ORDER

Smt. Annapurna Gupta, Accountant Member. – The present appeal has been filed by the Department against order passed by the Commissioner of Income Tax (Appeals)-36, New Delhi (hereinafter referred to as CIT(A)) under section 250 (6) of the Income Tax Act 1961(hereinafter referred to as “Act”) pertaining to Assessment Year 2012-13.

2. Grounds No.1 and 2 raised by the Revenue relate to the same issue of loss incurred on account of trading in gold derivatives which was disallowed by the AO treating it as speculative in nature, in terms of its definition u/s 43(5) of the Act, which, however, was allowed by the ld.CIT(A). The said grounds read as under:-

1. “On facts and circumstances of the case and in law, the Ld. CIT(A) has erred in deleting the disallowance of speculative loss for Rs. 27,84,23,191/-ignoring the fact that the assessing had incurred the said loss on account of trading in gold derivative on MCX whereas MCX was recognized under the rule 6DDD w.e.f. 29.11.2013 vide CBDT notification no. 92/2013.

2. On facts and circumstances of the case and in law, the Ld. CIT(A) has erred in fact that the assessee has done trading in gold derivative on MCX which falls under the provision of section 43(5)(a) which was introduced in the act w.e.f. 01.04.2014 and was not applicable to F.Y. 2011-12 relevant to A.Y. 2012-13.”

3. The facts relating to the issue are that the assessee company is engaged in the business of trading in gold, silver, bullion, precious and semi-precious metals. During the impugned year, the assessee had claimed deduction of Rs.27.84 crores on account of arbitrage and hedging. The AO treated the same as speculative loss, rejecting the assessee’s contention that it was primarily a hedging transaction to guard against loss through future price fluctuation in respect of his contracts for actual delivery of goods as per the exclusion to the definition of speculative transaction in proviso (a) to section 43(5) of the Act. The ld.CIT(A), however, found merit in the contention of the assessee and held that the loss incurred was on account of hedging and was excluded, therefore, from the definition of speculative transaction in terms of Section 43(5)(a) of the Act. The entire controversy, therefore, before us rests on the interpretation of section 43(5)(a) and before proceeding further, we are reproducing the relevant section along with the proviso as under:-

43. In sections 28 to 41 and in this section, unless the context otherwise requires—

………………..

(5) “speculative transaction” means a transaction in which a contract for the purchase or sale of any commodity, including stocks and shares, is periodically or ultimately settled otherwise than by the actual delivery or transfer of the commodity or scrips:

Provided that for the purposes of this clause—

(a) a contract in respect of raw materials or merchandise entered into by a person in the course of his manufacturing or merchanting business to guard against loss through future price fluctuations in respect of his contracts for actual delivery of goods manufactured by him or merchandise sold by him; or

(b)…………

……………

shall not be deemed to be a speculative transaction.”

4. As is evident from a bare perusal of section 43(5) of the Act, transactions for purchase or sale of commodities which are settled otherwise than by the actual delivery are treated as speculative transaction. Proviso (a) deals with an exception to this definition stating that where such transactions, settled otherwise than by actual delivery, are in respect of raw materials or merchandise dealt with by a person in the course of his business and are for the purpose of guarding against loss through future price fluctuation in respect of his contract for actual delivery of goods manufactured or sold by him, they shall not be treated as speculative transactions. Briefly put, hedging transactions for raw material or goods sold, entered into for safeguarding against business losses are not treated as speculative transactions as per the proviso (a) to section 43(5) of the Act.

5. In the case before us, the assessee had claimed to have entered into a transaction of trading in derivatives of gold on the Multi-commodity Exchange (MCX), which item the assessee dealt with in the course of its business. The claim of the assessee being that in the business of bullion trading, that it was indulging in, the price of gold experienced a lot of volatility and, therefore, any downward movement of gold price subsequent to purchase of gold would result in significant amount of loss to the assessee and, therefore, to protect itself from negative or downward movement in the price of gold, the company indulged into derivative trading of gold on MCX for hedging purposes, which was excluded from the definition of speculative transaction as per proviso (a) to section 43(5) of the Act.

6. The case of the AO for rejecting assesses claim is that the exception in 43(5)(a) of the Act excludes only hedging transactions entered into with the purpose of safeguarding loss through future price fluctuation in respect of contract of actual sale (emphasis provided by us). That, if the purpose of hedging is to safeguard loss on account of price volatility in contracts of purchases, the said transactions are not covered in the exception provided in clause (a) of the proviso. The AO’s case is that the assessee, admittedly, is doing his hedging transactions both for sale and purchase and since no bifurcation is provided, therefore, he disallowed the entire amount of Rs.27.84 crores of loss in the derivative transactions undertaken by the assessee. The other reason with the AO for denying the assessee the benefit of the exclusion from speculative transaction was that it applies only to manufacturers and the assessee being a trader, the same is not applicable to it.

7. The Ld.CIT(A) found no merit on either basis of the AO for rejecting assesses claim of the derivative transactions being excluded from being treated as speculative in nature.

8. We shall first take up the basis of the AO/Ld.DR for denying the assessee the benefit of the exclusionary clause to section 43(5), i.e., the same applies only to manufacturers and not to traders.

9. A bare perusal of proviso (a) would show that it covers contracts settled otherwise than by actual delivery, both in respect of raw material and merchandise which are entered into by a person in the course of his manufacturing or merchandising business to safeguard against loss through price fluctuation in respect of his contracts for actual delivery of goods manufactured by him or merchandise sold by him.

10. The repeated use of the word ‘merchandise’ along with ” raw material”, “merchandising business” along with “manufacturing business” and “merchandise sold” along with “sale of goods manufactured” by him,clearly reveals the intent of the legislature to include traders also in the exclusionary clause.

11. During the course of hearing before us, the ld. counsel for the assessee pointed out that this aspect of the application of the exclusionary clause to both traders and manufacturers has been settled by the Hon’ble apex court in the case of SK.AR.K.AR. Somasundaram Chettiar & Co. v. CIT, wherein at page 5 the Hon’ble apex court categorically held clause (a) of the proviso to apply to both manufacturers and merchants as under:

“The proviso containing Clauses (a) to (c) is a proviso to Explanation 2 which defines what a speculative transaction is. Clause (a) of the proviso contemplates and applies to a manufacturer as well as a merchant. The assesee herein is not a manufacturer but only a merchant.”

12. Our attention was also drawn to the decision of the Hon’ble Bombay High Court in the case of CIT v. Ramchandra Shivnarain (Bombay). categorically holding traders also to be covered under the exclusionary clause at para 4 of the order is as under:-

“4. Section 43(5) defines speculative transaction. It reads as under:-

“Definitions of certain terms relevant to income from profits and gains of business or profession. (1) to (4)*****

(5) ‘speculative transaction means a transaction in which a contract for the purchase or sale of any commodity, including stocks and shares, is periodically or ultimately settled otherwise than by the actual delivery or transfer of the commodity or scrips;

Provided that for the purposes of this clause-

| (a) | | A contract in respect of raw materials or merchandise entered into by a person in the course of his manufacturing or merchanting beniness to guard against loss through future price fluctuations in respect of his contracts for actual delivery of goods manufactured by him, or merchandise sold by him; or |

| (b) | | a contract in respect of stocks and shares entered into by a dealer or investor therein to guard against loss in his holdings of stocks and shares through price fluctuations; or |

shall not be deemed to be a speculative transaction”

From a bare reading of this clause is clear that though a transaction in which a contract for the purchase or sale of a commodity is settled otherwise that by actual delivery or transfer of the commodity has been defined as speculative transaction, certain species of such transactions entered into under specific circumstances have been taken out of the definition by virtue of the three provisos thereto, the relevant proviso for our purpose being proviso (a). Proviso (a) clearly states that for the purposes of this clause a contract is inspect of raw materials or merchandise entered into by a person in the course of his manufacturing or merchanting business to guard against loss through future price speculations in respect of his contracts for actual delivery of goods manufactured by his or merchandise sold by him shall not be deemed to be a speculative transaction. This proviso is not confined to contracts in respect of raw materials entered into by persons in the course of their manufacturing business as has been sought to be contended by the revenue before the Tribunal and now before us. We do not find any scope for giving such a construction to this proviso. The proviso is clear and unambiguous. It applies equally to cases of persons carrying on manufacturing as well as persons carrying on business of selling goods. There is no scope to confine it to manufacturers. In that view of the matter, we do not find any merit in the submission of the revenue that the benefit of the proviso is available only to manufacturers in respect of purchase of raw materials. It clearly applies also to persons carrying on merchanting business. So far as the facts are concerned, the finding is clear as set out above. The requirements of this proviso are fully met in this case. Both the AAC and the Tribunal have arrived at a concurrent finding of fact. There is no challenge to this finding by raising any specific question in regard to its perversity or otherwise. Under the circumstances the finding of fact is binding. If that be so, proviso (a) to section 43(5) clearly applies to the facts of the present case.”

13. The ld. counsel for the assessee pointed out that the ld. CIT(A), therefore, correctly interpreted the section to hold that proviso (a) covers both manufacturer and trader.

14. The ld. DR before us was unable to support the order of the AO with any decision of either the jurisdictional High Court or the Hon’ble Apex Court holding to the contrary.

15. In the light of the same, we completely agree with the ld.CIT(A) that the finding of the AO that hedging transactions undertaken by the assessee in its capacity as trader of bullion would not be covered by proviso (a) to section 43(5) of the Act is contrary to settled law and based on an incorrect interpretation of the proviso(a) to section 43(5) of the Act.

16. Taking up the next aspect relating to the interpretation of section 43(5) proviso (a) of the Act, based on which the AO held the transactions undertaken by the assessee to be speculative in nature, it has been pointed out to us that the case of the AO was that proviso (a) does not save hedging of purchase transactions from the exclusionary clause to the definition of speculative transaction.

17. Ld. Counsel for the assessee contended that courts as also CBDT have categorically ruled out genuine hedging transactions, both of purchase and sale, from being treated as speculative.

18. Our attention was drawn to the decision of the Full Bench of the Hon’ble Gujarat High Court in the case of Pankaj Oil Mills v. CIT [1978] 115 ITR 824 (Gujarat), pointing out that it categorically held that the scope of exclusion in proviso (a) of section 43(5) would include hedging both of purchase and sale transactions and is not restricted in its scope in any manner. He also drew our attention to the conclusion in the said order as under;

“(1) Hedging contracts, in order to be out of speculative transactions, must be in respect of only raw materials so far as the manufacturer is concerned though these contracts may be both with regard to sales and purchases.

(2) Hedging contracts need not succeed the contracts for sale and actual delivery of goods manufactured, but the latter may be subsequently entered into, provided they are within the reasonable time not exceeding generally the assessment year.

(3) In order to be genuine and valid hedging contracts of sales, the total of such transactions should not exceed the total stocks of the raw materials or the merchandise on hand which would include existing stocks as well as the stocks acquired under the firm contracts of purchases.”

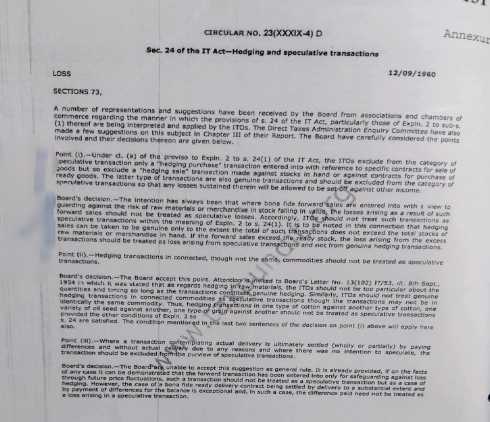

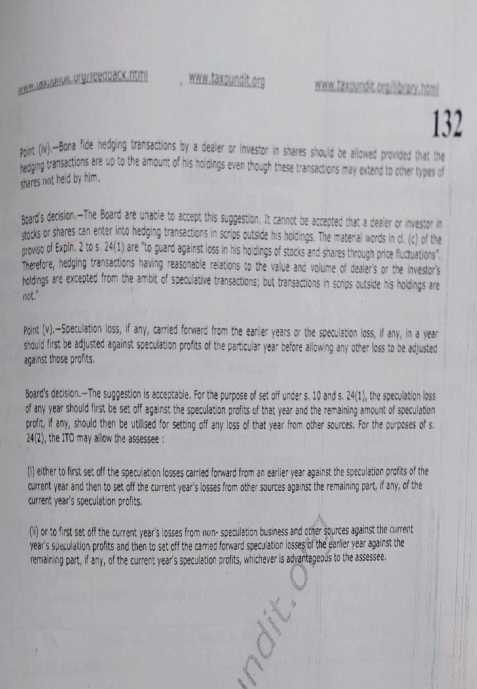

19. Ld. counsel for the assessee thereafter pointed out that the CBDT had clarified that hedging transactions entered into with a view to guard against the risk of raw material or mercantile in stock falling in value should not be treated as speculation. Our attention was drawn to Circular No.23 (XXXIX-4) D dated 12.09.1960 placed at page No.131 of the paper book which is as under:

20. Thereafter ld. counsel for the assessee drew our attention to the facts of the derivative transactions undertaken by the assessee as demonstrated to the authorities below. He pointed out the modus operandi followed by the assessee while entering into derivative transactions, stating that after purchasing gold/bullion and contemplating fluctuation or volatility in its price subsequently the assessee would enter into the sale transaction of derivative to be settled at a future date, to mitigate any losses on the actual sale of bullion. Similarly, the assessee entered into transaction of purchase of derivatives also to mitigate losses against sale contracts entered into by it which was to be executed at future date. In this regard, our attention was drawn to relevant documents corroborating these facts from the paper book filed before us at P.B 133-140 being:

| SI. No. | Particulars | gaper Boole gage No. |

| 1 | Copy of invoice for purchase of 30 kg gold from HHEC dated 18.08.2011 | 134 |

| 2 | Copy of contract note dated 17.08.2011 evidencing sale of 20kgs of gold in the derivative market ofMCX | 135-136 |

| 3 | Copy of contract note dated 18.08.2011:| • | | Evidencing sale of 1 Okgs of gold in the derivative market of MCX |

| • | | Evidencing purchase of 30 kgs of gold in the derivative market of the MCX |

| 137-138 |

| 4 | Copy of invoice for sale of 30 kg gold to Parker Bullion Pvt Ltd. dated 18.08.2011 | 140 |

21. He contended that the total of derivative transactions undertaken by the assessee never exceeded its purchase or sale. It was pointed out that such facts were brought to the notice of the CIT(A) also which stands reproduced at page 6 & 7 of his order as under:

“(vi). To demonstrate that it falls within the parameters set by judicial decisions, the assessee gave various examples of its contracts, interalia as under:

On 17.08.2011, the appellant purchased an additional 30 kg of gold from The Handicrafts & Handlooms Exports Corporation of India (HHEC). To hedge the sale price of gold purchased by it, it simultaneously sold (a) 20 kgs of gold in the form of derivatives on the MCX on the same date viz. 17.08.2011 and (b) 10 kgs of gold in the form of derivatives on the MCX on 18.08.2011, copy of the contract note no. M/D/0817/469638 dated 17.08.2011 and M/D/0818/475194 dated 17.08.2011 and 18.08.2011 issued by its broker RCL evidencing the aforesaid was enclosed.

Thus, on 17.08.2011, the appellant had a stock of 30 kg in physical gold and had correspondingly sold 30 kg of gold in the derivative markets of the MCX to hedge the sale price of the stock of gold held by it.

On 18.08.2011, the appellant sold 30kg of gold vide invoice no. AMD/5/1112 dated 18.08.2011 to Parker Bullion Pvt. Ltd. and simultaneously squared up the forward sale position taken by it in respect of the aforesaid gold by purchasing 30 kgs of gold in the form of derivatives in the derivative market of the MCX on the same date viz. 18.08.2011. Other such examples on various dates were also provided.”

22. Ld.Counsel for the assessee contended that clearly the assessee had demonstrated the derivative transactions to be genuine hedging transactions, based on equal value of underlying assets and not exceeding it, and considering the judicial decisions as also the CBDT Circular, the impugned transactions were rightly treated as non-speculative by the Ld.CIT(A). Our attention was drawn to para 6 (iii) – (vi) of the Ld.CIT(A)’s order as under:

“(iii). Another argument of the AD is that the exception clause is available only for loss on forward sale and not against the loss on forward purchase and that the assessee in this case is doing hedging transaction both for sale and purchase. By mentioning the above sentence in the order, it is apparent that the AO has himself considered the transaction as hedging, thus making earlier discussion of treating the transaction as speculative, irrelevant.

Coming to the issue of whether loss on forward purchase will be allowable to the assessee or not, the assessee has made submission based on judicial decisions and the circular of the CBDT. In the case of the assessee, both purchases and sales of large quantity in gold and silver are made. It was also demonstrated that the price of gold was fluctuating to a great extent in the relevant AY. Therefore, it is a part of the business to enter into hedging transaction to protect itself from the fluctuation in the price. However, in no instance the assessee has sold more gold than it has purchased. This was also demonstrated by various example of sale and purchase made at different times. It therefore appears that the assessee is not carrying any speculative business. However, if at any date the sale is more than the available stock, that amount is to be taken as speculative.

(iv). From the various judicial decisions, it is clear that although the word “purchase’ is not included in the clause (a) of section 43(5), where only the word merchandised sold by him is mentioned, such transaction would cover both. Various Courts have relied on the CBDT Circular No. 230 of 12.09.1960 which clarifies that the proviso to section 43(5) is not restricted only to forward purchase contracts but also to bona fide forward sale contract. No other circular/notification/instruction or any other case law has been brought on record by the AD to rebut the Board’s decision in the above mentioned circular. The circular also mentions that only if the forward sale exceeds the stock, the excess transaction should be treated as speculative losses and not genuine hedging transaction. The assessee had already demonstrated that the forward sale has not exceeded the forward purchases. This fact may reverified by the AO.

(v). Other conditions to allow such transaction have been enumerated in para 5.1 (v)(a) above. It is seen that in the assessee’s case there is no breach of any of the conditions mentioned i.e. hedging transaction can be both for purchase and sale, the sale have not exceeded the purchase/stock, actual delivery has been made.

(vi). In view of the above detailed discussion, in my opinion, the transaction of the assessee are covered by the exclusion as per proviso (a) of section 43(5) and it applies to the case of the assessee and the transaction is held to be not speculative in nature. It is also relevant to note here that despite the order of AY 2012-13, the AO has not made the disallowance in AY 2013-14 and accepted the Return of Income of the assessee.”

23. Having heard both the parties, we find no infirmity in the order of the Ld.CIT(A). The judicial decisions cited by the Ld.Counsel for the assessee read alongwith the CBDT Circular No.23D of 12-09-1960, clearly bring out the position of law that hedging of purchases is also included in the exception carved to speculative transactions in proviso (a) to section 43(5) of the Act. The Revenue does not dispute the fact that the derivative transactions entered into by the assessee were genuine hedging transactions. Ld.CIT(A) has recorded the fact of the hedging transactions undertaken by the assessee not exceeding its total stock of raw material or merchandise, which has remained uncontroverted before us. The interpretation by the AO of the proviso (a) to section 43(5) of the Act as not excluding hedging of purchase transactions from being treated as speculative, we agree with the ld.CIT(A), is incorrect.

24. We do not, therefore, find any infirmity in the order of the ld.CIT(A) deleting the disallowance of losses incurred by the assessee in derivative transaction amounting to Rs.27.84 crores.

25. We have also noted that the grounds raised by the Revenue before us raise a completely different issue. As per the grounds raised, the case of the Revenue is that trading in derivatives of commodities in the MCX platform has been excluded from the definition of speculative transaction only w.e.f. 01.01.2014 and the impugned assessment year before us being 2012-13, the assessee, therefore, was not entitled to any benefit of the exclusionary clause.

26. There is no merit in this argument of the Revenue. The assessee in any case has sought exclusion under proviso (a) to section 43(5) of the Act and has been held to be entitled so by the ld.CIT(A) whose order has been confirmed by us also. The assessee has held its transactions to be in the nature of hedging transactions to safeguard against any loss from the sale of its goods in terms of proviso (a) to section 43(5). The clause (e) to which the Revenue has drawn our attention to stating that the assessee is entitled to be excluded by virtue of this proviso alone having traded on the MCX platform applies only to traders dealing in derivatives on the MCX platform. While proviso (a) excludes hedging transactions from the purview of speculative transaction, proviso (e) deals with a completely different set of and nature of transactions. Proviso (e) excludes all derivative transactions carried out on the MCX platform of trading of commodities transaction tax by all traders to be not speculative in nature. Therefore, the scope of both the provisos are completely different. In the present case, it is not the claim of the assessee that it was dealing on the MCX platform as a trader. On the contrary, the claim of the assessee is that it was dealing in derivatives on the MCX platform for hedging its sale contracts. Therefore, the assessee had rightly claimed benefit of exclusion from the definition of speculative transaction under proviso (a), proviso (e) not being not applicable to it at all. The grounds raised by the Revenue, therefore, are of no consequences.

27. In view of the above, grounds No.1 and 2 raised by the Revenue are dismissed.

28. Ground No.3 raised by the Revenue reads as under:-

“3. That on facts and circumstances of the case and in law, the Ld. CIT(A) has erred in deleting the addition of Rs. 1,30,452/- paid on account of fines and penalties as this is not an allowable expense u/s 37(1) of the I.T. Act, 1961.”

29. The Revenue in the above ground is aggrieved by the order of the ld.CIT(A) in deleting the disallowance of Rs.1,30,452/- made by the AO treating it as fines and penalties. The findings of the ld.CIT(A) in this regard are contained in para 6.2 as under:-

“6.2 The second issue is regarding the charges of Rs. 1,30,452/- disallowed by the AO, By the order, it is clear that the AO while making the said disallowance has neither analysed the nature of the expense (whether compensatory or penal) nor did he seek any information or documents about the said expense. The assessee has submitted that charges of Rs. 1,30,452/- were paid by it to DLB for storage in its vault, the gold purchased form it. The said payment was made on account of delay in taking delivery of the said gold beyond the agreed period viz. The period for which charges had been paid by the supplier due to additional time taken by the appellant in identifying buyers. Thus said payment is in the nature of a compensation paid by the appellant to DLB on account of non-fulfilment of a specific clause in the purchase agreement the said payment of Rs. 1,30,452/-. It is therefore clear that this payment is apparently incidental to the appellant’s main business operation of Trading in gold, silver etc. It does not tantamount to breach or infraction of any law or statute in force. The AO is therefore directed to allow the charges for late payment.”

30. On going through the same we find that the ld.CIT(A) has recorded a categorical finding of fact that the impugned amount was paid by the assessee to DLB for storage in its vault the gold purchased from it and the said payment was made on account of delay in taking delivery of the said gold beyond the agreed period. It was the charges paid due to additional time taken by the assessee in identifying buyers. The ld.CIT(A) has noted that the AO while making the disallowance had neither analysed the nature of expense nor did he seek any information or document about the said expense. The ld. DR was unable to controvert the above factual finding of the ld.CIT(A). In the light of the same, we see no reason to interfere in the order of the ld.CIT(A). The ld.CIT(A), after recording the facts relating to the impugned expenditure and deriving therefrom that they were in the nature of compensation paid by the assessee, which finding both on facts and interpretation, the ld. DR has been unable to dislodge before us, has allowed the assessee’s claim of expenditure. The ground of appeal No.3 raised by the Revenue is, therefore, dismissed.

31. In effect, the appeal of the Revenue is dismissed.