Circular No 46/2017 Customs

F.No: 473/10/2017-LC

Govt. of India

Ministry of Finance

Dept. of Revenue

Central Board of Excise & Customs

North Block, New Delhi

Dated 24th November 2017

To,

All Principal Chief Commissioners / Chief Commissioners / Principal Commissioners / Commissioners

of Customs

Subject: Applicability of IGST / GST on goods transferred / sold while being deposited in a warehouse. -reg.

References have been received from the trade regarding levy of IGST/GST on sales of goods deposited in a customs bonded warehouse.

2. Ch IX of the Customs Act provides for deposit of goods into a customs bonded warehouse

licensed under section 57 or 58 or 58A without payment of duty and the procedures to be followed with

respect to the warehoused goods. Sub-section (5) of section 59 provides that the importer is at liberty to

transfer the ownership of such goods to another person while the goods remain deposited in the warehouse.

3. It is to be noted that the value of imported goods, for purposes of charging customs duty, is determined as per section 14 of the Customs Act, 1962 at the time of import i.e. at the time of filing of the into-bond Bill of Entry. Any costs incurred after the import of goods, such as, port charges / port demurrage charges or costs for customs clearing or transporting the goods from the port to the customs bonded warehouse or costs of storage at the customs bonded warehouse, cannot be added to the value of the goods, for the purpose of levy of duties of customs at the stage of ex-bonding. Further, clause (b) of sub-section (1) of Section 15 of the Customs Act provides that the rate of duty or tariff valuation for an ex-bond Bill of Entry shall be the date on which it is filed. There is no provision to vary the assessable value of the goods at the ex-bond stage unless they are such goods on which tariff valuation applies.

Therefore, duties of customs (BCD + IGST) shall be paid on the imported goods at the stage of exbonding

on the value determined under section 14 of the Customs Act.

4. However, the transaction of sale / transfer etc. of the warehoused goods between the importer and any other person may be at a price higher than the assessable value of such goods. Such a transaction squarely falls within the definition of “supply” as per section 7 of the Central Goods and Services Tax Act, 2017 (hereinafter referred to as, “CGST Act”) and shall be taxable in terms of section 9 of the CGST Act read with section 20 of the Integrated Goods and Services Tax Act, 2017 (hereinafter referred to as, “IGST Act”). It may be noted that as per sub-section (2) of section 7 of the IGST Act, any supply of imported goods which takes place before they cross the customs frontiers of India, shall be treated as an inter-State supply. Thus, such a transaction of sale/transfer will be subject to IGST under the IGST Act. The value of such supply shall be determined in terms of section 15 of the CGST Act read with section 20 of the IGST Act and the rules made thereunder, without prejudice to the fact that customs

duty (which includes BCD and applicable IGST payable under the Customs Tariff Act) will be levied and

collected at the ex-bond stage.

5. Thus, in respect of goods stored in a customs bonded warehouse, there is a possibility that

certain cases may involve an additional taxable event, if a transfer of ownership of warehoused goods

takes place between the importer and another person, before clearance of the goods, whether for home

consumption or for export.

5.1 In other words, when goods remain deposited in a customs bonded warehouse and are transferred by the importer to another person, the transaction will be subject to payment of IGST at the value determined as per section 20 of the IGST Act read with section 15 of the CGST Act, 2017 and the rules made thereunder and the tax liability shall be reckoned as per section 9 of the CGST Act, 2017

5.2 However, it may be noted that so long as such goods remain deposited in the warehouse the

customs duty to be collected shall remain deferred. Further, it is only when such goods are ex-bonded

under section 68, shall the deferred duty be collected, at the value as had been determined under section

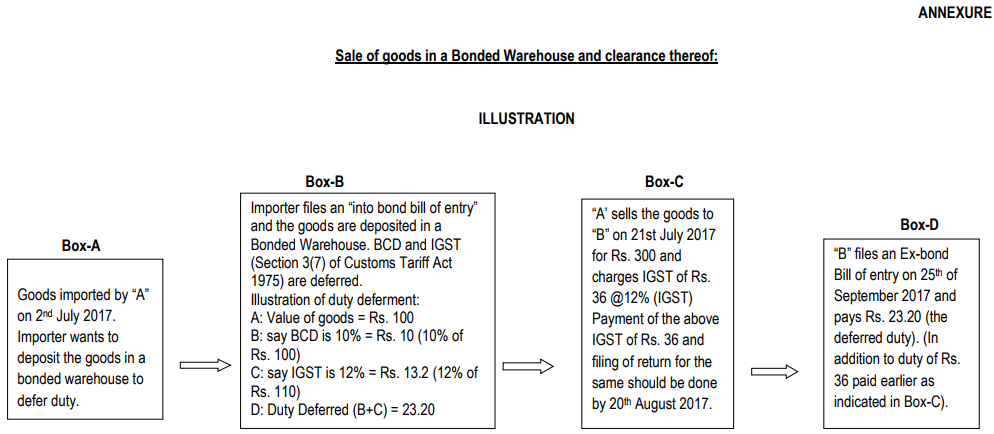

14 of the Customs Act, 1962 in addition to IGST leviable, as indicated at Para 5.1 above. An illustrative

chart on in bond sales and clearance thereof is attached as Annexure.

6. Difficulties in implementation, if any, may be brought to the notice of the Board

7. Hindi version follows.

(Temsunaro Jamir)

Officer On Special Duty (ICD)

Download Circular in PDF

Related Topic on GST

| Topic | Click Link |

| GST Acts | Central GST Act and States GST Acts |

| GST Rules | GST Rules |

| GST Forms | GST Forms |

| GST Rates | GST Rates |

| GST Notifications | GST Act Notifications |

| GST Circulars | GST Circulars |

| GST Judgments | GST Judgments |

| GST Press Release | GST Press Release |

| GST Books | Best Books on GST in India |

| GST Commentary | Topic wise Commentary on GST Act of India |

| GST You Tube Channel | TaxHeal You Tube Channel |

| GST Online Course | Join GST online Course |

| GST History | GST History and Background Material |