Circular No 37/11/2018 GST

Clarifications on exports related refund issues .Circular No 37/11/2018 GST Dated the 15th March, 2018

F. No.349/47/2017-GST

Government of India

Ministry of Finance

Department of Revenue

Central Board of Excise and Customs

GST Policy Wing

New Delhi, Dated the 15th March, 2018

To,

The Principal Chief Commissioners/Chief Commissioners/Principal Commissioners/

Commissioners of Central Tax (All)

The Principal Directors General/ Directors General (All)

Madam/Sir,

Subject: Clarifications on exports related refund issues- regarding

Board vide Circular No. 17/17/2017 – GST dated 15th November 2017 and Circular No. 24/24/2017 – GST dated 21st December 2017 clarified various issues in relation to processing of claims for refund. Since then, several representations have been received seeking further clarifications on issues relating to refund. In order to clarify these issues and with a view to ensure uniformity in the implementation of the provisions of the law across field formations, the Board, in exercise of its powers conferred by section 168 (1) of the Central Goods and Services Tax Act, 2017 (CGST Act), hereby clarifies the issues raised as below:

2. Non-availment of drawback: The third proviso to sub-section (3) of section 54 of the CGST Act states that no refund of input tax credit shall be allowed in cases where the supplier of goods or services or both avails of drawback in respect of central tax.

2.1 This has been clarified in paragraph 8.0 of Circular No. 24/24/2017 – GST, dated 21st December 2017. In the said paragraph, reference to “section 54(3)(ii) of the CGST Act” is a typographical error and it should read as “section 54(3)(i) of the CGST Act”. It may be noted

that in the said circular reference has been made only to central tax, integrated tax, State /

Union territory tax and not to customs duty leviable under the Customs Act, 1962. Therefore,

a supplier availing of drawback only with respect to basic customs duty shall be eligible for refund of unutilized input tax credit of central tax / State tax / Union territory tax / integrated tax / compensation cess under the said provision. It is further clarified that refund of eligible credit on account of State tax shall be available even if the supplier of goods or services or both has availed of drawback in respect of central tax.

3. Amendment through Table 9 of GSTR-1: It has been reported that refund claims are not being processed on account of mis-matches between data contained in FORM GSTR-1, FORM GSTR-3B and shipping bills/bills of export. In this connection, it may be noted that the facility of filing of Table 9 in FORM GSTR-1, an amendment table which allows for amendments of invoices/ shipping bills details furnished in FORM GSTR-1 for earlier tax period, is already available. If a taxpayer has committed an error while entering the details of an invoice / shipping bill / bill of export in Table 6A or Table 6B of FORM GSTR-1, he can rectify the same in Table 9 of FORM GSTR-1.

3.1. It is advised that while processing refund claims on account of zero rated supplies, information contained in Table 9 of FORM GSTR-1 of the subsequent tax periods should be

taken into cognizance, wherever applicable.

3.2. Field formations are also advised to refer to Circular No. 26/26/2017 – GST dated 29th December, 2017, wherein the procedure for rectification of errors made while filing the returns in FORM GSTR-3B has been provided. Therefore, in case of discrepancies between the data furnished by the taxpayer in FORM GSTR-3B and FORM GSTR-1, the officer shall refer to the said Circular and process the refund application accordingly.

4. Exports without LUT: Export of goods or services can be made without payment of

integrated tax under the provisions of rule 96A of the Central Goods and Services Tax Rules 2017 (the CGST Rules), . Under the said provisions, an exporter is required to furnish a bond

or Letter of Undertaking (LUT) to the jurisdictional Commissioner before effecting zero rated

supplies. A detailed procedure for filing of LUT has already been specified vide Circular No. 8/8/2017 –GST dated 4th October, 2017. It has been brought to the notice of the Board that in

some cases, such zero rated supplies have been made before filing the LUT and refund claims

for unutilized input tax credit have been filed.

4.1. In this regard, it is emphasised that the substantive benefits of zero rating may not be

denied where it has been established that exports in terms of the relevant provisions have

been made. The delay in furnishing of LUT in such cases may be condoned and the facility

for export under LUT may be allowed on ex post facto basis taking into account the facts and

circumstances of each case.

5. Exports after specified period: Rule 96A (1) of the CGST Rules provides that any registered person may export goods or services without payment of integrated tax after furnishing a LUT / bond and that he would be liable to pay the tax due along with the interest as applicable within a period of fifteen days after the expiry of three months or such further period as may be allowed by the Commissioner from the date of issue of the invoice for export, if the goods are not exported out of India. The time period in case of services is fifteen days after the expiry of one year or such further period as may be allowed by the Commissioner from the date of issue of the invoice for export, if the payment of such services is not received by the exporter in convertible foreign exchange.

5.1 It has been reported that the exporters have been asked to pay integrated tax where the goods have been exported but not within three months from the date of the issue of the invoice for export. In this regard, it is emphasised that exports have been zero rated under the Integrated Goods and Services Tax Act, 2017 (IGST Act) and as long as goods have actually been exported even after a period of three months, payment of integrated tax first and claiming refund at a subsequent date should not be insisted upon. In such cases, the jurisdictional Commissioner may consider granting extension of time limit for export as provided in the said sub-rule on post facto basis keeping in view the facts and circumstances of each case. The same principle should be followed in case of export of services.

6. Deficiency memo: It may be noted that if the application for refund is complete in terms of sub-rule (2), (3) and (4) of rule 89 of the CGST Rules, an acknowledgement in FORM GST RFD-02 should be issued. Rule 90 (3) of the CGST Rules provides for communication in FORM GST RFD-03 (deficiency memo) where deficiencies are noticed. The said sub-rule also provides that once the deficiency memo has been issued, the claimant is required to file a fresh refund application after the rectification of the deficiencies.

6.1. In this connection, a clarification has been sought whether with respect to a refund claim, deficiency memo can be issued more than once. In this regard rule 90 of the CGST Rules may be referred to, wherein it has been clearly stated that once an applicant has been communicated the deficiencies in respect of a particular application, the applicant shall furnish a fresh refund application after rectification of such deficiencies. It is therefore, clarified that there can be only one deficiency memo for one refund application and once such a memo has been issued, the applicant is required to file a fresh refund application, manually in FORM GST RFD-01A. This fresh application would be accompanied with the original ARN, debit entry number generated originally and a hard copy of the refund application filed online earlier. It is further clarified that once an application has been submitted afresh, pursuant to a deficiency memo, the proper officer will not serve another

deficiency memo with respect to the application for the same period, unless the deficiencies pointed out in the original memo remain unrectified, either wholly or partly, or any other substantive deficiency is noticed subsequently.

7. Self-declaration for non-prosecution: It is learnt that some field formations are asking for a self-declaration with every refund claim to the effect that the claimant has not been prosecuted.

7.1. The facility of export under LUT is available to all exporters in terms of notification No. 37/2017- Central Tax dated 4th October, 2017, except to those who have been prosecuted for any offence under the CGST Act or the IGST Act or any of the existing laws in force in a case where the amount of tax evaded exceeds two hundred and fifty lakh rupees. Para 2(d) of the Circular No. 8/8/2017-GST dated 4th October, 2017, mentions that a person intending to export under LUT is required to give a self-declaration at the time of submission of LUT that he has not been prosecuted. Persons who are not eligible to export under LUT are required to export under bond.

7.2. It is clarified that this requirement is already satisfied in case of exports under LUT and asking for self–declaration with every refund claim where the exports have been made under LUT is not warranted.

8. Refund of transitional credit: Refund of unutilized input tax credit is allowed in two scenarios mentioned in sub-section (3) of section 54 of the CGST Act. These two scenarios

are zero rated supplies made without payment of tax and inverted tax structure. In sub-rule (4) and (5) of rule 89 of the CGST Rules, the amount of refund under these scenarios is to be calculated using the formulae given in the said sub-rules. The formulae use the phrase ‘Net ITC’ and defines the same as “input tax credit availed on inputs and input services during the relevant period other than the input tax credit availed for which refund is claimed under subrules (4A) or (4B) or both”. It is clarified that as the transitional credit pertains to duties and taxes paid under the existing laws viz., under Central Excise Act, 1944 and Chapter V of the Finance Act, 1994, the same cannot be said to have been availed during the relevant period and thus, cannot be treated as part of ‘Net ITC’.

9. Discrepancy between values of GST invoice and shipping bill/bill of export: It has been brought to the notice of the Board that in certain cases, where the refund of unutilized input tax credit on account of export of goods is claimed and the value declared in the tax invoice is different from the export value declared in the corresponding shipping bill under the Customs Act, refund claims are not being processed. The matter has been examined and it is clarified that the zero rated supply of goods is effected under the provisions of the GST laws. An exporter, at the time of supply of goods declares that the goods are for export and the same is done under an invoice issued under rule 46 of the CGST Rules. The value recorded in the GST invoice should normally be the transaction value as determined under section 15 of the CGST Act read with the rules made thereunder. The same transaction value should normally be recorded in the corresponding shipping bill / bill of export.

9.1 During the processing of the refund claim, the value of the goods declared in the GST invoice and the value in the corresponding shipping bill / bill of export should be examined and the lower of the two values should be sanctioned as refund.

10. Refund of taxes paid under existing laws: Sub-sections (3), (4) and (5) of section 142 of the CGST Act provide that refunds of tax/duty paid under the existing law shall be disposed of in accordance with the provisions of the existing law. It is observed that certain taxpayers have applied for such refund claims in FORM GST RFD-01A also. In this regard, the field formations are advised to reject such applications and pass a rejection order in FORM GST PMT-03 and communicate the same on the common portal in FORM GST RFD-01B. The procedures laid down under the existing laws viz., Central Excise Act, 1944 and Chapter V of the Finance Act, 1994 read with above referred sub-sections of section 142 of the CGST Act shall be followed while processing such refund claims.

10.1 Furthermore, it has been brought to the notice of the Board that the field formations are rejecting, withholding or re-crediting CENVAT credit, while processing claims of refund filed under the existing laws. In this regard, attention is invited to sub-section (3) of section 142 of the CGST Act which provides that the amount of refund arising out of such claims shall be refunded in cash. Further, the first proviso to the said sub-section provides that where any claim for refund of CENVAT credit is fully or partially rejected, the amount so rejected shall lapse and therefore, will not be transitioned into GST. Furthermore, it should be ensured that no refund of the amount of CENVAT credit is granted in case the said amount has been transitioned under GST. The field formations are advised to process such refund applications accordingly.

11. Filing frequency of Refunds: Various representations have been made to the Board regarding the period for which refund applications can be filed. Section 2(107) of the CGST Act defines the term “tax period” as the period for which the return is required to be furnished. The terms ‘Net ITC’ and ‘turnover of zero rated supply of goods/services’ are used in the context of the relevant period in rule 89(4) of CGST Rules. The phrase ‘relevant period’ has been defined in the said sub-rule as ‘the period for which the claim has been filed’.

11.1 In many scenarios, exports may not have been made in that period in which the inputs

or input services were received and input tax credit has been availed. Similarly, there may be

cases where exports may have been made in a period but no input tax credit has been availed in the said period. The above referred rule, taking into account such scenarios, defines relevant period in the context of the refund claim and does not link it to a tax period.

11.2 In this regard, it is hereby clarified that the exporter, at his option, may file refund

claim for one calendar month / quarter or by clubbing successive calendar months / quarters.

The calendar month(s) / quarter(s) for which refund claim has been filed, however, cannot

spread across different financial years.

12. BRC / FIRC for export of goods: It is clarified that the realization of convertible foreign exchange is one of the conditions for export of services. In case of export of goods, realization of consideration is not a pre-condition. In rule 89 (2) of the CGST Rules, a statement containing the number and date of invoices and the relevant Bank Realisation Certificates (BRC) or Foreign Inward Remittance Certificates (FIRC) is required in case of export of services whereas, in case of export of goods, a statement containing the number and date of shipping bills or bills of export and the number and the date of the relevant export invoices is required to be submitted along with the claim for refund. It is therefore clarified that insistence on proof of realization of export proceeds for processing of refund claims related to export of goods has not been envisaged in the law and should not be insisted upon.

13. Supplies to Merchant Exporters: Notification No. 40/2017 – Central Tax (Rate), dated 23rd October 2017 and notification No. 41/2017 – Integrated Tax (Rate) dated 23rd October 2017 provide for supplies for exports at a concessional rate of 0.05% and 0.1% respectively, subject to certain conditions specified in the said notifications.

13.1 It is clarified that the benefit of supplies at concessional rate is subject to certain conditions and the said benefit is optional. The option may or may not be availed by the supplier and / or the recipient and the goods may be procured at the normal applicable tax rate.

13.2 It is also clarified that the exporter will be eligible to take credit of the tax @ 0.05% / 0.1% paid by him. The supplier who supplies goods at the concessional rate is also eligible for refund on account of inverted tax structure as per the provisions of clause (ii) of the first proviso to sub-section (3) of section 54 of the CGST Act. It may also be noted that the exporter of such goods can export the goods only under LUT / bond and cannot export on payment of integrated tax. In this connection, notification No. 3/2018-Central Tax, dated 23.01.2018 may be referred.

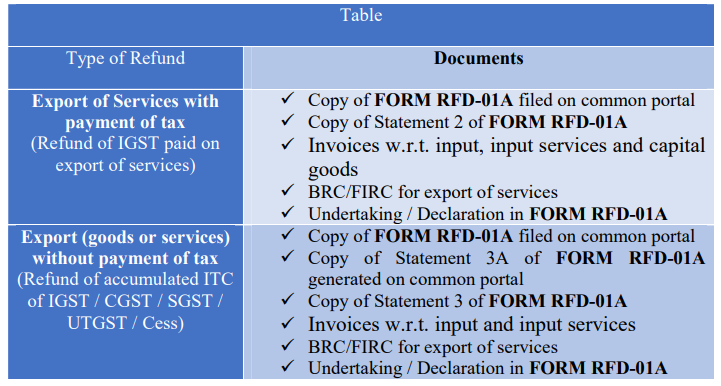

14. Requirement of invoices for processing of claims for refund: It has been brought to the notice of the Board that for processing of refund claims, copies of invoices and other additional information are being insisted upon by many field formations.

14.1 It was envisaged that only the specified statements would be required for processing of refund claims because the details of outward supplies and inward supplies would be available on the common portal which would be matched. Most of the other information like shipping bills details etc. would also be available because of the linkage of the common portal with the Customs system. However, because of delays in operationalizing the requisite modules on the common portal, in many cases, suppliers’ invoices on the basis of which the exporter is claiming refund may not be available on the system. For processing of refund claims of input tax credit, verifying the invoice details is quintessential. In a completely electronic environment, the information of the recipients’ invoices would be dependent upon the suppliers’ information, thus putting an in-built check-and-balance in the system. However, as the refund claims are being filed by the recipient in a semi-electronic environment and is completely based on the information provided by them, it is necessary that invoices are scrutinized.

14.2 A list of documents required for processing the various categories of refund claims on

exports is provided in the Table below. Apart from the documents listed in the Table below,

no other documents should be called for from the taxpayers, unless the same are not available

with the officers electronically:

15. These instructions shall apply to exports made on or after 1st July, 2017. It is also

advised that refunds may not be withheld due to minor procedural lapses or non-substantive

errors or omission.

16. It is requested that suitable trade notices may be issued to publicize the contents of

this circular.

17. Difficulty, if any, in implementation of the above instructions may please be brought

to the notice of the Board. Hindi version would follow.

(Upender Gupta)

Commissioner (GST)

Download Complete Circular in PDF

Pingback: Notification No 37/2020 Central Tax : PMT 9 Rule 87(13) w.e.f 21.04.2020