IGST Act 2017

Integrated Goods and Services Tax Act

1. The introduction of Goods and Services Tax (GST) is a significant reform in the field of indirect taxes in our country. Multiple taxes levied and collected by the Centre and the States will be replaced by one tax called the Goods and Services Tax (GST). GST is a multi-stage value added tax levied on the consumption of goods or services or both.

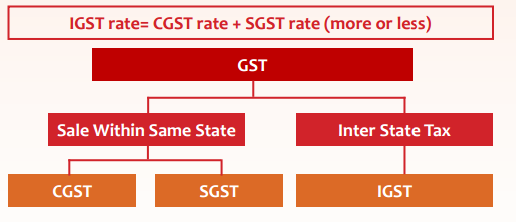

2. A “Dual GST” model has been adopted in view of the federal structure of our country. Centre and States will simultaneously levy GST on every supply of goods or services or both which, takes place within a State or Union Territory. Thus, there shall be two components of GST:

(Levied & collected under the authority of CGST Act, 2017 passed by the Parliament)

(ii) State tax (SGST)

(Levied & collected under the authority of SGST Act, 2017 passed by

respective State)

3. Why a third tax in the name of IGST ?

Before discussing the IGST Model and its features, it is important to understand how inter-State trade or commerce is being regulated in the present indirect tax system. It is significant to note that presently the Central Sales Tax Act, 1956 regulates the inter-State trade or commerce (hereinafter referred to as “CST”), the authority for

which is constitutionally derived from Article 269 of the Constitution. Further, as per article 286 of the Constitution of India, no State can levy sales tax on any sales or purchase of goods that takes place outside the State or in the course of the import of the goods into, or export of the goods out of the territory of India. Only the Parliament can levy tax on such a transaction. The Central Sales Tax Act was

enacted in 1956 to formulate principles for determining when a sale or purchase of goods takes place in the course of inter-State trade or commerce. The Act also provides for the levy and collection of taxes on sales of goods in the course of inter-State trade.

4. The CST suffers from the following shortcomings

(i) CST is collected and retained by the origin State, which is an aberration. Any indirect tax, by definition, is a consumption tax, the incidence of which, is borne by the consumer. Logically, the tax must accrue to the destination State having jurisdiction over the consumer.

(ii) Input Tax Credit (hereinafter referred to as ITC) of CST is not allowed to the buyer which, results in cascading of tax (tax on tax) in the supply chain.

(iii) Various accounting forms are required to be filed in CST viz., C Form, E1, E2, F, I, J Forms etc. which add to the compliance cost of the business and impedes the free flow of trade.

(iv) Another negative feature of CST is the opportunity for “arbitrage” because of the huge difference between tax rates under VAT and CST being levied on intra-State sales and interState sales respectively.

5. The IGST model would remove all these deficiencies.

IGST is a mechanism to monitor the inter-State trade of goods and services

and ensure that the SGST component accrues to the consumer State.

It would maintain the integrity of ITC chain in inter-State supplies. The IGST rate would broadly be equal to CGST rate plus SGST rate. IGST would be levied by the Central Government on all inter-State transactions of taxable goods or services.

6. Cross-utilisation of credit

It requires the transfer of funds between respective accounts. The utilisation of credit of CGST & SGST for payment of IGST by “B” would require the transfer of funds to IGST accounts. Similarly, the utilisation of IGST credit for payment of CGST & SGST by “C” would necessitate the transfer of funds from IGST account. As a result, CGST account and SGST (of, say, Rajasthan) would have Rs. 1300/- each, whereas, there will not be any amount left in IGST and SGST (of, say, Maharashtra) after the transfer of ITC.

7. Prescribed order of utilisation of IGST /CGST / SGST credit

The IGST payment can be done by utilising the ITC. The amount of ITC on account of IGST is allowed to be utilised towards the payment of IGST, CGST and SGST, in that order.

8. Nature of Supply

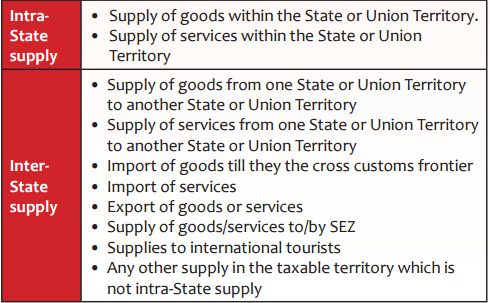

It is very important to determine the nature of supply – whether it is inter-State or intra-State, as the kind of tax to be paid (IGST or CGST+SGST) depends on that.

(i) Inter-State Supply:

Subject to the place of supply provisions, where the location of the supplier and the place of supply are in:

(a) Two different States;

(b) Two different Union territories; or

(c) A State and a Union Territory.

Such supplies shall be treated as the supply of goods or services in the course of inter-State trade or commerce.

Any supply of goods or services in the taxable territory, not being an intra-State supply, shall be deemed to be a supply of goods or services in the course of inter-State trade or commerce. Supplies to or by SEZs are defined as inter-State supply.

Further, the supply of goods imported into the territory of India till they cross the customs frontiers of India or the supply of services imported into the territory of India shall be treated as supplies in the course of inter-State trade or commerce. Also, the supplies to international tourists are to be treated as inter-State supplies.

(ii) Intra-State supply:

It has been defined as any supply where the location of the supplier and the place of supply are in the same State or Union Territory.

Thus, the nature of the supply depends on the location of the supplier and the place of supply. Both these terms have been defined in the IGST Act.

9. Location of Supplier

Broadly, it is the registered place of business or the fixed establishment of the supplier from where the supply is made. Sometimes, a service provider has to go to a client location for providing service. However, such place would not be considered as the location of the supplier. It has to be either a regular place of business or a fixed establishment, which is having sufficient degree of permanence and suitable structure in terms of human and technical resources.

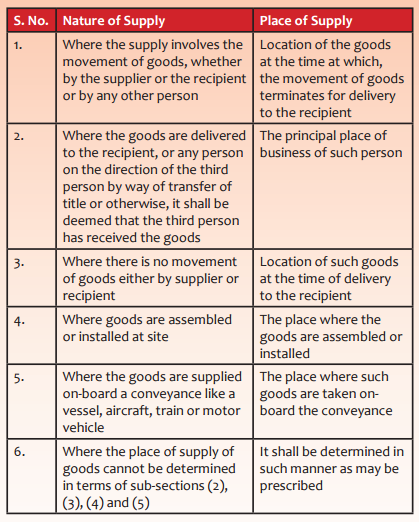

10. Place of supply

10.1 (i) Places of supply provisions have been framed for goods and services, keeping in mind the destination/consumption principle. In other words, the place of supply is based on the place of consumption of goods or services. As goods are tangible, the

determination of their place of supply, based on the consumption principle, is not difficult. Generally, the place of delivery of goods becomes the place of supply.

However, the services being intangible in nature, it is not easy to determine the exact place where services are acquired, enjoyed and consumed. In respect of certain categories of services, the place of supply is determined with reference to a

proxy.

[ Read Analysis of Place of Supply in GST (India ) with Examples ]

10.2 (ii) A distinction has been made between B2B (Business to Business) & B2C (Business to Consumer) transactions, as B2B transactions are wash transactions since the ITC is availed by the registered person (recipient) and no real revenue accrues to the Government.

10.3 (iii) Separate provisions for the supply of goods and services have been made for the determination of their place of supply. Separate provisions for the determination of the place of supply in respect of domestic supplies and cross border supplies have been framed.

A. Place of supply of goods other than import and export [Section 10]

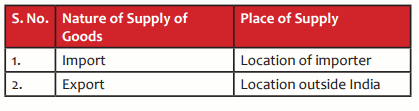

B. Place of supply of goods in case of Import & Export [Section 11]

C. Place of supply of services in case of Domestic Supplies [Section 12]

(Where the location of supplier of services and the location of the recipient of services is in India)

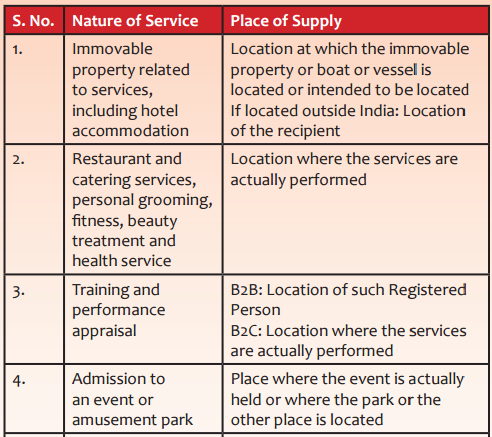

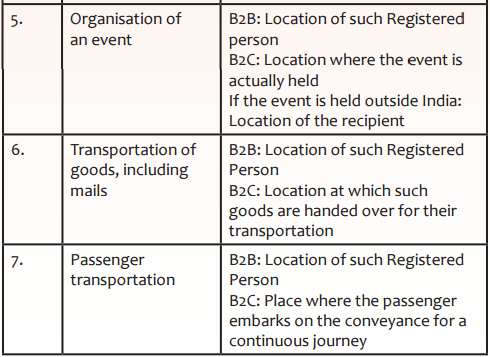

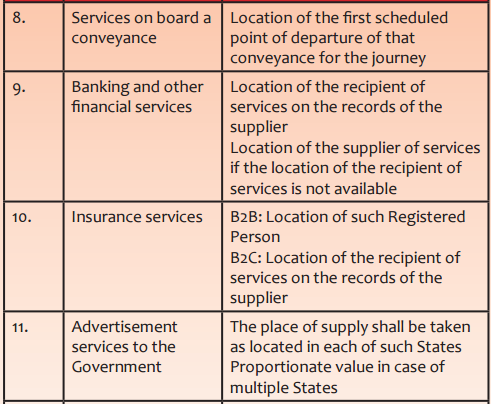

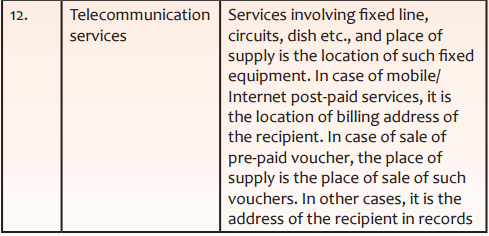

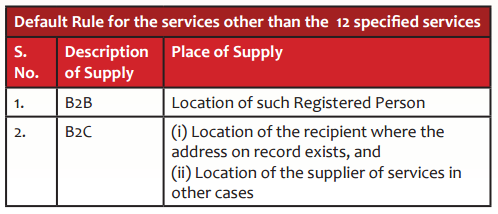

(i) In respect of the following 12 categories of services, the place of supply is determined with reference to a proxy. Rest of the services are governed by a default provision.

(ii) For the rest of the services other than those specified above, a default provision has been prescribed as under:

[ Note B2B means Business to Business , B2C means Businesss to Consumer ]

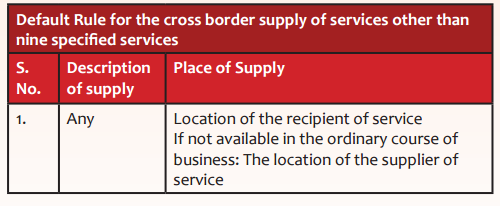

D. Place of supply of services in case of cross-border supplies:(Section 13 )

(Where the location of the supplier of services or the location of the recipient of services is outside India)

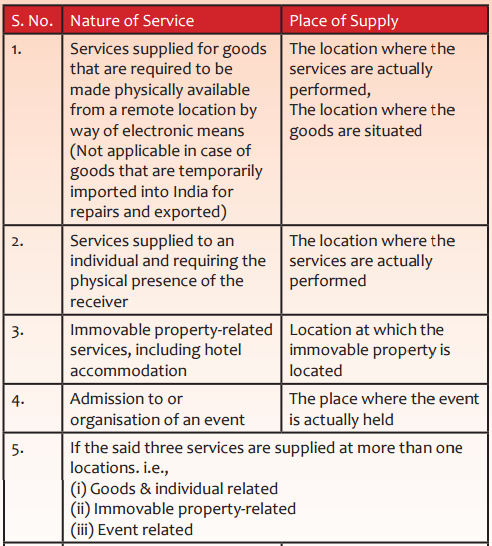

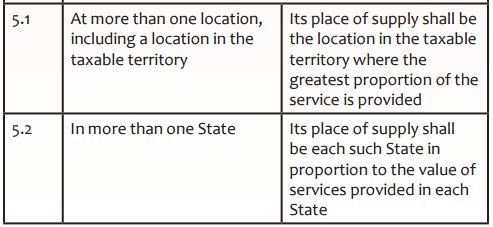

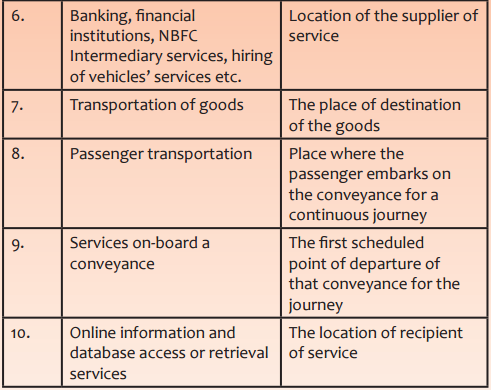

(i) In respect of the following categories of services, the place of supply is determined with reference to a proxy. Rest of the services are governed by a default provision.

(ii) For the rest of the services other than those specified above, a default provision has been prescribed as under:

11. Supplies in territorial waters

Where the location of the supplier is in the territorial waters, the location of such supplier, or where the place of supply is in the territorial waters, the place of supply is deemed to be in the coastal State or Union Territory where the nearest point of the appropriate baseline is located.

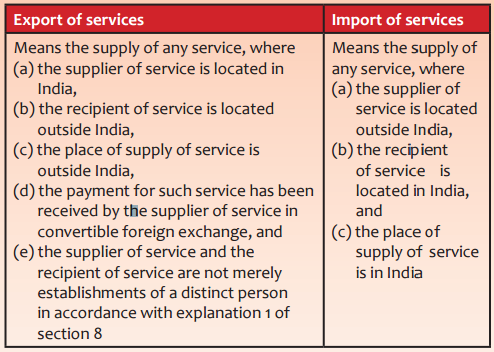

12. Export/Import of services

A supply would be treated as import or export, if certain conditions are satisfied.

These conditions are as under:

13. Zero rated supply

Exports and supplies to SEZs are considered as ‘zero rated supply’ on which no tax is payable. However, ITC is allowed, subject to such conditions, safeguards and procedure as may be prescribed, and refunds in respect of such supplies may be claimed by following either of these options:

(i) Supply made without the payment of IGST under Bond and claim refund of unutilied ITC or

(ii) Supply made on payment of IGST and claim refund of the same

14. Refund of integrated tax paid on supply of goods to tourist leaving India

Section 15 of the IGST Act provides for refund of IGST paid to an international tourist leaving India on goods being taken outside India, subject to such conditions and safeguards as may be prescribed. An international tourist has been defined as a non-resident of India who enters India for a stay of less than 6 months. IGST would be charged on such supplies as the same in the course of export.