ORDER

1. The petitioner/Karnataka Vikas Grameena Bank is before this Court seeking the following prayers:

“(A) Issue a writ of certiorari or any other writ or direction to quash impugned SCN No. DCCT (Enf-2)/HBL/SCN-03/2023-24 dated 27-12-2023 issued by respondent No.1, enclosed as Annexure-A, for the reasons stated in the grounds.

(B) Issue a writ of certiorari or any other writ or direction to quash impugned SCN No. ACCT/Audit-1/HBL/GST/DRC-1/23-24/B-337 dated 28-12-2023 along with Form DRC-1, issued by respondent No.2, enclosed as Annexure-B, for the reasons stated in the grounds.

(C) Issue a writ of certiorari or any other writ or direction to quash impugned SCN No. ACCT/Audit-1/HBL/GST/DRC-1/23-24/B-338 dated 28-12-2023 along with Form DRC-1, issued by respondent No.2, enclosed as Annexure-C, for the reasons stated in the grounds.

(D) Issue a writ of certiorari or any other writ or direction to quash impugned SCN No. ACCT/Audit-1/HBL/GST/DRC-1/23-24/B-339 dated 28-12-2023 along with Form DRC-1, issued by respondent No.2, enclosed as Annexure-D, for the reasons stated in the grounds.

(E) Issue a writ of certiorari or any other writ or direction or order to declare Notification 9/2023-CT dated 31st March, 2023, issued by respondent No.3, enclosed as Annexure-E, as ultra vires Section 168A of CGST Act, 2017 for the reasons stated in the grounds.

(F) Issue a writ of certiorari or any other writ or direction or order to declare Notification No.06/2023 dated 06.04.2023, issued by respondent No.4, enclosed as Annexure-F as ultra-vires Section 168A of KGST Act, 2017 for the reasons stated in the grounds.

And

(G) Grant such other consequential reliefs as this Honourable High Court may think fit including the cost of this writ petition.”

2. Heard Sri V.Raghuraman, learned senior counsel appearing for the petitioner, Sri G.M.Gangadhar, learned Additional Advocate General appearing for respondents 1, 2 and 4 and Sri M.B. Kanavi, learned counsel appearing for respondent No.3.

3. Facts, in brief, germane are as follows: –

3.1. The petitioner is a Regional Rural Bank established under the provisions of the Regional Rural Banks Act, 1976. The respondents are the State and the Union of India. The contesting respondents are respondents 1 and 2, the Commercial Taxes Department of the State Government. It would suffice if the narration would commence from 17-06-2022, the date on which an inspection is conducted by the 1st respondent/Deputy Commissioner of Commercial Taxes in the premises of the petitioner/Bank invoking power under Section 67 of the Central Goods and Services Tax Act, 2017 (‘CGST Act’) to verify tax compliance by the Bank. After the said inspection, a notification comes to be issued by the Central Board of Indirect Taxes and Customs under Section 168A of the CGST Act extending the time limit specified under Section 73(10) of the CGST Act for issuance of order under Section 73(9) of the CGST Act for recovery of tax not paid or short paid or input tax created wrongly shown for the financial years 2017-18, 2018-19 and 2019-20. The corresponding notification is issued by the Government of Karnataka on the same lines for the same period on 06-04-2023.

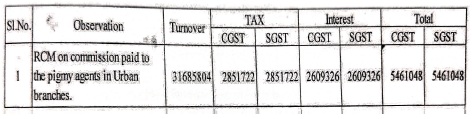

3.2. A report of inspection so conducted on 17-06-2022 is drawn on 20-07-2023 and is placed before the Joint Commissioner of Commercial Taxes (Enforcement) to initiate proceedings against the Bank under Section 73 of the CGST Act for short payment of tax and or no payment of tax rather under the Karnataka Goods and Services Tax Act, 2017 (‘KGST Act’). On 09-08-2023,Form DRC-01A is issued by the 1st respondent for the financial year 2018-19 alleging that the petitioner Bank has failed to deposit tax amount under reverse charge mechanism, which would be on the commission paid to the pigmy agents in the urban branches. Similarly, Form DRC-01A is issued by the 2nd respondent for the financial year 2019-20 and 2021-22. To this, the petitioner replied contending that pigmy agents are employees of the Bank and hence, no GST can be levied on the salary paid to them. It was also contended by the Bank that pigmy agents do not come under the ambit of business facilitators to attract reverse charge levy. The aforesaid was the reply submitted by the petitioner to the 1st respondent. The petitioner also replies to the 2nd respondent on the same lines.

3.3. Finding the reply to be unsatisfactory, the 1st and 2nd respondents issued show cause notices to the Bank between 27-12-2023 and 28-12-2023. The petitioner now challenges these notices issued to the Bank, on the score that it is not liable to pay any CGST for any regime or the KGST. The petitioner, apart from challenging the show cause notices so issued, also challenges the notification which extended the time limit for issuing show cause notices under Section 73 of the KGST or CGST Acts as ultra vires of Section 168A of the CGST Act. The aforesaid is the broad contours of challenge in the case at hand.

SUBMISSIONS:

PETITIONER:

4. The learned senior counsel for the petitioner Sri V.Raghuraman would vehemently contend that pigmy agents are employees of the Bank and, therefore, their services cannot be charged under the GST. He would seek to place reliance upon Section 7(2)(a) r/w Sl.No.1 of Schedule III which exempts services by an employee to the employer in the course of or in relation to his employment. He would contend that pigmy agents are workmen under the Industrial Disputes Act, 1947 as held by the Apex Court in INDIAN BANK’S ASSOCIATION’s case. TDS deducted on payments made to pigmy agents is enough circumstance to consider the commission that they receive as salary. The learned senior counsel would further contend that pigmy agents are not to be considered as business facilitators as defined in the Notification dated 28-06-2017. They are not intermediaries appointed by the banking company under the guidelines issued by the Reserve Bank of India. They are employees of the Bank. The impugned show cause notices thus suffer from want of jurisdiction when the Bank has exemption to pay tax. The time limit extended for issuing notices and passing orders is contrary to Section 168A of the KGST Act. The demand made in the show cause notices cannot be sustained as per the principle of revenue neutrality. The learned senior counsel seeks the prayers that are sought to be granted at the hands of this Court on the aforesaid score.

AAG – STATE:

5. Per contra, the learned Additional Advocate General Sri G.M. Gangadhar would vehemently refute the submissions in contending that the petitioner has an alternative and efficacious remedy of filing an appeal under Section 107 of the CGST Act. The basis for issuing show cause notices is legal and valid. The GST charged on the commission payable to pigmy agents is in consonance with the provisions of the CGST Act. The pigmy agents are paid commission and not salary in the case before the Court. Therefore, the petitioner would be liable to pay GST on the commission so paid in terms of Section 9(3) of the CGST Act. The petitioner/Bank has not furnished documents to show that there exists an employer-employee relationship between the petitioner bank and pigmy agents. The Reserve Bank of India Circular referred to by the petitioner does not restrict the definition of business facilitator as intermediary. The pigmy agents are used for financial facilitation or as business facilitator providing financial services. As a rule, pigmy agent is not restricted only to collection of deposits for one particular scheme of deposits. It can be extended to other services. They are akin to business correspondents. Therefore, the charge of GST is valid and legal.

6. I have given my anxious consideration to the submissions made by the respective learned counsel and have perused the material on record. In furtherance whereof, the only issue that falls for consideration is:

THE ISSUE:

“Whether the petitioner is liable to discharge Goods and Services Tax, on the services rendered and commission paid to the pigmy agents?”

CONSIDERATION:

Nature of employment of pigmy agents:

7. The learned senior counsel with considerable emphasis contends that pigmy agents are in essence and in law, employees of the Bank. Consequently, the services rendered by them cannot be brought within the taxable net of GST. It is further urged that such agents fall within the definition of ‘workmen’ under the Industrial Disputes Act, 1947 thereby fortifying the existence of employer-employee relationship. The question as to the true nature of engagement of deposit collectors/pigmy agents, whether they are workmen within the meaning of the Industrial Disputes Act, 1947 or independent agents, has not remained in the realm of ambiguity. The issue comes to be decided by the Apex Court in Indian Banks Association v. Workmen of Syndicate Bank (SC)/(2001) 3 SCC 36 wherein it is held as follows:

“…. …. ….

25. Further, as seen from Section 2(rr) of the Industrial Disputes Act, the commission received by Deposit Collectors is nothing else but wage, which is dependent on the productivity. This commission is paid for promoting the business of the various banks.

26. We also cannot accept the submission that the banks have no control over the Deposit Collectors. Undoubtedly, the Deposit Collectors are free to regulate their own hours of work, but that is because of the nature of the work itself. It would be impossible to fix working hours for such Deposit Collectors because they have to go to various depositors. This would have to be done at the convenience of the depositors and at such times as required by the depositors. If this is so, then no time can be fixed for such work. However, there is control inasmuch as the Deposit Collectors have to bring the collections and deposit the same in the banks by the very next day. They have then to fill in various forms, accounts, registers and passbooks. They also have to do such other clerical work as the Bank may direct. They are, therefore, accountable to the Bank and under the control of the Bank.”

The Apex Court holds that the commission earned by deposit collectors/pigmy agents partakes the character of ‘wages’ under Section 2(rr) of the Industrial Disputes Act, 1947. More importantly, such collectors were held to be workmen being subject to the pervasive control and supervision of the Bank. The relationship that thus emerges is not one of detached contractual engagement, but one imbued with the attributes of a master-servant nexus. The pigmy agents operate under the command, control and disciplinary framework of the Bank, their remuneration though termed as commission, is in substance, akin to wages, further evidenced by deduction of tax at source. The issue, therefore no longer remains res integra. It has travelled beyond the pale of controversy and stands settled as on date.

Applicability of GST to pigmy agents:

8. The next facet that requires consideration is, whether the services rendered by such employees – pigmy agents – can be subjected to GST. Section 7 of the CGST Act, read in conjunction with Section 7(2)(a) and schedule III forms statutory edifice governing the issue in the lis. It reads as follows:

“7. Scope of supply.—(1) For the purposes of this Act, the expression “supply” includes—

(a) all forms of supply of goods or services or both such as sale, transfer, barter, exchange, licence, rental, lease or disposal made or agreed to be made for a consideration by a person in the course or furtherance of business;

[(aa) the activities or transactions, by a person, other than an individual, to its members or constituents or vice-versa , for cash, deferred payment or other valuable consideration.

Explanation . — For the purposes of this clause, it is hereby clarified that, notwithstanding anything contained in any other law for the time being in force or any judgment, decree or order of any Court, tribunal or authority, the person and its members or constituents shall be deemed to be two separate persons and the supply of activities or transactions inter se shall be deemed to take place from one such person to another;]

(b) import of services for a consideration whether or not in the course or furtherance of business; [and]

(c) the activities specified in Schedule I, made or agreed to be made without a consideration; [* * *]

[* * *]

[(1-A) where certain activities or transactions constitute a supply in accordance with the provisions of sub-section (1), they shall be treated either as supply of goods or supply of services as referred to in Schedule II.]

(2) Notwithstanding anything contained in sub-section (1),—

(a) activities or transactions specified in Schedule III; or

(b) such activities or transactions undertaken by the Central Government, a State Government or any local authority in which they are engaged as public authorities, as may be notified by the Government on the recommendations of the Council,

shall be treated neither as a supply of goods nor a supply of services.

(3) Subject to the provisions of —[sub-sections (1), (1-A) and (2)], the Government may, on the recommendations of the Council, specify, by notification, the transactions that are to be treated as—

(a) a supply of goods and not as a supply of services; or

(b) a supply of services and not as a supply of goods.

Section 7(2)(a) supra mandates that service by an employee to the employer in the course of or in relation to his employment cannot be charged under the GST. Schedule III mandates so. Schedule-III reads as follows:

“SCHEDULE III

[See Section 7]

ACTIVITIES OR TRANSACTIONS WHICH SHALL BE TREATED NEITHER AS A SUPPLY OF GOODS NOR A SUPPLY OF SERVICES

| 1. |

|

Services by an employee to the employer in the course of or in relation to his employment. |

| 2. |

|

Services by any court or Tribunal established under any law for the time being in force. |

| 3. |

|

(a) the functions performed by the Members of Parliament, Members of State Legislature, Members of Panchayats, Members of Municipalities and Members of other local authorities; |

| (b) |

|

the duties performed by any person who holds any post in pursuance of the provisions of the Constitution in that capacity; or |

| (c) |

|

the duties performed by any person as a Chairperson or a Member or a Director in a body established by the Central Government or a State Government or local authority and who is not deemed as an employee before the commencement of this clause. |

| 4. |

|

Services of funeral, burial, crematorium or mortuary including transportation of the deceased. |

| 5. |

|

Sale of land and, subject to clause (b) of paragraph 5 of Schedule II, sale of building. |

| 6. |

|

Actionable claims, other than [specified actionable claims]. |

| 7. |

|

Supply of goods from a place in the non-taxable territory to another place in the non-taxable territory without such goods entering into India. |

The legislative intent, in terms of sub-clause (1) of Schedule-III clearly holds that the services rendered by an employee to the employer in the course of, or in relation to, his employment are placed outside the ambit of ‘supply’ and, therefore, exempt from GST. Schedule III in unambiguous terms, renders this exemption. Although the GST enactments do not define the expressions employer and employee, their contours have been sculpted through judicial pronouncements. It becomes necessary therefore to draw upon the jurisprudence that is replete, as laid down by the Apex Court. The nature of duties performed by pigmy agents, as evidenced through the terms of their engagement unmistakably reflects employer-employee relationship.

9. In the case at hand, the petitioner/Bank exercises complete control over the agents as per the terms and conditions laid down in the agreements of their employment. Memorandum of agreement is appended to the petition. Certain clauses of the said agreement are necessary to be noticed. One Kiran Toggi is appointed as a pigmy agent and certain clauses of the memorandum of agreement read as follows:

“1. The Agent shall on behalf of the Bank receive the collections from the customers of the Bank at branch office and / or at any other of their branch or branch offices regularly in terms of the rules of business relating to the Vikas Nirantara Daily Deposits scheme 2009 and enter the said collections Daily in the machines. The Vikas Nirantara Daily Deposit accounts shall be opened by the customer in the manner prescribed.

2. The Agent shall render a true and correct account in the prescribed manner of the Vikas Nirantara Daily Deposits collected by him to the Bank’s branch at Head Office and/or at any other of their branch or branch offices as required by the Bank.

…. …. ….

5. *The Agent has deposited a sum of Rs.20000/- as Vikas Nirantara Deposit Agents Security deposit for faithful and sincere discharge of his duties.

OR

*The agent has offered a surety for Rs.40000/- to the Bank in lieu of the security deposit of Rs.20000/- and the agent further agrees that the surety will be discharged/released by the Bank only after the agent build up cash security deposit of Rs.20000/-. 1

The agent binds himself to deposit every month, a sum equivalent to 10% of the fall back wages and incentive remuneration payable by the Bank to him as incentive rentmeration for Vikas Nirantara Deposit Collections towards his security deposit to be maintained separately and further agrees to furnish such other or more security as may be desired by the Bank from time to time. The agent hereby agrees that the Bank shall hold the said amounts so long as the Agent continues as Vikas Nirantara Deposit Agent and so long as the Bank desires or so long as any claim against the Agent with regard to any money or securities or other valuables of any description entrusted to the Agent or Agent’s care including the cost of machine is pending and so long as there is any dispute between the Agent and Bank with respect to any loss or damage that the Bank may or might have suffered, is pending. If at any time any liability is incurred by the Bank in respect of any loss or damage or other injury sustained, incurred for whatsoever reason or occasioned by dishonesty or fraud or cheating or any act of commission or omission or negligence in relation to the duties as Vikas Nirantara Deposit Agent, the Bank shall be at liberty to adjust and appropriate in part or full, the amount either of the security deposit or any other moneys available to the credit of the agent with it, now or hereafter without any reference to the agent in this behalf.

*Select whichever is applicable.

The right of the Bank over these securities shall be absolute and the Agent may be entitled to the refund of the same only upon his full acquiescence by the Bank.

The bank will pay interest to this deposit at the highest rate applicable to term deposits of public, prevailing at the relevant time. The deposit rates are subject to change from time to time.

6. (A) The Agent has agreed to be a Vikas Nirantara Deposit

Agent on the commission at rates determined by the Bank, and as laid down by the final Award of the industrial Tribunal, Hyderabad in ID 14/1980 dated 22.12.1988 as modified by the Judgment dated 28.3.1997 of the High Court of Andhra Pradesh in WP, No.9793 of 1989 and affirmed by the Judgment dated 13.2.2001 of the Supreme Court of India in Civil Appeal No. 3355 of 1998.

(B) The agent is entitled to the following as per the said Final Award:

(i) Fall back wages of Rs.750/- per month linked with minimum collection of Rs.7500/- per month and incentive remuneration at 2% for collection of amounts over and above Rs.7500/- per month.

(ii) Uniform conveyance allowance of Rs.50/- per month for deposits of less than Rs. 10000/- per month and Rs.100/- per month for deposits of more than Rs. 10000/- per month.

(iii) Gratuity of 15 days commission for each year of agency.

PAYMENT OF GRATUITY IS AS A PART OF THE AWARD GRANTED BY THE INDUSTRIAL TRIBUNAL, HYDERABAD IN ID 14/1980 DATED 22.12.1988 AND NOT UNDER THE PAYMENT OF GRATUITY ACT 1972.

Notwithstanding this,

(i) In case his agency is terminated for any act of willful omission or negligence causing any damage or loss or destruction of property belonging to the Bank, gratuity shall be forfeited to the extent of the damage or loss caused;

(ii) No Gratuity is payable in case Agency has been terminated for

(a) Commission of fraud/misappropriation.

(b) Riotous or disorderly conduct or any other act of violence on his part.

(c) Conviction in a criminal case involving moral turpitude,

(d) Abandoning the Agency or noncollection for thirty days without intimation.

C) The agent is not entitled to the following:

(i) Weekly holidays, annual leave etc.

(ii) Bonus, pension and provident fund

(iii) Medical and hospitalization charges and risk insurance as Agent is not a regular employee.

(iv) Any other allowance or claim or other benefits available and applicable to regular employees of the Bank whatsoever that are beyond the terms of the final Award mentioned above.

D) The Agent has agreed to discharge functions as Agent honestly, sincerely and dili-gently and he has agreed to obey and carry out the orders and instructions of the Manager or any other person placed in charge of the Bank at the above said Branch and/or at any other of their branch.

7. The Agent hereby agrees to give a month’s notice in writing before renouncing his agency to the Branch of the Bank. He also agrees to keep the Bank informed in writing, of his inability to make collections of deposits on any day or days. On getting such information the Bank is at liberty to make alternate arrangements for the collections of Vikas Nirantara deposit in respect of the cards dealt with by the Agent, during the period of his inability to collect the same, without reference to him. When such other Stationery as desired by the Bank to such person appointed by the Bank and from him he shall obtain the cards back after he is able to make the collections. It is made clear that the Agent is not entitled to for any fall back wages / commission for the amounts not collected by him and the agent should not entrust the work of collection to any other agent of this or any other branch of the Bank or to any other unauthorized person on his own. The agent shall have no right whatsoever to appoint a Sub-Agent. He shall deposit the Machine at the branch on the days he is not able to collect contributions towards Vikas Nirantara deposit scheme for whatsoever reason.”

The agreement governing the engagement of these pigmy agents reveal several telling features: The bank exercises pervasive control over their functioning; the agents are required to maintain security deposits; they are assured minimum remuneration; they are entitled to benefits such as, gratuity; and their disengagement is regulated by notice requirements. These are not indicia of an independent contractor, but hallmarks of employment.

10.1. The aforesaid kind of characteristics, whether could become an employer-employee relationship, is considered by the Apex Court in Dharangadhara Chemical Works Ltd. v. State of Saurashtra 1956 SCC OnLine SC 11 wherein it is held as follows:

“…. …. ….

13. The position in law is thus summarised in Halsbury’s Laws of England, Hailsham Edn., Vol. 22, p. 112, para 191:

“Whether or not, in any given case, the relation of master and servant, exists is a question of fact; but in all cases the relation imports the existence of power in the employer not only to direct what work the servant is to do, but also the manner in which the work is to be done.”;

and until the position is restated as contemplated in Short v. J.W. Henderson Ltd. [Short v. J.W. Henderson Ltd., (1946) 62 TLR 427 at p. 429 (HL)] we may take it as the prima facie test for determining the relationship between master and servant.

14. The principle which emerges from these authorities is that the prima facie test for the determination of the relationship between master and servant is the existence of the right in the master to supervise and control the work done by the servant not only in the matter of directing what work the servant is to do but also the manner in which he shall do his work, or to borrow the words of Lord Uthwatt at AC p. 23 in Mersey Docks & Harbour Board v. Coggins & Griffith (Liverpool) Ltd. [Mersey Docks & Harbour Board v. Coggins & Griffith (Liverpool) Ltd. , 1947 AC 1 at p. 23 (HL)] :

“. The proper test is whether or not the hirer had authority to control the manner of execution of the act in question.”

10.2. The Apex Court later in Hussainbhai v. Alath Factory Tozhilali Union (SC)/(1978) 4 SCC 257 has held as follows:

“…. …. ….

5. The true test may, with brevity, be indicated once again. Where a worker or group of workers labours to produce goods or services and these goods or services are for the business of another, that other is, in fact, the employer. He has economic control over the workers’ subsistence, skill, and continued employment. If he, for any reason, chokes off, the worker is, virtually, laid off. The presence of intermediate contractors with whom alone the workers have immediate or direct relationship ex contractu is of no consequence when, on lifting the veil or looking at the conspectus of factors governing employment, we discern the naked truth, though draped in different perfect paper arrangement, that the real employer is the Management, not the immediate contractor. Myriad devices, half-hidden in fold after fold of legal form depending on the degree of concealment needed, the type of industry, the local conditions and the like may be resorted to when labour legislation casts welfare obligations on the real employer, based on Articles 38, 39, 42, 43 and 43-A of the Constitution. The court must be astute to avoid the mischief and achieve the purpose of the law and not be misled by the maya of legal appearances.”

10.3. The Apex Court, in Sushilaben Indravadan Gandhi v. New India Assurance Company Ltd. (2021) 7 SCC 151 holds as follows:

“…. …. ….

32. A conspectus of all the aforesaid judgments would show that in a society which has moved away from being a simple agrarian society to a complex modern society in the computer age, the earlier simple test of control, whether or not actually exercised, has now yielded more complex tests in order to decide complex matters which would have factors both for and against the contract being a contract of service as against a contract for service. The early “control of the employer” test in the sense of controlling not just the work that is given but the manner in which it is to be done obviously breaks down when it comes to professionals who may be employed. A variety of cases come in between cases which are crystal clear — for example, a master in a school who is employed like other employees of the school and who gives music lessons as part of his employment, as against an independent professional piano player who gives music lessons to persons who visit her premises. Equally, a variety of cases arise between a ship’s master, a chauffeur and a staff reporter, as against a ship’s pilot, a taxi driver and a contributor to a newspaper, in order to determine whether the person employed could be said to be an employee or an independent professional. The control test, after moving away from actual control of when and how work is to be performed to the right to exercise control, is one in a series of factors which may lead to an answer on the facts of a case slotting such case either as a contract of service or a contract for service. The test as to whether the person employed is integrated into the employer’s business or is a mere accessory thereof is another important test in order to determine on which side of the line the contract falls. The three-tier test laid down by some of the English judgments, namely, whether wage or other remuneration is paid by the employer; whether there is a sufficient degree of control by the employer and other factors would be a test elastic enough to apply to a large variety of cases. The test of who owns the assets with which the work is to be done and/or who ultimately makes a profit or a loss so that one may determine whether a business is being run for the employer or on one’s own account, is another important test when it comes to work to be performed by independent contractors as against piece-rated labourers. Also, the economic reality test laid down by the US decisions and the test of whether the employer has economic control over the workers’ subsistence, skill and continued employment can also be applied when it comes to whether a particular worker works for himself or for his employer. The test laid down by the Privy Council in Lee Ting Sang v. Chung Chi-keung [Lee Ting Sang v. Chung Chi-keung, (1990) 2 AC 374 (PC)] , namely, is the person who has engaged himself to perform services performing them as a person in business on his own account, is also an important test, this time from the point of view of the person employed, in order to arrive at the correct solution. No one test of universal application can ever yield the correct result. It is a conglomerate of all applicable tests taken on the totality of the fact situation in a given case that would ultimately yield, particularly in a complex hybrid situation, whether the contract to be construed is a contract of service or a contract for service. Depending on the fact situation of each case, all the aforesaid factors would not necessarily be relevant, or, if relevant, be given the same weight. Ultimately, the Court can only perform a balancing act weighing all relevant factors which point in one direction as against those which point in the opposite direction to arrive at the correct conclusion on the facts of each case.

(Emphasis supplied at each instance)

The Apex Court, in DHARANGADHARA supra has held that the degree of control exercised by the employer over the manner in which the work is performed is a decisive test of employment. The principle was further elaborated in HUSSAINBHAI where the Apex Court emphasizes the real test lies whether the worker is engaged in the business of another and is economically dependant upon that enterprise. The Apex Court later in SUSHILABEN supra reiterates that the determinative factor remains the degree of control exercised by the employer.

11. The jurisprudential thread, running through these decisions, is clear – the essence of relationship is control, supervision and economic dependence. When these elements coalesce, the relationship assumes the character of employment. Once this conclusion is reached, the inevitable corollary follows, services rendered by such agents falls squarely within the exemption carved out under Sl.No.1 of Schedule III to the Act. Such services, being in the course of employment, are insulated from levy of GST.

12. The State, however, seeks to cloak these pigmy agents under a different nomenclature, describing them as “business facilitators” and places reliance upon a notification dated 28-06-2017 issued under Section 11 of the CGST Act. The contention though ingeniously projected falters upon closer scrutiny. It, therefore, becomes necessary to refer to the notification issued by the Government of India. Clause 2 of Notification defines a business facilitator. Clause 2(o) reads as follows:

“2. Definitions.-

Xxxx xxxx xxxx

(o) “business facilitator or business correspondent” means intermediary appointed under the business facilitator model or the business correspondent model by a banking company or an insurance company under the guidelines issued by the Reserve Bank of India;”

The definition of a business facilitator, as contained in the afore-quoted clause, contemplates an intermediary appointed under the models recognized and regulated by the Reserved Bank of India. Such facilitators are expected to perform specified functions, within the defined regulatory architecture.

13. What is a business facilitator model or a business correspondent model bears definition in a subsequent official memorandum. The business facilitator model and business correspondent model read as follows:

“2. Business Facilitator Model: Eligible Entities and Scope of Activities

2.1 Under the “Business Facilitator” model, banks may use intermediaries, such as, NGOs/Farmers’ Clubs, cooperatives, community based organisations, IT enabled rural outlets of corperate entities, Post Offices, insurance agents, well functioning Panchayats, Village Knowledge Centres, Agri Clinics/ Agri Business Centers, Krishi Vigyan Kendras and KVIC/ KVIB units, depending on the comfort level of the bank, for providing facilitation services. Such services may include (i) identification of borrowers and fitment of activities; (ii) collection and preliminary processing of loan applications including verification of primary information/data; (iii) creating awareness about savings and other products and education and advice on managing money and debt counselling; (iv) processing and submission of applications to banks; (v) promotion and nurturing Self Help Groups/ Joint Liability Groups; (vi) postsanction monitoring; (vii) monitoring and handholding of Self Help Groups/ Joint Liability Groups/ Credit Groups/ others; and (vii) follow-up for recovery.

2.2 As these services are not intended to involve the conduct of banking business by Business Facilitators, no approval is required from RBI for using the above intermediaries for facilitation of the services indicated above.

3. Business Correspondent Model: Eligible Entities and Scope of Activities

3.1 Under the “Business Correspondent” Model, NGOs/ MFIs set up under Societies/ Trust Acts, Societies registered under Mutually Aided Cooperative Societies Acts or the Cooperative Societies Acts of States, section 25 companies, registered NBFCs not accepting public deposits and Post Offices may act as Business Correspondents. Banks may conduct thorough due diligence on such entities keeping in view the indicative parameters given in Annex 3.2 of the Report of the Internal Group appointed by Reserve Bank of India (available on RBI website: www.rbi.org.in) to examine issues relating to Rural Credit and Micro-Finance (July 2005). In engaging such intermediaries as Business Correspondents, banks should ensure that they are well established, enjoying good reputation and having the confidence of the local people. Banks may give wide publicity in the locality about the intermediary engaged by them as Business Correspondent and take measures to avoid being misrepresented.

The pigmy agents, in the present case, do not answer to the afore-quoted description. They are not intermediaries appointed under the Reserve Bank of India – sanctioned model. Their role is confined to collection of deposits under the Bank’s pigmy deposit scheme and they do not undertake activities envisaged under the business facilitator or correspondent models. The attempt to artificially transpose pigmy agents into the category of business facilitators is, therefore, fundamentally flawed. It is a mischaracterization, that cannot withstand judicial scrutiny.

14. In the teeth of the aforesaid narration, it becomes necessary to notice one of the show cause notices issued by the 1st respondent. The reason behind issue of show cause notice dated 27-12-2023 is as follows:

“…. …. ….

| A. |

|

The Tax payer submitted that; the definition of Business Facilitator (BF) in GST Act is borrowed from the RBI Circular No. 58/22-01-001/2005-06 Dated: 25-01-2006. As per the RBI Circular, mentioned above in Para 2. Business Facilitator Model: Eligible entities and Scope of activities: |

2.1 Under the Business Facilitator model, banks may use intermediaries, such as, NGOs/Farmers’ clubs, Cooperatives, community based organizations, IT enabled rural outlets of cooperate entities, Post officer, insurance agents, well-functioning Panchayats, Village knowledge Centers, Agri Clinics/ Agri Business Centers, Krishi Vigyan Kendra sans KVIC/KVIB units, depending on the comport level of the bank, for proving facilitation services, Such services may include (i) identification of barrows and fitment of activities; (ii) collection and preliminary processing of loan application including verification of primary information/data/; (iii) creating awareness about savings and other products and education and advice on managing money and debt counselling; (iv) post-sanction monitoring; (vii) monitoring and handholding of self-help Groups/ Joint liability Groups/Credit Groups/ others; and (viii) follow up recovery.

2.2 As these services are not intended to involve the conduct of banking business by Business Facilitators, no approval is required from RBI for using the above intermediaries for facilitation of the services indicated above,

From plane reading of above RBI’s guidelines, it is noticed that, under” BF model” the bank may use intermediaries, such as, NGOs/ Farmers clubs, Cooperatives, community-based organizations, IT enabled rural outlets of cooperate entities, Post officer, insurance agents, well-functioning Panchayats etc., there is no restrictions from RBI that banks must use the above persons/entities only as intermediaries, here the RBI in its circular used a non-restrictive clause (may and such as). Further, the RBI has said that depending on the comfort level of the bank, they may use any other individual (including pigmy agents) or groups for providing finanacial facilitation services i.e., creating awareness about savings and other products including pigmy deposit accounts.

Further, in terms of business, business facilitation is the combination of arrangements that ease the doing of business. The people or the organizations which provide such facilities to the businesses are known as ‘Business Facilitators’. The pigmy agents are nothing but “Business Facilitators” for bank. Because they help the bank to ease the doing of business by making the arrangements in daily deposit collection from doorstep of customers. By doing so they are helping the bank to increase its CASA ratio.

Further, the contention of the taxpayer regarding “pigmy agents” is workmen are acceptable term within the meaning of the term as defined in the Industrial Dispute Act. But as per the provisions of the GST Act-2017, the terms like “Agent” (U/s.2(5)), “Business” (2(17)(a)(b)) “Person”(2(84)), “Principal” (2(88)),

“Recipient” (2(93)), “Intermediaries”(2(13) of IGSt) “Reverse charge”(2(98)), “Services”(2(102)), “Supplier” (2(105)) and “Consideration” (2(31)) are all well-defined Under KGST/CGST/IGST Act-2017. The definitions of Agent and Principal are reproduced for reference as under:

S.2 (5) “agent” means a person, including a factor, broker, commission agent, arhatia, del credere agent, an auctioneer or any other mercantile agent, by whatever name called, who carries on the business of supply or receipt of goods or services or both on behalf of another, S. 2(88) “principal” means a person on whose behalf an agent carries on the business of supply or receipt of goods or services or both;

The person for whom such act is done, or who is so represented, is called the “principal”. As delineated in the definition, an agent can be appointed for performing any act on behalf of the principal which may or may not have the potential for representation on behalf of the principal. So, the crucial element here is the representative character of the agent which enables him to carry out activities on behalf of the principal.

3. The following two key elements emerge from the above definition of agent: Circular No. 57/31/2018-GST

(a) the term “agent” is defined in terms of the various activities being carried out by the person concerned in the principal-agent relationship; and

(b) the supply or receipt of goods or services has to be undertaken by the agent on behalf of the principal.

Therefore, as per the provisions of the GST Act, the service rendered by the pigmy agents to bank is taxable service, it is clearly Principal-Agent relationship and the same falls under “business facilitator model” and by virtue of notification no 13/2017-central tax (rate) & notification no 29/2018-central tax (rate) dated:31-12-2018, the GST payable on the said taxable services of pigmy agents as business facilitator shall be paid on reverse charge basis by the recipients of such services w.e.f., 01-01-2019.

| B. |

|

The Tax payer accepted that, commission has been paid to the Pigmy agents for the service they rendered to the bank based on the deposits collected (in Para-03 Page-10). Further, the payment of minimum wages, conveyance and gratuity is in accordance with the Judgment of Hon’ble Supreme Court of India in Indian Banks Association v. Workmen of Syndicate Bank and Ors on 13-Feb-2001. However, it is to be noted here that, the Tax payer though in their reply submitted that, they have deducted TDS on payment made to Pigmy Agents as per the provisions of Income Tax Act. But the Tax payer not submitted any such documents to substantiate their submission. In the absence of classified turnover of commission, the entire amount paid to pigmy agents are considered as commission and the taxpayer is liable to pay tax @18% U/s.9(3) of the Act as RCM basis on the entire amount paid as commission to pigmy agents. |

| C. |

|

Pigmy agents were appointed to collect small deposits (pigmy deposits) from the customers of the bank. The terms of the agreement made with such Pigmy agents as far as wages, incentive remuneration, conveyance allowance are all related to collection of small deposits. The Tax payer utilising the services of Business Facilitators/ Business Correspondents for loan disbursement, loan recovery and other activities. For such services the Tax payer is charged with GST by such Business Facilitators. It is further to be noted that, in Annual Audit Report for the year 2018-19 in Para (7) under Recovery of Loan Head, the Tax payer declared that, they have formulated a special scheme for recovery of bad debts, written off accounts through Business Correspondents and Nirantara (Pigmy) Deposit agents and Ex-staff. The scheme is effective from 25.08.2014. Under this scheme, the BCs and Pigmy agents are eligible for commission of 10% on actual recoveries. |

From the above it is induced that, apart from paying wages, remuneration, conveyance to such Pigmy agents for collection of small deposits they are also paying them commission at 10% on recovery of bad debts. The Tax payer is utilising the services of the Pigmy agents on par with Business Correspondents/ Facilitators. Therefore, the Tax payer is liable for payment under the provisions of GST Act in case of Pigmy agents also, as the Pigmy agents are providing their services on par with Business Facilitators apart from terms of agreement made with the Tax payer.

In view of the above discussions, you are hereby given an opportunity to show cause as to why you should not pay the amount of Tax specified as below along with applicable interest thereon till the date of payment of tax U/s 50 within 7 days from the receipt of this notice. Failing to comply with this Show cause Notice, action as deemed fit under the provisions of KGST/CGST Act, 2017 will be initiated.

Further, it is to be noted that, if you fail to pay the amount as ascertained by the undersigned within 30 days of issue of Show Cause Notice, you will be liable for Penalty U/s 122 of the Act.

(Emphasis added)

The show cause notices issued by the respondent proceed on an erroneous premise, making an attempt to describe the Pigmy agents as business facilitators. The foundation of the show cause notice, in the light of the aforesaid narration, is itself infirm, the superstructure in the form of the show cause notice, built upon it, would tumble down. Pigmy agents employed by the petitioner, in the light of the aforesaid reasons, can never be treated as business facilitators for them to be coming under the GST and the services rendered by these pigmy agents are in the course of their employment with the Bank as pigmy agents, which is clearly exempt from levy of GST in terms of Sl.No.1 of Schedule III quoted supra.

15. In the teeth of this fundamental flaw, forming the fulcrum of the show cause notices, they are rendered devoid of jurisdiction and are to be obliterated. Certain other prayers are also sought with regard to extension of time by issuance of a notification and contending that those notifications are ultra vires the Act and need not be considered, as the taxation regime i.e., CGST and KGST itself is not applicable to the petitioner qua pigmy agents. Therefore, those prayers need not bear consideration. It is at best left to be decided in an appropriate case. Therefore, the impugned show cause notices which form the prayers in (A) to (D) are to be granted and (E) and (F) are to be abandoned for the time being to be decided in an appropriate case.

16. For the aforesaid reasons, the following: –

ORDER

| (i) |

|

Writ Petition is allowed. |

| (ii) |

|

Impugned show cause notices in (i) No. DCCT (Enf-2)/HBL/SCN-03/2023-24 dated 27-12-2023 issued by the 1st respondent; (ii) No. ACCT/Audit-1/HBL/GST/ DRC-1/23-24/B-337 dated 28-12-2023 along with Form DRC-01 issued by respondent No.2; (iii) No. ACCT/Audit-1/HBL/GST/DRC-1/23-24/B-338 dated 2812-2023 along with Form DRC-01 issued by respondent No.2; and (iv) No.ACCT/Audit-1/HBL/GST/ DRC-1/23-24/B-339 dated 28-12-2023 along with Form DRC-01 issued by respondent No.2 stand obliterated. |

| (iii) |

|

The petitioner is entitled to all consequential benefits that would flow from quashment of afore-mentioned show cause notices. |

Consequently, I.A.No.1 of 2025 also stands disposed.