Column 3 to the above notification for the “Time charter of vessels for transport of goods”. Thus, it was stated that the petitioner continued to avail input tax credit wrongly and was, therefore, not eligible to avail the benefit of the above Serial No.10(ii) of Notification No.11/2017-CGST (Rate) dated 28.06.2017.

6. By the impugned order, it has been concluded that the petitioner will be liable to tax in terms of Serial No.10(iii) to the above Notification at 18%.

7. The discussion in the impugned order leading to the aforesaid conclusion is as under :-

8. In this writ petition, the petitioner has challenged the impugned order primarily on the ground that the issue is no longer res intergra is covered by the decision of the Hon’ble Supreme Court in Chandrapur Magnet Wires (P.) Ltd. v. CCE (SC)/1996 (81) E.L.T. 3 (SC), wherein the Hon’ble Supreme Court in Paragraph No.7 held as under:

“7. In view of the aforesaid clarification by the Department, we see no reason why the assessee cannot make a debit entry in the credit account before removal of the exempted final product. If this debit entry is permissible to be made, credit entry for the duties paid on the inputs utlised in manufacture of the final exempted product will stand deleted in the accounts of the assessee. In such a situation, it cannot be said that the assessee has taken credit for the duty paid on the inputs utilised in the manufacture of the final exempted product under Rule 57A. In other other words, the claim for exemption of duty on the disputed goods cannot be denied on the plead that the assessee has taken credit of the duty paid on the inputs used in manufacture of these goods. “

9. The learned counsel for the petitioner submitted that this view has been reiterated in several cases, not only by the Tribunal but also by various High Courts across the country. Reference is made to the decision of the Division Bench of Allahabad High Court in Hello Minerals Water (P.) Ltd. v. Union of India 2004 (174) E.L.T. 422 (All.) wherein the reference was made to the decision of the Larger Bench of the Tribunal in Franco Italian Co. (P.) Ltd. v. CCE (CEGAT- New Delhi)/2000 (120) E.L.T.792.

10. The learned counsel for the petitioner submits that the aforesaid decision had recently also followed by the Tribunal in its recent decision in the case of Pepsico India Holdings (P.) Ltd. v. CCE [Excise Tax Appeal No. E/41318 of 2015-DB, dated 10-12-2019].

11. On the other hand, the learned counsel for the respondent would submit that the challenge to the impugned Order is without merits and the submissions made by the learned counsel for the petitioner cannot be countenanced.

12. It is submitted by the learned counsel for the respondent that the dispute pertains to availing of ineligible Input Tax Credit which denied the petitioner the benefit of Serial No.9(II) and 10(II) to Notification No.11/2017-Central Tax(Rate) dated 28.06.2017. After the impugned order was issued on 25.07.2024, the petitioner reversed the input tax credit which was wrongly availed by the petitioner on 28.03.2025 and therefore, the decision of the Hon’ble Supreme Court as also that of the High Courts cannot be applied to the facts of present case.

13. It is submitted that after availing the Input Tax Credit, the petitioner should have immediately reversed it to avail the benefit of the aforesaid notification. It is stated that in this case, the petitioner had an opportunity to reverse the Input Tax Credit earlier, which was wrongfully availed. However, the petitioner chose not to reverse the credit and therefore the benefit of exemption under Notification No.11/2017-Central Tax (Rate) dated 28.06.2017 has been denied to the petitioner, which cannot be found fault with.

14. That apart, it is submitted by the learned counsel for the respondent that even decision of the Allahabad High Court which was cited by the learned counsel for the petitioner in Hello Minerals Water (P) Ltd. (supra) which followed the decision of the Hon’ble Supreme Court in Chandrapur Magnet Wires Pvt Ltd. (supra), the circular issued by the Board. It is submitted that the reversal should have been made before its utilization, hence, it is submitted that this writ petition is liable to be dismissed.

15. I have considered the arguments advanced by the learned counsel for the petitioner as well as the learned counsel for the respondent and I have also perused the impugned order passed by the respondent.

16. In the present case, the petitioner wrongly availed input tax credit to pay tax at 2.5% under Serial No.9(ii) and 10(ii) to the Notification No.11/2017-CGST (Rate) dated 28.06.2017 as amended by Notification No.01/2018-CGST (Rate) dated 25.04.2018 with effect from 25.01.2018 during the period in dispute.

17. Thus, the impugned order has been passed whereby the benefit under the said Serial Nos to the above Notification No.11/2017-CGST (Rate) dated 28.06.2017 as amended by Notification No.01/2018-CGST (Rate) dated 25.04.2018 with effect from 25.01.2018, has been denied. Instead, tax at 9% under Serial No.9(v) and 10(iii) has been imposed on the petitioner.

18. By virtue of Section 20 of IGST Act, 2017, the provisions of the CGST Act apply mutatis mutandis, insofar as may be, in relation to integrated tax as they apply in relation to Central tax as if they were enacted under the IGST Act. In other words, there is an incorporation of the provisions of the CGST Act into the IGST Act, 2017.

19. The decision of the Hon’ble Supreme Court in Chandrapur Magnet Wires Pvt Ltd. (supra) which was cited by the learned counsel for the petitioner applies only to a situation where the Input Tax Credit was wrongly availed and was reversed before removal of the final product. In other words, before its utilization.

20. The decision of the Allahabad High Court in Hello Minerals Water (P.) Ltd. (supra) which purports to follow the above decision of the Hon’ble Supreme Court is not in accordance with the law settled by the Hon’ble Supreme Court in Chandrapur Magnet Wires Pvt Ltd case, referred to supra and is therefore not binding on this Court.

21. Therefore, I shall proceed to pass an order independently following the principle laid down by the Hon’ble Supreme Court in Chandrapur Magnet Wires Pvt Ltd case (supra) in the changed scenario under the GST regime.

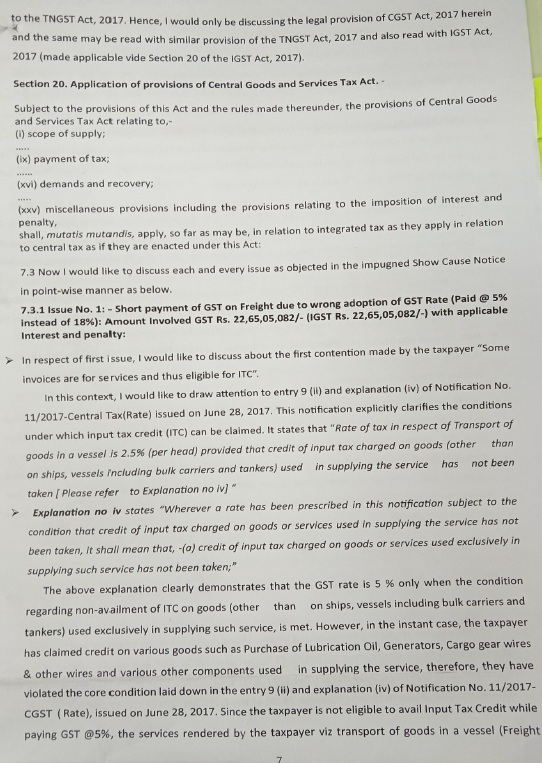

22. For the purpose of a proper disposal of the present case, it will be useful to refer to Serial No.9(ii) and (v) and Serial No.10(ii) and (iii) to the Notification No.11/2017-CGST (Rate) dated 28.06.2017

23. Notification No.11/2017-CGST (Rate) referred to supra not only specifies the rate of tax, but also exempts a registered person from payment of tax and also specifies the circumstances under which tax is to be paid on a Reverse Charge Mechanism.

24. Text of relevant portion of Serial No.9(ii) and (v), and Serial No.10(ii) and (iii) of Notification No.11/2017-Central Tax (Rate) are reproduced below:

G.S.R……(E).- In exercise of the powers conferred by sub-section (1) of section 9, sub section (1) of section 11, sub-section (5) of section 15 and sub-section (1) of section 16 of the Central Goods and Services Tax Act, 2017 (12 of 2017), the Central Government, on the recommendations of the Council, and on being satisfied that it is necessary in the public interest so to do, hereby notifies that the central tax, on the intra-State supply of services of description as specified in column (3) of the Table below, falling under Chapter, Section or Heading of scheme of classification of services as specified in column (2), shall be levied at the rate as specified in the corresponding entry in column (4), subject to the conditions as specified in the corresponding entry in column (5) of the said Table:-

| Sl.No. |

Chapter, Section or Heading |

Description of Service |

Rate (per cent) |

Condition |

| (1) |

(2) |

(3) |

(4) |

(5) |

| 9 |

Heading 9965 (Goods transport services) |

(ii) Transport of goods in a vessel. |

2.5 |

Provided that credit of input tax charged on goods (other than on ships, vessels including bulk carriers and tankers) used in supplying the service has not been taken [Please refer to Explanation no.(iv)] |

|

|

(v) Goods transport services other than (i), (ii), (iii) and (iv) above. |

9 |

|

| 10 |

Heading 9966 (Rental services of transport vehicles) |

(ii) Time charter of vessels for transport of goods. |

2.5 |

Provided that credit of input tax charged on goods (other than on ships, vessels including bulk carriers and tankers) has not been taken [Please refer to Explanation no.(iv)]. |

|

|

(iii) Rental services of transport vehicles with or without operators, other than (i) and (ii) above. |

|

|

25. Explanation (iv) to the above Notification which is relevant is extracted hereunder:-

Explanation (iv):-

” (iv) Wherever a rate has been prescribed in this notification subject to the condition that credit of input tax charged on goods or services used in supplying the service has not been taken, it shall mean that:-

(a) credit of input tax charged on goods or services used exclusively in supplying such service has not been taken: and

(b) credit of input tax charged on goods or services used partly for supplying such service and partly for effecting other supplies eligible for input tax credits, is reversed as if supply of such service is an exempt supply and attracts provisions of sub section (2) of Section 17 of the Central Goods and Services Tax Act, 2017 and the rules made thereunder”.

26. The above Notification No.11/2017-CGST (Rate) dated 28.06.2017 has been issued by the Central Government in exercise of the powers conferred under the following provisions of the CGST Act, 2017 (12 of 2017):-

| Sections |

Descriptions |

| 9(1) |

Subject to the provisions of sub-section (2), there shall be levied a tax called the central goods and services tax on all intra-State supplies of goods or services or both, except on the supply of alcoholic liquor for human consumption, on the value determined under section 15 and at such rates, not exceeding twenty per cent., as may be notified by the Government on the recommendations of the Council and collected in such manner as may be prescribed and shall be paid by the taxable person. |

| 9(3) |

The Government may, on the recommendations of the Council, by notification, specify categories of supply of goods or services or both, the tax on which shall be paid on reverse charge basis by the recipient of such goods or services or both and all the provisions of this Act shall apply to such recipient as if he is the person liable for paying the tax in relation to the supply of such goods or services or both. |

| 9(4) |

The Government may, on the recommendations of the Council, by notification, specify a class of registered persons who shall, in respect of supply of specified categories of goods or services or both received from an unregistered supplier, pay the tax on reverse charge basis as the recipient of such supply of goods or services or both, and all the provisions of this Act shall apply to such recipient as if he is the person liable for paying the tax in relation to such supply of goods or services or both. |

| 11(1) |

Where the Government is satisfied that it is necessary in the public interest so to do, it may, on the recommendations of the Council, by notification, exempt generally, either absolutely or subject to such conditions as may be specified therein, goods or services or both of any specified description from the whole or any part of the tax leviable thereon with effect from such date as may be specified in such notification. |

| 15(5) |

Notwithstanding anything contained in sub-section (1) or sub-section (4), the value of such supplies as may be notified by the Government on the recommendations of the Council shall be determined in such manner as may be prescribed.

Explanation.—For the purposes of this Act,––

(a) persons shall be deemed to be “related persons” if––

(i) such persons are officers or directors of one another‘s businesses;

(ii) such persons are legally recognised partners in business;

(iii) such persons are employer and employee;

(iv) any person directly or indirectly owns, controls or holds twenty-five per cent. or more of the outstanding voting stock or shares of both of them;

(v) one of them directly or indirectly controls the other;

(vi) both of them are directly or indirectly controlled by a third person;

(vii) together they directly or indirectly control a third person; or

(viii) they are members of the same family;

(b) the term “person” also includes legal persons;

(c) persons who are associated in the business of one another in that one is the sole agent or sole distributor or sole concessionaire, howsoever described, of the other, shall be deemed to be related. |

| 16(1) |

Every registered person shall, subject to such conditions and restrictions as may be prescribed and in the manner specified in section 49, be entitled to take credit of input tax charged on any supply of goods or services or both to him which are used or intended to be used in the course or furtherance of his business and the said amount shall be credited to the electronic credit ledger of such person. |

| 148 |

(1) Every registered person may be assigned a goods and services tax compliance rating score by the Government based on his record of compliance with the provisions of this Act.

(2) The goods and services tax compliance rating score may be determined on the basis of such parameters as may be prescribed.

(3) The goods and services tax compliance rating score may be updated at periodic intervals and intimated to the registered person and also placed in the public domain in such manner as may be prescribed.

|

27. The petitioner was expected to satisfy the requirements, conditions in Column 5 to the above Notification and Explanation (iv) to the aforesaid Notification by not availing the Input Tax credit used on supply exclusively used for supplying taxable service and wherever Input Tax Credit charged on goods or services was used partly for supplying such service.

28. The proposal in the Show Cause Notice dated 25.07.2024 which has been confirmed in the impugned order dated 08.01.2025 of the Respondent has resulted in denial of the benefit of Serial No.9(ii) and Serial No.10(ii) to Notification No.11/2017-CT (Rate) dated 28.06.2017 as amended by Notification No.01/2018-CGST (Rate) dated 25.04.2018 with effect from 25.01.2018.

29. The denial of benefit of the concessional rate of tax, in view of the aforesaid notification is purely on account of the petitioner wrongly availing Input Tax Credit on goods used for supplying the service namely transport of goods in a vessel as per the Serial No.9(ii) and time charter of vessel for transport of goods as per Serial No.10(ii) of the aforesaid Notification.

30. Notification No.11/2017-CGST (Rate) dated 28.06.2017 as amended by Notification No.01/2018-CGST (Rate) dated 25.04.2018 with effect from 25.01.2018 is not only a rate ratification, but also exemption notification.

31. Ideally, the Show Cause Notice issued to the petitioner should have called upon the petitioner to show cause as to why the Input Tax Credit that was wrongly availed by the petitioner contrary to condition in Column (5) should not be denied together with interest and penalty applying the ratio of the Hon’ble Supreme Court in Unichem Laboratories Ltd. v. CCE 2002 (145) E.L.T. 502 (SC)/(2002) 7 SCC 145. In Paragraph No.12, the Hon’ble Supreme Court held as under:-

“12. For the aforementioned reasons, we are of the view that denial of benefit of the notification to the appellant was unfair. There can be no doubt that the authorities functioning under the Act must, as are in duty bound, to protect the interest of the Revenue by levying and collecting the duty in accordance with law — no less and also no more. It is no part of their duty to deprive an assessee of the benefit available to him in law with a view to augment the quantum of duty for the benefit of the Revenue. They must act reasonably and fairly.”

32. Following the ratio of the Hon’ble Supreme Court in Unichem Laboratories referred to supra to the facts of the present case, it has to be held that it was no part of the duty of the Department to collect or to retain tax amount, which is not due to it or is legitimately due from the petitioner nor it was part of the duty of the Department to augment Revenue by depriving the benefit that was otherwise available to the petitioner.

33. If the true and accurate ratio of the Hon’ble Supreme Court in Chandrapur Magnet Wires Pvt Ltd. (supra) was applied to the facts of the present case, the petitioner should have been called to reverse the wrongly availed and utilized Input Tax Credit together with interest and penalty under Section 74 of the respective GST Enactments.

34. Therefore, denial of concessional rate of duty in terms of the aforesaid Notification cannot be justified as the authorities under the statute are not expected to impose a higher tax liability on account of inadvertent mistake that may have been committed by an assessee.

35. In my view, the denial of substantive benefit of the above rate Notification also cannot be justified to impose a disproportionate liability under Section 74 of the respective GST Enactments merely because Input Tax Credit was wrongly availed / utilized by the petitioner.

36. In this case, the petitioner has paid the amount post facto on 28.03.2025, after the impugned order was passed under Section 74 of the respective GST Enactments on 08.01.2025. The reversal Input Tax Credit post facto was not sufficient unless it is accompanied with payment of interest and penalty in accordance with Section 74 of the respective GST Enactments.

37. Under Section 74 of the respective GST Enactments, payment of tax or reversal of Input Tax Credit wrongly availed and utilised has to accompany payment of Interest or Penatly. In fact, Section 74 of the respective GST Enactments itself contains an inbuilt amnesty in so far as payment of penalty is concerned. There is no concession from payment of interest. For the sake of clarity, Section 74 of the respective GST Enactments can be summarized as follows:

| Section 74(5) |

Section 74(8) |

Section 74(11) |

| Before issuance of Show Cause Notice |

After issuance of Show Cause Notice |

After passing of the Assessment Order |

| Payment of |

| (i) tax, not paid, or short paid or erroneously refunded or ITC wrongly availed and utilized together with |

| (ii) interest under section 50, and |

| (iii) Penalty equivalent to fifteen per cent |

Penalty equivalent to twenty-five percent of such tax within thirty days of issue of the notice |

Penalty equivalent to fifty per cent of such tax within thirty days of communication of the order |

38. In this case, the impugned order is dated 08.01.2025. The wrongly availed ITC has been purportedly paid only on 08.03.2025 for a sum of Rs.5,67,514/-. Therefore, the benefit of Section 74(5), (8) and (11) of the respective GST Enactments is also not available to the petitioner. Hence, the petitioner has asked to pay 100% penalty equivalent to the Input Tax Credit that was wrongly availed and utilised by the petitioner. However, whether the reversal/payment made on 08.03.2025 commensurates with the actual Input Tax Credit that was wrongly availed and utilised by the petitioner. Therefore, this aspect would require a proper determination.

39. Therefore, following the decisions of the Hon’ble Supreme Court in Chandrapur Magnet Wires Pvt Ltd. (supra) and Unichem Laboratories Ltd. (supra) referred to supra, the impugned order is liable to be quashed for such determination of Input Tax Credit that was wrongly availed and utilised by the petitioner and determination of 100% penalty equivalent to such Input Tax Credit that was wrongly availed and utilised by the petitioner.

40. Therefore, this writ petition is partly allowed by remitting the case back to the respondent to determine the actual amount of Input Tax Credit that was wrongly availed and utilized and for determination of interest under Section 50 and 100% of penalty on the wrongly availed and utilized Input Tax Credit. Connected miscellaneous petition is closed. No costs.